38. Expected Return. Dr. Kevin Lenahan & Associates is a local optometrist considering two alternative

capital budgeting projects. Project A is an investment of $800,000 in a new office addition to showcase an

expanded selection of designer frames and contact lenses. Project B is an investment of $750,000 to upgrade

existing testing facilities. Relevant annual cash flow data for the two projects over their expected seven-year

lives are as follows:

Project A

Project B

Pr.

Cash Flow

Pr.

Cash Flow

0.50

$ 0

0.045

$ 0

0.50

500,000

0.910

200,000

0.045

400,000

A.

Calculate the expected value, standard deviation, and coefficient of variation of cash flows for each project.

B.

Calculate the risk-adjusted NPV for each project, using a 20% cost of capital for the more risky project and 15% for the less risky one.

Which project is preferred using the NPV criterion?

C.

Calculate the PI for each project, and rank them according to their PIs.

D.

Calculate the IRR for each project, and rank them according to their IRRs.

E.

Compare your answers to parts B, C, and D, and discuss any differences.

A.

Project A

= $150,000(PVIFA, n = 5, i = X%) – $450,000 = 0

IRR criterion.

despite being riskier, project B has an IRR that is no greater than the less risky project A.

39. Incremental Analysis. Cunningham’s Drug Store, a medium-sized drug store located in Milwaukee,

Wisconsin, is owned and operated by Richard Cunningham. Cunningham’s sells pharmaceuticals, cosmetics,

toiletries, magazines, and various novelties. Cunningham’s most recent annual net income statement is as

follows:

Sales revenue

$2,000,000

Total costs

Cost of goods sold

$1,250,000

Wages and salaries

100,000

Rent

120,000

Depreciation

100,000

Utilities

40,000

Miscellaneous

40,000

Total

1,650,000

Net profit before tax

$ 350,000

Cunningham’s sales and expenses have remained relatively constant in the past few years and are expected to continue unchanged in the near future.

To increase sales, Cunningham is considering using some floor space for a small soda fountain. Cunningham would operate the soda fountain for an

initial five-year period, and then reevaluate its profitability. The soda fountain requires an incremental investment of $25,000 to lease furniture,

equipment, utensils, and so on. This is the only capital investment required during the initial five-year period. At the end of that time, additional

capital would be required to continue operating the soda fountain and no capital would be recovered if it were dropped. The soda fountain is expected

to have sales of $125,000 and food and materials expenses of $30,000 per year. The soda fountain is also expected to increase wage and salary

expenses by 8% and utility expenses by 5%. Because the soda fountain will reduce the floor space available for display of other merchandise, sales of

nonsoda fountain items are expected to decline by 10%.

A.

Calculate net incremental cash flows for the soda fountain.

B.

Assume that Cunningham has the capital necessary to install the soda fountain and places a 12% before-tax opportunity cost on those

funds. Should the soda fountain be installed? Why or why not?

A.

The relevant annual cash flows from the proposed soda fountain are:

Incremental revenue:

$125,000

Increment cost:

Food and materials

$30,000

Wages and salaries ($100,000 ´ 0.08)

8,000

Utilities ($40,000 ´ 0.05)

2,000

Opportunity Cost: Profit contribution lost on regular

sales = 0.1($2,000,000 – $1,250,000)

75,000

Total incremental cost

115,000

Net incremental annual cash flow

$ 10,000

Incremental investment

$ 25,000

Therefore, 18% < IRRB < 20% (or exactly 18.58%).

40. Incremental Analysis. Warren Buffet is a medium-sized restaurant located in Omaha, Nebraska. Warren

Buffet currently offers elegant dining to luncheon and dining customers. The restaurant’s most recent annual net

income statement is as follows:

Sales revenue:

$5,000,000

Total costs:

Cost of goods sold

$1,500,000

Wages and salaries

2,500,000

Rent

180,000

Depreciation

250,000

Utilities

75,000

Miscellaneous

20,000

Total

4,525,000

Net profit before tax

$ 475,000

Luncheon and dining customer sales and expenses have remained relatively constant in the past few years and are expected to continue unchanged in

the near future. To increase sales, Warren Buffet is considering offering a new Sunday buffet brunch service. Warren Buffet would offer Sunday

brunch for an initial two-year period, and then reevaluate its profitability. Offering a Sunday brunch would require an initial outlay of $10,000 to

cover new buffet equipment and utensils. This is the only capital investment required during the initial two-year period. At the end of that time,

additional capital would be required to continue operation, and no capital would be recovered if the buffet were dropped. Buffet sales of $300,000 are

anticipated, and the share of revenues devoted to cost of goods sold expenses are expected to represent the same as previously. Wage and salary

expenses are expected to increase by 8% and utility expenses by 5%. No other incremental costs are expected.

