Page 1

1.

In perfect competition:

A)

a firm’s total revenue is found by multiplying the market price by the firm’s

quantity of output.

B)

the firm’s total revenue curve is a downward-sloping line.

C)

at any price, the more sold, the higher is a firm’s marginal revenue.

D)

the firm’s total revenue curve is nonlinear.

2.

A firm’s total output times the price at which it sells that output is _____ revenue.

A)

net

B)

total

C)

average

D)

marginal

3.

Total revenue is a firm’s:

A)

change in revenue resulting from a unit change in output.

B)

ratio of revenue to quantity.

C)

difference between revenue and cost.

D)

total output times the price of that output.

4.

If a perfectly competitive firm increases production from 10 units to 11 units and the

market price is $20 per unit, total revenue for 11 units is:

A)

$10.

B)

$20.

C)

$200.

D)

$220.

5.

If a perfectly competitive firm decreases production from 11 units to 10 units and the

market price is $20 per unit, total revenue for 10 units is:

A)

-$20.

B)

$20.

C)

$200.

D)

$210.

6.

The difference between total revenue and total cost is:

A)

economic profit or loss.

B)

nominal revenue.

C)

average revenue.

D)

marginal revenue.

Page 2

7.

In a perfectly competitive industry, the market demand curve is usually:

A)

perfectly inelastic.

B)

perfectly elastic.

C)

downward-sloping.

D)

relatively elastic.

8.

The demand curve faced by a single perfectly competitive firm is:

A)

perfectly inelastic.

B)

perfectly elastic.

C)

downward sloping.

D)

relatively but not perfectly elastic.

9.

Marginal revenue:

A)

is the slope of the average revenue curve.

B)

equals the market price in perfect competition.

C)

is the change in quantity divided by the change in total revenue.

D)

is the price divided by the change in quantity.

10.

The marginal revenue received by a firm in a perfectly competitive market:

A)

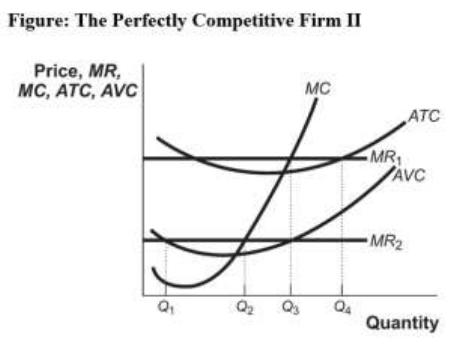

is greater than the market price.

B)

is less than the market price.

C)

is equal to its average revenue.

D)

increases with the quantity of output sold.

11.

If a perfectly competitive gardening shop sells 30 evergreen bushes at $10 per bush, its

marginal revenue is:

A)

$10.

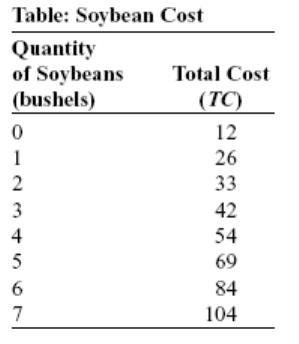

B)

more than $10.

C)

less than $10.

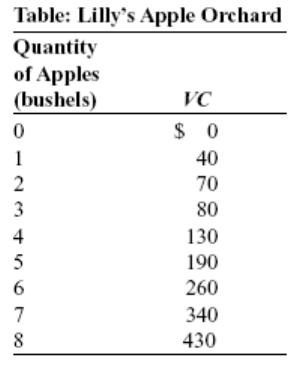

D)

$300.

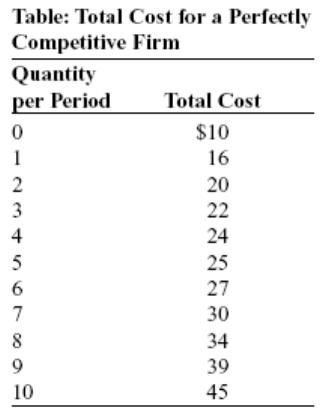

12.

Marginal revenue is a firm’s:

A)

ratio of profit to quantity.

B)

ratio of average revenue to quantity.

C)

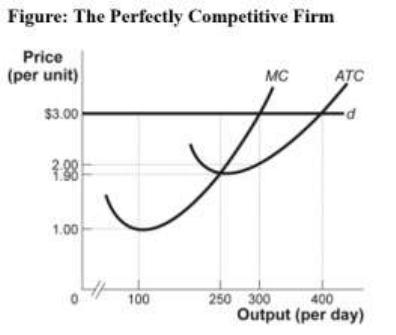

price per unit times the number of units sold.

D)

increase in total revenue when it sells an additional unit of output.

Page 3

13.

Perfectly competitive firms will:

A)

maximize total revenue by using the marginal decision rule.

B)

increase output up to the point that the marginal revenue of an additional unit of

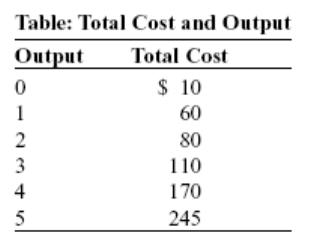

output is greater than the marginal cost.

C)

increase output up to the point that the marginal revenue of an additional unit of

output is equal to the marginal cost.

D)

always attempt to minimize average variable cost.

14.

For a perfectly competitive firm, marginal revenue:

A)

is less than price.

B)

is greater than price.

C)

decreases as the firm increases output.

D)

is equal to price.

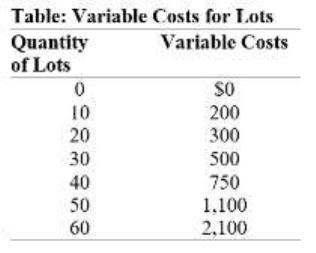

15.

A perfectly competitive firm will maximize profits when the:

A)

marginal revenue equals marginal cost.

B)

marginal revenue is lower than average variable cost.

C)

price is lower than marginal cost.

D)

price is higher than marginal cost.

16.

