United States – BPROG: Analytic

Monetary and fiscal policy

The State and Local Tax System

136. The idea of horizontal equity in taxation implies that

a.

equally situated individuals should be taxed equally.

b.

unequally situated individuals should be taxed unequally.

c.

benefits should be given first to those individuals who need them most.

d.

the greatest tax burden should be borne by the wealthiest individuals.

DISC: Monetary and fiscal policy

United States – BPROG: Reflective Thinking – BPROG: Analysis

Monetary and fiscal policy

The Concept of Equity in Taxation

137. Horizontal equity is the concept that

a.

equally situated individuals should be taxed equally.

b.

persons with the same income should be taxed equally.

c.

equal property value should be taxed equally.

d.

persons living in the same neighborhood should be taxed equally.

United States – BPROG: Analytic

The study of economics, and defi – The study of economics, and definitions of economics

The Concept of Equity in Taxation

138. The notion that equally situated individuals should be taxed equally is referred to as

a.

horizontal equity.

b.

vertical equity.

c.

the benefits principle.

d.

the Gini principle.

DISC: The study of economics, an – DISC: The study of economics, and definitions in

United States – BPROG: Analytic

The study of economics, and defi – The study of economics, and definitions of economics

The Concept of Equity in Taxation

139. If two families are equally situated except that one rents and the other owns their home, the existing tax system will

lead to

a.

vertical inequity.

b.

equal treatment of both.

c.

horizontal inequity.

d.

equal burden sharing.

DISC: Monetary and fiscal policy

United States – BPROG: Reflective Thinking – BPROG: Analysis

Monetary and fiscal policy

The Concept of Equity in Taxation

140. Horizontal equity is a difficult concept to implement because

a.

it is difficult to determine how unequally unequals should be treated.

b.

it is difficult to measure ability to pay.

c.

it is difficult to determine which people are equally situated.

d.

people object to the use of absolute tax liability instead of percentage of income.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

141. If two families are identical with respect to size, income, general expenses, etc., and are taxed equally, we say that

there is

a.

horizontal equity.

b.

vertical equity.

c.

observance of the ability-to-pay principle.

d.

intergenerational equity.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

142. The ability-to-pay principle is most closely tied to the concept of

a.

horizontal equity in taxation.

b.

fiscal federalism.

c.

vertical equity in taxation.

d.

the benefits principle of tax equity.

c

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

143. Which of the following best reflects the ability-to–pay philosophy of taxation?

a.

an excise tax on coffee

b.

an excise tax on gasoline

c.

a progressive income tax

d.

a tax on residential property

c

Easy

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

144. “Those most able should pay the highest taxes” reflects the

a.

ability-to-pay principle.

b.

concept of horizontal equity.

c.

idea of fiscal federalism.

d.

benefits principle.

a

Easy

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

145. A congress member concerned about ensuring vertical equity in taxation would be most likely to argue for obtaining

government revenue through a

a.

progressive tax on personal income.

b.

regressive tax on corporate income.

c.

sales tax.

d.

head tax.

DISC: Efficiency and equity

United States – BPROG: Analytic

Efficiency and equity

The Concept of Equity in Taxation

146. “People who make more money should pay higher taxes” is an example of

a.

the benefits principle.

b.

horizontal equity.

c.

vertical efficiency.

d.

the ability-to-pay principle.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

147. The concept of vertical equity is that

a.

income should be taxed instead of property.

b.

property should be taxed instead of income.

c.

there should be little movement up or down the social scale.

d.

persons who are unequal should be treated unequally.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

148. In practice, turning horizontal and vertical equity into tax law

a.

hasn’t been tried.

b.

has been fairly easy.

c.

is resisted by nearly all taxpayers.

d.

has been extremely difficult.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

149. In England the Thatcher government substituted a “poll tax” for the local property tax. People took strong exception

to the tax, which is basically a head or “lump sum” tax. The principle of taxation such a tax violates is called

a.

the benefits principle.

b.

the excess burden principle.

c.

the ability-to-pay principle.

d.

the constitutional principle.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

150. The benefits principle states that those who

a.

pay the taxes should reap the benefits.

b.

reap the benefits from government should pay the taxes.

c.

are best able to pay should pay for what they receive.

d.

pay taxes get the benefits they deserve.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

151. Which of the following situations is a clear application of the benefits principle of taxation?

a.

wealthier people are taxed more heavily

b.

heavier vehicles are charged higher tolls on turnpikes

c.

state government providing a free education to any child in the state

d.

sales of measles vaccine exempt from sales tax

Difficult

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

152. Which of the following would be the most likely candidate for direct application of the benefits principle of taxation?

a.

education

b.

fire protection

c.

police protection

d.

use of roads

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

153. The benefits principle is often used to justify

a.

the progressive income tax.

b.

a flat income tax.

c.

a regressive excise tax.

d.

earmarking the proceeds from taxes for specific public services.

