Macroeconomics: Policy and Practice, 2e (Mishkin)

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis

13.1 The Objectives of Macroeconomic Policy

1) Which of the following is a primary objective of macroeconomic policy?

A) achieving a zero rate of unemployment

B) achieving a zero rate of inflation

C) stabilizing economic activity

D) all of the above

E) none of the above

2) Which of the following is a primary objective of monetary policy?

A) achieving a zero natural rate of unemployment

B) targeting a zero rate of inflation

C) achieving price stability

D) all of the above

E) none of the above

3) Frictional unemployment is to ________ as structural unemployment is to ________.

A) search; mismatch

B) temperature; rigidity

C) job training; output gap

D) all of the above

E) none of the above

4) A good reason for policy makers to pursue a goal of stabilizing economic activity is that

________.

A) high unemployment is always accompanied by high variability of unemployment

B) in a stable economy, there is little or no frictional unemployment

C) in a stable economy, there is little or no structural inflation

D) all of the above

E) none of the above

2

5) A good reason for policy makers to pursue a goal of stabilizing economic activity is that

________.

A) high inflation is always accompanied by high variability of inflation

B) high unemployment causes human misery and lost output

C) in a stable economy, there is little or no structural inflation

D) all of the above

E) none of the above

6) The goal of maximum sustainable employment is roughly equivalent to achieving ________.

A) the natural rate of unemployment

B) an inflation target that is slightly above zero

C) the elimination of frictional and structural unemployment

D) all of the above

E) none of the above

7) Which of the following is a likely objective of monetary policy?

A) achieving price stability

B) stabilizing economic activity

C) closing the output gap to zero

D) all of the above

E) none of the above

8) Which of the following is a likely objective of monetary policy?

A) achieving a zero inflation gap

B) stabilizing economic activity

C) avoiding large changes in unemployment

D) all of the above

9) Some central banks pursue price stability before they pursue other goals. Which of the

following central banks have this kind of hierarchical mandate?

i. Bank of England

ii. Bank of Canada

iii. European Central Bank

iv. Federal Reserve (U.S.A.)

A) i, ii, and iv only

B) i and iii only

C) i and iv only

D) ii, iii, and iv only

E) none of the above

10) A central bank with a hierarchical mandate will seek ________ as a condition of pursuing

other goals.

A) stable inflation

B) high employment

C) moderate interest rates

D) the approval of the legislature

E) none of the above

11) Suppose that inflation is at the target rate and output has fallen substantially below potential

output. A central bank with a primary objective of price stability should ________.

A) do nothing, because inflation cannot rise when unemployment is high

B) ease monetary policy, to avoid a decrease in the inflation rate

C) do nothing, because stabilizing economic activity is not a primary objective

D) ease monetary policy, because avoiding high unemployment is more important than avoiding

high inflation

E) none of the above

12) In recent decades, the trend among central banks has been to adopt ________.

A) high employment as a central goal

B) a dual mandate that gives equal weight to both price stability and low unemployment.

C) price stability as a central goal

D) a target of zero inflation

E) none of the above

4

13) How do the hierarchical and dual mandates differ in terms of macroeconomic consequences?

13.2 The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

1) The equilibrium real interest rate is the rate ________.

A) at which the output gap is zero

B) at which the inflation rate is low

C) controlled by the central bank

D) all of the above

E) none of the above

2) A change in the equilibrium real interest rate may result from ________.

A) an autonomous monetary policy

B) a change in the central bank’s target inflation rate

C) a change in expected inflation

D) all of the above

E) none of the above

3) Every six weeks, the Federal Open Market Committee (FOMC) meets to discuss monetary

policy. This discussion is mainly focused on ________.

A) information of the equilibrium real interest rate from the past three years

B) the current month’s release of the CPI by the BLS

C) the three year projections of the equilibrium real interest rate

D) the past 18 month history and future 18 month projections of the discount rate

E) none of the above

5

4) Shocks to the macroeconomy will cause a change in the equilibrium real interest rate, except

________.

A) permanent supply shocks

B) aggregate demand shocks

C) temporary supply shocks

D) all of the above

E) none of the above

5) Every six weeks, the Federal Open Market Committee (FOMC) meets to discuss how to best

adjust ________ to accommodate shocks that shift the level of ________.

A) the equilibrium real interest rate; the target Fed Funds rate

B) the target Fed Funds rate; the equilibrium real interest rate

C) the 3 month T-bill rate; the inflation gap

D) target rate of inflation; money demand

E) none of the above

6) Ceteris Paribus, if current output has fallen below potential ________.

