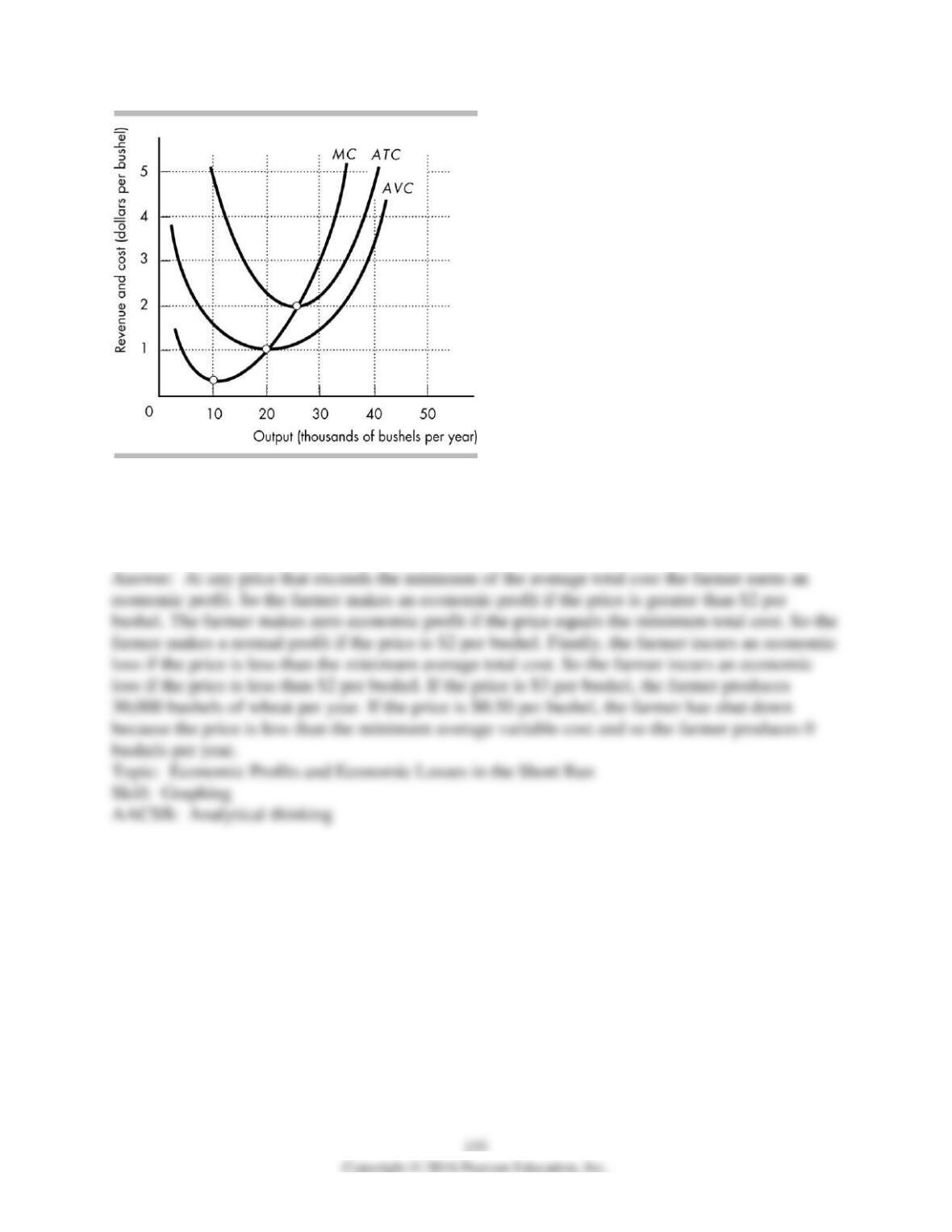

14) The above diagram shows the cost curves for a perfectly competitive wheat farmer. At what

price(s) does the wheat farmer make an economic profit? Make zero economic profit? Incur an

economic loss? How many bushels of wheat does the farmer produce if the price is $3 per

bushel? If the price is $0.50 per bushel?

