116) Consider the perfectly competitive firm in the above figure. At the profit maximizing level

of output, the firm is

A) incurring an economic loss equal to $119.00.

B) incurring an economic loss equal to $123.50.

C) incurring an economic loss equal to $187.00.

D) making zero economic profit.

117) Consider the perfectly competitive firm in the above figure. The shutdown point occurs at a

price of

A) $11.00.

B) $12.00.

C) $16.00.

D) $22.00.

118) Consider the perfectly competitive firm in the above figure. What will the firm choose to do

in the short-run and why?

A) shut down because the firm incurs an economic loss

B) stay in business because the firm is making an economic profit

C) stay in business because the firm’s economic loss is less than fixed costs

D) stay in business because it is making zero economic profit

119) A perfectly competitive firm’s short-run supply curve is the same as its

A) ATC curve.

B) MR curve.

C) AVC curve.

D) MC curve above the minimum of the AVC curve.

120) The short-run supply curve for a perfectly competitive firm is its

A) marginal cost curve above the horizontal axis.

B) marginal cost curve above its shutdown point.

C) average cost curve above the horizontal axis.

D) average cost curve above its shutdown point.

121) The short-run supply curve for a perfectly competitive firm is its marginal cost curve

A) above the horizontal axis.

B) above its shutdown point.

C) below its shutdown point.

D) everywhere.

122) The short-run supply curve for a perfectly competitive firm is its marginal cost curve above

the minimum point on the

A) average fixed cost curve.

B) average variable cost curve.

C) average total cost curve.

D) demand curve.

123) The firm’s supply curve is its

A) marginal cost curve, at all points above the minimum average variable cost curve.

B) marginal cost curve, at all points above the minimum average fixed cost curve.

C) marginal cost curve, at all points above the minimum average total cost curve.

D) marginal revenue curve, at all points above the minimum average total cost curve.

124) A perfectly competitive firm’s short-run supply curve is

A) its marginal cost curve above the shutdown point.

B) its marginal revenue curve above the shutdown point.

C) its demand curve.

D) horizontal at the going price.

125) The section of the marginal cost curve that lies above the average variable cost curve is

A) a perfectly competitive firm’s supply curve.

B) a perfectly competitive firm’s average total cost curve.

C) a perfectly competitive firm’s total fixed costs curve.

D) irrelevant to the firm because it never produces at any point along this curve.

126) A perfectly competitive firm’s supply curve

A) shows the relationship between the price and the quantity the firm will produce.

B) is the portion of the marginal cost curve above the average variable cost curve.

C) is upward sloping.

D) All of the above are correct.

127) A perfectly competitive firm’s short-run supply curve is

A) its marginal cost curve above the shutdown point.

B) its average total cost curve above the minimum of the average variable cost.

C) its average variable cost curve above the breakeven point.

D) horizontal at the market price.

128) The firm’s short run supply curve is equal to the

A) entire marginal cost curve.

B) marginal cost curve above the AVC curve.

C) marginal cost curve above the ATC curve.

D) marginal cost curve above the AFC curve.

129) Which of the following best describes the short-run supply curve for an individual perfectly

competitive firm?

A) It is the firm’s marginal cost curve.

B) It is the upward-sloping part of the firm’s marginal cost curve.

C) It is the vertical axis at prices less than minimum average variable cost and is the firm’s

marginal cost curve at prices above minimum average variable cost.

D) It is the vertical axis at prices less than minimum average total cost and is the firm’s marginal

cost curve at prices above minimum average total cost.

130) An individual perfectly competitive firm has a supply curve

A) with a positive slope.

B) with a negative slope.

C) that is parallel to the quantity axis.

D) that has a positive slope at lower output levels and a negative slope at higher output levels.

