Page 1

1.

If a California avocado stand operates in a perfectly competitive market, that stand’s

owner will be a price:

A)

maker.

B)

taker.

C)

discriminator.

D)

maximizer.

2.

If all firms in an industry are price takers:

A)

each firm can sell at the price it wants to charge, provided it is not too different

from the prices other firms are charging.

B)

each firm takes the market price as given for its output level, recognizing that the

price will change if it alters its output significantly.

C)

an individual firm cannot alter the market price even if it doubles its output.

D)

the market sets the price, and each firm can take it or leave it by setting a different

price.

3.

The assumptions of perfect competition imply that:

A)

individuals in the market accept the market price as given.

B)

individuals can influence the market price.

C)

the price will be fair.

D)

the price will be high.

4.

Price takers are individuals in a market who:

A)

select a price from a wide range of alternatives.

B)

select the lowest price available in a competitive market.

C)

select the average of prices available in a competitive market.

D)

have no ability to affect the price of a good in a market.

5.

Individuals in a market who must take the market price as given are:

A)

quantity minimizers.

B)

quantity takers.

C)

price takers.

D)

price searchers.

6.

Perfect competition is characterized by:

A)

rivalry in advertising.

B)

fierce quality competition.

C)

the inability of any one firm to influence price.

D)

widely recognized brands.

Page 2

7.

When a firm cannot affect the market price of the good that it sells, it is said to be a:

A)

price taker.

B)

natural monopoly.

C)

dominant firm.

D)

cartel.

8.

The assumptions of perfect competition imply that:

A)

individuals in the market determine the market price.

B)

firms in the market accept the market price as given.

C)

there will be no new competition due to natural monopolies.

D)

the price will be decreasing yearly.

9.

In the model of perfect competition:

A)

the consumer is at the mercy of powerful firms that can set prices wherever they

prefer.

B)

individual firms can influence the price, but only slightly.

C)

no individual or firm has enough power to affect price.

D)

the price is determined by how many years are left in the product’s patent.

10.

A perfectly competitive firm is a:

A)

price taker.

B)

price searcher.

C)

cost maximizer.

D)

quantity taker.

11.

If a Florida strawberry wholesaler operates in a perfectly competitive market, that

wholesaler will have a _____ share of the market, and consumers will consider her

strawberries and her competitors’ strawberries to be _____. Therefore, _____

advertising will take place in this market.

A)

large; standardized; no

B)

small; standardized; little or no

C)

small; differentiated; no

D)

large; differentiated; extensive

12.

One characteristic of a perfectly competitive market is that there are _____ sellers of the

good or service.

A)

one or two

B)

a few

C)

usually fewer than 10

D)

many

Page 3

13.

Which statement is not a characteristic of a perfectly competitive industry?

A)

Firms seek to maximize profits.

B)

Profits may be positive in the short run.

C)

There are many firms.

D)

Products are differentiated.

14.

In a perfectly competitive industry, each firm:

A)

is a price maker.

B)

produces about half of the total industry output.

C)

produces a differentiated product.

D)

produces a standardized product.

15.

For the Colorado beef industry to be classified as perfectly competitive, ranchers in

Colorado must have _____ on prices and beef must be a _____ product.

A)

no noticeable effect; standardized

B)

a huge effect; standardized

C)

a huge effect; differentiated

D)

no noticeable effect; differentiated

16.

Which statement describes a necessary condition for perfect competition?

A)

A small number of firms control a large share of the total market.

B)

Movement into and out of the market is limited.

C)

Firms produce a standardized product.

D)

Extensive advertising is used to promote the firm’s product.

17.

Which statement is not characteristic of perfect competition?

A)

All firms produce the same standardized product.

B)

There are many producers, and each has only a small market share.

C)

There are many producers; one firm has a 25% market share, and all of the

remaining firms have a market share of less than 2% each.

D)

There are no obstacles to entry into or exit from the industry.

18.

The perfectly competitive model does not assume:

A)

a great number of buyers.

B)

easy entry to and exit from the market.

C)

a standardized product.

D)

that firms attempt to maximize their total revenue.

Page 4

19.

The market for breakfast cereal contains hundreds of similar products, such as Fruit

Loops, cornflakes, and Rice Krispies, that are considered to be different products by

different buyers. This situation violates the perfect competition assumption of:

A)

many buyers and sellers.

B)

a standardized product.

C)

ease of entry.

