480 Miller Economics Today, 16th Edition

9) Using a graph, show a short run equilibrium for the industry and the firm. Explain the graph.

23.9 The Long Run Industry Situation: Exit and Entry

1) Market signals

A) are ways of conveying information. B) do not involve economic profits.

C) are best ignored by investors. D) do not involve economic losses.

2) What is the shape of the long run supply curve in a decreasing cost industry?

A) Horizontal B) Increasing

C) Downward sloping D) Upward sloping

3) In the long run when a perfectly competitive firm experiences positive economic profits,

A) firms exit the industry, the market supply curve shifts rightward, and the market price

falls.

B) firms enter the industry, the market supply curve shifts rightward, and the market price

falls.

C) firms exit the industry, the market supply curve shifts leftward, and the market price rises.

D) firms enter the industry, the market supply curve shifts rightward, and the market price

rises.

4) In the long run when a perfectly competitive firm experiences negative economic profits,

A) firms exit the industry, the market supply curve shifts rightward, and the market price

falls.

B) firms enter the industry, the market supply curve shifts rightward, and the market price

falls.

C) firms exit the industry, the market supply curve shifts leftward, and the market price rises.

D) firms enter the industry, the market supply curve shifts rightward, and the market price

rises.

5) If an industry has constant marginal and average costs, any shift in demand will eventually

A) result in a higher equilibrium price.

B)

b

e met by a smaller change in quantity supplied.

C)

b

e met by an equal change in quantity supplied, and equilibrium price will not change.

D) make economic profits zero in the short run.

6) In a perfectly competitive market, positive economic profits act to

A) attract new entrants into the industry.

B) drive potential competitors away from the industry.

C) prevent reinvestment on the part of firms within the industry.

D) signal resource owners elsewhere not to invest their capital in this industry.

7) In a perfectly competitive market, if P ATC in the short run, there is apt to be

A) entry of new firms into the market.

B) an accounting loss for existing firms.

C) an inward shift in the industry supply curve.

D) an upward pressure on price.

8) If a perfect competitor faces P ATC in the long run, the firm will

A) earn economic profits. B) earn economic losses.

C) leave the industry. D) remain in the industry.

9) The exiting of firms from a perfectly competitive industry occurs when

A) opportunity costs cannot be covered.

B) P ATC.

C) accounting profit is less than economic profit.

D) MR equals MC.

10) In a perfectly competitive industry, which of the following is a market signal to resource

owners?

