Chapter 22 The Firm: Cost and Output Determination 371

113) In the above table, what is the average total cost to produce 3 units of output?

A) $33.33 B) $53.33 C) $55 D) $20

114) Which of the following statements regarding the relationship between average and marginal

costs is INCORRECT?

A) There is always a definite relationship between average and marginal cost.

B) When marginal costs are less than average costs, the latter must fall.

C) When marginal costs are greater than average costs, the latter must rise.

D) There is no way for average variable costs to fall when marginal costs are falling.

115) Assume that in the short run a firm is producing 100 units of output, has average total costs of

$100, and average variable costs of $50. The firm stotal fixed costs are

A) $50. B) $5,000. C) $150. D) $15,000.

116) Assume that in the short run a firm is producing 100 units of output, has average total costs of

$100, and average fixed costs of $20. The firm stotal variable cost at this output level is

A) $120. B) $80. C) $8,000. D) $12,000.

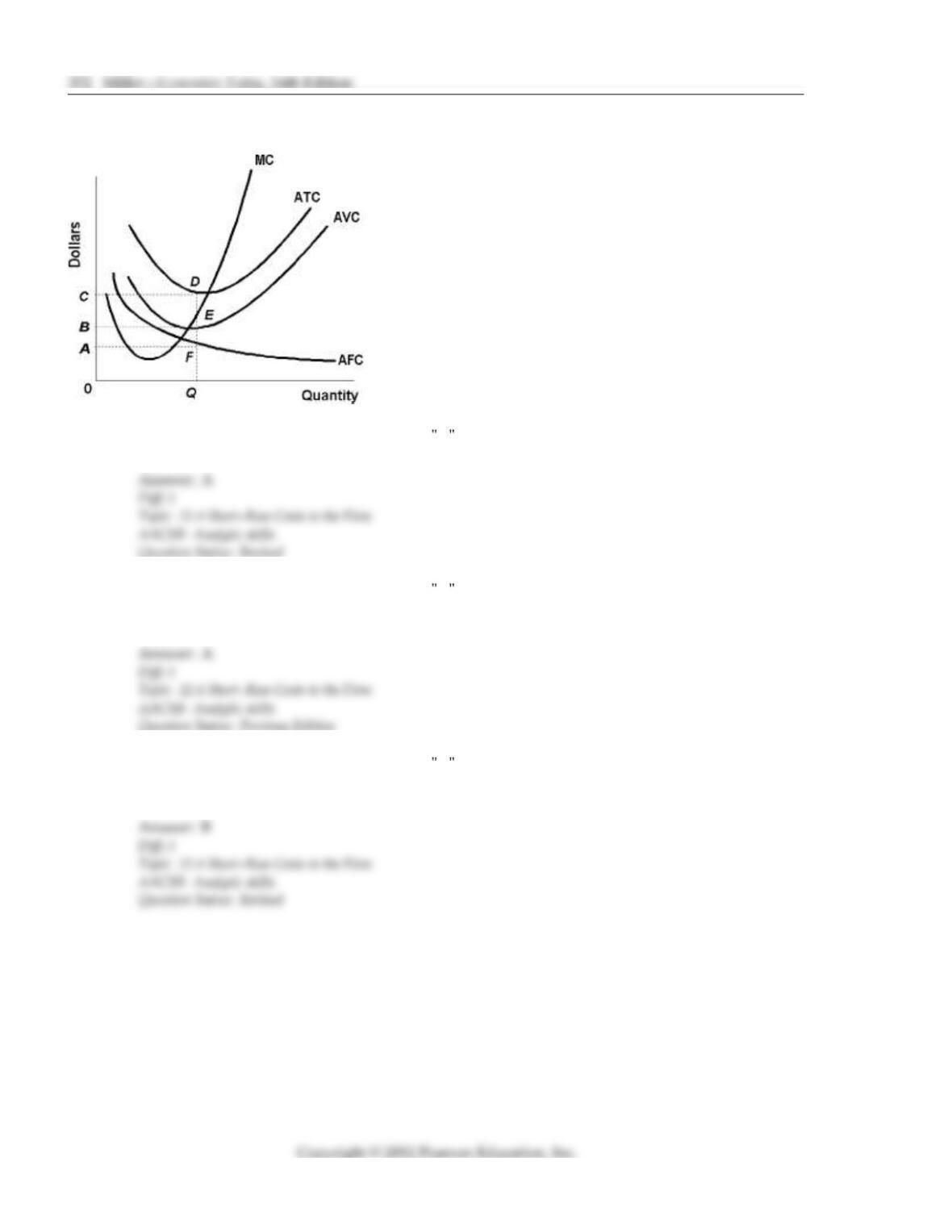

117) Use the above figure. At an output equal to Q the total cost for the firm will be the area

A) OQDC. B) OQFA. C) OQBC. D) OQEB.

