76) Which of the following is TRUE regarding the long run for a firm in monopolistic

competition?

A) P = ATC = MC = MR

B) P = ATC

C) ATC = MC

D) P = MC

77) Which of the following is TRUE regarding the long run for a firm in monopolistic

competition?

A) P = MC = ATC

B) P = MC = MR

C) ATC = MC = MR

D) P = ATC

78) In the long run, a monopolistically competitive firm ________ make an economic profit and

a monopoly ________ make an economic profit.

A) can; can

B) can; cannot

C) cannot; can

D) cannot; cannot

79) In monopolistically competitive industries

A) entry and exit push economic profits toward zero.

B) there is no diversity of products.

C) firms do not respond to changes in demand.

D) firms produce where marginal cost equals the marginal benefit to the consumers.

80) In a monopolistically competitive industry

A) firms can make an economic profit in the long run because of barriers to entry.

B) the firms can never make an economic profit.

C) if firms are making an economic profit, new firms enter the industry.

D) firms can make an economic profit in the long run because of product differentiation.

81) When new firms enter a monopolistically competitive industry, each existing firm’s

A) demand curve shifts rightward.

B) demand curve shifts leftward.

C) marginal cost curve shifts rightward.

D) marginal cost curve shifts leftward.

82) If firms in a monopolistically competitive industry are making an economic profit, then

definitely there is

A) a leftward shift in each firm’s demand curve as new firms enter the market.

B) a rightward shift in each firm’s marginal revenue curve as new firms enter the market.

C) an upward shift in each firm’s cost curves as new firms enter the market.

D) All of the above answers are correct.

83) If firms monopolistically competitive firms are making an economic profit, as new firms

enter the market, each of the existing firms’ demand curve shifts ________, the marginal curve

shifts ________, and the profit-maximizing quantity ________.

A) leftward; leftward; decreases

B) rightward; leftward; increases

C) leftward; rightward; decreases

D) leftward; leftward; increases

84) A monopolistically competitive firm is making a positive economic profit. In the long run,

which of the following is most likely?

A) It will produce less output and it will charge a lower price.

B) It will produce the same output and charge the same price.

C) It will produce less output but keep price the same.

D) It will keep output the same but will charge a higher price.

85) In the long run, monopolistically competitive firms make zero economic profit because of

A) excess capacity.

B) product variety.

C) easy entry and exit.

D) government regulation.

86) If in monopolistic competition in the short run, firms make ________ profits, then in the long

run, new firms will enter the market. The ________ each individual firm’s product will

________. In the new long-run equilibrium firms will make ________ profit.

A) economic; demand for; decrease; zero economic

B) normal; demand for; increase; zero economic

C) economic; supply of; decrease; an economic

D) economic; supply of; increase; zero economic

87) In long-run equilibrium, a firm in monopolistic competition makes

A) an economic profit but the economic profit is less than it would be if the firm was a

monopoly.

B) an economic profit that is higher than what it would be if the firm was a monopoly.

C) zero economic profit.

D) an economic profit that is the same amount as it would be if the firm was a monopoly.

88) Which of the following is TRUE regarding the long run for a firm in monopolistic

competition?

A) The firm’s price equals its marginal cost.

B) The firm’s economic profit equals zero.

C) The firm’s average total cost is minimized.

D) The firm’s marginal cost equals its average total cost.

89) In the long run, all firms in a monopolistically competitive industry make

A) negative accounting profit.

B) zero accounting profit.

C) an economic profit.

D) zero economic profit.

90) In the long run, a firm in monopolistic competition will

A) make a negative economic profit, that is, an economic loss.

B) make zero economic profit, that is, a normal profit.

C) make a positive economic profit.

D) None of the above answers is necessarily correct because the amount of the profit or loss

depends on the slope of the demand curve.

91) In the long run, in monopolistic competition

A) a firm’s price equals its marginal cost.

B) firms make an economic profit.

C) firms make zero economic profit.

D) Both answers A and C are correct.

92) Which of the following is TRUE regarding the long run for a firm in monopolistic

competition?

A) The firm’s economic profit equals zero.

B) There are barriers to entry.

C) Price exceeds average total cost.

D) Marginal revenue is less than marginal cost.

93) In the long run, monopolistically competitive firms are ________ to perfectly competitive

firms because ________.