D)

ease of exit.

20.

An assumption of the model of perfect competition is:

A)

discrimination.

B)

difficult entry and exit.

C)

many buyers and sellers.

D)

limited information.

21.

The competitive model of markets does notassume:

A)

a large number of buyers.

B)

easy entry into and exit from the market.

C)

a standardized product.

D)

patents and copyrights that serve as barriers to entry into the industry.

22.

_____ almost always take the market price as given; that is, they are considered _____.

However, this is often not true of _____.

A)

Consumers; quantity minimizers; producers

B)

Producers; quantity takers; consumers

C)

Consumers and producers; price takers; firms that produce a differentiated product

D)

Producers; price searchers; consumers

23.

An assumption of the model of perfect competition is:

A)

identical goods.

B)

difficult entry and exit.

C)

few buyers and sellers.

D)

cooperation and interdependence between sellers.

24.

People in the eastern part of Beirut are prevented by border guards from traveling to the

western part of Beirut to shop for or sell food. This situation violates the perfect

competition assumption of:

A)

price-setting behavior.

B)

a small number of buyers and sellers.

C)

differentiated goods.

D)

ease of entry and exit.

Page 5

25.

When perfect competition prevails, which characteristic of firms are we likely to

observe?

A)

They erect and maintain barriers to new firms.

B)

There are not many of them.

C)

They all try to highlight the substantial product differentiation between producers.

D)

They are all price takers.

26.

If a perfectly competitive firm reduces its output, the market price will increase.

A)

True

B)

False

27.

Microsoft’s Windows operating system is a standardized product, since everyone who

buys a particular version of the product gets exactly the same thing. This means that

Microsoft is a perfectly competitive firm.

A)

True

B)

False

28.

If the Kansas corn market is perfectly competitive, it means there is easy entry into this

market.

A)

True

B)

False

29.

Markets for new drugs are not usually perfectly competitive since the companies that

manufacture these drugs are usually granted patents, restricting entry into the industry.

A)

True

B)

False

30.

Why is the market for soybeans a better example of perfect competition than is the

market for cars?

31.

Why are perfectly competitive firms described as price takers?

32.

In a perfectly competitive market, _____ are price takers.

A)

only consumers

B)

only producers

C)

both producers and consumers

D)

neither producers nor consumers

Page 6

33.

Perfectly competitive industries are characterized by:

A)

few sellers and many buyers.

B)

consumers who can differentiate between products.

C)

standardized goods.

D)

a few producers who make up most of the market share of the industry.

34.

In perfect competition, _____ are _____, and _____ are price takers.

A)

all goods; standardized; all market participants

B)

some goods; standardized; consumers but not producers

C)

all goods; differentiated; producers but not consumers

D)

some goods; differentiated; consumers but not producers

35.

Market structures are categorized by:

A)

the number and size of the firms.

B)

whether products are differentiated and the extent of advertising.

C)

the number of firms and whether products are differentiated.

D)

the size of the firms and the extent of advertising.

36.

Which statement about the differences between monopoly and perfect competition is

incorrect?

A)

A monopolist has market power, while a perfect competitor does not.

B)

Unlike a perfectly competitive firm, a monopoly can make positive economic

profits in the long run.

C)

A monopoly will charge a higher price and produce a smaller quantity than will a

competitive market with the same demand and cost structure.

D)

Monopoly profits can continue in the long run because the monopoly produces

more and charges a higher price than does a comparable perfectly competitive

industry.

37.

Which statement concerning monopoly is true?

A)

Monopoly firms are always larger than are perfectly competitive firms.

B)

A monopoly has no rivals.

C)

Barriers to entry do not prevent other firms from entering a monopolized industry.

D)

Monopolists produce more output than does a competitive market with the same

demand and cost structure.

Page 7

38.

_____ firms have the most market power.

A)

Monopoly

B)

Duopoly

C)

Oligopoly

D)

Monopolistic competition

39.

An industry with a single producer that sells a single product with no substitutes is a:

A)

perfectly competitive industry.

B)

monopoly.

C)

oligopoly.

D)

monopolistically competitive industry.

40.

An industry with a firm that is the only producer of a good or service for which there are

no close substitutes and for which entry by potential rivals is prohibitively difficult is:

A)

a duopoly.

B)

a monopoly.

C)

an oligopoly.

D)

perfect competition.

41.

A monopoly is a market characterized by a:

A)

single seller.