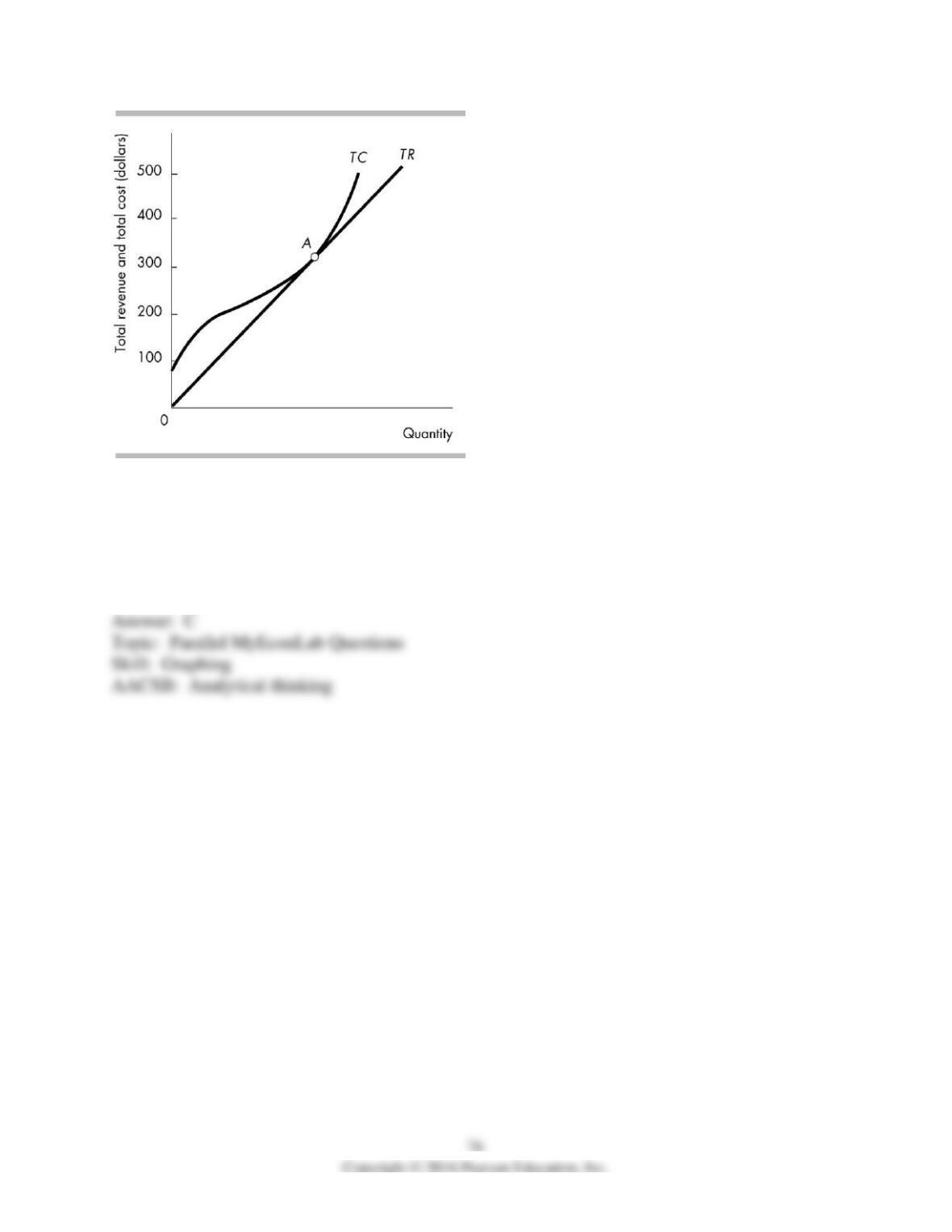

131) The figure above shows short-run cost curves for a perfectly competitive firm. If the price

of the product is $8, in the short run the firm will

A) make zero economic profit.

B) make an economic profit.

C) incur an economic loss.

D) None of the above answers is correct because more information is needed to determine the

firm’s economic profit or loss.

132) The figure above shows short-run cost curves for a perfectly competitive firm. If the price

of the product is $8 and the firm does not shut down, the firm’s output in the short run

A) will be 0.

B) will be between 0 and 10.

C) will be 10 or higher.

D) cannot be determined without more information.

