Reference: Ref 12-12

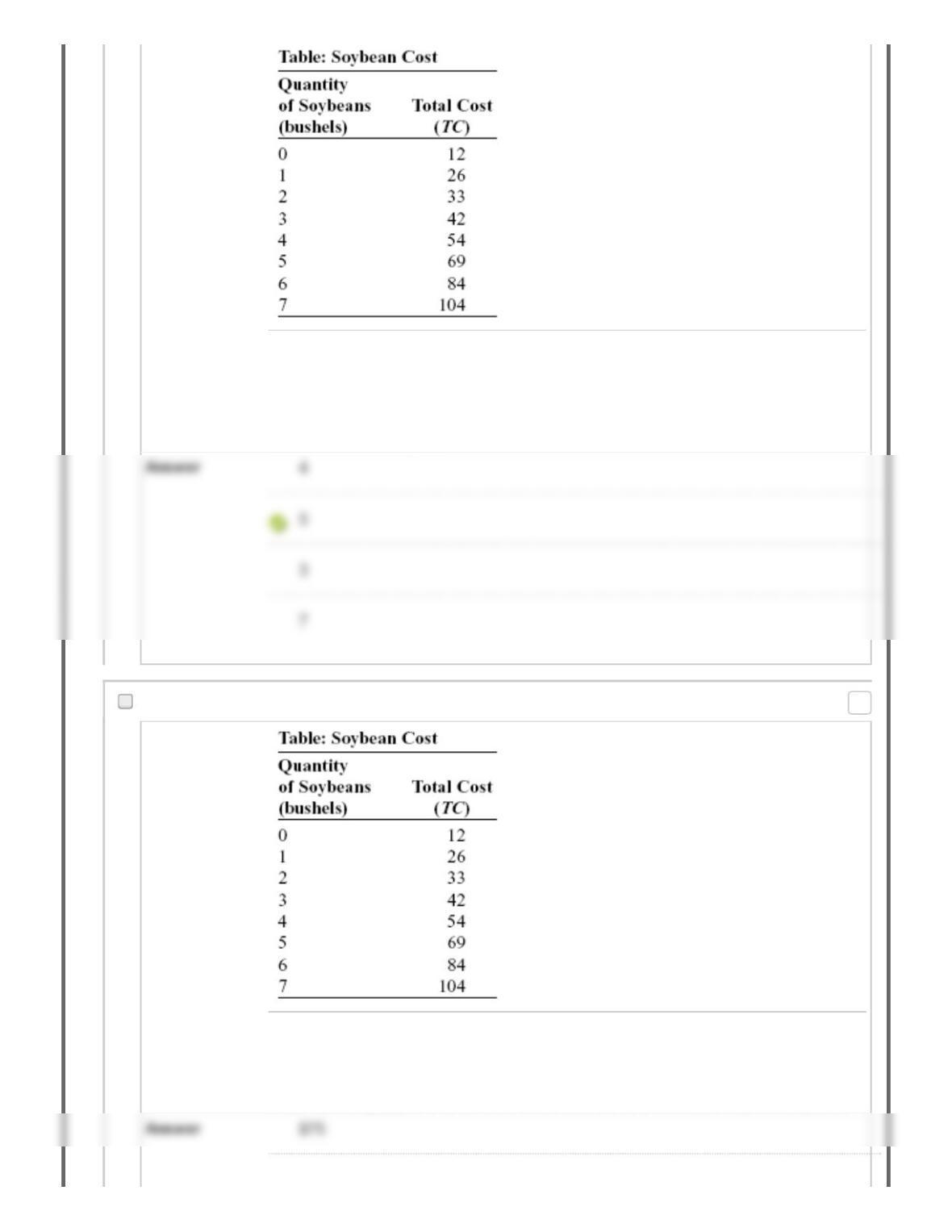

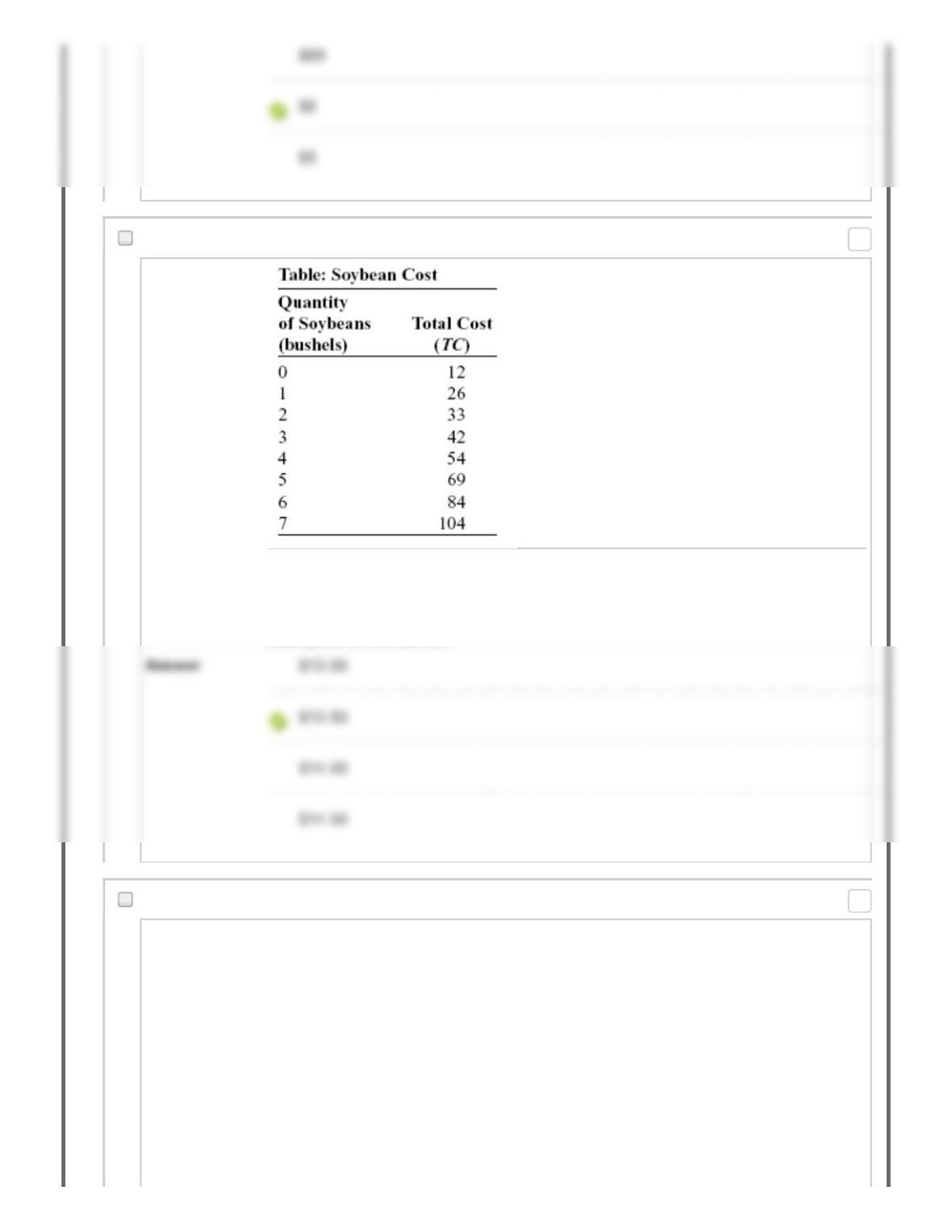

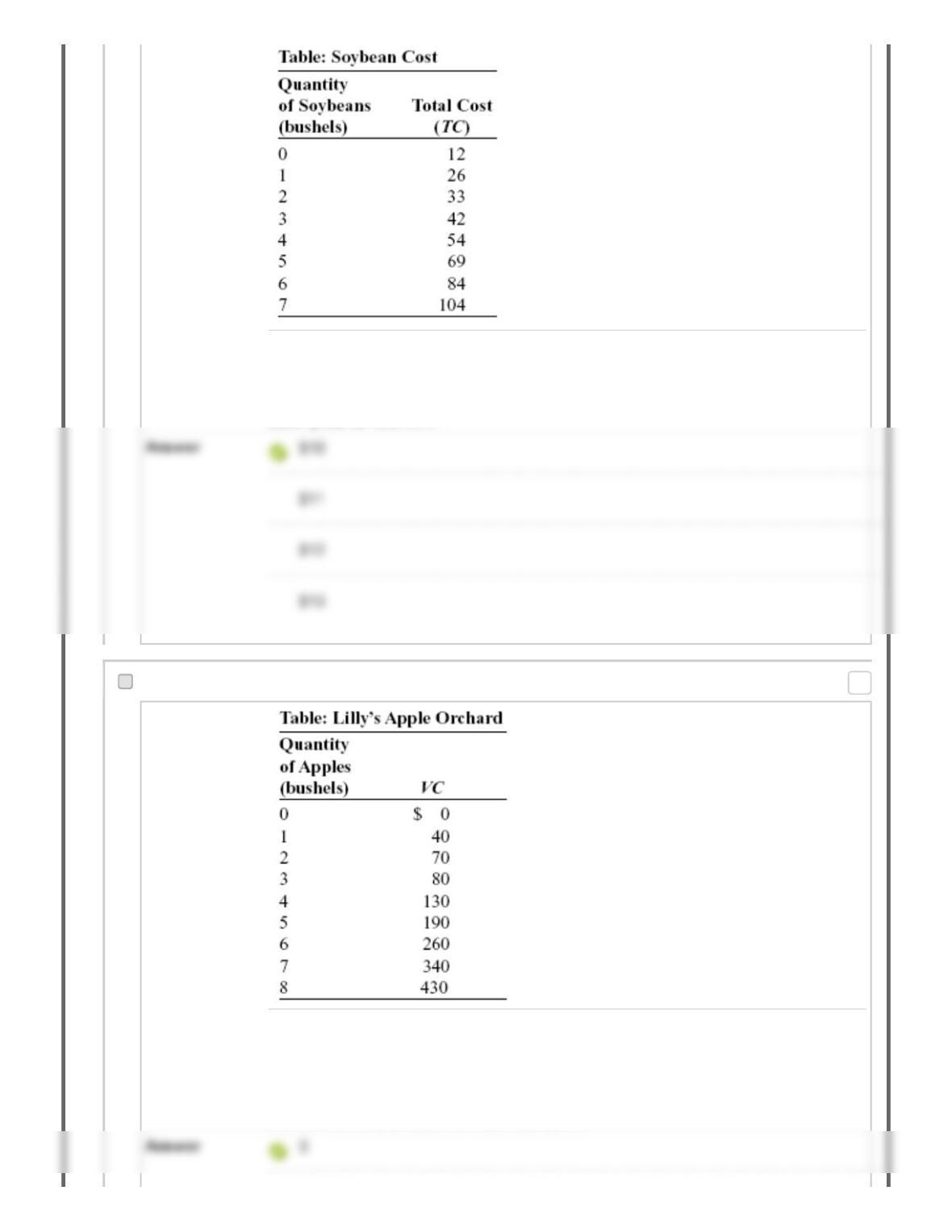

(Table: Soybean Cost) Look at the table Soybean Cost. The costs of production of

a perfectly competitive soybean farmer are given in the table. If the market price of

a bushel of soybeans is $15, how many bushels will the farmer produce to

maximize short-run profit?

186. Multiple Choice: Reference: Ref 12-12 (Table: Soybean...

Question

Reference: Ref 12-12

(Table: Soybean Cost) Look at the table Soybean Cost. The costs of production of

a perfectly competitive soybean farmer are given in the table. If the market price of

a bushel of soybeans is $15, what will be the farmer‘s short-run maximum profit?

Points: 0

187. Multiple Choice: Reference: Ref 12-12 (Table: Soybean...

Question

Reference: Ref 12-12

