80 ❖ Chapter 14/Firms in Competitive Markets

62. When firms in a perfectly competitive market face the same costs, in the long run they must be operating

a.

under diseconomies of scale.

b.

with small, but positive, levels of profit.

c.

at their efficient scale.

d.

where price is equal to average fixed cost.

63. Regardless of the cost structure of firms in a competitive market, in the long run

a.

firms will experience rising demand for their products.

b.

the marginal firm will earn zero economic profit.

c.

firms will experience a less competitive market environment.

d.

exit and entry is likely to lead to a horizontal long-run supply curve.

64. In a long-run equilibrium, the marginal firm has

a.

price equal to average total cost.

b.

total revenue equal to total cost.

c.

economic profit equal to zero.

d.

All of the above are correct.

65. In a long-run equilibrium, the marginal firm has

a.

price equal to minimum marginal cost.

b.

total revenue equal to total cost.

c.

accounting profit equal to zero.

d.

All of the above are correct.

66. In the long-run equilibrium of a market with free entry and exit, if all firms have the same cost structure, then

a.

marginal cost exceeds average total cost.

b.

the price of the good exceeds average total cost.

c.

average total cost exceeds the price of the good.

d.

firms are operating at their efficient scale.

67. In the long-run equilibrium of a market with free entry and exit, marginal firms are operating

a.

at the point where average variable cost equals marginal cost.

b.

at the minimum point on their marginal cost curves.

c.

at their efficient scale.

d.

where accounting profit is zero.

Chapter 14/Firms in Competitive Markets ❖ 81

68. Consider a competitive market with a large number of identical firms. The firms in this market do not use any

resources that are available only in limited quantities. In long-run equilibrium, market price is determined by

a.

the minimum point on the firms’ average variable cost curve.

b.

the minimum point on the firms’ average total cost curve.

c.

the portion of the marginal cost curve below average variable cost.

d.

a firm’s level of sunk costs.

69. If all firms have the same costs of production, then in long-run equilibrium,

a.

price exceeds average total cost for all firms.

b.

price exceeds marginal cost for all firms.

c.