118) Use the above figure. At an output equal to Q the average fixed cost for the firm will be the

line segment

A) DE. B) AB. C) BE. D) CD.

119) Use the above figure. At an output equal to Q the total variable cost for the firm will be the

area

A) OQAB. B) OQEB. C) OQFA. D) OQDC.

120) In the table below, what are the marginal costs of the fourth unit of output?

Total Total

Output Variable Cost

0 $0

1 $10,000

2 $20,000

3 $30,000

4 $40,000

A) $10,000 B) $20,000 C) $30,000 D) $40,000

121) Which of the following is true?

A) The MC curve intersects AFC at its minimum point.

B) If MC is below AVC, AVC must be increasing.

C) If MC is above ATC, ATC must be increasing.

D) None of the above.

122) If average total cost is decreasing as more and more units are produced, then marginal cost must

be

A) rising. B) constant.

C)

b

elow average total cost. D) negative.

123) What is the difference between average variable costs and average total costs?

124) What are the relationships between the marginal cost curve and the average cost curves?

Explain in words.

125) All average costs have a U shaped curve. Do you agree or disagree? Explain why?

22.5 The Relationship Between Diminishing Marginal Product and Cost Curves

1) Marginal cost begins to rise when

A) diminishing marginal product begins. B) diminishing marginal product ends.

C) average total cost falls. D) fixed cost falls.

2) At the output rate at which diminishing marginal product begins, a firm will experience

A) constant average total costs. B) increasing average fixed costs.

C) increasing marginal costs. D) decreasing average variable costs.

3) Which of the following statements is correct?

A) Average variable costs always exceed average total costs.

B) Average fixed costs are constant.

C) Average variable cost reaches its minimum when average product equals its maximum.

D) Average fixed costs are always less than average variable costs.

4) If the marginal product of an input is falling, then

A) average fixed cost is constant. B) marginal cost is falling.

C) average total cost is constant. D) marginal cost is rising.

5) When marginal product is rising,

A) total product is falling. B) marginal cost is falling.

C) marginal cost is rising. D) average fixed cost is rising.

6) The shape of the short run average total cost curve is a result of

A) economies of scale.

B) diseconomies of scale.

C) the law of diminishing marginal product.

D) falling profits.

7) As a firm s production increases in the short run, the average total cost curve eventually slopes

upward because

A) marginal physical product eventually declines as output increases.

B) marginal cost eventually declines as output increases.

C) average fixed cost declines with increases in output.

D) average physical product rises with increases in output.

8) The law of diminishing marginal product is NOT responsible for the shape of

A) the total cost curve. B) the average variable cost curve.

C) total fixed cost curve. D) marginal cost curve.

9) When the marginal physical product is rising,

A) total cost is falling. B) average total cost is increasing.

C) marginal cost is falling. D) marginal cost is rising.

10) When the marginal physical product is falling,

A) marginal cost is rising. B) average fixed costs are rising.

C) total costs are falling. D) average variable costs are falling.

11) When the average physical product is rising,

A) total cost is falling. B) average total cost is increasing.

C) average variable cost is falling. D) marginal cost is always rising.

12) When the average physical product is falling,

A) average variable costs are rising. B) average fixed costs are rising.

C) total costs are falling. D) average variable costs are falling.

13) Marginal costs will begin to rise at the point where

A) fixed costs increase. B) variable costs increase.

C) average variable costs increase. D) diminishing marginal product begins.

Chapter 22 The Firm: Cost and Output Determination 37

7

Quantity of Total Average Marginal

Labor Product Product Product

1 22 22 22

2 52 26 30

3 81 27 29

4 100 25 19

5 115 23 15

6 126 21 11

14) Refer to the above table. At what quantity of labor does the marginal cost curve start to

increase?

A) After 1 unit B) After 2 units C) After 3 units D) After 6 units

15) Refer to the above table. At what quantity of labor does the average variable cost curve start to

increase?

A) After 1 unit B) After 2 units C) After 3 units D) After 6 units

16) Marginal physical product of labor equals

A) the wage. B) the wage divided by marginal cost.

C) marginal cost divided by the wage. D) marginal cost times the wage.

17) Short run cost relationships for a firm are

A) determined by the law of diminishing marginal product.

