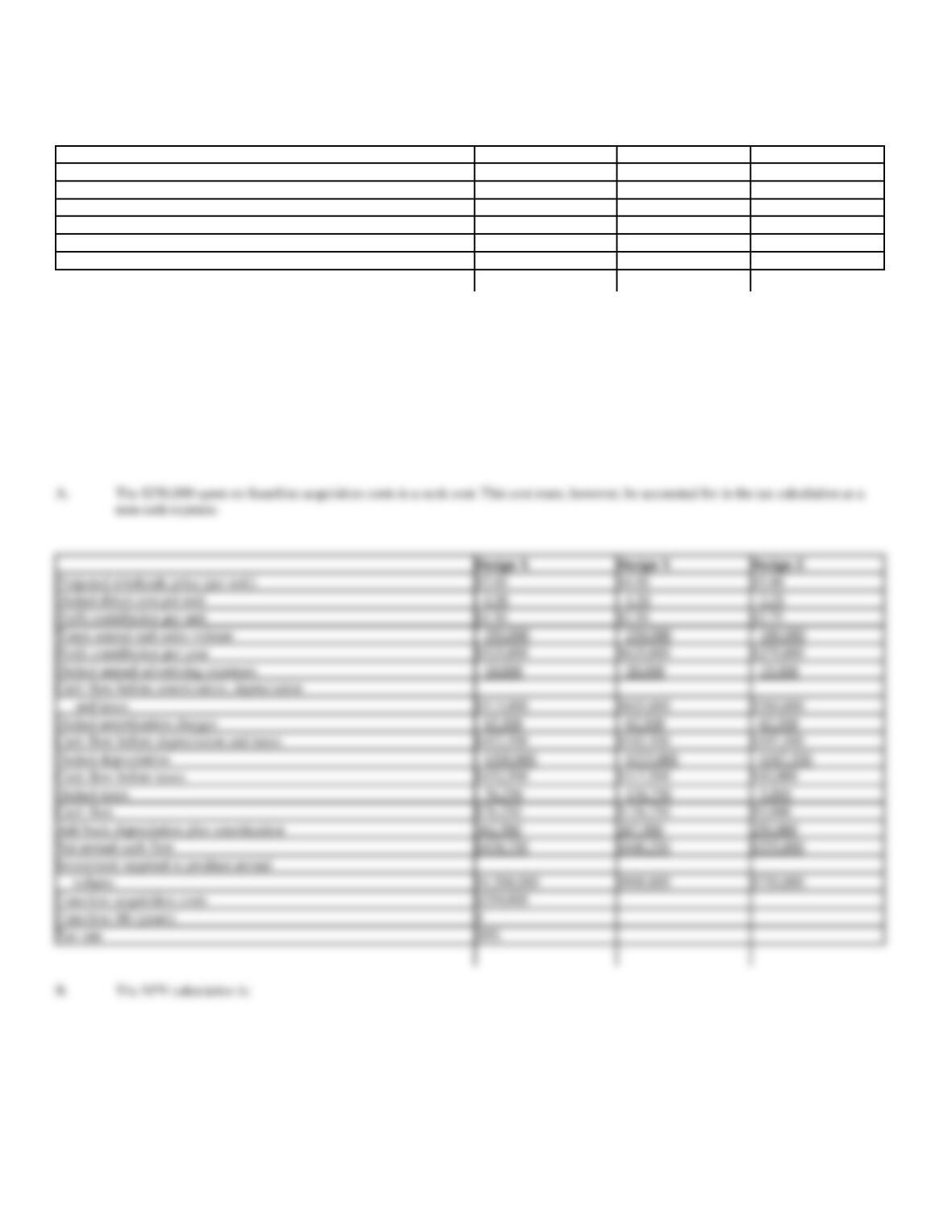

Assume that: (1) The company’s marginal city-plus-state-plus-federal tax rate is 40%, (2) each product is expected to have a three-year life, (3) the

firm uses straight-line depreciation, (4) the average cost of capital is 20%, (5) the products have the same risks as the firm’s other business, and (6)

the company has already spent $25,000 on research and development (R&D) for these products. This $250,000 has been capitalized and will be

amortized over the life of the product chosen, if any.

A.

What is the expected net cash flow each year? (Hint: Cash flow equals net profit after taxes plus depreciation and amortization charges.)

B.

What is the net present value of each product? Which product, if any, should BDI introduce?