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Equity in Taxation

154. The burden of a tax is

a.

the amount of revenue that the government raises from the tax.

b.

what it would cost in alternative tax revenue to provide the same level of service.

c.

greater as the total revenue from the tax decreases.

d.

the amount the taxpayer would have to be given to be just as well off in the presence of the tax as in its

absence.

Moderate

DISC: The study of economics, an – DISC: The study of economics, and definitions in

United States – BPROG: Analytic

The study of economics, and defi – The study of economics, and definitions of economics

The Concept of Efficiency in Taxation

155. The total burden of a tax is the

a.

absolute number of dollars an individual pays.

b.

percentage of income a person pays.

c.

number of dollars a person must be given after taxation to make him as well off as he was before taxation.

d.

revenue lost to loopholes.

United States – BPROG: Analytic

The study of economics, and defi – The study of economics, and definitions of economics

The Concept of Efficiency in Taxation

156. An efficient tax is one that raises the desired tax revenue but creates the least possible

a.

total burden.

b.

excess burden.

c.

tax incidence.

d.

tax shifting.

DISC: Efficiency and equity

United States – BPROG: Analytic

Efficiency and equity

The Concept of Efficiency in Taxation

157. A tax has an excess burden whenever

a.

people are unable to alter their behavior to avoid paying it.

b.

government seeks to raise it.

c.

it raises a great deal of revenue.

d.

it induces people to change their behavior.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

158. In which of the following examples is excess burden not present?

a.

Harriet decides to give up her Saturday hours at her law office after income tax rates rise.

b.

Rudolf still smokes three packs a day even after the excise tax on cigarettes rose 10 cents a pack.

c.

Wilma reduced the automatic payroll deduction to her savings account after the tax on interest was imposed.

d.

Harper decided to take a vacation in Bermuda rather than invest in stocks after the tax rate on capital gains was

increased.

Easy

DISC: Monetary and fiscal policy

United States – BPROG: Reflective Thinking – BPROG: Analysis

Monetary and fiscal policy

The Concept of Efficiency in Taxation

BLOOMS: Application

159. Edgar Browning and William Johnson, in a paper published in the Journal of Political Economy (1984), presented

evidence that a one-dollar transfer to the bottom 40 percent of income distribution costs the top 60 percent nine dollars. If

correct, this finding proves

a.

the tax system is generating significant excess burdens.

b.

these transfers are not worth the cost.

c.

loopholes have to be closed.

d.

the burden of the tax system is too great.

a

Difficult

DISC: Monetary and fiscal policy

United States – BPRPOG: Analysis

Monetary and fiscal policy

The Concept of Efficiency in Taxation

160. Many environmentalists have advocated a substantial increase in the gasoline tax to cut down the federal deficit and

to reduce pollution due to auto emissions. Such a tax increase would be devastating to people who commute significant

distances to work. In fact, it would provide an incentive to relocate closer to work or change jobs. Economists refer to

such effects of taxes as the

a.

burden of a tax.

b.

regressive incidence of a tax.

c.

incidence of a tax.

d.

excess burden of a tax.

Difficult

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

161. The concept that describes the situation where the economy has used every available opportunity to make someone

better off without making someone else worse off is

a.

economic efficiency.

b.

the benefits principle.

c.

horizontal equity.

d.

vertical equity.

a

Moderate

DISC: Efficiency and equity

United States – BPROG: Analytic

Efficiency and equity

The Concept of Efficiency in Taxation

162. A tax that does not change consumers’ behavior creates no

a.

economic burden.

b.

excess burden.

c.

tax revenue.

d.

tax incidence.