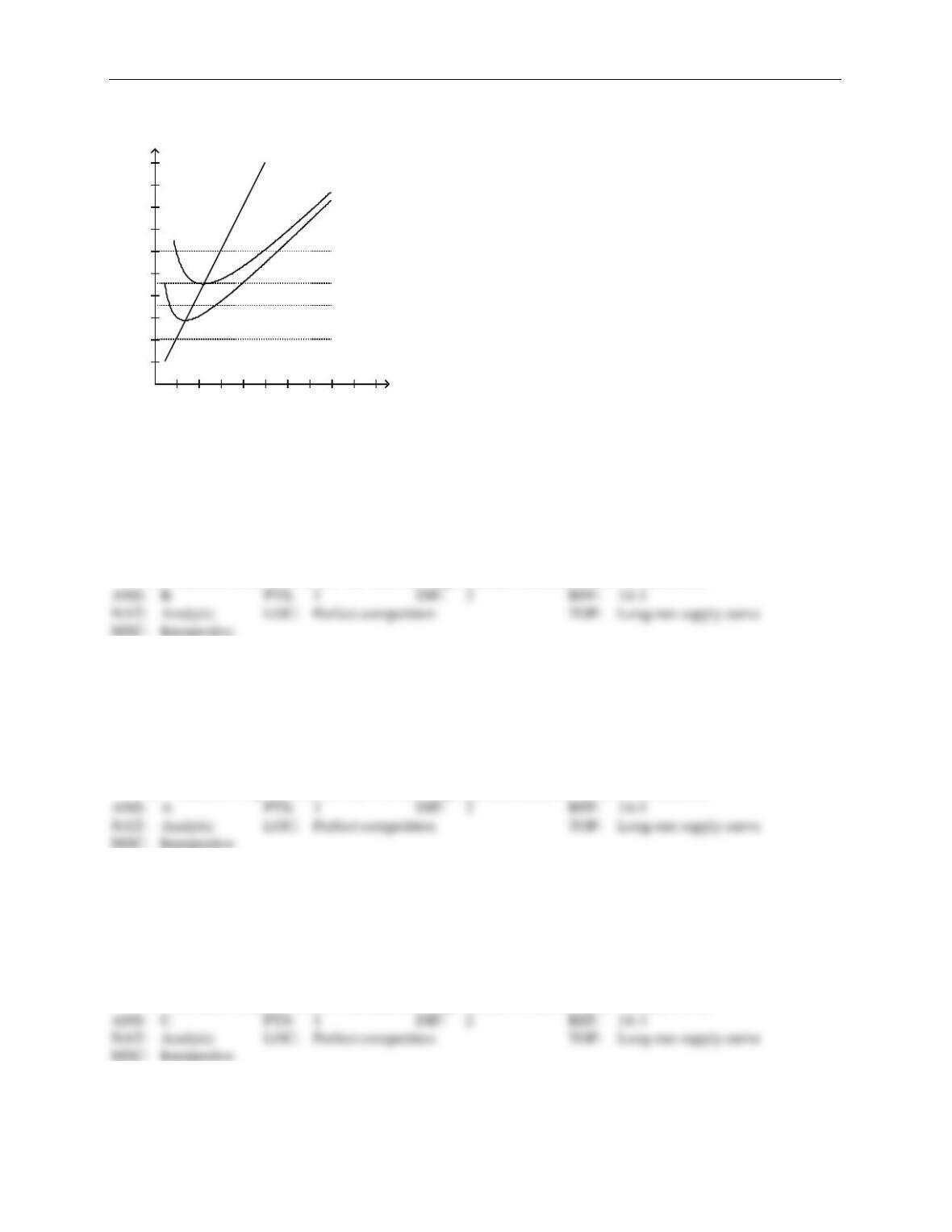

some firms may earn positive economic profits.

d.

all firms have zero economic profits and just cover their opportunity costs.

70. Suppose that firms in a competitive industry are earning positive economic profits. All else equal, in the long

run, we would expect the number of firms in the industry to

a.

increase.

b.

decrease.

c.

remain the same.

d.

We do not have enough information with which to answer this question.

71. Suppose that some firms in a competitive industry are earning zero economic profits, while others are experi-

encing losses. All else equal, in the long run, we would expect the number of firms in the industry to

a.

increase.

b.

decrease.

c.

remain the same.

d.

We do not have enough information with which to answer this question.

82 ❖ Chapter 14/Firms in Competitive Markets

Figure 14-13

Suppose a firm in a competitive industry has the following cost curves:

MC

ATC

AVC

P1

P3

P4

P2

1 2 3 4 5 6 7 8 Quantity

1

2

3

4

5

6

7

8

9

10 Price

72. Refer to Figure 14-13. If the price is P1 in the short run, what will happen in the long run?

a.

Nothing. The price is consistent with zero economic profits, so there is no incentive for firms to

enter or exit the industry.

b.

Individual firms will earn positive economic profits in the short run, which will entice other firms

to enter the industry.

c.

Individual firms will earn negative economic profits in the short run, which will cause some firms

to exit the industry.

d.

Because the price is below the firm’s average variable costs, the firms will shut down.

73. Refer to Figure 14-13. If the price is P2 in the short run, what will happen in the long run?

a.

Nothing. The price is consistent with zero economic profits, so there is no incentive for firms to

enter or exit the industry.

b.

Individual firms will earn positive economic profits in the short run, which will entice other firms

to enter the industry.

c.

Individual firms will earn negative economic profits in the short run, which will cause some firms

to exit the industry.

d.

Because the price is below the firm’s average variable costs, the firms will shut down.

74. Refer to Figure 14-13. If the price is P3 in the short run, what will happen in the long run?

a.