Projected market price (per unit)

$100.00

$250.00

$300.00

Deduct direct cost per unit

– 25.00

– 50.00

– 75.00

Profit contribution per unit

$75.00

$200.00

$225.00

Times annual unit sales volume

´ 12,000

´ 15,000

´ 5,000

Profit contribution per year

$900,000

$3,000,000

$1,125,000

Deduct annual selling expenses

– 150,000

– 250,000

– 125,000

Cash flow before amortization, depreciation

and taxes

$750,000

$2,750,000

$1,000,000

Deduct amortization charges

– 83,333

– 83,333

– 83,333

Cash flow before depreciation and taxes

$666,667

$2,666,667

$916,667

Deduct depreciation

– 400,000

– 300,000

– 250,000

Cash flow before taxes

$266,667

$2,366,667

$666,667

Deduct taxes

– 106,667

– 946,667

– 266,667

Cash flow

$160,000

$1,420,000

$400,000

Add back depreciation plus amortization

483,333

– 383,333

– 333,333

Net annual cash flow

$643,333

$1,803,333

$733,333

Investment required to produce annual

volume

$1,200,000

$900,000

$750,000

Research and development expense

$250,000

Product life (years)

3

Tax rate

40%

B.

The NPV calculation is:

Net annual cash flow

$643,333

$1,803,333

$733,333

Times PVIFA

´ 2.1065

´ 2.1065

´ 2.1065

Present value of annual net cash flows

$1,355,181

$3,798,721

$1,544,766

Deduct initial investment cost

– 1,200,000

– 900,000

– 750,000

Net present value (NPV)

$155,181

$2,898,721

$794,766

Relevant discount rate

20%

Product life (years)

3

45. Cash Flow Analysis. Dick Tracy has acquired a franchise to sell one of three designs of a novelty watch in

the Gotham City Market:

Design X

Design Y

Design Z

Projected wholesale price (per unit)

$2.00

$4.00

$5.00

Direct cost per unit

$0.50

$1.50

$2.25

Annual unit sales volume

350,000

250,000

100,000

Annual advertising expenses

$10,000

$20,000

$15,000

Investment required to produce annual

volume

$1,200,000

$900,000

$750,000

Assume that: (1) The company’s marginal city-plus-state-plus-federal tax rate is 50%, (2) each product is expected to have a four-year life, (3) the

firm uses straight-line depreciation, (4) the average cost of capital is 12%, (5) the products have the same risk as the firm’s other business, and (6) the

company has already spent $250,000 on franchise acquisition costs. This $250,000 has been capitalized and will be amortized over the life of the

design chosen.

A.

What is the expected net cash flow each year? (Hint: Cash flow equals net profit after taxes plus depreciation and amortization charges.)

B.

What is the net present value of each product? Which design, if any, should Tracy sell?

Design X

Design Y

Design Z

Projected wholesale price (per unit)

$2.00

$4.00

$5.00

Deduct direct cost per unit

– 0.50

– 1.50

– 2.25

Profit contribution per unit

$1.50

$2.50

$2.75

Times annual unit sales volume

´ 350,000

´ 250,000

´ 100,000

Profit contribution per year

$525,000

$625,000

$275,000

Deduct annual advertising expenses

– 10,000

– 20,000

– 15,000

Cash flow before amortization, depreciation

and taxes

$515,000

$605,000

$260,000

Deduct amortization charges

– 62,500

– 62,500

– 62,500

Cash flow before depreciation and taxes

$452,500

$542,500

$197,500

Deduct depreciation

– $300,000

– $225,000

– $187,500

Cash flow before taxes

$152,500

$317,500

$10,000

Deduct taxes

– 76,250

– 158,750

– 5,000

Cash flow

$76,250

$158,750

$5,000

Add back depreciation plus amortization

362,500

287,500

250,000

Net annual cash flow

$438,750

$446,250

$255,000

Investment required to produce annual

volume

$1,200,000

$900,000

$750,000

Franchise acquisition costs

$250,000

Franchise life (years)

4

Tax rate

50%

B.

The NPV calculation is:

46. Crossover Discount Rates. Sally Rogers is the chief financial officer for Popular Productions, Inc.,

producers of The Allan Brady Show, a hit comedy series. Rogers is considering the desirability of purchasing

one of two alternative forms of post-production equipment used in the tape editing process. Rogers has

discovered that a serious problem can arise when using the NPV method of project valuation because projects

sometimes differ significantly in terms of the magnitude and timing of cash flows. When the size or pattern of

alternative project cash flows differs greatly, each project’s NPV can react quite differently to changes in the

discount rate. Changes in the appropriate discount rate can sometimes lead to reversals in project rankings.

Rogers discovered this problem when considering the following before-tax cash flow data:

Expected Net Cash Flow

Difference

Year

Project X

Project Y

Project X – Y

2008

($700,000)

($1,750,000)

$1,050,000

2009

150,000

500,000

(350,000)

2010

150,000

450,000

(300,000)

2011

150,000

400,000

(250,000)

2012

150,000

350,000

(200,000)

2013

150,000

300,000

(150,000)

2014

150,000

250,000

(100,000)

2015

150,000

200,000

(50,000)

2016

150,000

150,000

0

2017

150,000

100,000

50,000

2018

150,000

50,000

100,000

Net Cash Flow

$800,000

$1,000,000

($200,000)

IRR

16.95%

13.18%

7.99%

NPV @ 7.99%

$306,966

$306,878

$88

A.

