Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

True / False

1. Firms may easily enter a monopolistically competitive market.

a.

True

b.

False

True

2. Product differentiation helps explain the slope of the demand curve facing a firm in monopolistic competition.

a.

True

b.

False

True

3. Monopolistic competitors are protected by barriers to entry.

a.

True

b.

False

False

4. A monopolistically competitive firm produces where demand is inelastic.

a.

True

b.

False

False

5. Monopolistically competitive firms use product differentiation to increase the price elasticity of demand.

a.

True

b.

False

False

6. In the long run, in monopolistic competition, firms earn zero economic profit.

a.

True

b.

False

True

7. If a monopolistically competitive firm is in long-run equilibrium and average cost equals $150, then the market price

must be $150.

a.

True

b.

False

True

8. In the long run, firms in a monopolistically competitive market earn zero economic profit.

a.

True

b.

False

True

9. Firms in a monopolistically competitive market that earn economic profit in the short run will continue to earn profit in

the long run.

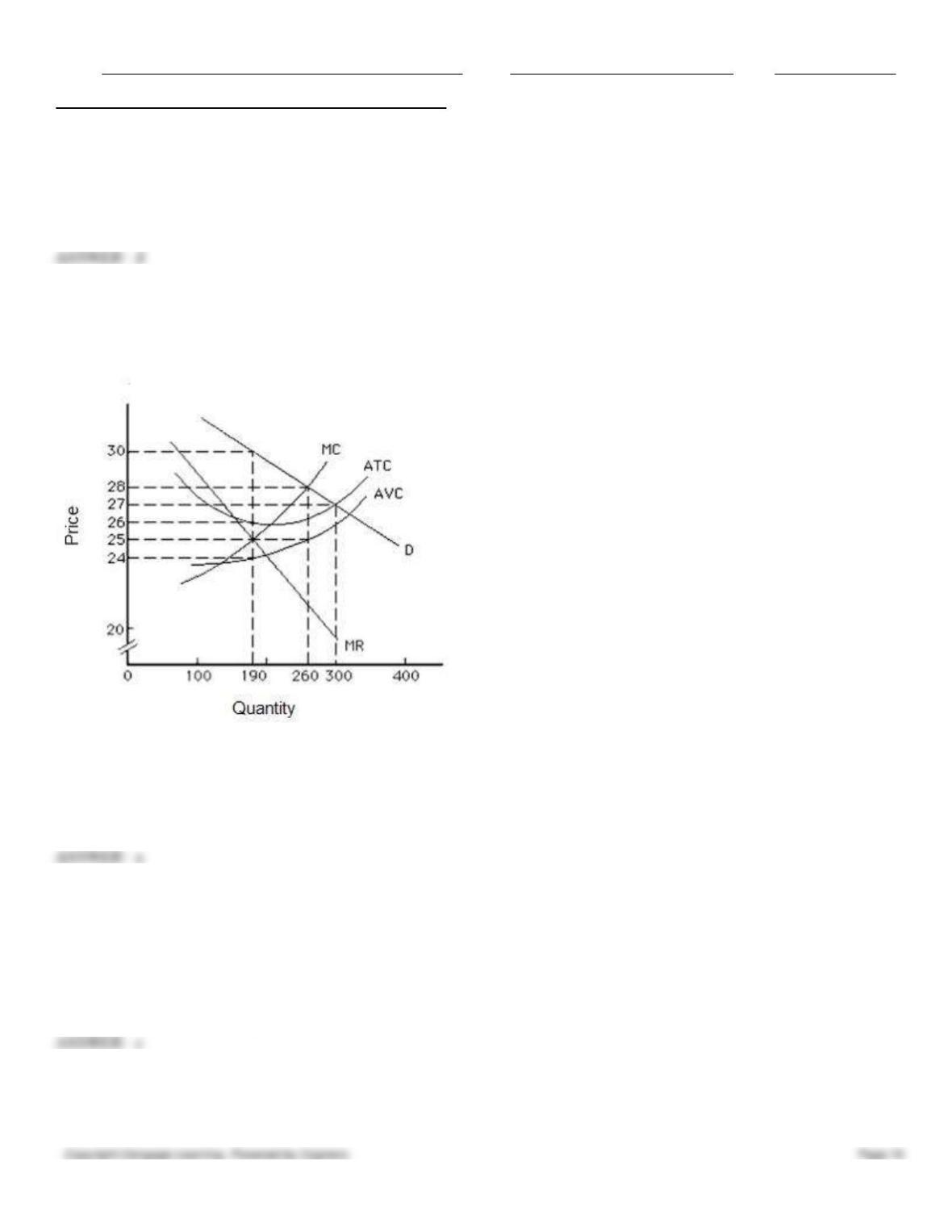

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

True

b.

False

False

10. In the long run, both perfectly competitive and monopolistically competitive firms produce at minimum average cost.

a.

True

b.

False

False

11. Excess capacity is defined as the difference between a firm’s maximum possible output and its actual output.

a.

True

b.

False

False

12. The defining characteristic of oligopoly is product differentiation.

a.

True

b.

False

False

13. When there are barriers to entry, a profit-maximizing firm already in the industry can charge any price it wants, even

in the long run.

a.

True

b.

False

False

14. In an oligopoly, a firm’s minimum efficient scale is large relative to the market.

a.

True

b.

False

True

15. Oligopolists often sacrifice economies of scale as they expand product variety.

a.

True

b.

False

True

16. Collusion is most likely to occur in those oligopolies in which firms have vastly different cost structures.

a.

True

b.