B)

product with many close substitutes.

C)

large number of small firms.

D)

small number of large firms.

42.

A monopoly:

A)

produces a product with no close substitutes.

B)

is composed of a single buyer and several sellers.

C)

is composed of a large number of small firms.

D)

is composed of a small number of large firms.

43.

Diamond rings are relatively scarce because:

A)

according to geologists, diamonds are less common than is any other gem-quality

stone.

B)

the demand for diamonds is so high.

C)

diamond producers limit the quantity supplied to the market.

D)

of monopolistic competition.

Page 8

44.

De Beers became a monopoly by:

A)

establishing control over diamond mines.

B)

use of economies of scale.

C)

use of technological superiority.

D)

ownership of a patent.

45.

A monopolist is likely to produce _____ and charge _____ than is a comparable

perfectly competitive firm.

A)

more; more

B)

less; more

C)

more; less

D)

less; less

46.

In contrast with perfect competition, a monopolist:

A)

produces more at a lower price.

B)

produces where MR > MC, and a perfectly competitively firm produces where P =

MC.

C)

may have economic profits in the long run.

D)

earns zero economic profits in the long run.

47.

Because of monopoly, consumers experience _____ than they do with perfect

competition.

A)

more choices

B)

larger quantities

C)

higher quality

D)

higher prices

48.

The ability of a monopolist to raise the price of a product above the competitive level by

reducing the output is known as:

A)

product differentiation.

B)

barrier to entry.

C)

market power.

D)

patents and copyrights.

49.

Of the four market structures, the only one that is characterized by product

differentiation is oligopoly.

A)

True

B)

False

Page 9

50.

A producer is a monopoly if it is the sole supplier of a good that has no close substitutes.

A)

True

B)

False

51.

A monopoly increases price by limiting the quantity supplied to a market.

A)

True

B)

False

52.

To maintain profits in the long run, a monopoly must be protected by barriers to the

entry of other firms into the industry.

A)

True

B)

False

53.

A monopoly may continue to make economic profits in the long run because of the

barriers to entry in its industry.

A)

True

B)

False

54.

The government can reduce the inefficiency associated with a monopoly through a

system of patents and copyrights.

A)

True

B)

False

55.

A natural monopoly has small fixed costs, which allows it to produce at lower cost than

can potential competitors.

A)

True

B)

False

56.

Years ago, Callaway Golf patented its signature Big Bertha line of drivers. Today, the

company spends a lot of money prosecuting individuals that try to sell knock-off Big

Bertha drivers to the public. What is the purpose of the patent, and why do companies

like Callaway Golf fight those that try to imitate their products?

A)

there are few firms, each producing a differentiated or similar product.

B)

there are many firms, each producing a similar product.

C)

all market participants are price takers.

D)

only one firm produces a very differentiated product.

Page 10

57.

A monopolistically competitive industry is made up of:

A)

a few firms, each producing a very differentiated good.

B)

one firm that produces a standardized good.

C)

market participants who are all price takers.

D)

many firms producing a slightly differentiated product.

58.

Entry barriers:

A)

exist in all market structures.

B)

exist in perfect competition and monopolistically competitive markets.

C)

do not exist in any market structures; otherwise nothing would be produced.

D)

exist in monopoly and oligopoly markets.

59.

Control of a scarce resource or input, economies of scale, technological superiority, and

government-set rules and regulations are forms of:

A)

market structure.

B)

pricing behavior.

C)

barriers to entry.

D)

public policy.

60.

When a firm finds that its ATC of production decreases as it increases production, this

firm is said to be experiencing:

A)

profit maximization.

B)

economic profit.

C)

economies of scale.

D)

a barrier to entry.

61.

If large fixed costs result in ATC falling as output increases and this occurs over the

relevant range of output, this industry is a:

A)

constant-cost industry.

B)

natural monopoly.

C)

network externality.

D)

profit maximizer.

62.

A natural monopoly exists when:

A)

a few firms collude to make one large firm.

B)

economies of scale provide large cost advantages to having one firm produce the

industry’s output.

C)

firms naturally maximize profit regardless of market structure.

D)

firms enter the industry as a result of profit incentives.

Page 11

63.

Goods that are subject to network externalities tend to be ones:

A)

for which the value of the good to an individual is lower when more people use it.

B)

that are land-intensive.

C)

for which the value of the good to an individual is higher when more people use it.

