Chapter 16: GOVERNMENT REGULATION OF BUSINESS

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

Multiple Choice

16-1 Natural monopoly arises when

a. there is only one firm in the area.

b. there are high barriers to entry.

c. costs are subadditive.

d. it is more cost efficient to have multiple firms.

e. none of the above

16-2 An overallocation of resources in an industry means that for the last unit produced,

a. economic profit is negative but rising.

b. society places a higher value on the resources required to produce the last unit than the

value society places on consuming the last unit.

c. the demand price for the last unit exceeds the marginal cost of producing the last unit.

d. the marginal cost of production is falling.

e. the average cost is falling.

16-3 An underallocation of resources in an industry means that for the last unit produced,

a. economic profit is still rising.

b. society places a higher value on the resources required to produce the last unit than the

value society places on consuming the last unit.

c. the demand price for the last unit exceeds the marginal cost of producing the last unit.

d. the cost of producing the last unit exceeds its value to society.

e. long-run average cost is falling.

16-4 When social surplus is maximized in competitive equilibrium

a. marginal social benefit equals marginal social cost.

b. allocative and productive efficiency are achieved.

c. consumer surplus is maximized and producer surplus is minimized.

d. both a and b

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

e. all of the above

16-5 When we say that market prices allocate goods to the highest-valued users, we mean that

a. only consumers with higher incomes will get any of the good, while lower income

consumers get none of the good.

b. only consumers who value the good more than the market price of the good will choose

to buy the good.

c. government allocation of the good is warranted because government can make sure that

the good gets consumed by deserving individuals.

d. there is no shortage.

16-6 The less information consumers have about product quality,

a. the greater will be the loss of social surplus due to productive inefficiency.

b. the smaller will be the loss of social surplus due to productive inefficiency.

c. the greater will be the loss of social surplus due to allocative inefficiency.

d. the smaller will be the loss of social surplus due to allocative inefficiency.

16-7 Private provision of public goods fails to achieve economic efficiency because

a. the free rider problem causes overproduction of the good.

b. the free rider problem prevents collection of sufficient revenue.

c. the price of the privately supplied public good must exceed zero in order to be

allocatively efficient.

d. both a and c

e. both b and c

16-8 In long-run perfectly competitive equilibrium, economic efficiency is achieved because

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

a. price equals long-run marginal cost for every firm in the industry.

b. price equals average fixed cost for every firm in the industry.

c. price equals minimum long-run average cost for every firm in the industry.

d. both a and c

16-9 Firms with market power

a. face downward sloping average cost curves.

b. face downward sloping marginal cost curves.

c. produce where P = MR = MC.

d. maximize profit but fail to maximize social surplus.

16-10 When a competitively produced product has negative externalities in production, the industry will

a. overproduce the good because marginal social cost will exceed marginal social benefit in

competitive equilibrium.

b. overproduce the good because marginal private cost is less than marginal private benefit

in competitive equilibrium.

c. underproduce the good because marginal social cost will exceed marginal social benefit

in competitive equilibrium.

d. underproduce the good because marginal private social cost is less than marginal private

benefit in competitive equilibrium in competitive equilibrium.

16-11 Price is $50 and quantity demanded is 2,000 units at point A on a linear demand curve. The linear

supply curve intersects the demand curve at point B, which is at a price of $30 and 3,000 units.

Which of the following is true?

a. Moving from point A to point B causes consumer surplus to rise by $50,000.

b. Moving from point A to point B causes consumer surplus to rise by $10,000.

c. Moving from point B to point A causes consumer surplus to rise by $10,000.

d. Moving from point B to point A causes consumer surplus to rise by $50,000.

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

16-12 “Market power”

a. is the ability to lower costs and earn monopoly profits.

b. is the ability to raise price without losing all sales.

c. becomes “monopoly power” when the degree of market power is sufficiently high.

d. both a and b

e. both b and c

16-13 An underallocation of resources occurs when

a. marginal private benefit exceeds marginal social benefit.

b. a negative externality in production exists.

c. a positive externality in consumption exists.

d. All of these lead to underallocation of resources.

16-14 Market or monopoly power leads to market failure because

a. price exceeds marginal revenue, which causes the profit-maximizing firm to under-

produce the good or service.

b. price exceeds marginal revenue, which causes the profit-maximizing firm to over-

produce the good or service.

c. when MR = MC in profit-maximizing equilibrium, the value of the last unit produced is

less than the marginal cost of producing the last unit.

d. firms with market power have no incentive to produce on their expansion paths.

16-15 The Golden Gate bridge is not a pure public good because

a. the bridge is not a non-depletable good.

b. the bridge is non-depletable.

c. the free rider problem could be solved by using tolls.

d. the marginal cost of another car crossing the bridge is zero.

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

16-16 Common property resources lead to market failure because

a. poorly defined property rights result in too little of the resource being used by society.

b. poorly defined property rights reduce production costs.

c. poorly defined property rights create a deadweight loss.

d. the resource is overexploited and undersupplied.

16-17 When there is negative externality in production,

a. marginal social benefit exceeds marginal private benefit.

b. marginal private benefit exceeds marginal social benefit.

c. marginal social cost exceeds marginal private cost.

d. marginal private cost exceeds marginal social cost.

16-18 Which of the following is NOT a characteristic of natural monopoly?

a. Two or more firms experiencing economies of scale can produce the industry output at

lower total cost than if a single firm produces the industry output.

b. One firm can produce the industry output at a lower total cost than two or more firms.

c. One firm is the technically efficient way to organize production.

d. Production of the industry output is characterized by cost subadditivity.

16-19 As a policy option for regulating natural monopoly, marginal cost pricing is desirable because

a. consumers pay the lowest possible price that will generate sufficient revenue to cover the

costs of the natural monopolist.

b. allocative efficiency is achieved.

c. price is set equal to minimum long-run average cost.

d. all of the above.