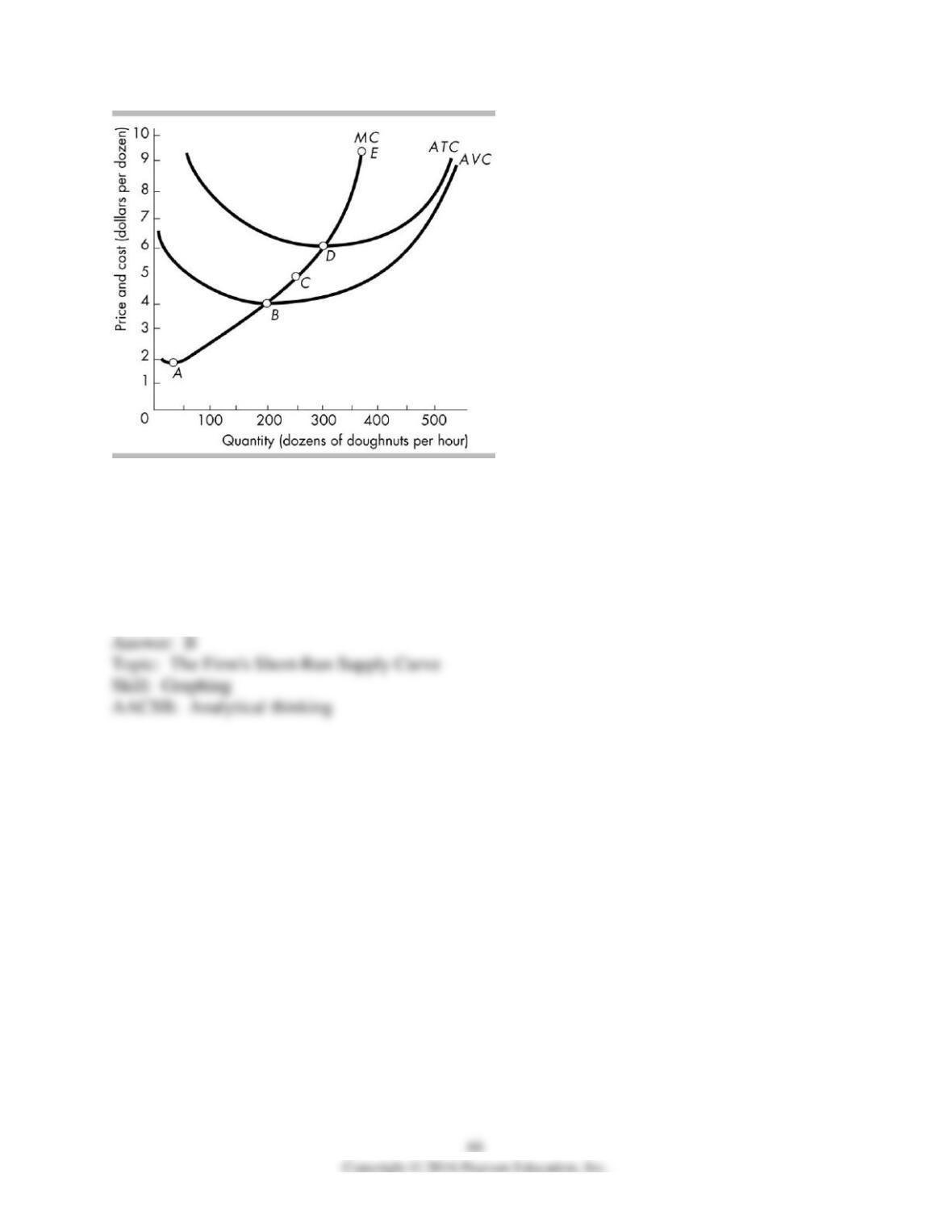

133) The donut market is perfectly competitive. The figure shows the costs of a typical donut

producer. In the short run, the donut producer’s supply curve is the curve running from point

________ to point E.

A) A

B) B

C) C

D) D

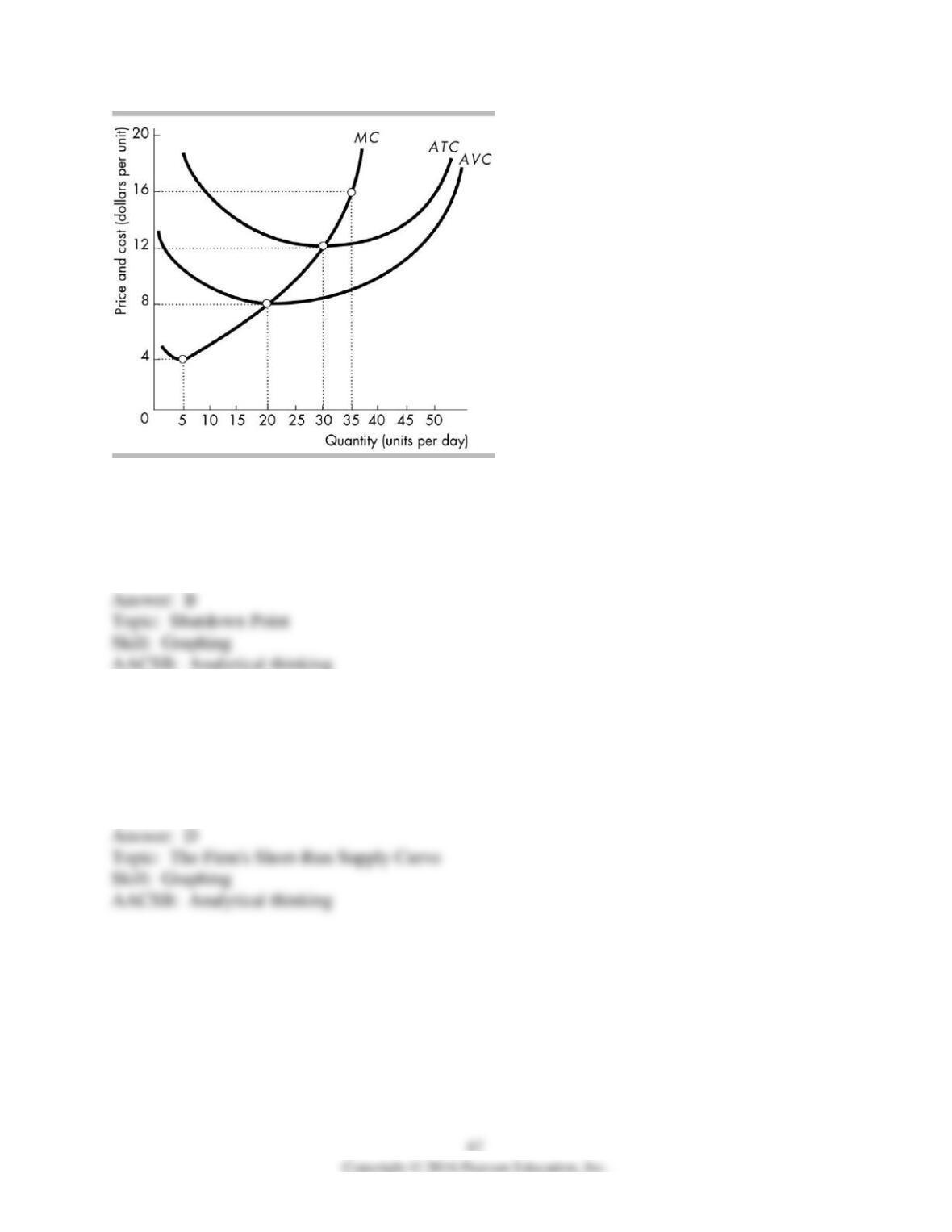

134) In the above figure, the perfectly competitive firm’s shutdown point is at a price of

A) $4 per unit.