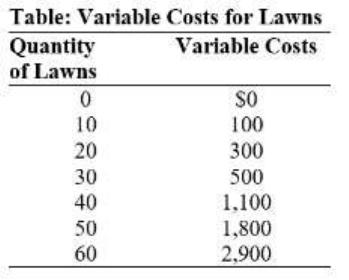

The equilibrium price of a guidebook is $35 in the perfectly competitive guidebook

industry. Our firm produces 10,000 guidebooks for an average total cost of $38,

marginal cost of $30, and average variable cost of $30. Our firm, in the short run,

should:

A)

raise the price of guidebooks because the firm is losing money.

B)

keep output the same because the firm is producing at minimum average variable

cost.

C)

produce more guidebooks because the next guidebook produced will increase profit

by $5.

D)

shut down because the firm is losing money.

17.

Zoe’s Bakery operates in a perfectly competitive industry and has standard cost curves.

The variable costs at Zoe’s Bakery increase, so all of the cost curves (except fixed cost)

shift upward. The demand for Zoe’s pastries does not change, nor does the firm shut

down. To maximize profits after the variable cost increase, Zoe’s Bakery will _____ its

price and _____ its level of production.

A)

raise; increase

B)

decrease; increase

C)

raise; decrease

D)

do nothing to; decrease

Page 4

18.

The slope of the total revenue curve is:

A)

marginal cost.

B)

net revenue.

C)

equal to marginal revenue and is constant under perfect competition.

D)

equal to marginal revenue and varies under perfect competition.

19.

The slope of the total cost curve is:

A)

marginal cost.

B)

marginal revenue.

C)

constant under perfect competition.

D)

always negative.

20.

For a firm producing at any level of output lower than the most profitable one, an

increase in output adds:

A)

more to total cost than to total revenue.

B)

more to total revenue than to total cost.

C)

the same amount to total revenue as to total cost.

D)

to total revenue but not to total cost.

21.

For a firm producing at any level of output greater than the most profitable one, a

reduction in output decreases total revenue _____ total cost.

A)

by less than it decreases

B)

by more than it decreases

C)

by the same amount as it decreases

D)

but not

22.

A perfectly competitive firm maximizes profit in the short run by producing the quantity

at which:

A)

TR = TC.

B)

MR = MC.

C)

Q * (P – ATC) = 0.

D)

P < AVC.

23.

The price received by a firm in a perfectly competitive market:

A)

is equal to the market price.

B)

is less than the market price.

C)

is greater than the market price.

D)

decreases with the quantity of output sold by the firm.

Page 5

24.

The marginal revenue received by a firm in a perfectly competitive market:

A)

is unrelated to the market price.

B)

is less than the market price.

C)

is greater than the market price.

D)

is the change in total revenue divided by the change in output.

25.

For a firm in a perfectly competitive market, _____ revenue equals _____.

A)

marginal; total revenue

B)

marginal; market price

C)

net; price

D)

net; marginal revenue

26.

If a perfectly competitive firm sells 10 units of output at $30 per unit, its marginal

revenue is:

A)

$10.

B)

$30.

C)

more than $30.

D)

$300.

27.

Price in a perfectly competitive industry:

A)

is determined by each firm, depending on its costs of production.

B)

is always equal to marginal revenue for the firm.

C)

must be greater than average total cost or the firm will shut down in the short run.

D)

is indeterminate in the short run.

28.

Marginal revenue is a firm’s:

A)

ratio of the change in total revenue to the change in output.

B)

ratio of average revenue to total revenue.

C)

profit per unit times the number of units sold.

D)

increase in profit when it sells an additional unit of output.

29.

If a firm in perfect competition sells 10 units of output at $5 per unit, its marginal

revenue is:

A)

$5.

B)

more than $5 but less than $50.

C)

$50.

D)

$250.

Page 6

30.

If a perfectly competitive firm sells 300 units of output at $1 per unit, its marginal

revenue is:

A)

less than $1.

B)

$1.

C)

more than $1 but less than $300.

D)

$300.

31.

In perfect competition:

A)

price and average variable cost are the same.

B)

price and marginal revenue are the same.

C)

price and total revenue are the same.

D)

total revenue and total variable cost are the same.

32.

The profit-maximizing level of output for a perfectly competitive firm in the short run

occurs where _____ equals _____.

A)

marginal cost; price

B)

marginal revenue; price

C)

total revenue; total cost

D)

average revenue; average total cost

33.

If a perfectly competitive firm is producing a quantity where MC > MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

34.

If a perfectly competitive firm is producing a quantity where MC < MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

35.

If a perfectly competitive firm is producing a quantity where MC = MR, then profit:

A)

is maximized.

B)

can be increased by increasing production.

C)

can be increased by decreasing production.

D)

can be increased by decreasing the price.

Page 7

36.

If a perfectly competitive firm is producing a quantity where P < MC, then profit:

A)

is maximized.

B)

can be increased by decreasing the price.

C)

can be increased by increasing production.

D)

can be increased by decreasing production.

37.

If a perfectly competitive firm is producing a quantity where P > MC, then the firm can

increase profit by:

A)

making no change in output or price because it is already maximizing profit.

B)

increasing the price.

C)

decreasing the price.

D)

increasing production.

38.

If a perfectly competitive firm is producing a quantity where P = MC, then profit:

A)

is maximized.

B)

can be increased by decreasing the quantity.

C)

can be increased by decreasing the price.

D)

can be increased by increasing production.

Use the following to answer question 39:

Page 8

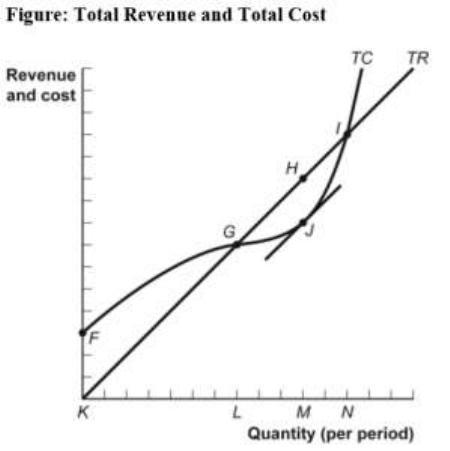

39.

(Ref 24-1 Figure: Total Revenue and Total Cost) Use Figure 24-1: Total Revenue and

Total Cost. The MOST profitable level of output occurs at quantity:

A)

F.

B)

K.

C)

L.

D)

M.

40.

If the price is greater than average total cost at the profit-maximizing quantity of output

in the short run, a perfectly competitive firm will:

A)

produce at a loss.