A) similar; both firms produce at the minimum ATC

B) similar; both firms make zero economic profit

C) not similar; monopolistically competitive firms set P = MC to maximize profits

D) not similar; monopolistically competitive firms can make an economic profit and perfectly

competitive firms cannot

94) Which one of the following statements is TRUE for BOTH perfect competition and

monopolistic competition?

A) Each type of firm faces a downward sloping demand curve.

B) Each type of firm produces a homogeneous product.

C) In the long run, firms in both industries make zero economic profit.

D) Each type of firm competes on product quality and price.

95) Which of the following is TRUE regarding the long run for a firm in monopolistic

competition?

A) The firm’s economic profit equals zero.

B) Marginal revenue equals marginal cost.

C) Price exceeds marginal cost.

D) All of the above are true.

96) A monopolistically competitive firm is similar to

A) a monopoly in the short run because it can make an economic profit in the short run and is

similar to a perfectly competitive firm in the long run because it cannot make a positive

economic profit.

B) a perfectly competitive firm in the short run because it cannot make an economic profit in the

short run and is similar to a monopoly in the long run because it can make an economic profit.

C) a monopoly because it can make an economic profit in both the short run and long run.

D) a perfectly competitive firm because its economic profit is equal to zero in both the short run

and long run.

97) In monopolistic competition, in the long run customers pay a price that is

A) less than the minimum ATC.

B) more than the minimum ATC.

C) equal to both the minimum ATC and the minimum AVC.

D) equal to the minimum ATC, but not equal to the minimum AVC.

98) In the long run, a monopolistically competitive firm’s price equals

A) its average total cost and its marginal cost.

B) its average total cost but not its marginal cost.

C) its marginal cost but not its average total cost.

D) neither marginal cost nor its average total cost.

99) In the long run, a firm in a monopolistically competitive industry has its price equal to its