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

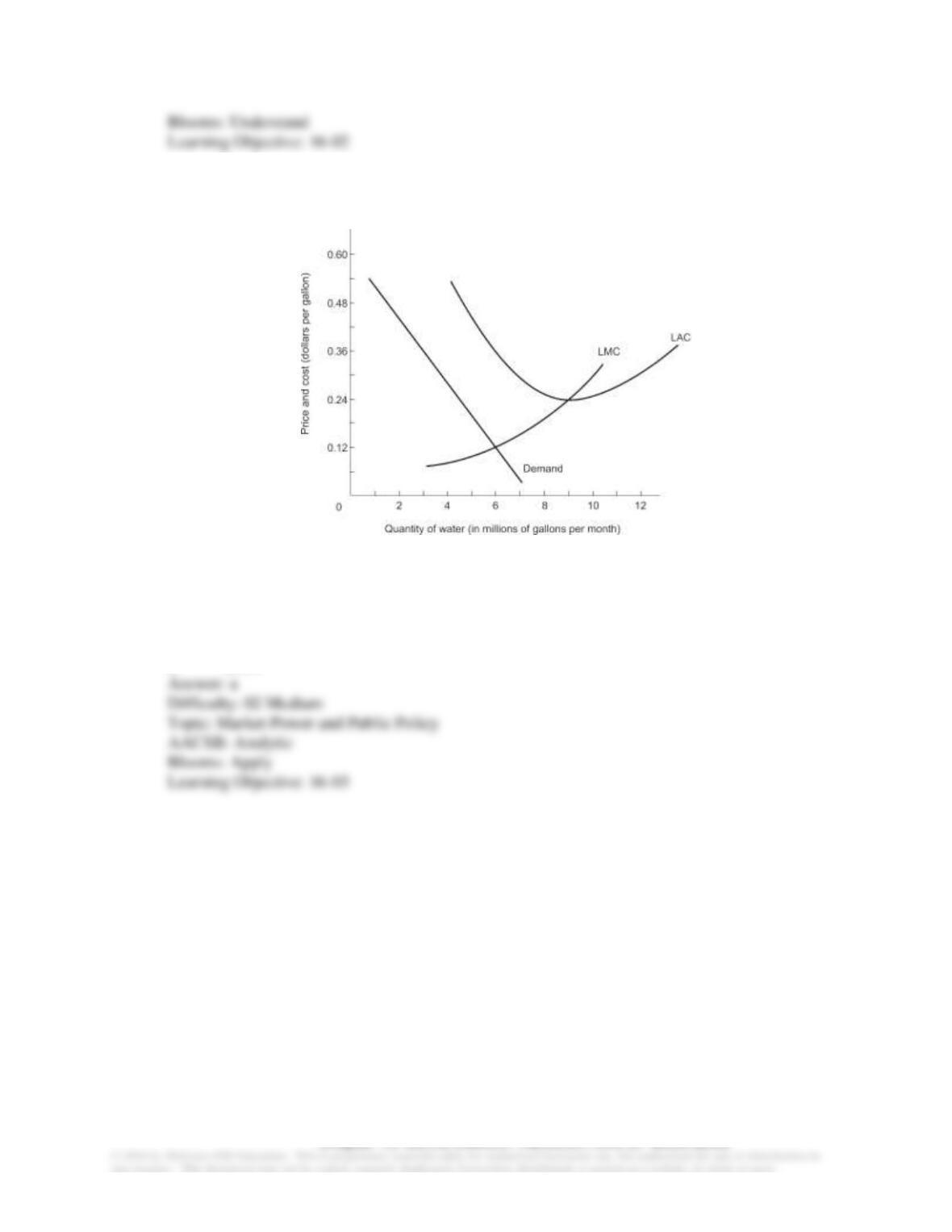

16-20 The cost and demand conditions for residential water consumption are shown below. If there are

450,000 residential water customers, then develop an optimal two-part pricing scheme and

answer the question.

The optimal usage fee to charge is _______ per gallon of water.