A) Economic profits

B) Quality of goods

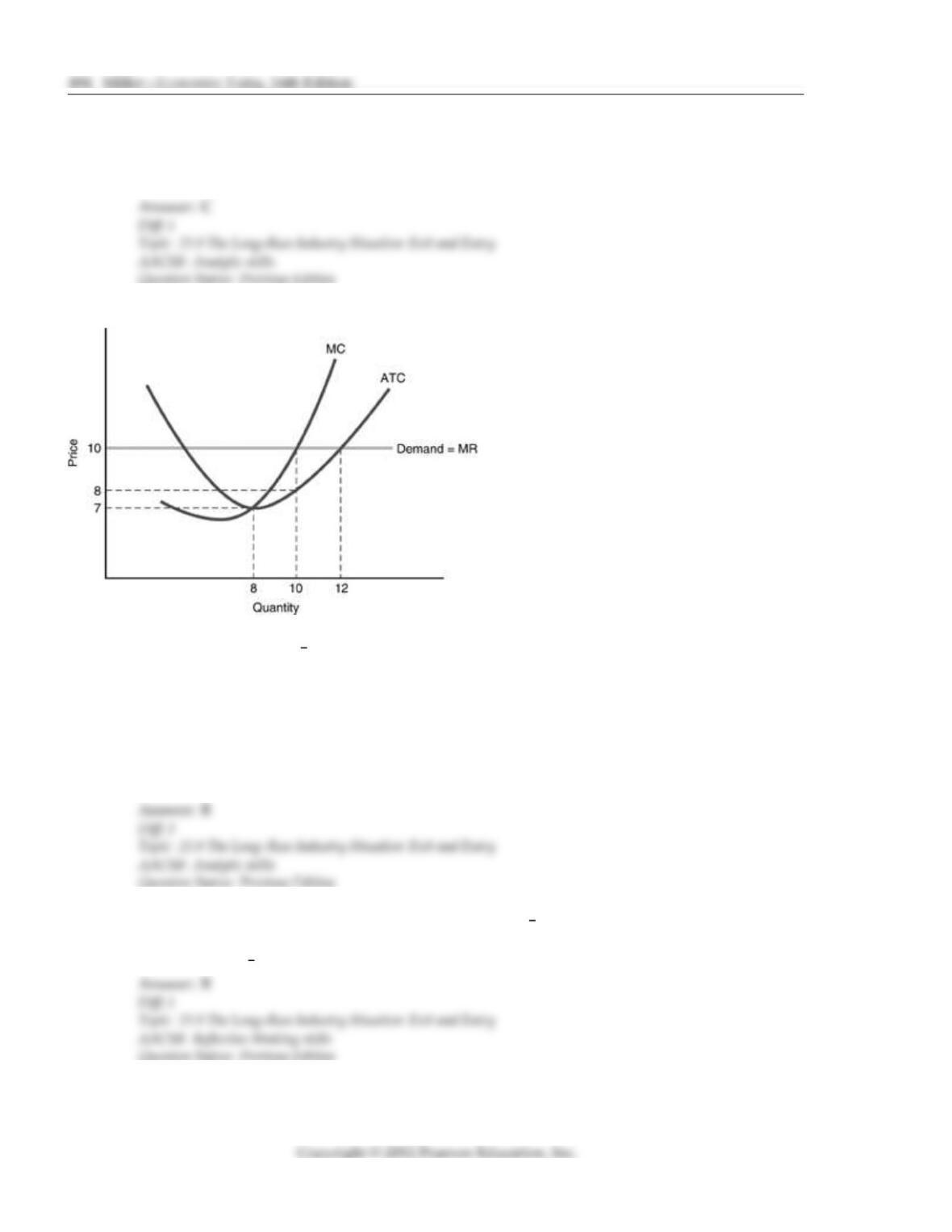

C) The level of exports in the country

D) The level of subsidies the industry receives

11) Economic profits and losses are true market signals because they

A) convey information in an asymmetrical fashion.

B) convey information about rewards people should anticipate experiencing by shifting

resources from one activity to another.

C) convey information to public officials about where to encourage people to invest and what

skills people should develop.

D) cause people to move into careers in both undesirable and desirable industries with equal

ease.

12) A law that restricts plant closings will

A) make the economy more efficient by slowing down the movement of resources to a more

optimal rate.

B) make the economy more efficient by reducing poor decisions on the part of entrepreneurs.

C) prevent resources from flowing to their highest valued uses.

D) allow profits and losses to provide a signaling function.

13) In a decreasing cost industry, an increase in output will lead to

A) an upward shift in the ATC curve. B) an upward shift in the MC curve.

C) a reduction in long run per unit costs. D) an increase in long run per unit costs.

14) In an increasing cost industry, an increase in output will lead to

A) an downward shift in the ATC curve. B) an downward shift in the MC curve.

C) a reduction in long run per unit costs. D) an increase in long run per unit costs.

15) If an industry s long run per unit costs increase as its output increases then

A) the firm s long run economic profits must be greater than zero.

B) the firm is most likely a decreasing cost industry.

C) the firm is most likely an increasing cost industry.

D) the firm is most likely a constant cost industry.

16) If an industry s long run per unit costs decrease as its output increases then

A) the firm s long run economic profits must be less than zero.

B) the firm is most likely a decreasing cost industry.

C) the firm is most likely an increasing cost industry.

D) the firm is most likely a constant cost industry.

17) If an industry s long run per unit costs are constant as its output increases then

A) the firm s long run economic profits must be greater than zero.

B) the firm is most likely a decreasing cost industry.

C) the firm is most likely an increasing cost industry.

D) the firm is most likely a constant cost industry.

18) If a constant cost, perfectly competitive industry experiences an increase in the demand for its

product, we would expect

A) only the market price of the good to increase.

B)

b

oth the market price and quantity supplied to increase.

