Chapter 13/The Costs of Production ❖ 61

104. Refer to Scenario 13-14. Farmer Brown’s marginal cost of producing 9 units of output (using 2 bags of seed)

is

a.

$240.

b.

$120.

c.

$40.

d.

$30.

Scenario 13–15

Farmer Jack is a watermelon farmer. If Jack plants no seeds on his farm, he gets no harvest. If he plants 1 bag

of seeds, he gets 30 watermelons. If he plants 2 bags of seeds, he gets 50 watermelons. If he plants 3 bags of

seeds he gets 60 watermelons. A bag of seeds costs $100, and the costs of seeds are his only costs.

105. Refer to Scenario 13–15. Which of the following statements is (are) true?

(i)

Farmer Jack experiences decreasing marginal product.

(ii)

Farmer Jack’s production function is nonlinear.

(iii)

Farmer Jack’s total cost curve is linear.

a.

(i) only

b.

(i) and (ii) only

c.

(ii) only

d.

(i) and (iii) only

106. Refer to Scenario 13–15. Farmer Jack’s marginal cost

(i)

curve is U-shaped.

(ii)

decreases with increased watermelon output.

(iii)

reflects diminishing marginal product.

a.

(ii) only

b.

(iii) only

c.

(i) and (iii) only

d.

(i) and (ii) only

107. Refer to Scenario 13–15. Farmer Jack’s production function will

a.

decrease at a decreasing rate.

b.

decrease at an increasing rate.

c.

increase at a decreasing rate.

d.

increase at an increasing rate.

108. Refer to Scenario 13–15. What is the shape of Farmer Jack’s marginal cost curve?

a.

upward sloping

b.

downward sloping

c.

U-shaped

d.

constant

62 ❖ Chapter 13/The Costs of Production

Scenario 13–16

A certain firm produces and sells staplers. Last year, it produced 7,000 staplers and sold each stapler for $6. In

producing the 7,000 staplers, it incurred variable costs of $28,000 and a total cost of $45,000.

109. Refer to Scenario 13–16. The firm’s fixed cost was

a.

$7,000.

b.

$17,000.

c.

$28,000.

d.

$42,000.

110. Refer to Scenario 13–16. In producing the 7,000 staplers, the firm’s average fixed cost was

a.

$1.00.

b.

$1.32.

c.

$2.21.

d.

$2.43.

111. Refer to Scenario 13–16. In producing the 7,000 staplers, the firm’s average variable cost was

a.

$2.43.

b.

$4.00.

c.

$6.00.

d.

$6.43.

112. Refer to Scenario 13–16. In producing the 7,000 staplers, the firm’s average total cost was

a.

$2.43.

b.

$4.00.

c.

$6.00.

d.

$6.43.

113. Refer to Scenario 13–16. Suppose the owner of the business had an offer to work for another firm for

$25,000. The firm’s accounting profit for the year was

a.

$-28,000.

b.

$-25,000

c.

$-3,000.

d.

$17,000.

114. Refer to Scenario 13–16. Suppose the owner of the business had an offer to work for another firm for

$25,000. The firm’s economic profit for the year was

a.

$-28,000.

b.

$-25,000

c.

$-3,000.

d.

$17,000.

Chapter 13/The Costs of Production ❖ 63

115. Marginal cost is equal to

a.

TC/Q.

b.

ATC/Q.

c.

TC/Q.

d.

Q/TC.

116. The amount by which total cost rises when the firm produces one additional unit of output is called

a.

average cost.

b.

marginal cost.

c.

fixed cost.

d.

variable cost.

117. The cost of producing an additional unit of output is the firm’s

a.

marginal cost.

b.

productivity offset.

c.

variable cost.

d.

average variable cost.

118. Marginal cost equals

(i)

change in total cost divided by change in quantity produced.

(ii)

change in variable cost divided by change in quantity produced.

(iii)

the average fixed cost of the current unit.

a.

(i) and (ii) only

b.

(ii) and (iii) only

c.

(i) only

d.

(i), (ii), and (iii)

119. Marginal cost equals

a.

total cost divided by quantity of output produced.

b.

total output divided by the change in total cost.

c.

the slope of the total cost curve.

d.

the slope of the line drawn from the origin to the total cost curve.

120. Marginal cost tells us the

a.

value of all resources used in a production process.

b.

marginal increment to profitability when price is constant.

c.

amount by which total cost rises when output is increased by one unit.

d.

amount by which output rises when labor is increased by one unit.

64 ❖ Chapter 13/The Costs of Production

121. Which of the following measures of cost is best described as “the increase in total cost that arises from an ex-

tra unit of production?”

a.

variable cost

b.

average variable cost

c.

average total cost

d.

marginal cost

122. A firm has a fixed cost of $500 in its first year of operation. When the firm produces 100 units of output, its

total costs are $3,500. When it produces 101 units of output, its total costs are $3,750. What is the marginal

cost of producing the 101st unit of output?

a.

$250

b.

$275

c.

$340.91

d.

$350

123. A firm has a fixed cost of $500 in its first year of operation. When the firm produces 100 units of output, its

total costs are $4,500. The marginal cost of producing the 101st unit of output is $300. What is the total cost

of producing 101 units?

a.

$46.53

b.

$800

c.

$4,800

d.

$5,300

124. A firm has a fixed cost of $700 in its first year of operation. When the firm produces 99 units of output, its

total costs are $4,000. The marginal cost of producing the 100th unit of output is $200. What is the total cost

of producing 100 units?

a.