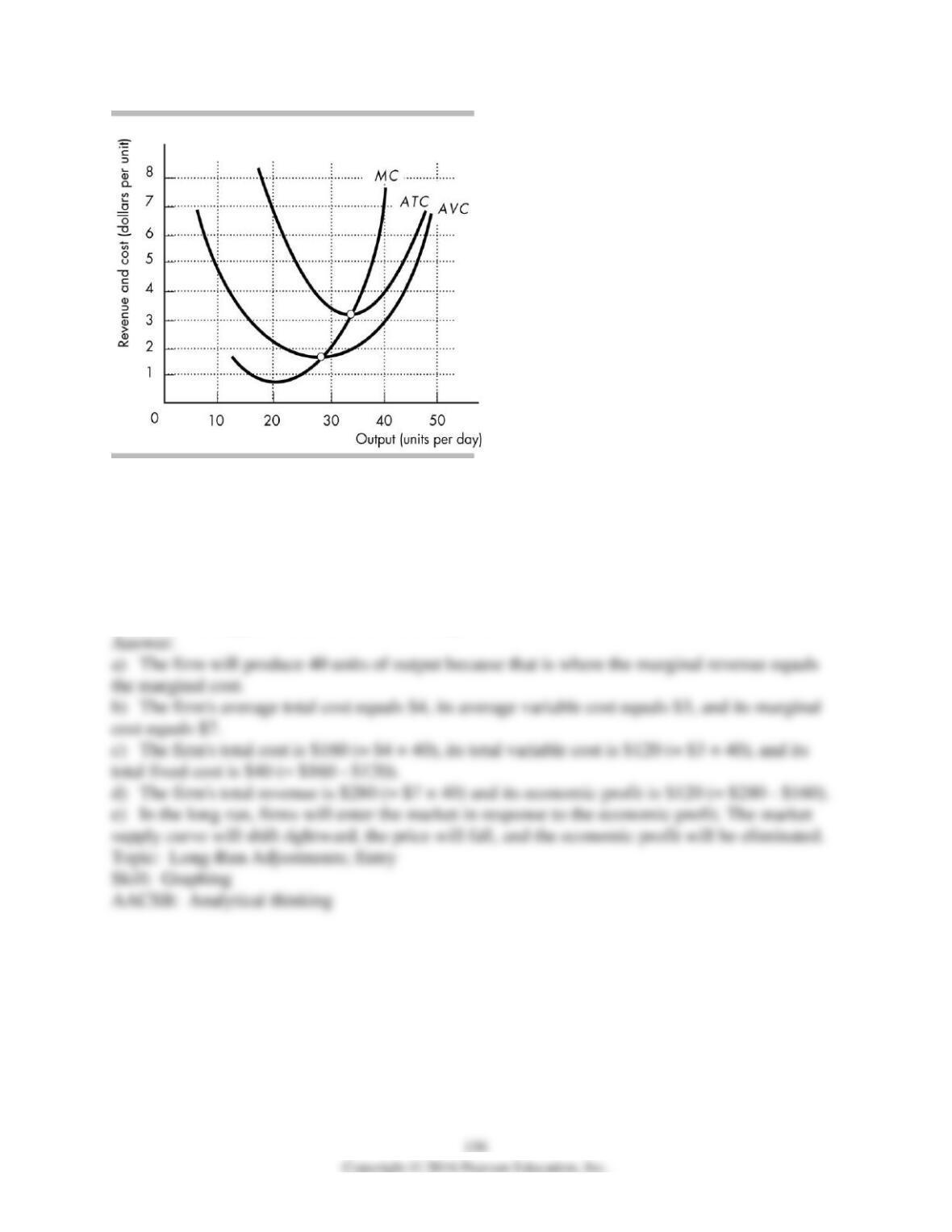

15) The above figure shows the cost curves of a profit-maximizing perfectly competitive firm. If

the price equals $7,

a) how much will the firm produce?

b) how much is the firm’s average total, average variable, and marginal costs?

c) how much is the firm’s total, total variable, and total fixed costs?

d) how much is the firm’s total revenue and economic profit?

e) what will happen in this market in the long run?