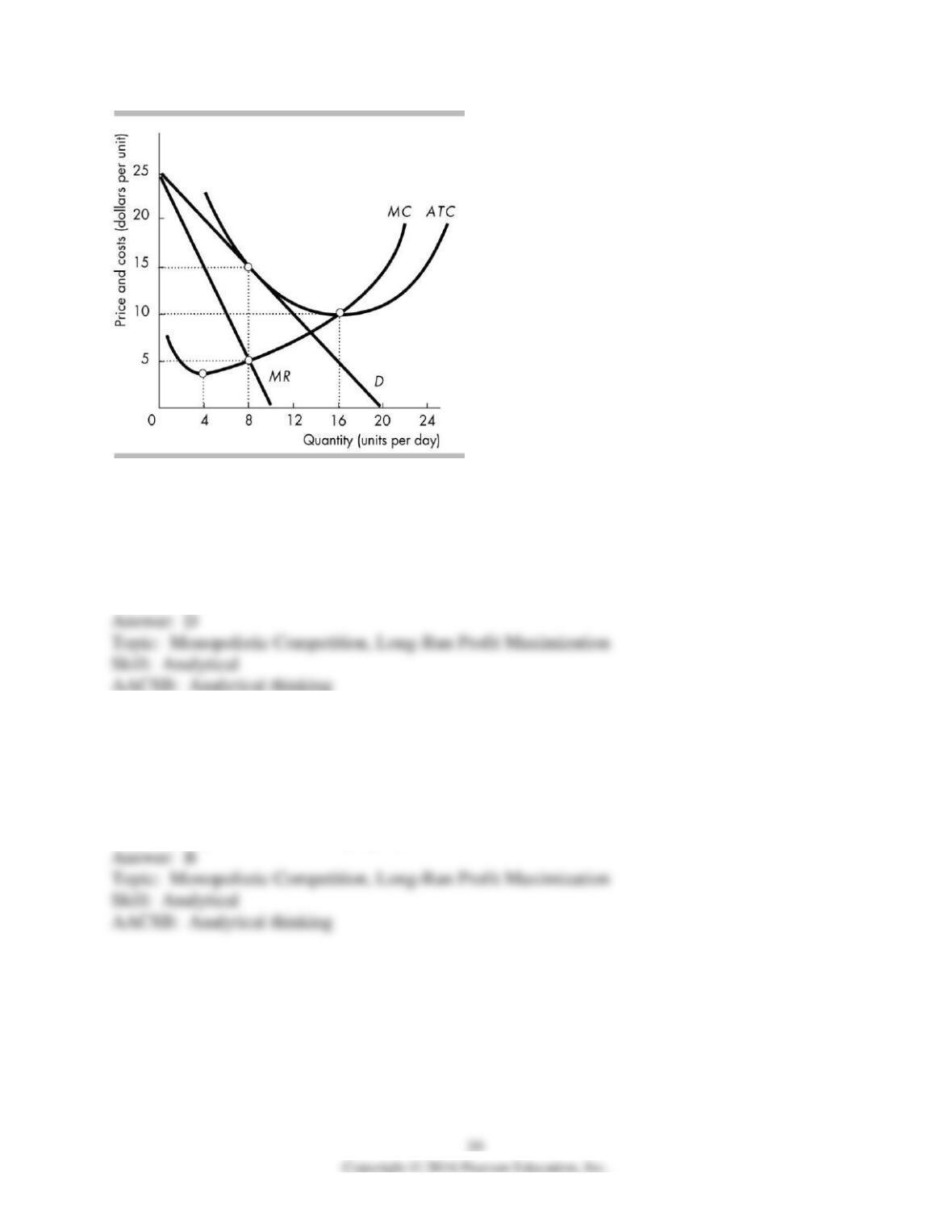

A) average total cost.

B) marginal cost.

C) marginal revenue.

D) elasticity of demand.

100) In the long-run, a firm in monopolistic competition has

A) a price that exceeds its average total cost.

B) a price that exceeds its marginal cost.

C) an average total cost that exceeds its price.

D) a marginal cost that exceeds its price.

101) In the long-run equilibrium, a firm’s price definitely equals its average total cost in

A) both monopoly and monopolistic competition.

B) neither monopoly nor monopolistic competition.

C) monopoly but not monopolistic competition.

D) monopolistic competition but not monopoly.

102) In monopolistic competition in the long run, firms ________.

A) make zero economic profit and require more capacity

B) incur an economic loss and require more capacity

C) make an economic profit and have excess capacity

D) make zero economic profit and have excess capacity

103) Excess capacity is the

A) difference between a perfectly competitive firm’s and a monopolistically competitive firm’s

output.

B) difference between a perfectly competitive firm’s and a monopoly’s output.

C) output at the maximum point of the ATC curve.

D) None of the above answers is correct.

104) In the long run, firms in monopolistic competition produce at a level that is ________ the

efficient scale of output.

A) less than

B) equal to

C) more than

D) All of the above are possible depending on market conditions.

105) A firm is said to have excess capacity when it produces the amount of output

A) such that price is greater than marginal cost.

B) such that marginal revenue is greater than marginal cost.

C) smaller than that which minimizes average total cost.

D) larger than that which minimizes average total cost.

106) The efficient scale of a firm is defined as the point where

A) average total cost is minimized.

B) marginal revenue equals marginal cost.

C) price equals marginal cost.

D) marginal revenue equals zero.