False

False

17. Cartels are inherently unstable.

a.

True

b.

False

True

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

18. An oligopolist that cheats on a collusive agreement by reducing price will quickly be forced out of the industry by its

competitors.

a.

True

b.

False

False

19. Consensus becomes easier to achieve as the number of firms in a cartel grows.

a.

True

b.

False

False

20. The incentives for oligopolists to cheat on collusive agreements are strongest during periods of increasing industry

sales.

a.

True

b.

False

False

21. As firms in an oligopoly are interdependent, they attempt to maximize revenues rather than profits.

a.

True

b.

False

False

22. A group of firms that agree to coordinate their production and pricing decisions to reap monopoly profit is called an

oligopoly.

a.

True

b.

False

False

23. Price wars occur more often in monopolistic competition than in other market structures.

a.

True

b.

False

False

24. A payoff matrix is a table listing the expected economic profit resulting from different possible strategies.

a.

True

b.

False

True

25. Game theory provides us with a general approach to understanding the behavior of firms when their choices are

interdependent.

a.

True

b.

False

True

26. The concept of the prisoner’s dilemma is applicable only when considering the illegal behavior that firms in a non–

competitive market may pursue.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

True

b.

False

False

27. The outcome in the prisoner’s dilemma is referred to as the profit-maximizing equilibrium.

a.

True

b.

False

False

28. Firms will always achieve dominant-strategy equilibrium if game theory is used to analyze oligopoly.

a.

True

b.

False

False

29. Table 10.2 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to

advertise or not. Eagle Tobacco has a dominant strategy.

Table 10.2

Dan’l Boone Tobacco

Advertise

Don’t advertise

Eagle Tobacco

Advertise

1150, 1150

2020, 630

Don’t advertise

630, 2020

1500, 1500

a.

True

b.

False

True

30. Table 10.2 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to

advertise or not. Eagle Tobacco’s dominant strategy is not to advertise.

Table 10.2

Dan’l Boone Tobacco

Advertise

Don’t advertise

Eagle Tobacco

Advertise

1150, 1150

2020, 630

Don’t advertise

630, 2020

1500, 1500

a.

True

b.

False

False

Multiple Choice

31. The term “monopolistic competition”:

a.

is an alternate expression for monopoly.

b.

is used to describe perfect competition that has strong entry barriers.

c.

denotes an industry characterized by one seller of many differentiated products.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

d.

denotes an industry characterized by many sellers of homogeneous products.

e.

denotes an industry characterized by many sellers of differentiated products.

32. Monopolistically competitive industries consist of:

a.

one firm selling several products.

b.

one firm selling one product.

c.

many firms, all selling identical products.

d.

many firms, each selling a slightly different product.

e.

many firms, each selling a completely different product.

33. Collusion among firms to raise prices is rare in monopolistically competitive markets because:

a.

there are too many firms.

b.

there are too few firms.

c.

there is only one firm.

d.

products are homogeneous.

e.

there are price leaders.

34. Monopolistically competitive firms ignore the effect of their decisions upon other firms in the industry because:

a.

each firm is large relative to the market.

b.

each firm is small relative to the market.

c.

there are few sellers in the market.

d.

there is only one seller in the market.

e.

all firms follow the same pricing rule.

35. FlyHigh Travel Agency, a monopolistic competitor, offers services that are differentiated from the services of other

producers in the industry. This implies that it:

a.

faces a perfectly elastic demand curve.

b.

is a price taker.

c.

has some control over the price it charges.

d.

faces a perfectly inelastic demand curve.

e.

produces a product with no close substitutes.

36. If a monopolistically competitive firm raises its price, it:

a.

earns a higher economic profit.

b.

loses some, but not all, of its customers.

c.

shuts down.

d.

has to pay higher taxes.

e.

gains customers.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

37. Which of the following is most likely produced in a monopolistically competitive market?

a.

Soybeans

b.

Autos

c.

Fast food

d.

Oil

e.

Local phone service

c

38. Monopolistically competitive firms _____.

a.

are price takers

b.

are price makers

c.

produce homogeneous products

d.

face high barriers to entry

e.

act interdependently

39. A monopolistic competitor’s demand curve is

a.

perfectly elastic.

b.

less elastic than a monopolist’s or oligopolist’s but more elastic than a perfect competitor’s demand curve.

c.

as elastic as an oligopolist’s demand curve.

d.

more elastic than a monopolist’s or oligopolist’s but less elastic than a perfect competitor’s demand curve.

e.

perfectly inelastic.

40. The demand curve facing a firm is likely to be relatively elastic if:

a.

the firm has few competing firms.

b.

the firm sells more differentiated products.

c.

there are many substitutes for its product.

d.

the firm is a price maker.

e.

the firm has control over the supply of a key resource.

c

41. Which of the following factors makes a monopolistically competitive firm a price maker?

a.

Product differentiation

b.

Barriers to entry

c.

Product similarity

d.

Its homogeneous product

e.

High tariffs

a

42. The demand curve facing Imelda’s Shoe Boutique, a monopolistically competitive firm, _____.

a.

is horizontal because Imelda’s is small relative to the market as a whole

b.

is horizontal because Imelda’s is large relative to the market as a whole

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

c.

slopes downward because Imelda’s is small relative to the market as a whole

d.

slopes downward because Imelda’s sells a differentiated product

e.

slopes downward because Imelda’s products are identical to its rival’s products.

43. Which of the following is true of the relationship between price and marginal cost under monopolistic competition?

a.

Price equals marginal cost at all levels of output.

b.

Price equals marginal cost only at the profit-maximizing quantity

c.