Nothing. The price is consistent with zero economic profits, so there is no incentive for firms to

enter or exit the industry.

b.

Individual firms will earn positive economic profits in the short run, which will entice other firms

to enter the industry.

c.

Individual firms will earn negative economic profits in the short run, which will cause some firms

to exit the industry.

d.

Because the price is below the firm’s average variable costs, the firms will shut down.

Chapter 14/Firms in Competitive Markets ❖ 83

75. Consider a competitive market with a large number of identical firms. The firms in this market do not use any

resources that are available only in limited quantities. In this market, an increase in demand will

a.

increase price in the short run but not in the long run.

b.

increase price in the long run but not in the short run.

c.

increase price both in the short and the long run.

d.

not affect price in either the short or the long run.

76. A competitive market is in long-run equilibrium. If demand decreases, we can be certain that price will

a.

fall in the short run. All firms will shut down, and some of them will exit the industry. Price will

then rise to reach the new long-run equilibrium.

b.

fall in the short run. No firms will shut down, but some of them will exit the industry. Price will

then rise to reach the new long-run equilibrium.

c.

fall in the short run. All, some, or no firms will shut down, and some of them will exit the industry.

Price will then rise to reach the new long-run equilibrium.

d.

not fall in the short run because firms will exit to maintain the price.

77. A competitive market is in long-run equilibrium. If demand increases, we can be certain that price will

a.

rise in the short run. Some firms will enter the industry. Price will then rise to reach the new long–

run equilibrium.

b.

rise in the short run. Some firms will enter the industry. Price will then fall to reach the new long-

run equilibrium.

c.

fall in the short run. All, some, or no firms will shut down, and some of them will exit the industry.

Price will then rise to reach the new long-run equilibrium.

d.

not rise in the short run because firms will enter to maintain the price.

78. In the transition from the short run to the long run, the number of firms in a competitive industry is

a.

fixed.

b.

increasing at a constant rate.

c.

decreasing.

d.

able to adjust to market conditions.

79. The long-run supply curve for a competitive industry

a.

may be horizontal if entry into the industry lowers average total cost.

b.

may be upward-sloping if higher-cost firms enter the industry.

c.

will be horizontal if there is free entry into the industry.

d.

will be upward-sloping if there are barriers to entry into the industry.

84 ❖ Chapter 14/Firms in Competitive Markets

80. The long-run supply curve for a competitive industry may be upward sloping if

a.

there are barriers to entry.

b.

firms that enter the industry are able to do so at lower average total costs than the existing firms in

the industry.

c.

some resources are available only in limited quantities.

d.

accounting profits are positive.

81. If all existing firms and all potential firms have the same cost curves, there are no inputs in limited quantities,

and the market is characterized by free entry and exit, then the long-run market supply curve

a.

is horizontal and equal to the minimum of long-run marginal cost for each firm.

b.

must slope downward.

c.

must slope upward.

d.

is horizontal and equal to the minimum of long-run average cost for each firm.

82. When all firms and potential firms in a market have the same cost curves, the long-run equilibrium of a com-

petitive market with free entry and exit will be characterized by firms

a.

earning small but positive economic profits.

b.

facing the prospect of future losses.

c.

operating at the efficient scale.

d.

that work together to raise market prices.

83. When entry and exit behavior of firms in an industry does not affect a firm’s cost structure,

a.

the long-run market supply curve must be horizontal.

b.

the long-run market supply curve must be upward-sloping.

c.

the long-run market supply curve must be downward-sloping.

d.

we do not have sufficient information to determine the shape of the long-run market supply curve.

84. When some resources used in production are only available in limited quantities, it is likely that the long-run

supply curve in a competitive market is

a.

downward sloping.

b.

upward sloping.

c.

horizontal.

d.

vertical.

Chapter 14/Firms in Competitive Markets ❖ 85

85. When a competitive market experiences an increase in demand that increases production costs for existing

firms and potential new entrants, which of the following is most likely to arise?

a.