B) $8 per unit.

C) $12 per unit.

D) $16 per unit.

135) In the above figure, if the price is $16 per unit, how many units will a profit maximizing

perfectly competitive firm produce?

A) 0

B) 20

C) 30

D) 35

136) In the above figure, if the price is $12 per unit, how many units will a profit maximizing

perfectly competitive firm produce?

A) 0

B) 20

C) 30

D) 35

137) In the above figure, if the price is $8 per unit, how many units will a profit maximizing

perfectly competitive firm produce?

A) 5

B) 20

C) 30

D) 35

138) In the above figure, if the price is $4 per unit, how many units will a profit maximizing

perfectly competitive firm produce?

A) 0

B) 5

C) 20

D) 30

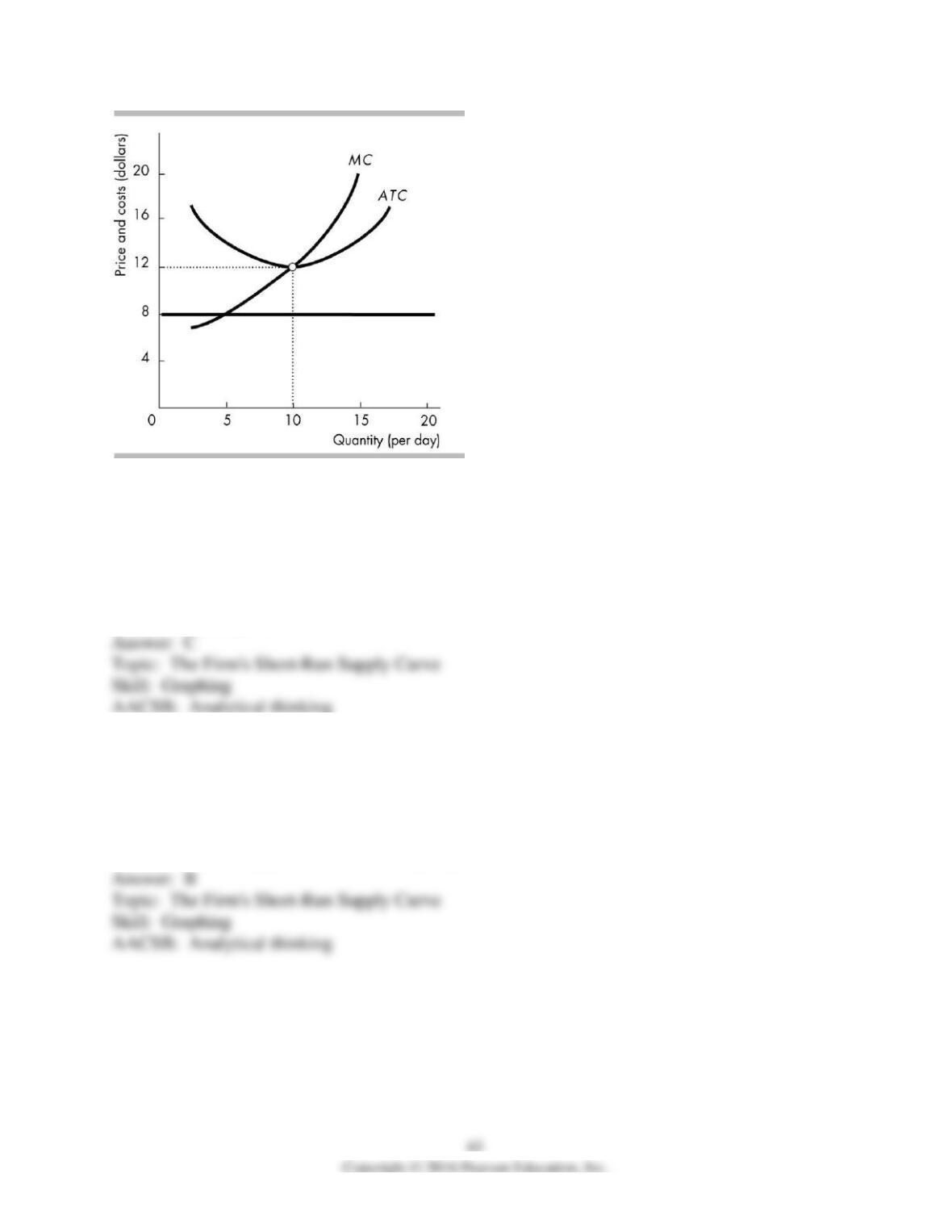

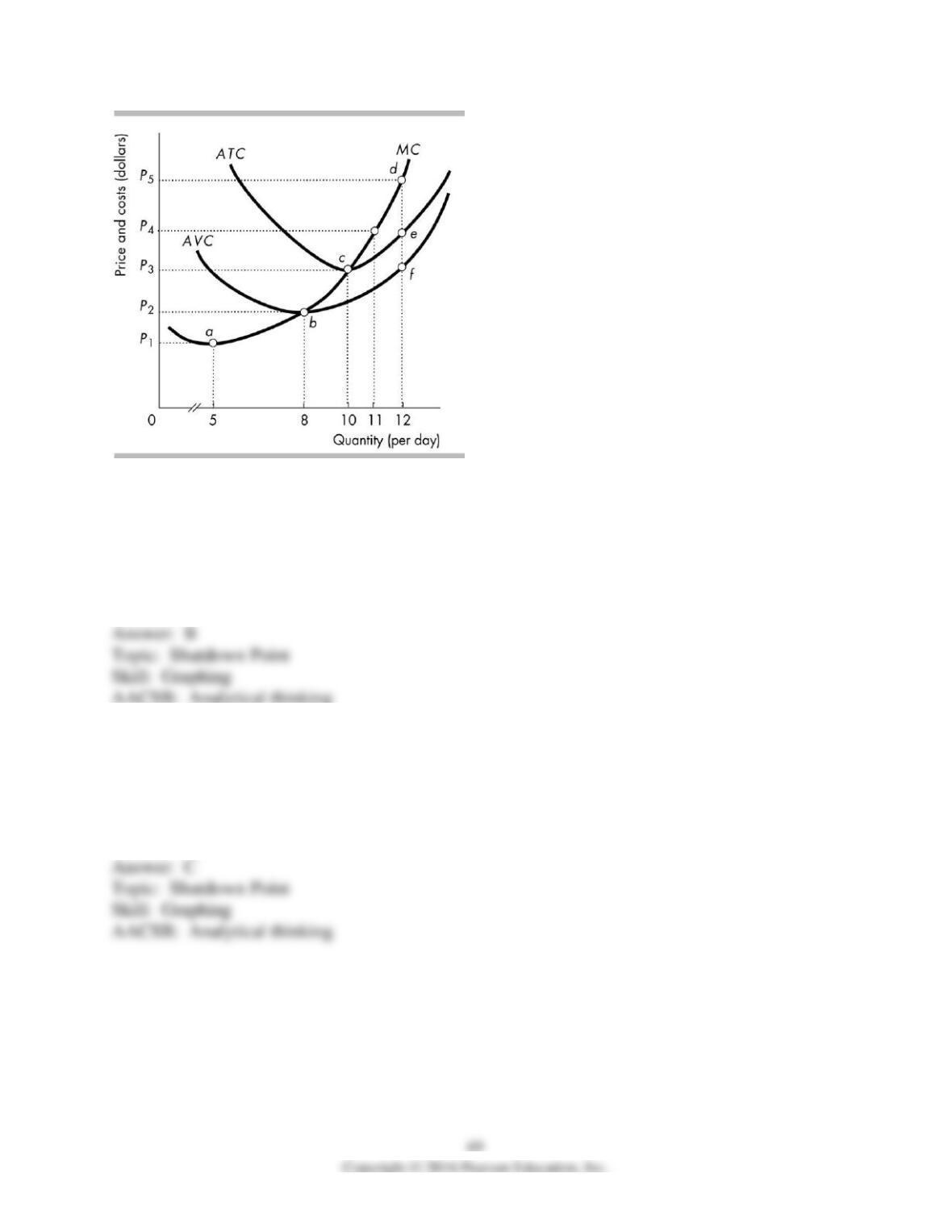

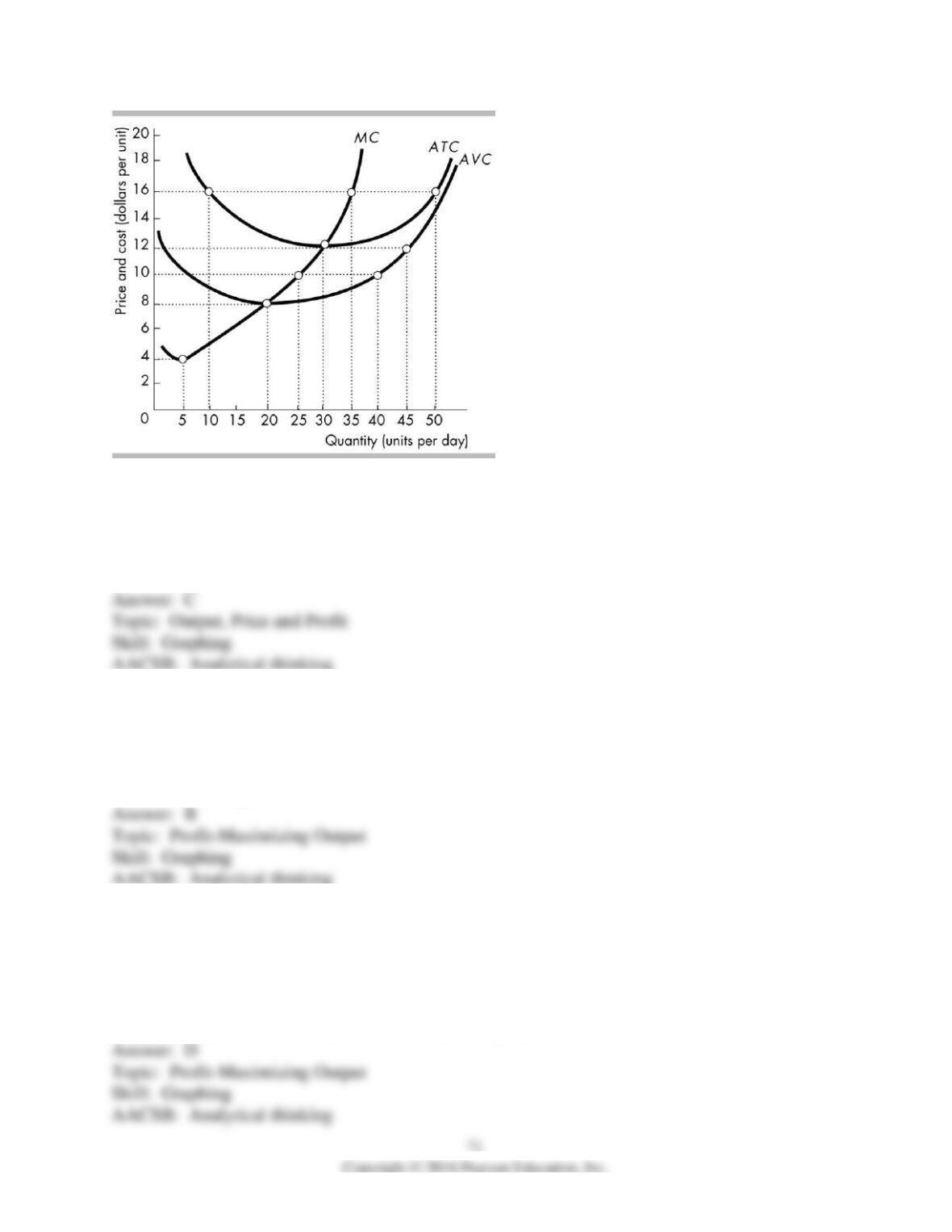

139) The figure above shows a firm in a perfectly competitive market. The firm will shut down if

price falls below

A) P1.

B) P2.

C) P3.

D) P4.

140) The figure above shows a firm in a perfectly competitive market. If the firm does not shut

down, the least amount of output that it will produce is

A) less than 5 units.

B) 5 units.

C) 8 units.

D) 10 units.

141) The figure above shows a firm in a perfectly competitive market. If the price rises from P3

to P4 then output will increase by

A) 0 units.

B) 1 unit.

C) 2 units.

D) 3 units.

142) The figure above shows a firm in a perfectly competitive market. The firm’s supply curve is

the curved line linking

A) point a to point c and stopping at point c.