$42

b.

$900

c.

$4,200

d.

$4,900

125. A firm has a fixed cost of $200 in its first year of operation. When the firm produces 99 units of output, its

total costs are $4,000. The marginal cost of producing the 100th unit of output is $700. What is the total cost

of producing 100 units?

a.

$900

b.

$4,200

c.

$4,700

d.

$4,900

Chapter 13/The Costs of Production ❖ 65

126. Thirsty Thelma owns and operates a small lemonade stand. When Thelma is producing a low quantity of lem-

onade she has few workers and her equipment is not being fully utilized. Because she can easily put her idle

resources to use,

a.

the marginal cost of an extra worker is large.

b.

the marginal cost of one more glass of lemonade is smaller than if output were high.

c.

the marginal product of an extra worker is small.

d.

her lemonade stand is likely to be crowded with workers.

127. Randy is a minor-league baseball player. His current cumulative batting average is 0.270. Randy believes

that if he can raise his cumulative batting average to 0.300, he will have a chance to play in the major leagues.

Which of the following statements is correct?

a.

If Randy gets between 27 and 30 hits out of his next 100 at bats, he will be able to raise his

cumulative batting average to 0.300.

b.

If Randy gets 30 hits out of his next 100 at bats, he will be able to raise his cumulative batting

average to 0.300.

c.

Randy must get more than 30 hits out of his next 100 at bats in order to raise his cumulative batting

average to 0.300.

d.

Either b or c could be correct.

128. Johnny is a sophomore in college and has a 1.5 cumulative grade point average (GPA). Johnny’s cumulative

GPA will fall even further next semester if he performs worse than

(i)

his cumulative GPA.

(ii)

he ever performed before.

(iii)

he did last semester.

a.

(i) and (ii) only

b.

(i) and (iii) only

c.

(ii) and (iii) only

d.

(i), (ii), and (iii)

129. Johnny is a sophomore in college and has a 1.5 cumulative grade point average (GPA). Johnny’s cumulative

GPA will be better next semester if he

(i)

performs better than he did last semester.

(ii)

performs better than his cumulative GPA.

(iii)

gives an average performance.

a.

(ii) only

b.

(iii) only

c.

(i) and (ii)

d.

(ii) and (iii)

66 ❖ Chapter 13/The Costs of Production

130. Jennifer is a junior in college. Her current cumulative grade point average (GPA) is 3.5 out of a 4.0 scale.

Jennifer is hoping that by the time she graduates, she can raise her cumulative GPA to a 3.7. Which of the fol-

lowing statements is correct?

a.

If Jennifer earns between a 3.5 and a 3.7 GPA in her senior year, she will be able to raise her

cumulative GPA to a 3.7.

b.

If Jennifer earns a 3.7 GPA in her senior year, she will be able to raise her cumulative GPA to a 3.7.

c.

Jennifer must earn above a 3.7 GPA in her senior year in order to raise her cumulative GPA to a

3.7.

d.

Either b or c could be correct.

131. If Franco‘s Pizza Parlor knows that the marginal cost of the 500th pizza is $3.50 and that the average total cost

of making 499 pizzas is $3.30, then

a.

average total costs are rising at Q = 500.

b.

average total costs are falling at Q = 500.

c.

total costs are falling at Q = 500.

d.

average variable costs must be falling.

132. Suppose that a firm has only one variable input, labor, and firm output is zero when labor is zero. When the

firm hires 6 workers the firm produces 90 units of output. Fixed costs of production are $6 and the variable

cost per unit of labor is $10. The marginal product of the seventh unit of labor is 4. Given this information,

what is the marginal cost of production when the firm hires the 7th worker?

a.

$1.50

b.

$2.50

c.

$5

d.