B) determined by the specific long run relationships that exist.

C) due to the level of wages relative to other input prices.

D) due to the normal contractual relations in a market.

18) If the marginal product curve is intersecting the average product curve, we know that

A) the average variable cost curve is intersecting the average total cost curve.

B) the marginal cost curve is intersecting the average fixed cost curve.

C) the average total cost curve lies above the marginal cost curve.

D) the marginal cost curve is intersecting the average total cost curve.

19) When marginal costs are rising,

A) marginal physical product is also rising. B) marginal physical product is falling.

C) average physical product is rising. D) average physical product is falling.

20) When average variable costs are rising,

A) marginal physical product is also rising. B) marginal costs is falling.

C) average physical product is rising. D) average physical product is falling.

21) What happens to the marginal cost curve when the marginal physical product of labor is rising?

A) It becomes upward sloping. B) It becomes vertical.

C) It becomes downward sloping. D) It becomes horizontal.

22) The typical cost curves are U shaped due to the

A) law of diminishing marginal utility. B) law of supply.

C) law of demand. D) law of diminishing marginal product.

23) If the price of labor is constant and a firm experiences diminishing marginal product, then its

A) marginal costs increase. B) marginal costs decrease.

C) fixed costs increase. D) total costs decrease.

24) If the price of labor is constant and a firm experiences diminishing marginal product, then its

A) marginal costs decrease. B) fixed costs increase.

C) average variable cost increases. D) total costs decrease.

25) What is the relationship between the marginal cost curve and marginal product? Explain.

26) What is the most important determinant of the firm s short run cost curves?

27) What is the relationship between marginal cost and marginal physical product?

380 Miller Economics Today, 16th Edition

22.6 Long Run Cost Curves

1) In economics, the planning horizon is defined as

A) 10 years for every firm.

B) the longest time period over which the firm can make decisions.

C) the period of time for which technology is fixed.

D) the long run, during which all inputs are variable.

2) The minimum possible short run average costs are equal to long run average costs when

A) the plant is producing at its short run minimum point.

B) short run and long run costs are declining.

C) the long run curve is at a minimum point.

D) production is at any point on the LAC curve.

3) The long run average cost curve

A) is always a downward sloping straight line.

B) is a curve which is tangent to each member of a set of short run average cost curves.

C) is identical to the marginal cost curve.

D) should always be horizontal.

4) A firm s long run average cost curve is

A) the locus of points representing the minimum unit cost of producing any given rate of

output when all inputs may be adjusted.

B) the locus of points made up of the minimum point on each short run average total cost

curve when only one input may be adjusted.

C) the envelope of the firm s variable cost curves.

D) identical to the lowest short run average cost curve the firm has.

5) The long run is

A) over one year.

B) over five years.

C) when all factors of production are fixed.

D) the time period in which all factors of production can be varied.

6) Which of the following is TRUE for a firm in the long run?

A) Variable costs will initially increase and then decrease.

B) The law of diminishing marginal product holds.

C) All costs are variable costs.

D) Variable costs will equal marginal cost at all output levels.

7) The planning horizon is the

A) long run.

B) short run.

C) point where production begins.

D) point where diminishing marginal product starts.

8) Which of the following statements is true about the planning horizon?

A) All inputs are fixed. B) All inputs are variable.

C) There are fixed and variable inputs. D) Costs do not exist.

9) Every point on the long run average cost curve is

A) also a minimum point on a short run average cost curve.

B) on a short run average total cost curve.

C) on a short run average variable cost curve.

D) on a short run marginal cost curve.

10) The locus of points representing the minimum unit cost of producing any given rate of output is

the

A) short run average total cost curve. B) long run marginal cost curve.

C) short run total cost curve. D) long run average cost curve.

11) The long run for a business is a period of time

A) longer than a year.

B) when most inputs are variable.

C) when all inputs can change.

D) when labor is the only input used by the business.

12) The long run is defined as a time period during which full adjustment can be made to any

change in the economic environment. Thus in the long run, all factors of production are

variable. Long run curves are sometimes called planning curves, and the long run is sometimes

called the

A) foreseeable future. B) minimum efficient time period.

C) non adjustment period. D) planning horizon.

