Page 1

1.

The long-run average total cost curve is tangent to an infinite number of short-run _____

cost curves.

A)

total

B)

marginal

C)

average variable

D)

average total

2.

Where the long-run average total cost curve is at its lowest point, it is tangent to the

_____ of the corresponding short-run average total cost curve.

A)

minimum

B)

maximum

C)

right of the minimum

D)

left of the minimum

3.

At quantities less than the long-run minimum cost per unit of output, the long-run

average total cost curve is _____ of the corresponding short-run average total cost

curve.

A)

tangent to the minimum

B)

tangent to the maximum

C)

to the right of the minimum

D)

to the left of the minimum

4.

At quantities greater than the long-run minimum cost per unit of output, the long-run

average total cost curve is _____ of the corresponding short-run average total cost

curve.

A)

tangent to the minimum

B)

tangent to the maximum

C)

to the right of the minimum

D)

to the left of the minimum

5.

(Figure: Long-Run and Short-Run Average Cost Curves) Use Figure: Long-Run and

Short-Run Average Cost Curves. If a firm faced the long-run average total cost curve

shown in the figure and it expected to produce 100,000 units of the good in the long run,

the firm should build the plant associated with:

Ref 11-18 Figure: Long-Run and Short-Run Average Cost Curves

A)

ATC1.

B)

ATC2.

C)

ATC3.

D)

ATC1 or ATC2.

Page 2

6.

(Figure: Long-Run and Short-Run Average Cost Curves) Use Figure: Long-Run and

Short-Run Average Cost Curves. If a firm is producing at point C on the ATC2 but

anticipates increasing output to 225,000 units in the long run, the firm will build a

_____ plant and have _____ of scale.

A)

smaller; economies

B)

smaller; diseconomies

C)

bigger; economies

D)

bigger; diseconomies

7.

In the long run, all costs are:

A)

fixed.

B)

constant.

C)

variable.

D)

marginal.

8.

In the long run:

A)

all factors are fixed.

B)

all factors are variable.

C)

production choices are more limited than in the short run.

D)

production is always greater than zero.

9.

When a firm adds physical capital, in the short run fixed costs will:

A)

increase.

B)

decrease.

C)

remain the same.

D)

decrease at first and then increase.

10.

When a firm adds capital, in the short run workers will be:

A)

less productive and let the machines do most of the work.

B)

more productive, since they have more equipment.

C)

at the same level of productivity.

D)

more productive at first and then less productive after a few weeks.

11.

When a firm adds capital, in the short run variable costs for any level of output will:

A)

increase.

B)

decrease.

C)

remain the same.

D)

increase at first and then decrease.

Page 3

Use the following to answer questions 12-38:

12.

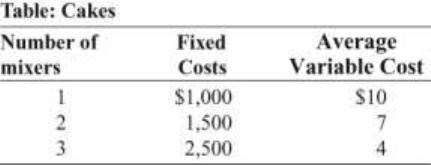

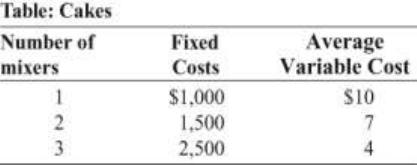

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 100 cakes per day, what is her average fixed cost?

A)

$10,000

B)

$1,000

C)

$15

D)

$10

13.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 100 cakes per day, what is her average total cost?

A)

$1,010

B)

$20

C)

$15

D)

$10

14.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 200 cakes per day, what is her average fixed cost?

A)

$5

B)

$10

C)

$200

D)

$1,000

Page 4

15.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 200 cakes per day, what is her average total cost?

A)

$5

B)

$15

C)

$200

D)

$1,000

16.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.025

B)

$2.50

C)

$1,000

D)

$400,000

17.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer and bakes 400 cakes per day, what is her average total cost?

A)

$2.50

B)

$10

C)

$12.50

D)

$1,010

18.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 5

19.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 1 mixer, her average total cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

20.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 100 cakes per day, what is her average fixed cost?

A)

$10,000

B)

$1,000

C)

$15

D)

$10

21.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 100 cakes per day, what is her average total cost?

A)

$8

B)

$10

C)

$15

D)

$22

22.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 200 cakes per day, what is her average fixed cost?

A)

$300,000

B)

$1,508

C)

$187.50

D)

$7.50

Page 6

23.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 200 cakes per day, what is her average total cost?

A)

$8

B)

$14.50

C)

$1,492

D)

$1,508

24.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.02

B)

$3.75

C)

$500

D)

$1,508

25.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers and bakes 400 cakes per day, what is her average total cost?

A)

$0.02

B)

$10.75

C)

$500

D)

$1,507

26.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 7

27.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 2 mixers, her average total cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

28.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 100 cakes per day, what is her average fixed cost?

