60) Jimmy’s utility of wealth schedule is given in the table above. Jimmy has a job with a one-

third chance of earning $200 and a two-thirds chance of earnings $400. Jimmy’s cost of risk is

A) $0.

B) $16.67.

C) $33.33.

D) Jimmy’s cost of risk cannot be determined without more information.

61) George is considering investing in a frozen yogurt store. If the store does well he will make

$20,0000, but if the store does poorly he will make only $10,000. There is a 50 percent chance of

each outcome. His utility of wealth schedule is in the above table. The expected utility of this

investment is

A) 115.

B) 140.

C) 165.

D) 180.

62) Based on the table and information in the previous question, which of the following is

TRUE?

A) George prefers to make $15,000 with certainty than make the investment.

B) George prefers making the investment than to make $15,000 with certainty.

C) George is indifferent between making $15,000 with certainty and making the investment.

D) As the investment has risk George should not make it under any circumstances.

Income

(dollars)

Total

utility

0

0

100

100

200

150

300

175

400

190

500

198

600

200

63) James has a utility of wealth schedule in the above table. He is offered a job selling video

games at Games Galore. James’ compensation depends on how much he sells. In a poor sales

period, a salesperson makes $100 per month. In a good sales period, a salesperson makes $600

per month. James is told by the manager that, in any given month, there is a 25 percent chance of

a poor sales period and a 75 percent chance of a good sales period. Suppose that one of James’

professors offers him the opportunity to be a research assistant for a fixed and guaranteed

amount each month. What amount must James’ professor pay in order to make James indifferent

between being a research assistant and working at Games Galore?

A) $300 per month

B) $350 per month

C) $475 per month

D) $600 per month

64) James has a utility of wealth schedule in the above table. He is offered a job selling video

games at Games Galore. James’ compensation depends on how much he sells. In a poor sales

period, a salesperson makes $100 per month. In a good sales period, a salesperson makes $600

per month. James is told by the manager that, in any given month, there is a 25 percent chance of

a poor sales period and a 75 percent chance of a good sales period. Suppose that one of James’

professors offers him the opportunity to be a research assistant for a fixed and guaranteed

amount each month. Comparing the two opportunities, working at Games Galore versus being a

research assistant, what is James’ cost of risk?

