Quantity

(pizzas per

hour)

Total cost, TC

(dollars per

hour)

0

10

1

18

2

30

3

48

4

70

5

98

6

120

10) Giuseppe’s Pizza is a perfectly competitive firm. The firm’s costs are shown in the table

above. If the market price is $15, the firm will

A) shut down.

B) leave the market in the long run.

C) stay in the market in the long run.

D) make an economic profit.

11) Giuseppe’s Pizza is a perfectly competitive firm. The firm’s costs are shown in the table

above. If the market price is $22, the firm will

A) shut down.

B) leave the market in the long run.

C) stay in the market in the long run.

D) incur an economic loss.

Quantity

(dozens of sea

shells per day)

Total variable

cost

(dollars)

200

60.00

201

61.00

202

62.50

203

64.00

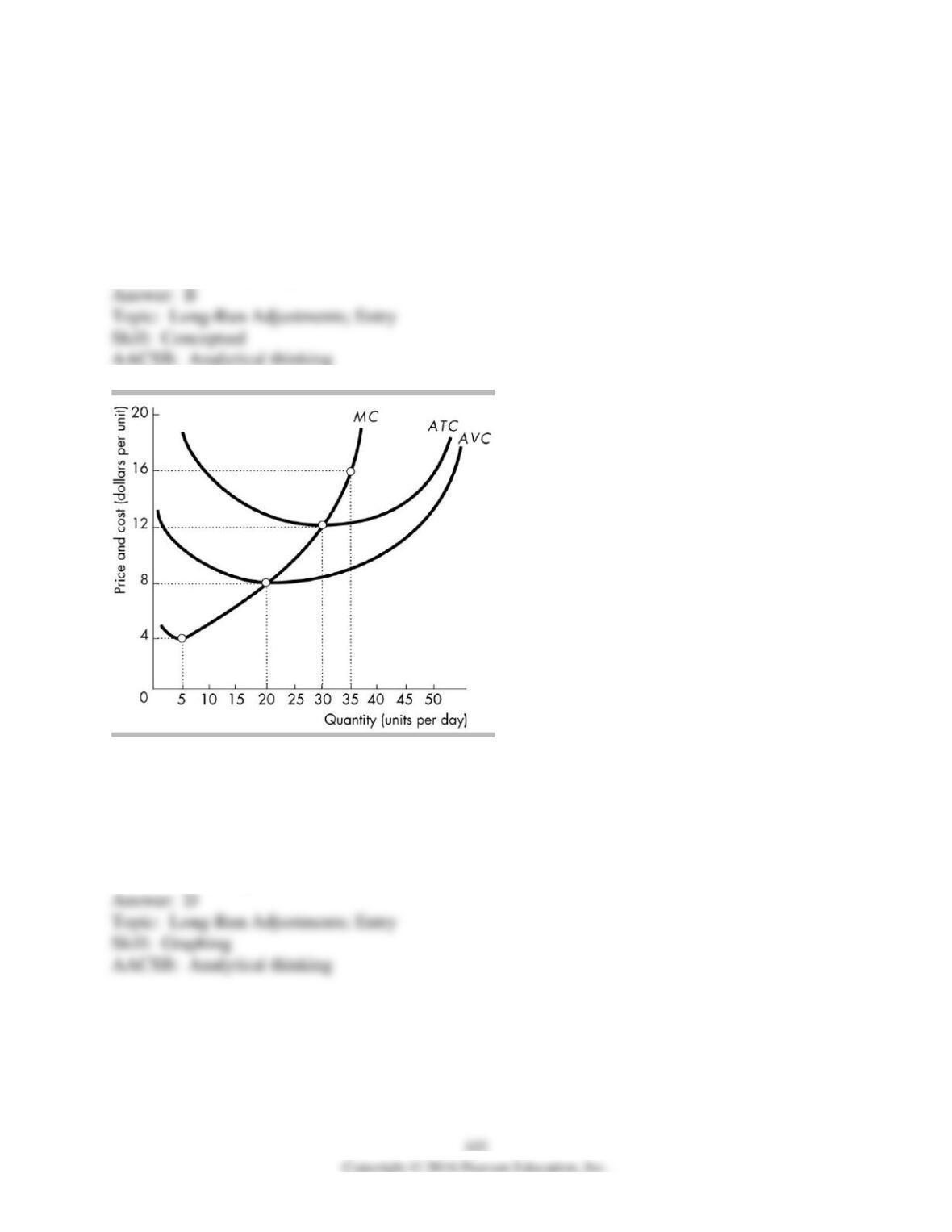

204

66.00

205

68.50

206

72.00

12) Sue’s Sea Shells by the Sea Shore is a perfectly competitive firm selling sea shells at the

market price of $2 per dozen. Sue’s Sea Shells by the Sea Shore has fixed costs of $40 per day

and a variable cost schedule in the table above. The profit-maximizing level of output for Sue’s

Sea Shells by the Sea Shore is

A) 202 dozen sea shells by the sea shore per day.