The long-run market supply curve will be upward sloping.

b.

The condition of free entry into the market will be violated.

c.

Producer profits will fall in the long run.

d.

The long-run market supply curve will be horizontal as new firms enter and drive the price

downward.

86. When firms in a competitive market have different costs, it is likely that

a.

free entry and exit in the market will be violated.

b.

the market will no longer be considered competitive.

c.

long-run market supply will be downward sloping.

d.

some firms will earn positive economic profits in the long run.

87. A long-run supply curve is flatter than a short-run supply curve because

a.

firms can enter and exit a market more easily in the long run than in the short run.

b.

long-run supply curves are sometimes downward sloping.

c.

competitive firms have more control over demand in the long run.

d.

firms in a competitive market face identical cost structures.

88. A market might have an upward-sloping long-run supply curve if

a.

firms have different costs.

b.

consumers exercise market power over producers.

c.

all factors of production are essentially available in unlimited supply.

d.

the entry of new firms into the market has no effect on the cost structure of firms in the market.

89. When new entrants into a competitive market have higher costs than existing firms,

a.

accounting profits will be the primary determinant of entry into the market.

b.

sunk costs become an important determinant of the short-run entry strategy.

c.

market price will rise.

d.

long-run supply is constant.

90. Suppose a competitive market has a horizontal long-run supply curve and is in long-run equilibrium. If de-

mand decreases, we can be certain that in the short-run,

a.

at least some firms will shut down.

b.

price will fall below marginal cost for some firms.

c.

price will fall below average total cost for some firms.

d.

at least some firms will enter the industry.

86 ❖ Chapter 14/Firms in Competitive Markets

91. The long-run market supply curve in a competitive market will

a.

always be horizontal.

b.

be the portion of the MC that lies above the minimum of AVC for the marginal firm.

c.

typically be more elastic than the short-run supply curve.

d.

be above the competitive firm’s efficient scale.

92. In the long run the market supply

a.

must always be horizontal.

b.

could be upward sloping if the cost of production falls as new firms enter the market.

c.

could be upward sloping if the cost of production rises as new firms enter the market.

d.

could be upward sloping if technological improvements lower the cost of producing in the market.

93. Suppose that a competitive market is initially in equilibrium. Then demand increases. If some resources used

in production are not available in sufficient quantities for entering firms,

a.

the long-run market supply curve will be upward sloping.

b.

the long-run market supply curve will be perfectly elastic.

c.

in the long run firms will suffer economic losses, leading them to exit the industry.

d.

the number of firms will decrease, and the market will become a monopoly.

94. Suppose that a competitive market is initially in equilibrium. Then demand increases. If entering firms face

the same costs as existing firms and sufficient resources are available for entering firms,

a.

the long-run market supply curve will be upward sloping.

b.

the long-run market supply curve will be perfectly elastic.

c.

in the long run firms will suffer economic losses, leading them to exit the industry.

d.

the number of firms will decrease, and the market will become a monopoly.

