14) In the short run, an increase in demand for a good that is sold in a perfectly competitive

market

A) increases the number of firms in the market.

B) increases the economic profits of existing firms in the market.

C) has no effect on the price.

D) causes more firms to shut down.

15) Which of the following statements is TRUE?

A) The presence of positive economic profit in a perfectly competitive market is consistent with

the characteristics of a long-run competitive equilibrium.

B) When firms in a perfectly competitive market incur economic losses, some will exit in the

long run, thereby shifting the industry supply curve rightward.

C) If a profit-maximizing firm in a perfectly competitive market is making an economic profit,

then it must be producing at a level of output where price is greater than average total cost.

D) If a profit-maximizing firm in a perfectly competitive market is incurring an economic loss,

then it must be producing at a level of output where price is greater than average total cost.

Quantity

(tattoos per

hour)

Total cost, TC

(dollars per

hour)

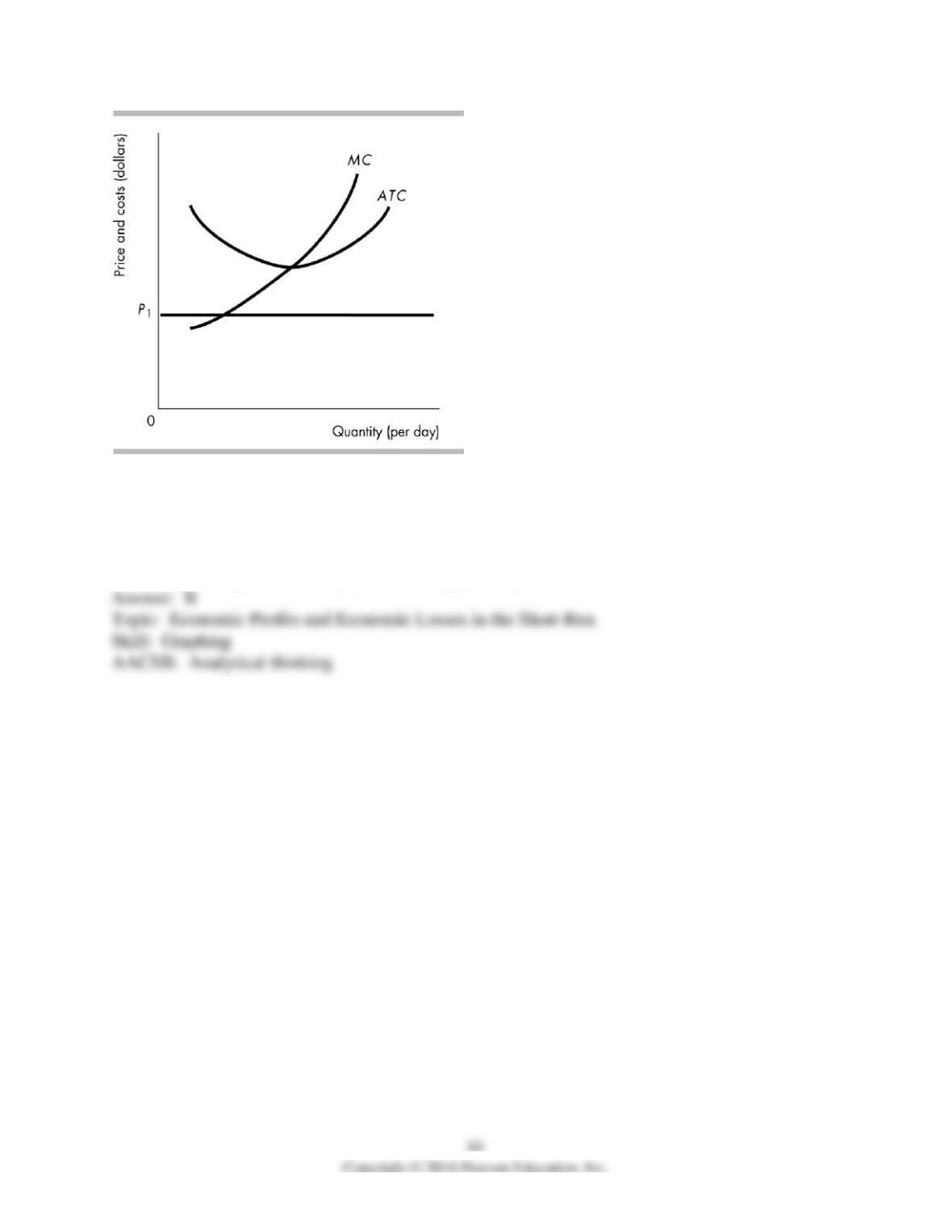

0

10

1

25

2

35

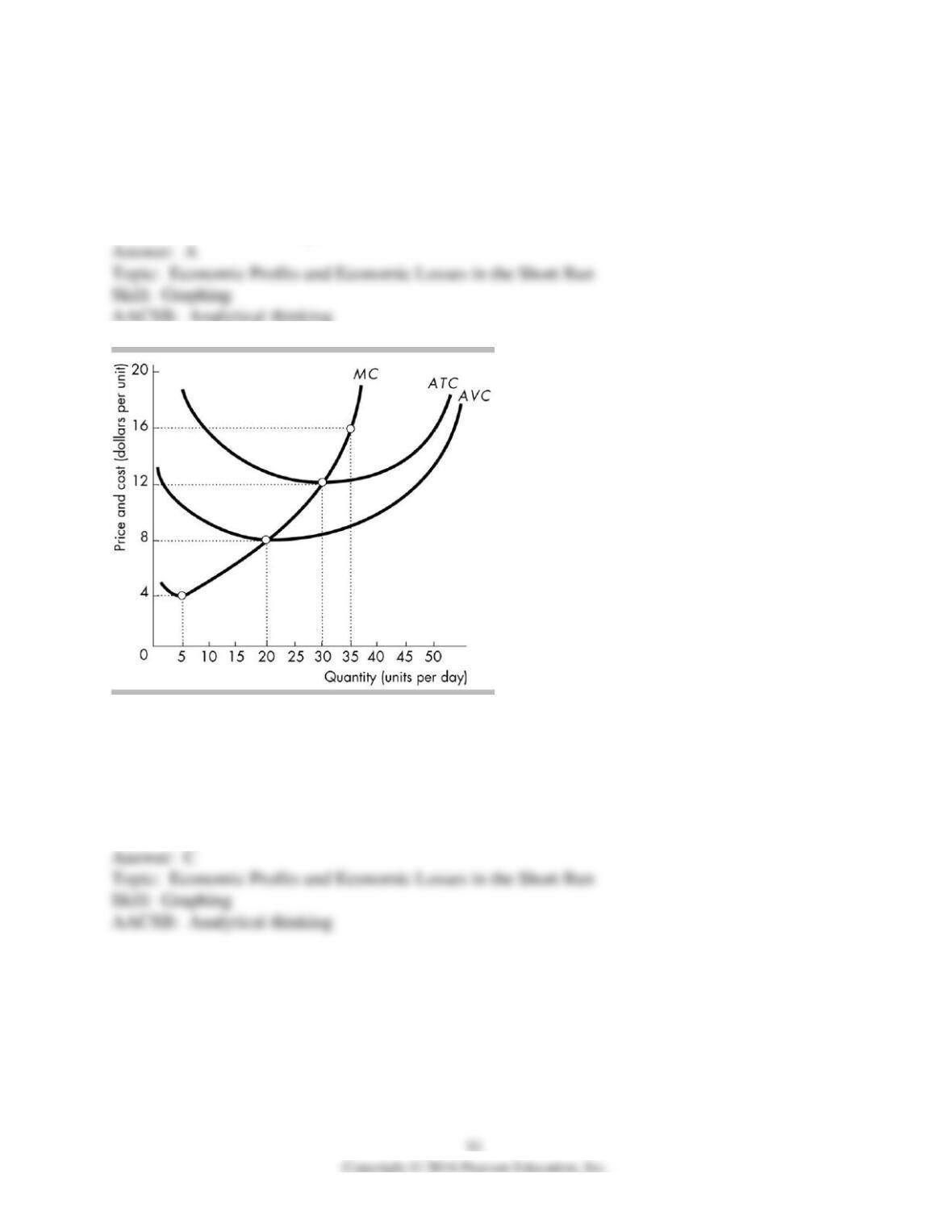

3

50

4

70

5

95

6

125

16) Archibald’s Tattoos is a perfectly competitive firm. The firm’s costs are shown in the table

above. If the market price of a tattoo is $17.50, what is the firm’s economic profit?

A) zero

B) $2.50 per hour

C) $12.50 per hour

D) -$10.00 per hour

Quantity

(gloves per day)

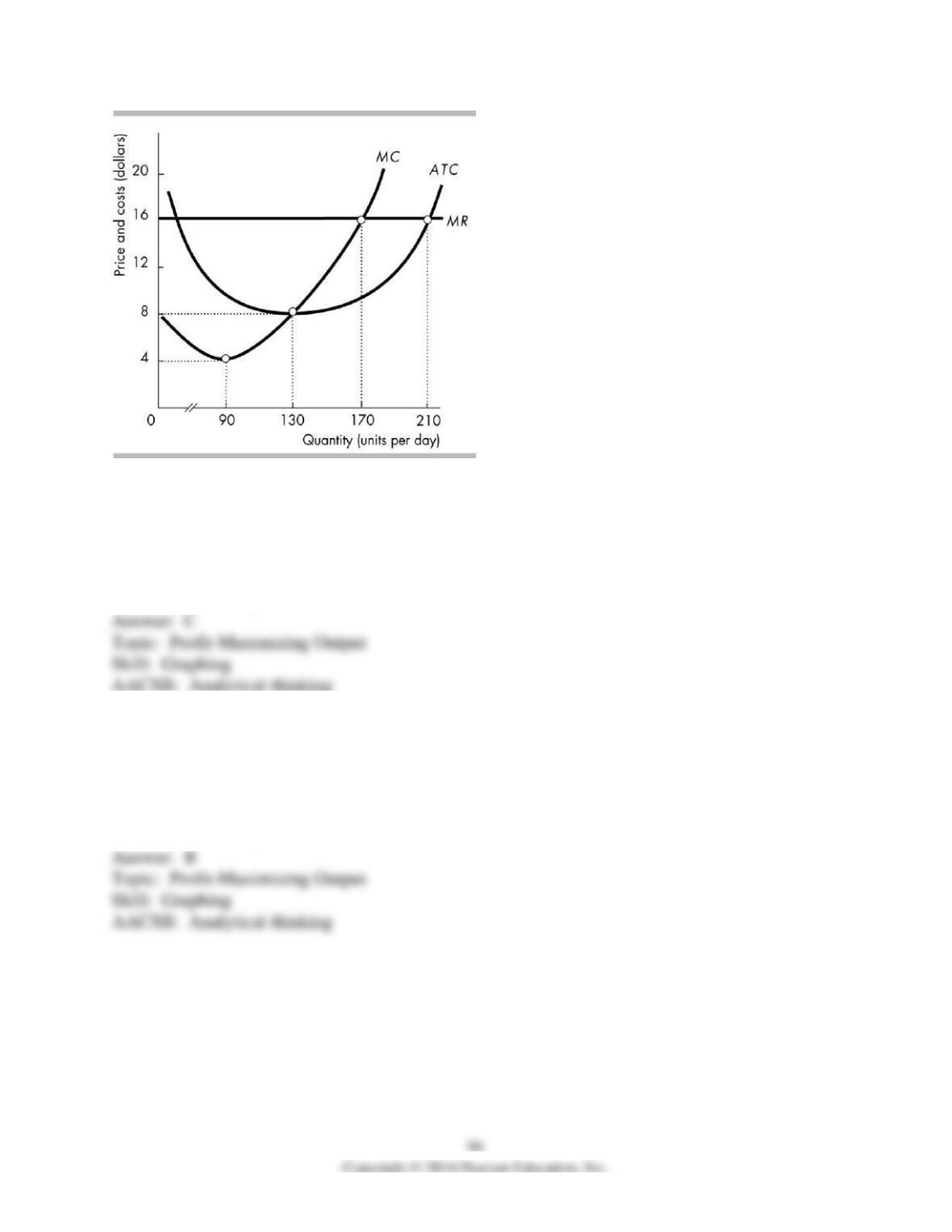

Total cost

(dollars)

0

80

1

100

2

105

3

135

4

170

5

210

6

270

7

350

8

450

17) The above table shows the per day total cost for Kiley’s Baseball Glove Company. Each

