Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

c.

earn no economic profit in the long run.

d.

take advantage of economies of scope.

e.

earn no economic profit in the short run.

78. Bubba’s Baby Boutique is a monopolistically competitive firm. In the long run, it earns:

a.

zero normal profit but positive economic profit.

b.

normal profit but zero economic profit.

c.

both normal and economic profit.

d.

zero normal and economic profit.

e.

less revenue than in the short run.

79. Monopolistically competitive firms:

a.

are guaranteed to earn short-run economic profit.

b.

may earn short-run economic profit, but long-run economic profit is typically zero.

c.

may earn economic profit both in the short run and in the long run.

d.

earn zero economic profit both in the short run and in the long run.

e.

can earn an economic profit only if they operate along the inelastic portion of their demand curves.

80. In the long run, economic profit earned by a monopolistically competitive firm:

a.

is zero due to the lack of barriers to entry.

b.

is zero due to the production of homogenous goods.

c.

may be positive due to strong barriers to entry.

d.

may be positive due to product differentiation.

e.

may be positive due to advertising and product promotion.

81. In the long run, the demand curve facing a monopolistically competitive firm:

a.

is perfectly elastic.

b.

slopes upward.

c.

is tangent to the firm’s average total cost curve.

d.

lies above the firm’s average total cost curve.

e.

is perfectly inelastic.

82. In the long run, a monopolistically competitive firm will not produce at the output level that minimizes average cost

because:

a.

MC is less than MR at that output level.

b.

MC is greater than MR at that output level.

c.

Price is greater than MR at that output level.

d.

demand is horizontal.

e.

that would leave the firm with excess capacity.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