D)

for which one person owning the good enhances its value because it’s the only one.

64.

Temporary monopolies via the provision of sole ownership rights to profit from the

production, use, or sale of a good are provided by:

A)

patents and copyrights.

B)

natural monopolies.

C)

profit-maximizing behavior.

D)

network externalities.

65.

The sum of the squared market shares of each firm in an industry is the:

A)

concentration ratio.

B)

employment rate.

C)

Herfindahl-Hirschman index.

D)

market number.

66.

A monopoly will have a Herfindahl-Hirschman index equal to:

A)

1.

B)

100.

C)

1,000.

D)

10,000.

67.

Which Herfindahl-Hirschman index is most likely to indicate a perfectly competitive

market?

A)

100

B)

1,800

C)

10,000

D)

100,000

68.

The Herfindahl-Hirschman index is a measure of concentration found by:

A)

squaring the percentage market share of each firm in the industry.

B)

squaring the percentage market share of each firm in the industry and then

summing the squared market shares.

C)

summing the percentage market shares of each firm in the industry.

D)

squaring the sums of the concentration ratios found in an industry survey of the

largest four and largest eight firms.

Page 12

69.

The largest Herfindahl-Hirschman index possible is _____, and the industry is a(n)

_____.

A)

10; monopoly

B)

10,000; monopoly

C)

100,000; monopoly

D)

100,000; oligopoly

70.

The Herfindahl-Hirschman index equals _____ when _____ have/has _____% of the

market.

A)

10,000; four firms each; 25

B)

5,000; three firms each; 33

C)

5,000; two firms each; 50

D)

100,000; one firm; 100

71.

In an oligopoly:

A)

there are many sellers.

B)

there are no barriers to entry.

C)

firms recognize their interdependence.

D)

total surplus is maximized.

72.

The most important source of oligopoly in an industry is:

A)

economies of scale.

B)

government regulation.

C)

technological inferiority.

D)

ownership of plentiful resources.

73.

An industry that is dominated by a few firms, each of which recognizes that its own

choices can affect the choices of its rivals and vice versa, is:

A)

a monopoly.

B)

an oligopoly.

C)

characterized by monopolistic competition.

D)

characterized by perfect competition.

74.

Oligopoly is a market structure that is characterized by a _____ number of _____ firms

producing _____ products.

A)

small; interdependent; identical or differentiated

B)

small; independent; identical or differentiated

C)

large; relatively small independent; differentiated

D)

large; relatively small independent; identical

Page 13

75.

To be called an oligopoly, an industry must have:

A)

independence in decision making.

B)

a horizontal demand curve.

C)

a small number of interdependent firms.

D)

relatively easy entry and exit.

76.

Oligopoly is a market structure characterized by:

A)

independence in decision making.

B)

interdependence: each firm’s decision affects the profit of the other firms.

C)

substantial diseconomies of scale.

D)

a large number of small firms.

77.

The market structure characterized by a few interdependent firms and barriers to entry is

called:

A)

monopolistic competition.

B)

perfect competition.

C)

oligopoly.

D)

monopoly.

78.

In oligopoly, a firm must realize that:

A)

what it does has no effect on the other firms in the industry.

B)

its behavior will be ignored by other firms in the industry.

C)

another major firm may dominate choices in the industry, and it will have to

behave accordingly.

D)

collusion was made legal in 2004.

79.

A firm that is in an oligopoly knows that its _____ affect its _____ and that the _____ of

its rivals will affect it.

A)

actions; rivals; reactions

B)

price changes; total revenue in a positive way; reactions

C)

actions rarely; rivals; actions

D)

price increases; total revenue in the long run only; large but not small price changes

80.

The market structure that is characterized by only a small number of producers is:

A)

oligopoly.

B)

perfect competition.

C)

monopoly.

D)

monopolistic competition.

Page 14

81.

Which scenarios best describes an oligopolistic industry?

A)

A single cable company serves customers in a small town.

B)

Thousands of soybean farmers sell their output in a global commodities market.

C)

Coca-Cola and Pepsi sell most of the soft drinks consumed around the world.

D)

A college has one bookstore selling textbooks to students.

82.

To calculate the Herfindahl-Hirschman index (HHI), one must _____ market share(s) of

_____ in the industry.

A)

sum the; the four largest firms

B)

sum the; all of the firms

C)

divide the; the largest firm by the sum of the four largest firms

D)

sum the squared; all of the firms

83.