Price exceeds marginal cost at the profit-maximizing level of output

d.

Price is less than marginal cost at the profit-maximizing quantity

e.

Price is less than marginal cost at all levels of output

44. Compared to regular grocery stores, convenience stores have:

a.

higher prices and a more limited selection of goods.

b.

higher prices and a greater selection of goods.

c.

lower prices and a more limited selection of goods.

d.

lower prices and a greater selection of goods.

e.

equal prices and an equal selection of goods.

45. Monopolistic competition is different from perfect competition because monopolistic competitors:

a.

produce homogeneous products

b.

are price takers.

c.

have high barriers to entry.

d.

produce differentiated products.

e.

act interdependently.

46. All of the following are examples of product differentiation except one. Which of the following is the exception?

a.

Developing a new video game or a computer program called “How to Teach Your New Dog Old Tricks”

b.

Manufacturing a car that minimizes outside noise more than other cars do

c.

Lowering the price of a good for a special sale

d.

Providing movies and special meals on airline flights

e.

Making sodium-free, caffeine-free colas

47. Economic analysis of product differentiation leads to all of the following conclusions except one. Which is the

exception?

a.

Product differentiation makes it harder for firms to collude.

b.

Product differentiation makes price leadership harder to maintain.

c.

Product differentiation sometimes contributes to wasteful allocation of resources.

d.

Product differentiation must be based on real, substantive differences among products.

e.

Product differentiation makes it easier for firms to liquidate assets.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

48. When firms differentiate their products, they:

a.

usually create barriers to entry into the market in which they operate

b.

always increase their profits.

c.

always increase product prices.

d.

frequently create artificial or superficial differences among products, thus raising production costs.

e.

usually strain the physical capacity of their plants.

49. If firms in an industry produce differentiated products, they are likely to:

a.

earn zero economic profit in the long run.

b.

earn positive economic profit in the short run.

c.

face perfectly elastic demand curves.

d.

face downward-sloping demand curves.

e.

incur lower production costs.

50. A common feature of monopolistic competition, pure monopoly, and perfect competition is that _____.

a.

entry is free in each market structure

b.

producers in each market structure earn economic profit in the long run

c.

producers in each market structure sell differentiated products

d.

firms in these market structures act as price takers

e.