B) 204 dozen sea shells by the sea shore per day.

C) 205 dozen sea shells by the sea shore per day.

D) 206 dozen sea shells by the sea shore per day.

13) Sue’s Sea Shells by the Sea Shore is a perfectly competitive firm selling sea shells at the

market price of $2 per dozen. Sue’s Sea Shells by the Sea Shore has fixed costs of $40 per day

and a variable cost schedule in the table above. The maximum profit attainable by Sue’s Sea

Shells by the Sea Shore is

A) $262.00 per day.

B) $262.50 per day.

C) $302.00 per day.

D) $302.50 per day.

14) Sue’s Sea Shells by the Sea Shore is a perfectly competitive firm selling sea shells at the

market price of $2 per dozen. Sue’s Sea Shells by the Sea Shore has fixed costs of $40 per day

and a variable cost schedule in the table above. Based on this information, we can expect the

number of firms in the sea shell market to

A) decrease.

B) increase.

C) remain constant.

D) It is impossible to say.

15) The above figure shows the cost curves for a perfectly competitive firm. If all firms in the

market have the same cost curves and the price equals $16 per unit

A) the market is in its long-run equilibrium.

B) over time, firms will leave this market.

C) the firm is making zero economic profit.

D) over time, the price will fall as new firms enter the market.

16) The apple market is perfectly competitive and is in long-run equilibrium. Now a disease kills

50 percent of the apple orchards. In the short run, the price of a bag of apples ________ and the

remaining apple growers make ________ economic profit. In the long run, the ________.

A) increases; zero; price of apples will return to their original level

B) remains the same; zero; orchards will be replanted and growers will make normal profits

C) increases; zero; orchards will be replanted and economic profit will return to zero

D) increases; positive; orchards will be replanted and economic profit will return to zero

17) Homer’s Holesome Donuts has determined that its profit-maximizing quantity is 10,000

donuts per year. Homer’s earns $12,000 in revenue from the sale of those donuts. Homer’s has

two costs. First he pays $16,000 in annual rental payments for its five-year lease on its store.

Second Homer incurs an additional cost of $5,000 for ingredients. Should Homer’s exit the

market in the long run?

A) yes, because he is incurring an economic loss

B) yes, because all costs are fixed in the long run

C) no, because he is making an economic profit

D) no, because all costs are variable in the long run

18) If firms in a competitive market are ________ then there is ________ for firms to ________

the industry.

A) incurring economic losses; an incentive; exit

B) incurring economic losses; no incentive; exit

C) making economic profits; no incentive; enter

D) making zero economic profit; an incentive; exit

19) Suppose some firms in a perfectly competitive market are incurring an economic loss. As a

result,

A) all the firms will eventually incur an economic loss.

B) some firms will leave the market and the price of the good will rise.

C) some firms will leave the market and the remaining firms’ quantity will decrease.

D) the total market economic profit must equal $0.

20) Suppose firms in a perfectly competitive market are incurring an economic loss. As firms

exit, the price ________ and the economic loss of the surviving firms ________.

A) rises; increases

B) rises; decreases

C) falls; increases

D) falls; decreases

21) In the long-run, if firms in a perfectly competitive market are incurring persistent economic

losses, some firms will

A) exit and the price will fall.

B) exit and the price will rise.

C) enter and the price might either rise or fall.

D) exit and the price might either rise or fall.

22) In the long run, if firms in a perfectly competitive market are incurring economic losses, then

A) new firms will enter the market and the price will rise.

B) some firms will leave the market and the price will fall.

C) some firms will leave the market and the price will rise.

D) new firms will enter the market and the price will fall.

23) If perfectly competitive firms exit a market, the

A) market supply curve shifts leftward.

B) price of the good or service falls.

C) profits of the remaining firms decrease.

D) output of the industry increases.

24) As perfectly competitive firms leave a market because they are incurring an economic loss,

the price of the good ________ and the economic loss of each remaining firm ________.

A) rises; increases

B) rises; decreases

C) falls; increases

D) falls; decreases

25) In the long run, a perfectly competitive firm will exit a market when

A) its total revenue is less than its total cost.

