Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13: Capital Structure and Leverage

75. El Capitan Foods has a capital structure of 36% debt and 64% equity, its tax rate is 35%, and its beta (leveraged) is

1.40. Based on the Hamada equation, what would the firm's beta be if it used no debt, i.e., what is its unlevered beta, bU?

a.

1.03

b.

1.29

c.

0.80

d.

0.88

e.

1.15

Chapter 13: Capital Structure and Leverage

76. Gator Fabrics Inc. currently has zero debt (i.e., wd = 0). It is a zero growth company, and additional firm data are

shown below. Now the company is considering using some debt, moving to the new capital structure indicated below. The

money raised would be used to repurchase stock at the current price. It is estimated that the increase in risk resulting from

the additional leverage would cause the required rate of return on equity to rise somewhat, as indicated below. If this plan

were carried out, by how much would the WACC change, i.e., what is WACCOld - WACCNew? Do not round your

intermediate calculations.

wd

40%

Orig cost of equity, rs

10.0%

wc

60%

New cost of equity = rs

11.0%

Interest rate new = rd

6.0%

Tax rate

40%

a.

2.29%

b.

1.96%

c.

2.04%

d.

1.65%

e.

2.16%

77. As a consultant to First Responder Inc., you have obtained the following data (dollars in millions). The company plans

to pay out all of its earnings as dividends, hence g = 0. Also, no net new investment in operating capital is needed because

growth is zero. The CFO believes that a move from zero debt to 80.0% debt would cause the cost of equity to increase

from 10.0% to 12.0%, and the interest rate on the new debt would be 9.0%. What would the firm's total market value be if

it makes this change? Hints: Find the FCF, which is equal to NOPAT = EBIT(1 - T) because no new operating capital is

Chapter 13: Capital Structure and Leverage

needed, and then divide by (WACC - g). Do not round your intermediate calculations.

Oper. income (EBIT)

$800

Tax rate

40.0%

New cost of equity (rs)

12.00%

New wd

80.0%

Interest rate (rd)

9.00%

a.

$7,143

b.

$8,000

c.

$7,357

d.

$5,357

e.

$5,929

78. You plan to invest in one of two home delivery pizza companies, High and Low, that were recently founded and are

about to commence operations. They are identical except for their use of debt (wd) and the interest rates on their debt--

High uses more debt and thus must pay a higher interest rate. Based on the data given below, how much higher or lower

will High's expected EPS be versus that of Low, i.e., what is EPSHigh – EPSLow? Do not round your intermediate

calculations.

Applicable to Both Firms

Firm High's Data

Firm Low's Data

Chapter 13: Capital Structure and Leverage

Capital

$3,000,000

wd

70%

wd

20%

EBIT

$565,000

Shares

90,000

Shares

240,000

Tax rate

35%

Int. rate

12%

Int. rate

10%

a.

$01.16

b.

$00.67

c.

$01.07

d.

$00.80

e.

$00.89

79. Firms HD and LD are identical except for their use of debt and the interest rates they pay--HD has more debt and thus

must pay a higher interest rate. Based on the data given below, how much higher or lower will HD's ROE be versus that of

Chapter 13: Capital Structure and Leverage

LD, i.e., what is ROEHD - ROELD? Do not round your intermediate calculations.

Applicable to Both Firms

Firm HD's Data

Firm LD's Data

Capital

$3,000,000

wd

70%

wd

20%

EBIT

$595,000

Int. rate

12%

Int. rate

10%

Tax rate

35%

a.

11.31%

b.

13.37%

c.

8.74%

d.

10.28%

e.

10.80%

Chapter 13: Capital Structure and Leverage

80. Firm A is very aggressive in its use of debt to leverage up its earnings for common stockholders, whereas Firm NA is

not aggressive and uses no debt. The two firms' operations are identical--they have the same total investor-supplied

capital, sales, operating costs, and EBIT. Thus, they differ only in their use of financial leverage (wd). Based on the

following data, how much higher or lower is A's ROE than that of NA, i.e., what is ROEA - ROENA? Do not round your

intermediate calculations.

Applicable to Both Firms

Firm A's Data

Firm NA's Data

Capital

$210,000

wd

50%

wd

0%

EBIT

$40,000

Int. rate

12%

Int. rate

10%

Tax rate

35%

a.

4.90%

b.

3.71%

c.

4.58%

d.

5.54%

e.

3.76%

Chapter 13: Capital Structure and Leverage

81. Your firm's debt ratio is only 5.00%, but the new CFO thinks that more debt should be employed. She wants to sell

bonds and use the proceeds to buy back and retire common shares so the percentage of common equity in the capital

structure (wc) = 1 – wd. Other things held constant, and based on the data below, if the firm increases the percentage of

debt in its capital structure (wd) to 60.0%, by how much would the ROE change, i.e., what is ROENew - ROEOld? Do not

round your intermediate calculations.

Operating Data

Other Data

Capital

$150,000

Old wd

5%

ROIC = EBIT (1 – T)/Capital

20.00%

Old interest ratio

10%

Tax rate

35%

New wd

60%

New interest rate

12%

a.

