18) In a perfectly competitive market, an increase in market demand

A) raises the price in the short run and attracts new firms in the long run.

B) raises the price in the short run and the long run.

C) lowers the price in the short run and in the long run.

D) has no effect on the price in either the short run or the long run because the firms are price

takers.

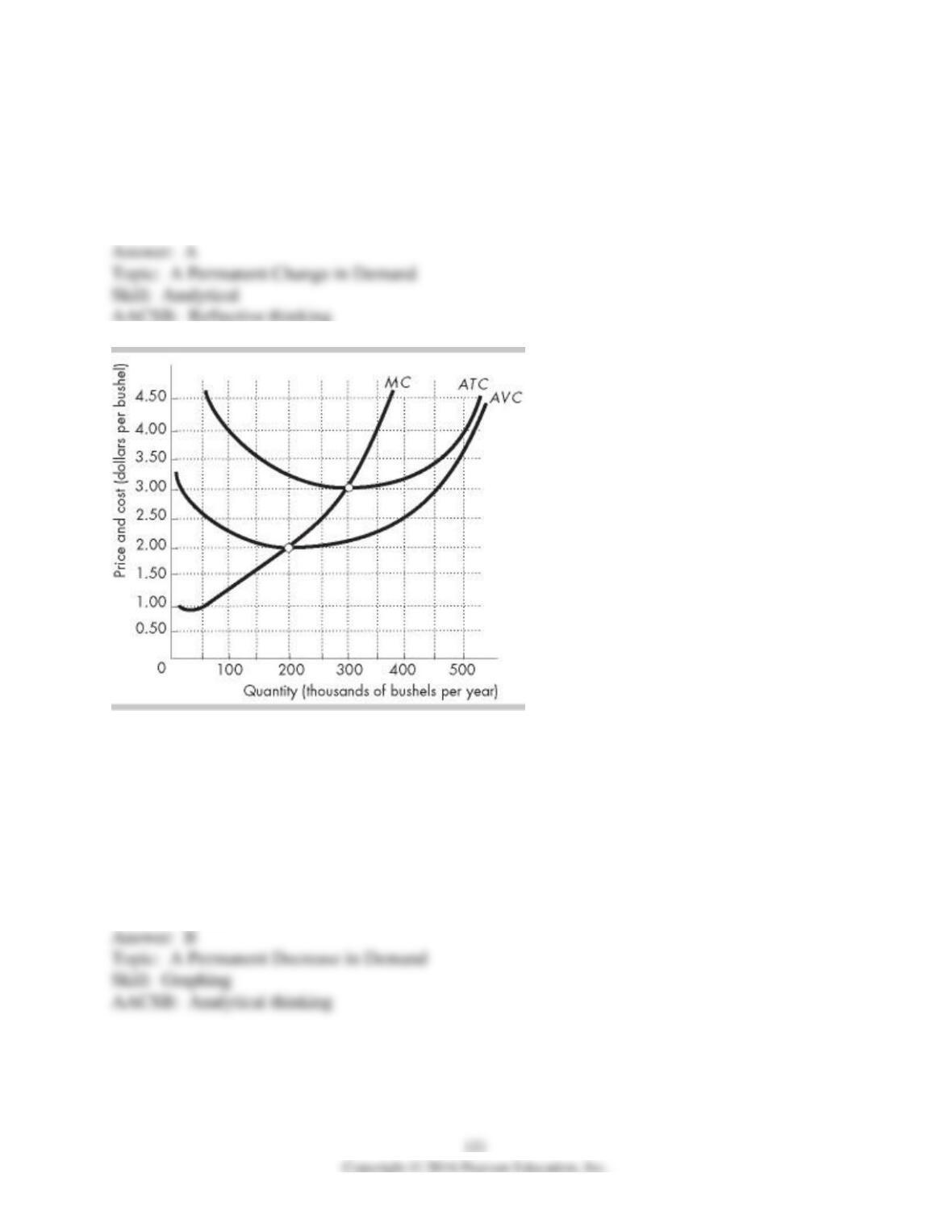

19) The figure above shows a typical perfectly competitive corn farm, whose marginal cost curve

is MC and average total cost curve is ATC. The market is initially in a long-run equilibrium,

where the price is $3.00 per bushel. Then, the market demand for corn decreases and, in the short

run, the price falls to $2.50 per bushel. In the new short-run equilibrium, the farm produces

________ bushels of corn and sells corn at ________ per bushel.

A) 250,000; $3.00

B) 250,000; $2.50

C) 300,000; $2.50

D) 200,000; $2.50

20) The figure above shows a typical perfectly competitive corn farm, whose marginal cost curve

is MC and average total cost curve is ATC. The market is initially in a long-run equilibrium,

where the price is $3.00 per bushel. Then, the market demand for corn decreases and, in the short

run, the price falls to $2.50 per bushel. In the new short-run equilibrium, the farm

A) incurs an economic loss of between $1 and $40,000.