$10

Chapter 13/The Costs of Production ❖ 67

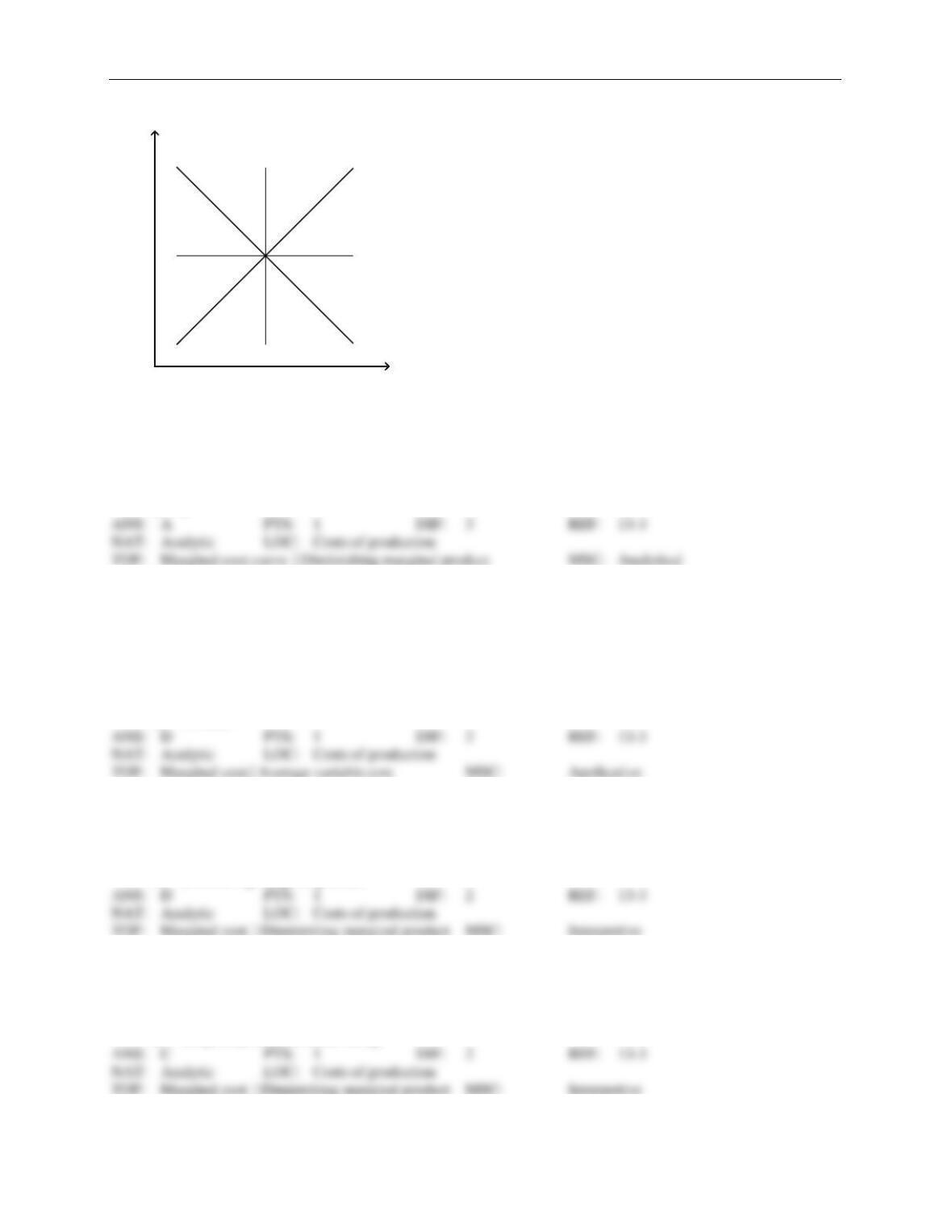

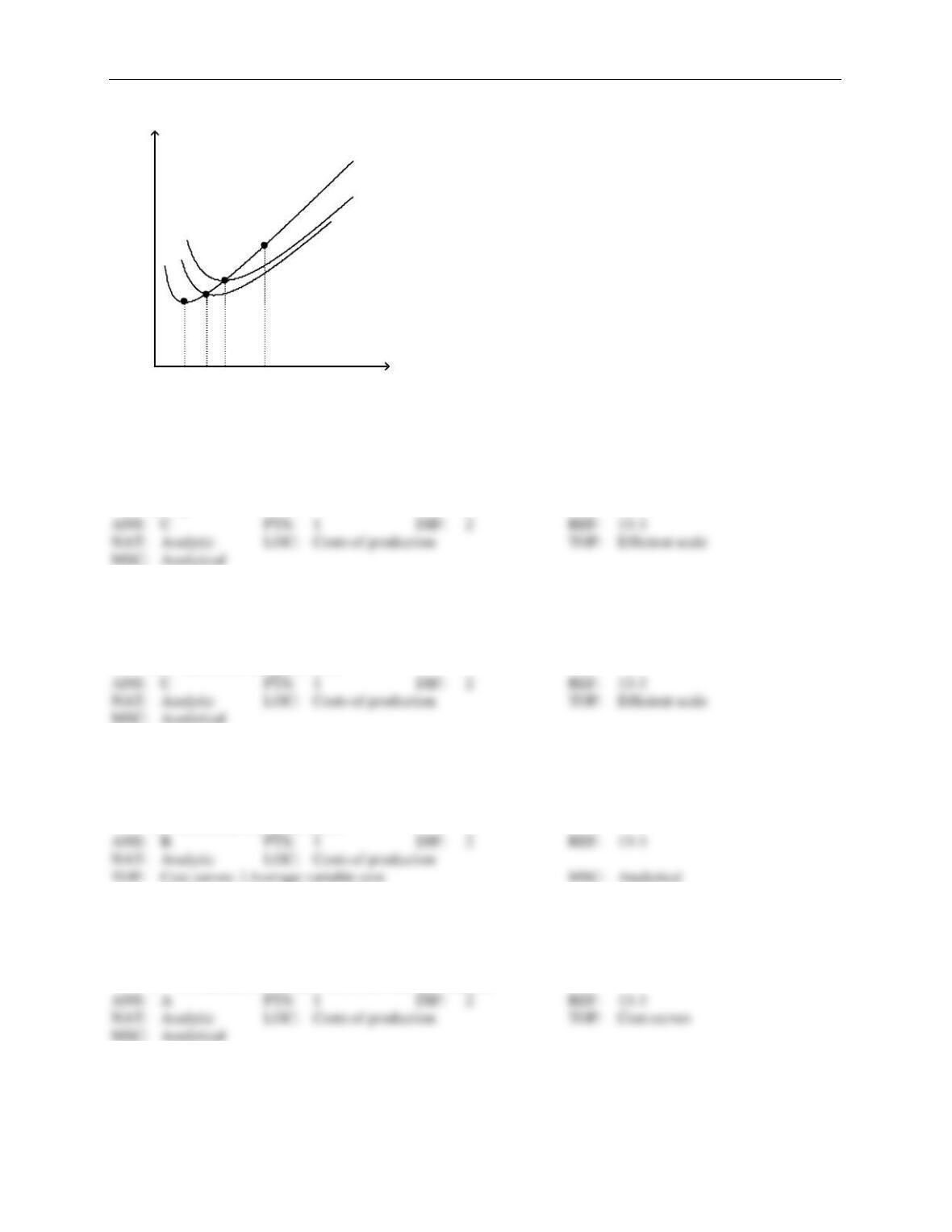

Figure 13-4

133. Refer to Figure 13-4. Which of the above marginal cost curves reflects diminishing marginal product?

a.