B) its marginal revenue curve is below the minimum of its average total cost curve.

C) the price is greater than the minimum of its average total cost curve.

D) Both answers A and B are correct.

26) A perfectly competitive firm initially is earning zero economic profit. Then, a decrease in

demand for the firm’s product occurs. Of the following, in the long run which action listed below

is the firm most likely to take?

A) Increase the quantity it produces.

B) Increase its advertising to increase the demand for its product.

C) Exit the market.

D) Increase the size of its plant.

27) Suppose that newspaper companies are now required to use recycled paper, which is more

expensive than new paper. Which of the following is most likely to result if the newspaper

industry is highly competitive?

A) The firms’ costs rise, resulting in positive economic profit in the short run and, hence, the

industry supply curve shifts rightward in the long run.

B) The firms’ costs rise, resulting in economic losses in the short run and, hence, the industry

supply curve shifts rightward in the long run.

C) The firms’ costs rise, resulting in economic losses in the short run and, hence, the industry

supply curve shifts leftward in the long run.

D) The industry supply curve shifts leftward in the short run, causing permanent long-run

economic losses.

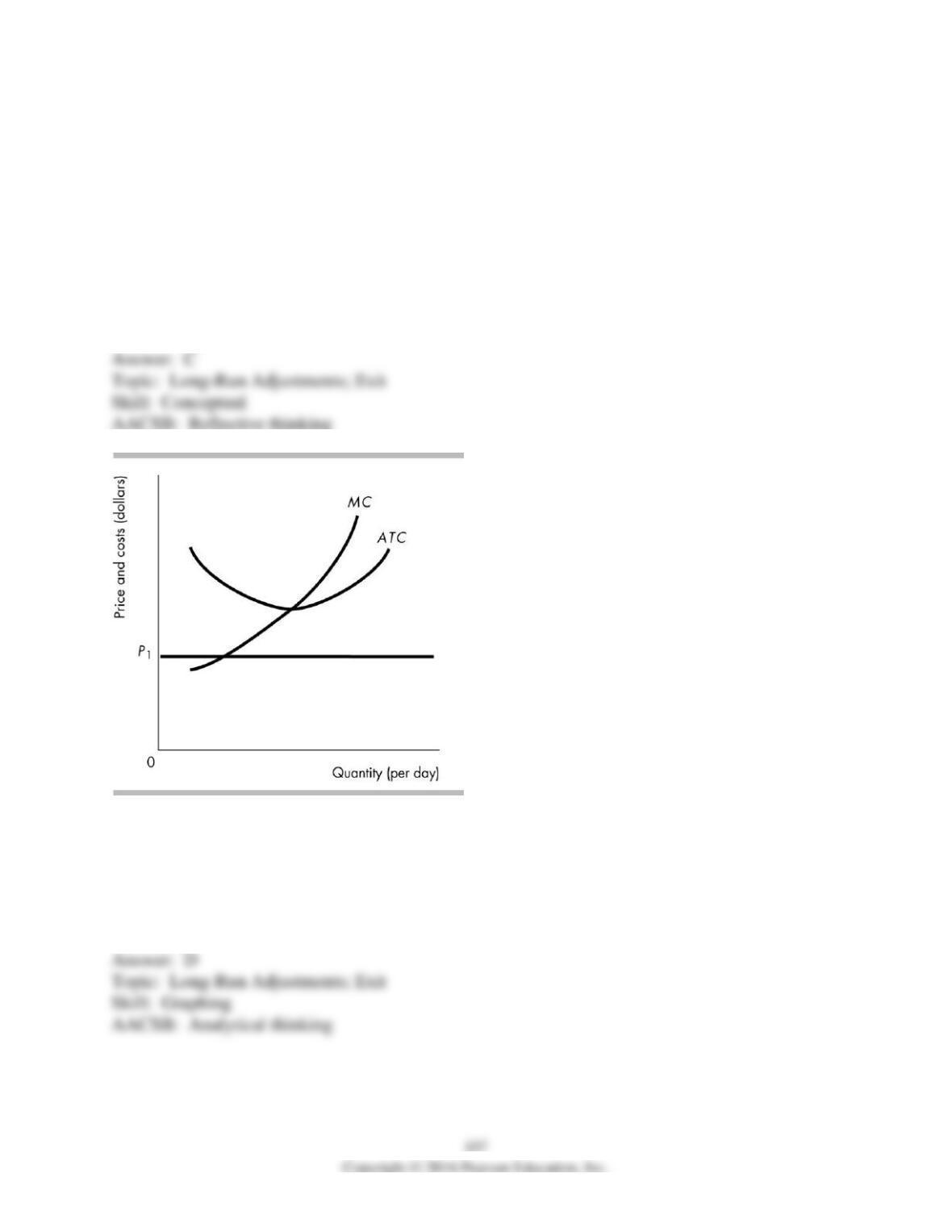

28) Suppose the cost curves in the above figure apply to all firms in the market. Then, if the

initial price is P1, in the long run the market

A) demand will increase.