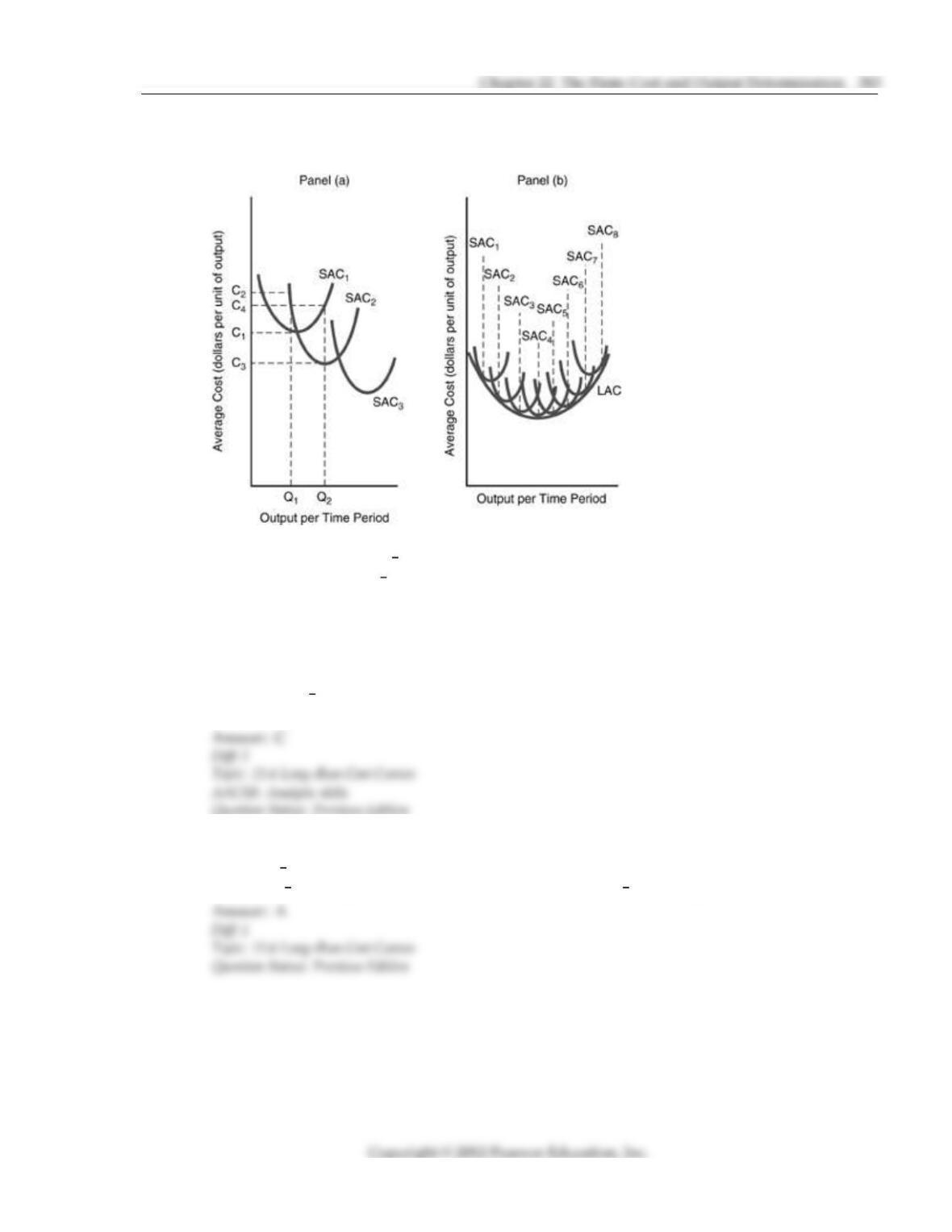

13) Which of the following statements with respect to the figure below is INCORRECT?

A) All the possible short run average cost curves that correspond to the different plant sizes

are shown as SAC1SAC8.

B) If the anticipated permanent rate of output per unit time period is Q1in panel (a), the

optimal plant would correspond to SAC1.

C) If the permanent rate of output increases to Q2in panel (a), it will be more profitable to

have a plant size corresponding to SAC3.

D) The long run average cost curve LAC in panel (b) is sometimes called the planning curve

representing the locus (path) of points.

14) The planning curve is the

A) long run average cost curve. B) production function.

C) short run marginal cost curve. D) short run average cost curve.

15) Explain how the long run average cost curve is constructed graphically.

16) How is the long run average cost curve found? What is its importance to the firm?

17) The long run average cost curve is derived from adding all short run average cost curves

together. Do you agree or disagree? Explain.

22.7 Why the Long Run Average Cost Curve Is U Shaped

1) Which of the following is NOT one of the reasons a firm might be expected to experience

economies of scale?

A) specialization B) the dimensional factor

C) improved productive equipment D) depreciation

2) Due to extremely large fixed costs, an electricity generating plant probably experiences which of

the following returns to size?