A) $125 per month

B) $175 per month

C) $375 per month

D) $500 per month

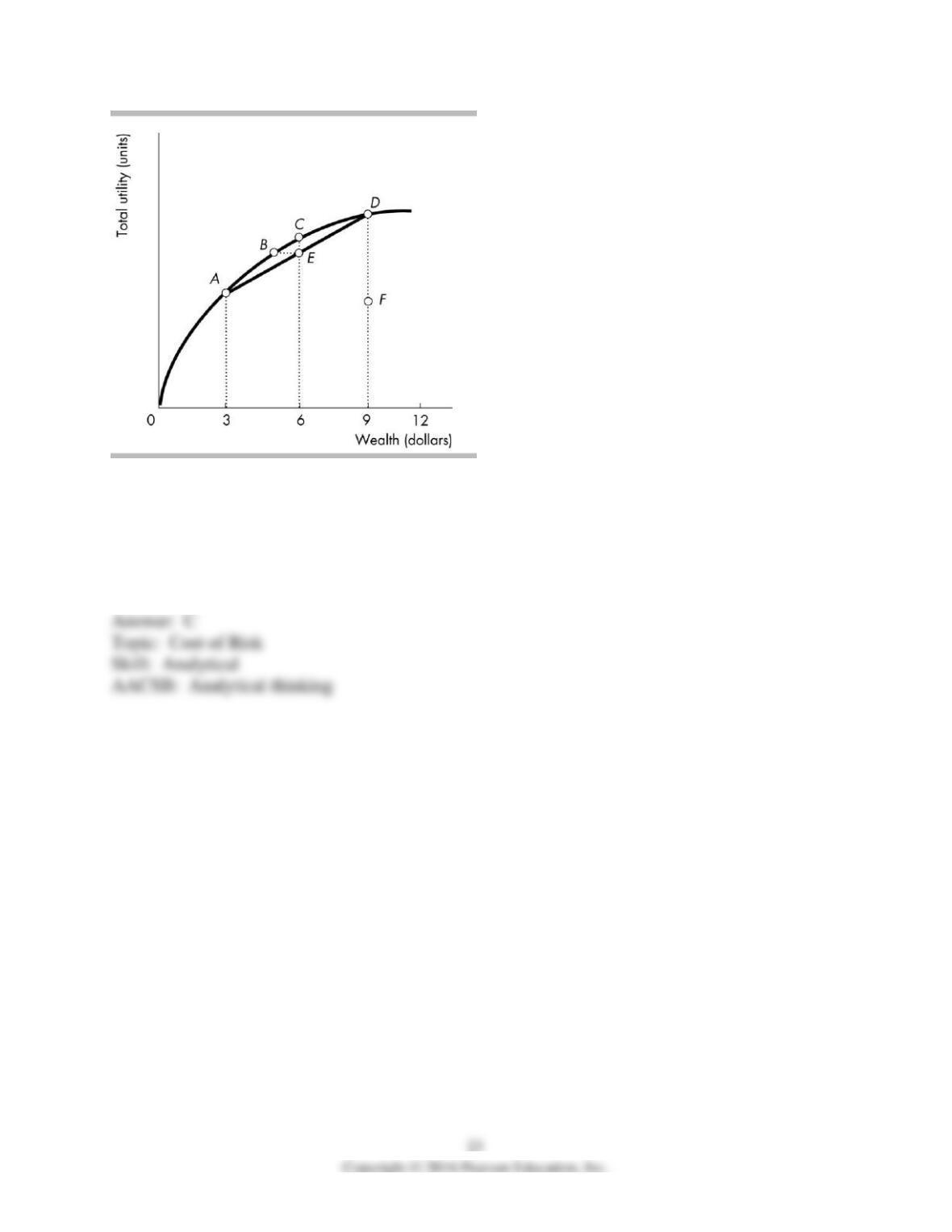

65) In the figure above, Lourdita faces a 0.5 probability of receiving $3,000 and a 0.5 probability

of receiving $9,000. Her cost of bearing this risk is the distance from

A) A to F.

B) A to D.

C) B to E.

D) C to E.