B) demand will decrease.

C) supply will increase.

D) supply will decrease.

29) Suppose the cost curves in the above figure apply to all firms in the market. If the initial

price is P1, firms are ________ and some firms will ________ the industry.

A) making an economic profit; leave

B) making an economic profit; enter

C) incurring an economic loss; leave

D) incurring an economic loss; enter

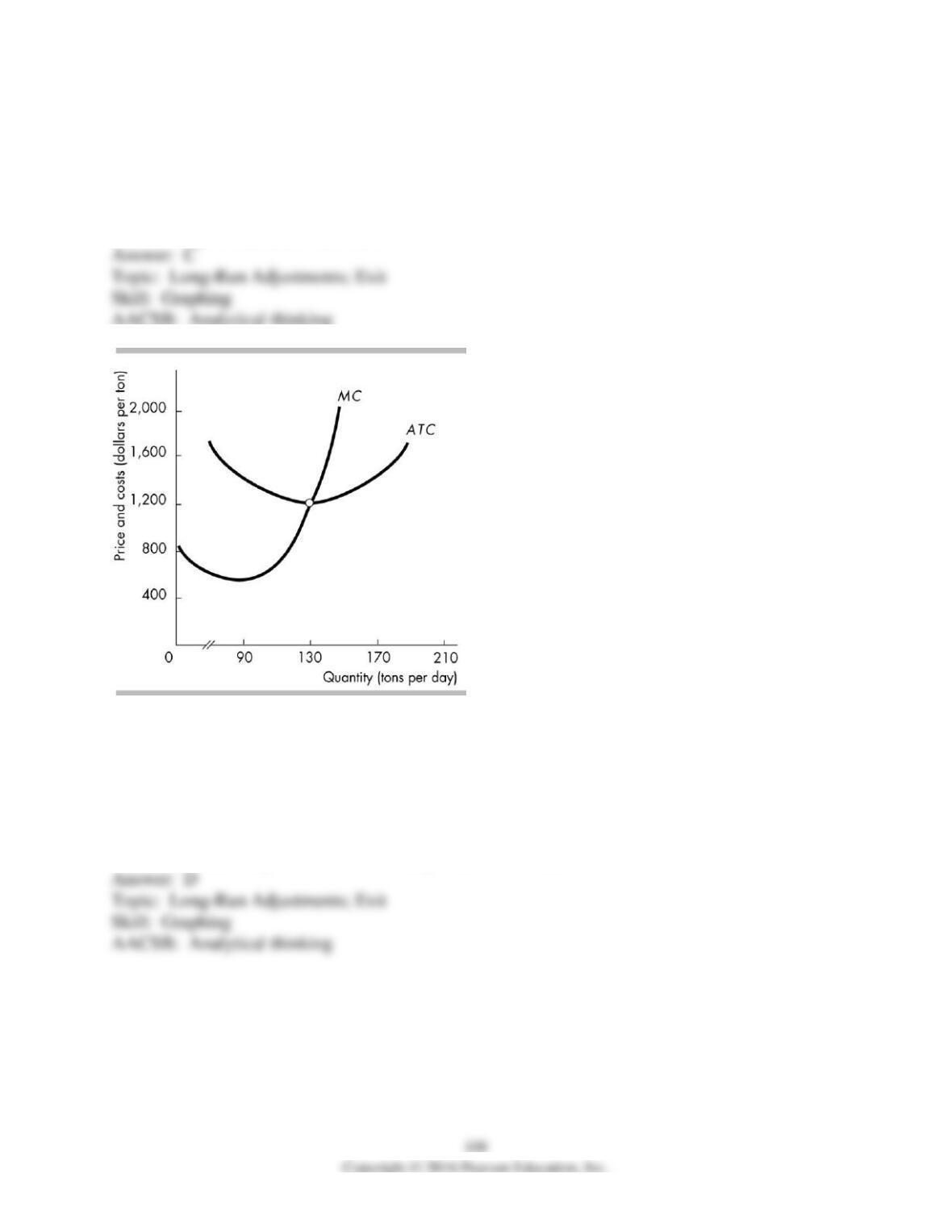

30) The figure above shows the costs for the typical grower in the perfectly competitive turnip

market. Currently, the price is $1,000 for a ton of turnips. In the long run, the market supply of

turnips will ________.