Chapter 14/Firms in Competitive Markets ❖ 87

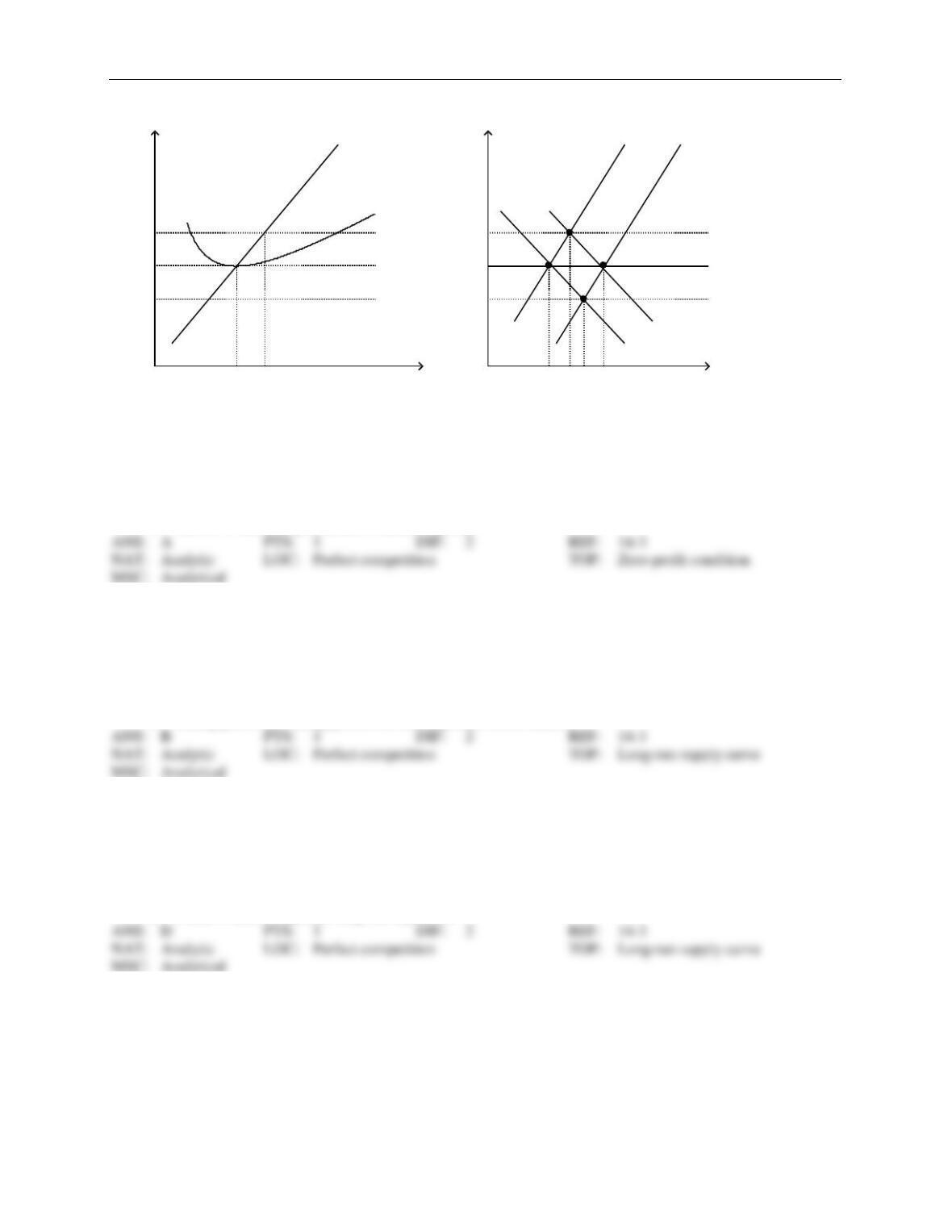

Figure 14-14

MC

ATC

P1

Q1

(a)

P0

P2

Q2

Quantity

Price

P1

QA

(b)

P0

P2

QCQBQD

S0 S1

D0

D1

A

B

C

D

Quantity

Price

95. Refer to Figure 14-14. When the market is in long-run equilibrium at point A in panel (b), the firm represent-

ed in panel (a) will

a.

have a zero economic profit.

b.

have a negative accounting profit.

c.

exit the market.

d.

choose to increase production to increase profit.

96. Refer to Figure 14-14. Assume that the market starts in equilibrium at point A in panel (b). An increase in

demand from D0 to D1 will result in

a.

a new market equilibrium at point D.

b.

an eventual increase in the number of firms in the market and a new long-run equilibrium at point

C.

c.

rising prices and falling profits for existing firms in the market.

d.

falling prices and falling profits for existing firms in the market.

97. Refer to Figure 14-14. Assume that the market starts in equilibrium at point A in panel (b) and that panel (a)

illustrates the cost curves facing individual firms. Suppose that demand increases from D0 to D1. Which of

the following statements is correct?

a.

