3) Purchasing power parity (PPP), postulates that the exchange rate between two countries equals the

ratio of the respective price indexes or ExchRate = (where ExchRate is the foreign exchange rate

between the two countries, and P represents the price index, with f indicating the foreign country). The

long–run version of PPP implies that that the exchange rate and the price ratio share a common trend.

(a) You collect monthly foreign exchange rate data from 1974:1 to 2002:4 for the U.S./U.K. exchange rate

($/£) and you collect data on the Consumer Price Index for both countries. Explain how you would used

the Engle–Granger test statistic to investigate the long–run PPP hypothesis.

(b) One of your peers explains that there may be an easier way to test for the validity of PPP. She

suggests to simply test whether or not the “real” exchange rate, or competitiveness, is stationary. (The

real exchange rate is given by ExchRate × ) Is she correct? Explain. How would you implement her

suggestion? Which alternative test–statistic is available?

4) You have collected quarterly Canadian data on the unemployment and the inflation rate from 1962:I to

2001:IV. You want to re–estimate the ADL(3,1) formulation of the Phillips curve using a GARCH(1,1)

specification. The results are as follows:

t = 1.17 – .56 ΔInft–1 – .47 ΔInft–2 – .31 ΔInft–3 – .13 Unempt–1

(.48) (.08) (.10) (.09) (.06)

= .86 + .27 + .53 .

(.40) (.11) (.15)

(a) Test the two coefficients for and in the GARCH model individually for statistical

significance.

(b) Estimating the same equation by OLS results in

t = 1.19 – .51 ΔInft–1 – .47 ΔInft–2 – .28 ΔInft–3 – .16Unempt–1

(.54) (.10) (.11) (.08) (.07)

Briefly compare the estimates. Which of the two methods do you prefer?

(c) Given your results from the test in (a), what can you say about the variance of the error terms in the

Phillips Curve for Canada?