An industry is dominated by a few firms. Each of these firms acknowledges that its own

choices affect the choices of its rivals. Each firm also recognizes that its rivals’ choices

affect the decisions it makes. This industry is an example of:

A)

a monopoly.

B)

an oligopoly.

C)

monopolistic competition.

D)

perfect competition.

84.

Oligopoly is a market structure that is characterized by a _____ number of _____ firms

that produce _____ products.

A)

large; relatively small and independent; identical

B)

small; independent; identical or differentiated

C)

large; relatively small and independent; differentiated

D)

small; interdependent; identical or differentiated

85.

An industry characterized by a few interdependent firms and by barriers to entry is

called:

A)

perfect competition.

B)

monopolistic competition.

C)

monopoly.

D)

oligopoly.

Page 15

86.

Large barriers to entry in the gas station business explain why the two only gas stations

in a small town:

A)

can earn an economic profit in the long run.

B)

must produce at the minimum average total cost in the long run.

C)

have no fixed costs in the long run.

D)

must produce a level of output such that MR = MC to maximize their profit.

87.

The term imperfect competition is used to refer to both oligopoly and monopolistic

competition.

A)

True

B)

False

88.

If the Baltimore furniture market had only a few sellers, it would be considered an

oligopoly.

A)

True

B)

False

89.

In the U.S. economy, oligopoly is rare.

A)

True

B)

False

90.

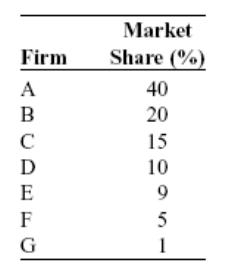

Suppose an industry is composed of seven producers with market shares given in the

table below.

A) Compute the Herfindahl–Hirschman index (HHI) for this market.

B) If firms B and C merge, how will this affect the HHI, all else being equal?

C) Instead, if firm A splits into two equal-sized competing firms, how would this affect

the HHI, all else being equal?

Support your answers with specific calculations. Do your results make sense?

Page 16

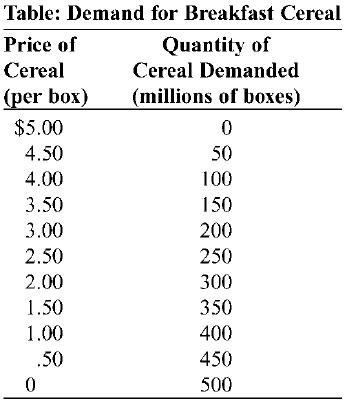

91.

(Table: Demand for Breakfast Cereal) Use Table: Demand for Breakfast Cereal.

Suppose that the marginal cost of producing cereal is zero.

A) If General Mills is the sole producer of breakfast cereal, how many boxes will the

firm produce, what price will be charged, and how much revenue will be earned?

B) Now assume that Kellogg enters the market, and the industry is now a duopoly with

two equal-sized firms. If these firms agree to split the monopoly output equally, how

much revenue will each firm earn under the agreement?

C) If General Mills can cheat on this agreement by producing 50 million more boxes

of cereal without punishment, will it? Analyze the price effect and quantity effect for

General Mills of producing 1 million more boxes.

92.

Oligopolies are industries:

A)

dominated by one seller who shares market power equally with all other sellers.

B)

made up of few firms, each with some market power and therefore aware of their

interdependence with the other firms.

C)

composed of many buyers and sellers, all of whom are price takers.

D)

that are the same as monopolistically competitive industries, except that they sell a

standardized product.

93.

An oligopoly may result from:

A)

increasing returns to scale.

B)

standardization of a product.

C)

low or no barriers to entry.

D)

price-taking conditions for both buyers and sellers.

Page 17

94.

If the Herfindahl-Hirschman index (HHI) for an industry is 300, the industry is

considered:

A)

unconcentrated.

B)

highly concentrated.

C)

oligopolistic.

D)

monopolistic.

95.

Suppose there are 10 identical firms in an industry and each produces 10% of the total

market sales. The HHI for this industry would indicate that the industry is:

A)

unconcentrated.

B)

monopolistic.

C)

oligopolistic.

D)

It cannot be determined from the information provided.

96.

An industry is made up of five firms. Three of the firms make up 20% of the total

market sales, one firm makes up 25%, and the remaining firm makes up 15%. What is

the HHI for this industry?