A) decrease and the price of a ton of turnips will fall to $600

B) increase and the turnip grower’s economic profit will increase

C) increase and the turnip grower’s economic profit will decrease

D) decrease and the price of a ton of turnips will rise to $1,200

31) The figure above shows the costs for the typical grower in the perfectly competitive turnip

market. Currently, the price of a ton of turnips is $1,200. The demand for turnips increases

permanently. The turnip industry experiences neither external economies nor external

diseconomies. In the long run, the price of a ton of turnips ________.

A) increases so it is above $1,200

B) is $1,200 and turnip growers will make normal profit

C) decreases so it is below $1,200, and turnip growers will make normal profit

D) decreases so it is below $1,200 and the turnip growers make an economic profit

32) In the long run, fixed costs are

A) zero and variable costs are zero.

B) zero and variable costs are positive.

C) positive and variable costs are zero.

D) positive and variable costs are positive.

33) In the long run, the economic profit of a firm in a perfectly competitive market

A) will be above zero.

B) will be below zero.

C) will equal zero.

D) can be above, below, or equal to zero.

34) In the long run, the firms in a perfectly competitive market

A) maximize their profit.

B) make an economic profit.

C) display price setting behavior.

D) are protected by barriers to entry.

35) In the long run, which of the following is present in a perfectly competitive market?

A) barriers to entry

B) many firms in the market

C) firms incurring an economic loss in the long run

D) firms making an economic profit in the long run

36) In the long-run equilibrium in a perfectly competitive market, the economic profit of the

firms is

A) positive.

B) negative.

C) zero.

D) increasing.

37) In the long-run equilibrium in a perfectly competitive market,

A) the firms make an economic profit.

B) the firms’ owners make a normal profit.

C) the average total cost is maximized.

D) marginal cost is at a minimum.

38) In the short run, perfectly competitive firms ________ but in the long run, perfectly

competitive firms ________.

A) can incur an economic loss; incur an economic loss

B) can incur economic losses; make an economic profit

C) must make an economic profit; make an economic profit

D) can incur an economic loss; make zero economic profit

39) In the long-run equilibrium, perfectly competitive firms make zero economic profit because

of

A) government regulations.

B) the ability of firms to enter and exit.

C) inefficient production processes.

D) high fixed costs.

40) In the long run, perfectly competitive firms make zero economic profit. This result is due

mainly to which of the following assumptions?

A) few buyers and sellers

B) unrestricted entry and exit

C) firms must act as price takers

D) demand for the firm’s output is perfectly elastic

41) Which of the following is NOT present in a perfectly competitive market?

A) profit maximizing firms

B) an economic profit in the long run

C) price taking behavior

D) identical products

42) In the long run, perfectly competitive firms make zero economic profit. This result is due

mainly to the point that a perfectly competitive market has

A) few buyers and sellers.

B) no barriers to entry and exit.

C) price taking by the firms.

D) firms with perfectly elastic market demand.

43) For a perfectly competitive firm, in the long-run equilibrium

A) P = MC = ATC = MR.

B) MR = MC = AFC.

C) MR = P = ATC = AFC.

D) P = MC > ATC.

44) In the long run, perfectly competitive firms earn just enough revenue to

A) pay all fixed costs.

B) pay all accounting costs.

C) pay all opportunity costs.

D) attract entry.

45) If the market for maple syrup is perfectly competitive, then in the long-run equilibrium, firms

are

A) entering the market.

B) exiting the market.

C) making zero economic profit.

D) temporarily shutting down.