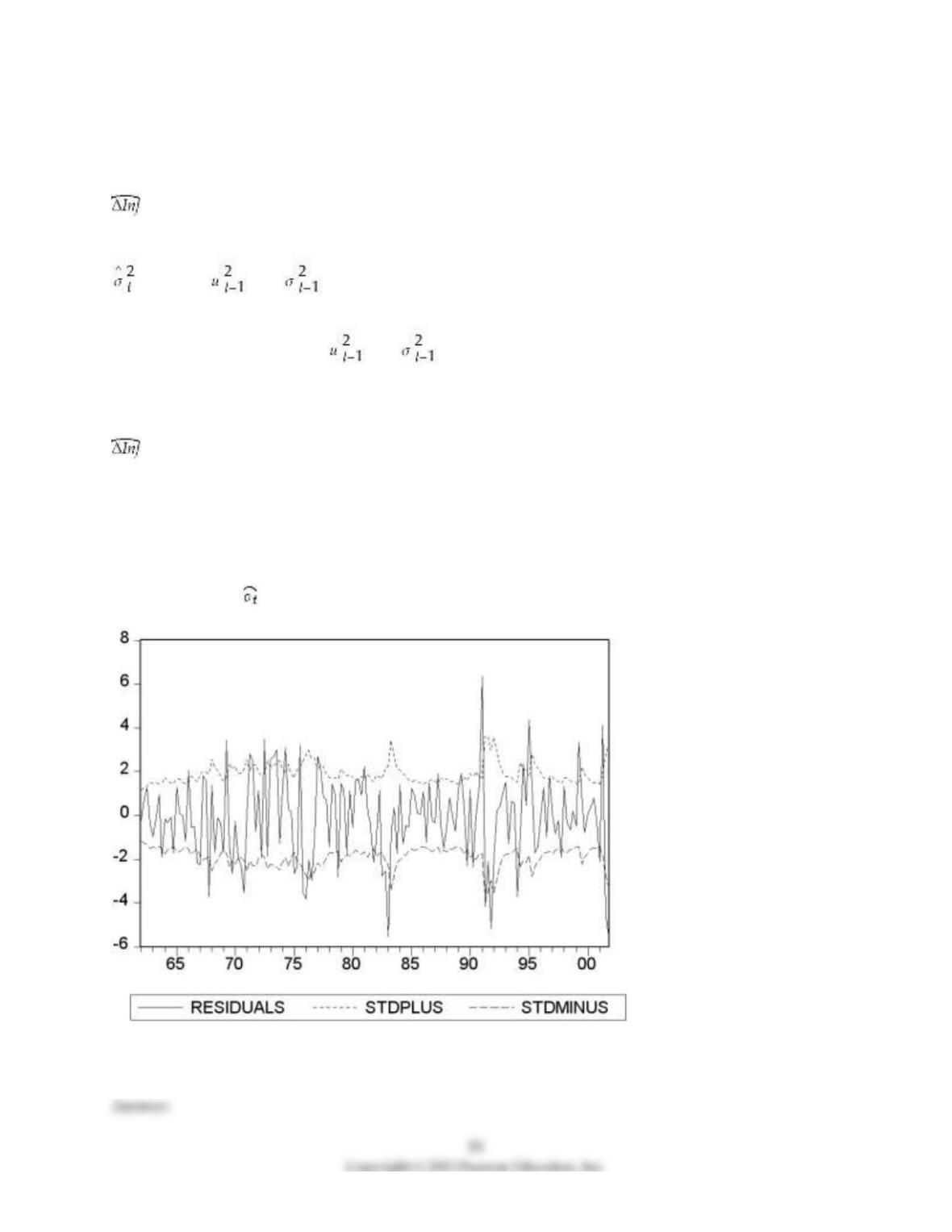

(d) The following figure plots the residuals along with bands of plus or minus one predicted standard

deviation (that is, ±) based on the GARCH(1,1) model.

Describe what you see.

17

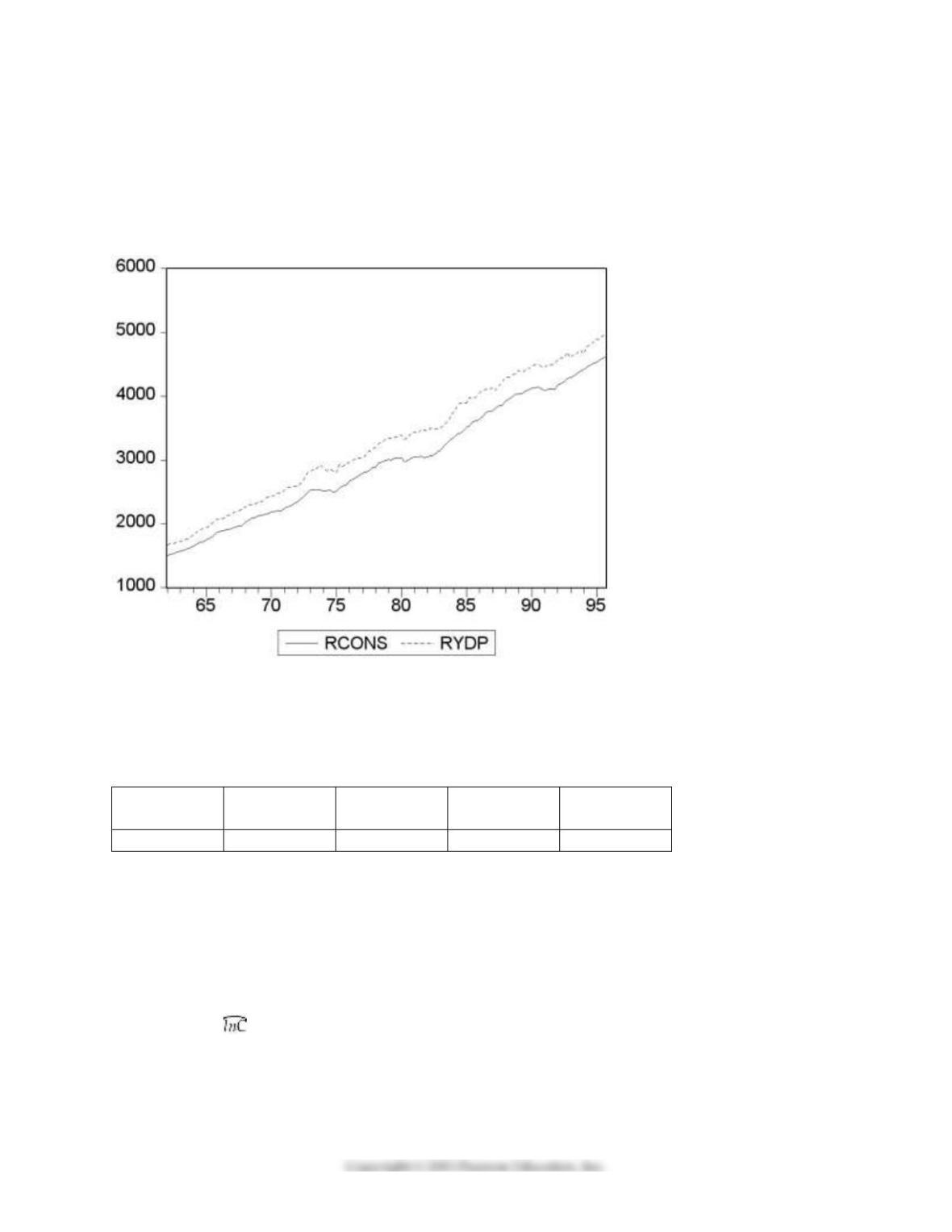

6) Your textbook states that there “are three ways to decide if two variables can plausibly be modeled as

cointegrated: use expert knowledge and economic theory, graph the series and see whether they appear

to have a common stochastic trend, and perform statistical tests for cointegration. All three ways should

be used in practice.” Accordingly you set out to check whether (the log of) consumption and (the log of)

personal disposable income are cointegrated. You collect data for the sample period 1962:I to 1995:IV and

plot the two variables.