A)

100

B)

1,200

C)

2,050

D)

1,800

97.

If an industry initially has an HHI of 1,250, a merger between two of the largest (in

terms of market share) firms in the industry:

A)

automobile production

B)

fresh bagel shops

C)

corn farming

D)

electric utility production

98.

A monopolistically competitive industry, such as corn snack chips, and a perfectly

competitive industry, like wheat farming, are alike in that:

A)

firms in both types of industries produce identical products.

B)

firms in both types of industries produce similar but not identical products.

C)

barriers to entry in both industries are large.

D)

there are many firms in each industry.

Page 18

99.

Monopolistic competition is characterized by:

A)

free entry and exit in the long run.

B)

each firm producing a standardized product.

C)

few producers.

D)

barriers to entry.

100.

In monopolistic competition, each firm:

A)

is a price taker.

B)

has some ability to set the price of its differentiated good.

C)

will set price equal to marginal cost.

D)

has marginal revenue that is greater than price.

101.

The wedding dress industry is monopolistically competitive. As a result:

A)

thousands of dress suppliers all sell identical products.

B)

dresses tend to be differentiated among the many sellers serving this market.

C)

it has freedom of entry but not exit.

D)

prices tend to be lower than if the dress industry approximated perfect competition.

102.

Monopolistic competition is similar to perfect competition because firms in both market

structures:

A)

are price takers.

B)

produce goods that are perfect substitutes.

C)

find it beneficial to advertise.

D)

do not face any barriers to entry to the industry in the long run.

103.

In monopolistic competition:

A)

firms earn zero economic profits in the long run.

B)

each firm produces a product identical to that of every other firm in the industry.

C)

firms are aware of their strategic interdependence.

D)

firms earn large economic profits in the long run.

104.

For the monopolistically competitive wild-caught seafood market, the demand curve for

any individual firm is _____, and there are _____ producers of seafood.

A)

downward sloping; few

B)

upward sloping; many

C)

vertical; few

D)

downward sloping; many

Page 19

105.

The downward-sloping demand curve for a monopolistically competitive firm:

A)

reflects product differentiation.

B)

eventually will become perfectly elastic as more firms enter.

C)

indicates collusion among firms in the industry.

D)

ensures that the firm will produce at minimum average cost in the long run.

106.

An industry characterized by many firms producing similar but differentiated products

in a market with easy entry and exit is called:

A)

perfectly competitive.

B)

monopolistic.

C)

monopolistically competitive.

D)

oligopolistic.

107.

An example of monopolistic competition is the _____ industry.

A)

restaurant

B)

soft-drink

C)

automobile

D)

airline

108.

A(n) _____ market has a single firm and _____, whereas a(n) _____ market has _____

firm(s) and _____.

A)

oligopolistic; no barriers to entry; monopolistic; many; easy entry and exit

B)

monopolistic; barriers to entry; monopolistically competitive; many; easy entry and

exit

C)

monopolistic; barriers to entry; oligopolistic; few; no barriers to entry

D)

monopolistically competitive; barriers to entry; monopolistic; one; barriers to entry

109.

In large shopping malls, the retail clothing market is MOST illustrative of:

A)

monopolistic competition.

B)

monopoly.

C)

perfect competition.

D)

perfect oligopoly.

110.

An industry with a large number of relatively small firms producing differentiated

products in a market with easy entry and exit of firms is:

A)

a monopoly.

B)

a duopoly.

C)

an oligopoly.

D)

monopolistically competitive.

Page 20

111.

A monopolistically competitive industry is characterized by a _____ number of firms

producing _____ products with _____ entry.

A)

small; identical; barriers to

B)

small; similar; relatively easy

C)

large; similar; relatively easy

D)

large; identical; relatively easy

112.

Monopolistic competition is an industry structure characterized by:

A)

a product with no close substitutes.

B)

a horizontal demand curve.

C)

a large number of firms.

D)

barriers to entry and exit.

113.

Because most communities have a large number of similar but not identical substitutes,

the market for chiropractors is BEST considered to be:

A)

an oligopoly.

B)

perfect competition.

C)

monopolistically competitive.

D)

a monopoly.

114.

Because most communities have a large number of similar but not identical substitutes,

the market for financial planners is BEST considered to be:

A)

a monopoly.

B)

an oligopoly.

C)

perfect competition.

D)

monopolistically competitive.

115.