glove is priced at $50 and Kiley’s Baseball Glove Company is a perfectly competitive firm. At

which of the following amounts of output is the economic profit maximized for Kiley’s Baseball

Glove Company?

A) 0

B) 2

C) 5

D) 8

18) The above table shows the per day total cost for Kiley’s Baseball Glove Company. Each

glove is priced at $50 and Kiley’s Baseball Glove Company is a perfectly competitive firm.

Between which two amounts of output does Kiley’s Baseball Glove Company make an economic

profit?

A) 0 and 8

B) 1 and 8

C) 2 and 7

D) 3 and 6

Quantity

(pizzas per

hour)

Total cost, TC

(dollars per

hour)

0

10

1

18

2

30

3

48

4

70

5

98

6

120

19) Giuseppe’s Pizza is a perfectly competitive firm. The firm’s costs are shown in the table

above. If the market price is $15, how much economic profit does the firm make?

A) $0

B) $30

C) -$10

D) -$15

20) Giuseppe’s Pizza is a perfectly competitive firm. The firm’s costs are shown in the table

above. If the market price is $20, how much economic profit does the firm make?

A) $0

B) $12

C) -$20

D) -$10

21) In the above figure, if the price is P1, the firm is

A) making an economic profit.

B) incurring an economic loss.

C) making zero economic profit.

D) earning enough revenue to pay all of its opportunity costs.

22) If the price is $12 per pizza, the perfectly competitive firm in the above figure is

A) making an economic profit.

B) making zero economic profit.

C) incurring an economic loss.

D) More information about the firm’s total cost is needed to determine if the firm has a positive

economic profit, zero economic profit, or an economic loss.