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

163. Tax deductions were significantly ____ under the Tax Reform Act of 1986.

a.

increased

b.

decreased

c.

expanded

d.

left unchanged for individual taxpayers

Easy

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

164. Loopholes have the effect of

a.

encouraging particular patterns of behavior and favoring particular types of people.

b.

eroding the progressivity of the income tax.

c.

altering the pattern of economic incentives.

d.

All of the above are correct.

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

165. In the spring of 1993, President Clinton proposed an energy tax. At one point in the congressional review of the

proposal there was discussion of various exemptions for farmers, truckers, etc. One plan was to dye fuel different colors to

better track the appropriate tax on the user of the fuel. Economists would label these exemptions

a.

loopholes.

b.

economically efficient.

c.

obviously fair.

d.

all of the above.

a

Moderate

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

The Concept of Efficiency in Taxation

166. The major objective of the 1986 tax reform was to: (i) enhance efficiency by lowering marginal tax rates; (ii)

enhance equity by closing “loopholes.”

a.

i and ii

b.

i but not ii

c.

ii but not i

d.

neither i nor ii

a

Difficult

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

167. When a tax is imposed on an item, it can generally be said that the incidence of the tax is

a.

entirely on the buyer.

b.

entirely on the seller.

c.

on both the buyer and seller.

d.

not determined in this manner.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

Shifting the Tax Burden: Tax Incidence

168. Which of the following taxes is least likely to be shifted?

a.

a federal excise tax on grapefruit

b.

a sales tax on some foodstuffs

c.

a personal income tax

d.

a state tax on football tickets

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

Shifting the Tax Burden: Tax Incidence

169. Which of the following taxes is most likely to be shifted?

a.

a property tax on an owner-occupied residence

b.

a progressive income tax

c.

a flat-rate state income tax

d.