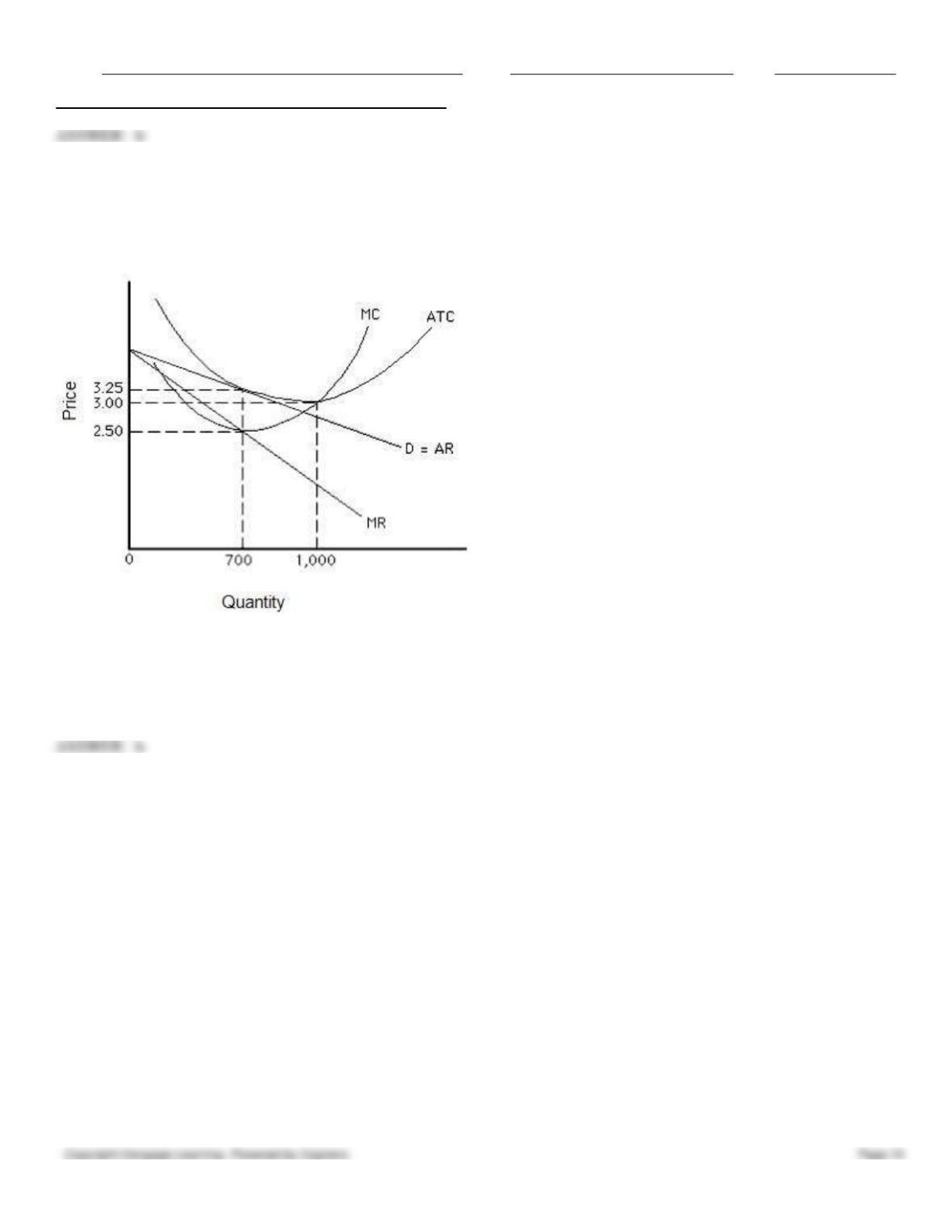

83. Figure 10.5 shows the demand, marginal revenue, and cost curves for a monopolistically competitive firm. The profit-

maximizing (or loss-minimizing) output for the firm is _____.

Figure 10.5.

a.

0 units

b.

700 units

c.

1,000 units

d.

more than 700 units and less than 1,000 units

e.

more than 1,000 units

84. Figure 10.5 shows the demand, marginal revenue, and cost curves for a monopolistically competitive firm. The profit-

maximizing (or loss-minimizing) price for the firm is _____.

Figure 10.5.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

higher than $3.25

b.

$3.25

c.

$3.00

d.

$2.50

e.

between $2.50 and $3.00

85. Figure 10.5 shows the demand, marginal revenue, and cost curves for a monopolistically competitive firm. At the

profit-maximizing (or loss-minimizing) output and price, the firm would:

Figure 10.5.

a.

be earning zero economic profit.

b.

be earning an economic profit.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