B) point b to point d and continuing on past point d along the MC curve.

C) point b to point f and stopping at point f.

D) point c to point e and continuing on past point e along the ATC curve.

143) In the above figure, the vertical distance between the ATC and AVC curves is

A) the marginal cost.

B) the total cost.

C) the average fixed costs.

D) None of the above answers is correct.

144) In the above figure, if the price is $16, a profit-maximizing perfectly competitive firm will

A) produce 50 units.

B) produce 35 units.

C) produce 10 units.

D) choose not to produce.

145) In the above figure, if the price is $12, a profit-maximizing perfectly competitive firm will

have an economic profit

A) of less than $100 but more than $0.

B) of more than $100.

C) that is negative, that is, it will have an economic loss.

D) of zero, that is, it will break even with a normal profit.

146) In the above figure, if the price is $10, a profit-maximizing perfectly competitive firm will

A) produce 40 units.

B) produce 25 units.

C) produce 10 units.

D) choose not to produce.

147) Using the above figure, of the prices below, which price enables a perfectly competitive

firm to earn the maximum economic profit?

A) $4 per unit.

B) $10 per unit.

C) $12 per unit.

D) $16 per unit.

148) In the above figure, at any price between $8 per unit to $12 per unit, how many units will a

profit-maximizing perfectly competitive firm produce?

A) None, because the producer will never choose to operate at a loss.

B) Less than 20 because this will reduce marginal cost.