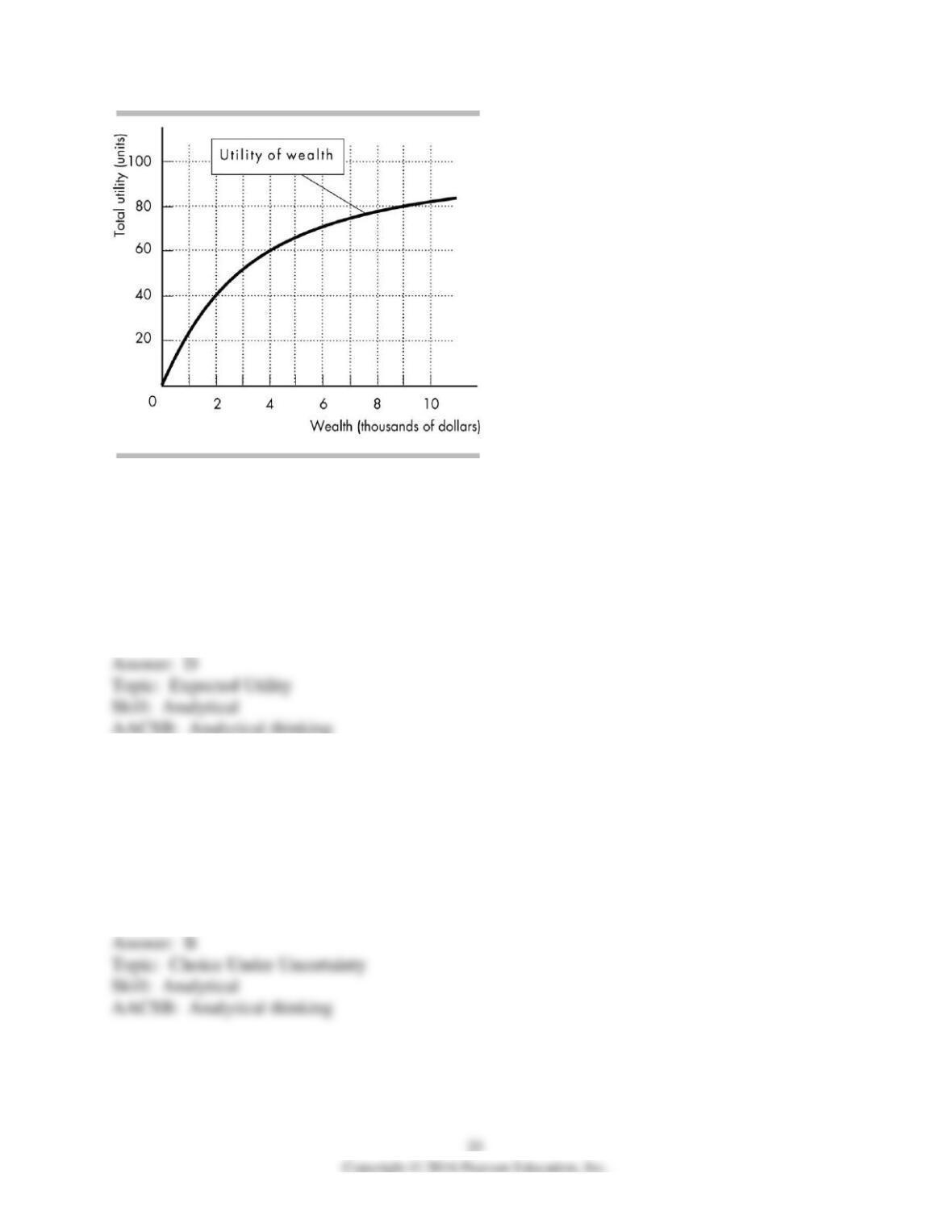

66) The above figure shows how an individual evaluates a bet in which he or she has a 0.5

probability of receiving $20 and a 0.5 probability of receiving $200. The individual would be

indifferent between

A) $110 with certainty or the expected value of the bet.

B) $80 with certainty or the expected value of the bet.

C) $200 with certainty or the expected value of the bet.

D) $20 with certainty or the expected value of the bet.