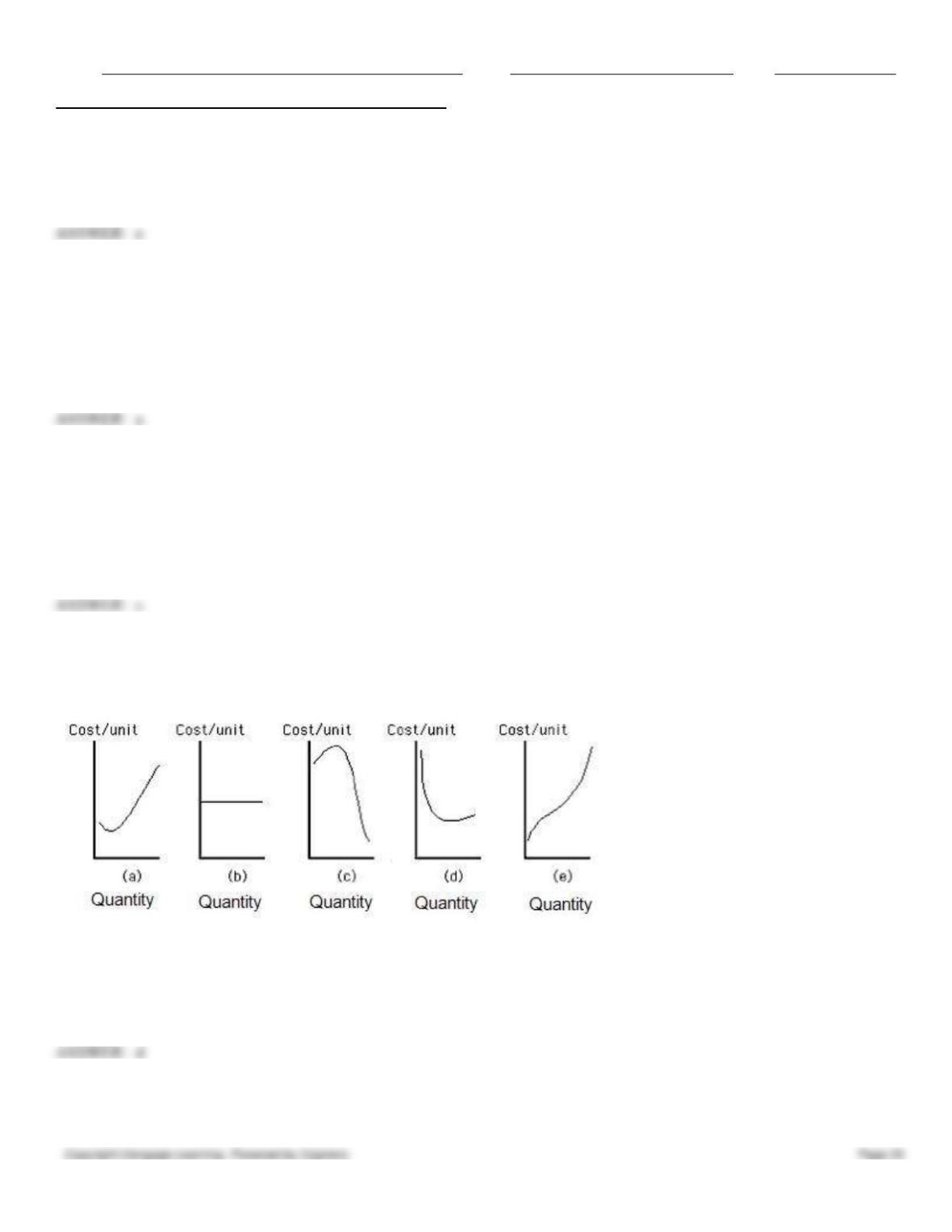

c.

be earning an economic loss.

d.

be better off shutting down since total revenue does not cover fixed costs.

e.

have to expand to stay in business in the long run.

86. If there occurs a permanent decrease in the demand for convenience store services, _____ in the long run

a.

each store will incur economic loss

b.

the price charged by each store will increase

c.

there will be a decrease in the number of such stores

d.

there will be an increase in the number of such stores

e.

each store will earn economic profit

87. Which of the following characteristics does perfect competition share with monopolistic competition?

a.

Price-taking firms

b.

Zero long-run economic profit

c.

Homogeneous products

d.

Strong barriers to entry

e.

Economies of scale in production

88. Suppose firms in a monopolistically competitive industry are currently earning short-run economic profit. In the long

run, the demand curve facing each individual firm is likely to:

a.

shift to the left and become flatter.

b.

shift to the left and become steeper.

c.

shift to the right and become flatter.

d.

shift to the right and become steeper.

e.

remain unchanged.