107) In the long run, monopolistically competitive firms produce where

A) excess capacity exists.

B) the markup is equal to zero.

C) the demand curve has shifted so that it intersects the minimum average total cost point.

D) average total cost is minimized.

108) In monopolistic competition, in the long run firms have

A) a capacity shortage.

B) excess capacity.

C) an economic profit.

D) an economic loss.

109) In monopolistic competition, in the long run firms produce

A) less output than that which minimizes their ATC.

B) more output than that which minimizes their ATC.

C) the amount of output that minimizes their ATC and their AVC.

D) the amount of output that minimizes their ATC but not their AVC.

110) A monopolistically competitive firm in the long run ________.

A) is inefficient because it makes zero economic profit

B) produces a profit-maximizing amount of output that is less than capacity output

C) is efficient because it makes zero economic profit

D) sets its price equal to its marginal cost

111) A firm has excess capacity if its output is

A) less than the quantity at which marginal cost is minimized.

B) less than the quantity at which economic profit is maximized.

C) less than the quantity at which average total cost is minimized.

D) more than the quantity at which average total cost is minimized.

112) In monopolistic competition, excess capacity results from

A) the presence of a large number of buyers.

B) the mobility of firms into and out of the industry.

C) imperfect information about price.

D) product differentiation.

113) In its long-run equilibrium, a firm in monopolistic competition

A) makes zero economic profit and operates with excess capacity.

B) makes zero economic profit and produces above capacity output.

C) makes a positive economic profit and operates with excess capacity.

D) makes a positive economic profit and produces above capacity output.

114) A firm’s markup is the amount by which ________ exceeds ________.