A

b.

B

c.

C

d.

D

134. Suppose that a firm has only one variable input, labor, and firm output is zero when labor is zero. When the

firm hires 6 workers the firm produces 90 units of output. Fixed costs of production are $6 and the variable

cost per unit of labor is $10. The marginal product of the seventh unit of labor is 4. Given this information,

what is the average variable cost of production when the firm hires 7 workers?

a.

$12.67

b.

$11

c.

81 cents

d.

75 cents

135. Marginal cost increases as the quantity of output increases. This reflects the property of

a.

increasing total cost.

b.

diminishing total cost.

c.

increasing marginal product.

d.

diminishing marginal product.

136. If marginal cost is rising,

a.

average variable cost must be falling.

b.

average fixed cost must be rising.

c.

marginal product must be falling.

d.

marginal product must be rising.

A

A

D

D

B

B

C C

Output

MC

68 ❖ Chapter 13/The Costs of Production

137. Diminishing marginal product suggests that the marginal

a.

cost of an extra worker is unchanged.

b.

cost of an extra worker is less than the previous worker’s marginal cost.

c.

product of an extra worker is less than the previous worker’s marginal product.

d.

product of an extra worker is greater than the previous worker’s marginal product.

138. Diminishing marginal product suggests that

a.

additional units of output become less costly as more output is produced.

b.

marginal cost is upward sloping.

c.

the firm is at full capacity.

d.

adding additional workers will lower total cost.

139. The fundamental reason that marginal cost eventually rises as output increases is because of

a.

economies of scale.

b.

diseconomies of scale.

c.

diminishing marginal product.

d.

rising average fixed cost.

140. The average-fixed-cost curve

a.

is constant.

b.

is always decreasing.

c.

intersects marginal cost at the minimum of average fixed cost.

d.

intersects marginal cost at the minimum of marginal cost.

141. Consider the following information about bread production at Beth’s Bakery:

Worker

Marginal Product

1

5

2

7

3

10

4

11

5

8

6

6

7

4

Beth pays all her workers the same wage, and labor is her only variable cost. From this information we can

conclude that Beth’s marginal cost

a.

declines as output increases from 0 to 33, but increases after that.

b.

declines as output increases from 0 to 11, but increases after that.

c.

increases as output increases from 0 to 11, but declines after that.

d.

is constant.

Chapter 13/The Costs of Production ❖ 69

142. The average-total-cost curve intersects

a.

average fixed cost at the minimum of average total cost.

b.

average variable cost at the minimum of average total cost.

c.

marginal cost at the minimum of average total cost.

d.

marginal cost at the minimum of marginal cost.

Scenario 13–17

Suppose that a given firm experiences decreasing marginal product of labor with the addition of each worker

regardless of the current output level.

143. Refer to Scenario 13-17. Average total cost will be

a.

rising at all points.

b.

falling at all points.

c.

constant.

d.

U-shaped.

144. Refer to Scenario 13–17. Average fixed cost will be

a.

rising at all points.

b.

falling at all points.

c.

U-shaped.

d.

constant.

145. Refer to Scenario 13–17. Average variable cost will be

a.

rising at all points.

b.

falling at all points.

c.

U-shaped.

d.

constant.

146. Refer to Scenario 13–17. Marginal cost will be

a.

rising at all points.

b.

falling at all points.

c.

U-shaped.

d.

constant.