C) Between 20 and 30, because variable costs are covered so the firm’s losses will be minimized

by producing rather than shutting down.

D) More than 30, because variable costs are covered so that the producer can earn economic

profits.

149) In the above figure, below what minimum price will a perfectly competitive firm shut down

rather than produce?

A) for any price less than $16 per unit

B) for any price less than $12 per unit

C) for any price less than $8 per unit

D) for any price less than $4 per unit

150) In the above figure, at a price of $4 per unit, a profit-maximizing perfectly competitive firm

will

A) shut down because its total revenue is less than its variable costs.

B) incur an economic loss.

C) produce 5 units.

D) Both answers A and B are correct.

151) Bubba’s BBQ has fallen on some hard times. Bubba has analyzed his past revenue and cost

information and knows that if he shuts down, he will incur an economic loss equal to $20,000 in

remaining lease payments. Apparently, Bubba’s current planning horizon is

A) the short run because he still faces some fixed costs.

B) the long run because he faces only variable costs.

C) the short run because he faces only variable costs.

D) neither the short run nor the long run because lease payments do not figure into cost

determinations.

152) Homer’s Holesome Donuts has determined that its profit-maximizing quantity is 10,000

donuts per year. Homer’s earns $12,000 in revenue from the sale of those donuts. Homer’s has

two costs. First he pays $16,000 in annual rental payments for its five-year lease on its store.