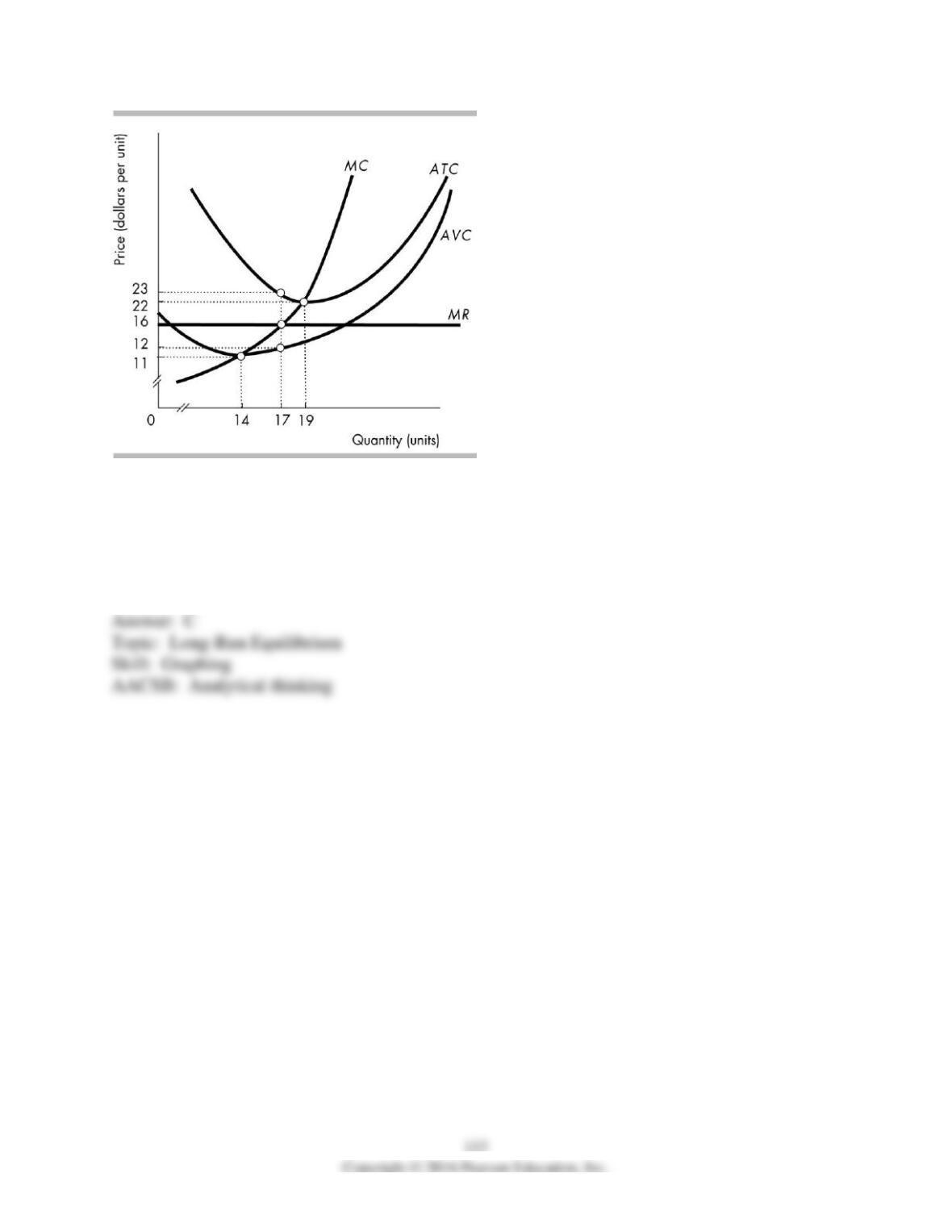

46) Consider the perfectly competitive firm in the above figure. At what price will long-run

equilibrium occur?