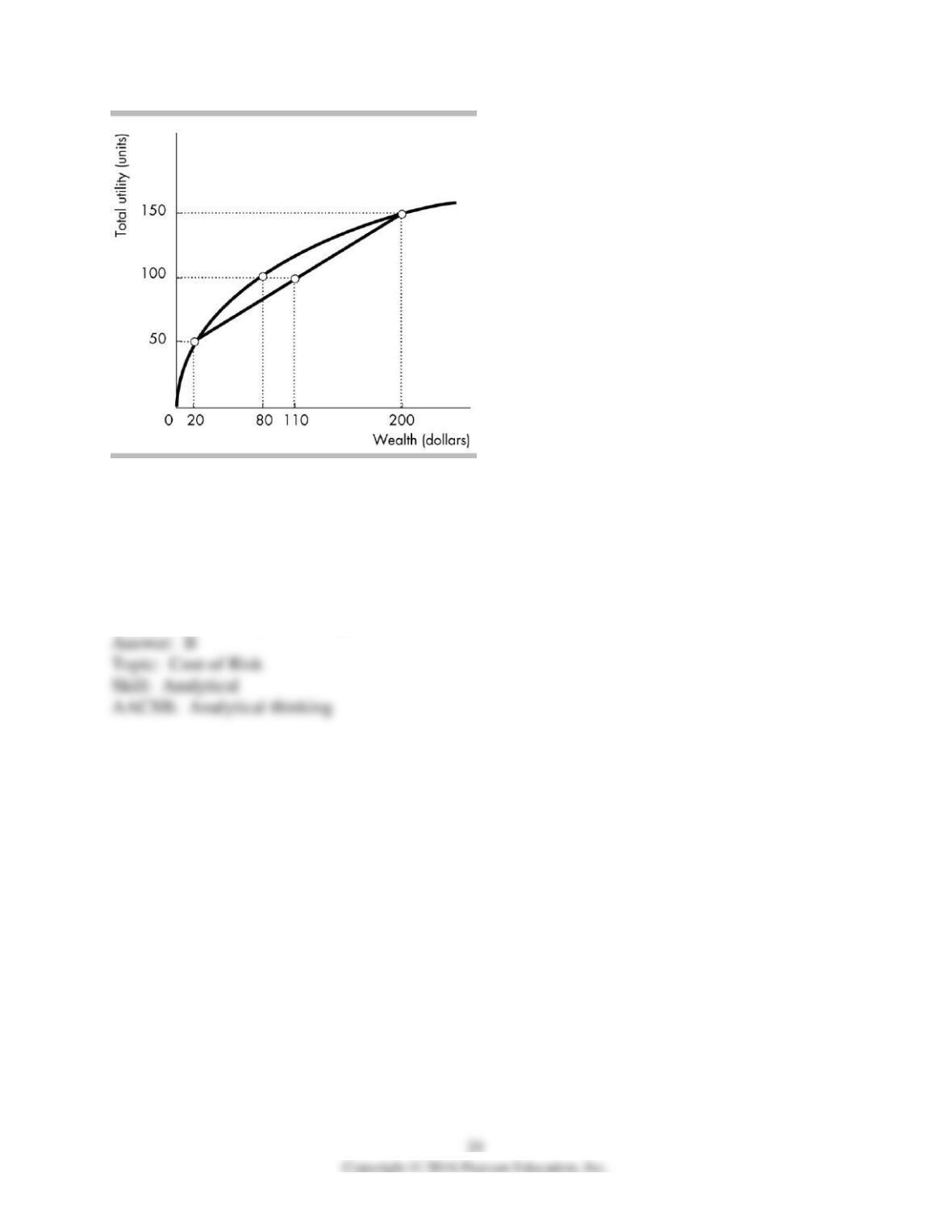

67) Adriana wants to try working as an independent contractor this summer. She has a 50 percent

chance that she will make $9,000 and 50 percent chance that she will make nothing. Her utility

of wealth curve is shown in the figure above. What’s Adriana’s expected utility from taking this

job?

A) 45

B) $4,500

C) $2,000

D) 40

68) Adriana wants to try working as an independent contractor this summer. She has a 50 percent

chance that she will make $9,000 and 50 percent chance that she will make nothing. Her utility

of wealth curve is shown in the figure above. What minimum fixed salary should another

employer offer Adriana to persuade her to work for his firm?

A) $1,001

B) $2,001

C) $3,001

D) $4,501

69) Adriana wants to try working as an independent contractor this summer. She has a 50 percent

chance that she will make $9,000 and 50 percent chance that she will make nothing. Her utility

of wealth curve is shown in the figure above. What’s Adriana’s cost of risk?

A) $2,500

B) $2,000

C) zero

D) $40

70) Bobby is offered a job as a salesperson in which there is a 50 percent chance that he will

make $2,000 and a 50 percent chance that he will make $10,000. Bobby’s utility of wealth curve

is shown in the figure above. What is Bobby’s expected income from taking this job?

A) $4,000

B) $6,000

C) $2,000

D) $10,000

71) Bobby is offered a job as a salesperson in which there is a 50 percent chance that he will

make $2,000 and a 50 percent chance that he will make $10,000. Bobby’s utility of wealth curve

is shown in the figure above. What is Bobby’s expected utility from taking this job?

A) 40

B) 50

C) 60

D) 70

72) Bobby is offered a job as a salesperson in which there is a 50 percent chance that he will

make $2,000 and a 50 percent chance that he will make $10,000. Bobby’s utility of wealth curve

is shown in the figure above. What is Bobby’s cost of risk?

A) $1,000

B) $2,000

C) $3,000

D) $4,000

73) Bobby is offered two fulltime jobs. In the first job, as a salesperson, he has a 50 percent

chance to make $2,000 a month and a 50 percent chance to make $10,000 a month. The second

job, as a construction worker, pays $4,500 a month with certainty. Bobby’s utility of wealth

curve is shown in the figure above. Bobby will take the ________ job because his expected

________ from this job is greater.

A) first; utility

B) second; utility

C) second; income

D) first; income

74) Erika’s utility with $3,000 of wealth is 6,000 and her utility with $3,001 of wealth is 6,005.

Her marginal utility from gaining the additional $1 of wealth is ________.

A) 6,005

B) 3,001

C) 6,000

D) 5

75) If Al is risk averse, as his wealth increases, his total utility of wealth ________ and his

marginal utility of wealth ________.

A) increases; increases

B) increases; decreases

C) decreases; increases

D) decreases; decreases

76) Soran is risk averse. If her wealth rises by $100, her total utility increases by 300. If her

wealth increases, her total utility will decrease

A) by more than 300.

B) by less than 300.

C) by 300.

D) by some amount that cannot be determined without more information.

2 Buying and Selling Risk

1) Buying insurance is similar to

A) selling risk.

B) irrationally avoiding life’s risks.

C) being a free rider.

D) buying risk.

2) Insurance can be profitable when it

A) eliminates risks.

B) decreases risks.

C) pools risks.