(Table: Soybean Cost) Look at the table Soybean Cost. The costs of production of

a perfectly competitive soybean farmer are given in the table. What is the break-

even price for this farmer?

188. Multiple Choice: Reference: Ref 12-12 (Table: Soybean...

Question

Points: 0

Points: 0

Reference: Ref 12-12

(Table: Soybean Cost) Look at the table Soybean Cost. The costs of production of

a perfectly competitive soybean farmer are given in the table. What is the shut–

down price for this firm?

189. Multiple Choice: Reference: Ref 12-13 (Table: Lilly‘s...

Question

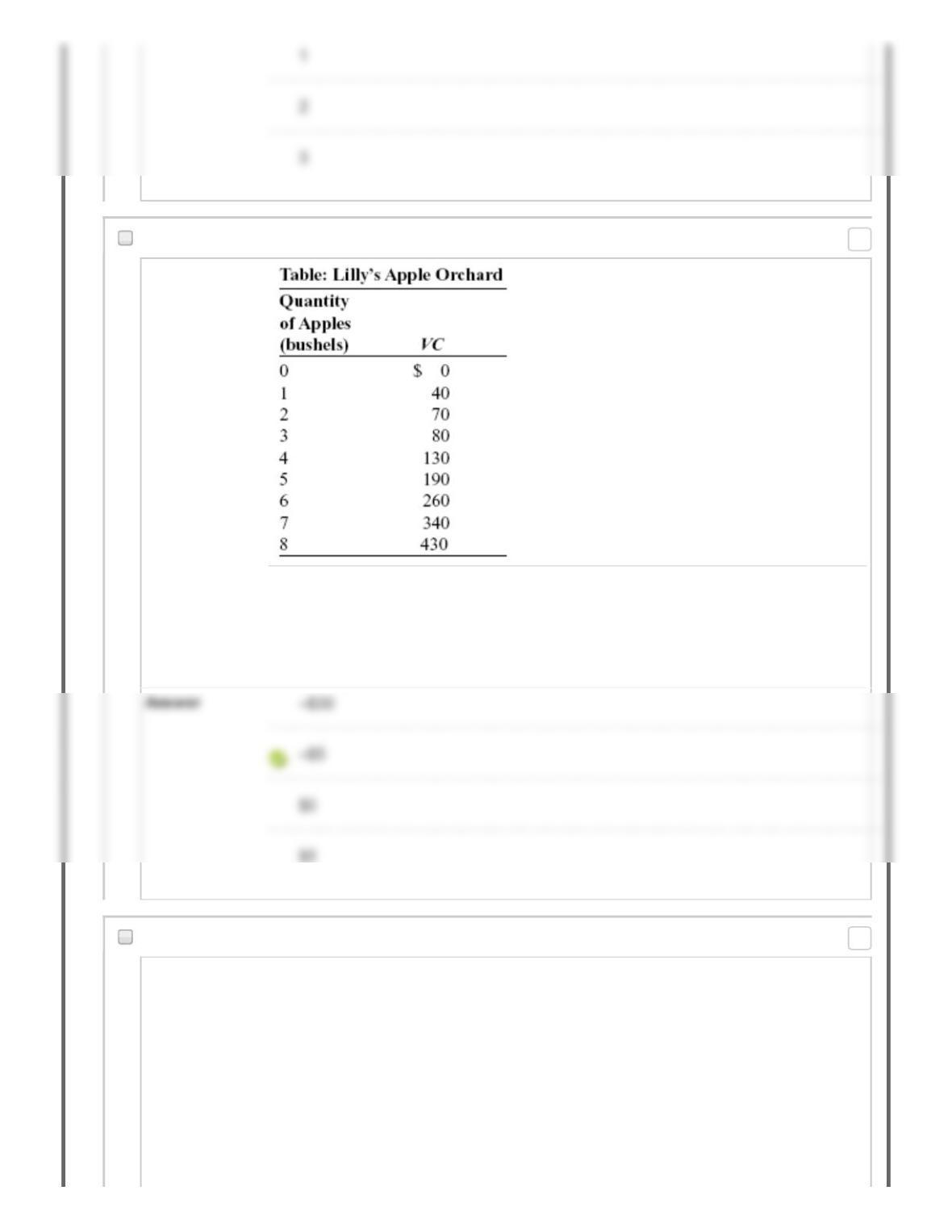

Reference: Ref 12-13

(Table: Lilly‘s Apple Orchard) Look at the table Lilly‘s Apple Orchard. Lilly is the

price-taking owner of an apple orchard; its variable costs are given in the table. Her

orchard has fixed costs of $30. If the price of a bushel of apples is $25, how many

bushels will Lilly produce to maximize profit?