157

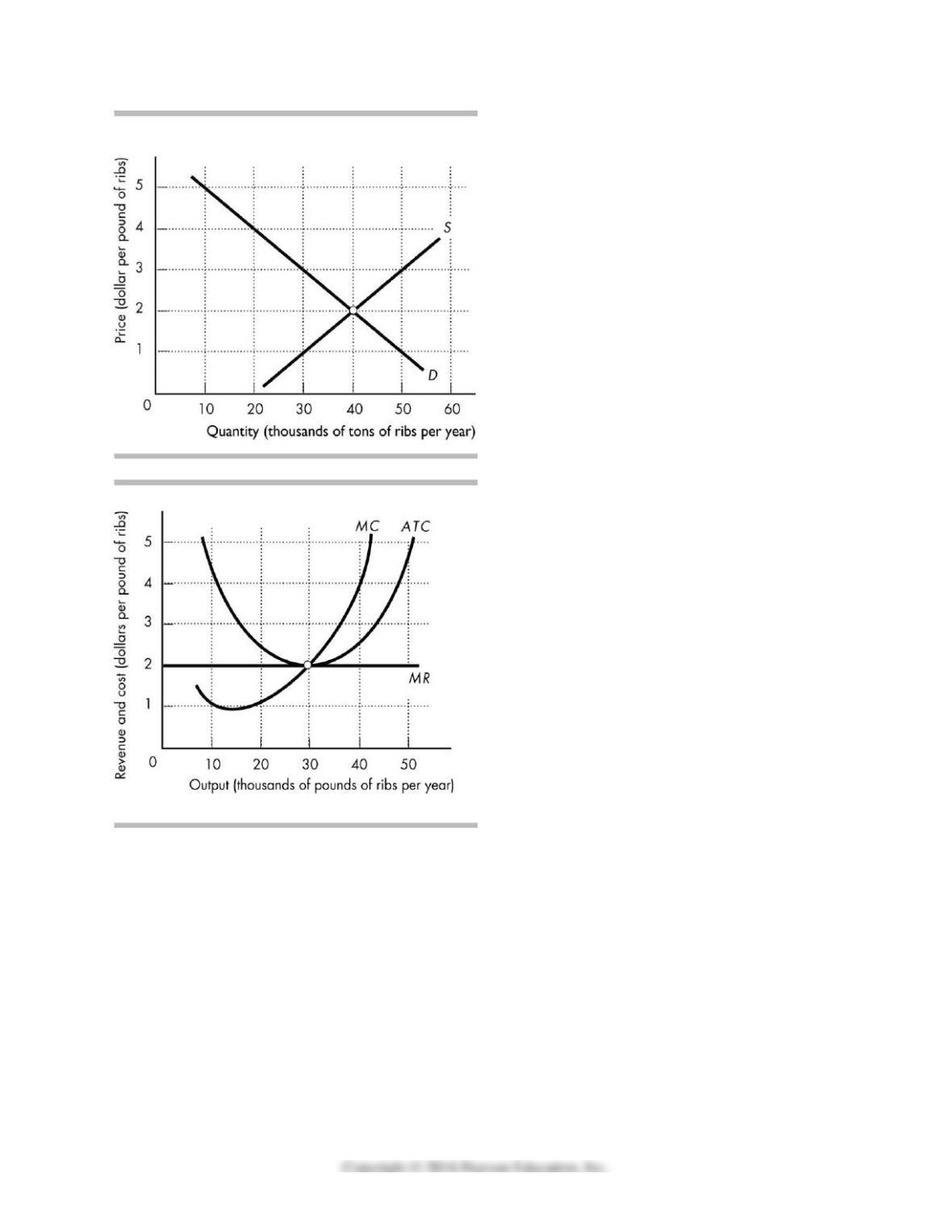

16) American restaurants receive their supply of baby back-ribs from American farms and from

farms in Denmark. In the figures above, the first diagram shows the perfectly competitive market

for baby back ribs in the United States. The second figure shows the situation at Premium

Standard Farm in Kansas, one of the many U.S. farms supplying these ribs.