Second Homer incurs an additional cost of $5,000 for ingredients. Homer’s fixed cost is equal to

A) 0.

B) $5,000.

C) $16,000.

D) $21,000.

153) Homer’s Holesome Donuts has determined that its profit-maximizing quantity is 10,000

donuts per year. Homer’s earns $12,000 in revenue from the sale of those donuts. Homer’s has

two costs. First he pays $16,000 in annual rental payments for its five-year lease on its store.

Second Homer incurs an additional cost of $5,000 for ingredients. Homer’s variable cost is equal

to

A) 0.

B) $5,000.

C) $16,000.

D) $21,000.

154) Homer’s Holesome Donuts has determined that its profit-maximizing quantity is 10,000

donuts per year. Homer’s earns $12,000 in revenue from the sale of those donuts. Homer’s has

two costs. First he pays $16,000 in annual rental payments for its five-year lease on its store.

Second Homer incurs an additional cost of $5,000 for ingredients. Homer’s economic profit is

equal to

A) -$16,000, that is, an economic loss of $16,000.

B) -$9,000, that is, an economic loss of $9,000.

C) +$9,000.

D) +$12,000.

155) Homer’s Holesome Donuts has determined that its profit-maximizing quantity is 10,000

donuts per year. Homer’s earns $12,000 in revenue from the sale of those donuts. Homer’s has

two costs. First he pays $16,000 in annual rental payments for its five-year lease on its store.

Second Homer incurs an additional cost of $5,000 for ingredients. Should Homer’s shut down in

the short run?

A) Yes, because he is incurring an economic loss.

B) Yes, because he cannot cover all of his fixed costs.

C) No, because is making positive economic profit.

D) No, because he can cover all of his variable costs.

156) Paul runs a shop that sells printers. Paul is a perfect competitor and can sell each printer for

a price of $300. The marginal cost of selling one printer a day is $200; the marginal cost of

selling a second printer is $250; and the marginal cost of selling a third printer is $350. To

maximize his profit, Paul should sell

A) one printer a day.

B) two printers a day.

C) three printers a day.

D) more than three printers a day.

157) Because of a decrease in the wage rate it must pay, a perfectly competitive firm’s marginal

costs decrease but its demand curve stays the same. As a result, the firm

A) decreases the amount of output it produces and raises its price.

B) increases the amount of output it produces and lowers it price.

C) increases the amount of output it produces and does not change its price.

D) decreases the amount of output it produces and lowers its price.

158) For prices above the minimum average variable cost, a perfectly competitive firm’s supply

curve is

A) horizontal at the market price.

B) vertical at zero output.

C) the same as its marginal cost curve.

D) the same as its average variable cost curve.

159) A perfectly competitive firm is definitely making an economic profit when

A) MR < MC.

B) P > ATC.

C) P < ATC.

D) P > AVC.

160) In the figure above, a firm is operating at point A on the graph. At point A, the firm’s

average cost curve

A) has negative slope.

B) has positive slope.

C) is horizontal.

D) is vertical.