A) price; average total cost

B) price; marginal cost

C) average total cost; marginal cost

D) price; average variable cost

115) A monopolistically competitive firm will end up selling its output for a price such that its

A) price is greater than marginal cost.

B) price is equal to marginal cost.

C) price is equal to marginal revenue.

D) price is equal to average total cost.

116) A positive markup is earned by a firm if its

A) price exceeds its marginal cost.

B) marginal revenue equals marginal cost.

C) price equals marginal cost.

D) price equals average total cost.

117) Which of the following statements regarding the efficiency of monopolistic competition is

FALSE?

A) Compared to a situation with total product uniformity, monopolistic competition might be

efficient.

B) Resources are used efficiently when marginal social benefits equals marginal social cost.

C) Monopolistic competition is definitely inefficient because price exceeds marginal cost.

D) A greater degree of product variety creates a loss because the quantity produced is less than

the efficient quantity.

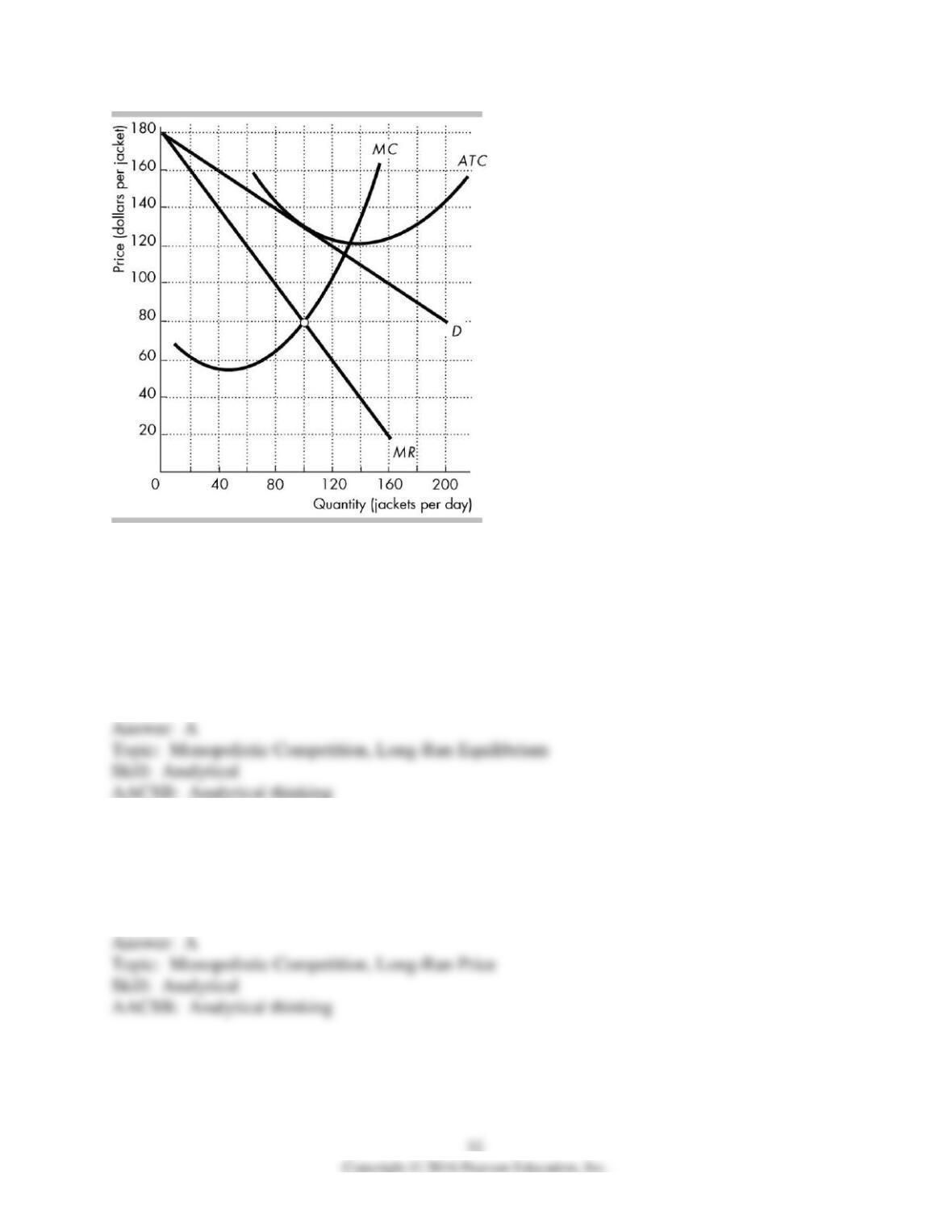

The figure shows the demand curve for Gap jackets (D), and Gap’s marginal revenue curve

(MR), marginal cost curve (MC), and average total cost curve (ATC).