A) diseconomies of scale B) diminishing marginal product

C) constant returns to scale D) economies of scale

3) If a firm gets so large that management of employees and other resources becomes a costly

problem, it will be experiencing

A) diseconomies of scale. B) diminishing marginal product.

C) constant returns to scale. D) economies of scale.

4) Suppose a firm doubles its output in the long run. At the same time the unit cost of production

remains unchanged. We can conclude that the firm is

A) exploiting the economies of scale available to it.

B) facing constant returns to scale.

C) facing diseconomies of scale.

D) not using the available technology efficiently.

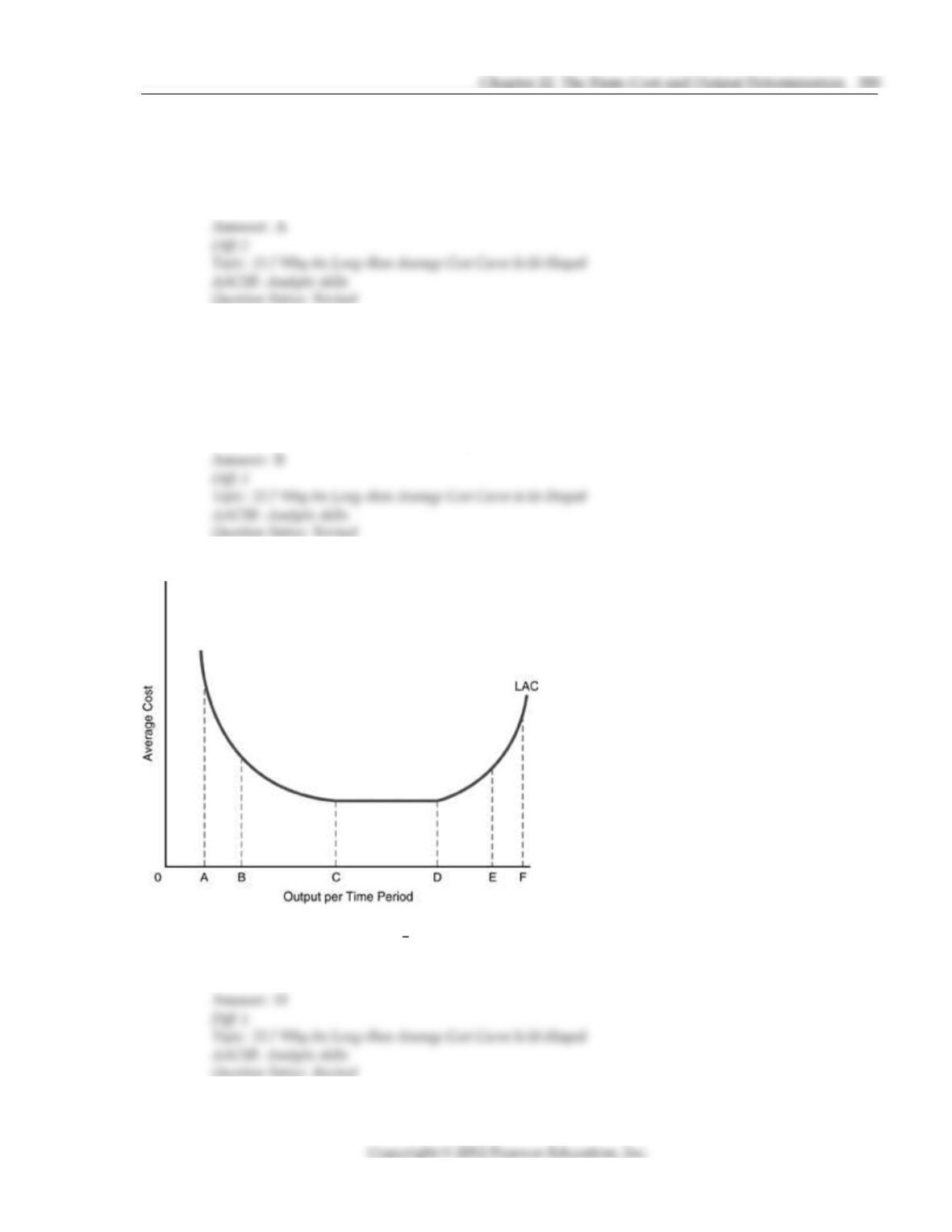

5) In the above figure, the long run cost curve between points A and B illustrates

A) diseconomies of scale. B) diminishing marginal product.

C) constant returns to scale. D) economies of scale.