Points: 0

190. Multiple Choice: Reference: Ref 12-13 (Table: Lilly‘s...

Question

Reference: Ref 12-13

(Table: Lilly‘s Apple Orchard) Look at the table Lilly‘s Apple Orchard. Lilly is the

price-taking owner of an apple orchard; its variable costs are given in the table. Her

orchard has fixed costs of $30. If the price of a bushel of apples is $35, her

economic profit will be equal to:

191. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

Points: 0

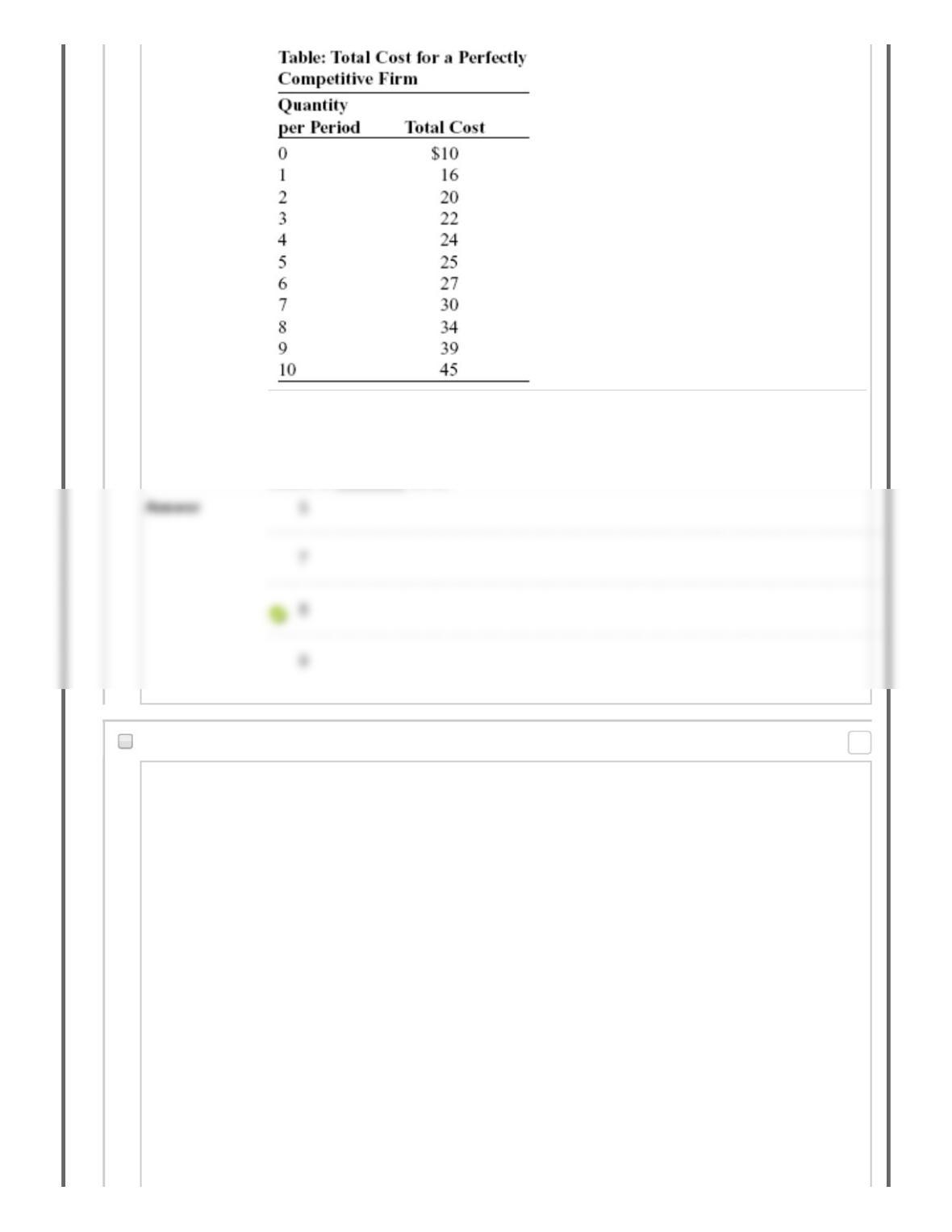

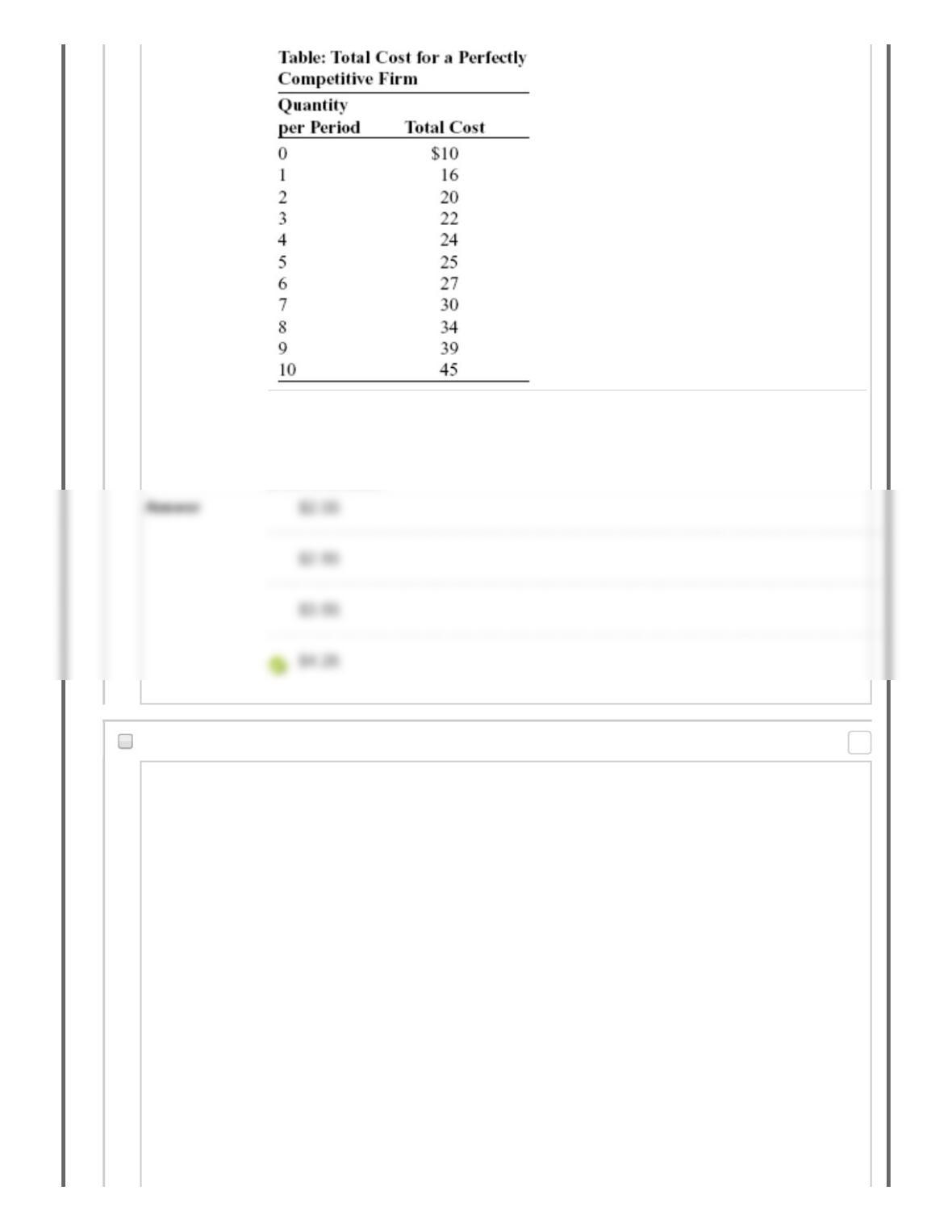

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. If the market price is $4.50, the profit-maximizing

output is ________ units.

192. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

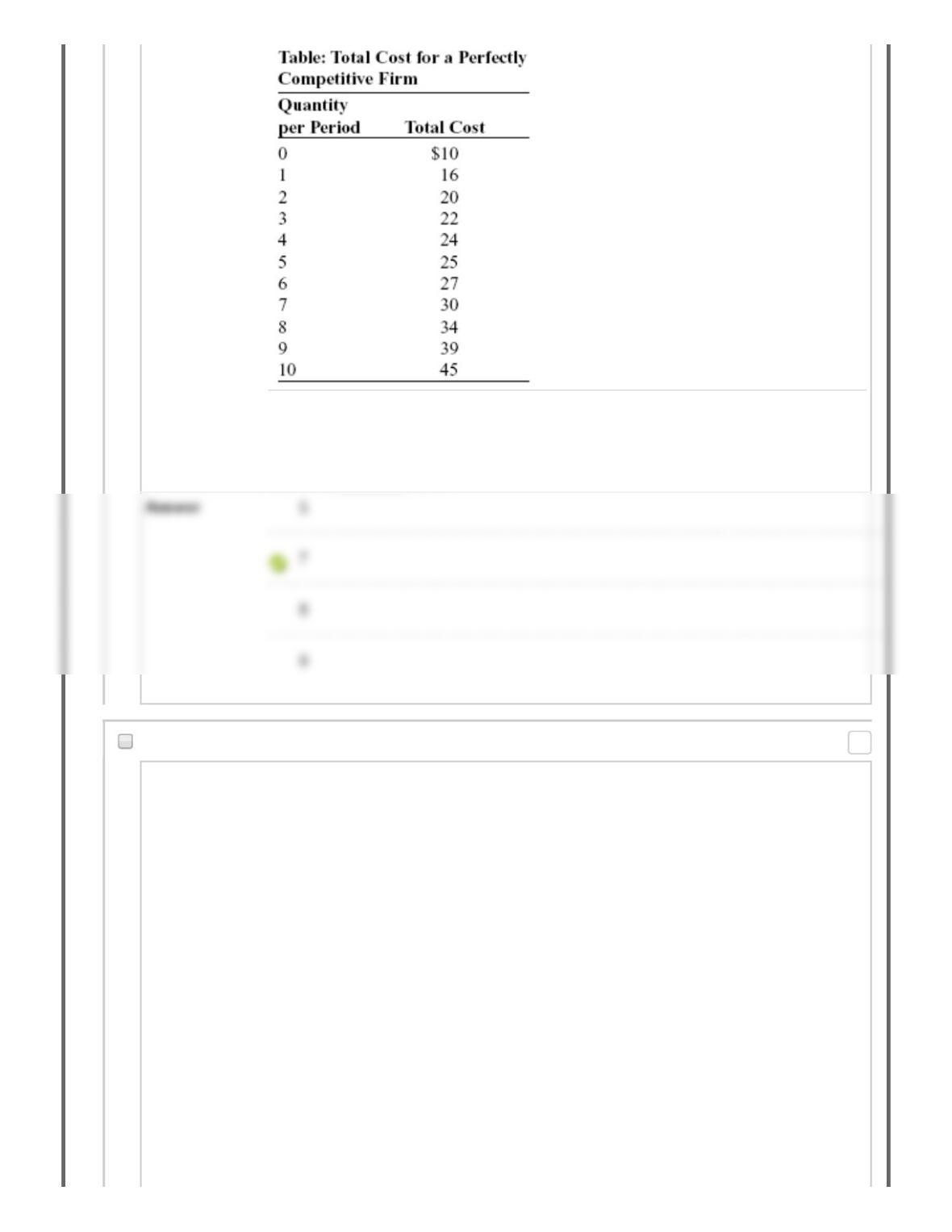

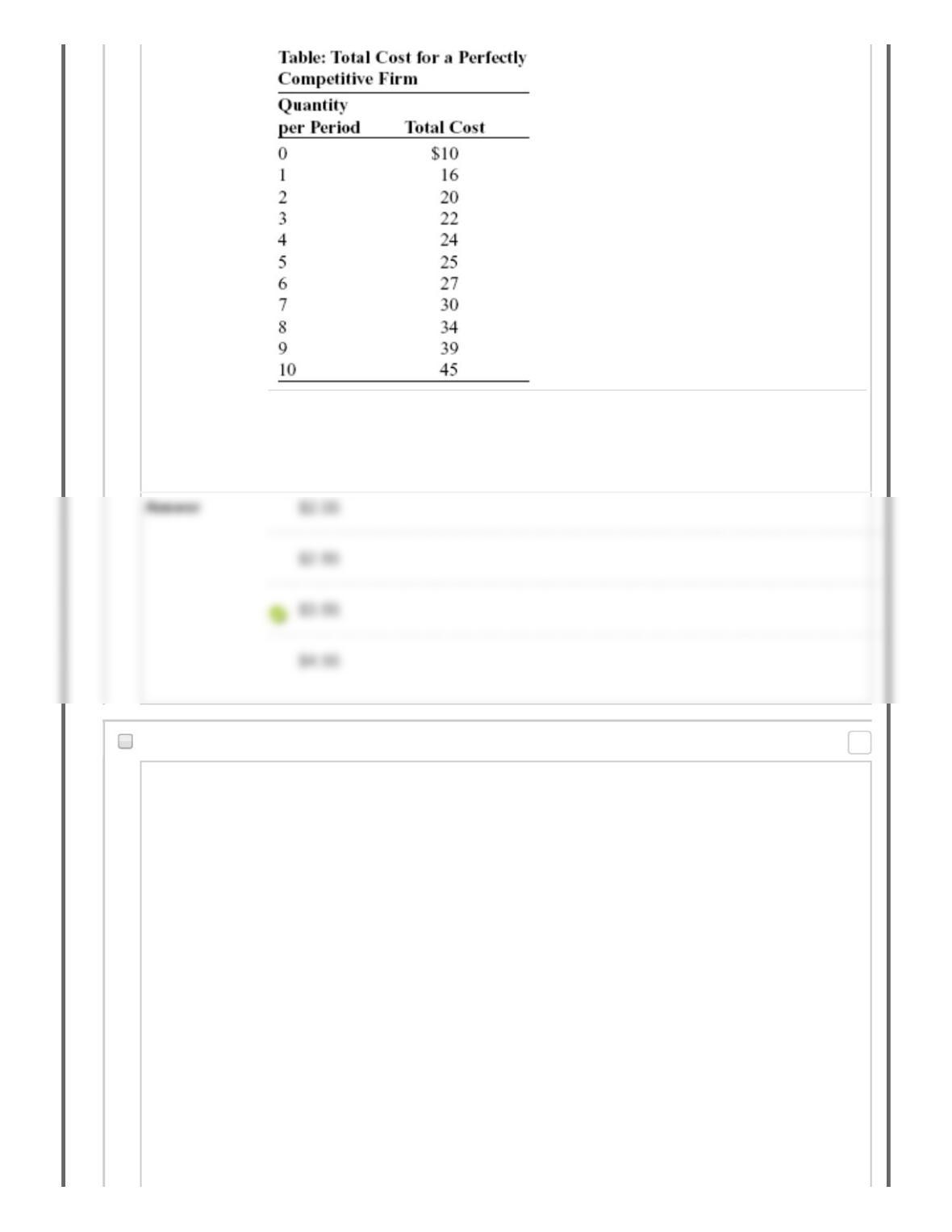

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. If the market price is $3.50, the profit-maximizing

output is ________ units.

193. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

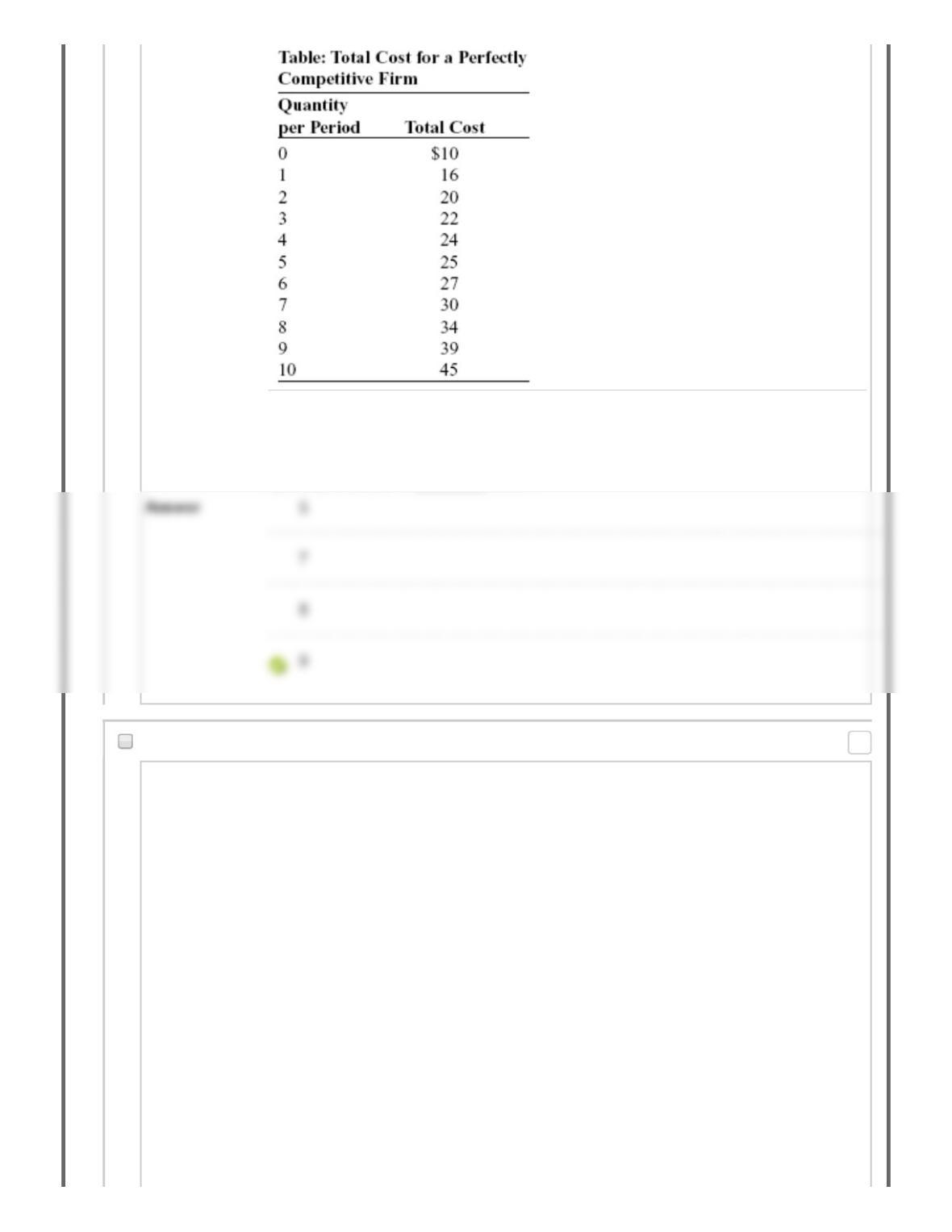

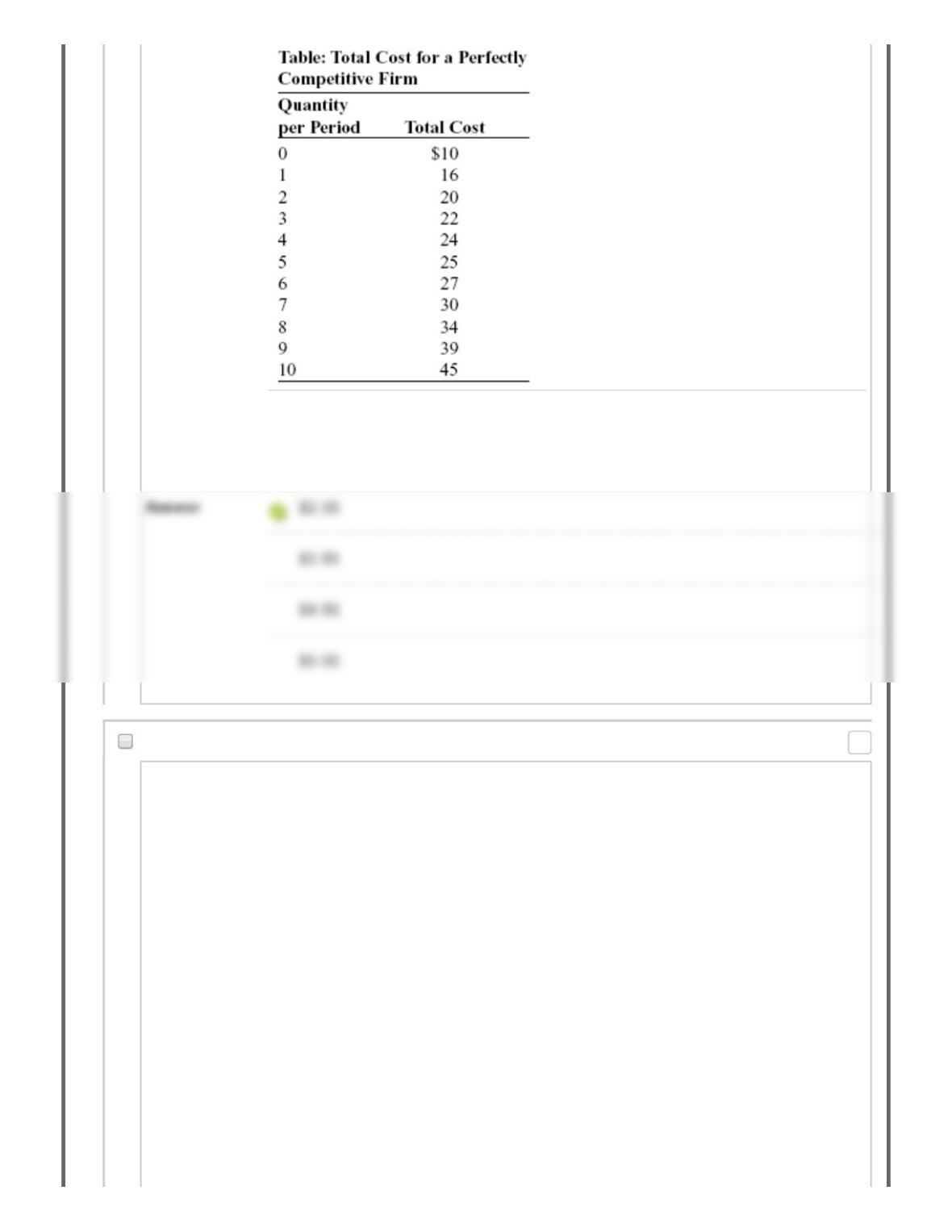

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. If the market price is $5.50, the profit-maximizing

quantity of output is ________ units.

194. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

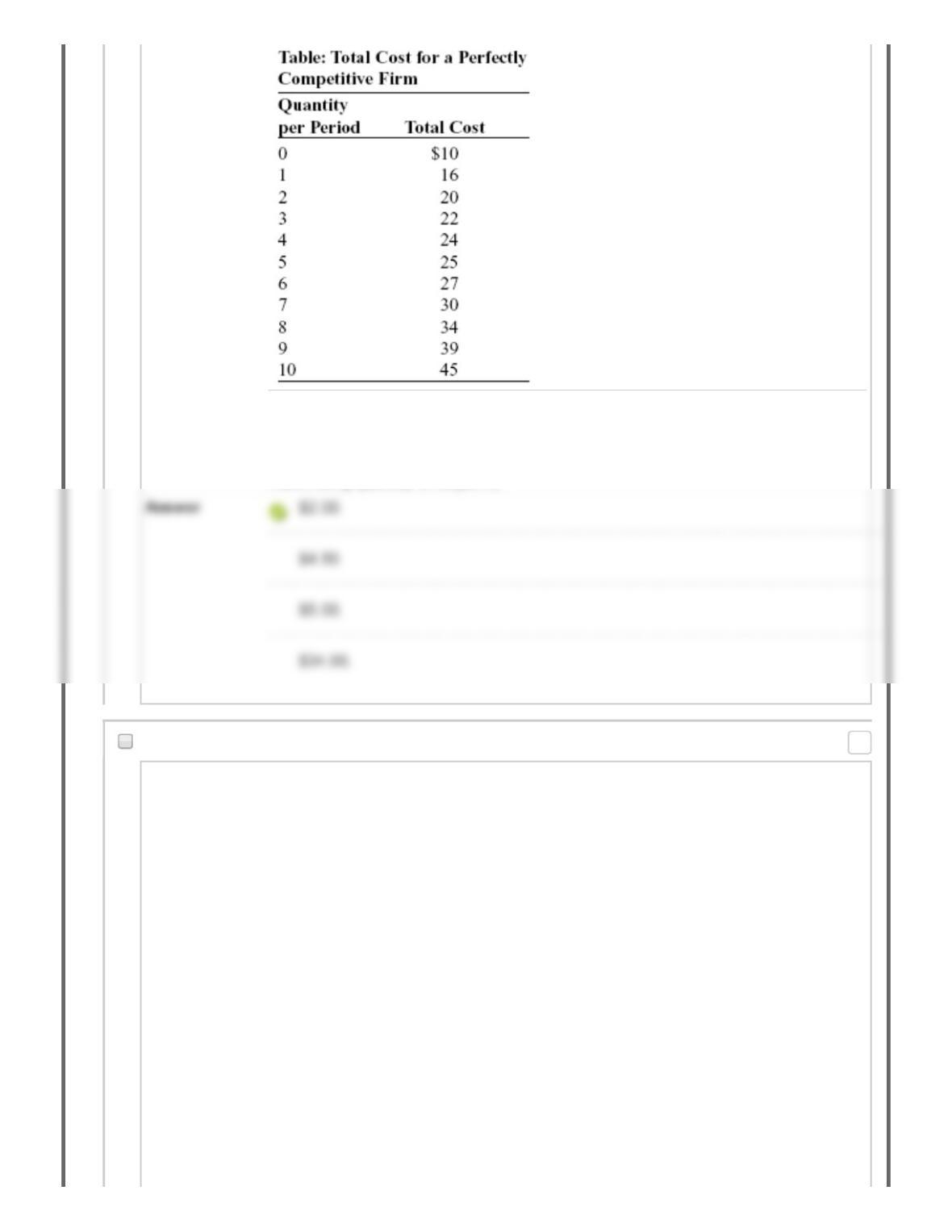

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. If the market price is $4.50, profit at the profit–