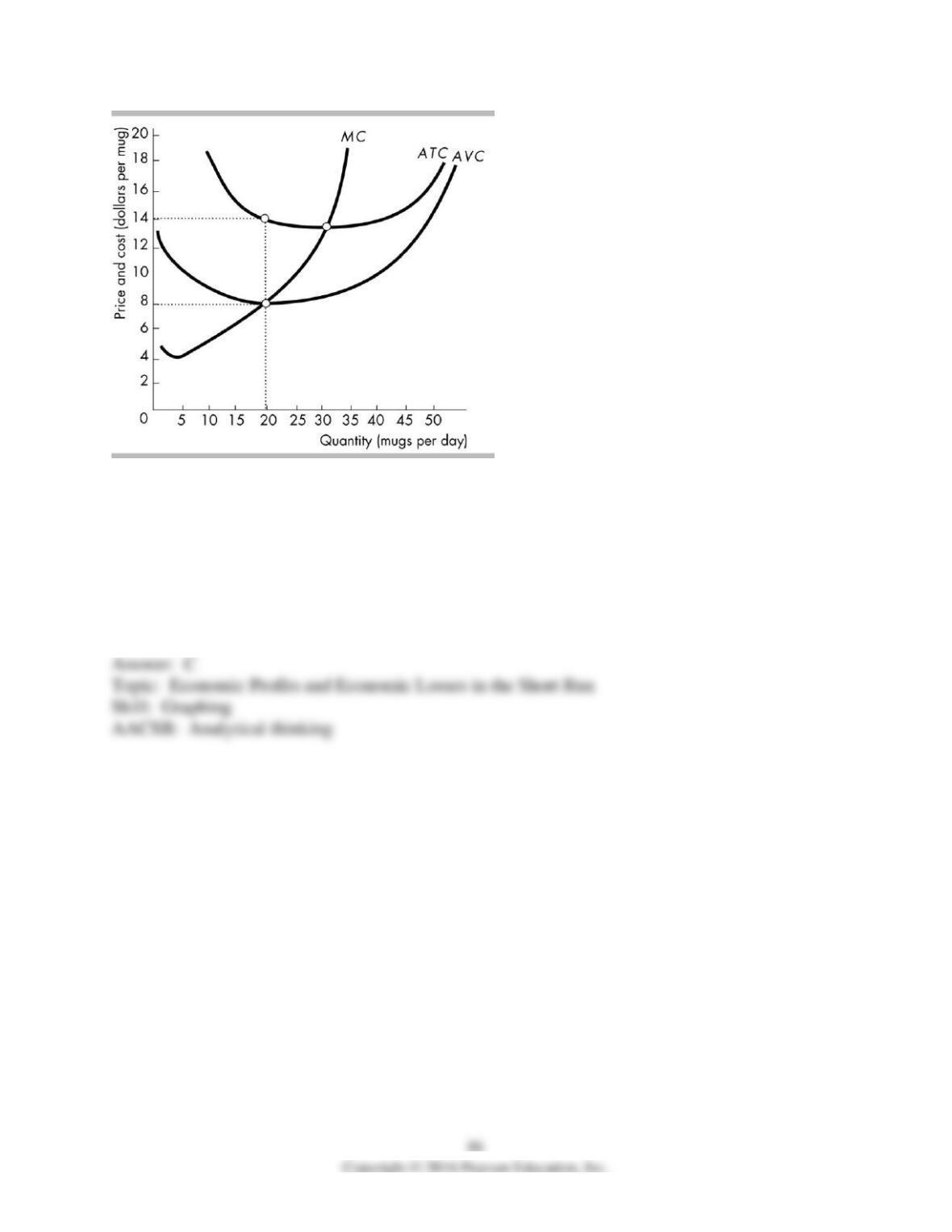

23) The figure above shows Mollie’s Mugs’ costs of producing mugs. The mug market is

perfectly competitive. If the market price of a mug falls to $5 and Mollie’s shuts down

temporarily, its total variable cost is ________ an hour and it incurs an economic loss of

________ an hour.

A) $160; $280

B) $8; $14

C) $0; $120

D) $0; $6

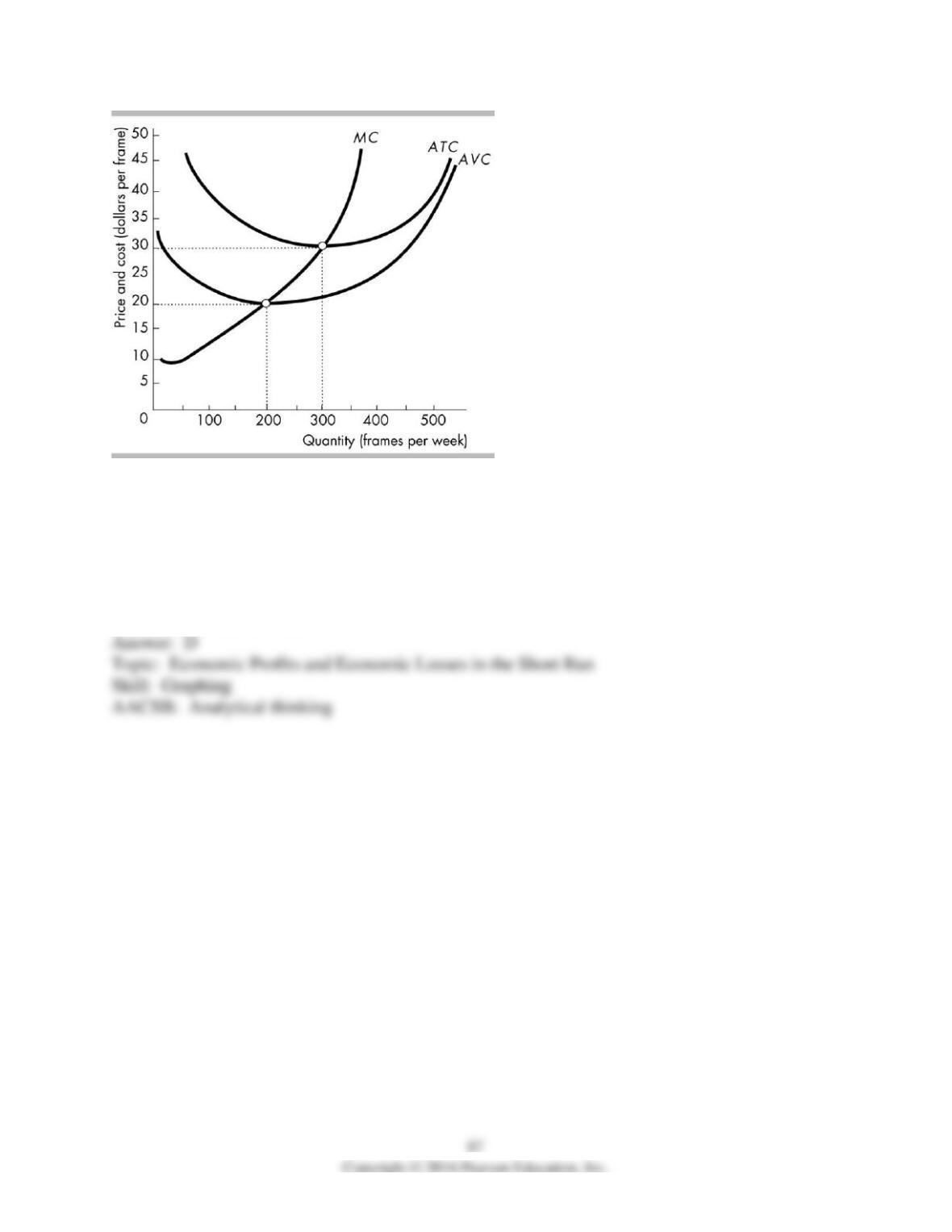

24) The figure illustrates the short-run costs of Paul’s Picture Frames Inc. The picture frame

market is perfectly competitive and the market price is $30 a frame. Paul produces ________

frames each week, makes ________ of total revenue, and makes zero ________ profit.

