189. A market is contestable if

a.

the number of firms is larger than oligopoly.

b.

firms spend a lot on advertising.

c.

there is free entry and exit.

d.

firms have kinked demand curves.

c

Moderate

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

190. If a market is contestable, then

a.

long-run economic profits are minimal due to inefficiency.

b.

long-run economic profits are zero.

c.

short-run and long-run economic profits are zero.

d.

positive economic profits are maximized due to the efficient production spurred by the threat of entry.

Moderate

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

191. A market which firms can enter if they choose and exit without losing money invested is

a.

pure monopoly.

b.

duopoly.

c.

contestable.

d.

a market where there are kinked demand curves.

c

Difficult

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

192. The contestable market theory best applies to

a.

pure monopoly.

b.

oligopoly.

c.

monopolistic competition.

d.

perfect competition.

Moderate

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

193. Contestable markets improve the performance of imperfect markets with

a.

government regulations.

b.

the threat of entry.

c.

advertising.

d.

tacit collusion.

Moderate

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

194. At any given airport, the airlines hold long-term leases for passenger loading gates. New gates cannot be added

without approval of the airlines. Frequent flier programs are also common in the industry. It is, therefore, more difficult

for a new airline to enter a given airport (market). Such factors:

(i)

are called barriers to entry.

(ii)

tend to decrease the contestability of the air travel market.

a.

i and ii

b.

i not ii

c.

ii not i

d.

neither i nor ii

a

Difficult

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

195. In the past, the Department of Transportation allowed airline mergers that gave the merged airlines market shares of

79 and 82 percent, respectively, in their hub cities. The concept the DOT used to allow mergers where there was obvious

concentration was most likely

a.

the good trust principle.

b.

contestability.

c.

the efficient market principle.

d.

the monopolistic competition principle.

Difficult

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition, Oligopoly, and Public Welfare

196. In a perfectly contestable market in the long run, each firm

a.

produces at the minimum point on its long-run average total cost curve.

b.

earns a profit below its opportunity cost of capital.

c.

avoids making capital expenditures.

d.

All of the above are correct.

a

Moderate

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

197. An empirical study determines that price exceeds marginal cost at the levels of output of firms in long-run

equilibrium in the widget industry. The widget industry may therefore

a.

be monopolistically competitive.

b.

have firms whose goal is sales maximization.

c.

have firms that act as price leaders.

d.

All of the above are correct.

Difficult

DISC: Monopolistic competition

United States – BPROG: Analytic

Monopolistic competition

A Glance Backward: Comparing the Four Market Forms

198. A perfectly competitive firm and a monopolistically competitive firm are similar in each of the following respects

except

a.

each has many buyers and sellers.

b.

firms sell homogeneous products in both markets.

c.

in having perfect information.

d.

for freedom of exit and entry.

DISC: Monopolistic competition

United States – BPROG: Analytic

Monopolistic competition

A Glance Backward: Comparing the Four Market Forms

199. Which of the following conditions distinguishes the monopolistic competitor from the monopolist?

a.

profit-maximizing rule

b.

downward slope of demand curve

c.

entry of rivals

d.

short-run economic profits

DISC: Monopolistic competition

United States – BPROG: Analytic

Monopolistic competition

A Glance Backward: Comparing the Four Market Forms

200. Deviations from the perfectly competitive market can lead to

a.

inefficiently high production costs.

b.

higher prices and smaller outputs.

c.

less efficient resource allocation.

d.

All of the above are correct.

DISC: Perfect competition

United States – BPROG: Analytic

Perfect competition

A Glance Backward: Comparing the Four Market Forms

201. All four market forms discussed in the text maximize profit where

a.

P = MC.

b.

AR = AC.

c.

MR = MC.

d.

MC = AR.

DISC: Perfect competition

United States – BPROG: Analytic

Perfect competition

A Glance Backward: Comparing the Four Market Forms

202. Markets in which the behavior of the firms theoretically leads to an efficient allocation of resources that maximizes

the benefits to consumers given the resources available to consumers are

a.

monopolistic competition and oligopoly.

b.

monopoly and oligopoly.

c.

monopolistic competition and monopoly.

d.

perfect competition and perfectly contestable.

DISC: Perfect competition

United States – BPROG: Analytic

Perfect competition

A Glance Backward: Comparing the Four Market Forms

203. The behavior of the perfectly competitive firm:

a.

theoretically leads to an inefficient allocation of resources.

b.

maximizes the benefits to consumers, given the resources available to the economy.

c.

reduces output in order to raise prices in the short-term.

d.

results in excess capacity and inefficiency.