C) decreases in the market price, but increases in quantity supplied.

D) only the quantity supplied of the product to increase.

19) A constant cost industry is one in which

A) output increases lead to productivity gains.

B) the marginal product of labor is constant.

C) there is no change in long run per unit costs, even as output varies.

D) each firm has a horizontal long run average cost curve.

20) In an increasing cost industry, an increase in industry output will

A) lead to a higher market price.

B) lead to a lower market price.

C) shift each firm s average fixed cost curve down.

D) shift each firm s short run supply curve down.

21) In a decreasing cost industry, an increase in industry output will

A) lead to a higher market price.

B) lead to a lower market price.

C) shift each firm s average fixed cost curve up.

D) shift each firm s short run supply curve up.

22) A constant cost industry

A) is one in which an increase in demand is matched by a proportional increases in long run

supply.

B) generates increasing profits whenever demand increases because the new long run

equilibrium price is above the old price even though average costs have not changed.

C) has a horizontal long run supply curve.

D) has a downward sloping long run supply curve.

23) When economic profits in a perfectly competitive industry are positive,

A) new firms will be attracted to the industry, and economic profits will decline to zero.

B) the industry is in equilibrium.

C) firms will increase output to earn even higher profits.

D) firms will increase prices while they have the opportunity.

24) In a perfectly competitive industry, any restrictions that prevent new firms from entering

A) lead to negative profits.

B) guarantee that all existing firms will earn exactly a zero profit.

C) hinder economic efficiency.

D) reduce the average cost of production.

25) Signals are

A) used by economic decision makers to inform others about their plans.

B) the method by which government planners inform economic decision makers about the

types of decisions they should make.

C) the method by which firms determine their profit maximizing quantity.

D) compact ways of conveying to economic decision makers information needed to identify

industries where more resources are needed.

26) A true signal must

A) convey information only.

B) convey information and direct the resource owners to act appropriately.

C) convey information about the long run future.

D) explain in detail why something should be done.

27) Profits and losses are true signals because they

A) convey information about true long run profits.

B) cannot be misinterpreted by entrepreneurs.

C) convey information about where to place resources and reward people who act on the

information.

D) reward people who make profits with even more profits and punish those who make

losses with even more losses.

28) Firms in a perfectly competitive industry are earning economic losses. This is

A) a signal to entrepreneurs that some of the firms in the industry should exit and the

resources of these firms should move into production of other goods.

B) a signal to entrepreneurs that additional resources should be brought into this industry in

order to make it profitable.

C) a signal that the entrepreneurs are doing a poor job and should become workers for

someone else.

D) a signal to government officials that a subsidy is needed for the firms in the industry.