D) changes the individual’s marginal utility of wealth.

3) Insurance works because

A) all policyholders pay in according to risks and all then receive a pay out in return.

B) all policyholders pay in according to risks and then receive a pay out only if they incur a loss.

C) all policyholders pay in according to risks and nobody receives any pay out.

D) only high risk policyholders pay in while everyone is entitled to a pay out.

4) You overhear the following in the hallway, “Everyone eventually dies, so how can a life

insurance company make a profit? Isn’t it a losing battle? You will always have to pay the death

benefit to your clients!” You know that life insurance companies can be profitable. This is

because

A) the premiums you pay on a life insurance policy are always more than any death benefit, so

the insurance company always comes out ahead.

B) older people with a greater probability of dying during the term of a policy are denied any

death benefits.

C) the insurance company collects more than enough in premiums today to cover expected

benefits payable today.

D) life insurance companies are notorious for cheating clients with “fine print” policy clauses.

5) Insurance is possible and can be profitable because of

A) private information.

B) adverse selection.

C) moral hazard.

D) consumers are risk aversion.

6) Jon is risk averse. When he buys insurance against all risks, then

A) he knows his wealth with certainty.

B) his utility exceeds his expected utility.

C) his wealth exceeds his expected wealth.

D) all of the above.

7) Ashwini is thinking of buying travel insurance (which pays her if she needs to cancel her trip)

for her trip to Cancun over spring break. There is a 5 percent chance that she will need to cancel

her trip. Without insurance she would lose the full $2,000 price of the trip; with insurance she

would get a full refund of $2,000. The premium for this insurance is $105. Which of the

following is CORRECT?

I. The expected value of Ashwini’s loss is $100.

II. If Ashwini is risk averse she is willing to buy the insurance only if its price is less than $100.

A) I only

B) II only

C) I and II

D) neither I nor II

8) Many residents of the city of Adelphia drive without automobile insurance. Assuming that

Adelphia is just like any other city and these are risk averse individuals, which of the following

is most likely TRUE?

A) Economic models do not work.

B) These people maximize wealth.

C) The price of automobile insurance exceeds their maximum value of insurance.

D) There are no automobile accidents or thefts in the city of Adelphia.

9) Dane has a car valued at $20,000 that gives him a utility of 80. There is a 5 percent chance

that he will have an accident that will make his car worthless, in which case his utility will be

zero. His utility from a wealth of $15,000 is 76. The maximum amount Dane will be willing to

pay for insurance is

A) $1,000.

B) $3,000.

C) $5,000.

D) $15,000.

10) Dan has a car valued at $10,000 that gives him a utility of 50 units. There is a 10 percent

chance that he will have an accident that will make his car worthless, in which case his utility

will be zero. His utility from a wealth of $7,000 is 45 units. The maximum amount Dan will be

willing to pay for car insurance is

A) $1,000.

B) $3,000.

C) $7,000.

D) zero.

Wealth

(dollars)

Total

utility

0

0

20,000

200

40,000

245

60,000

270

80,000

287

100,000

300

11) Beachcomber Beatrice spent her entire wealth of $100,000 to build a beach house on the

Gulf of Mexico. There is a 10 percent chance that the house will be totally destroyed by a

hurricane. Beatrice’s utility of wealth schedule is given in the table above. What is Beatrice’s

expected wealth?

A) $10,000

B) $50,000

C) $90,000

D) $100,000

12) Beachcomber Beatrice spent her entire wealth of $100,000 to build a beach house on the

Gulf of Mexico. There is a 10 percent chance that the house will be totally destroyed by a

hurricane. Beatrice’s utility of wealth schedule is given in the table above. What is Beatrice‘s

expected utility of wealth?

A) between 0 and 200

B) 245

C) 270

D) between 287 and 300

13) Beachcomber Beatrice spent her entire wealth of $100,000 to build a beach house on the

Gulf of Mexico. There is a 10 percent chance that the house will be totally destroyed by a

hurricane. Beatrice’s utility of wealth schedule is given in the table above. What is the minimum

amount that the insurance company would require Beatrice to pay for an insurance policy that

pays $100,000 if her beach house is destroyed by a hurricane? (Assume the insurance company

has no other costs.)

A) $10,000

B) $30,000

C) $40,000

D) $60,000

14) Beachcomber Beatrice spent her entire wealth of $100,000 to build a beach house on the

Gulf of Mexico. There is a 10 percent chance that the house will be destroyed by a hurricane.