A) 200; $4,000; economic

B) 300; $9,000; normal

C) 200; $4,000; normal

D) 300; $9,000; economic

25) The figure above shows a perfectly competitive firm. The firm is operating; that is, the firm

has not shut down. The firm is

A) making an economic profit of $200.

B) incurring a economic loss of $200.

C) incurring an economic loss of $600.

D) making zero economic profit.

26) The figure above shows a perfectly competitive firm. The firm is operating; that is, it has not

shut down. The firm produces

A) 20 units of output and makes zero economic profit.

B) 20 units of output and incurs an economic loss.

C) 10 units of output and makes zero economic profit.

D) 10 units of output and incurs an economic loss.

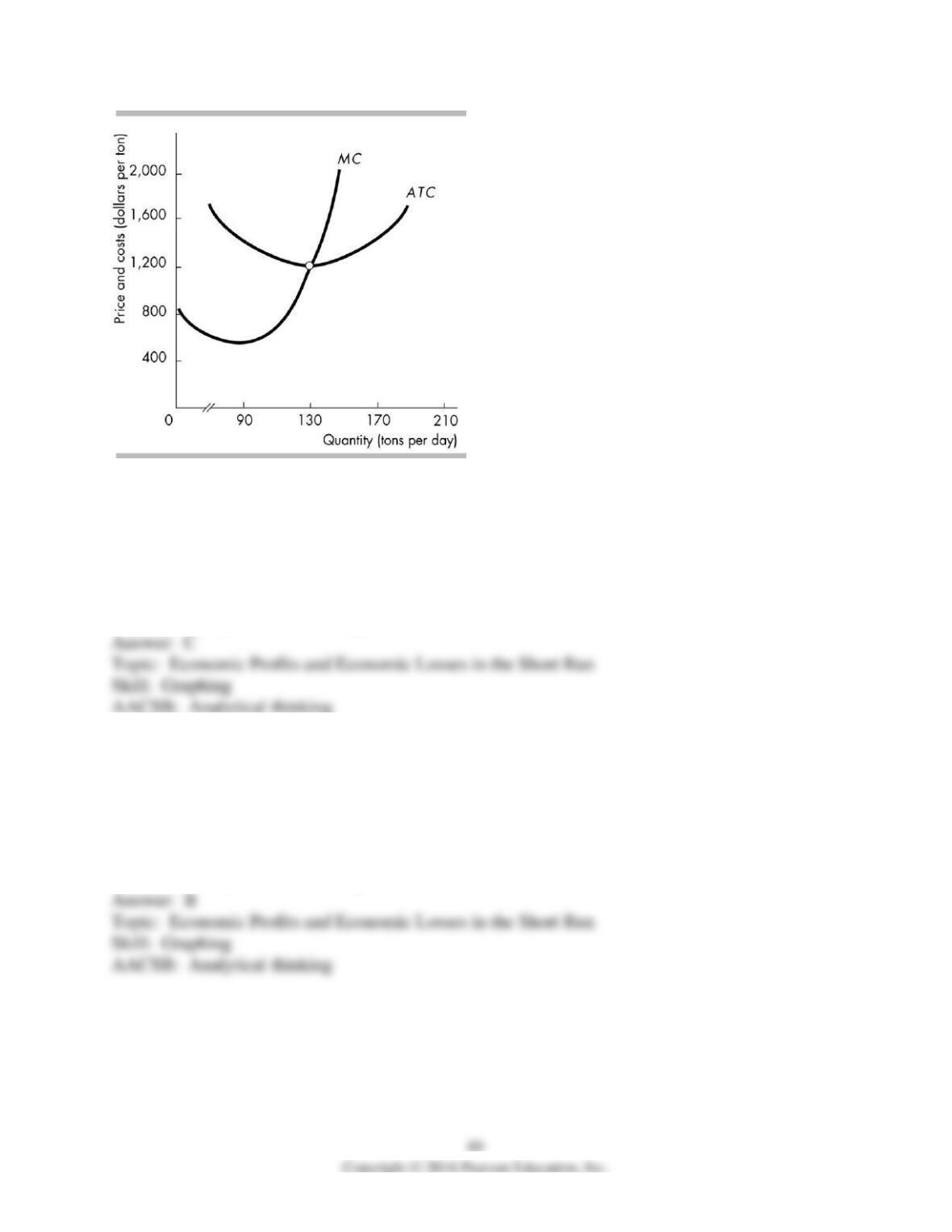

27) The figure above shows the costs for a grower in the perfectly competitive turnip market. If

the price is $1,000 for a ton of turnips, the firm is

A) making an economic profit.

B) making zero economic profit.

C) incurring an economic loss.

D) More information is needed to determine if the firm is making a positive economic profit,

zero economic profit, or incurring an economic loss.

28) The figure above shows the costs for a grower in the perfectly competitive turnip market. If

the price is $1,200 for a ton of turnips, the firm is

A) making an economic profit.

B) making zero economic profit.

C) incurring an economic loss.

D) More information is needed to determine if the firm is making a positive economic profit,

zero economic profit, or incurring an economic loss.

29) The figure above shows the costs for a grower in the perfectly competitive turnip industry. If

the price is $1,400 for a ton of turnips, the firm is

A) making an economic profit.

B) making zero economic profit.

C) incurring an economic loss.

D) More information is needed to determine if the firm is making a positive economic profit,

zero economic profit, or incurring an economic loss.