A) $11

B) $12

C) $22

D) $23

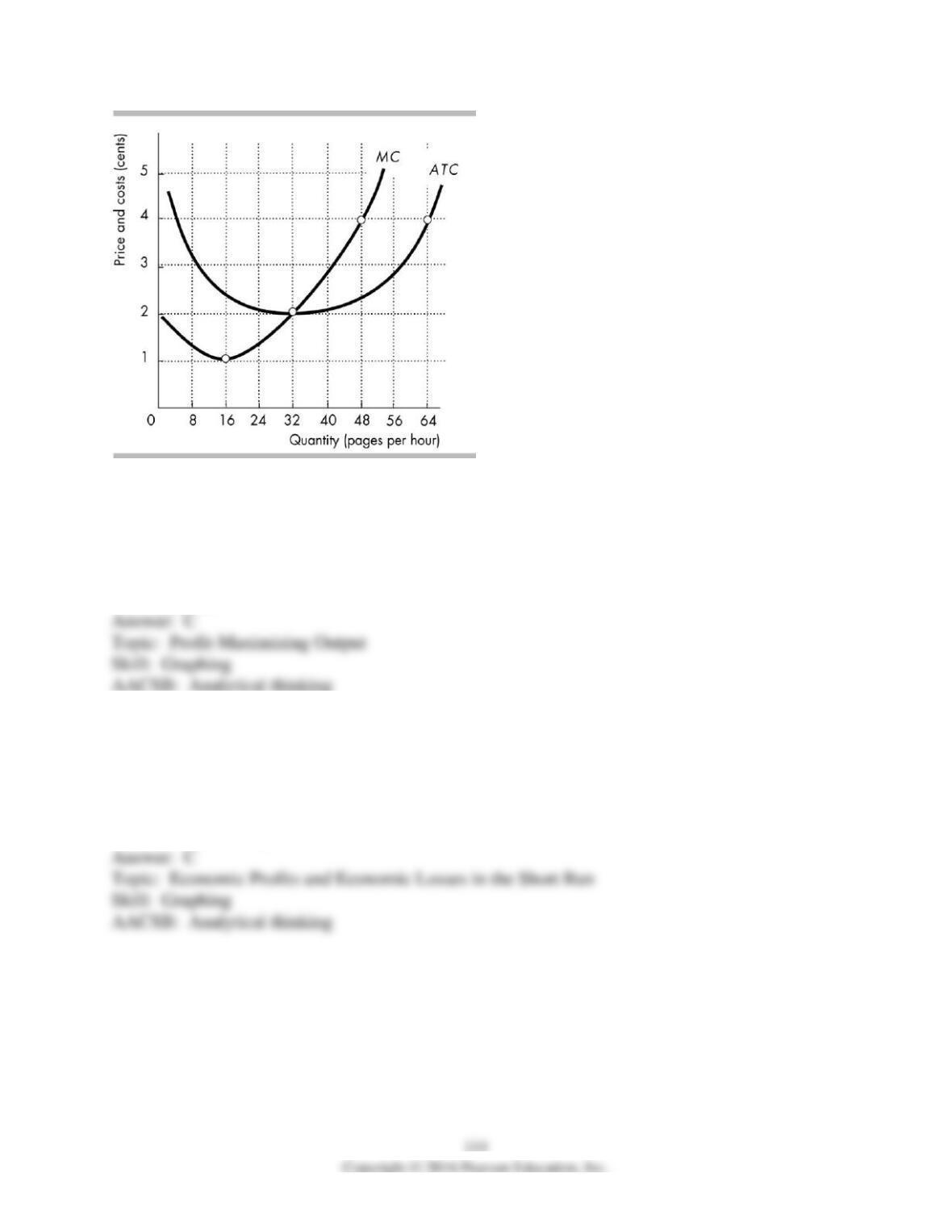

47) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves. If

the market price is 4 cents per page, what is Fast Copy’s profit maximizing level of output?

A) 16 pages per hour

B) 32 pages per hour

C) 48 pages per hour

D) 64 pages per hour

48) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves. If

the market price is 4 cents per page, what is Fast Copy’s economic profit?

A) zero

B) between 0 and $0.50 per hour

C) between $0.51 and $1.00 per hour

D) more than $1.00 per hour

49) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves.

The current market price is 4 cents per page. With no change in demand and technology, in the

long run, the price will

A) remain unchanged.

B) rise to 5 cents per page.

C) fall to 2 cents per page.

D) fall to 1 cent per page.

50) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves. If

the market price is 2 cents per page, what is Fast Copy’s profit maximizing level of output?

A) 16 pages per hour

B) 32 pages per hour

C) 48 pages per hour

D) 64 pages per hour

51) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves. If

the market price is 2 cents per page, what is Fast Copy’s economic profit?

A) zero

B) between 0 and $0.50 per hour

C) between $0.51 and $1.00 per hour

D) more than $1.00 per hour

52) Fast Copy is a perfectly competitive firm. The figure above shows Fast Copy’s cost curves.

The current market price is 2 cents per page. With no change in demand and technology, in the

long run, the price will

A) remain unchanged.

B) rise to 5 cents per page.

C) rise to 4 cents per page.

D) fall to 1 cent per page.

53) Suppose firms in a perfectly competitive market are incurring an economic loss. Over time

A) other firms enter the market, so the price rises and the economic loss decreases.

B) some firms leave the market, so the price rises and the economic loss decreases.

C) other firms enter the market, so the price falls and the economic loss decreases.

D) some firms leave the market, so the price falls and the economic loss decreases.

54) As firms enter a perfectly competitive market, the price

A) falls and the existing firms’ economic profits do not change.

B) rises and the existing firms’ economic profits decrease.

C) falls and the existing firms’ economic profits decrease.

D) falls and the existing firms’ economic losses do not change.

55) In the long run, a perfectly competitive firm can

A) only make an economic profit.

B) only make zero economic profit.

C) only incur an economic loss.

D) make an economic profit, make zero economic profit, or incur an economic loss.