B)

produce at a profit.

C)

shut down production.

D)

produce more than the profit-maximizing quantity.

41.

In the short run, a perfectly competitive firm produces output and earns an economic

profit if:

A)

P > ATC.

B)

P = ATC.

C)

P < MC.

D)

P < ATC.

42.

In the short run, a perfectly competitive firm produces output and earns zero economic

profit if:

A)

P < ATC.

B)

P = ATC.

C)

P < MC.

D)

P > ATC.

43.

Which statement is true?

A)

Profit per unit is price minus MC.

B)

Total economic profit is per-unit profit times quantity.

C)

If price is less than ATC, the firm will break even in the short run.

D)

If price is less than marginal cost, the perfectly competitive firm should raise the

price and increase output.

Page 9

44.

A perfectly competitive firm will earn a profit in the short run when it produces the

profit-maximizing quantity of output and the price is:

A)

greater than marginal cost.

B)

less than marginal cost.

C)

less than average variable cost.

D)

greater than average total cost.

45.

If the price is greater than average total cost at the profit-maximizing quantity of output

in the short run, a perfectly competitive firm will:

A)

continue to produce at a loss.

B)

produce at a profit.

C)

shut down production.

D)

reduce its fixed costs.

46.

For a perfectly competitive firm in the short run, if the firm produces the quantity at

which _____, the firm _____.

A)

P > ATC; is profitable

B)

P < ATC; breaks even

C)

P = ATC; incurs a loss

D)

P < ATC; is profitable

47.

In the short run, a perfectly competitive firm produces output and breaks even if the firm

produces the quantity at which:

A)

P < ATC.

B)

P = ATC.

C)

P > ATC.

D)

P = (TR/Q + TC/Q) * Q.

48.

In the short run, if P = ATC, a perfectly competitive firm:

A)

produces output and earns zero economic profit.

B)

produces output and earns an economic profit.

C)

produces output and incurs an economic loss.

D)

does not produce output and incurs an economic loss.

49.

In the short run, if P > ATC, a perfectly competitive firm:

A)

produces output and earns zero economic profit.

B)

produces output and earns an economic profit.

C)

produces output and incurs an economic loss.

D)

does not produce output and earns economic profit.

Page 10

50.

In perfectly competitive markets, if the price is _____, the firm will _____.

A)

greater than ATC; make an economic profit

B)

greater than the minimum ATC; break even

C)

less than ATC; make an economic profit

D)

less than ATC; break even

51.

A perfectly competitive firm will earn a profit and will continue producing the

profit-maximizing quantity of output in the short run if the price is:

A)

less than the average fixed cost.

B)

less than marginal cost.

C)

greater than average variable cost but less than average total cost.

D)

greater than average total cost.

52.

Consider a perfectly competitive firm in the short run. Assume that the firm produces

the profit-maximizing output and earns economic profits. Which statement is definitely

false?

A)

Price is equal to marginal cost.

B)

Price is equal to marginal revenue.

C)

Price is equal to average total cost.

D)

Marginal cost is greater than average total cost.

53.

Suppose a perfectly competitive firm can increase its profits by increasing its output.

Then it must be true that the firm’s _____ exceeds its _____.

A)

marginal revenue; marginal cost

B)

price; average total cost but is less than marginal cost

C)

marginal cost; marginal revenue

D)

price; marginal revenue

54.

A competitive firm operating in the short run is producing at the output level at which

ATC is at a minimum. If ATC = $8 and MR = $9, to maximize profits (or minimize

losses), this firm should:

A)

increase output.

B)

reduce output.

C)

increase price.

D)

do nothing; because it is already maximizing profits.

Page 11

55.

Zoe’s Bakery operates in a perfectly competitive industry. When the market price of iced

cupcakes is $5, the profit-maximizing output level is 150 cupcakes. Her average total

cost is $4, and her average variable cost is $3. Zoe’s marginal cost is _____, and her

short-run profits are _____.

A)

$5; $150

B)

$5; $300

C)

$1; $150

D)

$1; $300

56.

A perfectly competitive firm is definitely earning an economic profit when:

A)

MR > MC.

B)

P > ATC.

C)

P > MC.

D)

P < ATC.

57.

Mikail’s perfectly competitive camera memory card-producing factory is making

positive economic profits. If the price of memory cards is $9, Mikail’s output is 3,000

cards a month, and his monthly average total cost is $7, what are his monthly profits?

A)

$6,000

B)

$27,000

C)

$21,000

D)

$2

58.

Suppose Sarah’s pottery studio is charging the market price, which is slightly higher

than her average total cost. This means that Sarah:

A)

is breaking even.

B)

should shut down immediately.

C)

is earning a small economic profit.

D)

is incurring a small economic loss.

59.

The break-even price for a perfectly competitive firm is equal to the:

A)

minimum value of average variable cost.

B)

marginal revenue, provided that marginal revenue is equal to marginal cost.

C)

average fixed cost at the given output level.

D)

minimum value of average total cost.

Page 12

60.

Which statement is true?

A)

If the price falls below the average total cost, the firm will earn economic profits.

B)

Price and marginal revenue are the same in perfect competition.

C)

Economic profit per unit is found by subtracting AVC from the price.

D)

Economic profit is always positive in the short run.

61.

Wenqin is a farmer, and in the short run she produces 100 bushels of wheat. Her average

total cost per bushel is $1.75, total revenue is $450, and total fixed costs are $100.

Wenqin’s:

A)

average fixed cost is $1.50.

B)

economic profit per bushel is $2.75.

C)

average variable cost is $1.25.

D)

economic profit is $250.

Use the following to answer questions 62-63:

62.

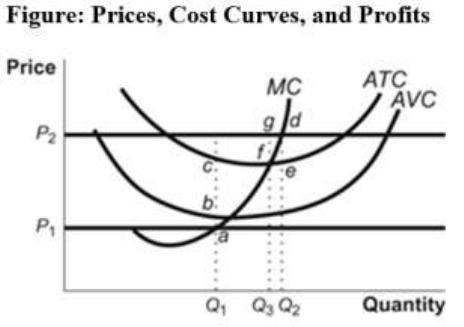

(Ref 24-2 Figure: Prices, Cost Curves, and Profits) Use Figure 24-2: Prices, Cost

Curves, and Profits. If the price is P1 and the firm decides to produce at output Q1, then

the firm earns:

A)

a loss equal to (ba) * Q1.