a. $0.12

b. $0.18

c. $0.24

d. $0.30

e. $0.36

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

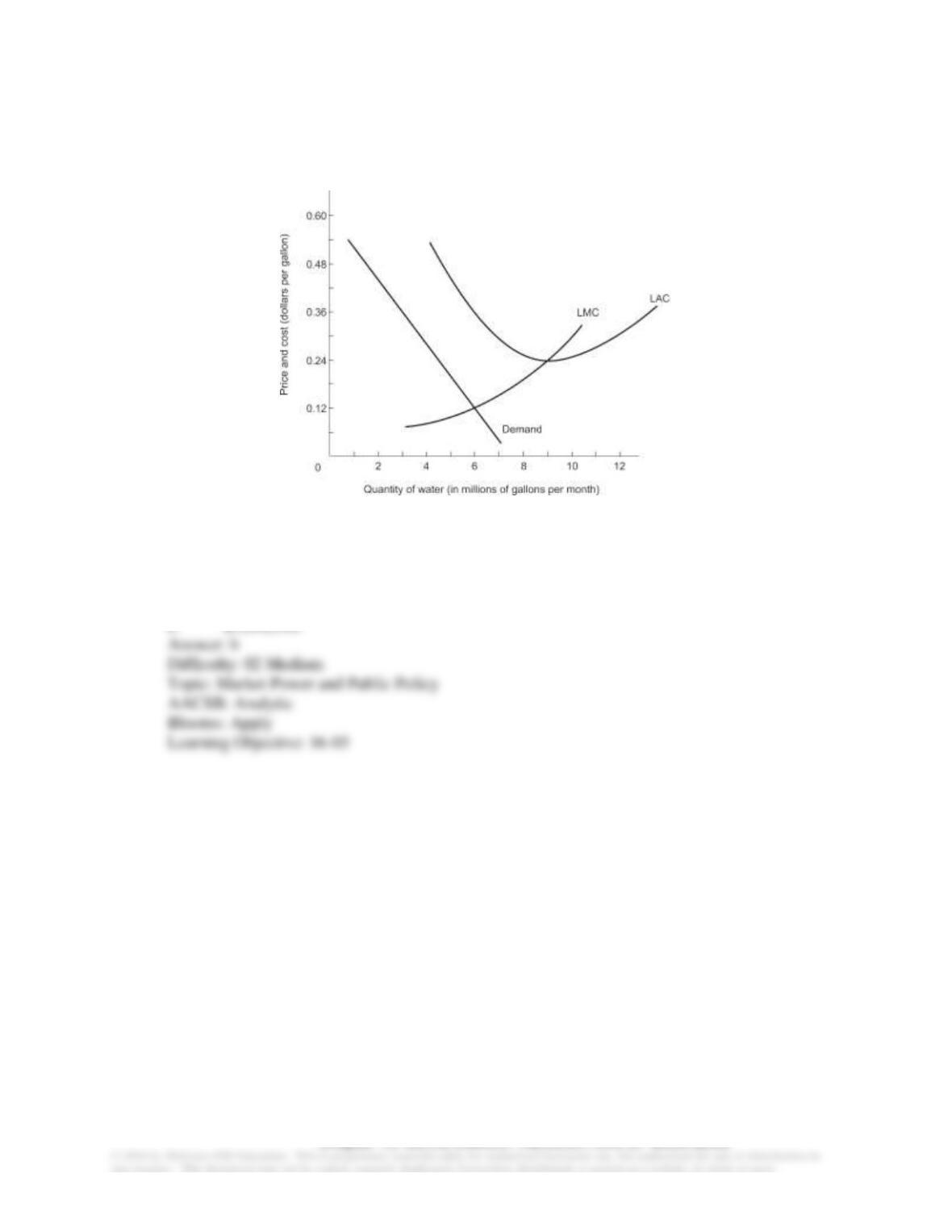

16-21 The cost and demand conditions for residential water consumption are shown below. If there are

450,000 residential water customers, then develop an optimal two-part pricing scheme and

answer the question.

At the optimal user fee, the water utility company will lose _______ per month.

a. $0

b. $1,440,000

c. $1,680,000

d. $2,400,000

e. $3,242,500

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

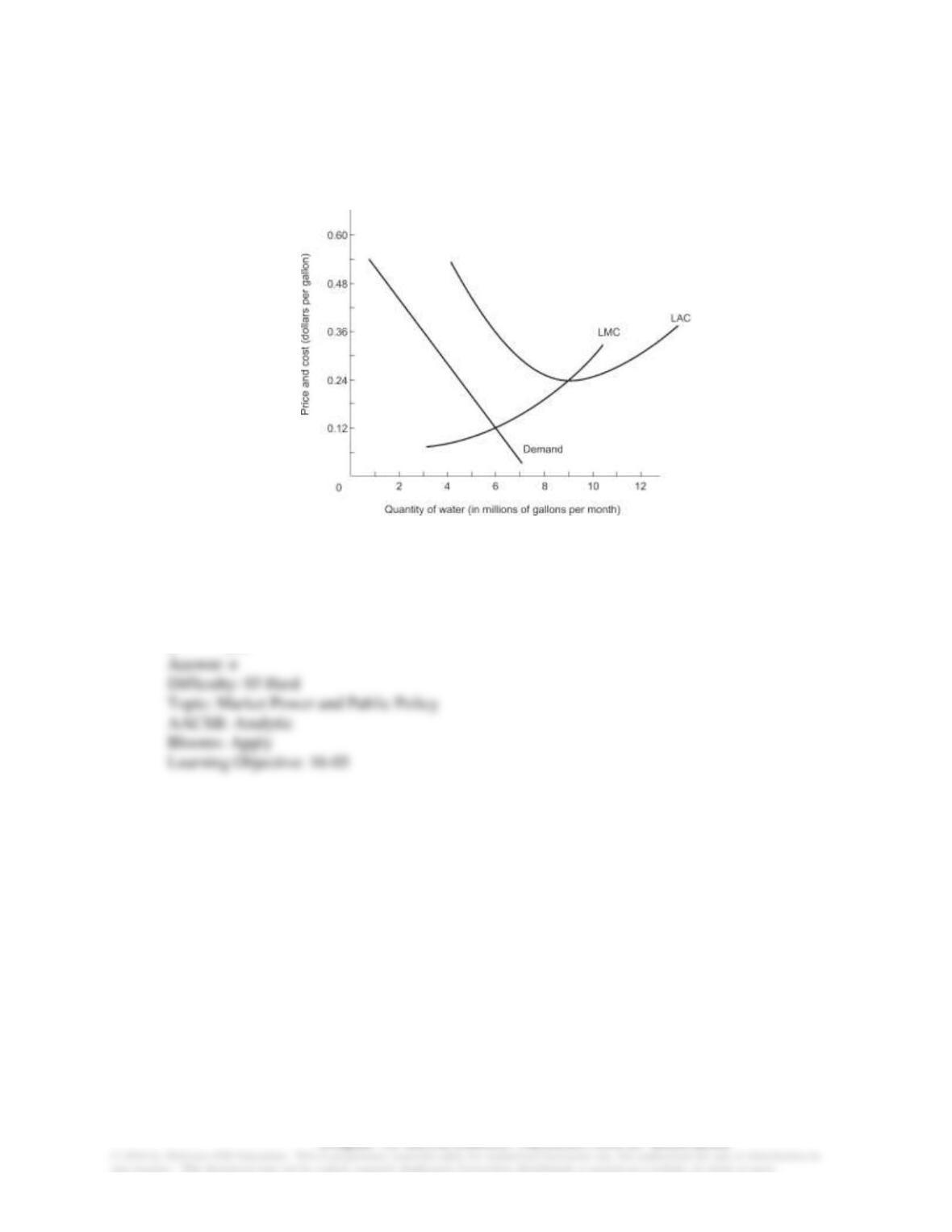

16-22 The cost and demand conditions for residential water consumption are shown below. If there are

450,000 residential water customers, then develop an optimal two-part pricing scheme and

answer the question.

