15) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

Suppose that a combination of fiscal stimulus and recovery of consumer and business confidence

shifts the IS and AD curves, as shown in the figure, while monetary policy sets the real interest

rate at one percent. If the short-run aggregate supply curve is π = Y – 13, then the resulting

values of output and inflation are ________.

A) $12 trillion & 3 percent

B) $13.5 trillion & 5 percent

C) $9.75 trillion & 0 percent

D) $13.5 trillion & 0 percent

E) $12.5 trillion & 2 percent

16) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

Suppose that a combination of fiscal stimulus and recovery of consumer and business confidence

shifts the IS and AD curves, as shown in the figure. The equilibrium real interest rate is

________ percent.

A) 3

B) one

C) 2.5

D) 2

E) zero

17) How might openness to the global economy influence the debate between policy activists

and nonactivists?

18) How might long policy lags impact the divine coincidence?

13.4 The Taylor Rule

1) According to the Taylor rule, which of the following will lead to a higher nominal federal

funds rate?

A) an increase in inflation

B) a positive output gap

C) a positive inflation gap

D) all of the above

E) none of the above

2) According to the Taylor rule, which of the following will lead to a higher nominal federal

funds rate?

A) a decrease in inflation

B) a negative output gap

C) a positive inflation gap

D) all of the above

E) none of the above

3) According to the Taylor rule, which of the following will lead to the largest increase in the

nominal federal funds rate?

A) a two percentage point increase in the target inflation rate

B) a one percentage point decrease in the target inflation rate

C) a one percentage point increase in output

D) a two percentage point decrease in output

E) a one percentage point increase in the inflation rate

4) If the inflation rate target is 2%, the current inflation rate is also 2%, and the output gap is

zero, then according to the Taylor rule, the nominal federal funds rate should be ________

percent.

A) zero

B) two

C) four

D) three

E) none of the above

5) If the inflation rate target is 2%, the current inflation rate is 3%, and the output gap is 2%, then

according to the Taylor rule, the nominal federal funds rate should be ________ percent.

A) 4.5

B) 7

C) 6.5

D) 5.5

E) none of the above

6) If the inflation rate target is 2%, the current inflation rate is 1%, and the output gap is minus

2%, then according to the Taylor rule, the nominal federal funds rate should be ________

percent.

A) zero

B) two

C) four

D) three

E) none of the above

7) Since 2010, the federal funds rate has been well below the rate suggested by the Taylor rule. A

likely explanation for the discrepancy is that ________.

A) the Fed’s dual mandate prevents a close reliance on the Taylor rule

B) policy makers decided that instability of the coefficients prevents the Taylor rule from having

any role in policy decisions

C) in the past, adherence to the Taylor rule led to policy mistakes

D) all of the above

E) none of the above

8) Is the Taylor rule of greater use to activist or to nonactivist policy makers?

20

9) Is the Taylor rule compatible with a hierarchical mandate?