A.

Calculate net incremental cash flows for the Sunday buffet.

B.

Assume that Warren Buffet’s has the necessary capital and places a 20% before-tax opportunity cost on those funds. Should the buffet

service be offered? Why or why not?

A.

The relevant annual cash flows from the proposed soda fountain are:

Incremental revenue:

$300,000

Increment cost:

Food and materials ($300,000 ´ 0.3)

$ 90,000

Wages and salaries ($2,500,000 ´ 0.08)

200,000

Utilities ($75,000 ´ 0.05)

3,750

Total incremental cost

293,750

Net incremental annual cash flow

$ 6,250

Incremental investment

$ 10,000

NPV

= (Incremental annual cash flow)(PVIFA, n = 5, i = 12%) – $25,000

= $10,000(3.6048) – $25,000

= $11,048

project.

41. Incremental Analysis. Grey’s Anatomy, Ltd., is contemplating opening a new retail outlet in a suburban

shopping mall. Projections for an initial 10-year period for the potential outlet are:

Sales revenue:

$2,000,000

Total costs:

Advertising

$500,000

Cost of goods sold

750,000

Wages and salaries

350,000

Rent

75,000

Depreciation

25,000

Utilities

75,000

Miscellaneous

25,000

Total

1,800,000

Projected Net profit before tax

$ 200,000

A.

Calculate the NPV for the proposed outlet assuming that an initial investment of $750,000 is required and the cost of capital is k=20%.

B.

Given the proposed outlet’s projected net profit before tax, calculate the maximum initial investment that could be justified when

k=20%.

A.

The NPV for the proposed outlet is calculated as follows:

NPV

= (Incremental annual cash flow)(PVIFA, n = 10, i = 20%)

– $750,000

= $200,000(4.1925) – $750,000

= $88,500

NPV

= (Incremental annual cash flow)(PVIFA, n = 2, i = 20%) – $10,000

= $6,250(1.5278) – $10,000

= $451.25 (a loss)