70 ❖ Chapter 13/The Costs of Production

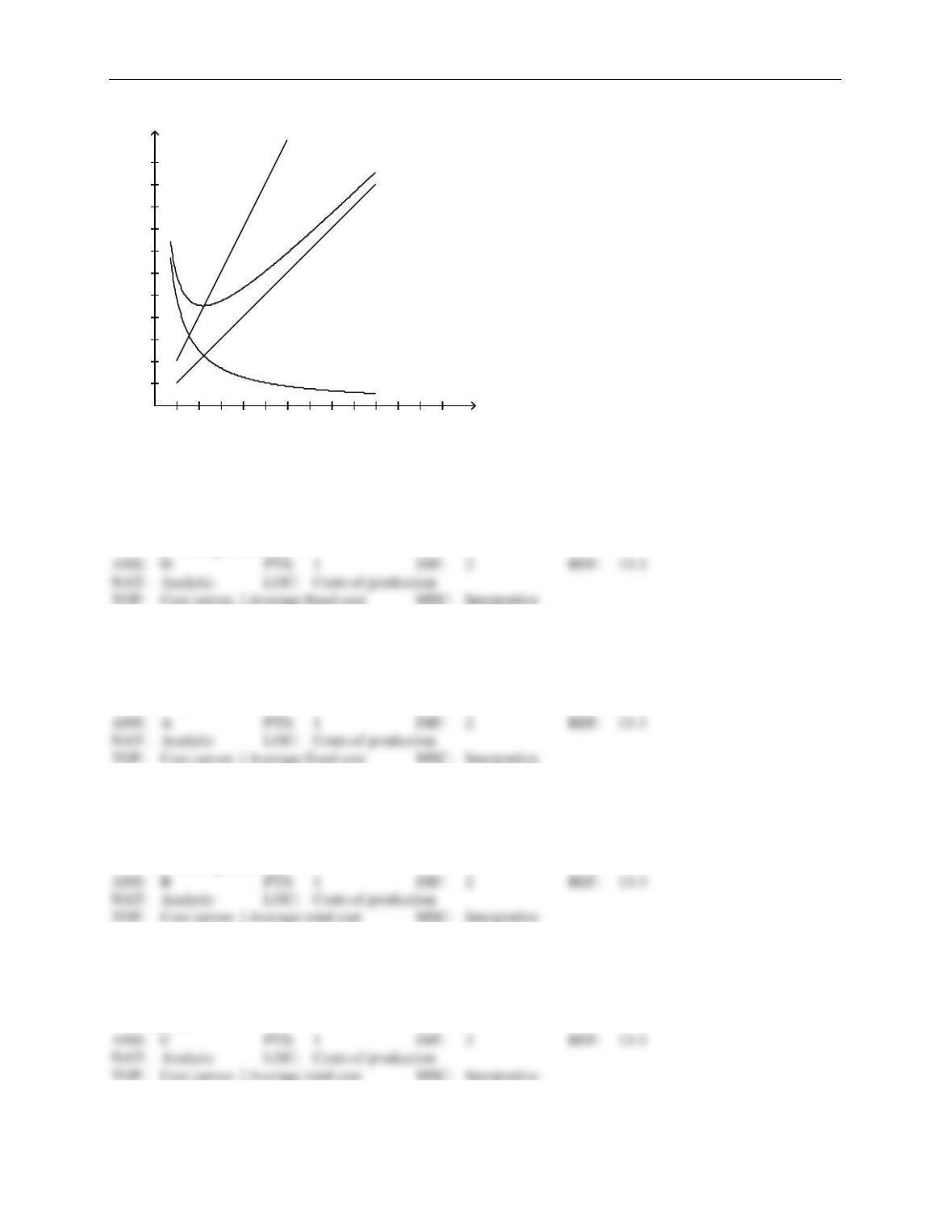

Figure 13-5

147. Refer to Figure 13-5. Curve A represents which type of cost curve?

a.

marginal cost

b.

average total cost

c.

average variable cost

d.

average fixed cost

148. Refer to Figure 13-5. Which of the curves is most likely to represent average fixed cost?

a.

A

b.

B

c.

C

d.

D

149. Refer to Figure 13-5. Curve C represents which type of cost curve?

a.

marginal cost

b.

average total cost

c.

average variable cost

d.

average fixed cost

150. Refer to Figure 13-5. Which curve is most likely to represent average total cost?

a.

A

b.

B

c.

C

d.

D

A

B

C

D

1 2 3 4 5 6 7 8 9 10 11 12 Quantity

1

2

3

4

5

6

7

8

9

10

11

Cost

Chapter 13/The Costs of Production ❖ 71

151. Refer to Figure 13-5. Curve D represents which type of cost curve?

a.

marginal cost

b.

average total cost

c.

average variable cost

d.

average fixed cost

152. Refer to Figure 13-5. Which curve is most likely to represent marginal cost?

a.

A

b.

B

c.

C

d.

D

153. Refer to Figure 13-5. Curve D is increasing because

a.

of diminishing marginal product.

b.

of increasing marginal product.

c.

marginal product first increases, then decreases.

d.

marginal product first decreases, then increases.

154. Refer to Figure 13-5. Curve A is always declining because

a.

of diminishing marginal product.

b.

we are dividing fixed costs by higher and higher levels of output.

c.

marginal product first increases, then decreases.

d.

marginal product first decreases, then increases.

155. Refer to Figure 13-5. Curve D intersects curve C

a.

where the firm maximizes profit.

b.

at the minimum of average fixed cost.

c.

at the efficient scale.

d.

where fixed costs equal variable costs.