118) In the figure above, Gap maximizes its profit if it sells ________ jackets per day.

A) 100

B) 64

C) 129

D) 133

119) In the figure above, Gap maximizes its profit if it charges ________ per jacket.

A) $130

B) $80

C) $115

D) $100

120) In the figure above, what is Gap’s economic profit?

A) zero

B) $5,000

C) -$5,000

D) -$1,160

121) In the figure above, the market for jackets ________ in long-run equilibrium, and there is

________ for new firms to enter.

A) is; no incentive

B) is; an incentive

C) is not; an incentive

D) is not; no incentive

122) In the figure above, if the market for jackets were perfectly competitive, in long-run

equilibrium, each firm would sell ________ jackets per day at ________ per jacket.

A) 132; $122

B) 100; $130

C) 100; $80

D) 128; $114

123) In the figure above, what is Gap’s excess capacity?

A) 32 jackets per day

B) zero

C) 4 jackets per day

D) 132 jackets per day

124) In the figure above, what is Gap’s markup?

A) $50

B) $15

C) $35

D) zero

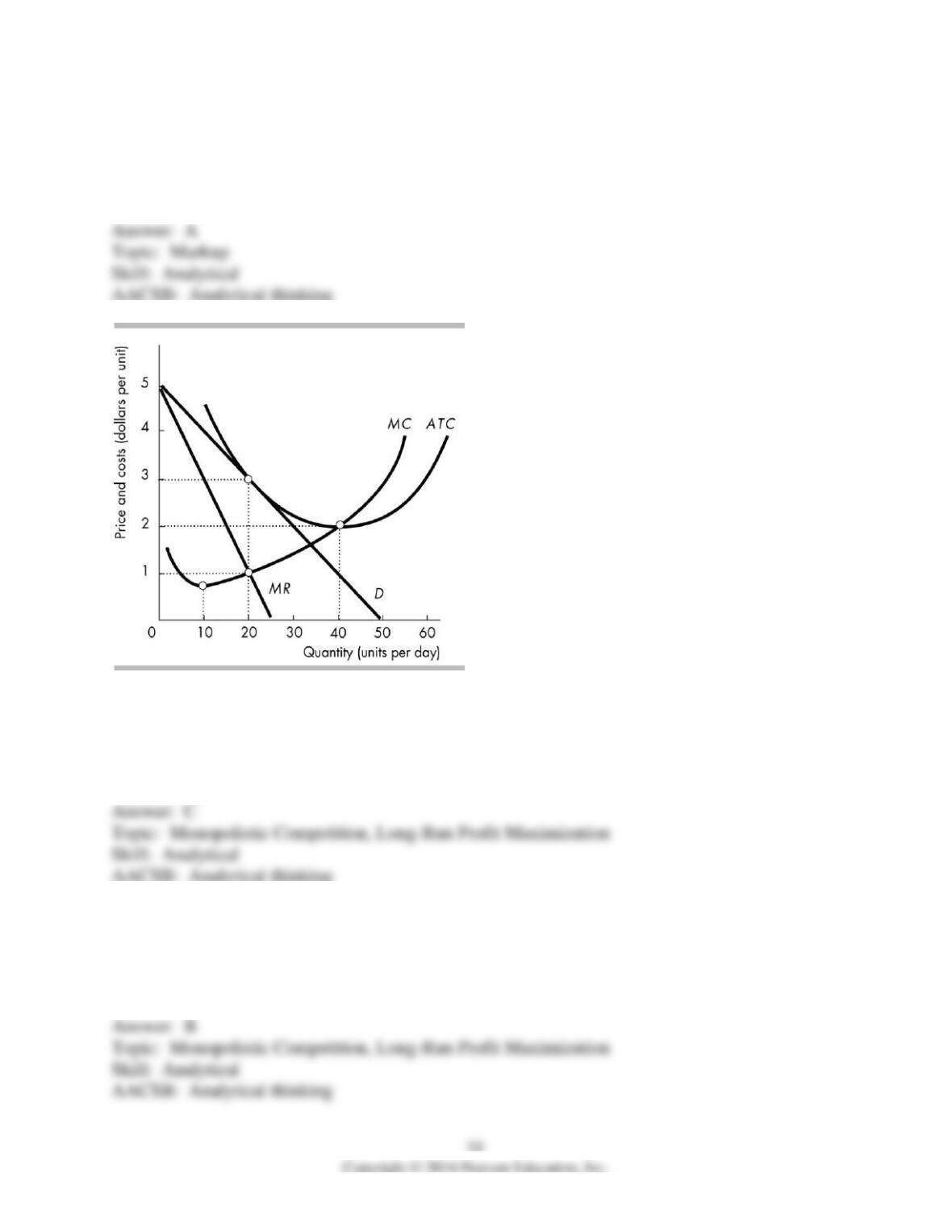

125) The firm in the figure above is in monopolistic competition. It will set a price equal to

A) $1.

B) $2.

C) $3.

D) more than $3.

126) The firm in the figure above is in monopolistic competition. It will produce

A) 10 units.

B) 20 units.

C) 30 units.

D) 40 units.

127) The firm in the figure above is in monopolistic competition. The firm has

A) no excess capacity.

B) excess capacity of 10 units.

C) excess capacity of 20 units.

D) excess capacity of 30 units.