Now assume that the United States imposes a ban on European meat in response to the foot-and-

mouth disease that has infected livestock in Europe. (Which the United States did several years

ago.) In particular, suppose that the U.S. ban decreases the supply by 40 tons a year. Using the

first figure, show the impact of this ban on the baby back rib market. Using the second figure,

show the impact on Premium Standard Farm in Kansas.

17) Suppose the bobby pin industry is perfectly competitive. The price of a packet of bobby pins

is $2.00. Pins and Needles, Inc. is a firm in this industry and is producing 1,000 packets of bobby

pins per day at the point where the MC = MR. The average cost of production at this output level

is $1.50 per packet.

a) What is the marginal cost of the 1,000th packet?

b) Is this firm making an economic profit, zero economical profit, or an economic loss? How

much?

c) Is the firm in long-run equilibrium? Why or why not?

10 True or False

1) In a perfectly competitive market, many firms sell an identical product.

2) Perfectly competitive firms are price takers.

3) A perfectly competitive firm produces so that its marginal cost equals the price.

4) A perfectly competitive firm maximizes its profit by producing the level of output so that its

average total cost equals the market price.

5) If a firm is maximizing profits, the extra revenue it receives from selling its last unit of output

exceeds the extra cost of producing that unit.

6) In perfect competition, firms enter the market whenever the market price exceeds the

minimum average variable cost.

7) A perfectly competitive firm definitely will shut down in the short run if its price is below its

average total cost.

8) A firm’s shutdown point is the output and price at which the firm’s total revenue just equals its

total variable cost.

9) Perfectly competitive firms will sometimes operate even though they incur an economic loss

in the short run.

10) The supply curve for a perfectly competitive firm is the portion of its marginal cost curve

that lies above its marginal revenue curve.

11) The supply curve for a perfectly competitive firm is the portion of its marginal cost curve

that lies above the average variable cost curve.

12) In the long run, a perfectly competitive firm can make an economic profit because its

marginal cost equals its average total cost.

13) In the long run, perfectly competitive firms cannot earn an economic profit.

14) Entry of new firms into a perfectly competitive market raises the product’s price.

15) Entry of new firms into a perfectly competitive market lowers the profits of the existing

firms.

16) In the long run, a perfectly competitive firm leaves the market if the market price is less than

the firm’s average total cost.

17) Easy entry and exit ensure that perfectly competitive firms cannot make a long-run economic

profit.

18) In the long run, perfectly competitive firms make zero economic profit, that is, their owners

make a normal profit.

19) In a perfectly competitive market, in the long run a permanent decrease in the market

demand results in a smaller number of firms.

20) When the market demand increases in a perfect competition, the long-run result is a larger

number of firms, a higher price, and a permanent economic profit for the firms.