DISC: Monopolistic competition

United States – BPROG: Analytic

A Glance Backward: Comparing the Four Market Forms

204. The behavior of the monopolistic firm:

a.

maximizes the benefits to consumers, given the resources available to the economy.

b.

reduces output in order to raise prices in the short-term.

c.

results in excess capacity and inefficiency.

d.

both b and c

DISC: Monopolistic competition

United States – BPROG: Analytic

Monopolistic competition

A Glance Backward: Comparing the Four Market Forms

Essay

205. Define the following terms and explain their importance to the study of economics.

a.

monopolistic competition

b.

oligopoly

c.

cartel

d.

oligopolistic interdependence

Easy

DISC: Oligopoly

United States – BPROG: Analytic

Oligopoly

Monopolistic Competition

206. Briefly and concisely define the following terms and explain their importance in the study of economics.

a.

excess capacity theorem

b.

price leadership

c.

kinked demand curve

d.

perfectly contestable market

than marginal cost (MU > MC).

207. In what way is monopolistic competition more like competition, and in what way is it more like monopoly?

208. Monopolistic competition tends to lead firms to have wasted capacity. Why?

209. Can positive economic profits persist under monopolistic competition in the long run. Why?

210. What are the advantages and disadvantages of resource allocation under monopolistic competition compared to

perfect competition?

211. Explain how short-run and long-run equilibrium in monopolistic competition differ. Use graphs to illustrate your

answer. Be sure that your graphs are completely and correctly labeled.

212. Here is an excerpt form an editorial praising capitalism in The Economist: “It is competition that delivers choice,

holds prices down, encourages invention and service, and (through all these things) delivers economic growth.” To what

type of competition does the writer refer? Is it the sort of competition that economists study? Explain.

Moderate

213. Baumol and Blinder argue that oligopolies are interdependent firms. What do they mean by this? Give three

examples of the types of interdependence which might occur.

1

Difficult

Oligopoly

Oligopoly

214. What quantity of output and price do they try to set, when a group of oligopoly firms form a cartel? Will there be any

changes in the price and quantity supplied if the cartel gets broken down?

falls.

1

Difficult

Oligopoly

Oligopoly

215. Demand for a firm has been reliably measured as P = 100 − 5Q where Q is output and P is price in dollars. Total cost

is in the table below. Complete the table and indicate the level of output and price which a profit-maximizing firm would

select and indicate the same for a sales-maximizing firm.

Quantity

Price

Revenue

Cost

Profit

1

_____

_____

200

_____

2

_____

_____

210

_____

3

_____

_____

220

_____

4

_____

_____

231

_____

5

_____

_____

243

_____

6

_____

_____

256

_____

7

_____

_____

270

_____

8

_____

_____

285

_____

9

_____

_____

301

_____

10

_____

_____

320

_____

11

_____

_____

345

_____

12

_____

_____

375

_____

Quantity

Price

Revenue

Cost

Profit

1

95

200

2

90

180

210

3

85

255

220

4

80

320

231

5

75

375

243

132

6

70

420

256

164

7

65

455

270

185

8

60

480

285

195

9

55

495

301

194

10

50

500

320

180

11

45

495

345

150

12

40

480

375

105

1

Difficult

Oligopoly

Oligopoly

216. What are the assumptions of the kinked demand curve model? What is its main conclusion about oligopoly behavior?

1

Moderate

Oligopoly

Oligopoly

217. Is it likely that oligopolistic firms will be in both a kinked demand curve situation and also engage in price

leadership? Why or why not?

DISC: Oligopoly

United States – BPROG: Analytic

218. Economists tend to be concerned about entry barriers. Why are entry barriers so important?

about profits than about efficiency.

DISC: Oligopoly

United States – BPROG: Analytic

219. Define the following terms and explain their importance to the study of economics.

a.

maximin criterion

b.

Nash equilibrium

c.

Dominant Strategy

d.

Zero-sum game

e.

Credible threat

what choice of strategy is made by her competitors.

this type of game.