A) a positive inflation gap will ensue

B) it is likely that the equilibrium real rate has fallen below the policy rate

C) a negative unemployment gap will ensue

D) it is likely that the equilibrium real rate has risen above the policy rate

E) none of the above

7) Many borrowers defaulted on subprime mortgages ultimately disrupting financial markets by

August 2007. Which of the following is a likely result of this increase in financial frictions?

A) The AD curve likely shifted left which caused a positive inflation gap.

B) The AD curve likely shifted right which caused a positive inflation gap.

C) The AD curve likely shifted left which caused an upward movement along the MP curve to a

higher general equilibrium interest rate.

D) The AD curve likely did not shift.

E) none of the above

8) Many borrowers defaulted on subprime mortgages ultimately disrupting financial markets by

August 2007. Which of the following is a likely result of this increase in financial frictions?

A) The AD curve likely shifted left which caused a negative output gap.

B) The AD curve likely shifted left which caused a positive inflation gap.

C) The AD curve likely shifted left which caused an upward movement along the MP curve to a

higher general equilibrium interest rate.

D) The AD curve likely did not shift.

E) none of the above

9) Many borrowers defaulted on subprime mortgages ultimately disrupting financial markets by

August 2007. Which of the following is a likely result of this increase in financial frictions?

A) The AD curve likely shifted left which caused a negative output gap.

B) The AD curve likely shifted left causing a negative inflation gap.

C) The AD curve likely shifted left followed by an downward movement along the MP curve to

a lower equilibrium interest rate in the short run.

D) all of the above

E) none of the above

10) A negative shock in aggregate demand will likely result in ________.

A) a short run decrease in output

B) a permanently lower equilibrium inflation rate if the central bank does not respond by

lowering interest rates

C) an eventual increase in aggregate supply for any inflation rate if the central bank does not

respond by lowering interest rates

D) all of the above

E) none of the above

11) A negative shock in aggregate demand will likely result in ________.

A) a permanent change in output, unless the central bank responds by lowering interest rates

B) a permanently lower equilibrium inflation rate, unless the central bank responds by lowering

interest rates

C) an eventual increase in aggregate supply for any inflation rate, if the central bank responds by

lowering interest rates

D) all of the above

E) none of the above

12) A negative shock in aggregate demand will likely result in ________.

A) a permanent change in output, if the central bank responds by lowering interest rates

B) no permanent change in the equilibrium inflation rate, unless the central bank responds by

lowering interest rates

C) an eventual increase in aggregate supply for any inflation rate, if the central bank responds by

lowering interest rates

D) all of the above

E) none of the above

13) A negative shock in aggregate demand will likely result in no permanent change in

________.

A) output

B) the equilibrium inflation rate if the central bank responds by lowering interest rates

C) aggregate demand, if the central bank responds by lowering interest rates

D) all of the above

E) none of the above

14) When an aggregate demand shock hits the economy ________.

A) there is no conflict for the central bank between pursuing price or output stability because of

the divine coincidence

B) the same long-run equilibrium real interest rate is reached whether the central bank intervenes

or not

C) the long-run level of output is unaffected

D) all of the above

E) none of the above

15) When a permanent negative supply shock hits the economy, a permanently ________.

A) lower equilibrium level of output ensues if the central bank raises interest rates

B) lower equilibrium level of output ensues if the central bank does not respond

C) higher equilibrium level of inflation ensues if the central bank does not respond

D) all of the above

E) none of the above

16) When a permanent negative supply shock hits the economy ________.

A) in the long-run, the output gap returns to zero only if the central bank raises interest rates

B) the long-run equilibrium level of output depends on whether and how the central bank

responds

C) there is no permanent effect on inflation if the central bank raises interest rates

D) all of the above

E) none of the above

17) When a permanent negative supply shock hits the economy ________.

A) in the long-run, output is permanently lowered whether the central bank reacts or not

B) inflation decreases in the short-run

C) there is no long-run effect on inflation whether the central bank reacts or not

D) all of the above

E) none of the above

18) When a temporary negative supply shock hits the economy ________.

A) the divine coincidence does not always hold

B) the divine coincidence holds in the short-run

C) the divine coincidence does not hold in the long-run

D) all of the above

E) none of the above

19) When a temporary negative supply shock hits the economy, then in the short-run ________.

A) if the central bank focuses on stabilizing output, it cannot stabilize inflation

B) if the central bank focuses on stabilizing inflation, it cannot stabilize output

C) the divine coincidence does not hold

D) all of the above

E) none of the above

20) If higher inflation ensues from a temporary negative supply shock, and in response, the

central bank raises interest rates, then ________.