14.95%

b.

19.17%

c.

17.59%

d.

21.64%

e.

14.42%

Chapter 13: Capital Structure and Leverage

82. You have been hired by a new firm that is just being started. The CFO wants to finance with 60% debt, but the

president thinks it would be better to hold the percentage of debt in the capital structure (wd) to only 10%. Other things

held constant, and based on the data below, if the firm uses more debt, by how much would the ROE change, i.e., what is

ROENew - ROEOld? Do not round your intermediate calculations.

Operating Data

Other Data

Capital

$4,000

Higher wd

60%

ROIC = EBIT(1 – T)/Capital

17.00%

Higher interest rate

13%

Tax rate

35%

Lower wd

10%

Lower interest rate

9%

a.

10.31%

b.

11.59%

c.

10.43%

d.

9.15%

e.

10.54%

Chapter 13: Capital Structure and Leverage

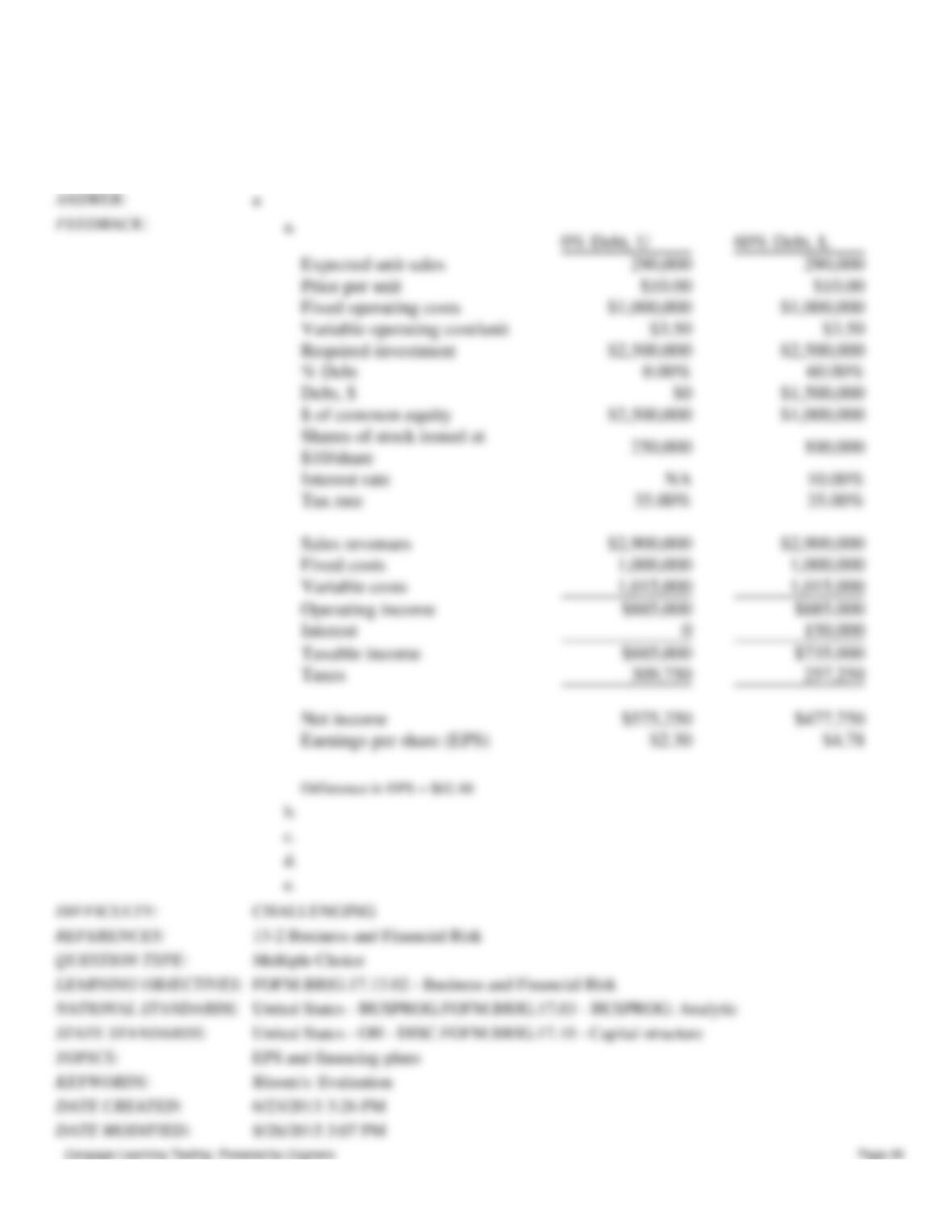

83. Your girlfriend plans to start a new company to make a new type of cat litter. Her father will finance the operation, but

she will have to pay him back. You are helping her, and the issue now is how to finance the company, with equity only or

with a mix of debt and equity. The price per unit will be $10.00 regardless of how the firm is financed. The expected fixed

and variable operating costs, along with other information, are shown below. How much higher or lower will the firm's

expected EPS be if it uses some debt rather than only equity, i.e., what is EPSL - EPSU? Do not round your intermediate

calculations.