the profit-maximizing condition in each market is the same

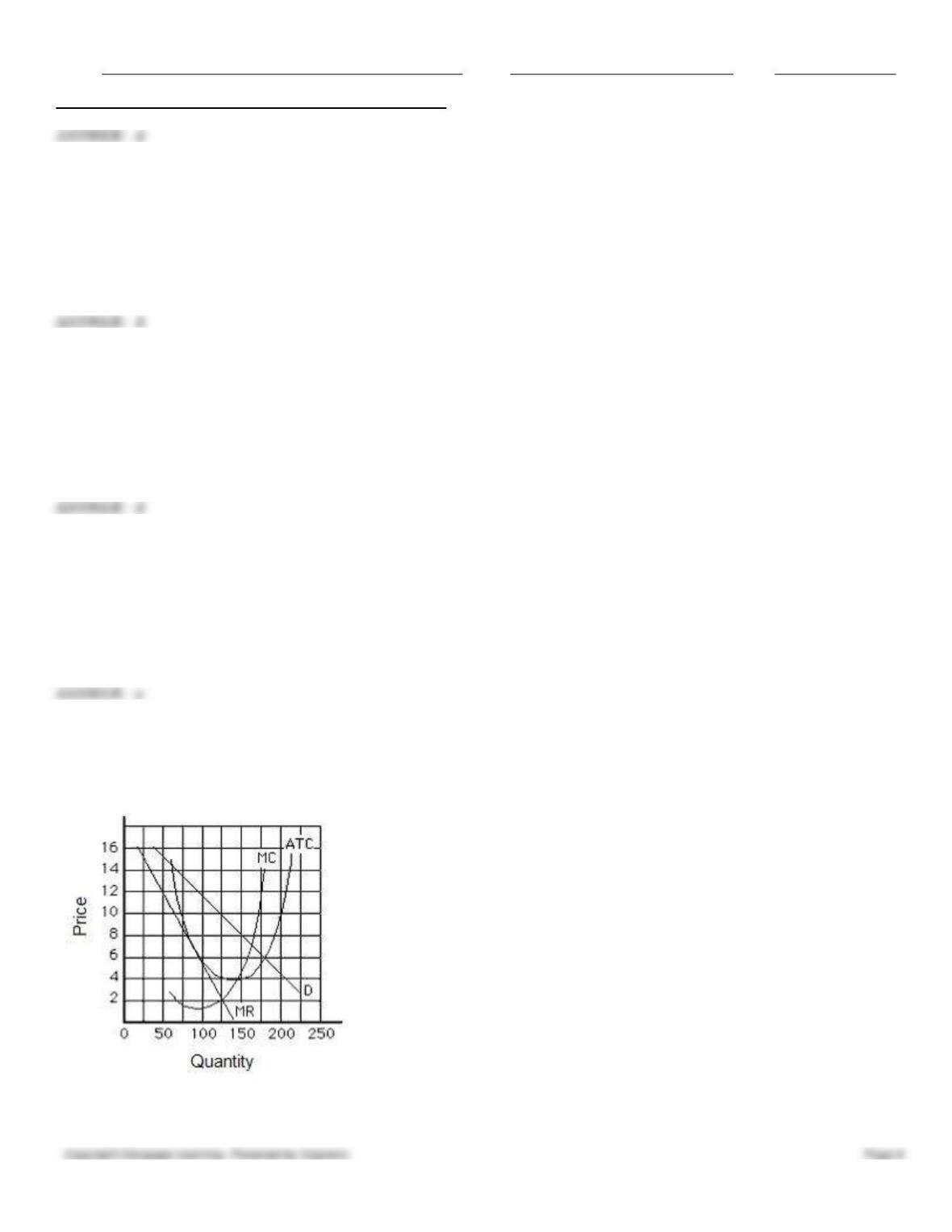

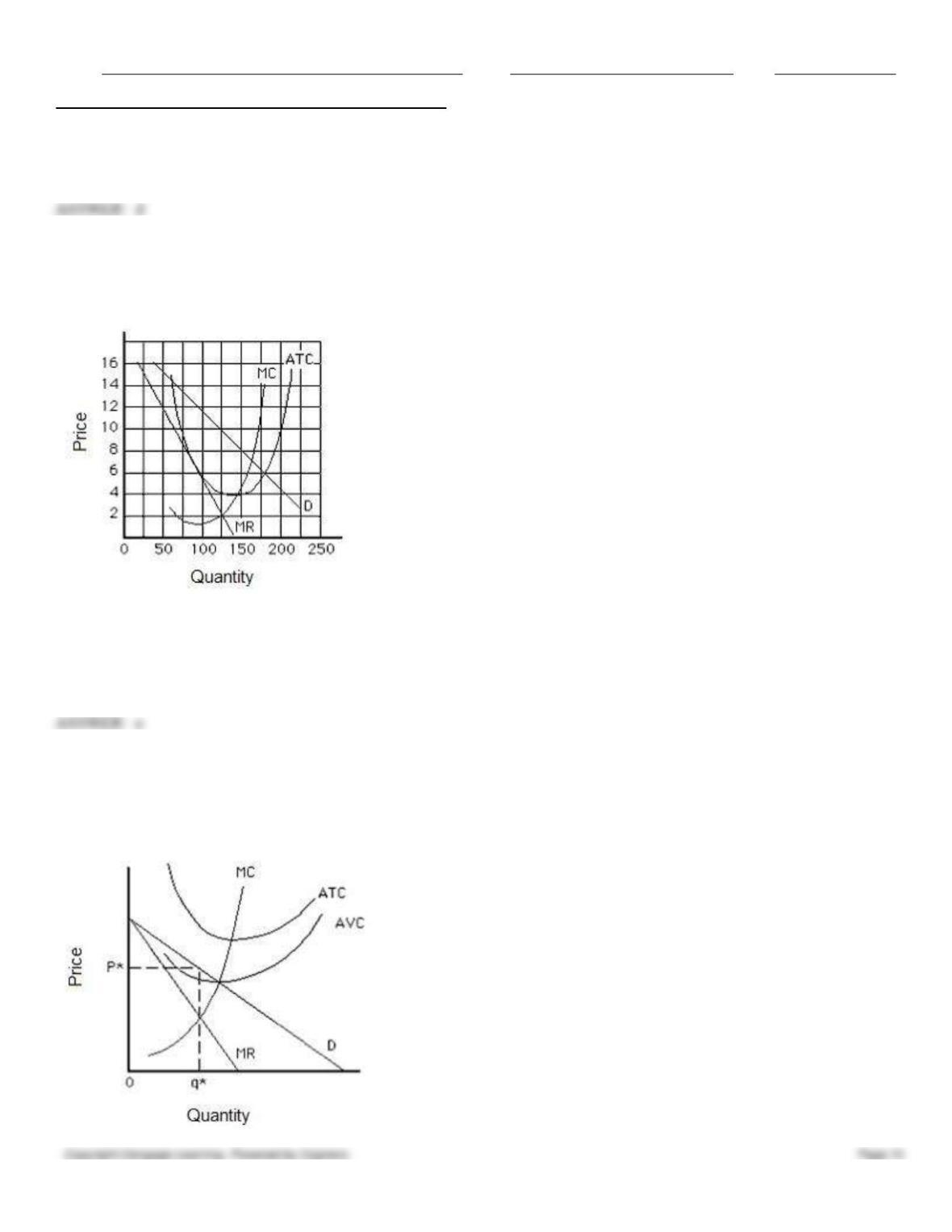

51. Figure 10.1 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. The monopolistic

competitor’s profit-maximizing level of output is:

Figure 10.1.

a.

75 units.

b.

100 units.

c.

125 units.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

d.

150 units.

e.

137.5 units.

52. Figure 10.1 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. The price that the

monopolistic competitor will charge at the profit-maximizing level of output is _____.

Figure 10.1.

a.

$2

b.

$4

c.

$8

d.

$9

e.

$10

53. Figure 10.1 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. The monopolistic

competitor is in:

Figure 10.1.

a.

long-run equilibrium because price equals average total cost.

b.

long-run equilibrium because marginal cost equals marginal revenue.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

c.

long-run equilibrium because price exceeds marginal cost.

d.

short-run equilibrium because it is earning a positive economic profit.

e.

short-run equilibrium because price equals average total cost.

54. Figure 10.1 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. The monopolistic

competitor’s total economic profit at the profit-maximizing level of output is:

Figure 10.1.

a.

$0.

b.

$4.

c.

$600.

d.

$6.

e.