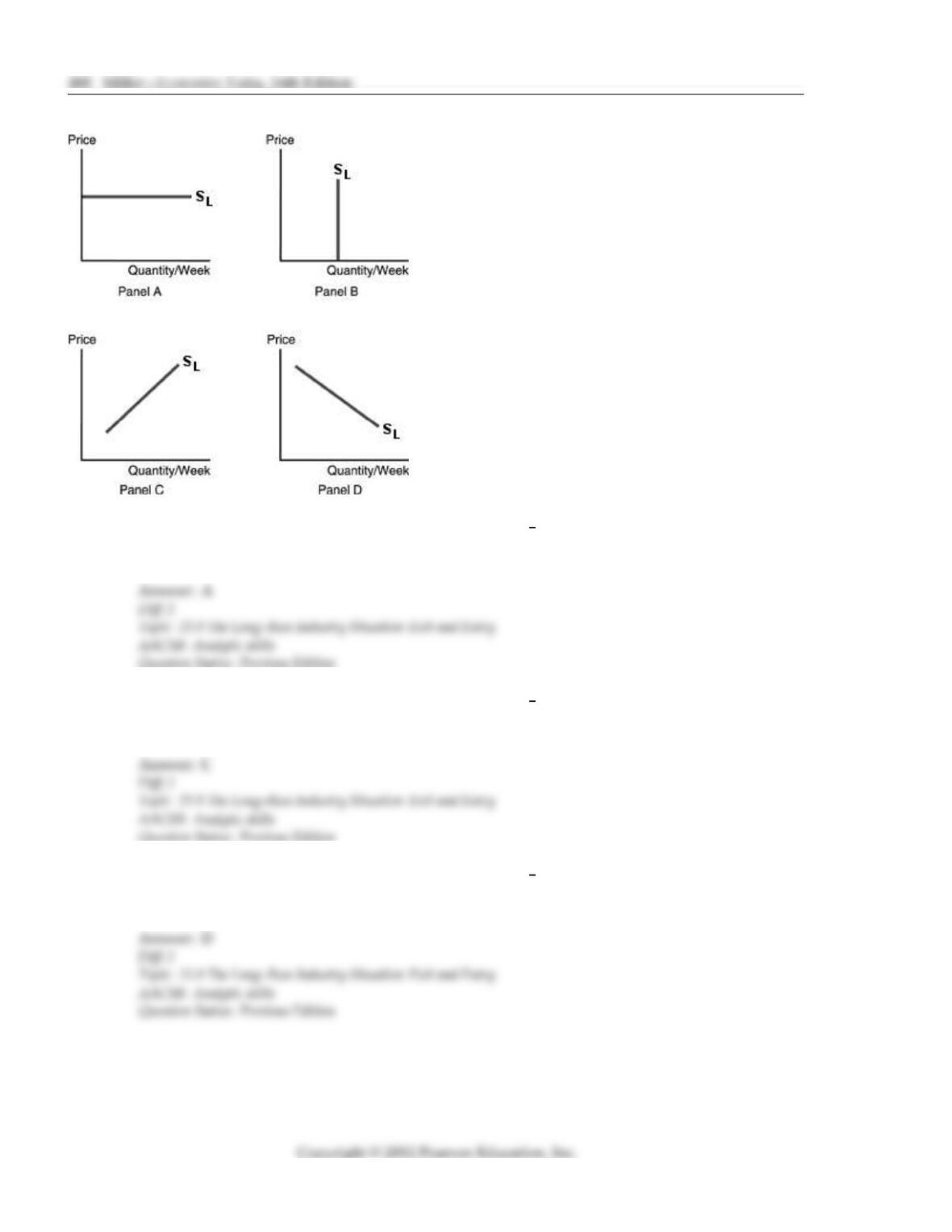

29) Refer to the above figure. Which panel represents the long run supply curve for a constant cost

industry?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

30) Refer to the above figure. Which panel represents the long run supply curve for an increasing

cost industry?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

31) Refer to the above figure. Which panel represents the long run supply curve for a decreasing

cost industry?

A) Panel A. B) Panel B. C) Panel C. D) Panel D.

32) Which of the following would tell us that resources are not flowing to their highest valued uses?

A) Short run economic profits B) Short run economic losses

C) Long run economic profits D) Some firms are just breaking even.

33) Along an industry s long run supply curve,

A) economic profits are positive.

B) economic profits are zero.

C) entrepreneurs earn an above average rate of return.

D) the number of firms is constant.

34) If the long run supply curve is upward sloping, we know that

A) entrepreneurs are earning higher profits as output expands.

B) some input prices are increasing as the industry expands.

C) firms are getting larger as the industry contracts.

D) the law of diminishing marginal returns has set in.

35) An industry whose total output can be increased without a change in long run per unit costs is

a(n)

A) increasing cost industry. B) constant cost industry.

C)

b

reak even cost industry. D) decreasing cost industry.

36) An industry in which an increase in industry output is accompanied by an increase in long run

per unit costs is a(n)

A) increasing cost industry. B) constant cost industry.

C)

b

reak even cost industry. D) decreasing cost industry.

37) An industry in which an increase in output leads to a reduction in long run per unit costs is

a(n)

A) increasing cost industry. B) constant cost industry.

C)

b

reak even cost industry. D) decreasing cost industry.

38) Suppose a perfectly competitive industry is in long run equilibrium. If a decrease in demand

leads to a lower long run price, we know that

A) this is a decreasing cost industry.

B) this is an increasing cost industry.

C) some firms will be losing money in the long run.

D) after further adjustments, price will rise to its original level.