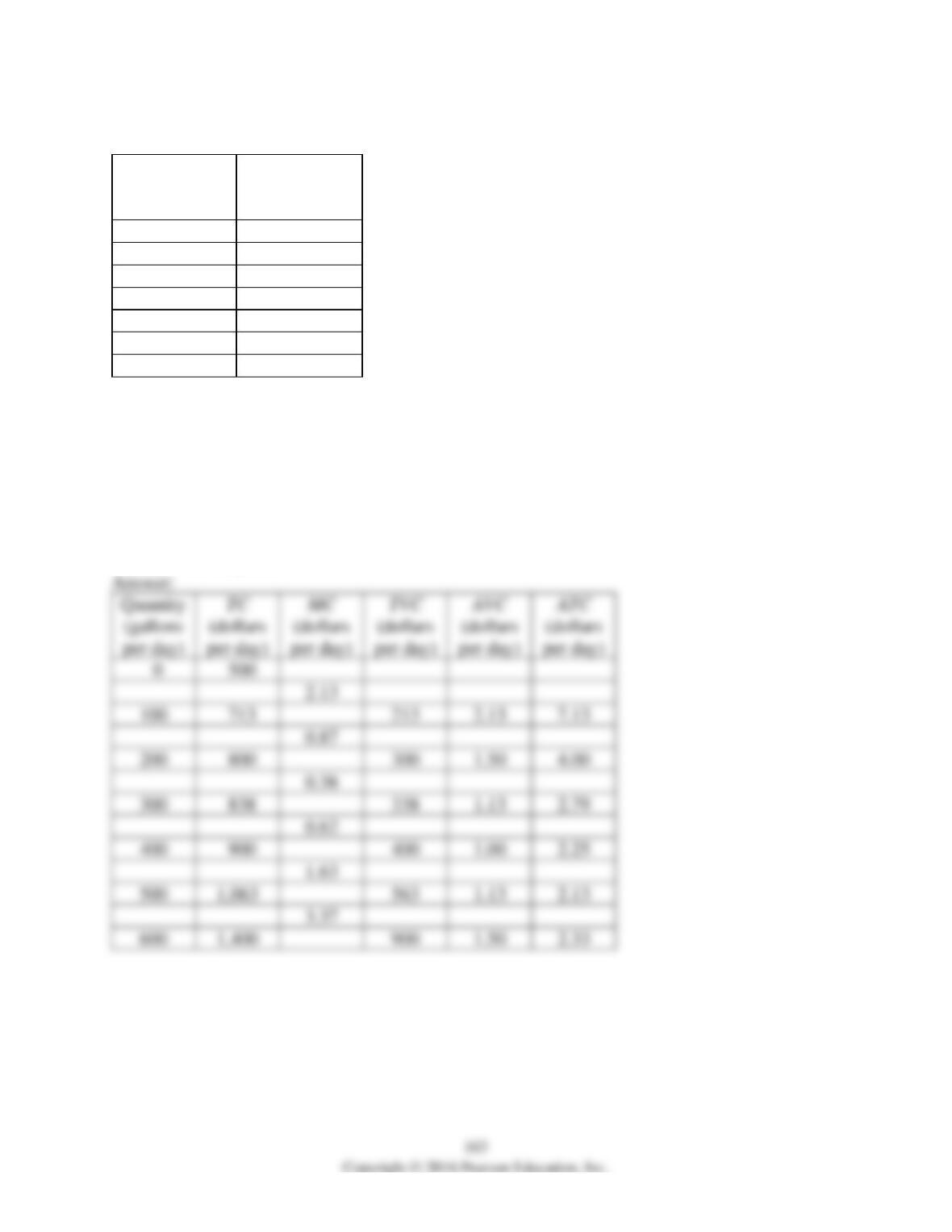

11 Extended Problems

Quantity

(gallons per

day)

Total cost

(dollars per day)