$750.

e

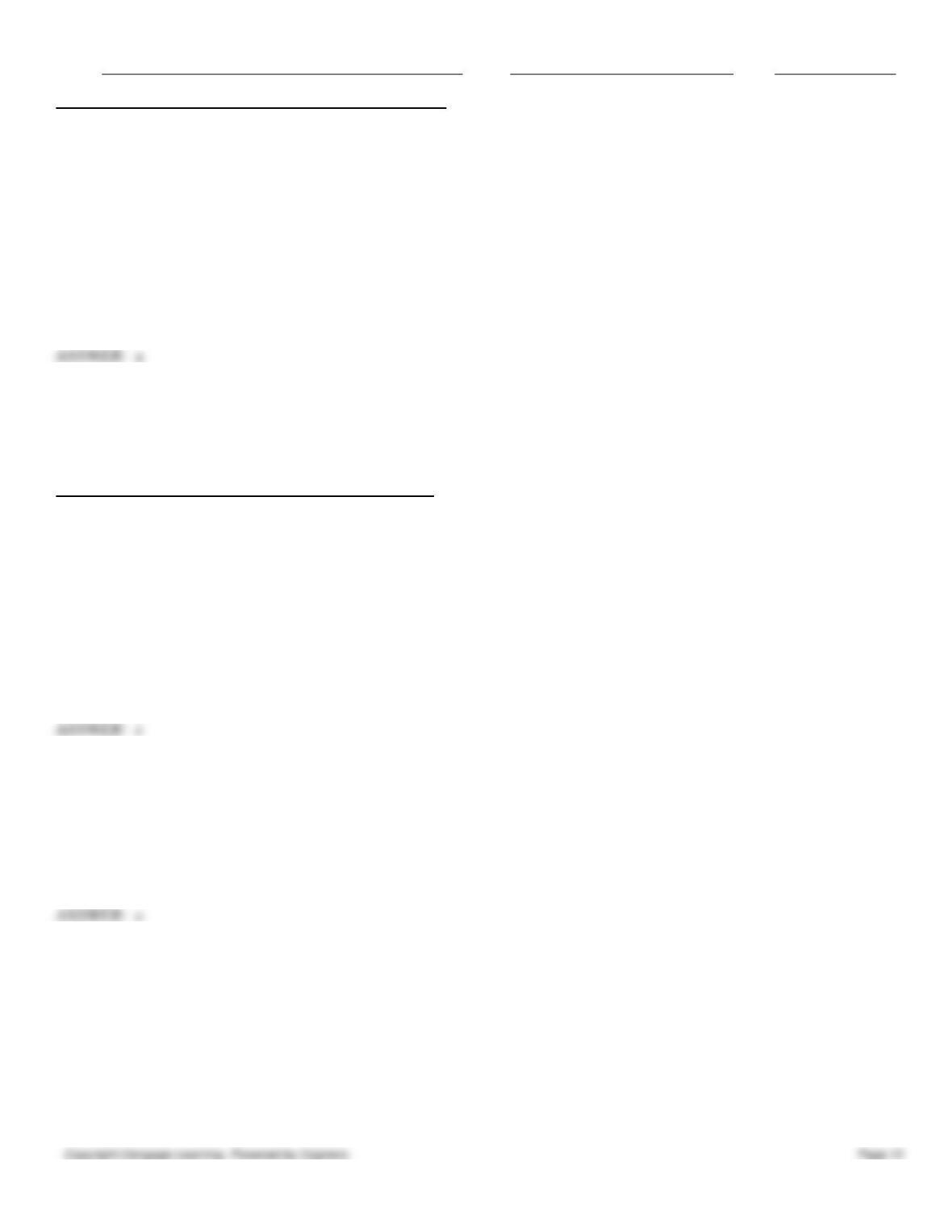

55. Figure 10.2 shows a firm that charges price P* for output q*. In order to minimize loss in the short run, the firm

should:

Figure 10.2.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

shut down because price is greater than average variable cost.

b.

shut down because price is greater than marginal cost.

c.

shut down because price is less than marginal revenue.

d.

continue to produce because price is greater than average variable cost.

e.

continue to produce because price is greater than marginal cost.

56. Table 10.1 shows the output, price, and total cost for a monopolistic competitor. The profit-maximizing output for the

monopolistic competitor is _____.

Table 10.1.

Q

P

TC

1

$27

$10

2

24

17

3

21

32

4

18

47

5

15

67

a.

0 units

b.

1 unit

c.

3 units

d.

5 units

e.

2 units

57. Table 10.1 shows the output, price, and total cost for a monopolistic competitor. The profit-maximizing price for the

firm is:

Table 10.1.

Q

P

TC

1

$27

$10

2

24

17

3

21

32

4

18

47

5

15

67

a.

$0.

b.

$27.

c.

$21.

d.

$15.

e.

$18.

58. Table 10.1 shows the output, price, and total cost for a monopolistic competitor. At the profit-maximizing output, the

firm earns:

Table 10.1.

Q

P

TC

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

1

$27

$10

2

24

17

3

21

32

4

18

47

5

15

67

a.

an economic profit of $31.

b.

an economic profit, but the amount cannot be determined.

c.

zero economic profit.

d.

an economic profit of $32.

e.

an economic loss.

59. Table 10.1 shows the output, price, and total cost for a monopolistic competitor. At the profit-maximizing output, the

monopolistically competitive firm is in:

Table 10.1.

Q

P

TC

1

$27

$10

2

24

17

3

21

32

4

18

47

5

15

67

a.

long-run equilibrium and price equals average total cost.

b.

long-run equilibrium and price is less than average total cost.

c.

short-run equilibrium and price is greater than average total cost.

d.

short-run equilibrium and incurs an economic loss.

e.

short-run equilibrium and there is zero economic profit.