B)

a loss equal to (ca) * Q1.

C)

a loss equal to (bc) * Q1.

D)

zero.

Page 13

63.

(Ref 24-2 Figure: Prices, Cost Curves, and Profits) Use Figure 24-2: Prices, Cost

Curves, and Profits. If the price is P2 and the firm is profit-maximizing, then the firm’s

profit is:

A)

(fg) * Q3.

B)

(de) * Q2.

C)

(fg) * Q2.

D)

(de) * P2.

Use the following to answer questions 64-66:

64.

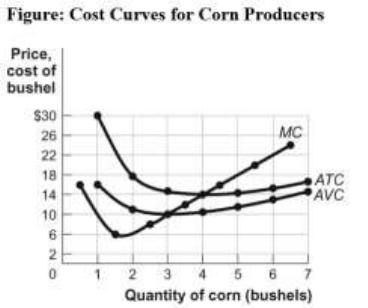

(Ref 24-3 Figure: Cost Curves for Corn Producers) Use Figure 24-3: Cost Curves for

Corn Producers. The market for corn is perfectly competitive. If the price of a bushel of

corn is $14, in the short run, the farmer will produce _____ of corn and earn an

economic _____ equal to _____.

A)

4 bushels; profit; $0

B)

4 bushels; profit; just less than $80 per bushel

C)

2 bushels; profit; $0

D)

2 bushels; loss; just more than $80 per bushel

65.

(Ref 24-3 Figure: Cost Curves for Corn Producers) Use Figure 24-3: Cost Curves for

Corn Producers. The market for corn is perfectly competitive. If the price of a bushel of

corn is $4, in the short run the farmer will produce _____ bushels of corn and earn an

economic _____ equal to _____.

A)

0; loss; average fixed costs

B)

0; loss; total fixed costs

C)

3; loss; $30 per bushel

D)

3; profit; $20 per bushel

Page 14

66.

(Ref 24-3 Figure: Cost Curves for Corn Producers) Use Figure 24-3: Cost Curves for

Corn Producers. The market for corn is perfectly competitive. If the price of a bushel of

corn is $10, then in the short run the farmer will produce _____ bushels of corn and take

an economic loss equal to _____.

A)

0; average fixed costs

B)

0; total variable costs

C)

3; total fixed costs

D)

3; $22 per bushel

Use the following to answer questions 67-69:

67.

(Ref 24-4 Figure: Costs and Profits for Tomato Producers) Use Figure 24-4: Costs and

Profits for Tomato Producers. The market for tomatoes is perfectly competitive. The

market price of a bushel of tomatoes is $18. If the market price increases to $20, the

farmer’s marginal revenue _____ and the profit-maximizing output _____.

A)

increases; increases

B)

increases; decreases

C)

decreases; increases

D)

decreases; decreases

68.

(Ref 24-4 Figure: Costs and Profits for Tomato Producers) Use Figure 24-4: Costs and

Profits for Tomato Producers. The market for tomatoes is perfectly competitive. The

market price of a bushel of tomatoes is $18. If the market price falls to $16, the farmer’s

marginal revenue _____ and the profit-maximizing output _____.

A)

increases; decreases

B)

increases; increases

C)

decreases; increases

D)

decreases; decreases

Page 15

69.

(Ref 24-4 Figure: Total Cost for Tomato Producers) Use Figure 24-4: Total Cost for

Tomato Producers. The market for tomatoes is perfectly competitive. The market price

of a bushel of tomatoes is $14. The farmer’s total cost at the profit-maximizing number

of bushels is:

A)

$3.50.

B)

$14.00.

C)

$56.00.

D)

$72.00.

Use the following to answer question 70:

70.

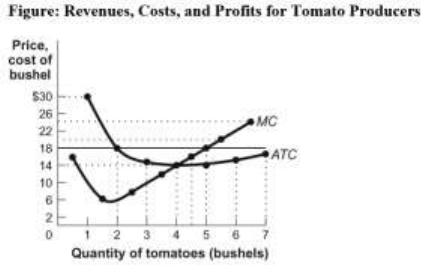

(Ref 24-5 Figure: Revenues, Costs, and Profits for Tomato Producers) Use Figure 24-5:

Revenues, Costs, and Profits for Tomato Producers. The market for tomatoes is

perfectly competitive. The market price of a bushel of tomatoes is $18. At the

profit-maximizing quantity of output in the figure, the farmer’s total revenue is _____,

total cost is _____, and economic profit is _____.

A)

$90; $14; $76

B)

$90; $70; $20

C)

$30; $42; -$12

D)

$48; $56; –$8

Page 16

Use the following to answer question 71:

71.

(Ref 24-6 Figure: Revenues, Costs, and Profits for Tomato Producers II) Use Figure

24-6: Revenues, Costs, and Profits for Tomato Producers II. The market for tomatoes is

perfectly competitive. The market price of a bushel of tomatoes is $10. At the farmer’s

profit-maximizing output, total revenue is _____, total cost is _____, and economic

profit is _____.

A)

$90; $72; $18

B)

$56; $56; $0

C)

$30; $48; -$18

D)

$48; $56; –$8

Use the following to answer questions 72-77:

Page 17

72.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If market price of a bushel of tomatoes is $18, in the short run the

farmer’s profit-maximizing output is _____ bushels.

A)

2

B)

3

C)

4

D)

5

73.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $14, in the short run

the farmer’s profit-maximizing output is _____ bushels.

A)

2

B)

3

C)

4

D)

5

74.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $8, in the short run

the farmer’s profit-maximizing output is _____ bushels.

A)

0

B)

1

C)

2.5

D)

3

75.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $18, this farm will:

A)

minimize its losses by shutting down.

B)

minimize its losses by continuing to produce.

C)

break even.

D)

earn an economic profit.

Page 18

76.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. If the market price of a bushel of tomatoes is $12, in the short run

this farm will:

A)

minimize its losses by shutting down.

B)

minimize its losses by continuing to produce.

C)

break even.

D)

earn an economic profit.

77.

(Ref 24-7 Figure: Revenues, Costs, and Profits for Tomato Producers III) Use Figure

24-7: Revenues, Costs, and Profits for Tomato Producers III. The market for tomatoes is

perfectly competitive. The farm’s short-run supply curve is the _____ cost curve above a

price of _____.