The optimal monthly access charge per household is _______ per residence (per month).

a. $0.12

b. $0.18

c. $12

d. $24

e. $32

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

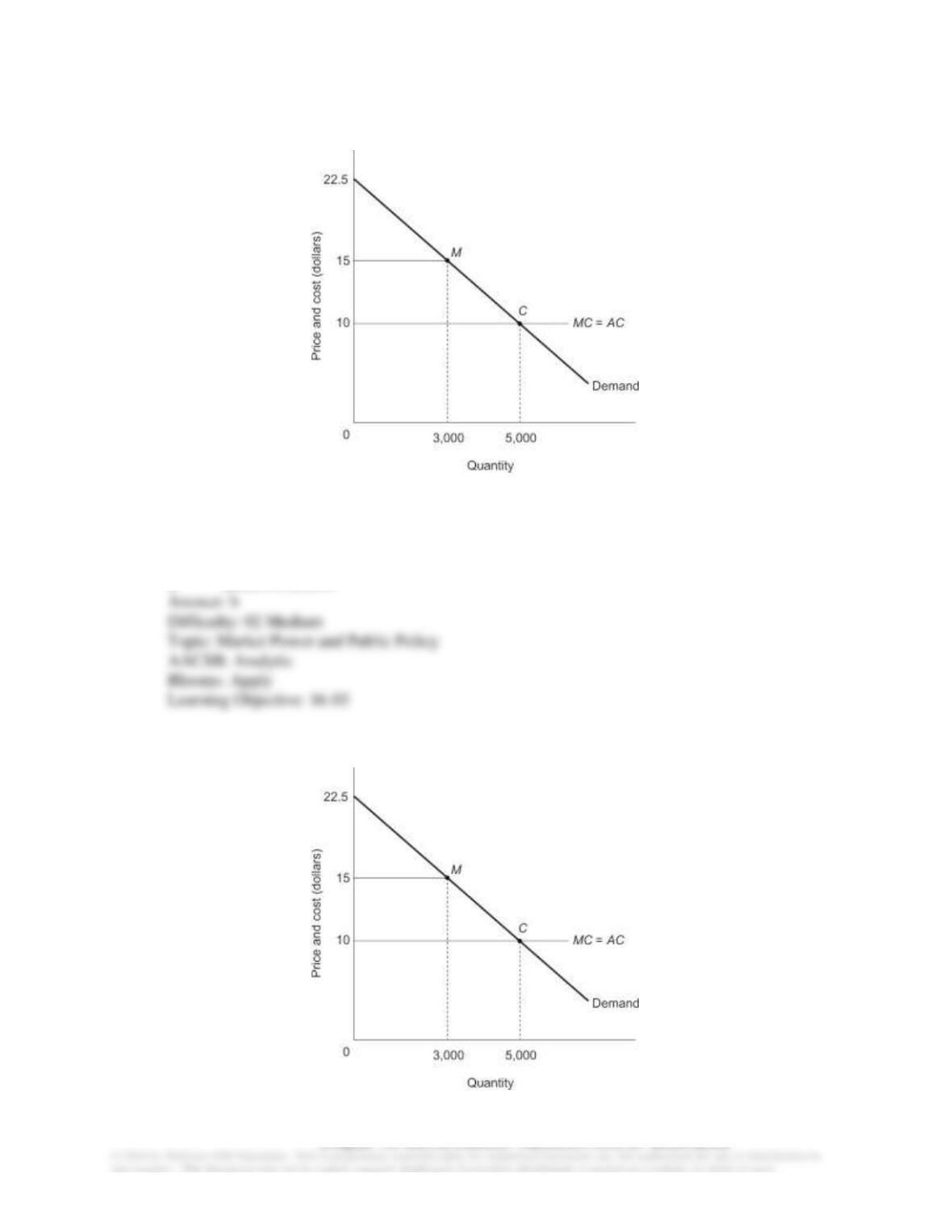

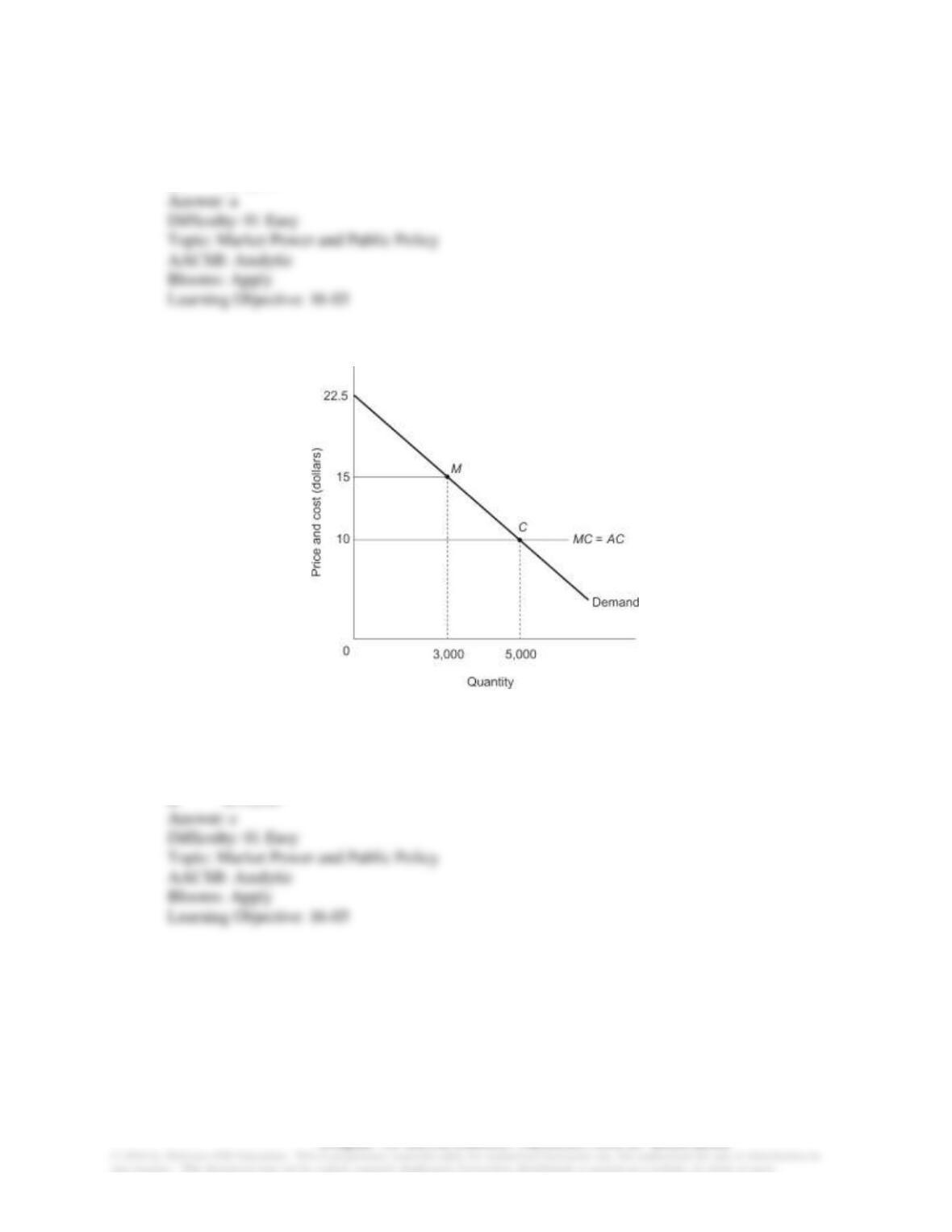

16-23 The figure below shows the result of a price fixing scheme that raised price above competitive

levels at point C to a price of $15 at point M.

By forming this price-fixing cartel, producers gained $__________ of producer surplus, while

consumers lost $__________ of consumer surplus.

a. $15,000; $10,000

b. $15,000; $20,000

c. $20,000; $10,000

d. $20,000; $5,000

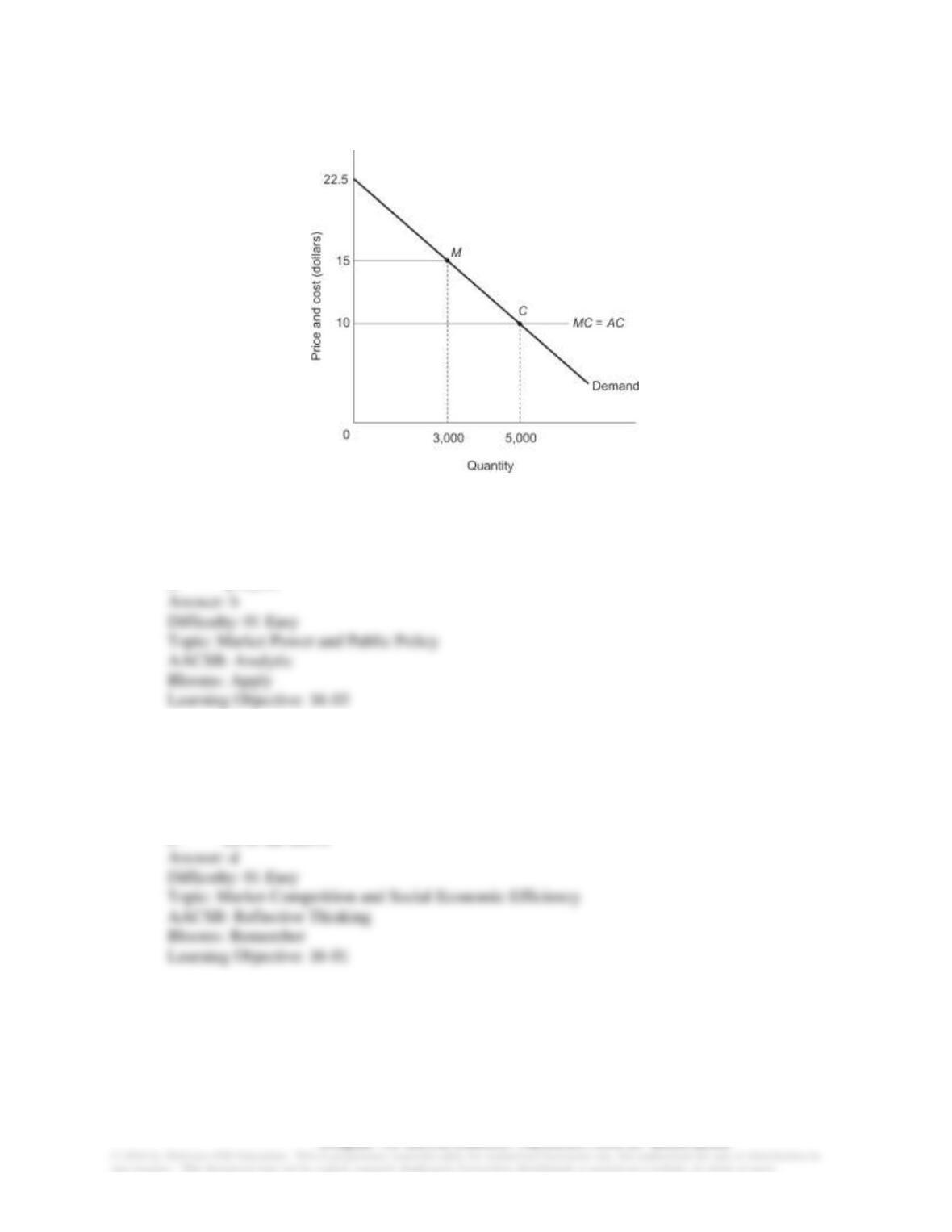

16-24 The figure below shows the result of a price fixing scheme that raised price above competitive

levels at point C to a price of $15 at point M.

The formation of this cartel caused a deadweight loss to society of $____________ of social

surplus.

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

a. $5,000

b. $15,000

c. $20,000

d. $31,250

16-25 The figure below shows the result of a price fixing scheme that raised price above competitive

levels at point C to a price of $15 at point M.

When antitrust enforcement agents break up this price-fixing cartel, consumers will gain

$__________ of consumer surplus.

a. $5,000

b. $15,000

c. $20,000

d. $31,250

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

16-26 The figure below shows the result of a price fixing scheme that raised price above competitive

levels at point C to a price of $15 at point M.