72 ❖ Chapter 13/The Costs of Production

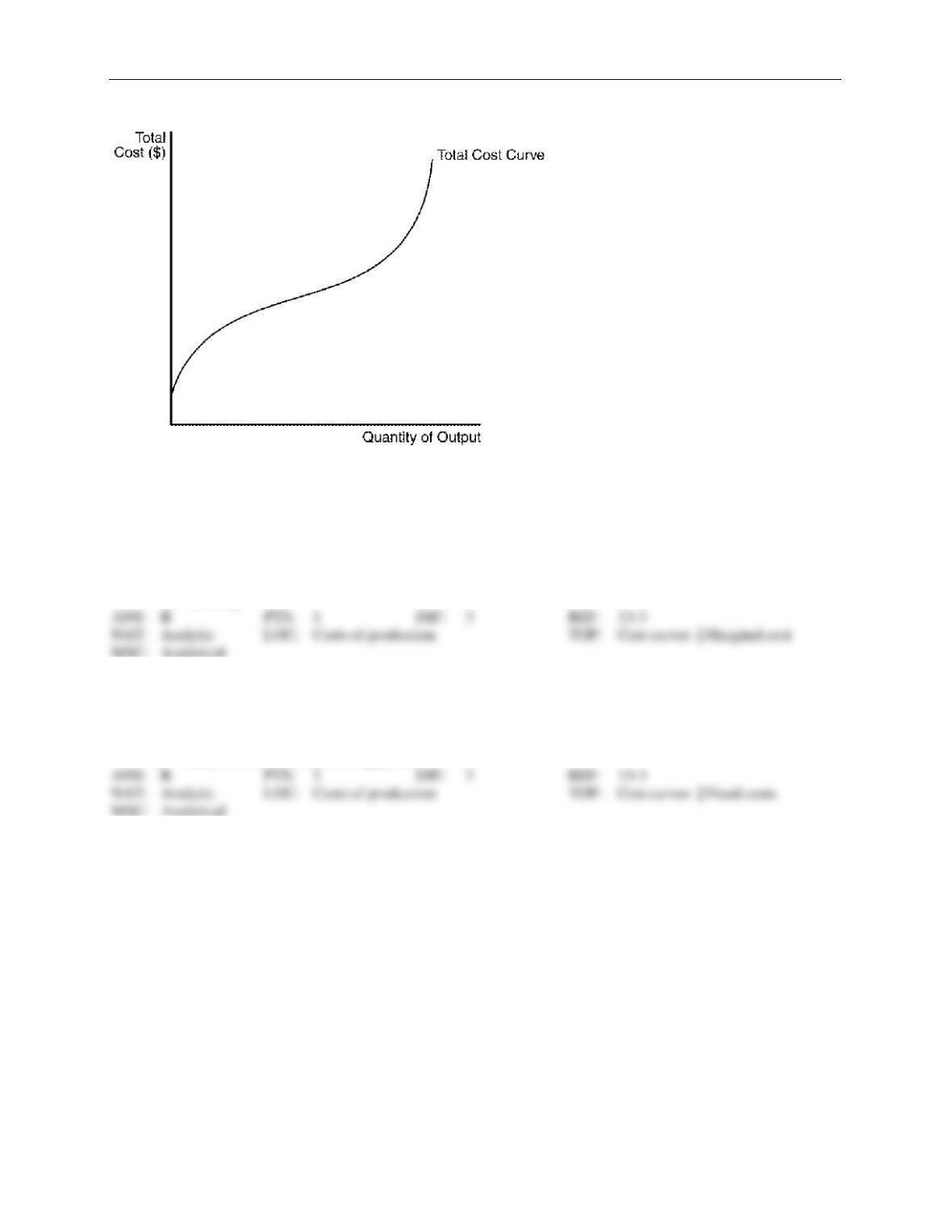

Figure 13-6

156. Refer to Figure 13-6. Which of the following can be inferred from the figure above?

(i)

Marginal cost is increasing at all levels of output.

(ii)

Marginal product is increasing at low levels of output.

(iii)

Marginal product is decreasing at high levels of output.

a.

(i) and (ii) only

b.

(ii) and (iii) only

c.

(i) and (iii) only

d.

(ii) only

157. Refer to Figure 13-6. Why doesn’t the total cost curve begin at the origin (the point 0,0)?

a.

because variable costs are positive when output is zero

b.

because fixed costs are positive when output is zero

c.

because the firm is producing at the efficient scale

d.