(a) Using the first two methods to examine the series for cointegration, what do you think the likely

answer is?

(b) You begin your numerical analysis by testing for a stochastic trend in the variables, using an

Augmented Dickey–Fuller test. The t–statistic for the coefficient of interest is as follows:

Variable with

lag of 1

LnYpd

ΔLnYpd

LnC

ΔLnC

t–statistic

–1.93

–5.24

–2.20

–4.31

where LnYpd is (the log of) personal disposable income, and LnC is (the log of) real consumption. The

estimated equation included an intercept for the two growth rates, and, in addition, a deterministic trend

for the level variables. For each case make a decision about the stationarity of the variables based on the

critical value of the Augmented Dickey–Fuller test statistic. Why do you think a trend was included for

level variables?

(c) Using the first step of the EG–ADF procedure, you get the following result:

t = -0.24 + 1.017 lnYpdt

Should you interpret this equation? Would you be impressed if you were told that the regression R2 was

0.998 and that the t–statistic for the slope was 266.06? Why or why not?

(d) The Dickey–Fuller test for the residuals for the cointegrating regressions results in a t–statistic of

(-3.64). State the null and alternative hypothesis and make a decision based on the result.

(e) You want to investigate if the slope of the cointegrating vector is one. To do so, you use the DOLS

estimator and HAC standard errors. The slope coefficient is 1.024 with a standard error of 0.009. Can you

reject the null hypothesis that the slope equals one?

7) Your textbook so far considered variables for cointegration that are integrated of the same order. For

example, the log of consumption and personal disposable income might both be I(1) variables, and the

error correction term would be I(0), if consumption and personal disposable income were cointegrated.

(a) Do you think that it makes sense to test for cointegration between two variables if they are integrated

of different orders? Explain.

(b) Would your answer change if you have three variables, two of which are I(1) while the third is I(0)?

Can you think of an example in this case?

8) For the United States, there is somewhat conflicting evidence whether or not the inflation rate has a

unit autoregressive root. For example, for the sample period 1962:I to 1999:IV using the ADF statistic,

you cannot reject at the 5% significance level that inflation contains a stochastic trend. However the null

hypothesis can be rejected at the 10% significance level. The DF–GLS test rejects the null hypothesis at the

five percent level. This result turns out to be sensitive to the number of lags chosen and the sample

period.

(a) Somewhat intrigued by these findings, you decide to repeat the exercise using Canadian data. Letting

the AIC choose the lag length of the ADF regression, which turns out to be three, the ADF statistic is

(–1.91). What is your decision regarding the null hypothesis?

(b) You also calculate the DF–GLS statistic, which turns out to be (–1.23). Can you reject the null

hypothesis in this case?

(c) Is it possible for the two test statistics to yield different answers and if so, why?

9) You have collected time series for various macroeconomic variables to test if there is a single

cointegrating relationship among multiple variables. Formulate the null hypothesis and compare the EG–

ADF statistic to its critical value.

(a) Canadian unemployment rate, Canadian Inflation Rate, United States unemployment rate, United

States inflation rate; t = (–3.374).

(b) Approval of United States presidents (Gallup poll), cyclical unemployment rate, inflation rate,

Michigan Index of Consumer Sentiment; t = (–3.837).

(c) The log of real GDP, log of real government expenditures, log of real money supply (M2); t = (–2.23).

(d) Briefly explain how you could potentially improve on VAR(p) forecasts by using a cointegrating

vector.

10) There has been much talk recently about the convergence of inflation rates between many of the

OECD economies. You want to see if there is evidence of this closer to home by checking whether or not

Canada’s inflation rate and the United States’ inflation rate are cointegrated.

(a) You begin your numerical analysis by testing for a stochastic trend in the variables, using an

Augmented Dickey–Fuller test. The t–statistic for the coefficient of interest is as follows:

Variable with

lag of 1

InfCan

ΔInfCan

InfUS

ΔInfUS

t–statistic

–1.93

–6.38

–2.37

–5.63

where InfCan is the Canadian inflation rate, and InfUS is the United States inflation rate. The estimated

equation included an intercept. For each case make a decision about the stationarity of the variables based

on the critical value of the Augmented Dickey–Fuller test statistic.