DISC: Oligopoly

United States – BPROG: Analytic

220. What is a repeated game? Hoe does this helps the players in a game?

DISC: Oligopoly

United States – BPROG: Analytic

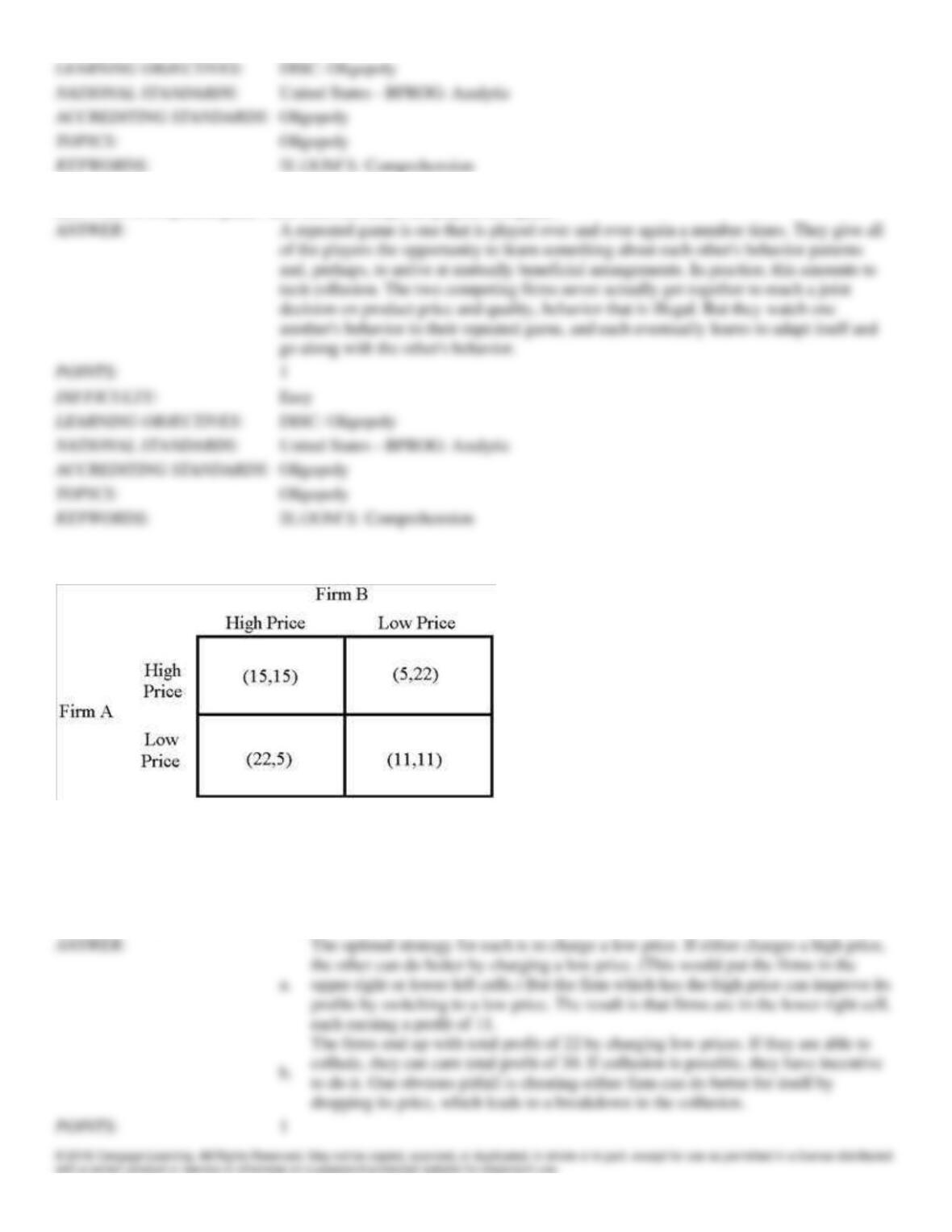

Figure 12-4

221. The above matrix (Figure 12–4) displays the possible profit results of two firms, A and B, from following two

different possible strategies: charging a high price and charging a low price. In each cell, the first number is the profit of

firm A, and the second number is the profit of firm B.

a.

Assume that collusion is not possible. Determine the optimal strategy for each firm. Explain

why it is the best strategy to follow.

b.

Based on your answer to a., explain why firms collude. What are the pitfalls of collusion?

222. Explain the prisoner’s dilemma case in game theory and its relevance to the maximin criterion.

223. Why is oligopoly more difficult to model than competition or monopoly?

224. When an airline reduces its fares, other airlines typically match the action. But when an airline increases its fare,

other airlines do not follow suit. Which oligopoly model cartel, price leadership, or kinked demand best fits the airline

industry as described? Justify your choice and explain why the other models are less appropriate.

225. Explain how a large number of firms in the industry and product heterogeneity affect the likelihood of cartel success.

226. How will price, output, and profit compare if firms maximize sales rather than profit?

227. Which oligopoly model leads to price rigidity? Graphically show why.

228. The airline dominating Charlotte, North Carolina, once contended that it could not overcharge for fear of potential

competition, if not at Charlotte, then at Raleigh, a two-hour drive away. Do you find this argument compelling, given the

theory of contestable markets?

229. Firms in a perfectly contestable market will be forced to operate as efficiently as possible and to charge prices as low

as long-run financial survival permits. Why?

230. What are the four types of industry structures? Compare and contrast them with the number of firms in the industry,

whether firms produce homogeneous or heterogeneous products, whether there are economic profits in long-run

equilibrium, and how frequently the model appears in the real world.