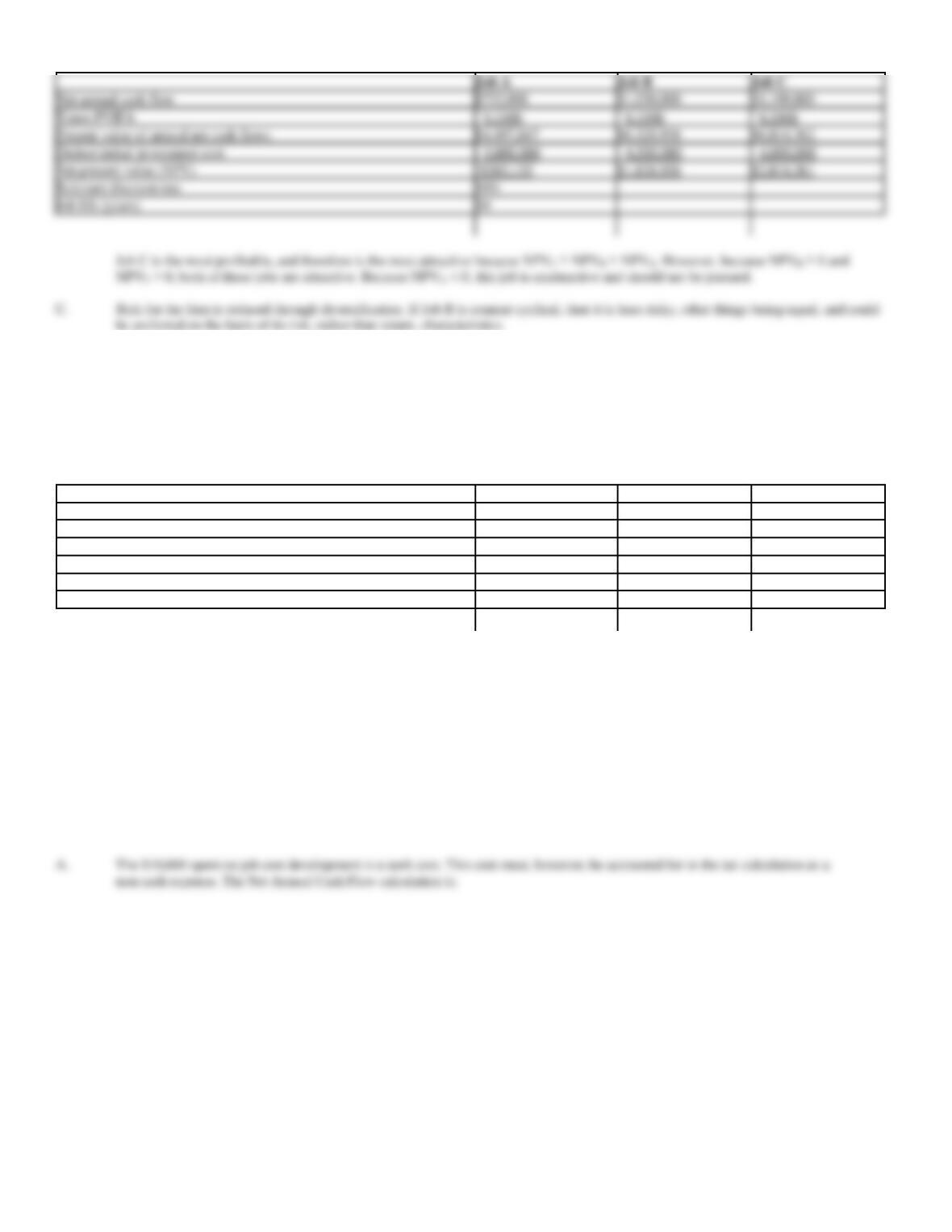

42. Cash Flow Analysis. The Gulf States Press, Inc., is analyzing the potential profitability of three printing

jobs put up for bid by the State Department of Transportation:

Job A

Job B

Job C

Projected winning bid (per unit)

$7.00

$9.00

$11.00

Direct cost per unit

$6.00

$6.00

$8.00

Annual unit sales volume

1,000,000

500,000

550,000

Annual distribution costs

$120,000

$90,000

$75,000

Investment required to produce annual

volume

$5,000,000

$4,500,000

$4,000,000

Assume that: (1) The company’s marginal state plus federal tax rate is 40%, (2) each job is expected to have a ten-year life, (3) the firm uses

straight-line depreciation, (4) the average cost of capital is 10%, (5) the jobs have the same risks as the firm’s other business, and (6) the company has

already spent $100,000 on developing the preceding data. This $100,000 has been capitalized and will be amortized over the life of the job chosen, if

any.

A.

What is the expected net cash flow each year? (Hint: Cash flow equals net profit after taxes plus depreciation and amortization charges.)

B.

What is the net present value of each job? On which job, if any, should Gulf States bid?

C.

Suppose that Gulf States’ primary business is quite cyclical, improving and declining with the economy, which Job B is expected to be

counter cyclical. Might this have any bearing on your decision?

Job A

Job B

Job C

Projected winning bid (per unit)

$7.00

$9.00

$11.00

Deduct direct cost per unit

– 6.00

– 6.00

– 8.00

Profit contribution per unit

$1.00

$3.00

$3.00

Times annual unit sales volume

´ 1,000,000

´ 500,000

´ 550,000

Profit contribution per year

$1,000,000

$1,500,000

$1,650,000

Deduct annual distribution costs

– 120,000

– 90,000

– 75,000

Cash flow before amortization, depreciation

and taxes

$880,000

$1,410,000

$1,575,000

Deduct amortization charges

– 10,000

– 10,000

– 10,000

Cash flow before depreciation and taxes

$870,000

$1,400,000

$1,565,000

Deduct depreciation

– $500,000

– $450,000

– $400,000

Cash flow before taxes

$370,000

$950,000

$1,165,000

Deduct taxes

– 148,000

– 380,000

– 466,000

Cash flow

$222,000

$570,000

$699,000

Add back depreciation plus amortization

510,000

460,000

410,000

Net annual cash flow

$732,000

$1,030,000

$1,109,000

Investment required to produce annual

volume

$5,000,000

$4,500,000

$4,000,000

Job cost development

$100,000

Job life (years)

Tax rate

40%

B.