13.5 Inflation: Always and Everywhere A Monetary Phenonenon

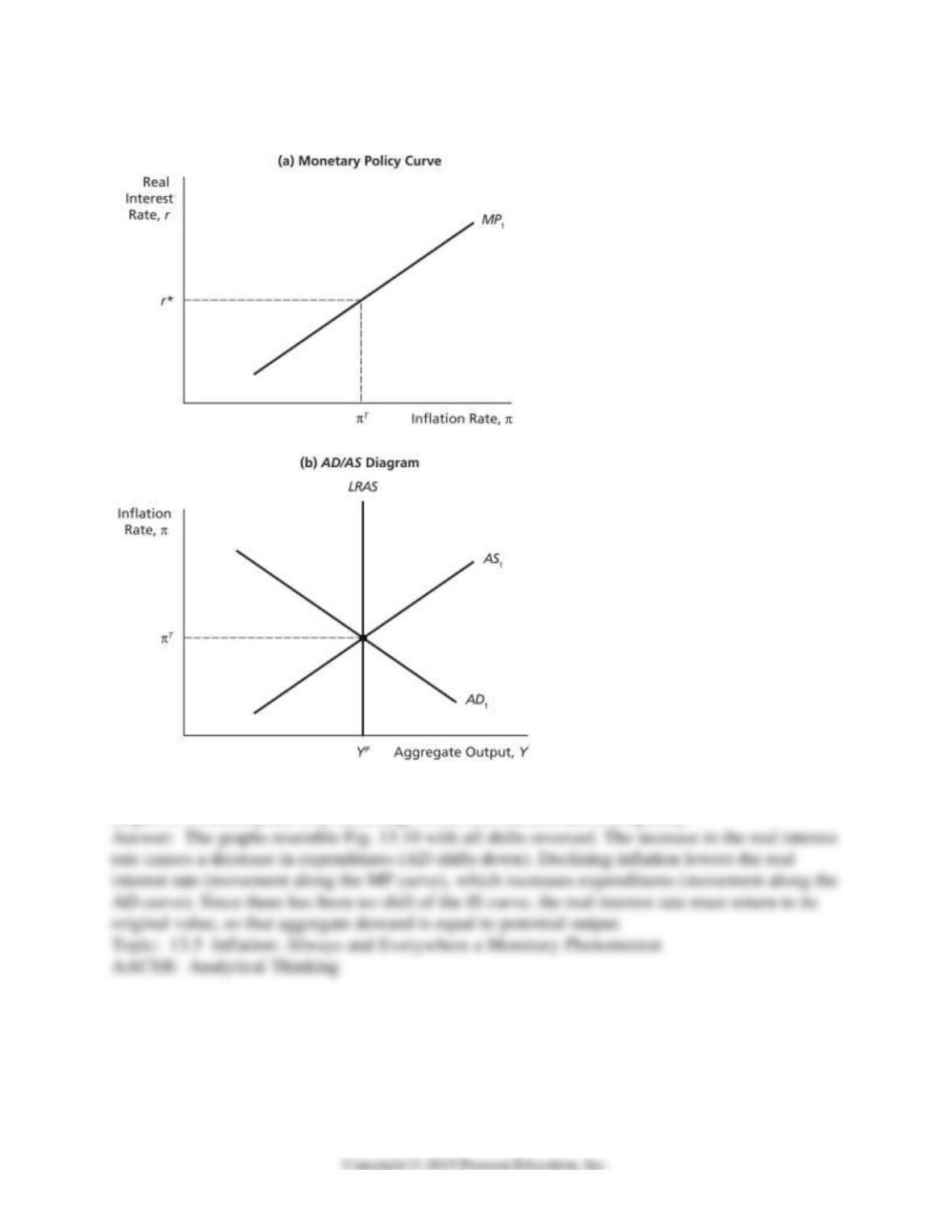

1) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) it would likely conduct an easing of monetary policy by raising the real interest rate for any

given inflation rate

B) it would likely conduct a tightening of monetary policy by raising the real interest rate for any

given inflation rate

C) it would likely conduct an easing of monetary policy where the real interest rate would

increase due to the ensuing decrease in aggregate demand

D) it would likely conduct a tightening of monetary policy where the real interest rate would

increase due to the ensuing increase in aggregate demand

E) none of the above

2) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) it would likely conduct a tightening of monetary policy by raising the real interest rate for any

given inflation rate

B) it would likely conduct an easing of monetary policy by lowering the real interest rate for any

given inflation rate

C) it would likely conduct an easing of monetary policy where the real interest rate would

increase due to the ensuing decrease in aggregate demand

D) it would likely conduct a tightening of monetary policy where the real interest rate would

increase due to the ensuing increase in aggregate demand

21

3) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) it would likely conduct an easing of monetary policy by lowering the real interest rate for any

given inflation rate

B) an increase in aggregate demand would ensue generating a positive output gap

C) an eventual decrease in short-run AS would drive the long-run equilibrium level of inflation

up

D) all of the above

E) none of the above

4) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) it would conduct monetary policy consistent with a downward shift of the MP curve

B) it would conduct monetary policy that would lead to a rightward shift of the AD curve

C) after an easing of monetary policy, an eventual decrease in short-run AS would drive the

long-run equilibrium level of inflation up

D) all of the above

E) none of the above

5) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) monetary policy would ultimately lead to higher inflation and real interest rates in the long

run

B) monetary policy would ultimately lead to higher inflation and thus higher potential output

C) monetary policy would ultimately lead to higher potential output and real interest rates but no

long-run impact on inflation

D) all of the above

E) none of the above

22

6) If the economy is in a long-run equilibrium when the Federal Reserve decides that its inflation

target is too low and chooses to raise it, ________.