B) makes zero economic profit.

C) incurs an economic loss of between $40,001 and $130,000.

D) incurs an economic loss of more than $130,001.

21) The figure above shows a typical perfectly competitive corn farm, whose marginal cost curve

is MC and average total cost curve is ATC. The market is initially in a long-run equilibrium,

where the price is $3.00 per bushel. Then, the market demand for corn decreases and, in the short

run, the price falls to $2.50 per bushel. In the long run, the price of corn is ________ and a

typical farm produces ________ bushels of corn.

A) $2.00; 200,000

B) $3.50; 250,000

C) $2.50; 250,000

D) $3.00; 300,000

22) The figure above shows a typical perfectly competitive corn farm, whose marginal cost curve

is MC and average total cost curve is ATC. Assuming there are no changes in technology, in the

long run the lowest possible price for corn is ________ per bushel.

A) $2.50

B) $2.00

C) $3.00

D) $3.50

23) In a perfectly competitive market, technological advances bring ________ economic profits

for producers and ________ lower prices for consumers.

A) permanent; permanently

B) permanent; temporarily

C) temporary; permanently

D) temporary; temporarily

24) There is a technological advance in a perfectly market. Which of the following statements is

NOT true?

A) As more firms begin to use the new technology, the market supply increases and the price

falls.

B) Technological change brings permanent gains to producers and temporary gains to

consumers.

C) In the new long-run equilibrium, all the old-technology firms have exited.

D) In the long-run equilibrium, competition eliminates any short-run economic profit.

25) The demand for a product produced in a perfectly competitive market permanently increases.

In the short run, the price

A) rises and each firm produces less output.

B) rises and each firm produces more output.

C) does not change as new firms enter the industry.

D) does not change because each firm produces more output.

26) The industry that produces zangs is in long-run equilibrium. Then the demand for zangs

increases permanently. As a result, firms in the industry will ________. Some firms will

________ the industry, and the industry supply curve will shift ________.

A) make economic an profit; enter; rightward

B) make zero economic profit; exit; leftward

C) incur economic losses; exit; rightward

D) incur economic losses; exit; leftward

27) Initially, a perfectly competitive industry that has 1,000 firms is in long-run equilibrium.

Then 100 firms in the industry adopt a new technology that reduces the average cost of

producing the good. In the short run, the price ________, firms with the new technology make

________ economic profit, and firms with the old technology ________.

A) remains the same; zero; incur economic losses

B) falls; positive; incur economic losses

C) remains the same; positive; make normal profit

D) remains the same; positive; incur economic losses

28) A perfectly competitive industry is in long-run equilibrium. Some firms in the industry adopt

new technology that reduces the average total cost of producing the good. In the long run, the

price is ________, firms with the new technology make ________ economic profit, and firms

with the old technology ________.

A) lower; zero; exit the industry

B) constant; a positive; make zero economic profit

C) lower; zero; switch to the new technology or exit the industry

D) constant; zero; exit the industry

6 Competition and Efficiency

1) In the long-run equilibrium for a perfectly competitive market

A) the firms’ economic profits are zero.

B) there is no incentive for entry or exit.

C) average total costs of production are minimized.

D) All of the above are correct.

2) If the donut industry is perfectly competitive and is in long-run equilibrium, then the price of a

donut

A) is greater than marginal cost.

B) is greater than short-run average cost.

C) is greater than long-run average cost.

D) equals long-run average cost.

3) In the long-run equilibrium, perfectly competitive firms produce the level of output such that

A) marginal cost is minimized.

B) average total cost is minimized.

C) marginal cost equals the price.

D) Both answers B and C are correct.

4) In the long-run equilibrium, perfectly competitive firms produce where

A) marginal cost is minimized.

B) average total cost is minimized.

C) average revenue is zero.