Beatrice’s utility of wealth schedule is given in the table above. What is the maximum amount

that Beatrice would be willing to pay for an insurance policy that pays $100,000 if her beach

house is destroyed by a hurricane?

A) $10,000

B) $30,000

C) $40,000

D) $60,000

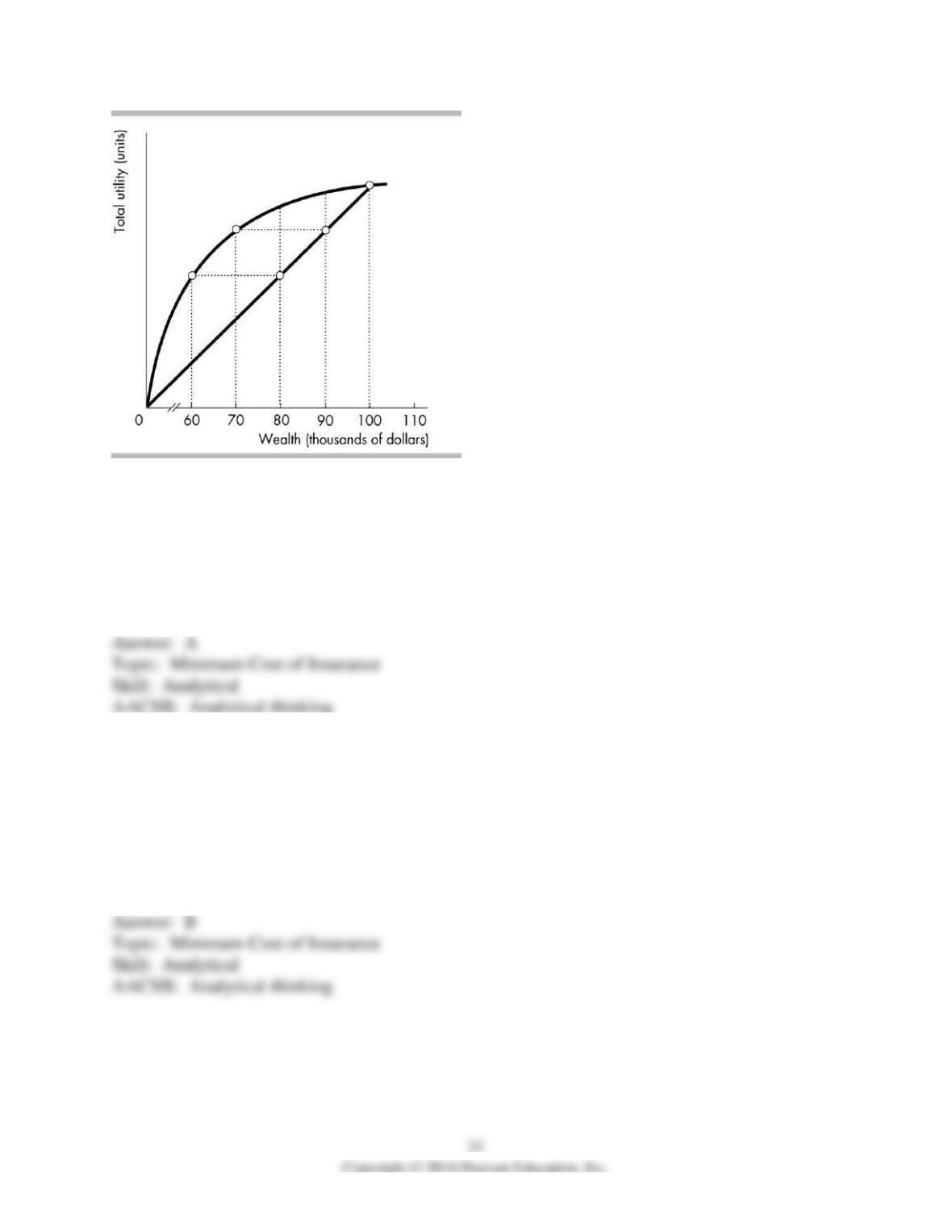

15) Van, whose utility of wealth curve is shown in the above figure, owns a home that is valued

at $100,000. There is a 10 percent chance that the house will be destroyed by hurricane. The

minimum cost of insurance in this case is

A) $10,000.

B) $20,000.

C) $30,000.

D) $40,000.