5 Changes in Demand and Supply as Technology Advances

1) If a perfectly competitive market is in long-run equilibrium and there is a permanent decrease

in demand, then

A) some firms will incur economic losses.

B) firms are no longer maximizing profits.

C) some firms must immediately exit.

D) each firm must produce less output in the new long run equilibrium and earn less economic

profit.

2) If there is a permanent decrease in demand in a perfectly competitive market, then there is an

initial ________ in price and existing firms ________.

A) rise; make an economic profit

B) rise; incur an economic loss

C) fall; make an economic profit

D) fall; incur an economic loss

3) Suppose a perfectly competitive market is in a long-run equilibrium when a permanent

decrease in the market demand occurs. In the long run, which of the following definitely occurs?

A) The price decreases.

B) The number of firms decreases.

C) The firms’ marginal cost increases.

D) Marginal revenue increases.

4) A perfectly competitive market is in long-run equilibrium. Then demand decreases. The

decrease in demand leads to

A) a rise in the price in the short run.

B) the firms’ incurring an economic loss in the short run.

C) firms entering the market in the long run.

D) none of the above

5) In a perfectly competitive market, a permanent decrease in demand initially brings a lower

price, economic

A) loss, and entry into the market.

B) loss, and exit from the market.

C) profit, and entry into the market.

D) profit, and exit from the market.

6) In a perfectly competitive market that is in long-run equilibrium, a permanent leftward shift in

the market demand curve

A) raises the price in the short run.

B) raises profits in the short run.

C) leads to new firms entering the market in the long run.

D) lowers the price at first but then raises it as firms leave the market.

7) In a perfectly competitive market that is in long-run equilibrium, a permanent leftward shift in

the market demand curve

A) raises the price in the short run.

B) raises profits in the short run.

C) leads to firms leaving the market in the long run.

D) raises the price at first but then returns it to its original level in the long run.

8) New reports indicate that eating turnips helps people remain healthy. The news shifts the

demand curve for turnips rightward. In response, new farms enter the turnip industry. During the

period in which the new farms are entering, the price of a turnip ________ and the economic

profit of each existing firm ________.

A) rises; rises

B) rises; falls

C) falls; rises

D) falls; falls

9) In a perfectly competitive market that is in long-run equilibrium, a rightward shift in the

market demand curve results in

A) the price falling in the short run.

B) the firms’ economic profits falling in the short run.

C) firms leaving the industry in the long run.

D) none of the events listed above.

10) Suppose a perfectly competitive market is in long-run equilibrium. If there is a permanent

increase in demand,

A) at least in the short run, some firms will increase their output.

B) at least in the short run, the price will increase initially.

C) new firms will enter the market.

D) All of the above answers are correct.

11) The market for maple syrup is perfectly competitive. Suppose that the market is in long-run

equilibrium when the market demand for maple syrup increases. What happens in the short run?

A) Firms will enter the market.

B) Some of the existing firms shut down.

C) The firms decrease production.

D) The firms increase production.

12) The market for maple syrup is perfectly competitive. Suppose that the market is in long-run

equilibrium when the market demand for maple syrup increases. After the demand increases, a

typical firm will

A) make zero economic profit.

B) make an economic profit.

C) incur an economic loss.

D) exit the market.

13) The market for maple syrup is perfectly competitive. Suppose that the market is in long-run

equilibrium when the market demand for maple syrup increases. In the long run, firms will

________ the market and the market ________ will ________.

A) leave; supply; decrease

B) enter; supply; increase

C) leave; demand; decrease

D) enter; supply; decrease

14) In a perfectly competitive market, a permanent increase in demand initially brings a higher

price, economic

A) loss, and entry into the market.

B) loss, and exit from the market.

C) profit, and entry into the market.

D) profit, and exit from the market.

15) In a perfectly competitive market that is in long-run equilibrium, which of the following will

NOT occur?

A) Firms make only zero economic profit.

B) Firms’ owners earn a normal profit.

C) The price equals the minimum average total cost.

D) Entrepreneurs want to enter this industry.

16) In the long run, perfectly competitive firms make zero economic profit (their owners earn a

normal profit) because

A) any economic profit would attract newcomers to the industry.

B) the firms are incompetent.

C) any economic loss would increase the demand for the good, thereby raising its price.

D) there are many buyers and sellers.

17) When a perfectly competitive market is in its long-run equilibrium, the fact that the firms

make zero economic profit will

A) encourage new firms to enter the market.

B) cause existing firms to shut down.

C) cause existing firms to leave the market.

D) mean that the firms’ owners earn a normal return.