a general sales tax

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

Shifting the Tax Burden: Tax Incidence

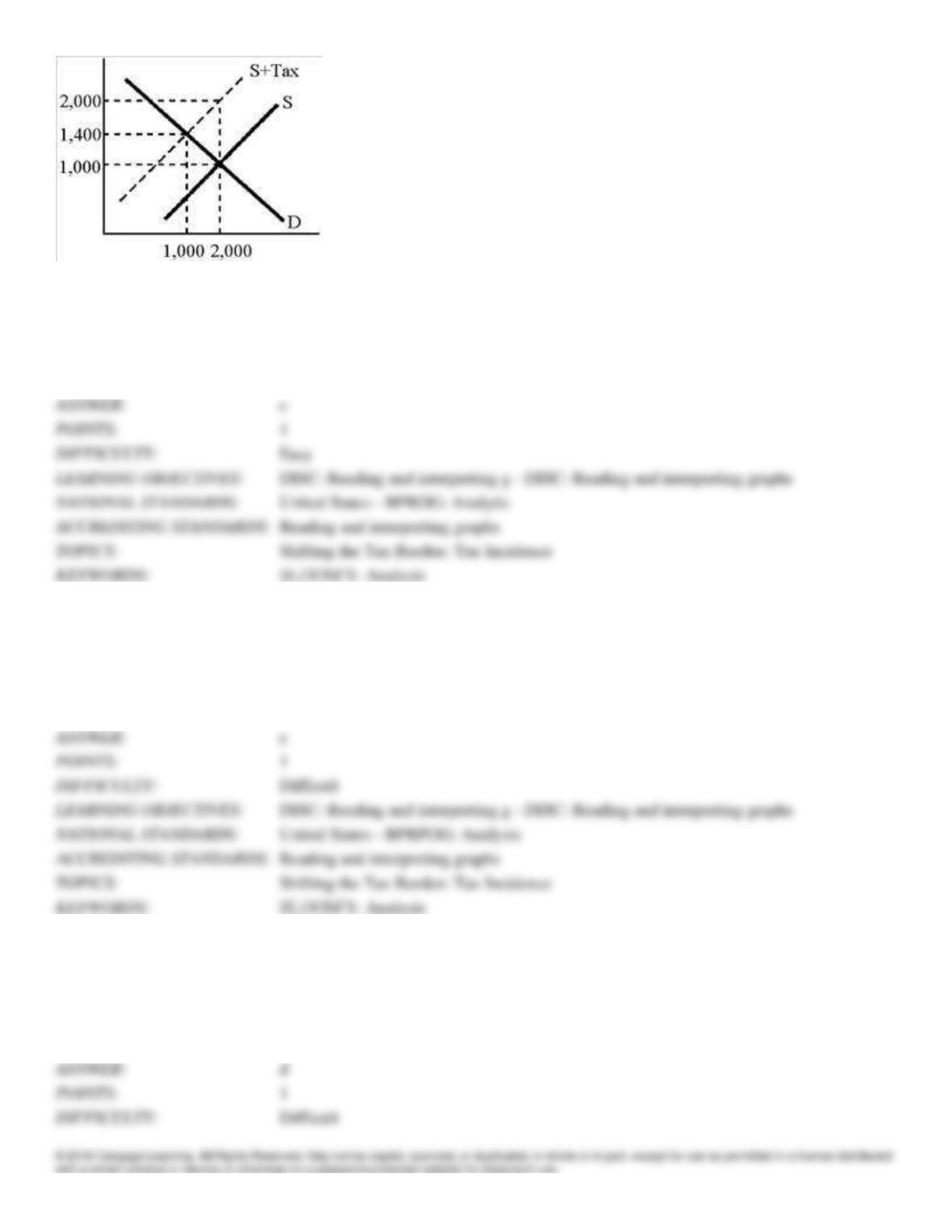

170. According to the graph in Figure 18–1, the tax is which of the following?

a.

400

b.

600

c.

1,000

d.

200

c

Easy

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPROG: Analytic

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

171. According to the graph in Figure 18–1, the increase in the amount that consumers pay as a result of the tax is

a.

1000

b.

600

c.

400

d.

indeterminate

c

Difficult

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPRPOG: Analysis

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

172. According to the graph in Figure 18–1, tax collections will be which of the following?

a.

14 million

b.

1.4 million

c.

12 million

d.

1 million

Difficult

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPRPOG: Analysis

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

173. The economic burden of an excise tax

a.

can usually be partially shifted from buyers onto sellers.

b.

equals the revenue from the tax.

c.

is less than the burden of an income tax that would raise the same revenue.

d.

is shared equally by buyers and sellers.

DISC: Monetary and fiscal policy

United States – BPROG: Analytic

Monetary and fiscal policy

Shifting the Tax Burden: Tax Incidence

174. The percentage of the burden of an excise tax that is borne by sellers generally depends on the

a.

size of the tax.

b.

relationship between the elasticity of demand and the elasticity of supply.

c.

elasticity of demand.

d.

elasticity of supply.

DISC: Elasticity

United States – BPROG: Reflective Thinking – BPROG: Analysis

Shifting the Tax Burden: Tax Incidence

175. If the supply of a good is perfectly inelastic, then suppliers will bear the full burden of an excise tax

a.

no matter how elastic the demand for the good is.

b.

only if demand is perfectly elastic.

c.

only if demand is perfectly inelastic.

d.

only if the government forbids them to raise the price of the good.

DISC: Elasticity

United States – BPROG: Analytic

Shifting the Tax Burden: Tax Incidence

176. The incidence of a tax refers to

a.

who actually collects the tax.

b.

how frequently the tax is collected.

c.

who bears the economic burden of the tax.

d.

how the tax affects prices or wages.

United States – BPROG: Analytic

The study of economics, and defi – The study of economics, and definitions of economics