A)

$4

B)

$25

C)

$2,496

D)

$10,000

29.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 100 cakes per day, what is her average total cost?

A)

$4

B)

$25

C)

$29

D)

$625

30.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 200 cakes per day, what is her average fixed cost?

A)

$0.05

B)

$2.50

C)

$5.00

D)

$12.50

Page 8

31.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 200 cakes per day, what is her average total cost?

A)

$50.00

B)

$12.50

C)

$16.50

D)

$800.00

32.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 400 cakes per day, what is her average fixed cost?

A)

$0.05

B)

$2.50

C)

$5.00

D)

$6.25

33.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers and bakes 400 cakes per day, what is her average total cost?

A)

$10.25

B)

$12.50

C)

$16.50

D)

$2,504.00

34.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers, her average fixed cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

Page 9

35.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

If Pat purchases 3 mixers, her average total cost _____ in the range of output between

100 and 400 cakes.

A)

increases

B)

decreases

C)

remains the same

D)

can’t be calculated

36.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

How many mixers should Pat buy to get the lowest average total cost if she plans to

make 100 cakes?

A)

1

B)

2

C)

3

D)

Can’t be determined without more information

37.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

How many mixers should Pat buy to get the lowest average total cost if she plans to

make 200 cakes?

A)

1

B)

2

C)

3

D)

Can’t be determined without more information

Page 10

38.

(Ref. 22-1 Table: Cakes) Use Table 22-1: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. She is trying to decide how many mixers to purchase. Her

estimated fixed and average variable costs if she purchases 1, 2, or 3 mixers are shown

in the table. Assume that average variable costs do not vary with the quantity of output.

How many mixers should Pat buy to get the lowest average total cost if she plans to

make 400 cakes?

A)

1

B)

2

C)

3

D)

Can’t be determined without more information

39.

The long-run average cost curve will be upward-sloping when the firm has:

A)

economies of scale.

B)

diseconomies of scale.

C)

constant returns to scale.

D)

diminishing returns.

Use the following to answer question 40:

40.

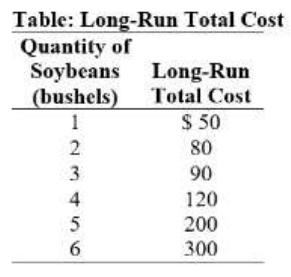

(Ref 22-2 Table: Long-Run Total Cost) Use Table 22-2: Long-Run Total Cost. This

soybean grower receives constant returns to scale over the _____ and _____ bushels.

A)

first; second

B)

third; fourth

C)

fourth; fifth

D)

fifth; sixth

Page 11

41.

When an increase in the firm’s output reduces its long-run average total cost, it achieves

_____ scale.

A)

economies of

B)

diseconomies of

C)

constant returns to

D)

variable returns to

42.

A university that benefits from lower costs per enrolled student as it builds more

buildings and enrolls more students is an example of a service provider with:

A)

economies of scale.

B)

diseconomies of scale.

C)

increasing opportunity costs.

D)

scale reduction.

43.

The slope of a long-run average total cost curve exhibiting diseconomies of scale is:

A)

zero.

B)

infinite.

C)

positive.

D)

negative.

44.

When diseconomies of scale occur:

A)

long-run average cost rises.

B)

marginal cost declines.

C)

average total cost declines.

D)

average variable cost declines.

Use the following to answer questions 45-49:

Page 12

45.

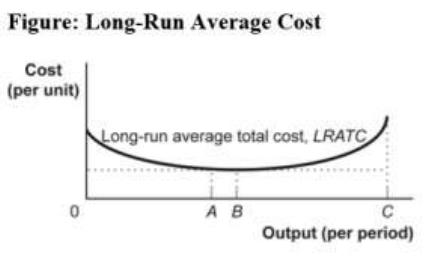

(Ref. 22-3 Figure: Long-Run Average Cost) Use Figure 22-3: Long-Run Average Cost.

This firm has _____ in the output region from 0 to A.

A)

diseconomies of scale

B)

constant returns to scale

C)

economies of scale

D)

negative costs of production

46.

(Ref. 22-3 Figure: Long-Run Average Cost) Use Figure 22-3: Long-Run Average Cost.

This firm has _____ in the output region from A to B.

A)

constant returns to scale

B)

economies of scale

C)

diseconomies of scale

D)

constant total cost as output increases

47.

(Ref. 22-3 Figure: Long-Run Average Cost) Use Figure 22-3: Long-Run Average Cost.

This firm has _____ in the output region from B to C.

A)

constant returns to scale

B)

diseconomies of scale

C)

economies of scale

D)

falling marginal cost

48.