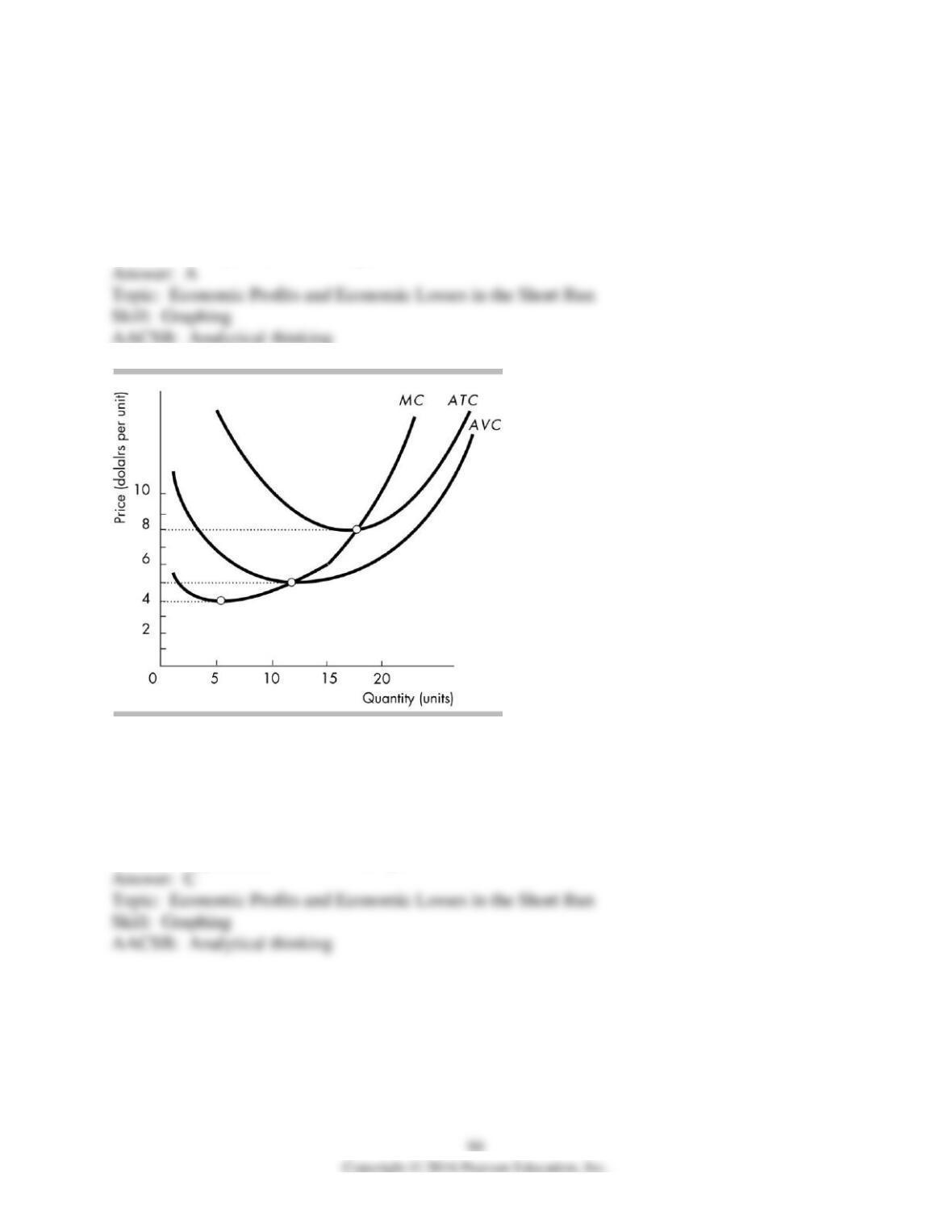

30) In the above figure, at a price of $8, a perfectly competitive firm produces ________ and it

________.

A) 0; incurs an economic loss

B) 0; makes zero economic profit

C) some output; makes zero economic profit

D) some output; makes an economic profit

31) In the above figure, at a price of $6, a perfectly competitive firm produces ________ and it

________.

A) some output; incurs an economic loss

B) 0; incurs an economic loss

C) 0; does not incur an economic loss or make an economic profit

D) 0; makes an economic profit

32) In the above figure, at what price does a perfectly competitive firm make zero economic

profit?

A) $4 per unit

B) $8 per unit

C) $12 per unit

D) $16 per unit

33) In the above figure, if the price is $16 per unit, a profit maximizing perfectly competitive

firm will

A) shut down.

B) incur an economic loss but continue to operate.

C) make zero economic profit.

D) make an economic profit.

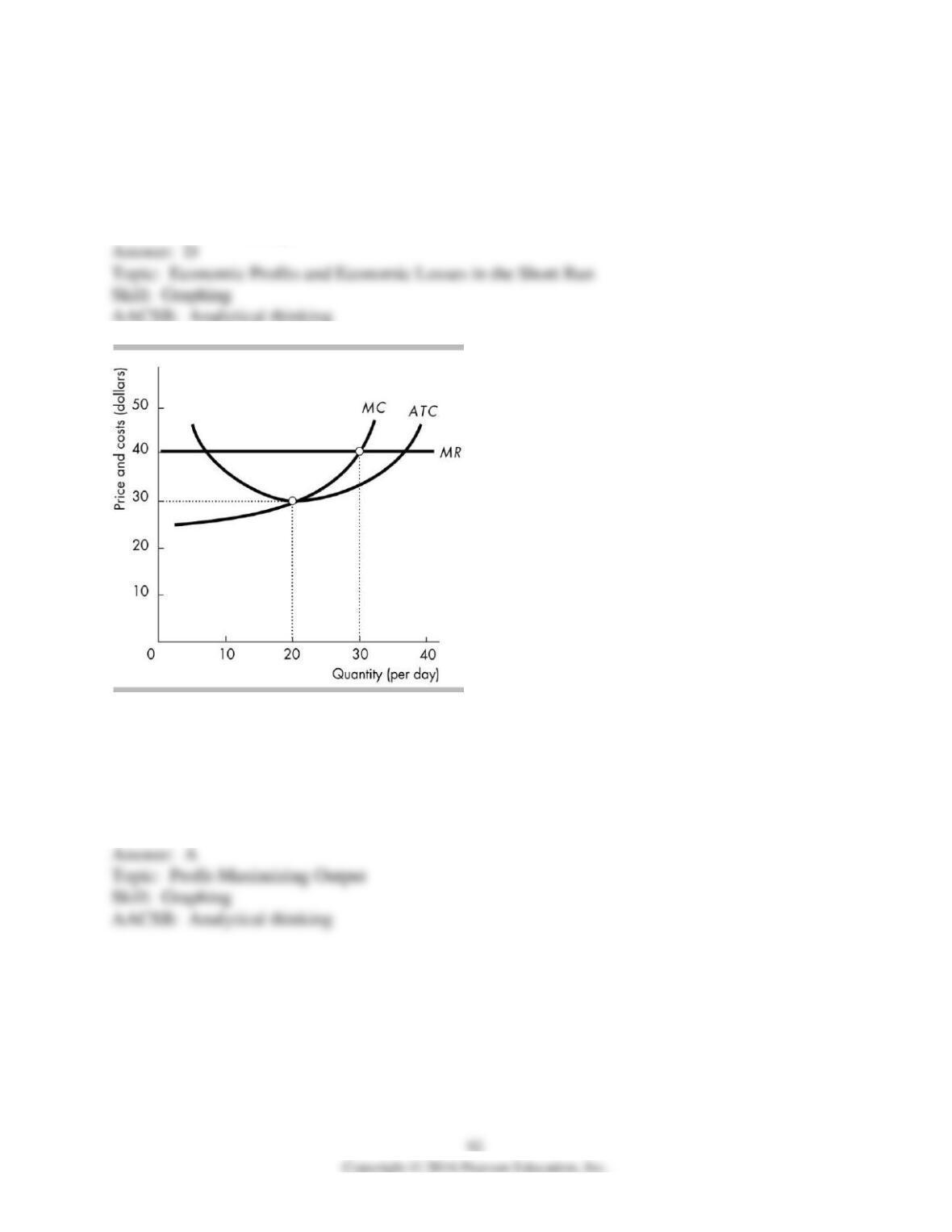

34) The figure above shows a perfectly competitive firm. To maximize its profit, the firm will

produce ________ units of output and the price will be ________ for a unit.