A)

average total; $14

B)

average variable; $10

C)

marginal; $10

D)

marginal; $14

Use the following to answer questions 78-83:

78.

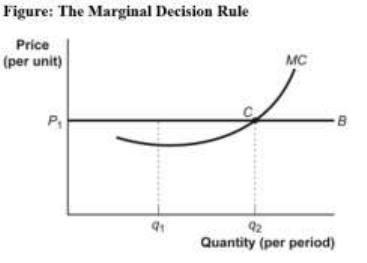

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. At q2, or the _____, the _____ price is equal to marginal cost.

A)

minimum-cost output; shut-down

B)

profit-maximizing quantity; market

C)

maximum-cost output; break-even

D)

profit-minimizing quantity; break-even

Page 19

79.

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. If P1 is the market price and if this firm is maximizing profit, it should produce:

A)

a quantity at which MR < MC.

B)

at quantity q2.

C)

at quantity q1, where MR > MC.

D)

a quantity greater than q1 but less than q2.

80.

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. Given the market price P1, B is the _____ curve.

A)

marginal revenue

B)

marginal cost

C)

marginal product

D)

average fixed cost

81.

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. Economic profit:

A)

is earned only for quantities between q1 and q2.

B)

is earned only for quantities between the origin and q1.

C)

is maximized at q1.

D)

cannot be determined from the information provided.

82.

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. As long as the price is above the minimum variable cost, this firm should produce

quantity _____, where _____ equals _____ and economic profit is maximized.

A)

q1; MR; MC

B)

q2; price; MC

C)

q2; MR; TR

D)

q1; TR; TC

83.

(Ref. 24-8 Figure: Marginal Decision Rule) Use Figure 24-8: The Marginal Decision

Rule. To the left of point C (e.g., at q1):

A)

economic profit is the vertical distance between curves B and MC.

B)

the firm is not maximizing profits.

C)

the firm is maximizing profits but not total revenue.

D)

the firm should produce less.

Page 20

Use the following to answer questions 84-97:

84.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. M is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

85.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. N is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

86.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. If the market price is P3, the firm will

produce quantity _____ and _____ in the short run.

A)

q2; make a profit

B)

q1; break even

C)

q2; incur a loss

D)

q4; incur a loss

Page 21

87.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. If the market price is P4, the firm will

produce quantity _____ and _____ in the short run.

A)

q1; break even

B)

q3; make a profit

C)

q4; break even

D)

q5; lose fixed costs

88.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure: The

Profit-Maximizing Firm. O is the _____ curve.

A)

ATC

B)

MR

C)

MC

D)

AVC

89.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. Curve M must cross curves N and O:

A)

at their maximum points.

B)

to the left of their minimum points.

C)

at their minimum points.

D)

to the right of their minimum points.

90.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. If the market price is less than P2, the firm

will _____ in the short run.

A)

produce q1 and break even

B)

produce q1 and incur a loss smaller than total fixed cost

C)

shut down

D)

produce q3 and make a profit

91.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. Which statement is TRUE?

A)

AFC is represented by the vertical distance between curve M and curve N at any

level of output.

B)

AFC is represented by the vertical distance between curve N and curve O at any

level of output.

C)

This figure illustrates the long run because all costs are variable.

D)

Quantity q2 is to the left of the shut-down point.

Page 22

92.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. The MC curve is represented by:

A)

none of the curves.

B)

curve O.

C)

curve M.

D)

curve N.

93.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. The ATC curve is represented by:

A)

curve N.

B)

curve M.

C)

curve O.

D)

none of the curves.

94.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. Which curve is the AVC curve?

A)

curve M

B)

none of the curves

C)

curve N

D)

curve O

95.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. If the market price is P4, marginal revenue:

A)

and price are the same.

B)

is less than P4.

C)

is greater than P4.

D)

and price are unrelated.

96.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. If the market price is P4:

A)

firms will leave the industry and the price will fall in the long run.

B)

there will be economic profits and firms will enter the industry in the long run.

C)

the market supply curve will shift to the left and price will fall in the long run.

D)

the firm will produce q4.

Page 23

97.

(Ref 24-9 Figure: The Profit-Maximizing Firm in the Short Run) Use Figure 24-9: The

Profit-Maximizing Firm in the Short Run. At q2, ATC is the vertical distance between q2

on the horizontal axis and:

A)

curve M.

B)

curve N.

C)

curve O.

D)

P4.

Use the following to answer questions 98-109:

98.

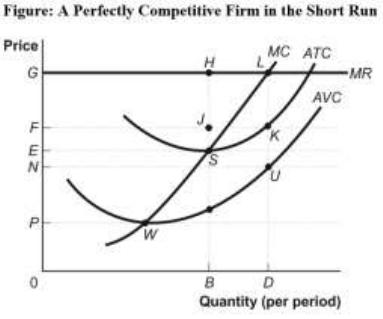

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10:

A Perfectly Competitive Firm in the Short Run. The firm’s total cost of producing its

most profitable level of output is:

A)

BS.

B)

DK.

C)

0FKD.

D)

0GLD.

99.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm’s total cost of producing its most

profitable level of output is:

A)

BS.

B)

DK.

C)

0FKD.

D)

0GLD.

Page 24

100.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm’s total revenue from the sale of

its most profitable level of output is:

A)

0GLD.

B)

0GHB.

C)

BH.

D)

DL.

101.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm’s total economic profit at its most

profitable level of output is:

A)

0GHB.

B)

EFJS.

C)

EGHS.

D)

FGLK.

102.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The lowest price that will yield

non-negative economic profit is indicated by the letter:

A)

G.

B)

F.

C)

E.

D)

N.

103.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm will produce in the short run if

the price is greater than or equal to:

A)

F.

B)

E.

C)

N.

D)

P.

104.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm will shut down in the short run if

the price falls below:

A)

G.

B)

F.

C)

E.

D)

P.

Page 25

105.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. If the market price is G, the firm’s total

cost of producing its most profitable level of output is:

A)

BS.

B)

DK.

C)

0FKD.

D)

0ESB.

106.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. If market price is G, the firm’s total

revenue from the sale of its most profitable level of output is:

A)

0GLD.