Conceptually describe how ranking reversals can occur at the crossover discount rate.

B.

Which investment project is preferred at a relevant cost of capital that is below the crossover discount rate? Why?

C.

Which investment project is preferred at a relevant cost of capital that is above the crossover discount rate? Why?

Design X

Design Y

Design Z

Net annual cash flow

$438,750

$446,250

$255,000

Times PVIFA

´ 3.0373

´ 3.0373

´ 3.0373

Present value of annual net cash flows

$1,332,615

$1,355,395

$774,512

Deduct initial investment cost

– 1,200,000

– 900,000

– 750,000

Net present value (NPV)

$132,615

$455,395

$24,512

Relevant discount rate

12%

Franchise life (years)

4

47. Cost of Capital. Chock Full O’Coffee, Inc., processes and markets a leading brand of coffee. A security

analyst’s report issued by a national brokerage firm indicates that debt yielding 9%, comprises 60% of the

company’s overall capital structure. Furthermore, both earnings and dividends are expected to grow at a rate of

4% per year.

Currently, common stock in the company is priced at $20, and it should pay $1.40 per share in dividends during

the coming year. This yield compares favorably with the 8% return currently available on risk-free securities

and the 14% average for all common stocks, given the company’s estimated beta of 0.5.

A.

Calculate the component cost of equity using both the capital asset pricing model and the dividend yield plus expected growth model.

B.

Assuming a 50% marginal federal plus state income tax rate, calculate the company’s weighted average cost of capital.

In the capital asset pricing model (CAPM) approach, the required return on equity is:

48. Cost of Capital. Northwest Bankshares, Inc., is a rapidly growing chain of commercial banks in north

central states. A security analyst’s report issued by a national brokerage firm indicates that debt yielding 15%,

comprises 25% of Northwest’s overall capital structure. Furthermore, both earnings and dividends are expected

to grow at a rate of 25% per year.

Currently, common stock in the company is priced at $25, and is not expected to pay dividends during the

coming year. This yield compares favorably with the 10% return currently available on risk-free securities and

the 16% average for all common stocks, given the company’s estimated beta of 2.5.

A.

Calculate Northwest’s component cost of equity using both the capital asset pricing model and the dividend yield plus expected growth

model.

B.

Assuming a 40% marginal federal plus state income tax rate, calculate Northwest’s weighted average cost of capital.

stock, and g is the expected growth

rate.

Therefore,

= 0.25 or 25%

49. Cost of Capital. Marine Transport, Ltd., operates a fleet of oil and chemical tankers. A security analyst’s

report issued by a national brokerage firm indicates that debt yielding 13%, comprises 50% of Marine’s overall

capital structure. Furthermore, both earnings and dividends are expected to grow at a rate of 10% per year.

Currently, common stock in the company is priced at $40, and it should pay $2 per share in dividends during the

coming year. This yield compares favorably with the 10% return currently available on risk-free securities and

the 15% average for all common stocks, given the company’s estimated beta of 1.

A.

Calculate Marine’s component cost of equity using both the capital asset pricing model and the dividend yield plus expected growth

model.

B.

Assuming a 50% marginal federal plus state income tax rate, calculate Marine’s weighted average cost of capital.

In the capital asset pricing model (CAPM) approach, the required return on equity is:

After tax component cost of debt, kd

= Interest rate ´ (1.0 – tax rate)

= 0.15 ´ (1.0 – 0.4)

= 0.09 or 9%

Therefore,

Weighted average cost of capital

= Debt percentage ´ kd + Equity percentage ´ ke

= 0.25(0.09) + 0.75(0.25)

= 0.21 or 21%

50. Cost of Capital. Dartmouth Systems, Inc., is a leading supplier of sorters and collators to the copier and

computer printer market. A security analyst’s report issued by a national brokerage firm indicates that debt

yielding 8%, comprises 50% of Dartmouth’s overall capital structure. Furthermore, both earnings and dividends

are not expected to grow during coming years.

Currently, common stock in the company is priced at $75, and it should pay $7.50 per share in dividends during

the coming year. This yield compares favorably with the 7% return currently available on risk-free securities

and the 13% average for all common stocks, given the company’s estimated beta of 0.5.

A.

Calculate Dartmouth’s component cost of equity using both the capital asset pricing model and the dividend yields plus expected growth

model.

B.

Assuming a 40% marginal federal plus state income tax rate, calculate Dartmouth’s weighted average cost of capital.

stock, and g is the expected growth

rate.

Therefore,

= 0.10 or 10%