60. In the short run, a monopolistically competitive firm is:

a.

likely to shut down.

b.

likely to charge a price that is less than the average cost of production.

c.

guaranteed to earn an economic loss.

d.

guaranteed to earn either zero or positive economic profit.

e.

not guaranteed any level of economic profit.

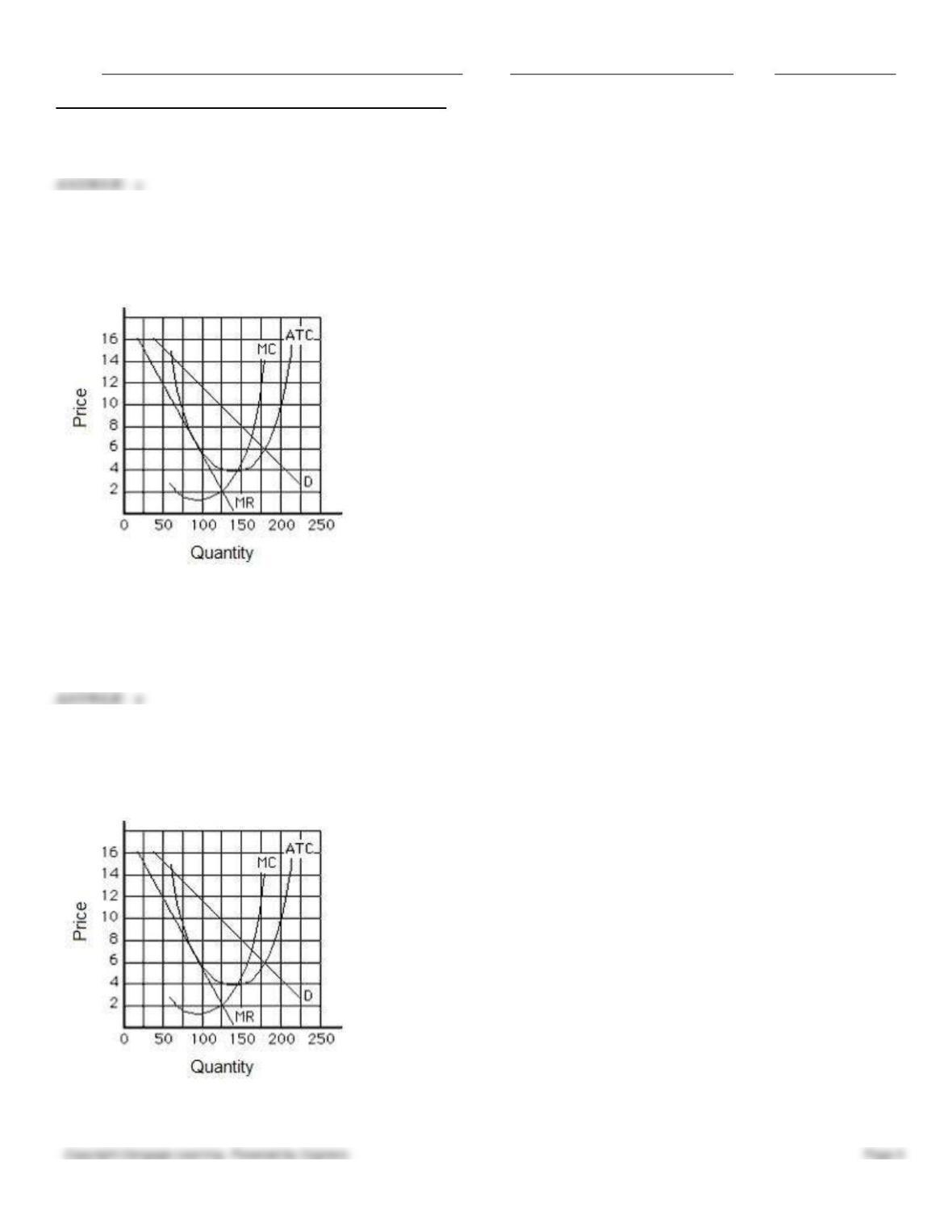

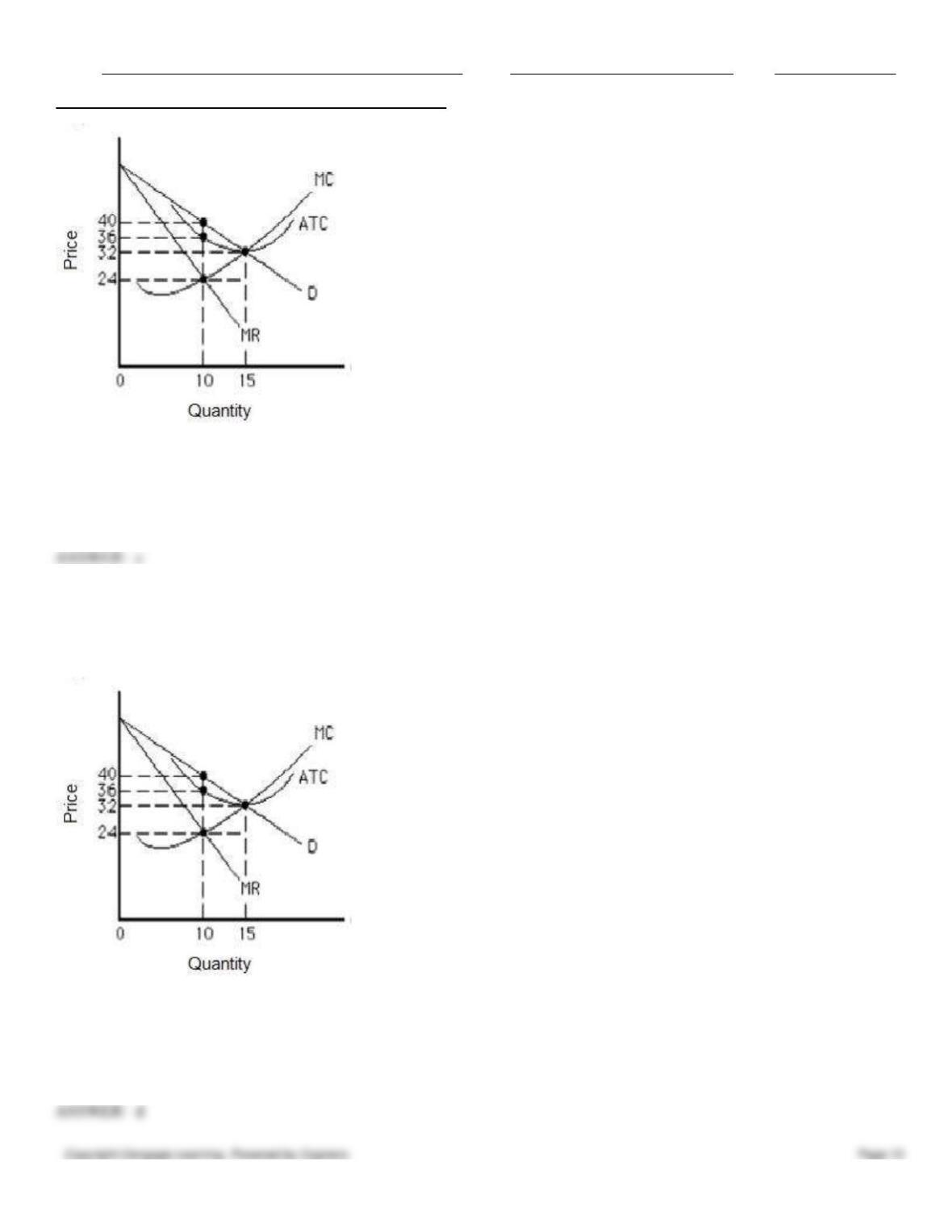

61. Figure 10.3 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. In the short run, the

firm will _____.

Figure 10.3.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

produce 10 units at a price of $36 per unit

b.

produce 10 units at a price of $24 per unit

c.

produce 10 units at a price of $40 per unit

d.

produce 15 units at a price of $32 per unit

e.

produce 15 units at a price of $24 per unit

62. Figure 10.3 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. In the long run,

_____.

Figure 10.3.

a.

new technology will lower average total costs and increase profits for the firm

b.

firms will exit this market, causing economic profit to increase

c.

product differentiation will lead to an increase in profits earned by the firm

d.

new firms will enter the market, driving economic profit to zero

e.

firms will produce 15 units of output in the long run

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

63. In the short run, a monopolistically competitive firm continues to increase production _____ if it can at least cover its

variable cost.

a.

as long as MR > AVC

b.

until MR = ATC

c.

as long as MC > MR

d.