A) it is likely adopting a policy to stabilize inflation in the short run

B) short-run inflation will fluctuate around (first go higher then go lower than) the long run level

of inflation

C) it will need to lower interest rates back to their original values to ensure that inflation returns

to its original rate

D) all of the above

E) none of the above

21) If higher inflation ensues from a temporary negative supply shock, and in response, the

central bank raises interest rates, then the resulting decrease in AD will return inflation back to

its original level ________.

A) and no further action will be required by the central bank

B) but the ensuing positive output gap will lead to higher inflation once again so further interest

rate increases will be required by the central bank to return inflation back to its long run level

C) but the ensuing negative output gap will lead to short-run increases in AS and the central bank

will have to “undo” its original interest rate hike in order to return inflation back to its target rate

D) all of the above

E) none of the above

22) If most shocks to the economy are ________ shocks, then ________.

A) aggregate demand; inflation stabilization policy will also stabilize activity in the short-run

B) permanent aggregate supply; inflation stabilization policy will also stabilize activity in the

short-run

C) temporary aggregate supply; inflation stabilization policy has no impact on economic activity

in the long-run

D) all of the above

E) none of the above

10

23) If most shocks to the economy are ________ shocks, then ________.

A) aggregate demand; there is a tradeoff between the dual objectives in the short-run

B) temporary aggregate supply; inflation stabilization policy will not stabilize activity in the

short-run

C) temporary aggregate supply; output stabilization policy is consistent with no change in

inflation in the long-run

D) all of the above

E) none of the above

24) What is the divine coincidence? When and why does it not hold true?