D) All of the above are correct.

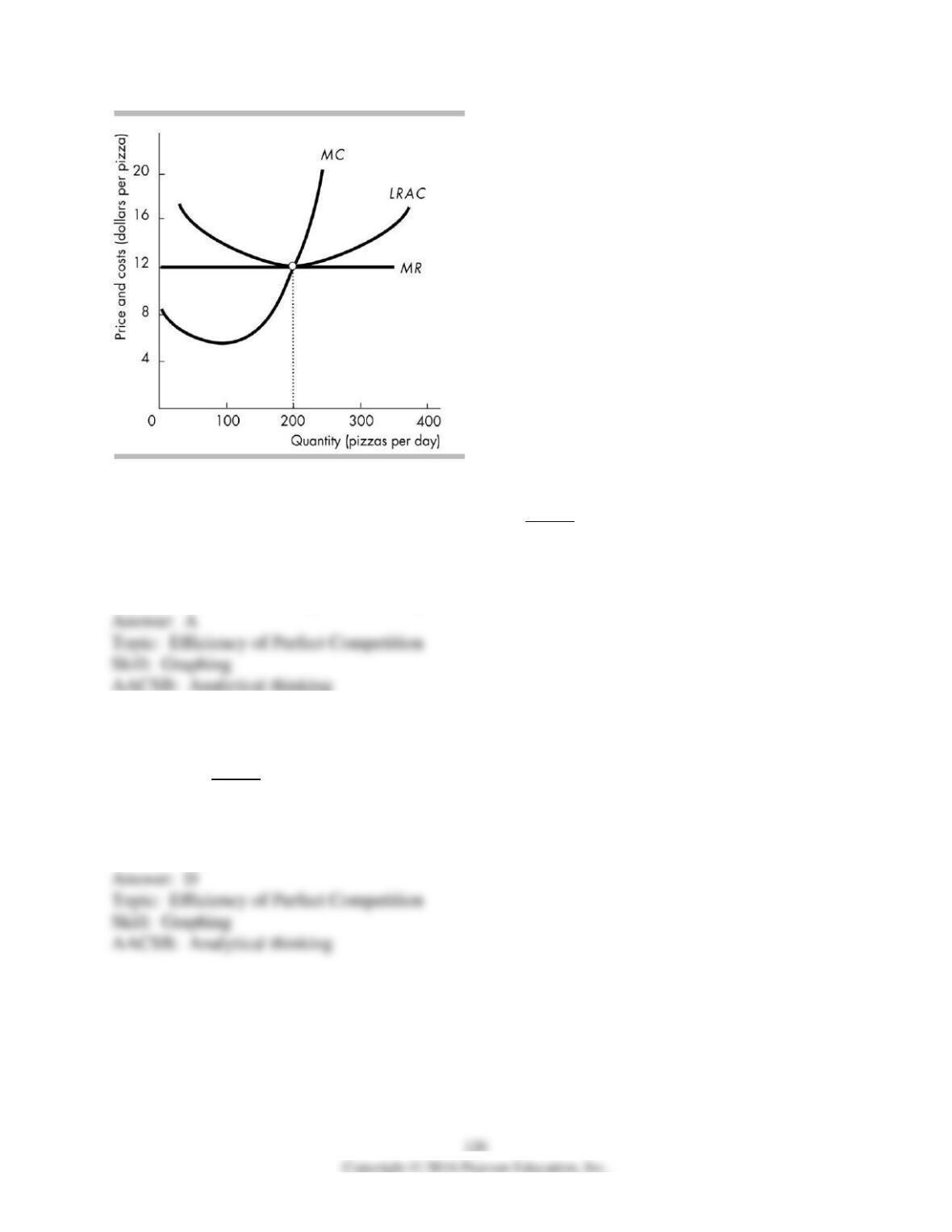

5) The figure above shows the marginal revenue and long-run cost curves for a perfectly

competitive firm. Which of the following statements is TRUE?

A) The firm is producing at minimum long-run average cost.

B) Over time, this firm will leave this industry.

C) The firm is earning positive economic profit.

D) The firm will eventually decrease its production.

6) The figure above shows the marginal revenue and long-run cost curves for a perfectly

competitive firm. All other firms in the industry have identical curves. Which of the following

statements is TRUE?

A) The firm’s average cost exceeds the price.

B) Over time, firms will enter this industry.