B)

0GHB.

C)

BH.

D)

DL.

107.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. If the market price is G, the firm’s total

economic profit at its most profitable level of output is:

A)

0GHB.

B)

EFJS.

C)

EGHS.

D)

FGLK.

108.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The minimum price that the firm must

receive to produce in the short run is:

A)

F.

B)

E.

C)

N.

D)

P.

109.

(Ref 24-10 Figure: A Perfectly Competitive Firm in the Short Run) Use Figure 24-10: A

Perfectly Competitive Firm in the Short Run. The firm’s short-run supply curve is the:

A)

entire MC curve.

B)

rising part of the MC curve beginning at point W.

C)

rising part of the MC curve beginning at the point at which the firm starts earning

economic profit.

D)

MC curve below point P.

Page 26

Use the following to answer questions 110-113:

110.

(Ref 24-11 Table: Soybean Cost) Use Table 24-11: Soybean Cost. If the market price of

a bushel of soybeans is $15, how many bushels will the farmer produce to maximize

short-run profit?

A)

2

B)

5

C)

3

D)

7

111.

(Ref 24-11 Table: Soybean Cost) Use Table 24-11: Soybean Cost. If the market price of

a bushel of soybeans is $15, what will be the farmer’s short-run profit at the optimal

level of production?

A)

$75

B)

$69

C)

$6

D)

$5

112.

(Ref 24-11 Table: Soybean Cost) Use Table 24-11: Soybean Cost. What is the

break-even price for this farmer?

A)

$13.00

B)

$13.50

C)

$14.00

D)

$14.50

Page 27

113.

(Ref 24-11 Table: Soybean Cost) Use Table 24-11: Soybean Cost. What is the

shut-down price for this farmer?

A)

$10

B)

$11

C)

$12

D)

$13

Use the following to answer questions 114-115:

114.

(Ref 24-12 Table: Lilly’s Apple Orchard) Use Table 24-12: Lilly’s Apple Orchard. Lilly

is the price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the

price of a bushel of apples is $25, how many bushels will Lilly produce to maximize

profit?

A)

0

B)

1

C)

2

D)

3

115.

(Ref 24-12 Table: Lilly’s Apple Orchard) Use Table 24-12: Lilly’s Apple Orchard. Lilly

is the price-taking owner of an apple orchard. Her orchard has fixed costs of $30. If the

price of a bushel of apples is $35, at the profit maximizing point, her economic profit

will be:

A)

-$30.

B)

-$5.

C)

$0.

D)

$5.

Page 28

Use the following to answer questions 116-122:

116.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. If the market price is $4.50, the

profit-maximizing output is _____ units.

A)

5

B)

7

C)

8

D)

9

117.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. If the market price is $3.50, the

profit-maximizing output is _____ units.

A)

5

B)

7

C)

8

D)

9

118.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. If the market price is $5.50, the

profit-maximizing quantity of output is _____ units.

A)

5

B)

7

C)

8

D)

9

Page 29

119.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. If the market price is $4.50, profit at the

profit-maximizing quantity of output is:

A)

$2.00.

B)

$4.50.

C)

$5.00.

D)

$34.00.

120.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. The firm will produce at a non-negative

economic profit in the short run if the price is at least:

A)

$2.00.

B)

$2.50.

C)

$3.50.

D)

$4.25.

121.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. In the short run, the firm will produce, but at a

loss, if the price is:

A)

$2.00.

B)

$2.50.

C)

$3.50.

D)

$4.50.

122.

(Ref 24-13 Table: Total Cost for a Perfectly Competitive Firm) Use Table 24-13: Total

Cost for a Perfectly Competitive Firm. The firm will stop production and shut down at

any price less than:

A)

$2.50.

B)

$2.83.

C)

$3.50.

D)

$5.00.

Page 30

Use the following to answer questions 123-124:

123.

(Ref 24-14 Figure: The Perfectly Competitive Firm) Use Figure 24-14: The Perfectly

Competitive Firm. The figure shows a perfectly competitive firm that faces demand

curve d and maximizes profit. If the market price is $3, the firm will produce _____

units of output per day.

A)

100

B)

250

C)

300

D)

400

124.

(Ref 24-14 Figure: The Perfectly Competitive Firm) Use Figure 24-14: The Perfectly

Competitive Firm. The figure shows a perfectly competitive firm that faces demand

curve d and maximizes profit. Given the market price, the firm’s total revenue per day

is:

A)

$475.

B)

$600.

C)

$900.

D)

$1,200.

Page 31

Use the following to answer question 125:

125.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of mowing each of the lawns from 1 through 10 is $10. Also assume that he can

only mow the quantities of lawn given in the table (and not numbers in between). His

only fixed cost is $1,000 for the mower. His variable costs include fuel, his time, and

mower parts. What is Alex’s break-even price?

A)

$100.00

B)

$10.00

C)

$50.00

D)

$27.50

Use the following to answer questions 126-127:

Page 32

126.

(Ref 24-14 Figure: The Perfectly Competitive Firm) Use Figure 24-14: The Perfectly

Competitive Firm. The figure shows a perfectly competitive firm that faces demand

curve d and maximizes profit. Given the market price, the firm’s total cost per day is:

A)

$475.

B)

$600.

C)

$900.

D)

$1,200.

127.

(Ref 24-14 Figure: The Perfectly Competitive Firm) Use Figure 24-14: The Perfectly

Competitive Firm. The figure shows a perfectly competitive firm that faces demand

curve d and maximizes profit. If the firm faces a market price of $3, its total profit per

day is:

A)

$0.

B)

$250.

C)

$600.

D)

$300.

Use the following to answer questions 128-129:

128.

(Ref 24-15 Figure: Short-Run Costs) Use Figure 24-15: Short-Run Costs. At the given

price, the MOST profitable level of output occurs at quantity:

A)

N.

B)

P.

C)

S.

D)

T.

Page 33

129.

(Ref 24-15 Figure: Short-Run Costs) Use Figure 24-15: Short-Run Costs. This firm’s

short-run supply curve begins at quantity:

A)

Q.

B)

R.

C)

S.

D)

T.

130.

Perfect competition is a model of the market that does not assume:

A)

a large number of firms.

B)

firms facing downward-sloping demand curves.

C)

firms producing identical goods.

D)

many buyers.