39) Suppose a perfectly competitive industry is in long run equilibrium. If a decrease in demand

leads to a higher long run price, we know that

A) this is a decreasing cost industry.

B) this is an increasing cost industry.

C) some firms will be losing money in the long run.

D) after further adjustments, price will fall to its original level.

40) A perfectly elastic long run supply curve indicates

A) a decreasing cost industry.

B) a constant cost industry.

C) an increasing cost industry.

D) that some input prices change as firms enter and exit the industry.

41) If the long run supply curve is horizontal, we know that this is

A) a decreasing cost industry.

B) a constant cost industry.

C) an increasing cost industry.

D) a situations in which some input prices change as firms enter and exit the industry.

42) If the long run supply curve slopes downward, we know that this is

A) a decreasing cost industry.

B) a constant cost industry.

C) an increasing cost industry.

D) a situation in which no input prices change as firms enter and exit the industry.

43) If the long run supply curve slopes upward, we know that this is

A) a decreasing cost industry.

B) a constant cost industry.

C) an increasing cost industry.

D) a situation in which no input prices change as firms enter and exit the industry.

44) Consider an industry that is in long run equilibrium. An increase in demand leads to an

increase in the price of the good. We know that this is

A) a decreasing cost industry. B) a constant cost industry.

C) an increasing cost industry. D) not a competitive industry.

45) Consider an industry that is in long run equilibrium. An increase in demand leads to a decrease

in the price of the good. We know that this is

A) a decreasing cost industry. B) a constant cost industry.

C) an increasing cost industry. D) not a competitive industry.

46) Consider an industry that is in long run equilibrium. An increase in demand leads to no change

in the price of the good. We know that this is

A) a decreasing cost industry. B) a constant cost industry.

C) an increasing cost industry. D) not a competitive industry.

47) An increasing cost industry will have

A) a perfectly elastic long run supply curve.

B) a perfectly inelastic long run supply curve.

C) an upward sloping supply curve in the long run.

D) an upward sloping demand curve in the long run.

48) A decreasing cost industry will have

A) a perfectly elastic long run supply curve.

B) a perfectly inelastic long run supply curve.

C) an upward sloping demand curve in the long run.

D) a downward sloping supply curve in the long run.

49) If an industry s long run supply curve slopes downward, then the industry is

A) a fixed cost industry. B) a constant cost industry.

C) an increasing cost industry. D) a decreasing cost industry.

50) A constant cost industry will have

A) a perfectly elastic long run supply curve.

B) a perfectly inelastic long run supply curve.

C) an upward sloping demand curve in the long run.

D) an upward sloping supply curve in the long run.

51) A perfectly competitive firm will not earn an economic profit in the long run, because

A) it is a price maker.

B) it faces a perfectly inelastic demand curve.

C) there are no barriers to entry into the industry.

D) it produces differentiated products.

52) When a perfectly competitive firm experiences positive economic profits,

A) the high barriers to entry prevent further competition.

B) existing firms exit the industry.

C) additional firms enter the industry.

D) firms have no incentive to exit or enter the industry.

53) In the long run when a perfectly competitive firm experiences negative economic profits,

A) the high barriers to entry prevent further competition.

B) existing firms exit the industry.

C) additional firms enter the industry.

D) firms have no incentive to exit or enter the industry.

54) When a perfectly competitive firm experiences zero economic profits,

A) the high barriers to entry prevent further competition.

B) existing firms exit the industry.

C) additional firms enter the industry.

D) firms have no incentive to exit or enter the industry.

55) The motive that drives firms to enter or exit an industry is

A) utility. B) governmental.

C) economic profit. D) accounting costs.

56) If a firm is earning short run economic profits shown in the above figure, in the long run

A) firms exit the industry, the market supply curve shifts rightward, and the market price

falls.

B) firms enter the industry, the market supply curve shifts rightward, and the market price

falls.

C) firms exit the industry, the market supply curve shifts leftward, and the market price falls.

D) firms enter the industry, the market supply curve shifts rightward, and the market price

rises.

57) Which of the following is the best example of a decreasing cost industry?

A) the health care industry B) the personal computer industry

C) the college education industry D) the oil industry