A) monetary policy would ultimately lead to higher potential output but real interest rates and

inflation would be unaffected in the long run

B) monetary policy would ultimately lead to higher inflation but real interest rates and potential

output would be unaffected in the long run

C) monetary policy would ultimately lead to higher interest rates but potential output and

inflation would be unaffected in the long run

D) monetary policy would ultimately lead to higher interest rates, potential output, and inflation

in the long run

E) none of the above

7) Which of the following statements is correct?

A) Through autonomous monetary policy adjustments the Federal Reserve can ultimately

determine the equilibrium real interest rate in the long run.

B) Through autonomous monetary policy adjustments the Federal Reserve can ultimately

determine potential output in the long run.

C) Through autonomous monetary policy adjustments the Federal Reserve can target any

inflation rate in the long run.

D) all of the above

E) none of the above

8) Which of the following statements is correct?

A) Through autonomous monetary policy adjustments the Federal Reserve can target any

inflation rate in the long run.

B) Ultimately, autonomous monetary policy adjustments by the Federal Reserve cannot

determine the equilibrium real interest rate in the long run.

C) Ultimately, autonomous monetary policy adjustments by the Federal Reserve cannot

determine long run aggregate output.

D) all of the above

E) none of the above

23

9) “With autonomous changes in the policy interest rate, the Federal Reserve cannot determine

the long run equilibrium level of the real interest rate or potential output and will only be able to

determine inflation.” This statement is consistent with ________.

A) the notion that shifts in the MP curve may lead to shifts in the AD and AS curves but the

LRAS remains unchanged

B) the notion of long-run independence between nominal and real variables

C) the notion of monetary neutrality

D) all of the above

E) none of the above

24

Macroeconomic Shocks & Policies

10) On the graphs above, show how the central bank implements a decrease in the inflation

target. In words, explain why the change in the real interest rate is temporary.

13.6 Causes of Inflationary Monetary Policy

1) Cost-push inflation is to ________ as demand-pull inflation is to ________.

A) impatience; inaccuracy

B) entering; exiting

C) activism; nonactivism

D) fiscal; monetary

E) none of the above

2) An activist policy to promote high employment ________.

A) could lead to inflationary pressures from an ensuing temporary negative supply shock

B) might incentivize workers to push for higher wages beyond what productivity gains can

justify

C) could lead to inflationary pressures from an ensuing increase in aggregate demand

D) all of the above

E) none of the above

3) If workers push for wages that are beyond what productivity gains can justify ________.

A) a positive output gap ensues which will lead to lower unemployment if the Federal Reserve

does not act

B) a temporary negative supply shock ensues driving up prices

C) and the Federal Reserve eases monetary policy aimed at increasing aggregate demand to

counter the negative supply shock, the inflation rate will decrease

D) all of the above

E) none of the above

4) If workers push for wages that are beyond what productivity gains can justify ________.

A) a temporary negative supply shock ensues driving up prices

B) a negative output gap ensues which will lead to higher unemployment if the Federal Reserve

does not act

C) and the Federal Reserve eases monetary policy aimed at increasing aggregate demand to

counter the negative supply shock, a price-wage spiral could ensue

D) all of the above

E) none of the above

26

5) A goal of very high employment may lead to ________.

A) inflationary monetary policy

B) inflationary fiscal policy

C) demand-pull inflation

D) all of the above

E) none of the above

6) High inflation that persists beyond the ending of expansionary policies is probably ________.

A) demand-pull inflation

B) Humphrey-Hawkins inflation

C) cost-push inflation

D) a result of unemployment remaining below the natural rate

E) none of the above

7) In the 1965 to 1973 period, U.S. policymakers ________.