A feature of monopolistic competition that makes it different from monopoly is the:

A)

fact that firms in monopolistically competitive industries follow the marginal

decision rule, while monopolies do not.

B)

downward-sloping demand curve.

C)

downward-sloping marginal revenue curve.

D)

number of firms in the industry.

116.

An industry characterized by many competitors, each producing identical products, with

free entry and exit, is described as:

A)

monopolistically competitive.

B)

oligopolistic.

C)

perfectly competitive.

D)

monopolistic.

Page 21

117.

Which characteristic is NOT indicative of monopolistic competition?

A)

product differentiation

B)

a lack of barriers to entry and exit in the long run

C)

many competing producers

D)

tacit collusion

118.

Which feature is shared by monopolistic competition and perfect competition?

A)

few firms in the industry

B)

no barriers to entry or exit in the long run

C)

absolute market power

D)

standardized products

119.

A common example of monopolistic competition is the market for:

A)

mandarin oranges.

B)

cable TV service.

C)

automobiles.

D)

gasoline for cars.

120.

An industry with a large number of relatively small firms producing _____ products in a

market with easy entry and exit is a(n) _____.

A)

similar; monopoly

B)

identical; monopolistic competition

C)

differentiated; oligopoly

D)

differentiated; monopolistic competition

121.

Monopolistic competition describes an industry characterized by a _____ number of

firms producing _____ products with _____ entry.

A)

small; identical; barriers to

B)

small; similar; relatively easy

C)

large; similar; relatively easy

D)

large; identical; relatively easy

122.

The market for dentists in most communities can be considered _____ because the

market has a large number of similar but not identical dental services.

A)

monopolistic competition

B)

a monopoly

C)

perfect competition

D)

an oligopoly

Page 22

123.

Monopolistic competition describes an industry characterized by:

A)

a product with many close substitutes.

B)

a horizontal demand curve.

C)

a small number of firms.

D)

barriers to entry and exit.

124.

Monopolistic competition is different from monopoly because firms:

A)

have some power to set prices.

B)

have a downward-sloping demand curve.

C)

face some competition.

D)

have a downward-sloping marginal revenue curve.

125.

Because most communities have a large number of similar but not identical substitutes,

the market for florists is BEST considered to be:

A)

a monopoly.

B)

an oligopoly.

C)

monopolistically competitive.

D)

perfectly competitive.

126.

Monopolistic competition describes an industry characterized by:

A)

a product with no close substitutes.

B)

many firms, each with some market power.

C)

a small number of firms.

D)

barriers to entry and exit.

127.

An industry with easy entry and exit of a large number of small firms producing a

standardized product is:

A)

in perfect competition.

B)

in monopolistic competition.

C)

an oligopoly.

D)

a monopoly.

128.

Because of the lack of substitutes, the market for a newly developed and freshly

patented prescription drug is BEST considered to be:

A)

in perfect competition.

B)

in monopolistic competition.

C)

an oligopoly.

D)

a monopoly.

Page 23

129.

An industry with a few interdependent firms is BEST described as being:

A)

in perfect competition.

B)

in monopolistic competition.

C)

an oligopoly.

D)

a monopoly.

130.

The market for grade A large eggs in California is BEST considered to be an example

of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

131.

An industry with a single firm producing a product for which there are no close

substitutes and that is protected by barriers to entry is an example of:

A)

perfect competition.

B)

monopolistic competition.

C)

oligopoly.

D)

monopoly.

132.

The market for soft drinks, which is dominated by Coca Cola and Pepsi, is best

considered to be an example of:

A)

True

B)

False

C)

oligopoly.

D)

monopoly.

133.

The hamburger industry has some differentiation and many firms, suggesting that the

hamburger industry is more oligopolistic than it is monopolistically competitive.

A)

True

B)

False

134.

Gas stations are not monopolistically competitive because everyone knows the gasoline

is the same, regardless of where it is purchased.

A)

True

B)

False

Page 24

135.

Tacit collusion is not feasible in monopolistic competition because of the large number

of competing firms.

A)

True

B)

False

136.

Monopolistic competition shares some characteristics with perfect competition and

monopoly. Explain where these market structures are similar and where they differ.

137.

Industries that are made up of many competing producers, each selling a differentiated

product, and whose firms earn zero economic profits in the long run are:

A)

perfectly competitive.

B)

monopolies.

C)

oligopolies.

D)

monopolistically competitive.

Page 26

Page 27

Page 28