C) The firm is earning economic profit.

D) None of the above is true.

7) Consumer surplus ________.

A) equals total revenue minus marginal cost

B) is maximized when the market outcome is efficient

C) equals total revenue minus opportunity cost

D) plus producer surplus is maximized when resources are used efficiently

8) In the long-run equilibrium in a perfectly competitive market, the firms produce at the

________ possible average total cost and the price equals the ________ possible average total

cost.

A) highest; highest

B) lowest; lowest

C) highest; lowest

D) lowest; highest

7 News Based Questions

1) Which of the following four firms would most likely be part of a perfectly competitive

market?

A) Village Pizza sells NY style pizza and hard-to-find microbrews in a college town.

B) The WaveHouse is the only place in San Diego where you can ride an indoor 10 foot wave.

C) Mark sells the tomatoes he grew in his backyard at the local farmers market.

D) Amara Massage specializes in pre- and post-natal massage.

2) Which of the following four firms would most likely NOT be part of a perfectly competitive

market?

A) Mark sells his tomatoes at the local farmers market.

B) The WaveHouse is the only place in San Diego where you can ride an indoor 10 foot wave.

C) Village Pizza sells pizza in a college town.

D) Space Age Fuel is a gas station in Bend, Oregon.

3) Fresno County, California is the largest agricultural producing county in the country and

almonds are an important crop with more than 99,000 acres harvested. Each acre produces about

a ton of almonds and sold at a price of $4300 a ton. The Sagardia Brothers grew 600 acres of

almonds that year. In what type of market does the Sagardia Brother operate?

A) perfect competition

B) monopoly

C) oligopoly

D) monopolistic competition

4) Fresno County, California is the largest agricultural producing county in the country and

almonds are an important crop with more than 99,000 acres harvested. Each acre produces about

a ton of almonds and sold at a price of $4300 a ton. The Sagardia Brothers grew 600 acres of

almonds that year and they are price takers. What is the Brother’s total revenue?

A) $4300

B) $4900

C) $59.4 million

D) $2.58 million

5) Fresno County, California is the largest agricultural producing county in the country and

almonds are an important crop with more than 99,000 acres harvested. Each acre produces about

a ton of almonds and sold at a price of $4300 a ton. The Sagardia Brothers grew 600 acres of

almonds. What would happen if the Sagardia Brothers priced their almonds at $4500 a ton?

A) Profits will be higher than when they sell them at the lower price.

B) The quantity sold will be higher.

C) They will not sell any almonds.

D) They will sell fewer almonds, but profits will be higher.

6) Fresno County, California is the largest agricultural producing county in the country and

almonds are an important crop with more than 99,000 acres harvested. Each acre produces about

a ton of almonds and sold at a price of $4300 a ton. The Sagardia Brothers grew 600 acres of

almonds. What would happen if the Sagardia Brothers priced their almonds at $4000 a ton?

A) Profits will be higher than when they sell them at the higher price.

B) They will sell the same amount of almonds, but profits will be lower.

C) The quantity sold will be higher.

D) They will not sell any almonds.

7) Fresno County, California is the largest agricultural producing county in the country and

almonds are an important crop with more than 99,000 acres harvested. Each acre produces about

a ton of almonds and sold at a price of $4300 a ton. The Sagardia Brothers grew 600 acres of

almonds. How many tons would the brothers sell if they priced the almonds at $4500 a ton?

A) 0 tons

B) 600 tons

C) 400 tons

D) 200 tons

8) All along the beach in San Diego, California are shops which rent boogie boards by the hour.

Tourists perceive that all rental boogie boards are identical, all prices are clearly listed on signs

in front of the shops, and there are no restrictions on entry and exit in the boogie board market.

What type of market is the boogie board market?

A) monopoly

B) oligopoly

C) monopolistic competition

D) perfect competition

9) All along the beach in San Diego, California are shops which rent boogie boards by the hour.

Tourists perceive that all rental boogie boards are identical, all prices are clearly listed on signs

in front of the shops, and there are no restrictions on entry and exit in the boogie board market.

Suppose Surf’s Up is a boogie board rental shop. What is the shape of Surf’s Up’s demand curve

as compared to the market demand curve?

A) Surf’s Up’s demand curve is vertical and the market demand curve is downward sloping.

B) Surf’s Up’s demand curve is horizontal and the market demand curve is upward sloping.