131.

When perfect competition prevails, which characteristic of firms are we likely to

observe?

A)

None of them ever has diminishing marginal returns.

B)

They all try to operate where price equals average variable cost.

C)

They all try to operate where price equals total cost.

D)

They are all price takers.

132.

Which statement is not an assumption that economists make when using the model of

perfect competition?

A)

Firms seek to maximize profits.

B)

The products of each firm in a particular market are identical.

C)

Each firm sets its price equal to its average total cost.

D)

Entry into and exit from the industry are easy.

Use the following to answer questions 133-148:

Page 34

133.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s costs for his perfectly competitive all-natural ice cream firm. If

the market price of a tub of ice cream is $67.50, how many tubs of ice cream will

Sergei’s firm produce?

A)

1

B)

2

C)

3

D)

4

134.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $67.50, how much is Sergei’s total

revenue at the profit-maximizing output?

A)

$270.00

B)

$170.00

C)

$100.00

D)

$67.50

135.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $67.50, how much is Sergei’s total cost

at the profit-maximizing output?

A)

$270.00

B)

$170.00

C)

$135.00

D)

$67.50

136.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $67.50, how much is Sergei’s profit at

the profit-maximizing output?

A)

$680.00

B)

$270.00

C)

$102.50

D)

$100.00

Page 35

137.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $50, what quantity will Sergei produce

to maximize profit?

A)

2

B)

3

C)

4

D)

5

138.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $50, how much is Sergei’s profit at the

profit-maximizing output?

A)

$680

B)

$330

C)

$150

D)

$40

139.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $35, how many tubs of ice cream will

Sergei produce in the short run?

A)

1

B)

2

C)

3

D)

4

140.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $35, how much is Sergei’s profit at the

optimal short-run output?

A)

-$5

B)

$110

C)

$180

D)

$330

Page 36

141.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $20, how many tubs of ice cream will

Sergei produce in the short run?

A)

0

B)

1

C)

2

D)

3

142.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. If the market price of a tub of ice cream is $20, how much is Sergei’s profit at the

optimal short-run output?

A)

$100

B)

$0

C)

-$5

D)

-$10

143.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. What is the minimum price that Sergei needs to receive for a tub of ice cream to

stay in business in the short run?

A)

$10.00

B)

$20.00

C)

$33.33

D)

$36.67

144.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. What is the minimum price that Sergei needs to receive for a tub of ice cream to

stay in business in the long run?

A)

$10.00

B)

$20.00

C)

$33.33

D)

$36.67

Page 37

145.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. How many tubs of ice cream will Sergei produce in the long run?

A)

1

B)

2

C)

3

D)

4

146.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. Where does Sergei’s short-run supply curve begin (assuming he can only produce

whole quantities of output)?

A)

P = $0, Q = 0

B)

P = $36.67, Q = 3

C)

P = $33.33, Q = 3

D)

P = $170, Q = 4

147.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all-natural ice cream

firm. Which point falls on Sergei’s short-run supply curve (assuming he can only

produce whole quantities of output)?

A)

P = $10, Q = 0

B)

P = $20, Q = 2

C)

P = $110, Q = 3

D)

P = $70, Q = 5

148.

(Ref 24-16 Table: Total Cost and Output) Use Table 24-16: Total Cost and Output,

which describes Sergei’s total costs for his perfectly competitive all natural ice cream

firm. If there are 100 firms in the all-natural ice cream industry, which point falls on the

industry short-run supply curve (assuming firms can only produce whole quantities of

output)?

A)

P = $10, Q = 0

B)

P = $20, Q = 200

C)

P = $110, Q = 3

D)

P = $70, Q = 5

Page 38

Use the following to answer questions 149-159:

149.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. What is Alexa’s shut-down price in the short run?

A)

$20

B)

$15

C)

$50

D)

$42

150.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price per cleared lot is $14, how many lots should Alexa clear?

A)

0

B)

40

C)

50

D)

20

Page 39

151.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $60, how many lots should Alexa clear?

A)

50

B)

40

C)

30

D)

20

152.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $60, what is Alexa’s profit or loss at the optimal

output?

A)

$3,000

B)

$1,100

C)

$900

D)

$3,850

153.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $60, what is Alexa’s profit per unit at the optimal

output?

A)

$60

B)

$42

C)

$35

D)

$18

Page 40

154.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $30, how many lots should Alexa clear?

A)

50

B)

40

C)

30

D)

0

155.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $30, what is Alexa’s profit at the optimal output?

A)

$1,200

B)

$450

C)

$0

D)

-$550

156.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. If the price to clear a lot is $30, what is Alexa’s profit per unit at the optimal

output?

A)

-$13.75

B)

$720

C)

$0

D)

-$12.25

Page 41

157.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. At what price does Alexa’ s short-run supply curve start?

A)

$200

B)

$15

C)

$50

D)

$42

158.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry. Assume that costs are constant in each interval; so, for example, the marginal

cost of clearing each of the lots from 1 through 10 is $20. Also assume that she can only

plow the quantities of the lots given in the table (and not numbers in between). Her only

fixed cost is $1,000 for a snowplow. Her variable costs include fuel, her time, and hot

coffee. Which point falls on Alexa’s short-run supply curve?

A)

P = $40, Q = 10

B)

P = $10, Q = 200

C)

P = $25, Q = 40

D)

P = $16, Q = 0

159.

(Ref 24-17 Table: Variable Costs for Lots) Use Table 24-17: Variable Costs for Lots.

During the winter, Alexa runs a snow-clearing service in a perfectly competitive

industry, which is made up of 50 identical firms. Assume that costs are constant in each

interval; so, for example, the marginal cost of clearing each of the lots from 1 through

10 is $20. Also assume that she can only plow the quantities of the lots given in the

table (and not numbers in between). Her only fixed cost is $1,000 for a snowplow. Her

variable costs include fuel, her time, and hot coffee. Which point falls on the industry

short-run supply curve?

A)

P = $40, Q = 60

B)

P = $10, Q = 10,000

C)

P = $25, Q = 2,000

D)

P = $25, Q = 40

Page 42

Use the following to answer questions 160-176:

160.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $60, how many lawns will

Alex mow?

A)

0

B)

20

C)

50

D)

40

161.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $60, how much is Alex’s

total revenue at the profit-maximizing output?