because the firm is maximizing profits

Chapter 13/The Costs of Production ❖ 73

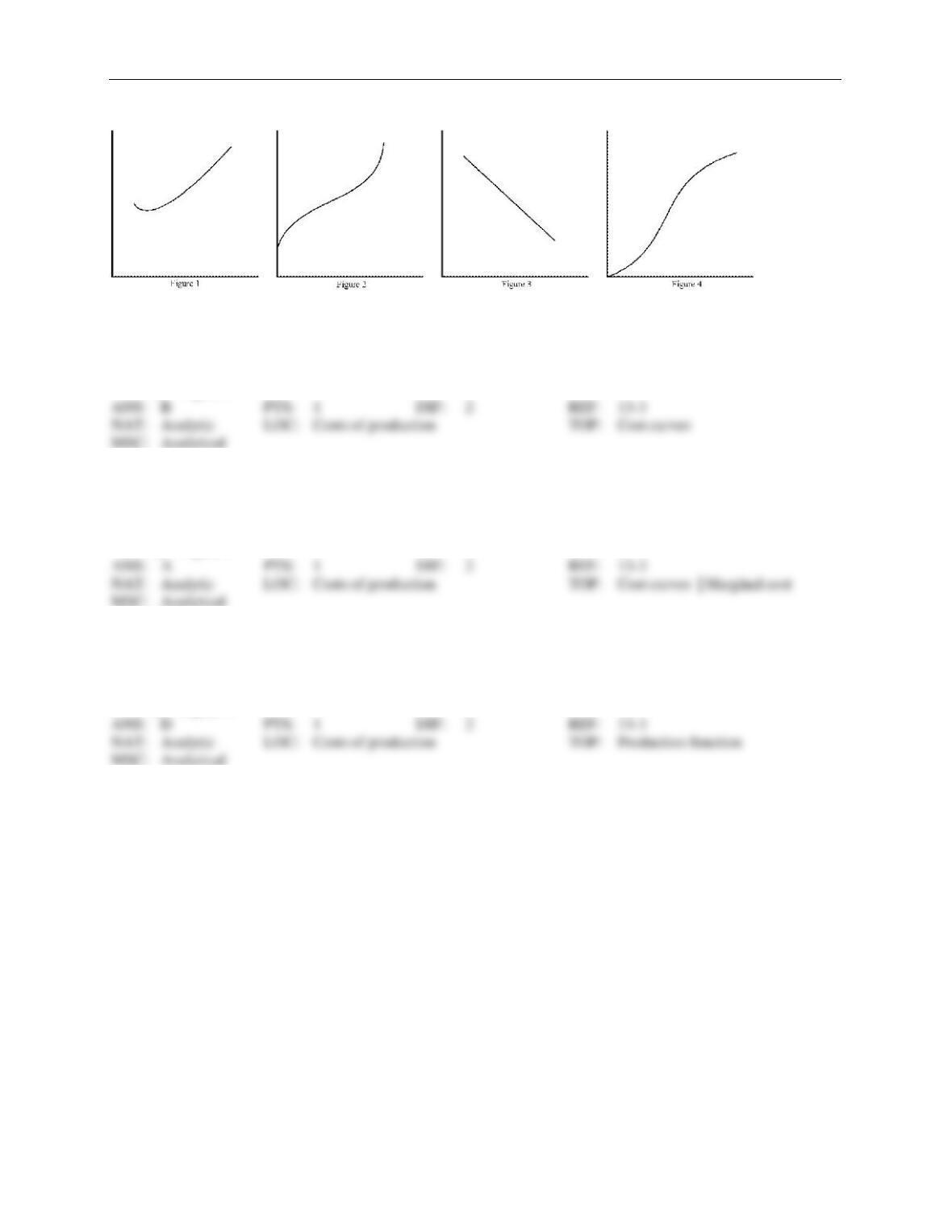

Figure 13-7

158. Refer to Figure 13-7. Which of the figures represents the total cost curve for a typical firm?

a.

Figure 1

b.

Figure 2

c.

Figure 3

d.

Figure 4

159. Refer to Figure 13-7. Which of the figures represents the marginal cost curve for a typical firm?

a.

Figure 1

b.

Figure 2

c.

Figure 3

d.

Figure 4

160. Refer to Figure 13-7. Which of the figures represents the production function for a typical firm?

a.

Figure 1

b.

Figure 2

c.

Figure 3

d.

Figure 4

74 ❖ Chapter 13/The Costs of Production

Figure 13-8

161. Refer to Figure 13-8. The efficient scale of production occurs at which quantity?

a.

A

b.

B

c.

C

d.

D

162. Refer to Figure 13-8. Quantity C represents the output level where the firm

a.

maximizes profits.

b.

minimizes total costs.

c.

produces at the efficient scale.

d.

minimizes marginal costs.

163. Refer to Figure 13-8. Quantity B represents the output level where the firm

a.

maximizes profits.

b.

minimizes average variable costs.

c.

produces at the efficient scale.

d.

minimizes marginal costs.

164. Which of the following factors is most likely to shift IBM’s total cost and marginal cost curves downward?

a.

a technological advance resulting in increased productivity

b.

higher property taxes charged by the municipal government

c.

increased wages to attract additional computer operators

d.

a reduction in subsidies from the state government

CA D

MC

ATC

AVC

B

Quantity

Cost

Chapter 13/The Costs of Production ❖ 75

165. If marginal cost is equal to average total cost, then

a.

marginal cost is minimized.

b.

average total cost is minimized.

c.

average variable cost is minimized.

d.

marginal cost is zero.

166. Which of the following statements is correct?

a.

If marginal cost is rising, then average total cost is rising.

b.

If marginal cost is rising, then average variable cost is rising.

c.

If average variable cost is rising, then marginal cost is minimized.

d.

If average total cost is rising, then marginal cost is greater than average total cost.

167. The average fixed cost curve

a.

always declines with increased levels of output.

b.

always rises with increased levels of output.

c.

declines as long as it is above marginal cost.

d.

declines as long as it is below marginal cost.

168. Average total cost is very high when a small amount of output is produced because

a.

average variable cost is high.

b.

average fixed cost is high.

c.

marginal cost is high.

d.

marginal product is high.

169. When marginal cost is less than average total cost,

a.

marginal cost must be falling.

b.

average variable cost must be falling.

c.

average total cost is falling.

d.

average total cost is rising.

170. When marginal cost exceeds average total cost,

a.

average fixed cost must be rising.

b.

average total cost must be rising.

c.

average total cost must be falling.

d.

marginal cost must be falling.

76 ❖ Chapter 13/The Costs of Production

171. Average total cost is increasing whenever

a.

total cost is increasing.

b.

marginal cost is increasing.

c.

marginal cost is less than average total cost.

d.

marginal cost is greater than average total cost.

172. Marginal cost is equal to average total cost when

a.

average variable cost is falling.

b.

average fixed cost is rising.

c.

marginal cost is at its minimum.

d.

average total cost is at its minimum.

173. If marginal cost is below average total cost, then average total cost

a.

is constant.

b.

is falling.

c.

is rising.

d.

may rise or fall depending on the size of fixed costs.

174. At all levels of production higher than the point where the marginal cost curve crosses the average variable

cost curve, average variable cost

a.

rises.

b.

remains unaffected.

c.

falls.

d.

All of the above are possible depending on the shape of the marginal cost curve.

175. Which of the following statements about costs is correct?

a.

When marginal cost is less than average total cost, average total cost is rising.

b.

The total cost curve is U-shaped.

c.

As the quantity of output increases, marginal cost eventually rises.

d.

All of the above are correct.

176. Whenever marginal cost is greater than average total cost,

a.

average total cost is rising.

b.

marginal cost is falling.

c.

average total cost is falling.

d.

Both b and c are correct.