Shifting the Tax Burden: Tax Incidence

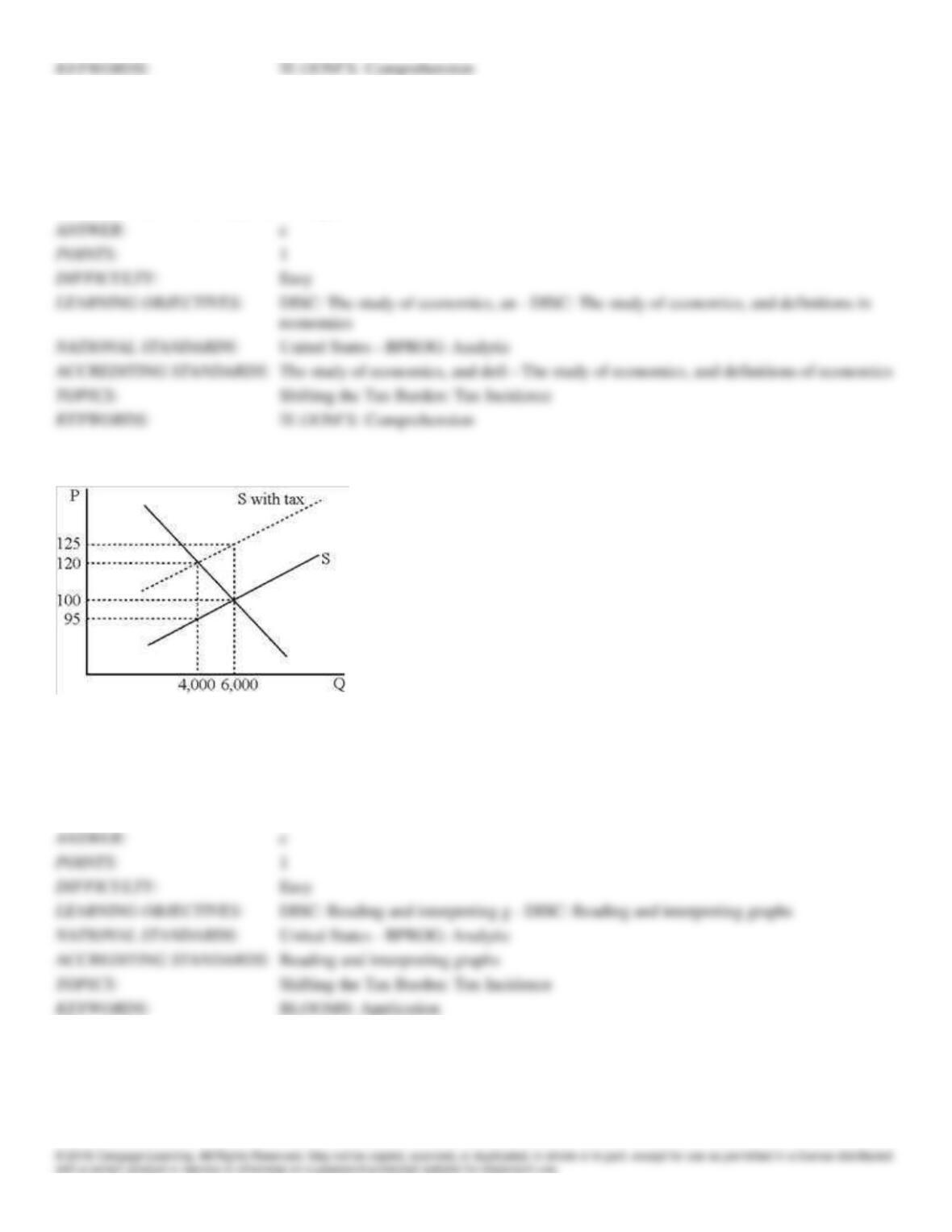

Figure 18-2

177. Figure 18-2 shows the widget market before and after an excise tax is imposed. The tax per widget equals ____.

a.

$5

b.

$20

c.

$25

d.

$30

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPROG: Analytic

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

BLOOMS: Application

178. Figure 18-2 shows the widget market before and after an excise tax is imposed. After the tax is imposed, the amount

that a firm keeps for itself from the sale of each widget is ____.

a.

$95

b.

$100

c.

$120

d.

$125

a

Easy

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPROG: Analytic

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

179. Figure 18-2 shows the widget market before and after an excise tax is imposed. The revenue collected by the tax is

____.

a.

$8,000

b.

$50,000

c.

$100,000

d.

$150,000

c

Moderate

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPROG: Reflective Thinking – BPROG: Analysis

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

180. Figure 18-2 shows the widget market before and after an excise tax is imposed. What percentage of the tax per

widget is borne by consumers, considering the true economic incidence of the tax?

a.

0 percent

b.

20 percent

c.

50 percent

d.

80 percent

Difficult

DISC: Reading and interpreting g – DISC: Reading and interpreting graphs

United States – BPRPOG: Analysis

Reading and interpreting graphs

Shifting the Tax Burden: Tax Incidence

181. On necessities, more of the incidence of tax is

a.

borne by the producer.

b.

borne by the consumer.

c.

shared equally between the producer and the consumer.

d.

None of the above is correct.