When antitrust enforcement agents break up this price-fixing cartel, producers will lose

$__________ of producer surplus.

a. $5,000

b. $15,000

c. $20,000

d. $31,250

16-27 Social economic efficiency means that the market is achieving

a. productive efficiency.

b. allocative efficiency.

c. maximum consumer surplus.

d. both a and b

e. all of the above

16-28 ___________ is/are example(s) of market failure that could justify government intervention.

a. Imperfect information

b. Public goods

c. A perfectly competitive bagel market

d. A dominant firm that undertakes pricing strategies aimed at maintaining high entry

barriers

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

e. only a, b, and d

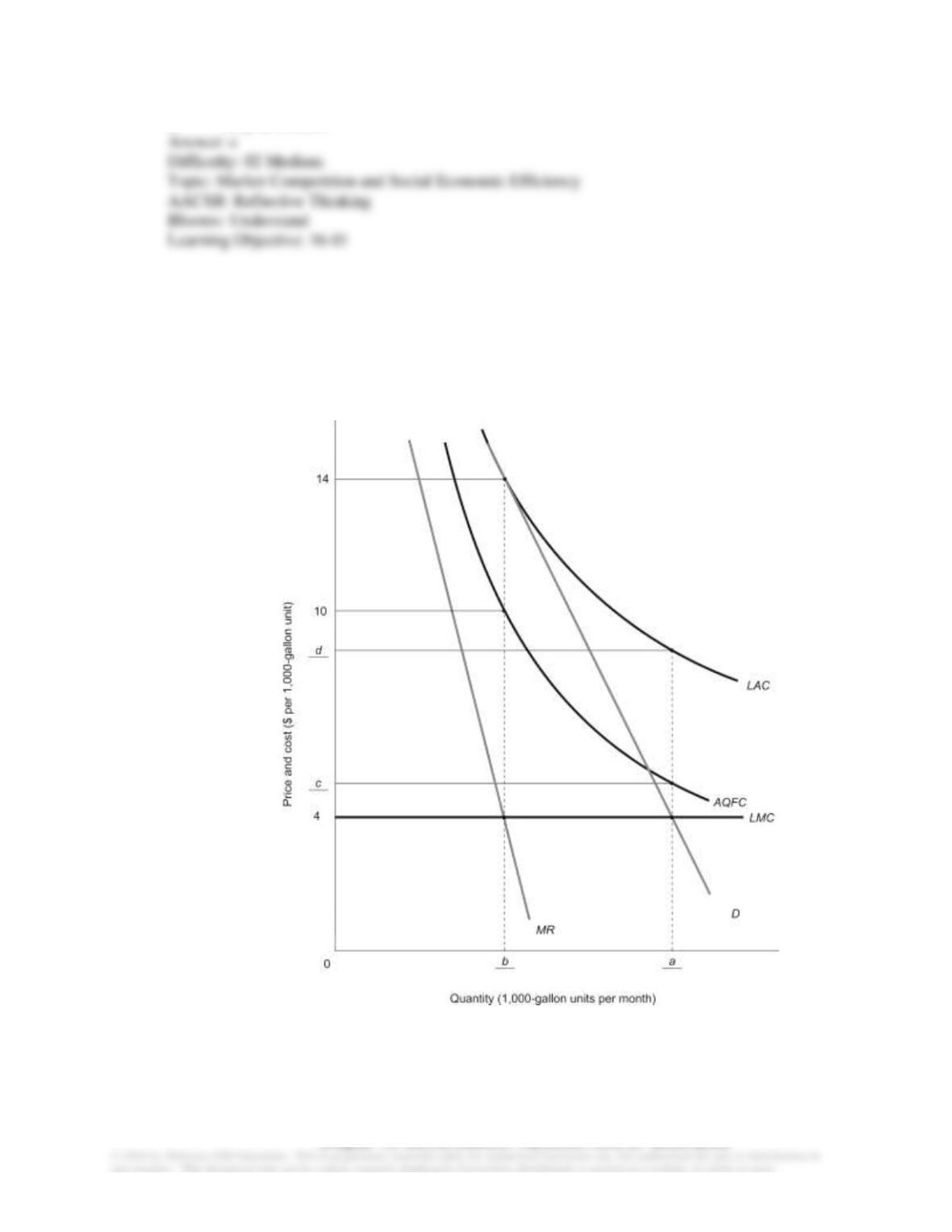

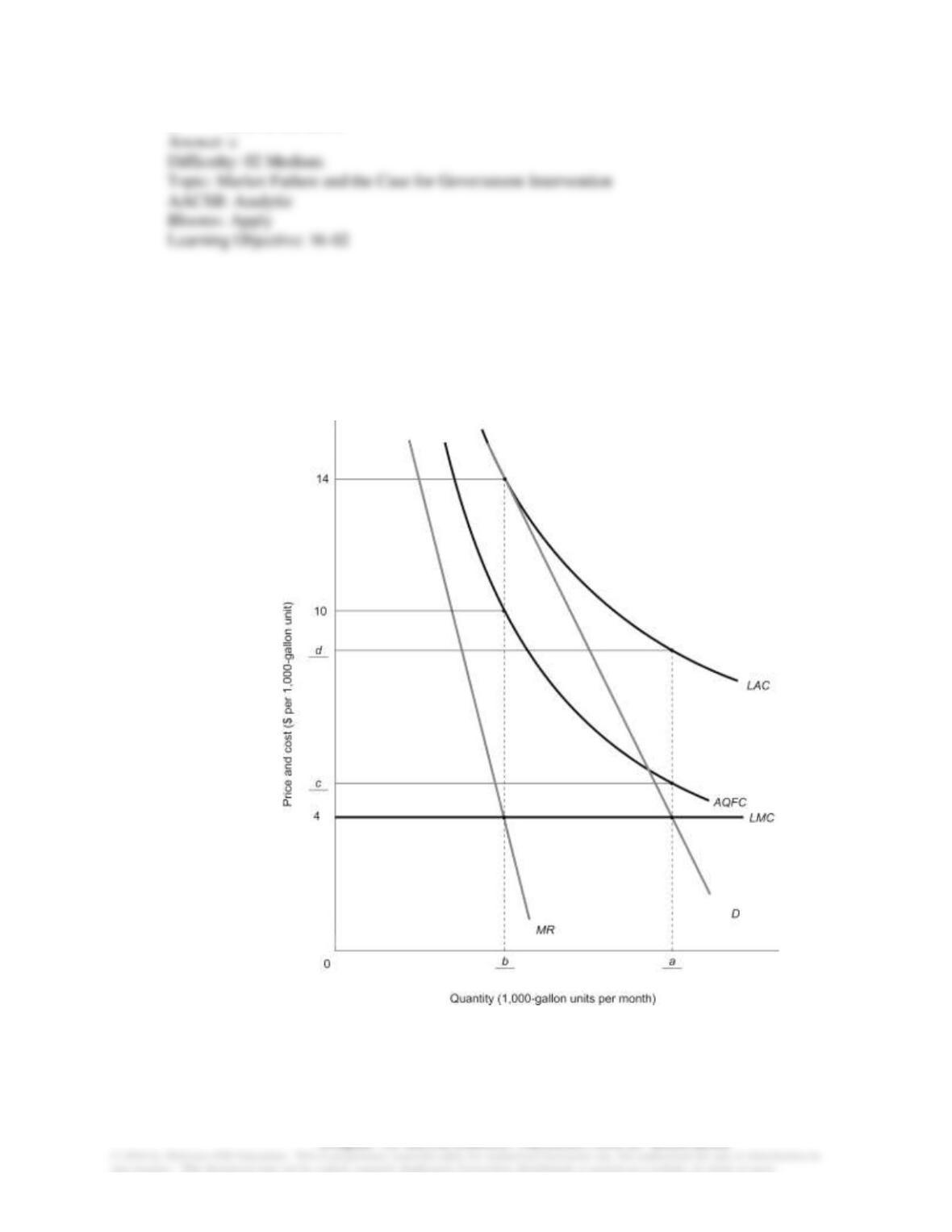

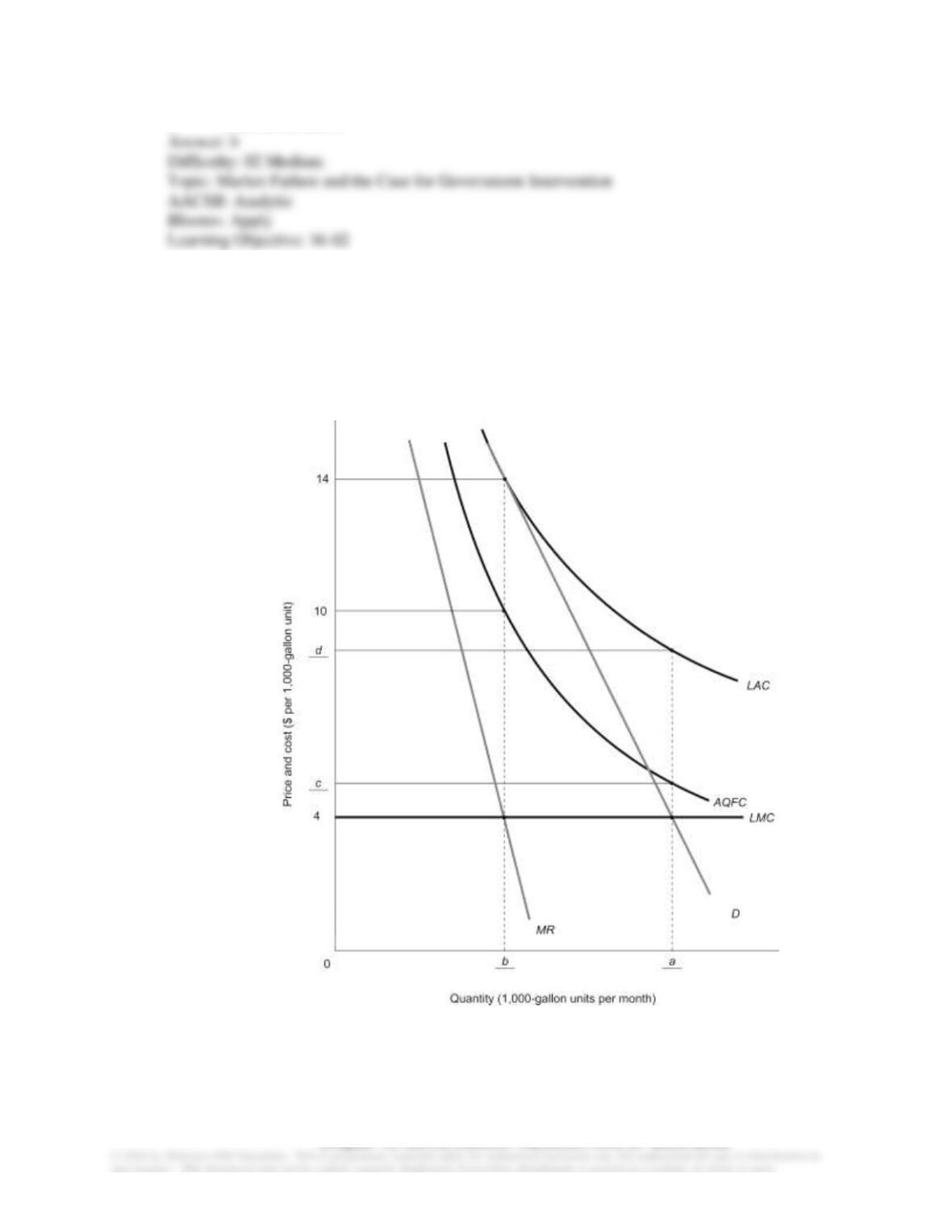

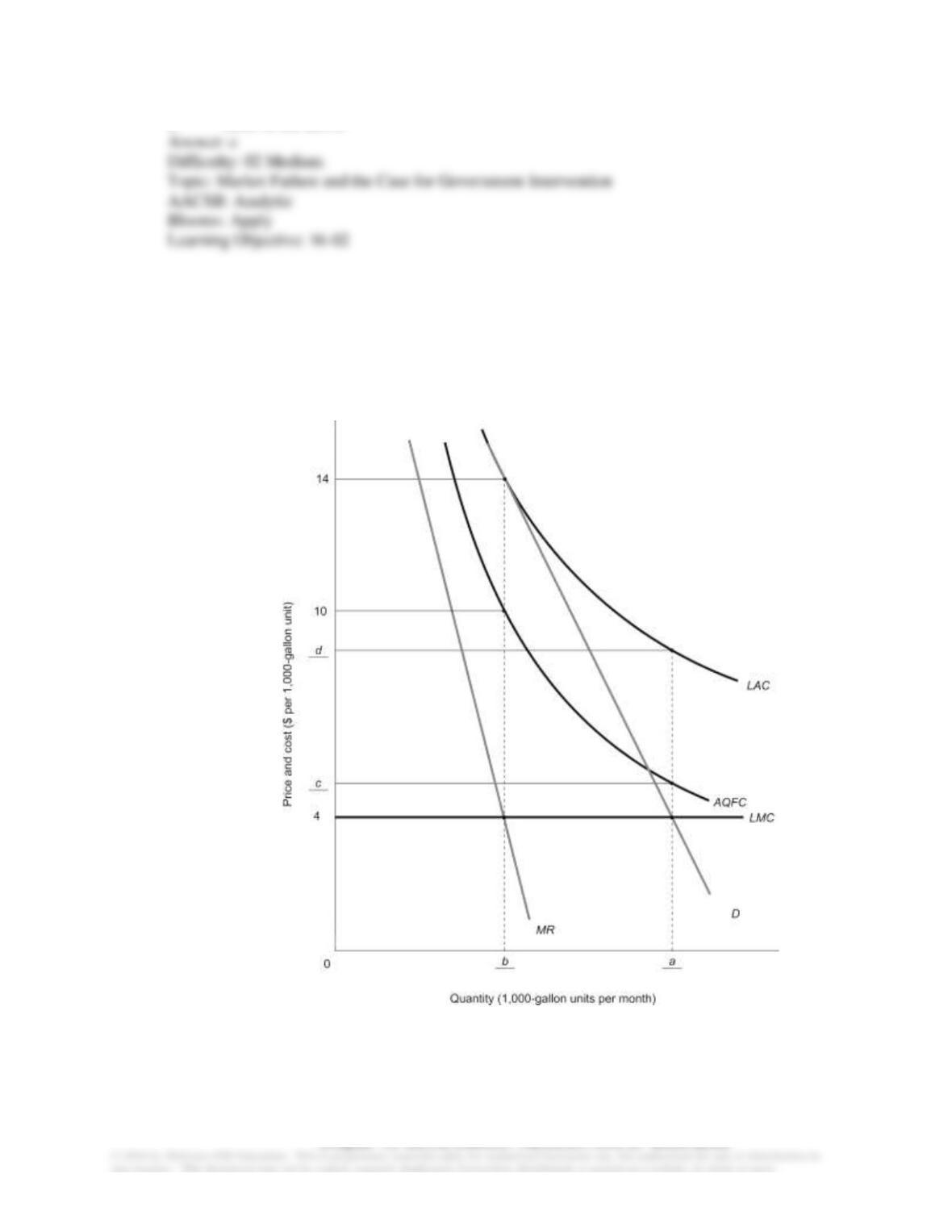

16-29 A municipal water utility employs quasi-fixed capital inputs—the water treatment plant and

distribution lines to homes—to supply water to 20,000 households in the community it serves.

The figure below shows the cost structure of this utility for various levels of water service.

Quantity of water consumption is measured in 1,000-gallon units per month. AQFC is the average