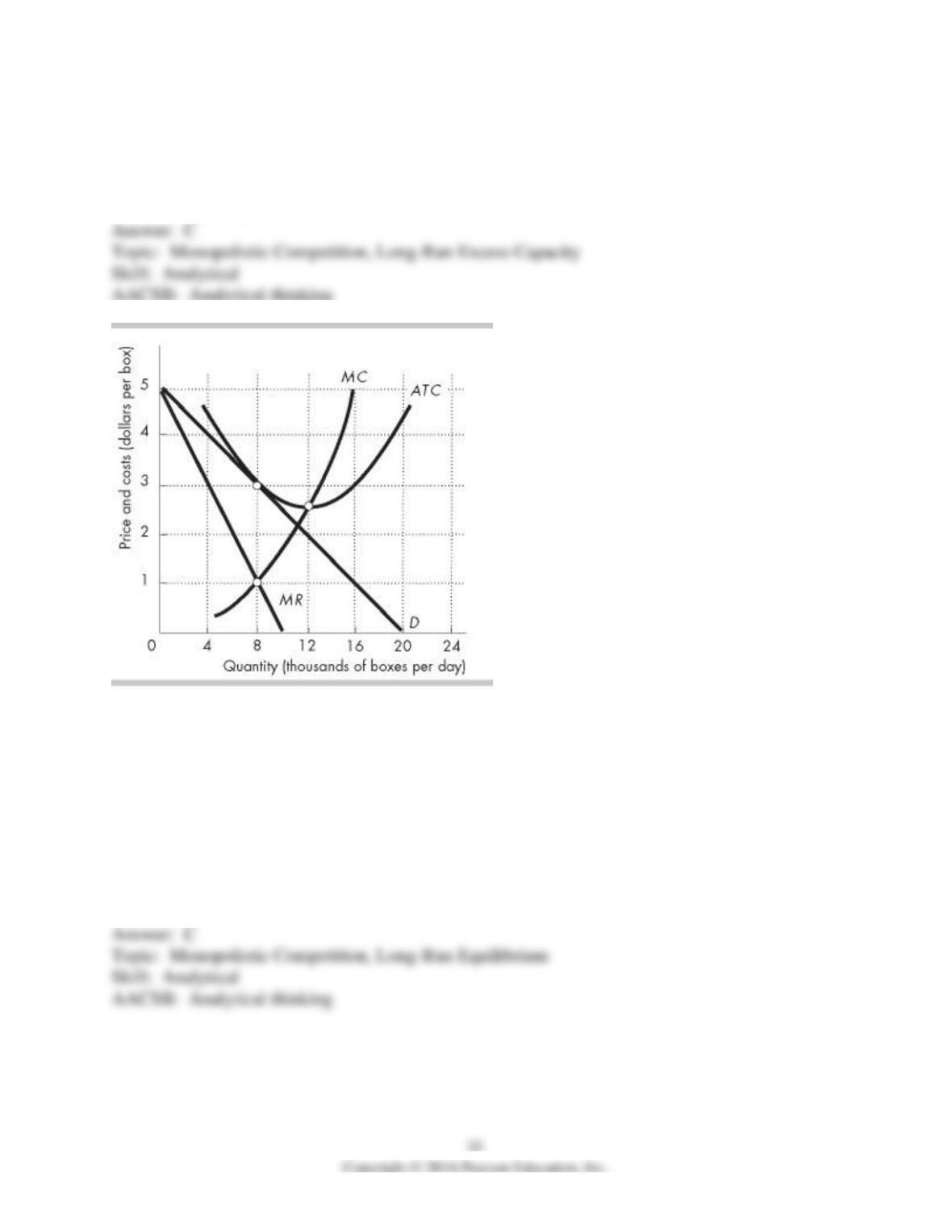

128) Fresh Taste, Inc. produces organic breakfast cereals. The market for breakfast cereals is

monopolistically competitive. The figure above shows the demand curve that Fresh Taste faces

(D), the company’s marginal revenue curve (MR), its marginal cost curve (MC), and its average

total cost curve (ATC).

Fresh Taste produces ________ thousand boxes of cereals per day and sets a price of ________ a

box.

A) 12; between $3.00 and $2.01

B) 8; $1.00

C) 8; $3.00

D) 12; $2.00

129) Fresh Taste, Inc. produces organic breakfast cereals. The market for breakfast cereals is

monopolistically competitive. The figure above shows the demand curve that Fresh Taste faces

(D), the company’s marginal revenue curve (MR), its marginal cost curve (MC), and its average

total cost curve (ATC). Fresh Taste’s economic profit is

A) $16,000 per day.

B) zero, that is, it earns only a normal profit

C) $8,000 per day.

D) None of the above answers is correct.

130) Fresh Taste, Inc. produces organic breakfast cereals. The market for breakfast cereals is

monopolistically competitive. The figure above shows the demand curve that Fresh Taste faces

(D), the company’s marginal revenue curve (MR), its marginal cost curve (MC), and its average

total cost curve (ATC). If Fresh Taste and other firms in the market are currently producing their

profit maximizing quantities of cereals, then the market is

A) in both short-run equilibrium and long-run equilibrium.

B) in short-run equilibrium but not in long-run equilibrium.

C) in long-run equilibrium but not in short-run equilibrium.

D) neither in short-run equilibrium nor in long-run equilibrium.

131) Fresh Taste, Inc. produces organic breakfast cereals. The market for breakfast cereals is

monopolistically competitive. The figure above shows the demand curve that Fresh Taste faces

(D), the company’s marginal revenue curve (MR), its marginal cost curve (MC), and its average

total cost curve (ATC). Fresh Taste’s excess capacity is

A) 12,000 boxes per day.

B) 4,000 boxes per day.

C) 8,000 boxes per day.

D) zero.

132) Fresh Taste, Inc. produces organic breakfast cereals. The market for breakfast cereals is

monopolistically competitive. The figure above shows the demand curve that Fresh Taste faces

(D), the company’s marginal revenue curve (MR), its marginal cost curve (MC), and its average

total cost curve (ATC). Fresh Taste’s markup is

A) more than zero but less than $1.00.

B) $3.00.

C) $2.00.

D) zero.