A) targeted an unemployment rate that, in hindsight, was likely too low

B) pursued an easing of monetary policy designed to increase aggregate demand

C) made some mistakes that led to the most sustained inflationary episode in U.S. history

D) all of the above

E) none of the above

8) After 1975, the U.S. economy continued to experience high inflation ________.

A) mainly because the public expected policymakers to continue their expansionary efforts, and

this led to increases in inflation expectations

B) most likely of the cost-push kind

C) until a very aggressive commitment to anti-inflationary monetary policy helped end this Great

Inflation period

D) all of the above

E) none of the above

27

9) How might strict adherence to the Taylor rule discourage demand-pull inflation? How might

demand-pull inflation occur, nonetheless?

13.7 Monetary Policy at the Zero Lower Bound

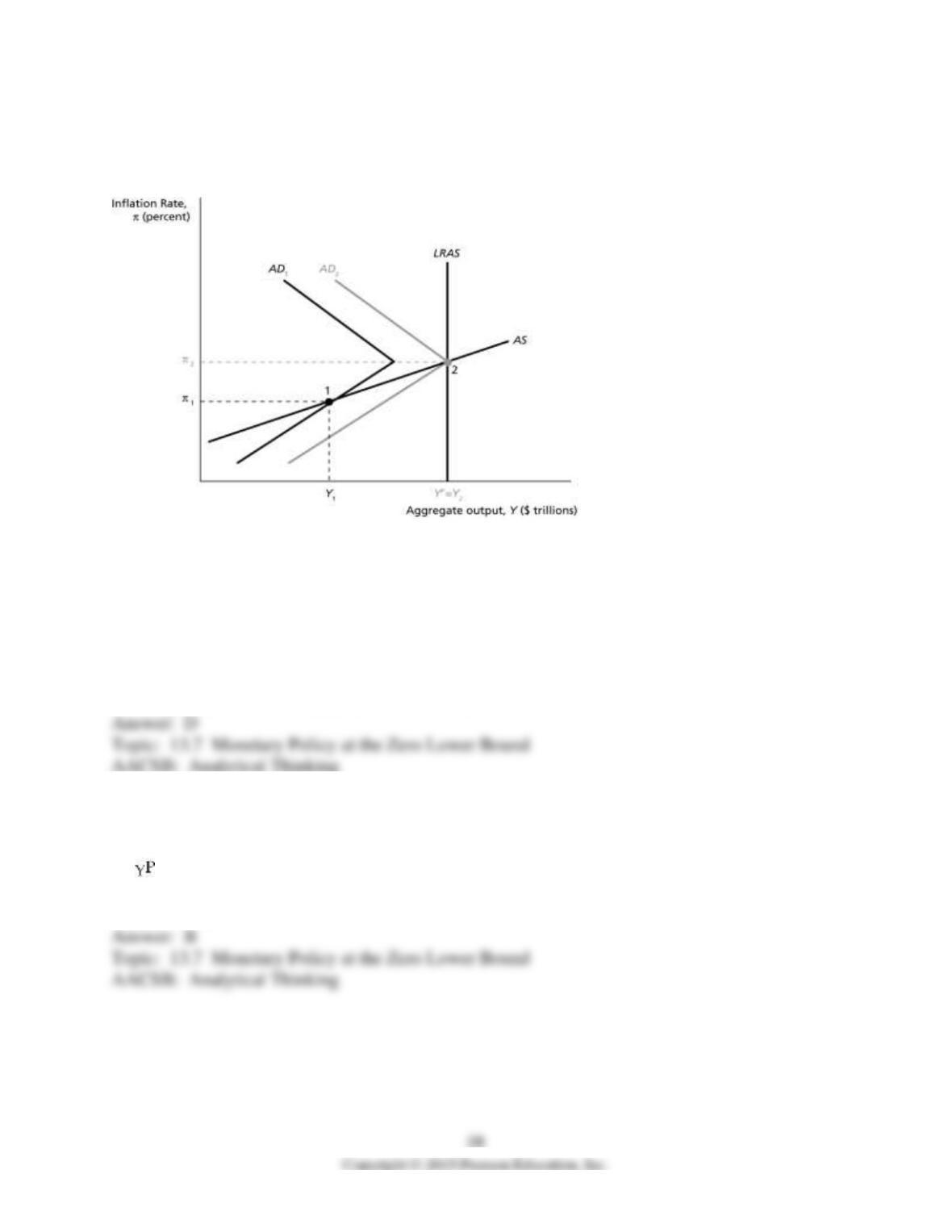

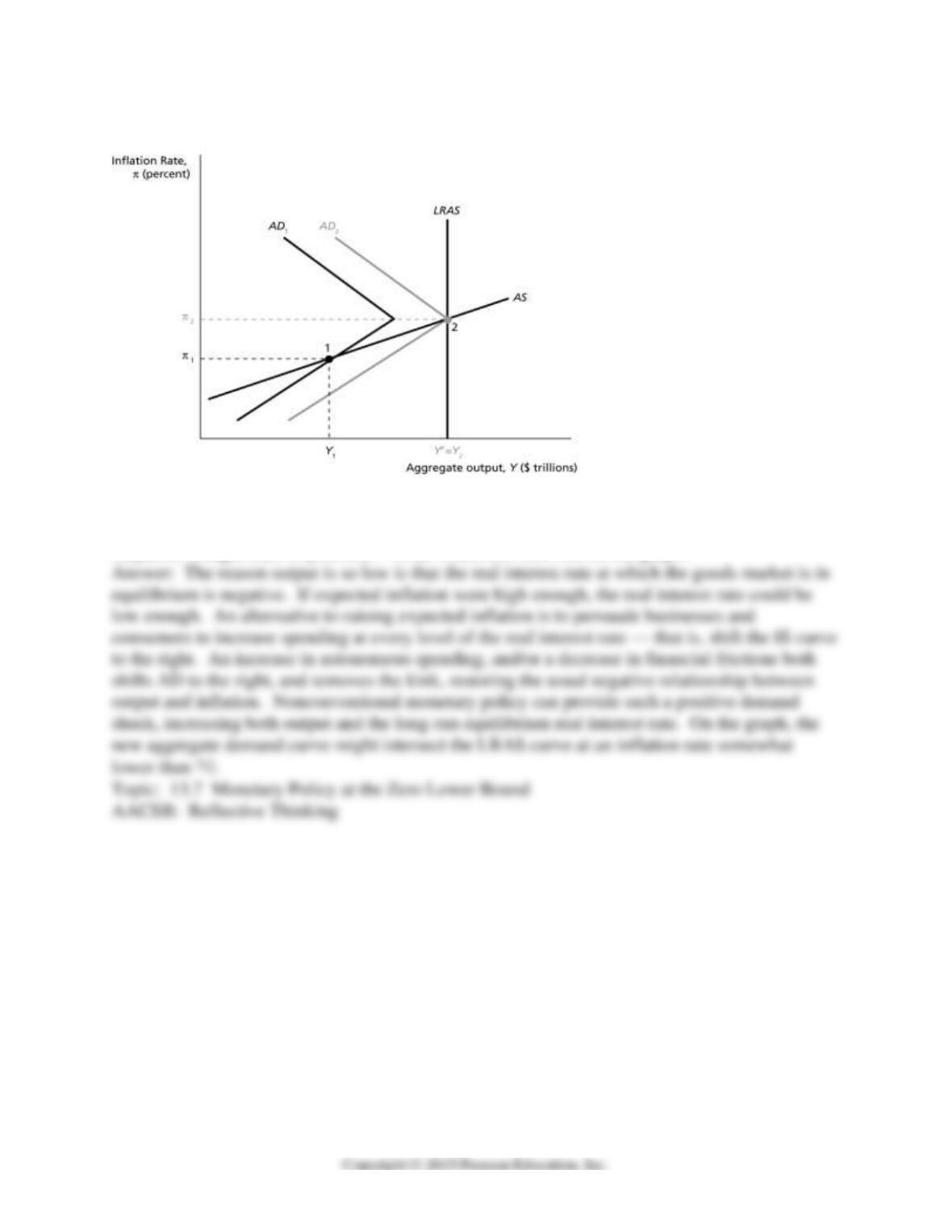

Figure 13.1

1) The aggregate demand curves in Figure 13.1 have a positively-sloped portion. The reason this

can happen is ________.