16) Van, whose utility of wealth curve is shown in the above figure, owns a home that is valued

at $100,000. Initially there is a 10 percent chance that the house will be destroyed by hurricane.

As the risk of destruction due to hurricane rises from 10 percent to 20 percent, the minimum cost

of insurance

A) stays the same.

B) increases by $10,000.

C) increases by $20,000.

D) increases by $30,000.

17) Van, whose utility of wealth curve is shown in the above figure, owns a home that is valued

at $100,000. There is a 10 percent chance that the house will be destroyed by hurricane. The

value of insurance to Van is

A) $10,000.

B) $15,000.

C) $20,000.

D) $30,000.

18) Bruce Copperwood’s utility of wealth curve is illustrated in the above figure. Bruce is

presently employed at a salary of $100,000. There is a 10 percent probability that Bruce will be

totally disabled, in which case he will have no wealth. The maximum amount that Bruce is

willing to pay for a disability insurance policy that would pay him $100,000 in the case of total

disability is

A) $10,000.

B) $20,000.

C) $80,000.

D) None of the above answers is correct.

19) Bruce Copperwood’s utility of wealth curve is illustrated in the above figure. Bruce is

presently employed at a salary of $100,000. There is a 10 percent probability that Bruce will be

totally disabled, in which case he will have no wealth. An insurance company (with no operating

expenses) would be willing to offer Bruce a disability insurance policy paying $100,000 in the

case of total disability for a minimum premium of

A) $1,000.

B) $10,000.

C) $20,000.

D) None of the above answers is correct.

20) Steve owns a motorcycle valued at $5,000, and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. With no

insurance, Steve’s expected wealth is

A) $4,000.

B) $4,500.

C) $3,500.

D) $5,000.

21) Steve owns a motorcycle valued at $5,000, and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. With no

insurance, Steve’s expected utility is

A) 97.

B) 84.

C) 90.

D) 100.

22) Steve owns a motorcycle valued at $5,000 and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. What is the

maximum insurance premium that Steve is willing to pay?

A) $2,000

B) $500

C) $1,000

D) $1,500

23) Steve owns a motorcycle valued at $5,000 and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. What is the

minimum premium that the insurance company will accept?

A) $1,000

B) $2,000

C) $500

D) $1,500

24) Steve owns a motorcycle valued at $5,000 and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. Both Steve

and the insurance company will gain if the insurance premium is

A) $900.

B) $1,200.

C) $1,600.

D) $700.

25) Steve owns a motorcycle valued at $5,000 and that is his only asset. There is a 5 percent

chance that Steve will have an accident within a year. If he does have an accident, his motorcycle

is worthless. Steve’s utility of wealth curve is shown in the figure above. An insurance company

agrees to pay Steve the full value of his motorcycle in case of an accident if he buys the

company’s insurance policy. The company’s operating expenses are $500 per policy. If Steve

buys the insurance for $1,000, his expected wealth will be ________, and his expected utility

will be ________ than with no insurance.