A) 30; $40

B) 30; $30

C) 20; $40

D) 20; $30

35) The figure above shows a perfectly competitive firm. When the firm maximizes its profit, its

total revenue is

A) $1,200.

B) $900.

C) $600.

D) unable to be determined without more information.

36) The figure above shows a perfectly competitive firm. When the firm maximizes its profit, its

total cost is

A) $1,200.

B) less than $1,200 but more than zero.

C) more than $1,200.

D) zero.

37) The figure above shows a perfectly competitive firm. When the firm maximizes its profit, its

economic profit

A) is more than $300.

B) is $300.

C) is less than $300.

D) The premise of the question is wrong because the firm is incurring an economic loss.

38) The figure above shows a perfectly competitive firm. The figure shows a firm

A) in the short run.

B) in the long run.

C) at its shutdown point.

D) Both answers A and C are correct.

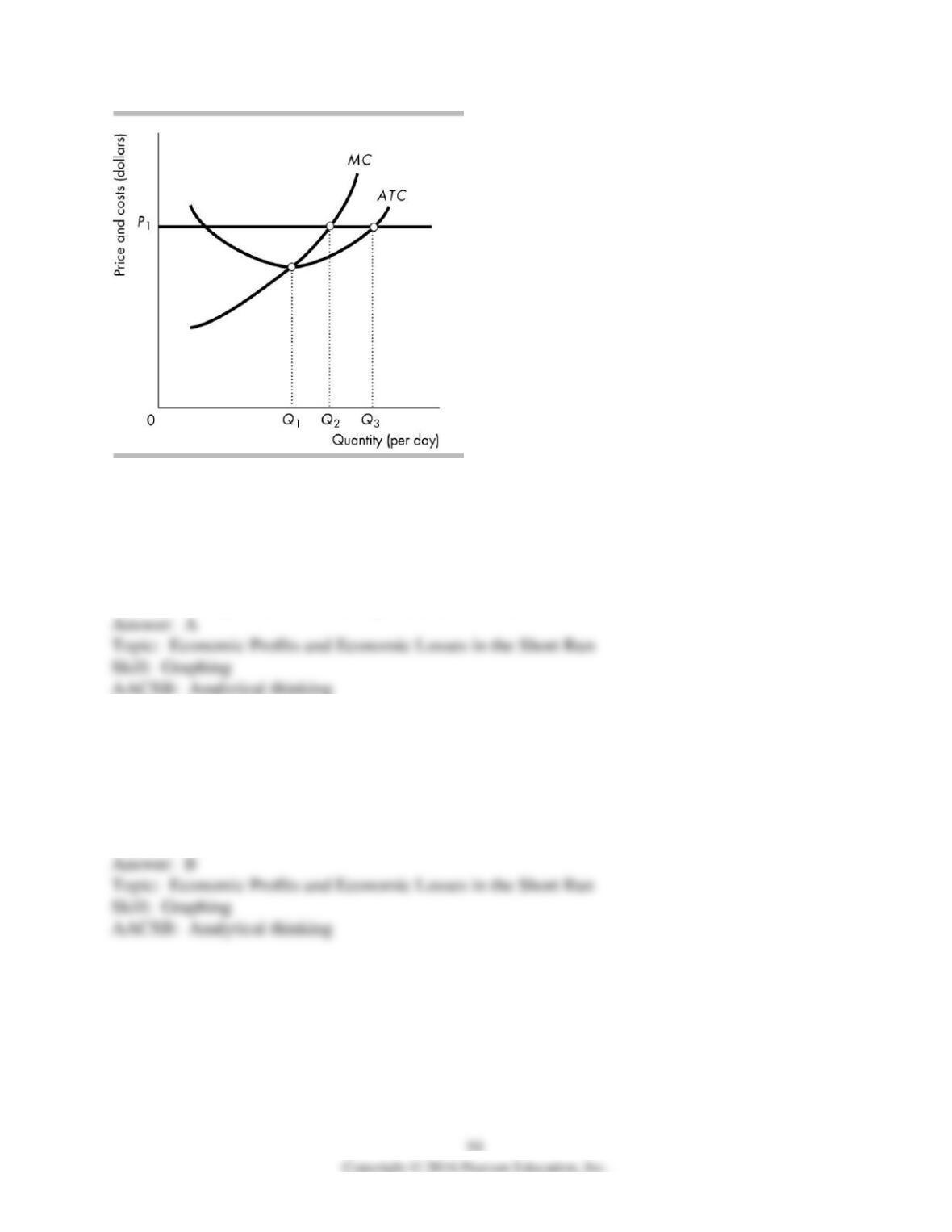

39) In the above figure, if the price is P1 and the firm produces Q2, it is

A) making an economic profit.

B) incurring an economic loss.

C) breaking even.

D) More information is needed to determine if the firm is earning a positive economic profit,

zero economic profit, or is incurring an economic loss.

40) In the above figure, if the price is P1 and the firm produced Q1, the firm’s economic profit is

________ than if it produced Q2 and ________ than if it produced Q3.

A) less; less

B) less; more

C) more; less

D) more; more

41) In the above figure, if the price is P1 and the firm produced Q3, the firm’s economic profit is