A) sloppy editing

B) the monetary policy response to declining inflation causes the real interest rate to fall, which

causes output to rise

C) a sudden increase in potential output

D) changes in expected inflation cause the real interest rate to change in the opposite direction

E) rising inflation causes financial frictions to increase

2) In Figure 13.1, “the zero lower bound” is displayed at ________.

A) point 1

B) point 2

C)

D) the origin (intersection of the axes)

E) none of the above

3) If the economy is at point 1 in Figure 13.1 and there is no policy intervention, what happens

next?

A) the economy moves to point 2

B) the economy remains at point 1

C) the economy moves to the left along the AS curve

D) the AS curve shifts down, causing both output and inflation to decline

E) the AS curve shifts up, causing both output and inflation to rise

4) If the economy is at point 1 in Figure 13.1 and the central bank issues a credible statement that

it can and will cause inflation to rise, what happens next?

A) the economy moves to point 2

B) the economy remains at point 1

C) the economy moves to the left along the AS curve

D) the AS curve shifts down, causing both output and inflation to decline

E) the AS curve shifts up, causing both output and inflation to rise

5) Which is a plausible cause of the movement in Figure 13.1 from point 1 to point 2?

A) a change in expectations that causes a decline in the real interest rate for investments

B) a decrease in expected inflation

C) the economy’s self-correcting mechanism

D) the central bank achieves a negative value for the nominal interest rate

E) none of the above

6) Nonconventional monetary policy attempts to reduce financial frictions by ________.

A) correcting the shortage of liquidity that has made it costly for businesses to invest

B) purchasing long-term assets, which raises their price and reduces the credit spread

C) reducing the expected future short-term interest rate

D) all of the above

E) none of the above

7) Nonconventional monetary policy attempts to reduce financial frictions by ________.

A) reversing the expansion of the central bank’s balance sheet that has made it costly for

businesses to invest

B) purchasing short-term assets, which raises their price and reduces the credit spread

C) increasing the expected future short-term interest rate

D) all of the above

E) none of the above

8) The key difference between “quantitative easing” and “credit easing” is that ________.

A) the goal of the former is to raise expected inflation

B) the latter refers to a substantial change in the composition of the central bank’s balance sheet

C) the latter refers to a substantial expansion of the central bank’s balance sheet

D) the former is endorsed by Federal Reserve Chairman Ben Bernanke, while the latter was

devised by Japan’s Prime Minister Shinzo Abe

E) none of the above

9) In the absence of financial frictions, ________.

A) interest rates for different borrowers move closely together

B) all loans in the economy are transacted at a common interest rate

C) the level of output is not affected by changes in the real interest rate

D) an increase in inflation leads to a decrease in the real interest rate

10) An increase in financial frictions results in ________.

A) an increase in output and inflation

B) a rise in the interest rate set by monetary policy

C) a decline in the real interest rates faced by households and firms

D) a decline in the interest rate set by monetary policy

11) An increase in financial frictions results in ________.

A) a movement to the left along the AD curve

B) a leftward shift of the MP curve

C) a decrease in output and increase in inflation

D) a leftward shift of the IS curve

31

12) An increase in financial frictions results in ________.

A) an increase in the federal funds rate

B) a reduced supply of credit to households and businesses

C) a decrease in short-run aggregate supply

D) an upward shift of the monetary policy curve

13) When the credit spread rises, an effective policy response might be to ________.

A) lower the real interest rate on safe assets

B) prevent the real federal funds rate from falling below zero

C) pursue nonconventional monetary policies to restore the functioning of financial markets

32

Figure 13.1

14) Suppose the economy is at point 1 in Figure 13.1. With output below potential output, it

might not be possible to create any expectation of an increase in inflation. How, then, might

output be brought back to potential? What would this look like on the graph?