(b) Your test for cointegration results in a EG–ADF statistic of (–7.34). Can you reject the null hypothesis

of a unit root for the residuals from the cointegrating regression?

(c) Using a working hypothesis that the two inflation rates are cointegrated, you want to test whether or

not the slope coefficient equals one. To do so you estimate the cointegrating equation using the DOLS

estimator with HAC standard errors. The coefficient on the U.S. inflation rate has a value of 0.45 with a

standard error of 0.13. Can you reject the null hypothesis that the slope equals unity?

(d) Even if you could not reject the null hypothesis of a unit slope, would that have been sufficient

evidence to establish convergence?

11) You have re–estimated the two variable VAR model of the change in the inflation rate and the

unemployment rate presented in your textbook using the sample period 1982:I (first quarter) to 2009:IV.

To see if the conclusions regarding Granger causality of changed, you conduct an F–test for this new

sample period. The results are as follows: The F–statistic testing the null hypothesis that the coefficients

on Unempt–1, Unempt–2, Unempt–3, and Unemplt–4 are zero in the inflation equation (Equation 16.5 in your

textbook) is 6.04. The F–statistic testing the hypothesis that the coefficients on the four lags of ΔInft are

zero in the unemployment equation (Equation 16.6 in your textbook) is 0.80.

a. What is the critical value of the F–statistic in both cases?

b. Do you think that the unemployment rate Granger–causes changes in the inflation rate?

c. Do you think that the change in the inflation rate Granger–causes the unemployment rate?

12) In this case, the Granger causality statistic does not exceed the critical value, and hence the conclusion

is that the change in the inflation rate does not Granger–cause the unemployment rate.

t = 0.05 – 0.31 ΔInft–1

(0.14) (0.07)

t = 1982:I – 2009:IV, R2 = 0.10, SER = 2.4

a. Calculate the one–quarter–ahead forecast of both ΔInf2010:I and Inf2010:I (the inflation rate in 2009:IV

was 2.6 percent, and the change in the inflation rate for that quarter was –1.04).

b. Calculate the forecast for 2010:II using the iterated multiperiod AR forecast both for the change in the

inflation rate and the inflation rate.

c. What alternative method could you have used to forecast two quarters ahead? Write down the

equation for the two–period ahead forecast, using parameters instead of numerical coefficients, which you

would have used.

13) You have collected quarterly data for real GDP (Y) for the United States for the period 1962:I (first

quarter) to 2009:IV.

a. Testing the log of GDP for stationarity, you run the following regression (where the lag length was

determined using the AIC):

t = 0.03 – 0.0024 lnYt–1 + 0.253 ΔlnYt–1 + 0.167 ΔlnYt–2

(0.03) (0.0014) (0.072) (0.072)

t = 1962:I – 2009:IV, R2 = 0.16, SER = 0.008

Use the ADF statistic with an intercept only to test for stationarity. What is your decision?

b. You have decided to test the growth rate of real GDP for stationarity for the same sample period. The

regression is as follows:

t = 0.0041 – 0.543 ΔlnYt–1 – 0.186 Δ2lnYt–1

(0.0009) (0.082) (0.071)

t = 1962:I – 2009:IV, R2 = 0.16, SER = 0.008

Use the ADF statistic with an intercept only to test for stationarity. What is your decision?

c. Using the orders of integration terminology, what order of integration is the log level of real GDP?

The growth rate?

d. Given that the SER hardly changed in the second equation, why is the regression R2 larger?

14) Economic theory suggests that the law of one price holds. Applying this concept to foreign and

domestic goods implies that goods will sell for the same price across countries. The consumer price index

is the price for a basket of goods, and is calculated for countries as a whole. Hence in the absence of

barriers to trade, and large transportation costs (and the fact that not all goods are traded) you should

observe Purchasing Power Parity (PPP) between two countries, or ExchRate × P = Pf, where ExchRate is

the foreign exchange rate between the two countries, and P represents the price index, with f indicating

the foreign country. Dividing both sides of the equation by the domestic price level then gives you the

standard formulation for PPP: ExchRate = . If PPP holds in the long run, then the exchange rate and

the price ratio should share a common trend. Since it is a long–run concept, cointegration provides an

interesting way to test for it.

a. Using monthly data for the U.S./U.K. exchange rate ($/₤) and the respective price indexes, you

estimate the following regression:

t = 0.44 + 0.69 (lnPUS – lnPUK)

Collecting the residuals from this regression and using an ADF test for cointegration, you find a t–statistic

of –2.71. Can you reject the null–hypothesis of no cointegration? What is the critical value?

b. Was it good econometric practice to test for cointegration right away? What else should you have

done before proceeding with the EG–ADF test?