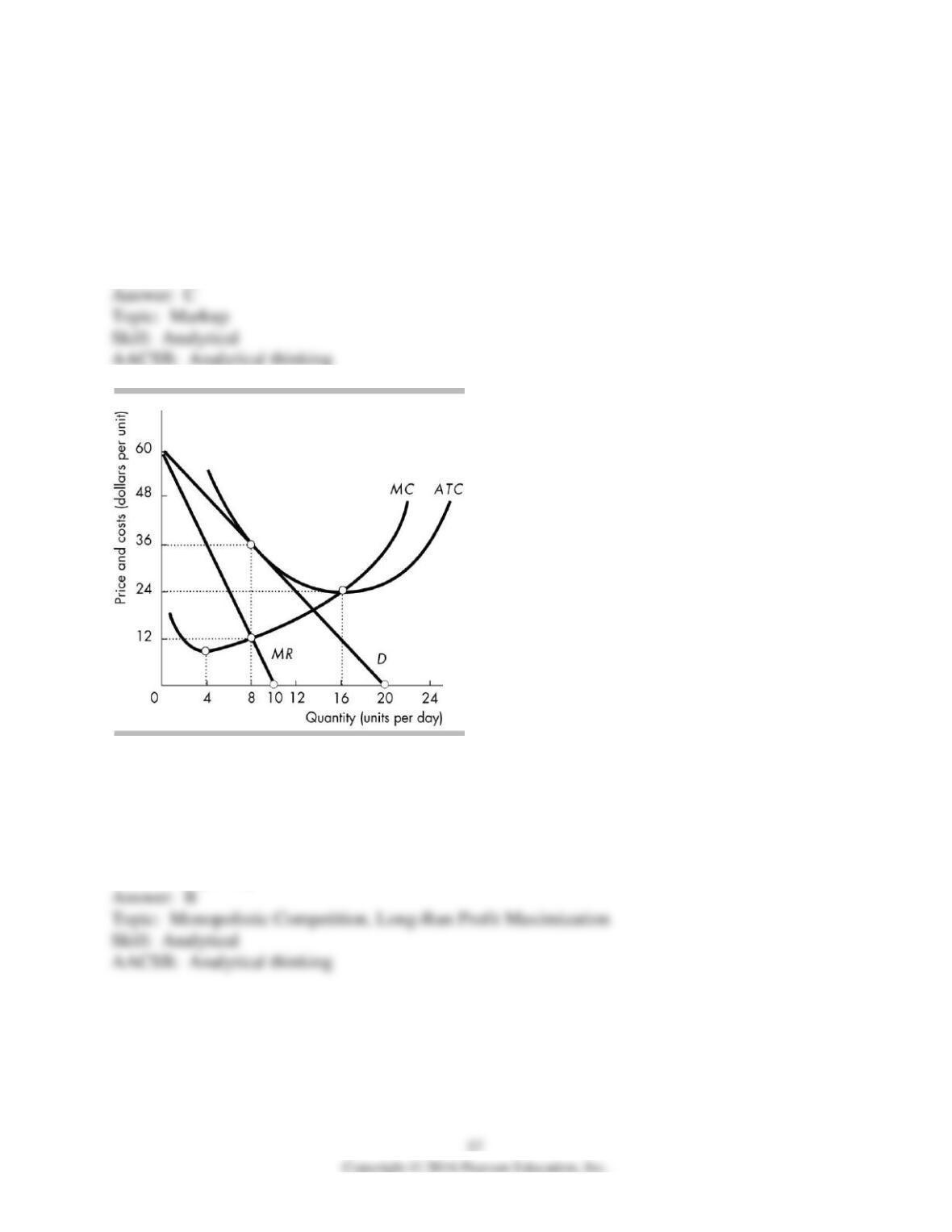

133) The above figure shows a firm in monopolistic competition. What is the profit maximizing

level of output the firm will produce?

A) 4 units per day

B) 8 units per day

C) 10 units per day

D) 16 units per day

134) The above figure shows a firm in monopolistic competition. What price will the firm

charge?

A) $12

B) $24

C) $36

D) None of the above answers is correct.

135) The above figure shows a firm in monopolistic competition. At the profit maximizing level

of output

A) the firm is making a positive economic profit.

B) the firm incurs an economic loss.

C) the firm is making zero economic profit.

D) this firm would choose to shut down in the short run.

136) The above figure shows a firm in monopolistic competition. At the profit maximizing level

of output, excess capacity for the firm is equal to

A) 0 units per day.

B) 4 units per day.

C) 8 units per day.

D) 16 units per day.

137) The above figure shows the demand and cost curves for a firm in monopolistic competition

in the long run. The firm maximizes its profit by

A) producing 4 units and charging a price of $15.

B) producing 8 units and charging a price of $5.

C) producing 16 units and charging a price of $10.

D) None of the above answers is correct.

138) The above figure shows the demand and cost curves for a monopolistically competitive firm

in the long run. The firm maximizes its profit by

A) producing 8 units and charging a price of $5.

B) producing 8 units and charging a price of $15.

C) producing 16 units and charging a price of $10.

D) producing 20 units and charging a price of $25.

139) The above figure shows the demand and cost curves for a monopolistically competitive firm

in the long run. The maximum economic profit this firm can make equal equals

A) $0.

B) $80.

C) $120.

D) $160.

140) The above figure shows the demand and cost curves for a monopolistically competitive firm

in the long run. The firm has excess capacity of

A) 4 units.

B) 8 units.

C) 16 units.

D) $10.