until MR = AR

e.

until MR = MC

64. Suppose a monopolistically competitive firm is earning an economic profit. The marginal revenue from selling an

additional unit is $30, and the marginal cost of producing that additional unit is $23. The firm should:

a.

change neither its price nor its output level.

b.

reduce its price and increase its output level.

c.

increase its price and reduce its output level.

d.

reduce both its price and its output level.

e.

increase both its price and its output level.

65. If there is an increase in the demand for restaurant meals in an economy in the short run, _____.

a.

the losses incurred by each restaurant will increase

b.

the price charged by each restaurant will fall

c.

there will be an increase in the number of restaurants in the economy

d.

there will be a decrease in the number of restaurants in the economy

e.

the profit incurred by each restaurant will increase

66. A monopolistically competitive firm is producing at an output level where marginal revenue is greater than marginal

cost. This firm should _____ quantity and _____ price to increase profit or reduce losses.

a.

increase, increase

b.

increase; decrease

c.

decrease; increase

d.

decrease; decrease

e.

increase; not change

67. A profit-maximizing firm in monopolistic competition should shut down in the short run if:

a.

marginal revenue is less than price.

b.

price is more than average total cost.

c.

price is less than average fixed cost.

d.

price is less than average variable cost.

e.

marginal revenue is equal to marginal cost.