(Ref. 22-3 Figure: Long-Run Average Cost) Use Figure 22-3: Long-Run Average Cost.

This firm has _____ in the output region from 0 to A.

A)

decreasing returns to scale

B)

constant returns to scale

C)

increasing returns to scale

D)

negative costs of production

49.

(Ref. 22-3 Figure: Long-Run Average Cost) Use Figure 22-3: Long-Run Average Cost.

This firm has _____ in the output region from B to C.

A)

constant returns to scale

B)

decreasing returns to scale

C)

increasing returns to scale

D)

falling marginal cost

Page 13

50.

A firm that is able to use its inputs more efficiently as it increases production in the long

run best demonstrates:

A)

economies of scale.

B)

diseconomies of scale.

C)

labor-intensive production.

D)

capital-intensive production.

51.

A firm that has diminishing returns in the management’s ability to use and disseminate

information as it increases production in the long run BEST demonstrates:

A)

economies of scale.

B)

diseconomies of scale.

C)

being too small for the relevant market.

D)

not having enough managers.

52.

It is common in large breweries for the long-run average total cost to decline as output

increases. This indicates that many breweries operate with:

A)

diseconomies of scale.

B)

diminishing marginal returns.

C)

economies of scale.

D)

constant returns to scale.

53.

Buffalo Aircraft doubles the amount of all of the inputs it uses – the factory doubles in

size and twice as many workers are hired. After this expansion, the number of aircraft

produced triples. If the price of inputs is unchanged, this means that Buffalo Aircraft is

operating with:

A)

increasing marginal cost.

B)

economies of scale.

C)

increasing average total cost.

D)

decreasing average variable cost.

54.

The long-run average total cost of producing 100 units of output is $4, while the

long-run average cost of producing 110 units of output is $4. These numbers suggest

that between 100 and 110 units of output, the firm producing this output has:

A)

economies of scale.

B)

diseconomies of scale.

C)

constant returns to scale.

D)

diminishing returns.

Page 14

55.

The -shape of the long-run average total cost curve is primarily due to:

A)

technological change.

B)

economies and diseconomies of scale.

C)

fixed costs.

D)

diminishing returns.

56.

When an increase in the firm’s output reduces its long-run average total cost, it has

_____ returns to scale.

A)

increasing

B)

decreasing

C)

constant

D)

variable

57.

If your firm is operating in the negatively sloped portion of a long-run average total cost

curve, then your production exhibits:

A)

higher wages.

B)

increasing returns to scale.

C)

decreasing returns to scale.

D)

increased input prices.

58.

A manufacturing company that benefits from lower costs per unit as it grows is an

example of a firm exhibiting:

A)

increasing returns to scale.

B)

decreasing returns to scale.

C)

increasing opportunity costs.

D)

scale reduction.

59.

A firm that has lower costs per unit as it increases production in the long run has:

A)

increasing returns to scale.

B)

decreasing returns to scale.

C)

increasing opportunity costs.

D)

scale reduction.

60.

The slope of a long-run average total cost curve exhibiting decreasing returns to scale is:

A)

zero.

B)

infinite.

C)

positive.

D)

negative.

Page 15

61.

Decreasing and increasing returns to scale account for the shape of the:

A)

short-run average total cost curve.

B)

short-run average variable cost curve.

C)

long-run average total cost curve.

D)

marginal cost curve in both the short run and the long run.

62.

The slope of a long-run average total cost curve exhibiting increasing returns to scale is:

A)

zero.

B)

infinite.

C)

positive.

D)

negative.

63.

In some complex production processes, such as nuclear power plants, some inputs have

to be treated as being fixed even in the long run.

A)

True

B)

False

64.

In the long run, some of a firm’s costs are fixed, while others are variable.

A)

True

B)

False

65.

Firms choose their level of fixed cost in the long run based on the amount of output that

they expect to produce.

A)

True

B)

False

66.

When a firm adds physical capital, its fixed cost will decrease in the short run.

A)

True

B)

False

67.

When a firm adds physical capital, labor will become more productive in the short run.

A)

True

B)

False

68.

When a firm adds physical capital, its variable cost will decrease in the long run.

A)

True

B)

False

Page 16

69.

The long run is the period during which fixed costs do not change.

A)

True

B)

False

70.

In the long run, when a firm adds physical capital, workers become more productive, so

variable costs increase.

A)

True

B)

False

71.

The long-run average total cost curve shows the relationship between output and the

average total cost when fixed cost has been chosen to minimize average total cost for

each level of output.

A)

True

B)

False

72.

The long-run average total cost curve shows the relationship between output and the

average total cost when variable cost has been chosen to minimize average total cost for

each level of output.

A)

True

B)

False

73.

A firm always operates at some point on its long-run average total cost curve in both the

long run and the short run.