Chapter 13/The Costs of Production ❖ 77

177. At what level of output will average variable cost equal average total cost?

a.

when marginal cost equals average total cost

b.

for all levels of output in which average variable cost is falling

c.

when marginal cost equals average variable cost

d.

There is no level of output where this occurs, as long as fixed costs are positive.

178. Which of the following must always be true as the quantity of output increases?

a.

Marginal cost must rise.

b.

Average total cost must rise.

c.

Average variable cost must rise.

d.

Average fixed cost must fall.

179. Which of the following statements is not correct?

a.

The marginal cost of the fifth unit of output equals the total cost of five units minus the total cost of

four units.

b.

The total variable cost of seven units equals the average variable cost of seven units times seven.

c.

If marginal cost is rising, then average variable cost must be rising.

d.

The marginal cost of the fifth unit of output equals the total variable cost of five units minus the

total variable cost of four units.

180. When marginal cost is rising, average variable cost

a.

must be rising.

b.

must be falling.

c.

must be constant.

d.

could be rising or falling.

181. When marginal cost is greater than average cost, average cost is

a.

rising.

b.

falling.

c.

constant.

d.

The direction of change in average cost cannot be determined from this information.

182. When average cost is greater than marginal cost, marginal cost must be

a.

rising.

b.

falling.

c.

constant.

d.

The direction of change in marginal cost cannot be determined from this information.

78 ❖ Chapter 13/The Costs of Production

183. Which of the following is not a property of a firm’s cost curves?

a.

Marginal cost must eventually rise as a result of diminishing marginal product.

b.

Average total cost is U-shaped.

c.

Economies of scale will exist when average total cost falls as output rises.

d.

Average total cost will cross marginal cost at the minimum of marginal cost.

184. If marginal cost is greater than average total cost, then

a.

profits are increasing.

b.

economies of scale are becoming greater.

c.

average total cost remains constant.

d.

average total cost is increasing.

185. The minimum points of the average variable cost and average total cost curves occur where the

a.

marginal cost curve lies below the average variable cost and average total cost curves.

b.

marginal cost curve intersects those curves.

c.

average variable cost and average total cost curves intersect.

d.

slope of total cost is the smallest.

186. Which of the following statements is correct?

a.

For most producers, the average total cost curve never crosses the marginal cost curve.

b.

The average fixed cost curve must eventually rise.

c.

The average total cost curve first rises, then falls with increased output.

d.

The marginal cost curve eventually rises with the quantity of output.

187. The marginal cost curve crosses the average total cost curve at

a.

the efficient scale.

b.

the minimum point on the average total cost curve.

c.

a point where the marginal cost curve is rising.

d.

All of the above are correct.

188. The efficient scale of the firm is the quantity of output that

a.

maximizes marginal product.

b.

maximizes profit.

c.

minimizes average total cost.

d.

minimizes average variable cost.

Chapter 13/The Costs of Production ❖ 79

189. The firm‘s efficient scale is the quantity of output that minimizes

a.

average total cost.

b.

average fixed cost.

c.

average variable cost.

d.

marginal cost.

190. When a firm is operating at an efficient scale,

a.

average variable cost is minimized.

b.

average fixed cost is minimized.

c.

average total cost is minimized.

d.

marginal cost is minimized.

COSTS IN THE SHORT RUN AND IN THE LONG RUN

1. The nature of a firm’s cost (fixed or variable) depends on the

a.

firm’s revenues.

b.

time horizon under consideration.

c.

price the firm charges for output.

d.

explicit but not implicit costs.

2. One assumption that distinguishes short-run cost analysis from long-run cost analysis for a profit-maximizing

firm is that in the short run,

a.

output is not variable.

b.

the number of workers used to produce the firm’s product is fixed.

c.

the size of the factory is fixed.

d.

there are no fixed costs.

3. When a factory is operating in the short run,

a.

it cannot alter variable costs.

b.

total cost and variable cost are usually the same.

c.

average fixed cost rises as output increases.

d.

it cannot adjust the quantity of fixed inputs.

4. The length of the short run

a.

is different for different types of firms.

b.

can never exceed 3 years.

c.

can never exceed 1 year.

d.

is always less than 6 months.

80 ❖ Chapter 13/The Costs of Production

5. How long does it take a firm to go from the short run to the long run?

a.

six months

b.

one year

c.

two years

d.

It depends on the nature of the firm.

6. A local potato chip company plans to operate out of its current factory, which is estimated to last 25 years. All

cost decisions it makes during the 25-year period

a.

are short-run decisions.

b.

are long-run decisions.

c.

involve only maintenance of the factory.

d.

are zero because the cost decisions were made at the beginning of the business.

7. In the short run, a firm that produces and sells cell phones can adjust

a.

how many workers to hire.

b.

the size of its factories.

c.

where to produce along its long-run average-total-cost curve.

d.

All of the above are correct.

8. The total cost to the firm of producing zero units of output is

a.

zero in both the short run and the long run.

b.

its fixed cost in the short run and zero in the long run.

c.

its fixed cost in both the short run and the long run.

d.

its variable cost in both the short run and the long run.

9. In the long run, a firm that produces and sells electronic book readers gets to choose

a.

how many workers to hire.

b.

the size of its factories.

c.

which short-run average-total-cost curve to use.

d.

All of the above are correct.

10. In the long run,

a.

inputs that were fixed in the short run remain fixed.

b.

inputs that were fixed in the short run become variable.

c.

inputs that were variable in the short run become fixed.

d.

variable inputs are rarely used.