0% Debt, U

60% Debt, L

Expected unit sales

290,000

290,000

Price per unit

$10.00

$10.00

Fixed costs

$1,000,000

$1,000,000

Variable cost/unit

$3.50

$3.50

Required investment

$2,500,000

$2,500,000

Shares issued at $10/share

250,000

100,000

% Debt

0.00%

60.00%

Debt, $

$0

$1,500,000

Equity, $

$2,500,000

$1,000,000

Interest rate

NA

10.00%

Tax rate

35.00%

35.00%

a.

$02.48

Chapter 13: Capital Structure and Leverage

b.

$02.35

c.

$03.10

d.

$02.85

e.

$02.60

Chapter 13: Capital Structure and Leverage

84. Southeast U's campus book store sells course packs for $15.00 each, the variable cost per pack is $11.00, fixed costs

for this operation are $300,000, and annual sales are 75,000 packs. The unit variable cost consists of a $4.00 royalty

payment, VR , per pack to professors plus other variable costs of VO = $7.00. The royalty payment is negotiable. The

book store's directors believe that the store should earn a profit margin of 10% on sales, and they want the store's

managers to pay a royalty rate that will produce that profit margin. What royalty per pack would permit the store to earn a

10% profit margin on course packs, other things held constant? Do not round your intermediate calculations.

a.

$2.50

b.

$1.88

c.

$2.78

d.

$2.25

e.

$2.00

Chapter 13: Capital Structure and Leverage

85. Dye Industries currently uses no debt, but its new CFO is considering changing the capital structure to 49.0% debt

(wd) by issuing bonds and using the proceeds to repurchase and retire some common shares so the percentage of common

equity in the capital structure (wc) = 1 – wd. Given the data shown below, by how much would this recapitalization

change the firm's cost of equity, i.e., what is rL - rU? Do not round your intermediate calculations.

Risk-free rate, rRF

6.00%

Tax rate, T

40%

Market risk prem, RPM

3.00%

Current wd

0%

Current beta, bU

1.30

Target wd

49.0%

a.

2.59%

b.

1.91%

c.

2.92%

d.

1.57%

e.

2.25%

Chapter 13: Capital Structure and Leverage

86. Dyson Inc. currently finances with 20.0% debt (i.e., wd = 20%), but its new CFO is considering changing the capital

structure so wd = 36.0% by issuing additional bonds and using the proceeds to repurchase and retire common shares so the

percentage of common equity in the capital structure (wc) = 1 – wd. Given the data shown below, by how much would this

recapitalization change the firm's cost of equity? Do not round your intermediate calculations. (Hint: You must unlever

the current beta and then use the unlevered beta to solve the problem.)

Risk-free rate, rRF

5.00%

Tax rate, T

40%

Market risk prem, RPM

6.00%

Current wd

20%

Current beta, bL1

1.65

Target wd

36.0%

a.

1.61%

b.

1.66%

c.

1.24%

d.

1.68%

e.

1.69%

Chapter 13: Capital Structure and Leverage

87. Monroe Inc. is an all-equity firm with 500,000 shares outstanding. It has $2,000,000 of EBIT, and EBIT is expected to

remain constant in the future. The company pays out all of its earnings, so earnings per share (EPS) equal dividends per

share (DPS), and its tax rate is 40%. The company is considering issuing $4,500,000 of 9.00% bonds and using the

proceeds to repurchase stock. The risk-free rate is 4.5%, the market risk premium is 5.0%, and the firm's beta is currently

1.10. However, the CFO believes the beta would rise to 1.30 if the recapitalization occurs. Assuming the shares could be

repurchased at the price that existed prior to the recapitalization, what would the price per share be following the

recapitalization? (Hint: P0 = EPS/rs because EPS = DPS.)

a.

$34.52

b.

$27.84

c.

$21.44

d.

$28.12

e.

$29.51

Chapter 13: Capital Structure and Leverage

88. You were hired as the CFO of a new company that was founded by three professors at your university. The company

plans to manufacture and sell a new product, a cell phone that can be worn like a wrist watch. The issue now is how to

finance the company, with equity only or with a mix of debt and equity. The price per phone will be $250.00 regardless of

how the firm is financed. The expected fixed and variable operating costs, along with other data, are shown below. How

much higher or lower will the firm's expected ROE be if it uses 60% debt rather than only equity, i.e., what is ROEL -

ROEU?

0% Debt, U

60% Debt, L

Expected unit sales (Q)

32,000

32,000

Price per phone (P)

$250.00

$250.00

Fixed costs (F)

$1,000,000

$1,000,000

Variable cost/unit (V)

$200.00

$200.00

Required investment

$2,500,000

$2,500,000

% Debt

0.00%

60.00%

Debt, $

$0

$1,500,000

Equity, $

$2,500,000

$1,000,000

Interest rate

NA

10.00%

Tax rate

35.00%

35.00%

a.

16.52%

b.

13.65%

c.

11.33%

d.

15.70%

e.

12.56%

Chapter 13: Capital Structure and Leverage