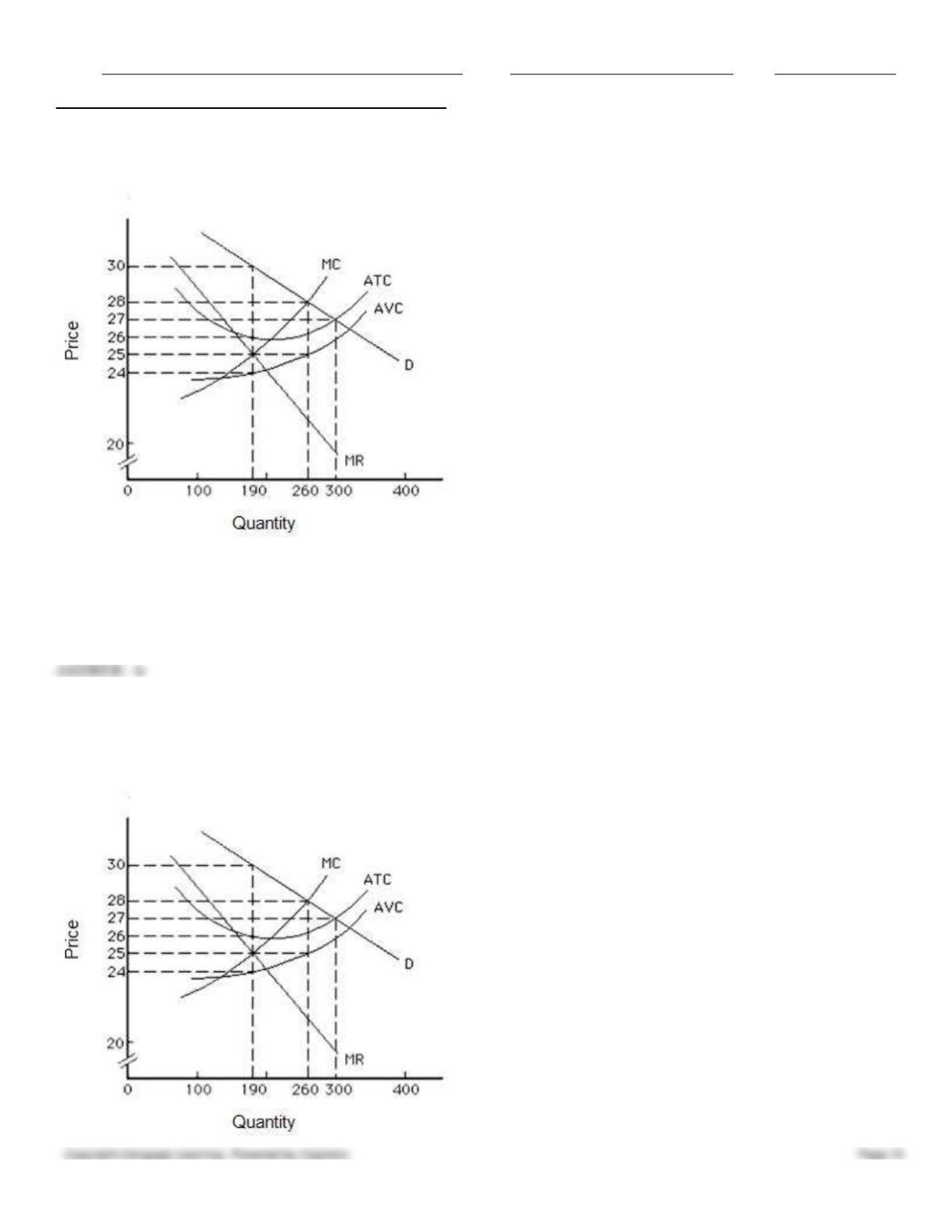

68. Figure 10.4 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. If the firm is

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

producing at a profit-maximizing level of output, its total revenue is _____.

Figure 10.4

a.

$5,320

b.

$5,700

c.

$4,750

d.

$8,120

e.

$8,100

69. Figure 10.4 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. At the profit-

maximizing output level, the total cost incurred by the firm in is approximately _____.

Figure 10.4

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

$5,700

b.

$5,320

c.

$4,750

d.

$4,940

e.

$8,100

70. Figure 10.4 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. At the profit-

maximizing output level, the firm is:

Figure 10.4

a.

earning an economic profit of $760.

b.

earning an economic profit of $950.

c.

earning zero economic profit.

d.

earning an economic profit of $990.

e.

suffering a loss of $1,000.

a

71. In both monopolistic competition and a non-price-discriminating monopoly, _____.

a.

the marginal revenue curve lies above the average revenue curve

b.

the marginal revenue curve lies above the demand curve

c.

the marginal revenue curve lies below the demand curve

d.

marginal revenue is equal to average revenue

e.

marginal revenue is equal to price

c

72. Suppose a monopolistically competitive firm is producing at an output level where marginal revenue is less than

marginal cost. This firm should _____quantity and _____ price to increase profit or reduce losses.

a.

increase, increase

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

b.

increase; decrease

c.

decrease; increase

d.

decrease; decrease

e.

increase; not change

73. In long-run equilibrium, a monopolistically competitive firm will produce:

a.

at its minimum average cost.

b.

at full capacity.

c.

along the downward-sloping portion of its ATC curve.

d.

along the upward-sloping portion of its ATC curve.

e.

at the minimum point of its marginal cost curve.

74. Monopolistically competitive firms do not achieve allocative efficiency in the long run because:

a.

marginal cost equals marginal revenue.

b.

marginal cost is greater than marginal revenue.

c.

marginal cost is less than marginal revenue.

d.

price is less than marginal cost.

e.

price is greater than marginal cost.

75. In the long run, a monopolistically competitive firm will:

a.

produce a greater variety of goods than do firms in other market structures.

b.

produce at a greater output level than a perfectly competitive firm.

c.

produce where price equals average total cost.

d.

earn an economic profit.

e.

suffer a loss because of its advertising budget.

76. Suppose a monopolistically competitive firm is in long-run equilibrium. The firm’s demand curve is tangent to its

average cost curve at Q = 25. Average cost is minimized at Q = 35, where average cost is $50. Which of the following is

true?

a.

This firm maximizes profit at an output level of 25 units.

b.

This firm maximizes profit at an output level of 35 units.

c.

This firm maximizes profit at an output level less than 25 units.

d.

This firm maximizes profit at an output level greater than 35 units.

e.

This firm incurs economic loss in the long run.

77. Due to the ease of entry of new firms into monopolistically competitive markets in the long run, existing firms in these

markets:

a.

produce at the lowest average total cost.

b.

charge a price equal to marginal cost.