A)

True

B)

False

74.

If output increases, a firm will move along its short-run average total cost curve in the

short run until it has time to adjust its fixed cost.

A)

True

B)

False

75.

The long-run average cost curve is tangent to a series of short-run average fixed cost

curves.

A)

True

B)

False

Page 17

76.

The long-run average cost curve is tangent to a series of short-run average total cost

curves.

A)

True

B)

False

77.

If a firm has to increase output suddenly to meet an increase in demand, its average total

cost will increase in the short run until it has time to add physical capital.

A)

True

B)

False

78.

If a firm has to increase output suddenly to meet an increase in demand, its average total

cost will decrease in the short run until it has time to add physical capital.

A)

True

B)

False

79.

When a firm has to increase its output, average total costs will increase in the short run

and then decrease in the long run, after the firm has time to add physical capital.

A)

True

B)

False

80.

When a firm has to increase its output, average total costs will decrease in the short run

and then increase in the long run after the firm has time to add physical capital.

A)

True

B)

False

81.

Scale is the size of a firm’s operations.

A)

True

B)

False

82.

When the long-run average total cost curve is downward-sloping as output increases, the

firm has diseconomies of scale.

A)

True

B)

False

83.

When long-run average total cost is constant as output increases, the firm has constant

returns to scale.

A)

True

B)

False

Page 18

84.

When the long-run average total cost curve is upward sloping as output increases, the

firm has diseconomies of scale.

A)

True

B)

False

85.

Economies of scale are often the result of increased specialization, which can occur

when output levels increase.

A)

True

B)

False

86.

Economies of scale most often occur in industries whose initial fixed cost of plant and

equipment is low.

A)

True

B)

False

87.

A production function that is characterized by economies of scale will not be subject to

diminishing returns.

A)

True

B)

False

88.

Diminishing returns are one explanation for diseconomies of scale.

A)

True

B)

False

89.

If a firm builds a larger plant and increases output and if its long-run average total cost

does not change, the firm has constant returns to scale.

A)

True

B)

False

90.

The advantage of specialization in production is one of the primary reasons for

decreasing returns to scale.

A)

True

B)

False

Page 19

Use the following to answer questions 91-93:

91.

(Ref. 22-4 Table: Cakes) Use Table 22-4: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. Her estimated fixed and average variable costs if she

purchases 1, 2, or 3 mixers are shown in the table. Assume that average variable costs

do not vary with the quantity of output. Suppose that Pat is producing 100 cakes with 1

mixer, but she has a sudden increase in demand, so she begins to produce 200 cakes.

Explain how her average total cost will change in the short run and in the long run.

92.

(Ref. 22-4 Table: Cakes) Use Table 22-4: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. Her estimated fixed and average variable costs if she

purchases 1, 2, or 3 mixers are shown in the table. Assume that average variable costs

do not vary with the quantity of output. Suppose that Pat is producing 200 cakes with

two mixers, but she has a sudden increase in demand, so she begins to produce 400

cakes. Explain how her average total cost will change in the short run and in the long

run.

93.

(Ref. 22-4 Table: Cakes) Use Table 22-4: Cakes. Pat is opening a bakery to make and

sell special birthday cakes. Her estimated fixed and average variable costs if she

purchases 1, 2, or 3 mixers are shown in the table. Assume that average variable costs

do not vary with the quantity of output. Suppose that Pat is producing 100 cakes with 1

mixer, but she has a sudden increase in demand, so she begins to produce 200 cakes.

Explain how her average total cost will change in the short run and in the long run.

94.

What are some factors that contribute to a firm achieving increasing returns to scale (or

economies of scale) in the long run?

Page 20

95.

The curve that illustrates the relationship between output and average total cost when

the fixed cost has been chosen to minimize average total cost for each level of output is

the _____ curve.

A)

short-run average total cost

B)

long-run average total cost

C)

marginal cost

D)

total product

96.

When all of a firm’s inputs are doubled, input prices do not change, and this results in

the firm’s level of production more than doubling, a firm is operating:

A)

on the upward-sloping portion of its long-run average total cost curve.

B)

on the downward-sloping portion of its long-run average total cost curve.

C)

at the minimum of its long-run average total cost curve.

D)

on the upward-sloping portion of its marginal cost curve.

97.

A firm’s long-run average total costs increase as it produces more output. This firm has:

A)

economies of scale.

B)

constant returns to scale.

C)

diseconomies of scale.

D)

a spreading effect.

98.

Economies and diseconomies of scale are associated with the:

A)

long-run average total cost curve and the long run.

B)

short-run average total cost curve and the short run.

C)

marginal cost curve and both the long and short run.

D)

average fixed cost curve and the short run.

Page 22

Page 23