Points A, B, and C represent both short-run and long-run equilibria.

b.

Points A, B, C, and D represent short-run equilibria.

c.

Points A and B represent long-run equilibria.

d.

Points A and C represent long-run equilibria.

88 ❖ Chapter 14/Firms in Competitive Markets

98. Refer to Figure 14-14. Assume that the market starts in equilibrium at point A in panel (b) and that panel (a)

illustrates the cost curves facing individual firms. Suppose that demand increases from D0 to D1. Which of

the following statements is not correct?

a.

Point A is a long-run equilibrium point.

b.

Points A, B, and C are short-run equilibria points.

c.

Point B is a long-run equilibrium point.

d.

Point C is a long-run equilibrium point.

99. Refer to Figure 14-14. If the market starts in equilibrium at point C in panel (b), a decrease in demand will

ultimately lead to

a.

more firms in the industry but lower levels of output for each firm.

b.

fewer firms in the market.

c.

a new long-run equilibrium at point D in panel (b).

d.

lower prices once the new long-run equilibrium is reached.

100. Refer to Figure 14-14. Suppose a firm in a competitive market, like the one depicted in panel (a), observes

market price rising from P1 to P2. Which of the following could explain this observation?

a.

The entry of new firms into the market.

b.

The exit of existing consumers from the market.

c.

An increase in market supply from S0 to S1.

d.

An increase in market demand from D0 to D1.

1. The production decisions of perfectly competitive firms follow one of the Ten Principles of Economics, which

states that rational people

a.

consider sunk costs.

b.

equate prices to the average costs of production.

c.

prefer to purchase products from smaller rather than larger firms.

d.

think at the margin.

2. If firms are competitive and profit maximizing, the price of a good equals the

a.

marginal cost of production.

b.

fixed cost of production.

c.

total cost of production.

d.

average total cost of production.

Chapter 14/Firms in Competitive Markets ❖ 89

3. Profit maximizing firms in competitive industries with free entry and exit face a price equal to the lowest pos-

sible

a.

marginal cost of production.

b.

fixed cost of production.

c.

total cost of production.

d.

average total cost of production.

TRUE/FALSE

1. For a firm operating in a perfectly competitive industry, total revenue, marginal revenue, and average revenue

are all equal.

2. For a firm operating in a perfectly competitive industry, marginal revenue and average revenue are equal.

3. If a firm notices that its average revenue equals the current market price, that firm must be participating in a

competitive market.

4. For a firm operating in a competitive market, both marginal revenue and average revenue exceed the market

price.

5. A profit-maximizing firm in a competitive market will increase production when average revenue exceeds

marginal cost.

6. A profit-maximizing firm in a competitive market will decrease production when marginal cost exceeds aver-

age revenue.

7. Because there are many buyers and sellers in a perfectly competitive market, no one seller can influence the

market price.

8. In competitive markets, firms that raise their prices are typically rewarded with larger profits.

90 ❖ Chapter 14/Firms in Competitive Markets

9. When an individual firm in a competitive market increases its production, it is likely that the market price will

fall.

10. When an individual firm in a competitive market decreases its production, it is likely that the market price will

rise.

11. In a competitive market, firms are unable to differentiate their product from that of other producers.

12. Firms in a competitive market are said to be price takers because there are many sellers in the market, and the

goods offered by the firms are very similar if not identical.

13. The two characteristics of a competitive market are 1) many buyers and sellers in the market and 2) the goods

offered by the various sellers are highly differentiated.

14. Firms operating in perfectly competitive markets try to maximize profits.

15. Because there are many sellers in a competitive market, individual firms are unable to maximize profits.

16. A firm’s incentive to compare marginal revenue and marginal cost is an application of the principle that ration-

al people think at the margin.

17. By comparing the marginal revenue and marginal cost from each unit produced, a firm in a competitive mar-

ket can determine the profit-maximizing level of production.