C) Surf’s Up’s demand curve is horizontal and the market demand curve is downward sloping.

D) Surf’s Up’s demand curve is vertical and the market demand curve is upward sloping.

10) All along the beach in San Diego, California are shops which rent boogie boards for $3 per

hour. Tourists perceive that all rental boogie boards are identical and there are no restrictions on

entry and exit in the boogie board market. Suppose Surf’s Up is a boogie board rental shop. To

maximize profits, Surf’s Up would produce a quantity where

A) Marginal revenue is greater than marginal cost.

B) Marginal revenue is equal to marginal cost.

C) Marginal revenue is less than marginal cost.

D) Price is maximized.

11) A worldwide hops (a flowers used in brewing) shortage made stouts, ales and other specialty

microbrews more pricy in 2008. A triple whammy of bad weather in Europe, an increase in the

price of barley and a decrease in hops production in the U.S. led to a price increase of 20 percent

for the most widely grown varieties, to 80 percent for specialty hops. What is the effect of this

hops shortage on a microbrewery’s cost curves?

A) Short run fixed costs would increase.

B) Short run total costs would decrease.

C) Short run average variable costs would decrease.

D) Short run variable costs would increase.

12) A worldwide hops (a flowers used in brewing) shortage made stouts, ales and other specialty

microbrews more pricy in 2008. Gayle Goshie, a hops farmer, blames overproduction for hops’

previously cheap place on the agricultural market. The glut pushed many hop farmers out

business, which gradually helped hop prices recover. Suppose farming hops is a perfectly

competitive market. Why would some hop farmers go out of business?

A) because the price of hops was below the minimum of average fixed cost

B) because the price of hops was lower than the minimum of average variable cost

C) because the price of hops was higher than the minimum of average variable cost

D) because the price of hops was lower than the minimum of average total cost

13) A worldwide hops (a flower used in brewing) shortage made stouts, ales and other specialty

microbrews more pricy in 2008. Gayle Goshie, a hops farmer, blames overproduction for hops’

previously cheap place on the agricultural market. The glut pushed many hops farmers out

business, which gradually helped hops prices recover. Suppose farming hops is a perfectly

competitive market. How did farmers going out of business help hops prices recover?

A) Fewer farmers cause the market supply curve to shift leftward, causing price to rise.

B) Fewer farmers cause an increase in market demand, causing price to rise.

C) Fewer farmers cause an increase in the surviving firms’ costs, causing higher prices.

D) Fewer farmers cause the individual firms’ supply curves to decrease, causing higher prices.

14) “Higher ethanol production definitely and directly raises the price of corn,” said USDA

economist Ephraim Leibtag. In the short run, what is TRUE if the production of ethanol

increases?

A) The demand for corn will increase.

B) The supply of ethanol will decrease.

C) The supply of corn will increase.

D) The demand for ethanol will increase.

15) “Higher ethanol production definitely and directly raises the price of corn,” said USDA

economist Ephraim Leibtag. In the short run in the corn market, what is TRUE if the production

of ethanol increases?

A) The demand curve for individual corn farmers will shift upward.

B) The price individual corn farmers receive will decrease.

C) The total cost curve for individual corn farmers will shift upward.

D) The marginal cost curve for individual corn farmers will shift downward.

16) “Higher ethanol production definitely and directly raises the price of corn,” said USDA

economist Ephraim Leibtag. In the short run in the corn market, what is TRUE if the production

of ethanol increases?

A) Individual corn farmers will incur an economic loss in the short run and will shut down.

B) Individual corn farmers will make an economic profit in the short run.

C) Individual corn farmers will incur an economic loss in the short run, but they will still

produce.

D) Individual corn farmers will make zero economic profit in the short run.

17) “Higher ethanol production definitely and directly raises the price of corn,” said USDA

economist Ephraim Leibtag. In the long run in the corn market, what is TRUE if the production

of ethanol increases?

A) Existing corn farmers will exit the market and decrease the market price.

B) New corn farmers will enter the market and increase the market price.

C) Existing corn farmers will exit the market and increase the market price.

D) New corn farmers will enter the market and decrease the market price.

18) “Higher ethanol production definitely and directly raises the price of corn,” said USDA

economist Ephraim Leibtag. In the long run in the corn market, what is TRUE if the production

of ethanol increases?

A) Individual corn farmers will make zero economic profit in the long run.