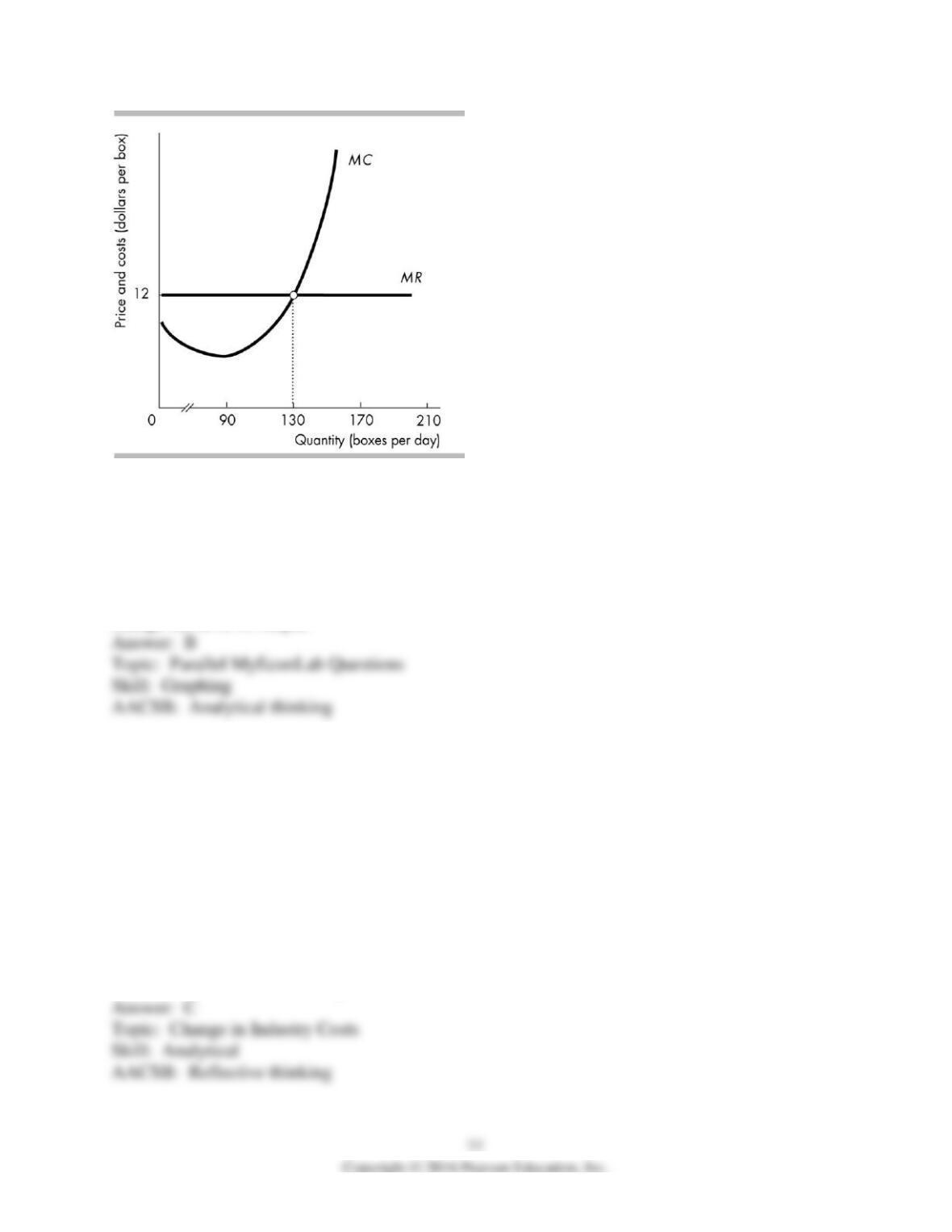

161) Carol’s Candies is producing 150 boxes of candy a day. Carol’s marginal revenue and

marginal cost curves are shown in the figure above. To increase her profit, Carol should

A) increase her output.

B) decrease her output.

C) maintain the current level of output because it gives her the maximum profit.

D) Not enough information is given to determine if Carol should increase, decrease, or not

change her level of output.

3 Output, Price, and Profit in the Short Run

1) If there are 1,000 rutabaga farms, all perfectly competitive, an increase in the price of fertilizer

used for growing rutabagas will

A) have no effect on the total quantity of rutabagas supplied, because no farm has enough market

power to raise the price.

B) have no effect on the total quantity of rutabagas supplied, because each farm’s supply curve is

a vertical line.

C) decrease the total quantity of rutabagas supplied, because each farm’s supply curve shifts

leftward.

D) reduce the total quantity of rutabagas supplied, because each farm’s supply curve is a

horizontal line and will shift upward.

2) The short-run market supply curve for a perfectly competitive market is obtained by summing

the part of each firm’s

A) AVC curve that lies above its MC curve.

B) MC curve that lies above its AVC curve.

C) AVC curve that lies below the MC curve.

D) MC curve that lies below the AVC curve.

3) In a perfectly competitive market, the market supply curve is the sum of the

A) supply curves of all the individual firms.

B) average variable cost curves of all the individual firms.

C) average total cost curves of all the individual firms.

D) average fixed cost curves of all the individual firms.

4) In the short run, a perfectly competitive firm’s economic profits

A) must equal zero, that is, the firm earns a normal profit.

B) must be positive.

C) might be positive, negative (an economic loss), or zero (a normal profit).

D) must be negative, that is the firm must incur an economic loss.

5) In the short run, a perfectly competitive firm

A) can either make an economic profit, incur an economic loss, or make zero economic profit.

B) never incurs an economic loss larger than its average fixed costs.

C) produces at any price.

D) always makes an economic profit.

6) In the short run, a perfectly competitive firm

A) cannot shut down.

B) must make zero economic profit.

C) can make an economic profit, incur an economic loss, or make zero economic profit.

D) will not incur an economic loss if it shuts down.

7) In the short run, a perfectly competitive firm

A) might not make an economic profit.

B) will always make an economic profit.

C) chooses its optimal plant size.

D) is in equilibrium only when its economic profit is zero.

8) In the short run, a perfectly competitive firm will make an economic profit as long as

A) it maximizes its profit.

B) P > AVC.

C) P > AFC.

D) P > ATC.

9) In the short run, the firm makes zero economic profit when the price is ________ minimum

average total cost, makes an economic profit when the price is ________ minimum average total

cost, and incurs an economic loss when the price is ________ minimum average total cost.

A) equal to; higher than; lower than

B) equal to; lower than; higher than

C) higher than; equal to; lower than

D) lower than; equal to; higher than

10) A perfectly competitive firm is making an economic profit when

A) its total revenue is greater than its total cost.

B) the price is greater than the minimum of its average total cost.

C) the price is greater than the minimum of its average variable cost.

D) Both answers A and B are correct.

11) A perfectly competitive firm will have an economic profit of zero if, at its profit-maximizing

output, its marginal revenue equals its

A) average total cost.

B) marginal cost.

C) average variable cost.

D) average fixed cost.

12) In a perfectly competitive market, which of the following will increase the economic profit

the firms make in the short run?

A) a decrease in market demand

B) an increase in market demand

C) an increase in labor costs

D) an increase in the number of firms

13) In a perfectly competitive market in the short run, as the market demand increases, the firms

________ their output and their economic profit ________.

A) increase; increases

B) increase; decreases

C) decrease; decreases

D) decrease; increases