18. Firms operating in perfectly competitive markets produce an output level where marginal revenue equals mar-

ginal cost.

Chapter 14/Firms in Competitive Markets ❖ 91

19. A firm is currently producing 100 units of output per day. The manager reports to the owner that producing

the 100th unit costs the firm $5. The firm can sell the 100th unit for $4.75. The firm should continue to pro-

duce 100 units in order to maximize its profits (or minimize its losses).

20. A firm is currently producing 100 units of output per day. The manager reports to the owner that producing

the 100th unit costs the firm $5. The firm can sell the 100th unit for $5. The firm should continue to produce

100 units in order to maximize its profits (or minimize its losses).

21. A firm is currently producing 100 units of output per day. The manager reports to the owner that producing

the 100th unit costs the firm $5. The firm can sell the unit for $6. The firm should produce more than 100

units in order to maximize its profits (or minimize its losses).

22. All firms maximize profits by producing an output level where marginal revenue equals marginal cost; for

firms operating in perfectly competitive industries, maximizing profits also means producing an output level

where price equals marginal cost.

23. When a profit-maximizing firm in a competitive market experiences rising prices, it will respond with an in-

crease in production.

24. A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if

the market price is less than that firm’s average total cost but greater than the firm’s average variable cost.

25. A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if

the market price is less than that firm’s average variable cost but greater than the firm’s average fixed cost.

26. A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if

the market price is less than that firm’s average variable cost.

27. A firm operating in a perfectly competitive industry will shut down in the short run but earn losses if the mar-

ket price is less than that firm’s average variable cost.

92 ❖ Chapter 14/Firms in Competitive Markets

28. In the short run, a firm should exit the industry if its marginal cost exceeds its marginal revenue.

29. The supply curve of a firm in a competitive market is the average variable cost curve above the minimum of

marginal cost.

30. A firm will shut down in the short run if revenue is not sufficient to cover its variable costs of production.

31. Suppose a firm is considering producing zero units of output. We call this shutting down in the short run and

exiting an industry in the long run.

32. Suppose a firm is considering producing zero units of output. We call this exiting an industry in the short run

and shutting down in the long run.

33. A firm will shut down in the short run if revenue is not sufficient to cover all of its fixed costs of production.

34. A firm operating in a competitive market will stay in business in the short run so long as the market price ex-

ceeds the firm’s average total cost; otherwise, the firm will shut down.

35. In the short run, if the market price is below the firm’s average total cost of production, the firm will always

shut down.

36. The marginal firm in a competitive market will earn zero economic profit in the long run.

37. A profit-maximizing firm in a competitive market will earn zero accounting profits in the long run.

Chapter 14/Firms in Competitive Markets ❖ 93

38. A miniature golf course is a good example of where fixed costs become relevant to the decision of when to

open and when to close for the season.

39. A popular resort restaurant will maximize profits if it chooses to stay open during the less–crowded “off sea-

son” when its total revenues exceed its variable costs.

40. A popular resort restaurant will maximize profits if it chooses to stay open during the less–crowded “off sea-

son” when its total revenues exceed its fixed costs.

41. A dairy farmer must be able to calculate sunk costs in order to determine how much revenue the farm receives

for the typical gallon of milk.

42. Because nothing can be done about sunk costs, they are irrelevant to decisions about business strategy.

43. The manager of a firm operating in a competitive market can ignore sunk costs when making business deci-

sions.

44. In the long run, when price is less than average total cost for all possible levels of production, a firm in a com-

petitive market will choose to exit (or not enter) the market.

45. In the long run, when price is greater than average total cost, some firms in a competitive market will choose

to enter the market.

46. In the long run, a firm should exit the industry if its total costs exceed its total revenues.

47. A competitive firm’s profit will be increasing as long as marginal revenue is greater than marginal cost.

94 ❖ Chapter 14/Firms in Competitive Markets

48. In making a short-run profit-maximizing production decision, the firm must consider both fixed and variable

cost.