11

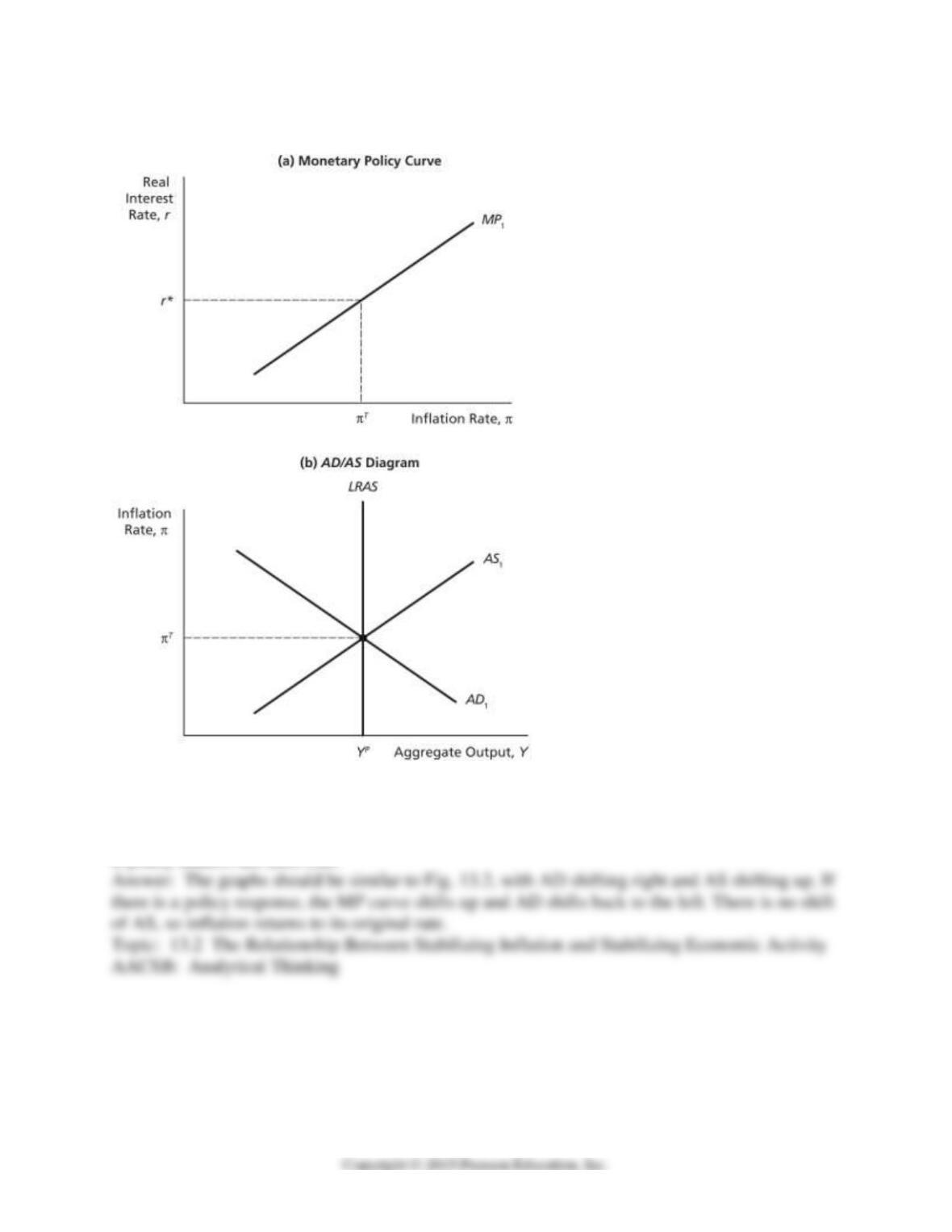

Macroeconomic Shocks & Policies

25) Suppose the economy is in a long-run equilibrium when a positive demand shock occurs. On

the graphs above, show what happens to bring the economy back to long-run equilibrium,

assuming that there is no policy response. In words, describe how the graph would be different,

if policy makers did intervene.

26) Suppose the economy is in a long-run equilibrium when a temporary, favorable aggregate

supply shock occurs. On the graphs above, show what happens to bring the economy back to

long-run equilibrium, assuming that there is no policy response. In words, explain why “no

response” is the best policy.

13.3 How Actively Should Policy Makers Try To Stabilize Economic Activity?

1) The time it takes for policymakers to obtain and to understand the data and to change the

policy instrument based on that information is known as ________, respectively.

A) the data, recognition, and effectiveness lags

B) the recognition, data, and effectiveness lags

C) the data, recognition, and implementation lags

D) the recognition, implementation, and effectiveness lags

E) the data, implementation, and effectiveness lags

2) What do the legislative and implementation lags have in common?

A) They are both more important for monetary than fiscal policy.

B) They are both more important for fiscal than monetary policy.

C) They are both harder to measure but less variable than the effectiveness lag.

D) They both take place before the data and recognition lags.

E) none of the above

3) Nonactivists believe that ________.

A) there is a very rapid self-correcting mechanism since prices and wages are very flexible

B) lags to policy implementation are so long that even the “correct” policies may lead to

undesirable consequences

C) policy interventions should take place less frequently than what Keynesians advocate

D) all of the above

E) none of the above

4) Activists believe that ________.

A) frictions to the self-correcting mechanism of markets prevent prices and wages from being

very flexible

B) it takes a very long time to reach the long run

C) Keynes was right with his statement “in the long-run, we are all dead”

D) all of the above

E) none of the above

5) Which statement is a good argument in support of policy activism?

A) Policy lags are generally longer than the time it takes the self-correcting mechanism to work.

B) Activist policies help to ensure stability of the real interest rate.

C) Well-considered policies can assist the economy’s self-correcting mechanism, thus reducing

the variability of inflation and unemployment.

D) all of the above

E) none of the above

6) An emphasis on inflation stability is compatible with a nonactivist stance only when shocks to

the macroeconomy are ________.

A) permanent supply shocks

B) temporary supply shocks

C) aggregate demand shocks

D) all of the above

E) none of the above

7) The American Recovery and Reinvestment Act of 2009 ________.

A) was a result of the Obama administration adopting an activist approach to policymaking

B) is still being debated after the fact in terms of its effectiveness

C) was supported by some economists, and opposed by as many economists

D) all of the above

E) none of the above

14

8) The American Recovery and Reinvestment Act of 2009 ________.

A) placed greater emphasis on monetary policy than fiscal policy

B) finally put an end to the inflationary spiral that had begun in 2005

C) was intended to reverse the sharp increase in the equilibrium real interest rate

D) all of the above

E) none of the above

9) Suppose that wages and prices are quite flexible, so that the short-run aggregate supply curve

is steep. In that case, ________.

A) policies to stabilize inflation are probably needed more than policies to stabilize economic

activity

B) supply shocks will destabilize inflation, but have minimal impact on output

C) demand shocks will destabilize output, but have minimal impact on inflation

D) all of the above

E) none of the above

10) Suppose that data for a particular economy over time suggest that its aggregate demand

curve is both steep and shifts frequently. We might reasonably infer that ________.