A) greater; greater

B) greater; less

C) less; greater

D) less; less

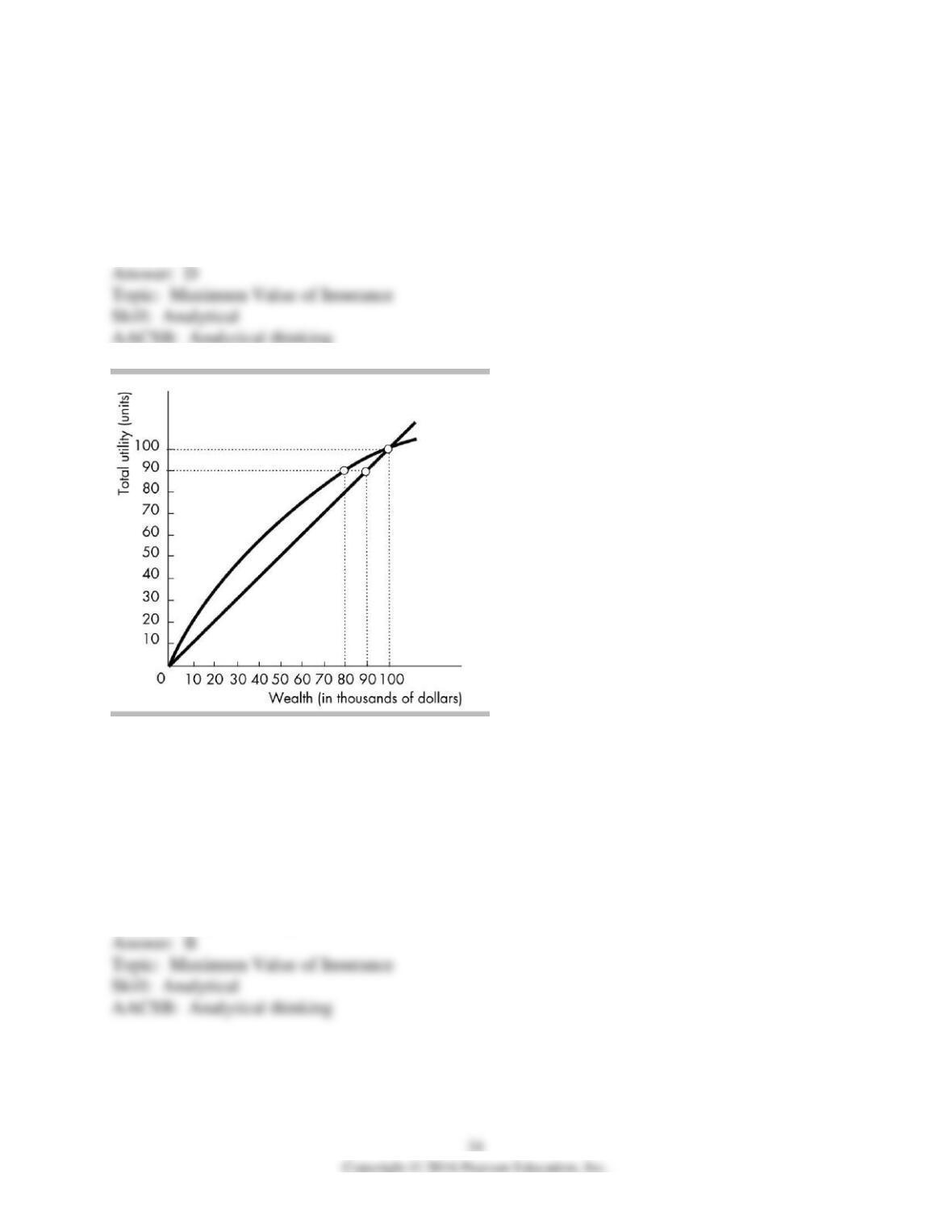

26) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. Which of the following statements is TRUE?

A) This person has diminishing marginal utility of wealth.

B) This person is not risk averse.

C) Risky situations cause this person no loss of utility.

D) None of the above are correct.

27) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. If there is a 20 percent chance that the home could be entirely destroyed,

what is the person’s expected wealth?

A) $10,000

B) $20,000

C) $30,000

D) $40,000

28) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. If there is a 20 percent chance that the home could be entirely destroyed,

what is the person’s cost of risk?

A) $10,000

B) $20,000

C) $30,000

D) $40,000

29) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. If there is a 20 percent chance that the home could be entirely destroyed, the

highest price for insurance this person would pay is

A) $0.

B) $5,000.

C) $10,000.

D) $20,000.

30) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. If there is a 20 percent chance that the home could be completely destroyed,

would this homeowner buy insurance?

A) No, because the homeowner is not risk averse.

B) Yes, at any price because the homeowner is risk averse.

C) Yes, but only if it costs less than $10,000.

D) Yes, but only if it costs less than $20,000.

31) The above figure shows the utility of wealth curve for a homeowner whose only possession

is a $50,000 house. If there is a 20 percent chance that the home could be entirely destroyed,

would this person buy a $20,000 insurance policy to replace the house if destroyed?

A) No, it is too expensive.

B) No, he is not risk averse.

C) Yes, the homeowner would pay even more.

D) Yes, this is the most the homeowner would pay.

32) John’s utility of wealth curve is shown in the above figure. He currently has wealth of

$20,000. If the state lottery offers a 1 in 10,000 chance of winning $10,000, John will

A) pay whatever price it takes to play.

B) pay $1 to play this game.

C) pay less than $1 to play this game.

D) not be willing to play this game at any price.

33) John’s utility of wealth curve is shown in the above figure. He currently has total wealth of

$20,000. If there is a 50 percent chance that his $10,000 car will be stolen, then his expected

wealth equals

A) $0.

B) $10,000.

C) $15,000.

D) $20,000.