49. A firm operating in a perfectly competitive industry will continue to operate if it earns zero economic profits

because it is likely to be earning positive accounting profits.

50. A firm operating in a perfectly competitive market may earn positive, negative, or zero economic profit in the

long run.

51. A firm operating in a perfectly competitive market may earn positive, negative, or zero economic profit in the

short run.

52. A firm operating in a perfectly competitive industry will shut down in the short run if its economic profits fall

to zero because it is likely to be earning negative accounting profits.

53. A firm operating in a perfectly competitive market earns zero economic profit in the long run but remains in

business because the firm’s revenues cover the business owners’ opportunity costs.

54. A competitive market will typically experience entry and exit until accounting profits are zero.

55. The long-run equilibrium in a competitive market characterized by firms with identical costs is generally char-

acterized by firms operating at efficient scale.

56. In the long run, a competitive market with 1,000 identical firms will experience an equilibrium price equal to

the minimum of each firm’s average total cost.

Chapter 14/Firms in Competitive Markets ❖ 95

57. In a long-run equilibrium where firms have identical costs, it is possible that some firms in a competitive mar-

ket are making a positive economic profit.

58. When economic profits are zero in equilibrium, the firm’s revenue must be sufficient to cover all opportunity

costs.

59. The stable, long-run equilibrium in a competitive market occurs when the market price equals the lowest point

on a firm’s average total cost curve.

60. All competitive firms earn zero economic profit in both the short run and the long run.

61. When a resource used in the production of a good sold in a competitive market is available in only limited

quantities, the long-run supply curve is likely to be upward sloping.

62. The short-run supply curve in a competitive market must be more elastic than the long-run supply curve.

63. The long-run supply curve in a competitive market is more elastic than the short-run supply curve.

64. If some resources used in the production of a good are only available in limited quantities, then the long run

market supply curve will be perfectly elastic.

MSC: Interpretive

SHORT ANSWER

1. Describe the difference between average revenue and marginal revenue. Why are both of these revenue

measures important to a profit-maximizing firm?

96 ❖ Chapter 14/Firms in Competitive Markets

2. List and describe the characteristics of a perfectly competitive market.

3. Why would a firm in a perfectly competitive market always choose to set its price equal to the current market

price? If a firm set its price below the current market price, what effect would this have on the market?

4. Use a graph to demonstrate the circumstances that would prevail in a competitive market where firms are earn-

ing economic profits. Can this scenario be maintained in the long run? Explain your answer.

5. Explain how a firm in a competitive market identifies the profit-maximizing level of production. When should

the firm raise production, and when should the firm lower production?

6. News reports from the western United States occasionally report incidents of cattle ranchers slaughtering a

large number of newborn calves and burying them in mass graves rather than transporting them to markets.

Chapter 14/Firms in Competitive Markets ❖ 97

Assuming that this is rational behavior by profit-maximizing “firms,” explain what economic factors may in-

fluence such behavior.

7. Use a graph to demonstrate the circumstances that would prevail in a perfectly competitive market where

firms are experiencing economic losses. Identify costs, revenue, and the economic losses on your graph. Using

your graph, determine whether an individual firm will shut down in the short run, or choose to remain in the

market. Explain your answer.

8. At its current level of production a profit-maximizing firm in a competitive market receives $12.50 for each

unit it produces and faces an average total cost of $10. At the market price of $12.50 per unit, the firm’s mar-

ginal cost curve crosses the marginal revenue curve at an output level of 1,000 units. What is the firm’s current

profit? What is likely to occur in this market and why?

9. Give two reasons why the long-run industry supply curve may slope upward. Use an example to demonstrate

your reasons.

98 ❖ Chapter 14/Firms in Competitive Markets

10. If identical firms that remain in a competitive market over the long run make zero economic profit, why do

these firms choose to remain in the market?