maximizing quantity of output is:

195. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. The firm will produce at a profit in the short run if the

price is at least:

196. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. In the short run, the firm will produce, but at a loss, if

the price is:

197. Multiple Choice: Reference: Ref 12-14 (Table: Total C…

Question

Points: 0

Reference: Ref 12-14

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for

a Perfectly Competitive Firm. The firm will stop production and shut down if the

price is:

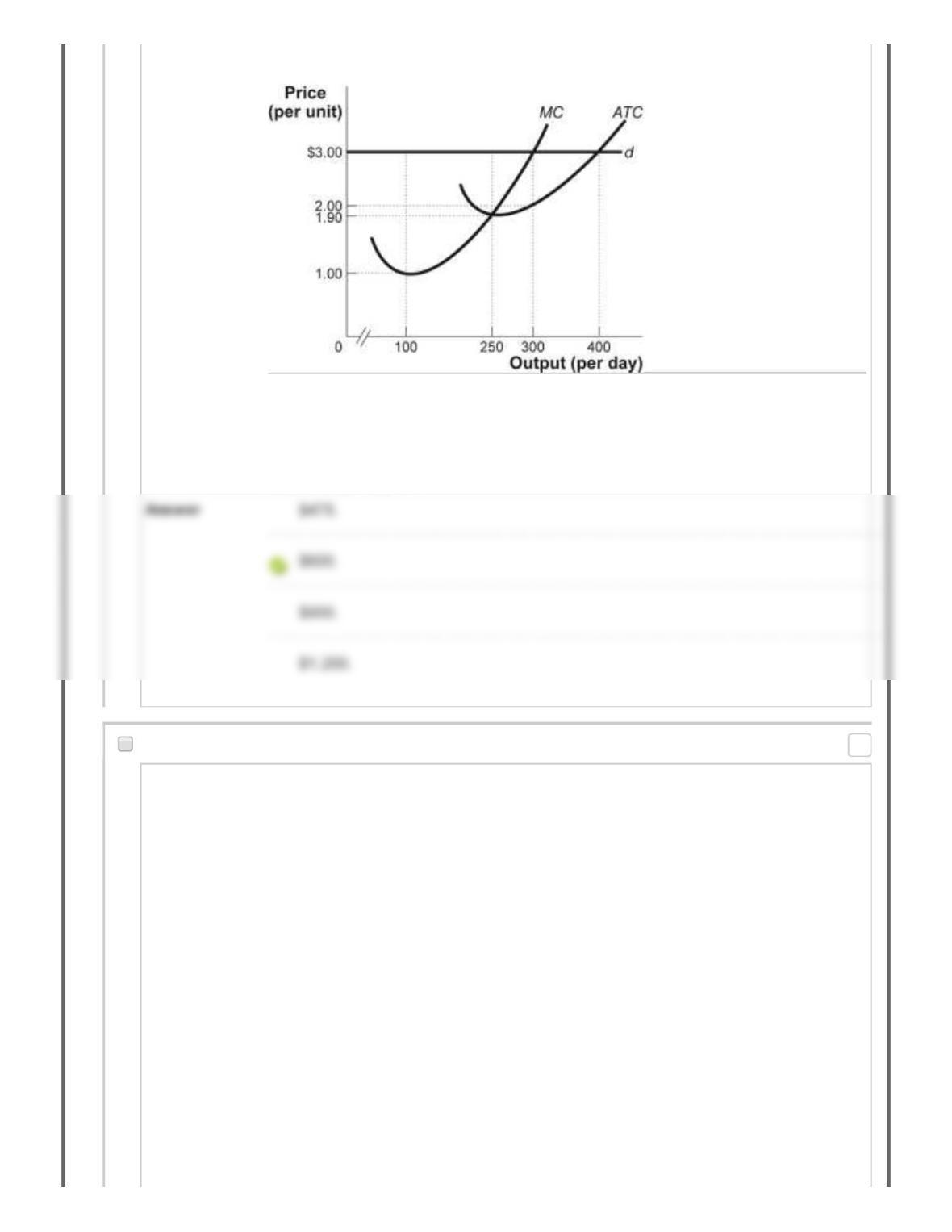

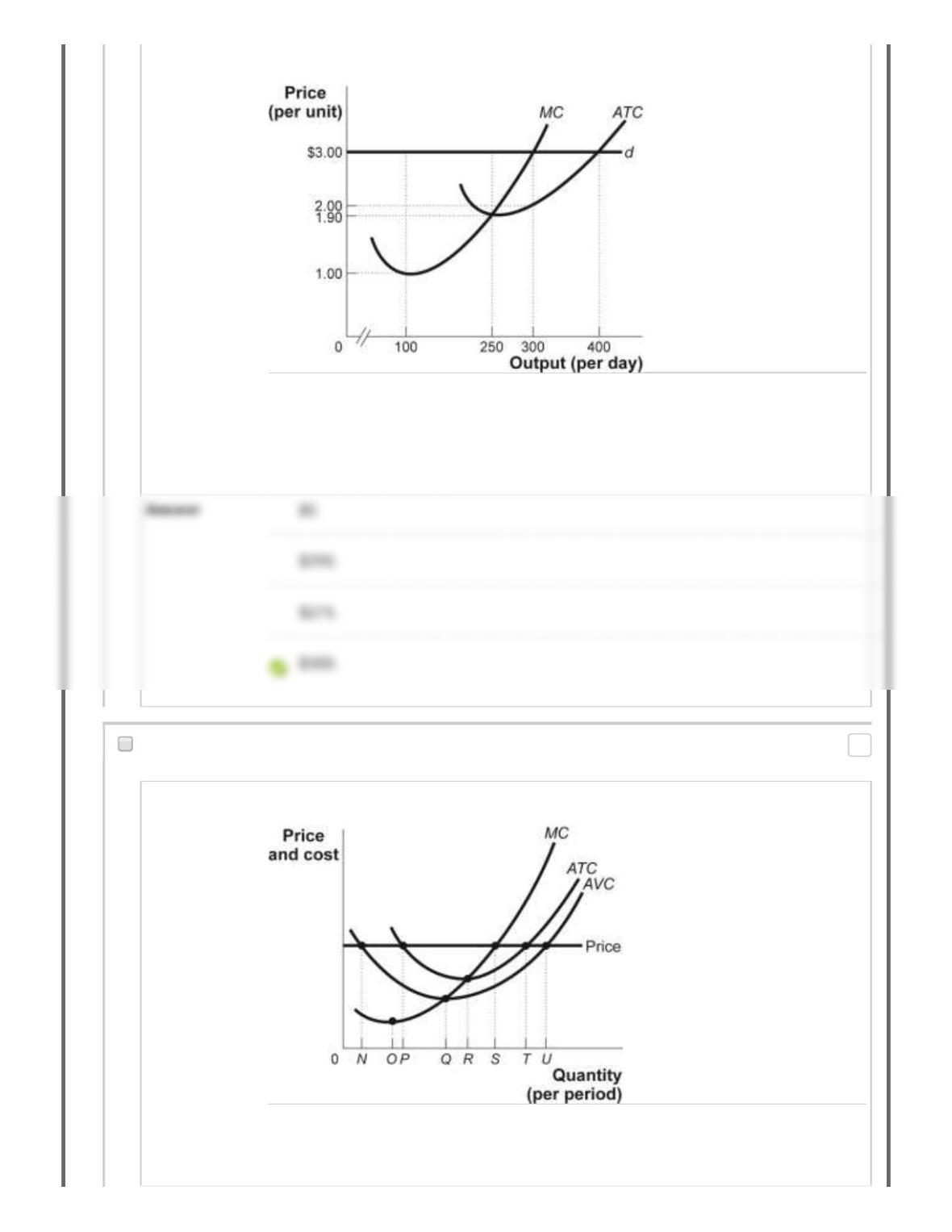

198. Multiple Choice: Figure: The Perfectly Competitive Fir...

Question

Points: 0

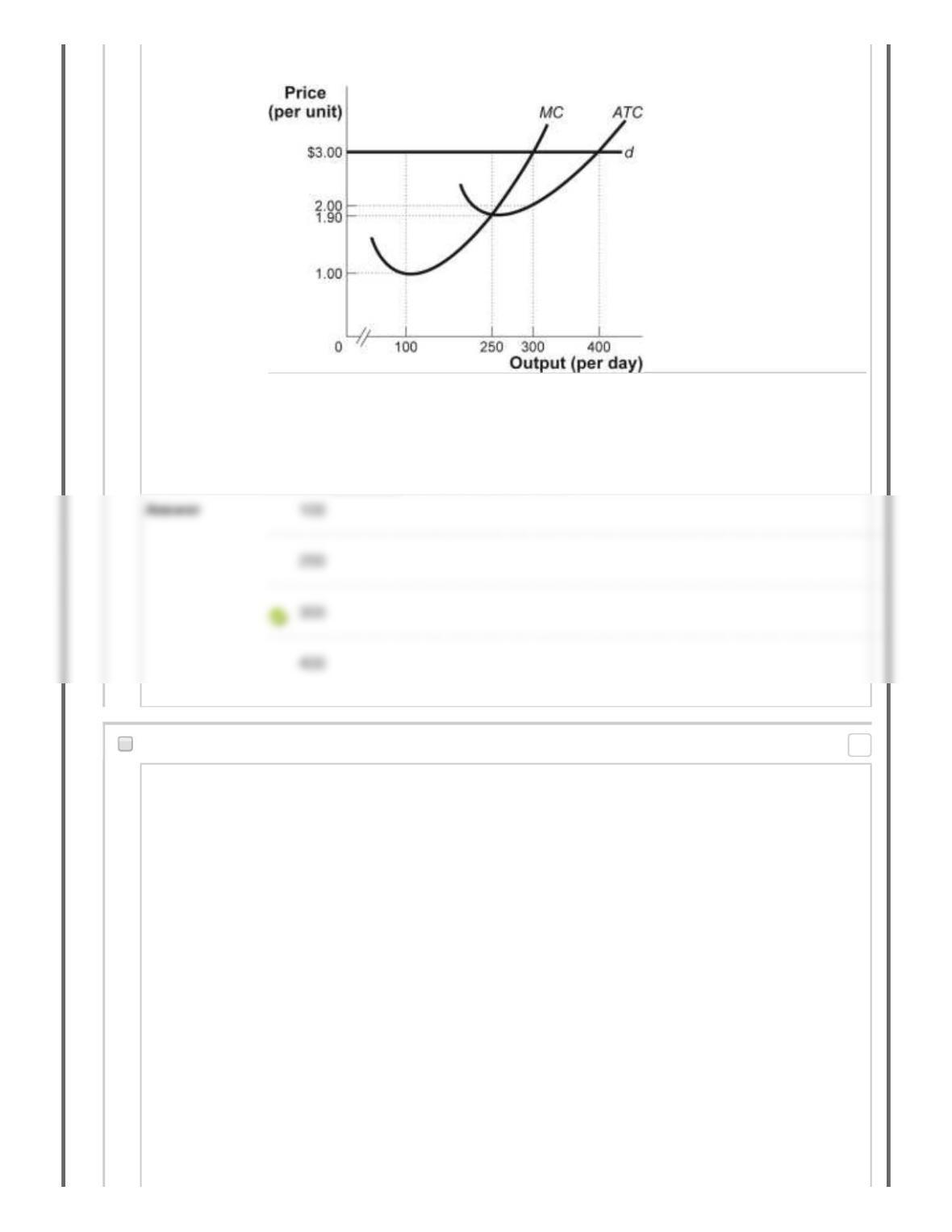

Figure: The Perfectly Competitive Firm

Reference: Ref 12-15

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d, has

the cost curves shown, and maximizes profit. If the market price is $3, the firm will

produce ________ units of output per day.

199. Multiple Choice: Figure: The Perfectly Competitive Fir...

Question

Points: 0

Figure: The Perfectly Competitive Firm

Reference: Ref 12-15