quasi-fixed cost curve, and LAC is long-run average cost. Long-run marginal cost, LMC, is

constant and equal to $4 per 1,000-gallon unit. The inverse demand equation is

P=24 –0.0004Qd

.

The value in blank a in the figure is ____.

a. 40,000

b. 45,000

c. 50,000

d. 55,000

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

e. none of the above

16-30 A municipal water utility employs quasi-fixed capital inputs—the water treatment plant and

distribution lines to homes—to supply water to 20,000 households in the community it serves.

The figure below shows the cost structure of this utility for various levels of water service.

Quantity of water consumption is measured in 1,000-gallon units per month. AQFC is the average

quasi-fixed cost curve, and LAC is long-run average cost. Long-run marginal cost, LMC, is

constant and equal to $4 per 1,000-gallon unit. The inverse demand equation is

P=24 –0.0004Qd

.

The value in blank b in the figure is ____.

a. 22,500

b. 25,000

c. 27,500

d. 30,000

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

e. none of the above

16-31 A municipal water utility employs quasi-fixed capital inputs—the water treatment plant and

distribution lines to homes—to supply water to 20,000 households in the community it serves.

The figure below shows the cost structure of this utility for various levels of water service.

Quantity of water consumption is measured in 1,000-gallon units per month. AQFC is the average

quasi-fixed cost curve, and LAC is long-run average cost. Long-run marginal cost, LMC, is

constant and equal to $4 per 1,000-gallon unit. The inverse demand equation is

P=24 –0.0004Qd

.

The value in blank c in the figure is ____.

a. $4.65

b. $4.75

c. $4.80

d. $5.50

Chapter 16: GOVERNMENT REGULATION OF BUSINESS

e. none of the above

16-32 A municipal water utility employs quasi-fixed capital inputs—the water treatment plant and

distribution lines to homes—to supply water to 20,000 households in the community it serves.

The figure below shows the cost structure of this utility for various levels of water service.

Quantity of water consumption is measured in 1,000-gallon units per month. AQFC is the average

quasi-fixed cost curve, and LAC is long-run average cost. Long-run marginal cost, LMC, is

constant and equal to $4 per 1,000-gallon unit. The inverse demand equation is

P=24 –0.0004Qd

.

The value in blank d in the figure is ____.

a. 6.50

b. 7.50

c. 8.00

d. 9.50