0

500

100

713

200

800

300

838

400

900

500

1,063

600

1,400

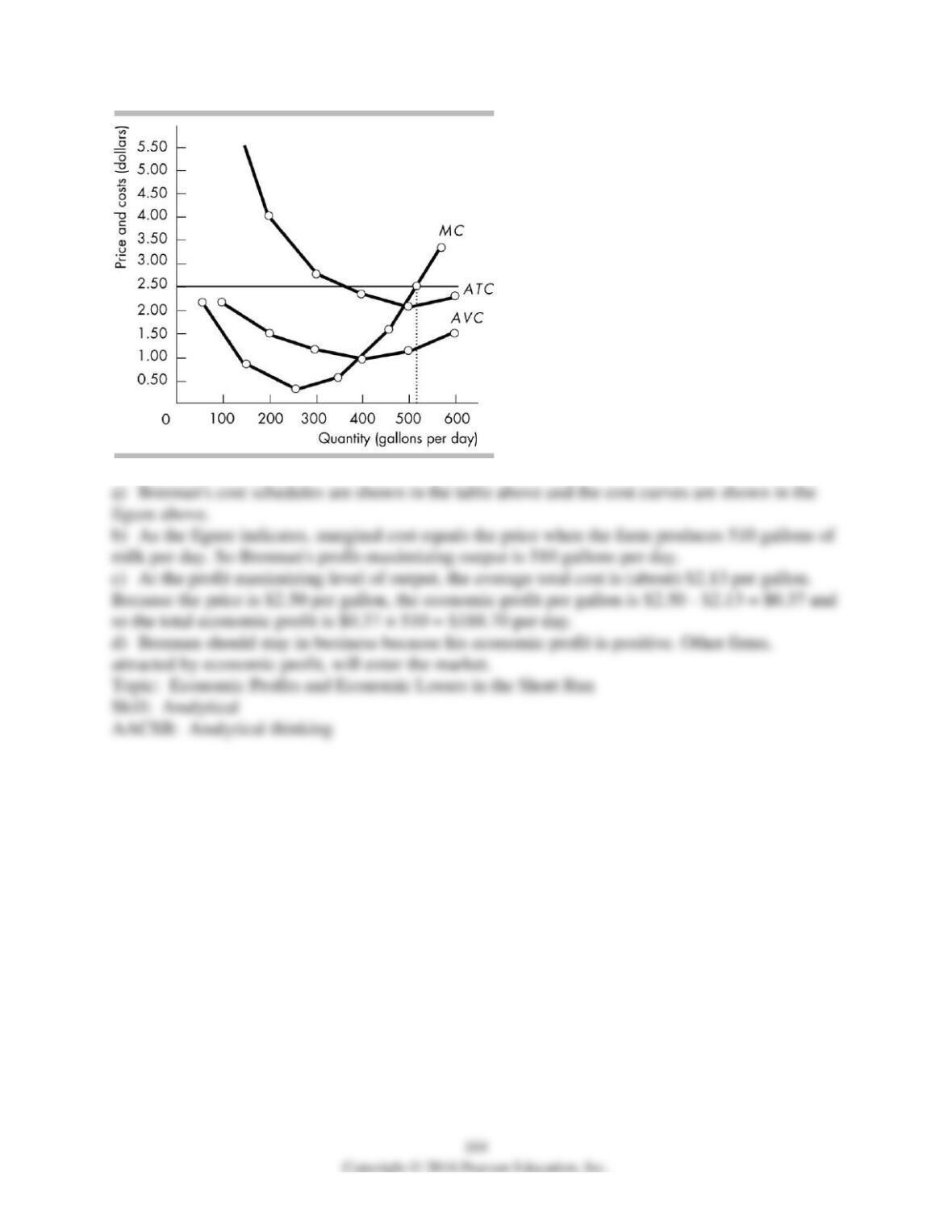

1) Brennan’s Farm produces and sells milk. The market for milk is perfectly competitive. The

market price of milk is $2.50 per gallon. The relationship between the farm’s output and total

costs is shown in the table above.

a) Draw Brennan’s average variable, average total, and marginal cost curves.

b) Use your graphs to find Brennan’s profit-maximizing output.

c) If Brennan maximizes his profit, how much profit does he make?

d) Should Brennan stay in business? Will other farms with costs the same as Brennan’s enter the

milk market? Explain.