________ than if it produced Q1 and ________ than if it produced Q2.

A) less; less

B) less; more

C) more; less

D) more; more

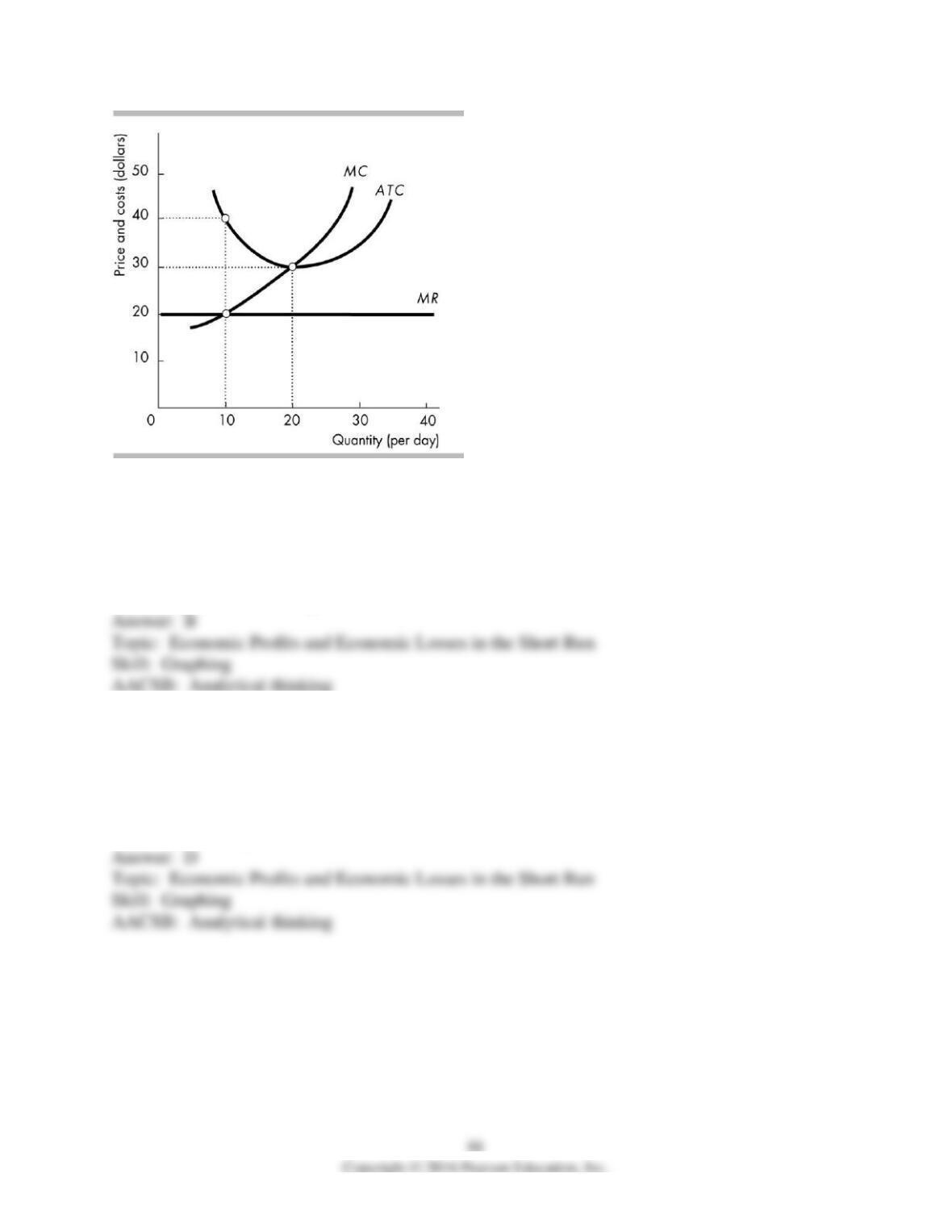

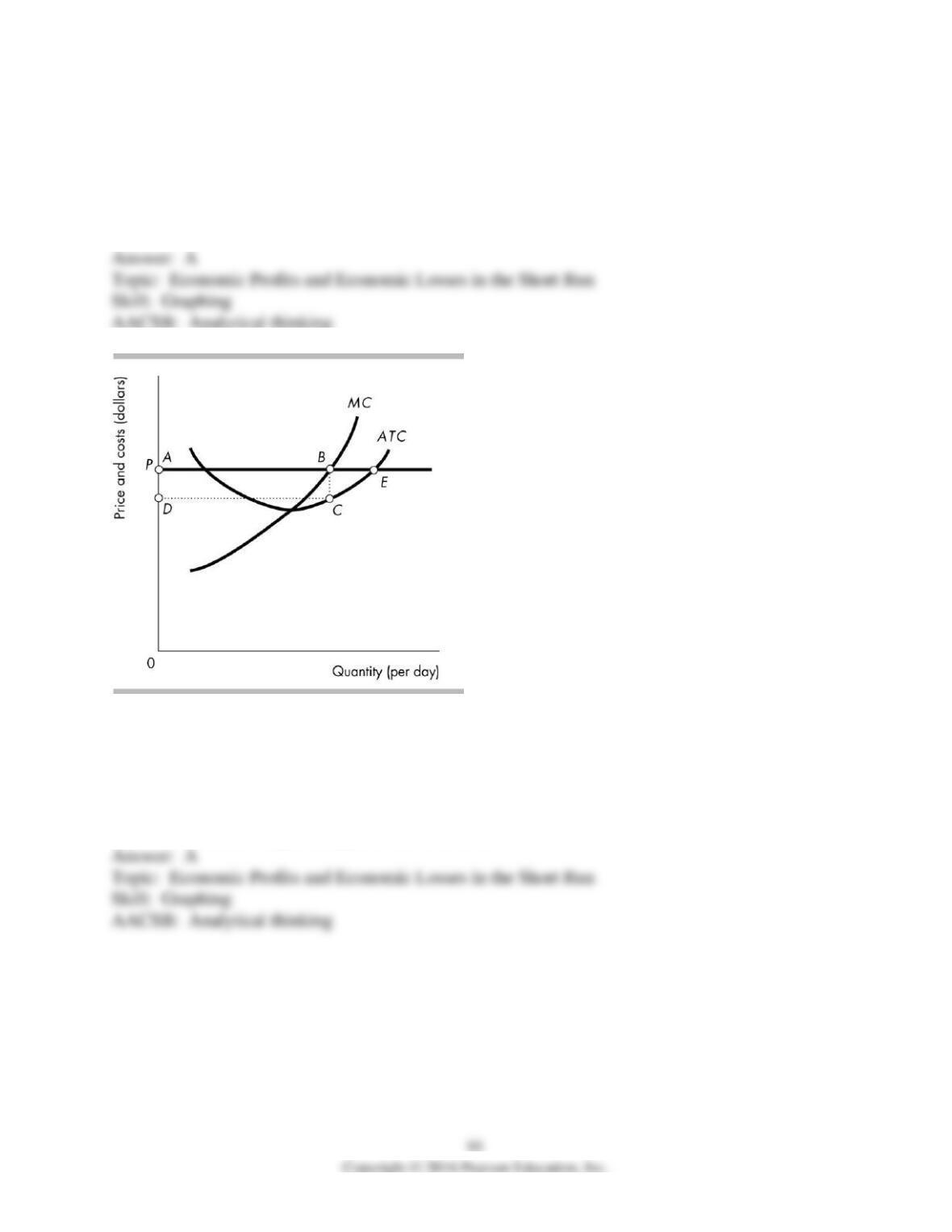

42) Consider the perfectly competitive firm in the figure above. At the profit maximizing level of

output, the firm will

A) make an economic profit equal to the area ABCD.

B) incur an economic loss equal to the area ABCD.

C) make zero economic profit.

D) make an economic profit equal to the area AECD.