A) the central bank has an activist emphasis on the stability of economic activity

B) wages and prices are remarkably flexible

C) policy lags are quite long

D) all of the above

E) none of the above

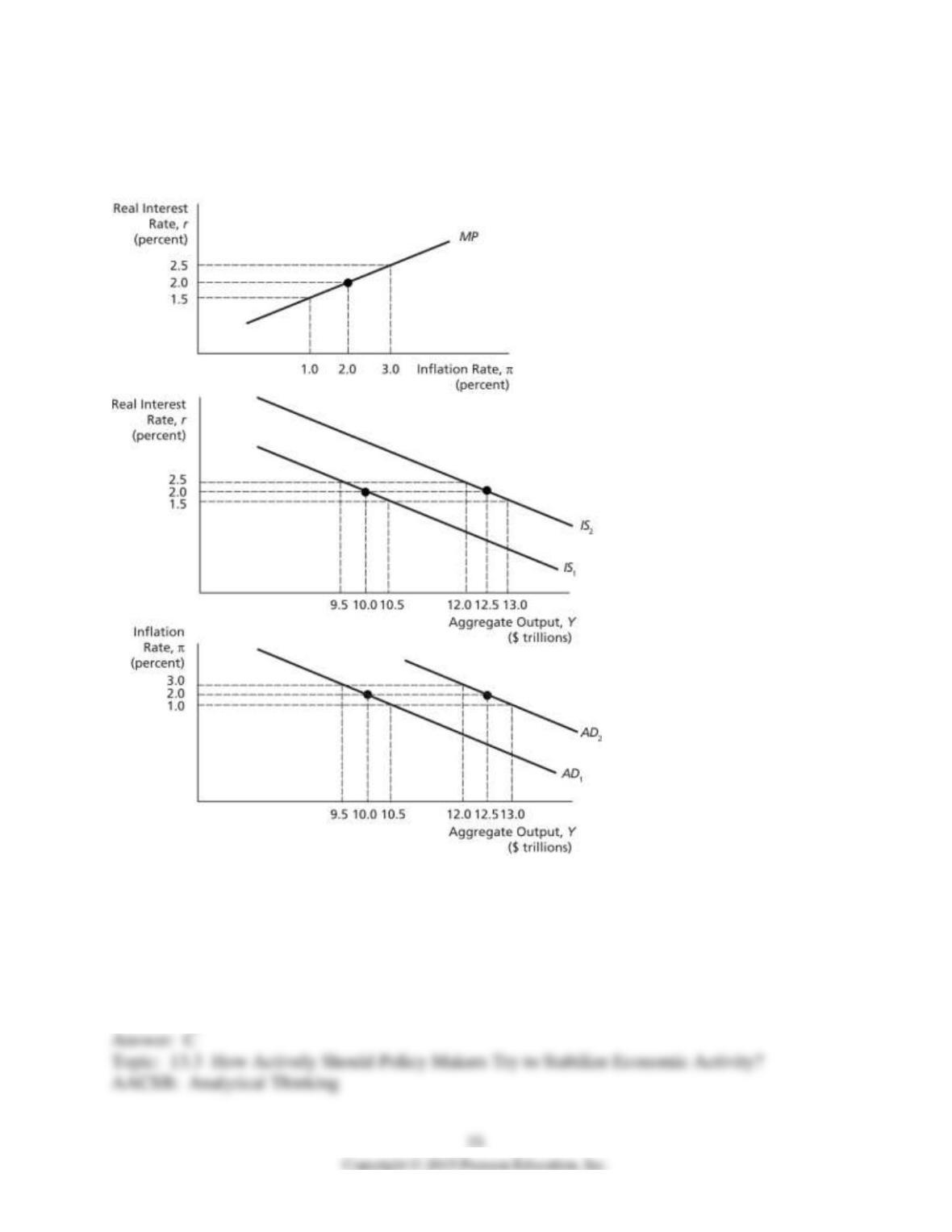

Aggregate Demand and Supply Analysis

11) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

If there is no policy intervention, we should expect ________.

A) rightward shifts of IS & AD, so that both output and inflation rise

B) a decrease in inflation to shift the MP curve, raising the real interest rate

C) declines in both the inflation rate and the real interest rate as output rises

D) a decrease in inflation to shift the AD curve, causing output to rise

E) none of the above

16

12) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

If a fiscal stimulus package is implemented quickly, raising output to $12 trillion, while inflation

remains constant at one percent, then the figure implies that the real interest rate will be

________ percent.

A) 1.5

B) zero

C) one

D) 0.5

E) 2.5

13) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

If autonomous monetary policy (alone) is used to bring output to $12 trillion, then the figure

implies that the real interest rate will be ________ percent, and the inflation rate will be one

percent.

A) 1.5

B) zero

C) one

D) 0.5

E) 2.5

14) In the figure above, assume that output is $10.5 trillion, while potential output is $12 trillion.

If there is no policy intervention, then the figure implies that when output has reached $12

trillion, the real interest rate will be ________ percent, and the inflation rate will be ________

percent.

A) 1.5; one

B) one; zero

C) zero; minus 2

D) 0.5; minus one

E) 2.5; three