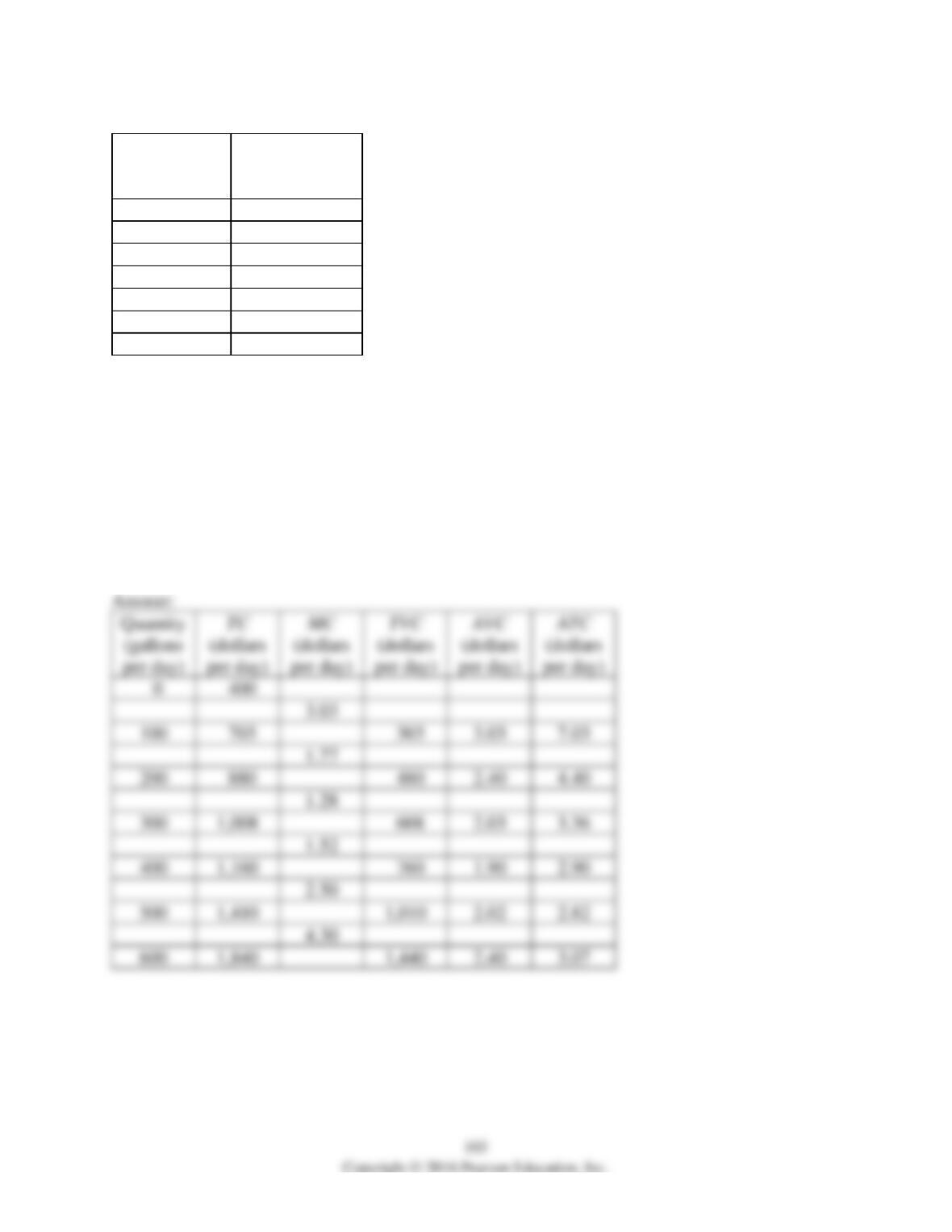

Quantity

(gallons per

day)

Total cost

(dollars per day)