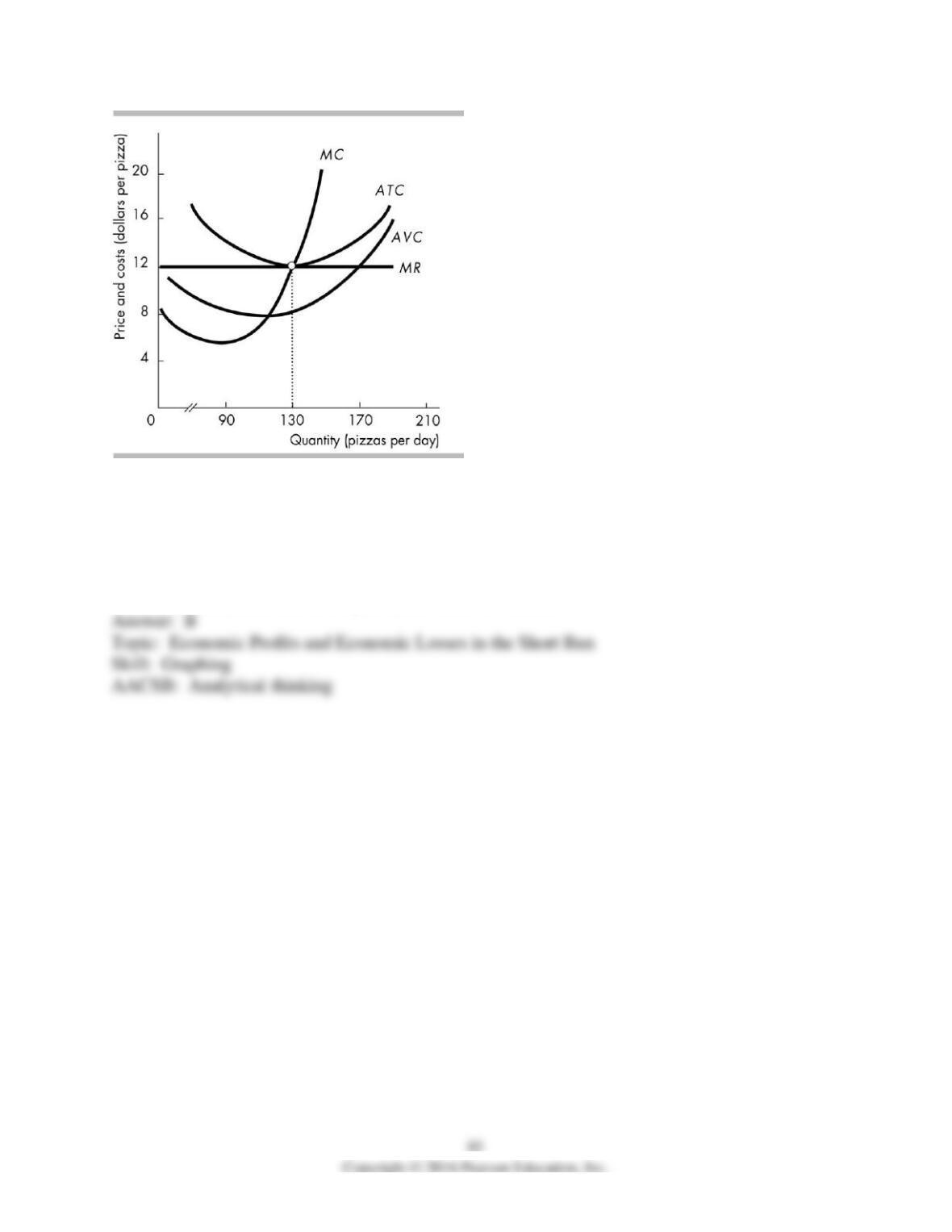

43) The figure above shows the marginal revenue and costs of a perfectly competitive firm. The

firm’s profit is maximized when the firm produces

A) 90 units of output.

B) 130 units of output.

C) 170 units of output.

D) 210 units of output.

44) The figure above shows the marginal revenue and costs of a perfectly competitive firm.

When the firm produces 170 units

A) marginal cost is less than marginal revenue.

B) marginal revenue equals marginal cost.

C) total revenue is less than total cost.

D) total revenue equals total cost.

45) The figure above shows the marginal revenue and costs of a perfectly competitive firm. The

marginal cost of the last unit produced is

A) $4 per unit.

B) $8 per unit.

C) $16 per unit.

D) None of the above answers is correct.

46) The figure above shows depicts the marginal revenue and costs of a perfectly competitive

firm. The price the firm charges is

A) $4 per unit.

B) $8 per unit.

C) $16 per unit.

D) None of the above answers is correct.

47) The figure above shows the marginal revenue and costs of a perfectly competitive firm.

When 170 units are produced, the

A) firm has total revenue of $2,720.

B) firm’s total costs are less than $2,720.

C) firm is making an economic profit.

D) All of the above are true.

48) The figure above shows depicts the marginal revenue and costs of a perfectly competitive

firm. When 170 units are produced, the firm

A) would definitely shut down.

B) would incur an economic loss.

C) would increase its price.

D) has total costs less than $2,720.

49) The short-run market supply curve is

A) the sum of the quantities supplied by all the firms.

B) undefined because the number of firms is constant in the short run.

C) vertical at the total level of output being produced by all firms.

D) horizontal at the current market price.

50) In the short run, a perfectly competitive firm can

A) only make an economic profit.

B) only make zero economic profit.

C) only incur an economic loss.

D) make an economic profit, zero economic profit, or incur an economic loss.

51) A perfectly competitive firm is definitely making an economic profit when

A) MR = MC.

B) P = ATC.

C) P < ATC.

D) P > ATC.

4 Output, Price, and Profit in the Long Run

1) If firms in a perfectly competitive industry are making zero economic profit, then

A) some of those firms will leave the industry, because firms cannot persistently go without

making economic profit.

B) new firms will enter the industry, because the new entrants would be ensured of doing as well

as in their best foregone alternative.

C) there is no incentive for either entry or exit.

D) some of the firms will temporarily shut down.

2) Today, firms in a perfectly competitive market are making an economic profit. In the long run,

firms will ________ the market until all firms in the market are ________.

A) exit; covering only their total fixed costs

B) enter; making zero economic profit

C) exit; producing at the minimum point on their long-run average cost curve

D) enter; making zero normal profit

3) Which of the following statements regarding the long-term equilibrium is TRUE?

A) As new firms enter a market, each existing firm increases the quantity it produces.

B) Firms leave a market if they are making zero economic profit.

C) Entry and exit stop when firms are making an economic profit.

D) Entry and exit stop when firms make zero economic profit.

4) The firms in a perfectly competitive are making an economic profit when new firms enter.

The entry shifts the short-run market supply curve ________, the market price ________, and

each firm’s economic profit ________.

A) leftward; rises; decreases

B) rightward; rises; increases

C) rightward; falls; decreases

D) leftward; falls; decreases

5) Suppose firms in a perfectly competitive industry are making economic profits. As a result

I. new firms enter the industry.

II. the market price falls.

III. the economic profits of the existing firms decrease.

A) I, II and III

B) I and II

C) II and III

D) I and III

6) Economic profit sends a signal to entrepreneurs by telling them where

A) price exceeds marginal cost.

B) there are many buyers and many sellers.

C) the shutdown point is.

D) an above normal return on investment can be earned.

7) In the long run, for a perfectly competitive market, if economic profit is

A) less than zero, then some firms will exit the market and the market supply curve will shift

leftward.

B) greater than zero, then some firms will enter the market and the market supply curve will shift

rightward.

C) equal to zero, then there is no entry or exit of firms into or out of the market.

D) All of the above answers are correct.

8) Entry in a perfectly competitive market

A) shifts the market supply curve rightward.

B) decreases the market price.

C) shifts the market supply curve leftward.

D) Both answers A and B are correct.

9) Suppose firms in a perfectly competitive market are earning an economic profit. As new firms

enter, the price ________ and the economic profit of each existing firm ________.

A) rises; increases

B) rises; decreases

C) falls; increases

D) falls; decreases