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d, has

the cost curves shown, and maximizes profit. Given the market price, the firm’s

total revenue per day is:

200. Multiple Choice: Figure: The Perfectly Competitive Fir...

Question

Points: 0

Figure: The Perfectly Competitive Firm

Reference: Ref 12-15

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d, has

the cost curves shown, and maximizes profit. Given the market price, the firm’s

total cost per day is:

201. Multiple Choice: Figure: The Perfectly Competitive Fir...

Question

Points: 0

Figure: The Perfectly Competitive Firm

Reference: Ref 12-15

(Figure: Perfectly Competitive Firm) Look at the figure The Perfectly Competitive

Firm. The figure shows a perfectly competitive firm that faces demand curve d, has

the cost curves shown, and maximizes profit. If the firm faces a market price of $3,

its total profit per day is:

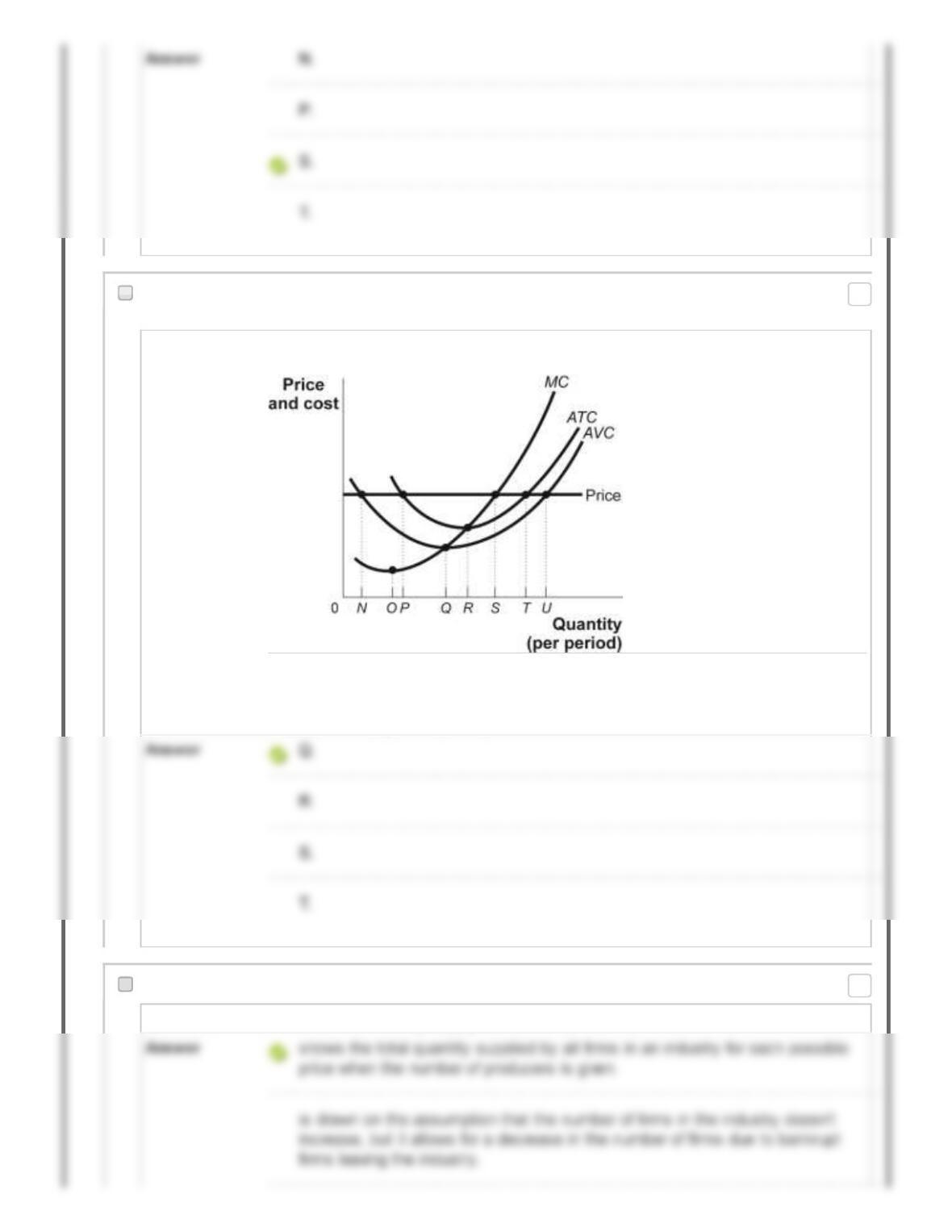

202. Multiple Choice: Figure: Short-Run Costs Reference: Re…

Question Figure: Short-Run Costs

Reference: Ref 12-16

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. At the given price,

the most profitable level of output occurs at quantity:

Points: 0

203. Multiple Choice: Figure: Short-Run Costs Reference: Re…

Question Figure: Short-Run Costs

Reference: Ref 12-16

(Figure: Short-Run Costs) Look at the figure Short-Run Costs. This firm’s short-run

supply curve begins at quantity:

204. Multiple Choice: The short-run industry supply curve:

Question The short-run industry supply curve:

Points: 0

Points: 0

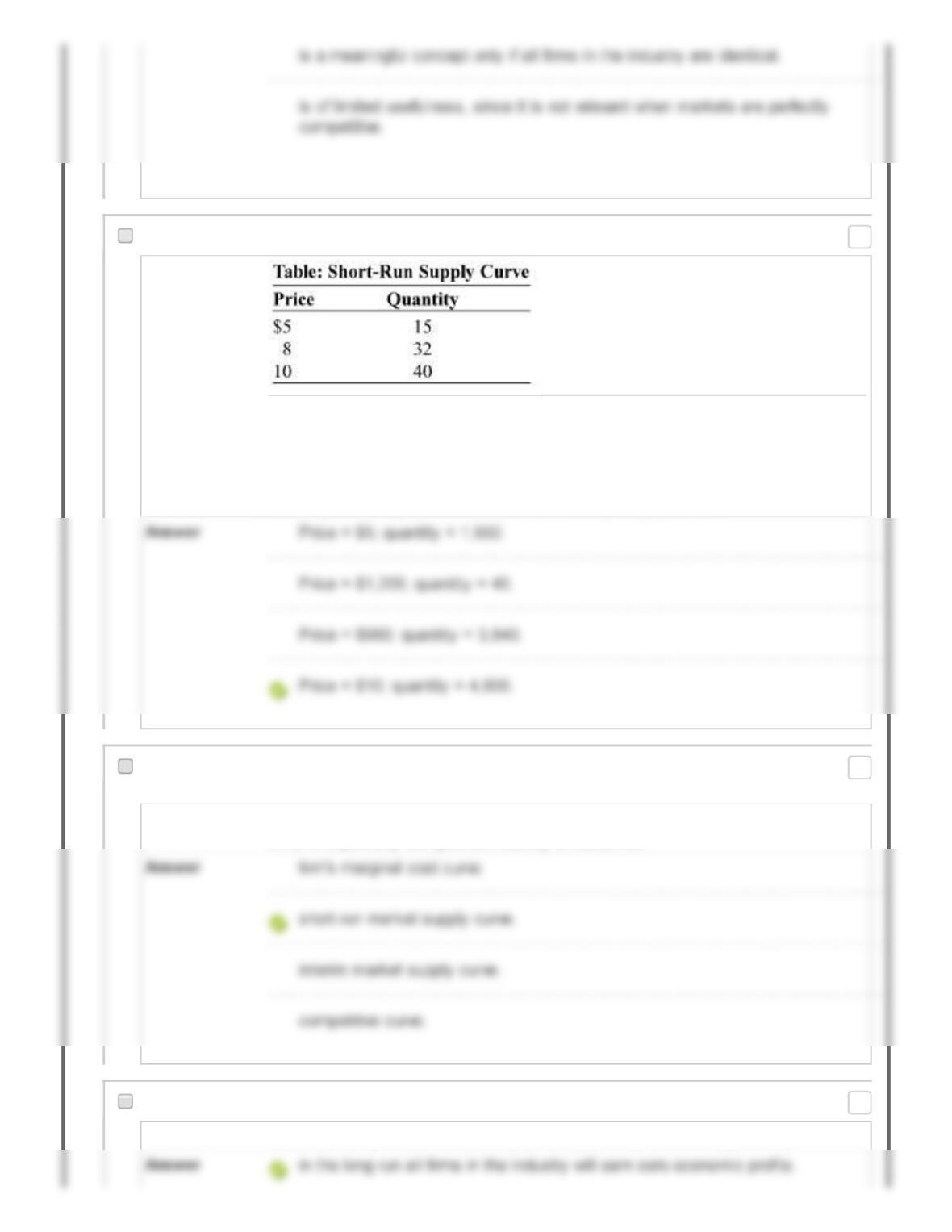

205. Multiple Choice: Reference: Ref 12-17 (Table: Short-R…

Question

Reference: Ref 12-17

(Table: Short-Run Supply Curve) Look at the table Short–Run Supply Curve. The

table lists three supply points for an individual, perfectly competitive firm operating

in the short run. If the industry is composed of 120 identical firms, which of the

following will be a point on the short-run industry supply curve?

206. Multiple Choice: The supply curve found by summing up ...

Question The supply curve found by summing up the short-run supply curves of all of the

firms in a perfectly competitive industry is called the:

207. Multiple Choice: In perfect competition, the assumptio...

Question In perfect competition, the assumption of easy entry and exit implies that:

Points: 0

Points: 0

Points: 0

208. Multiple Choice: If firms are making positive economic...

Question If firms are making positive economic profits in the short run, then in the long run:

209. Multiple Choice: The market for beef is in long-run eq...

Question The market for beef is in long–run equilibrium at a price of $3.25 per pound. The

announcement that mad cow disease has been discovered in the United States

reduces the demand for beef sharply, and the price falls to $2.00 per pound. If the

long-run supply curve is horizontal, then when the long–run equilibrium is

reestablished, the price will be:

210. Multiple Choice: If economic profits exist in perfect ...

Question If economic profits exist in perfect competition, then firms will enter in the long run

because of easy entry, the ________ curve will shift to the right, and ________ in

the market will ________.

Points: 0

Points: 0

Points: 0

211. Multiple Choice: Economic profits in a perfectly compe…

Question Economic profits in a perfectly competitive industry encourage firms to ________

the industry, and losses encourage firms to ________the industry.

212. Multiple Choice: Suppose that some firms in a perfectl...

Question Suppose that some firms in a perfectly competitive industry earn negative

economic profits. In the long run, the:

213. Multiple Choice: If firms are experiencing economic lo...

Question If firms are experiencing economic losses in the short run, firms will leave the

industry, industry output will ________, and economic losses will ________ in the

long run.

214. Multiple Choice: Suppose that the market for candy can...

Question

Points: 0

Points: 0

Points: 0

Points: 0

Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long–run equilibrium, and that the price of each

candy cane is $0.10. Now suppose that the price of sugar rises, increasing the

marginal and average total costs of producing candy canes by $0.05. Based on the

information given, we can conclude that in the short run a typical producer of candy

canes will be making:

215. Multiple Choice: Suppose that the market for candy can...

Question Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long–run equilibrium, and that the price of each

candy cane is $0.10. Now suppose that the price of sugar rises, increasing the

marginal and average total cost of producing candy canes by $0.05; there are no

other changes in production costs. Based on the information given, we can

conclude that in the long run we will observe:

216. Multiple Choice: Suppose that the market for candy can...

Question Suppose that the market for candy canes operates under conditions of perfect

competition, that it is initially in long–run equilibrium, and that the price of each

candy cane is $0.10. Now suppose that the price of sugar rises, increasing the

marginal and average total cost of producing candy canes by $0.05; there are no

other changes in production costs. Based on the information given, we can

conclude that once all of the adjustments to long–run equilibrium have been made,

the price of candy canes will equal:

Points: 0

Points: 0