0

400

100

703

200

880

300

1,008

400

1,160

500

1,410

600

1,840

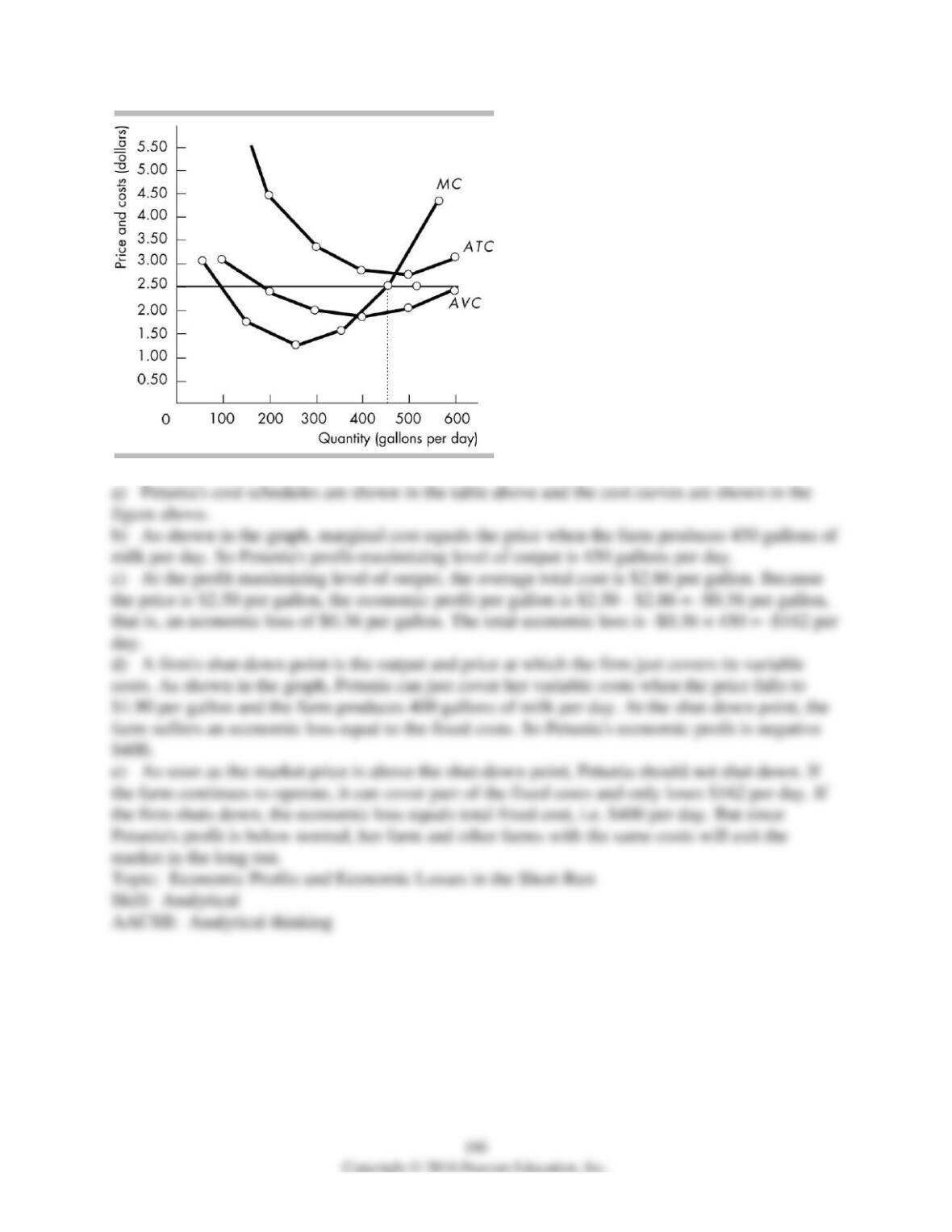

2) Petunia’s Farm produces and sells milk. The market for milk is perfectly competitive. The

market price of milk is $2.50 per gallon. The relationship between the farm’s output and total

costs is shown in the table above.

a) Draw Petunia’s average variable, average total, and marginal cost curves.

b) Use your graphs to find Petunia’s profit-maximizing output.

c) If Petunia maximizes her profit, how much profit does she make?

d) What is Petunia’s shutdown point? What is her economic profit at the shut-down point?

e) Should Petunia shut down? Will farms with costs the same as Petunia’s enter or exit the milk

market? Explain.

167

Price

(dollars per

gallon)

Quantity demanded

(thousands of gallons

per day)

2.50

600

3.50

500

4.50

400

3) The market for milk is perfectly competitive. There are 1,000 farms in the industry and the

relationship between a typical farm’s output and total costs is the same as in Problem 2. The

market demand schedule for milk is shown in the table above.

a) What is a typical farm’s supply schedule and what is the market supply schedule?

b) What is the market price? What quantity of milk is sold?

c) What is the output produced by each farm? What type of profit or loss is made by each farm?

d) Do farms enter or exit the market?

2.50

4.50