A)

$60

B)

$1,100

C)

$2,400

D)

$2,100

Page 43

162.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $60, how much is Alex’s

total cost at the profit-maximizing output?

A)

$60

B)

$1,100

C)

$2,400

D)

$2,100

163.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $60, how much is Alex’s

profit at the profit-maximizing output?

A)

$10

B)

$2,400

C)

$300

D)

$2,100

164.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $60, how much is Alex’s

profit per unit at the profit-maximizing output?

A)

$7.50

B)

$32.50

C)

$20.00

D)

$60.00

Page 44

165.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $40, how many lawns will

Alex mow?

A)

0

B)

20

C)

30

D)

40

166.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $40, how much is Alex’s

total revenue at the profit-maximizing output?

A)

$1,000

B)

$1,200

C)

$500

D)

$1,500

167.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $40, how much is Alex’s

total cost at the profit-maximizing output?

A)

$1,000

B)

$1,200

C)

$500

D)

$1,500

Page 45

168.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $40, how much is Alex’s

profit at the profit-maximizing output?

A)

-$10

B)

-$300

C)

$300

D)

-$1,000

169.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $40, how much is Alex’s

profit per unit at the profit-maximizing output?

A)

-$10.00

B)

$10.00

C)

$23.33

D)

-$20.00

170.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $70, how many lawns will

Alex mow?

A)

20

B)

30

C)

40

D)

50

Page 46

171.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $70, how much is Alex’s

total revenue at the profit-maximizing output?

A)

$3,500

B)

$2,800

C)

$2,100

D)

$1,800

172.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $70, how much is Alex’s

total cost at the profit-maximizing output?

A)

$3,500

B)

$2,800

C)

$2,100

D)

$1,500

173.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $70, how much is Alex’s

profit at the profit-maximizing output?

A)

$3,500

B)

-$300

C)

$700

D)

$1,700

Page 47

174.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. If the price for mowing a lawn is $70, how much is Alex’s

profit per unit at the profit-maximizing output?

A)

-$10

B)

$10

C)

$34

D)

$14

175.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry. Assume that costs are constant in each interval; so, for

example, the marginal cost of mowing each of the lawns from 1 through 10 is $10. Also

assume that he can only mow the quantities of lawn given in the table (and not numbers

in between). His only fixed cost is $1,000 for the mower. His variable costs include fuel,

his time, and mower parts. Which point falls on Alex’s short-run supply curve?

A)

P = $5, Q = 10

B)

P = $10, Q = 100

C)

P = $60, Q = 40

D)

P = $20, Q = 300

176.

(Ref 24-18 Table: Variable Costs for Lawns) Use Table 24-18: Variable Costs for

Lawns. During the summer, Alex runs a lawn-mowing service, and lawn-mowing is a

perfectly competitive industry with 100 firms. Assume that costs are constant in each

interval; so, for example, the marginal cost of mowing each of the lawns from 1 through

10 is $10. Also assume that he can only mow the quantities of lawn given in the table

(and not numbers in between). His only fixed cost is $1,000 for the mower. His variable

costs include fuel, his time, and mower parts. Which point falls on the industry short-run

supply curve?

A)

P = $5, Q = 100

B)

P = $8, Q = 1,000

C)

P = $40, Q = 1,100

D)

P = $70, Q = 5,000

177.

A perfectly competitive firm’s demand curve is perfectly elastic at the

market-determined price.

A)

True

B)

False

Page 48

178.

In the short run, if a perfectly competitive firm chooses to produce, then its profits are

maximized by producing the quantity of output where marginal cost equals marginal

revenue.

A)

True

B)

False

179.

According to the optimal output rule, profits are maximized when firms produce where

the difference between marginal revenue and marginal cost is the largest.

A)

True

B)

False

180.

State and explain the price-taking firm’s optimal output rule.

181.

Why does it make sense for a firm to shut down in the short run if the price falls below

minimum average variable cost?

182.

Sam is one of many growers who sell potatoes to a large food-processing plant. The

price of a bushel of potatoes is $4, and Sam sells 100 bushels at that price. He has $250

of fixed cost. Sam figures that, if he produces one more bushel of potatoes, his total

variable costs will increase from $175 to $180. Is Sam currently earning a positive

economic profit? Should he stay in business in the short run? Show how you came to

your answer. Also, should Sam produce any more bushels of potatoes (i.e., a 101st

bushel) at a price of $4? Explain.

183.

When a firm produces at an output level at which MR = MC, it is operating at the _____

level.

A)

shut-down

B)

break-even

C)

optimal-output

D)

minimum-cost

184.

The addition to the total revenue from selling one more unit of the good is:

A)

less than the market price.

B)

average profit.

C)

marginal cost.

D)

marginal revenue.

Page 49

185.

Ashley, who makes knitted caps, determines that her marginal cost of knitting one more

cap is $10. A consumer offers her $12 for one more knitted cap. Ashley will:

A)

not sell the additional cap since she does not know what her total costs will be.

B)

sell the additional cap since the marginal revenue is greater than the marginal cost

for the unit.

C)

realize that her production is not profitable and shut down her business.

D)

offer to sell 20 additional caps since it must be profitable.

186.

Tony runs Read Economic Reports. If Tony finds that the cost of completing an

additional report is $100 and someone offers him $125 to complete this additional

report, Tony should:

A)

not complete the additional report since he will incur a loss.

B)

complete the additional report only if the person buys two additional reports.

C)

complete the additional report.

D)

not complete the additional report since his additional cost is more than his

additional revenue.

187.

Firms will make a profit in the long run or short run if the price is:

A)

equal to marginal revenue.

B)

greater than ATC.

C)

less than MC.

D)

greater than AVC.

188.

If a firm’s economic profits are equal to zero, its accounting profits are MOST likely:

A)

less than zero.

B)

positive.

C)

less than fixed costs.

D)

equal to zero.

189.

A firm produces at the output level at which its average total costs are minimized. At

this output level, its average total costs are NOT equal to:

A)

price.

B)

MC.

C)

MR.

D)

AVC.

Page 50

190.

Maximizing profits also means that a firm is attempting to:

A)

make as much output as possible.

B)

change the market price.

C)

produce at the output level where the difference between total revenue and total

cost is the greatest.

D)

produce below its break-even price.

191.