The NPV calculations are:

43. Cash Flow Analysis. The Printing Press, Inc., (PPI) is analyzing the potential profitability of three printing

jobs put up for bid by a national textbook publisher:

Job A

Job B

Job C

Projected winning bid (per unit)

$25.00

$35.00

$50.00

Direct cost per unit

$5.00

$15.00

$10.00

Annual unit sales volume

10,000

20,000

7,500

Annual distribution costs

$150,000

$200,000

$50,000

Investment required to produce annual

volume

$500,000

$400,000

$250,000

Assume that: (1) The company’s marginal city-plus-state-plus-federal tax rate is 35%, (2) each job is expected to have a five-year life, (3) the firm

uses straight-line depreciation, (4) the average cost of capital is 15%, (5) the jobs have the same risks as the firm’s other business, and (6) the

company has already spent $10,000 on developing the preceding data. This $10,000 has been capitalized and will be amortized over the life of the

job chosen, if any.

A.

What is the expected net cash flow each year? (Hint: Cash flow equals net profit after taxes plus depreciation and amortization charges.)

B.

What is the net present value of each job? On which job, if any, should PPI bid?

C.

Suppose that PPI’s primary business is quite cyclical, improving and declining with the economy, which job B is expected to be counter

cyclical. Might this have any bearing on your decision?

Job A

Job B

Job C

Net annual cash flow

$732,000

$1,030,000

$1,109,000

Times PVIFA

´ 6.1446

´ 6.1446

´ 6.1446

Present value of annual net cash flows

$4,497,847

$6,328,938

$6,814,362

Deduct initial investment cost

– 5,000,000

– 4,500,000

– 4,000,000

Net present value (NPV)

-$502,153

$1,828,938

$2,814,361

Relevant discount rate

10%

Job life (years)

44. Cash Flow Analysis. Biometric Devices, Inc., is analyzing the potential profitability of three potential new

testing devices:

Product X

Product Y

Product Z

Projected market price (per unit)

$100.00

$250.00

$300.00

Direct cost per unit

$25.00

$50.00

$75.00

Annual unit sales volume

12,000

15,000

5,000

Annual selling expenses

$150,000

$250,000

$125,000

Investment required to produce annual

volume

$1,200,000

$900,000

$750,000

Job A

Job B

Job C

Projected winning bid (per unit)

$25.00

$35.00

$50.00

Deduct direct cost per unit

– 5.00

– 15.00

– 10.00

Profit contribution per unit

$20.00

$20.00

$40.00

Times annual unit sales volume

´ 10,000

´ 20,000

´ 7,500

Profit contribution per year

$200,000

$400,000

$300,000

Deduct annual distribution costs

– 150,000

– 200,000

– 50,000

Cash flow before amortization, depreciation

and taxes

$50,000

$200,000

$250,000

Deduct amortization charges

– 2,000

– 2,000

– 2,000

Cash flow before depreciation and taxes

$48,000

$198,000

$248,000

Deduct depreciation

– 100,000

– 80,000

– 50,000

Cash flow before taxes

-$52,000

$118,000

$198,000

Deduct taxes

– (18,200)

– 41,300

– 69,300

Cash flow

-$33,800

$76,700

$128,700

Add back depreciation plus amortization

102,000

82,000

52,000

Net annual cash flow

$68,200

$158,700

$180,700

Investment required to produce annual

volume

$500,000

$400,000

$250,000

Job cost development

$10,000

Job life (years)

5

Tax rate

35%

The NPV calculations are:

Net annual cash flow

$68,200

$158,700

$180,700

Times PVIFA

´ 3.3522

´ 3.3522

´ 3.3522

Present value of annual net cash flows

$228,620

$531,994

$605,742

Deduct initial investment cost

– 500,000

– 400,000

– 250,000

Net present value (NPV)

-$271,380

$131,994

$355,742

Relevant discount rate

15%

Job life (years)

5