B) Individual corn farmers will make an economic profit in the long run.

C) Individual corn farmers will incur an economic loss in the long run, but they will still

produce.

D) Individual corn farmers will incur an economic loss in the long run and will shut down.

19) What is one reason why would corn production, which takes place in a perfectly competitive

market, achieve an efficient use of resources?

A) because a perfectly competitive firm produces at the lowest possible long run average total

cost

B) because a perfectly competitive firm produces where marginal revenue exceeds marginal cost

C) because a perfectly competitive firm is a price maker

D) because the goal of a perfectly competitive firm is to profit maximize

8 Essay Questions

1) What are the requirements for perfect competition?

2) “A perfectly competitive firm is called a price maker because all the firms together must make

the market price.” Is the previous statement correct or incorrect? Briefly explain your answer.

3) “Perfectly competitive firms have total control over the price they set for their product.”

Explain why the previous statement is correct or incorrect.

4) Does a perfectly competitive producer have any incentive to undercut the current market

price? Explain your answer

5) Why are perfectly competitive ranchers in Montana price takers?

6) If a perfectly competitive firm manufacturing chairs decides to produce 100 more chairs, what

happens to the market price of a chair?

7) Why is the demand for a perfectly competitive firm’s good perfectly elastic even though the

market demand is not?

8) Hubert’s Copy Services is in perfect competition. Hubert currently charges 10 cents per page,

which is the going market price. He thinks that he can increase his profit by raising the price. Is it

possible? Why or why not?

9) Jane’s Copy Services is in perfect competition. Jane currently charges 10 cents per page,

which is the going market price. Jane thinks that she can increase her profit if she lowers her

price to 8 cents per page to increase the demand for her service. Is Jane right? Why or why not?

10) Do firms in perfect competition advertise their products? Why or why not?

11) What is a normal profit?

12) Why does the profit-maximizing level of production occur at the point where marginal

revenue equals marginal cost?

13) Martha’s Cleaning Services is a perfectly competitive firm that currently cleans 30 offices a

week and charges $20 per office, which is the going market price. Martha’s marginal cost is $15.

What should Martha do to increase her economic profit? Clean more offices? Raise her price?

Explain your answer.

14) Ellen’s Painting Services is a perfectly competitive firm that currently paints 10 houses a

month and charges $100 per house, which is the going market price. Ellen’s marginal cost is

positively related with the quantity of service she provides and is currently $120. What should

Ellen do to increase her economic profit? Paint more houses? Raise her price? Explain your

answer.

15) “A perfectly competitive firm will shut down if the price falls below its average total cost.”

Do you agree? Explain.

16) If the price received by a perfectly competitive firm is less than its average variable cost,

what will the firm do in the short run? Why?

17) Define the shutdown point. Explain why the firm shuts down in the short run if the price falls

below this point.

18) Will a perfectly competitive firm ever produce in the short run even though it is incurring an

economic loss?

19) What must be the case if a perfectly competitive firm’s economic loss is less by shutting

down rather than by producing and selling some output?

20) Can a perfectly competitive firm make an economic profit in the short run? Can it incur an

economic loss?

21) If the market price is less than a perfectly competitive firm’s average total cost, what sort of

profit or loss is the firm making?

22) What is the relationship between the price, P, and the average total cost, ATC, for a firm in

perfect competition that makes an economic profit? That makes zero economic profit? That

incurs an economic loss?

23) What is a perfectly competitive firm’s short-run supply curve?

24) If the market price faced by a perfectly competitive firm increases, in the short run how does

the firm respond?

25) Explain the process that drives the economic profit to zero in the long run for a perfectly

competitive firm.

26) Describe the different possible profit outcomes for a perfectly competitive firm in the short

run versus the long run. Explain why they occur.

27) When do new firms enter a perfectly competitive market? When does entry stop?

28) What role does economic profit play in a competitive market?

29) “For a perfectly competitive market, an economic profit attracts new firms. But when these

firms enter the market, the price falls and the economic profit is eliminated.” Are the previous

statements correct or incorrect? What is the long-run profit or loss outcome for firms in a

perfectly competitive market?

30) In the long run, perfectly competitive firms cannot make an economic profit. Why?

31) The U-pick berry market is perfectly competitive. Suppose that all U-pick blueberry farms

have the same cost curves and all are making an economic profit. What happens as time passes?

What is the long-run equilibrium outcome?