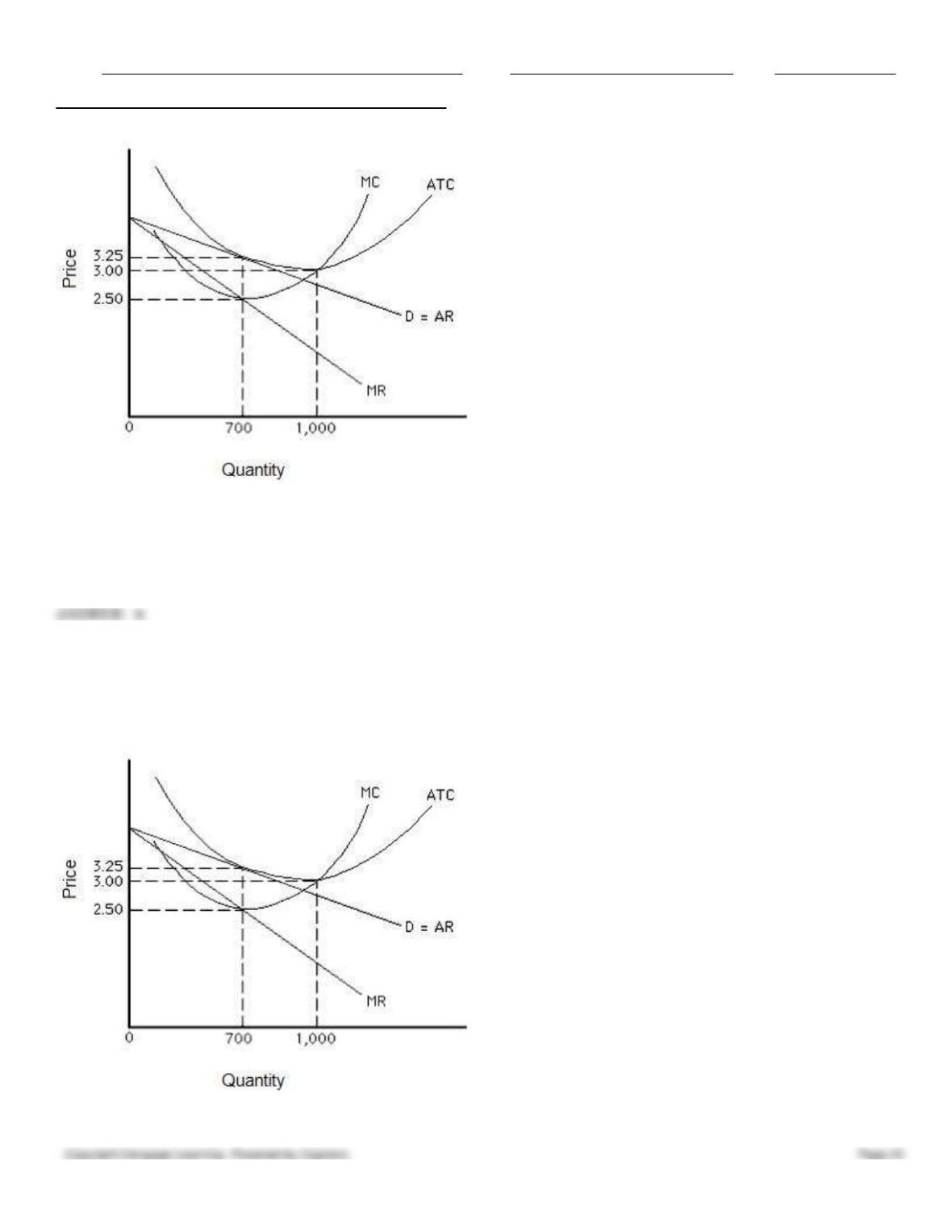

89. Figure 10.4 shows the demand, marginal revenue, and cost curves for a monopolistic competitor. In the long run, the

firm can expect:

Figure 10.4

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

to earn an economic profit of $760.

b.

to earn an economic profit of $950.

c.

to earn zero economic profit.

d.

to earn an economic profit of $990.

e.

to suffer a loss of $1,000.

90. A rise in demand for restaurant meals is likely to _____ in the long run.

a.

increase losses for each restaurant

b.

lower the price of restaurant meals

c.

decrease the number of restaurants

d.

increase the number of restaurants in the industry

e.

increase the economic profit earned by restaurants

91. Suppose a monopolistically competitive firm is in long-run equilibrium. The firm’s demand curve is tangent to its

average cost curve at Q = 25. Average cost is minimized at Q = 35, where average cost is $50. Which of the following is

true?

a.

This firm charges $50 for the good.

b.

This firm charges more than $50 for the good.

c.

This firm charges less than $50 for the good.

d.

The firm has excess capacity at all output levels greater than 35 units.

e.

Average cost is $50 at the profit-maximizing output level.

92. Which of the following is inconsistent with the model of perfect competition?

a.

Ease of entry into an industry

b.

Ease of exit from an industry

c.

Many buyers and sellers in the industry

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

d.

Advertising of product differences in the industry

e.

A horizontal demand curve facing each firm in the industry

93. In the long run, the profit-maximizing output of a monopolistically competitive firm:

a.

exceeds that of an otherwise similar perfectly competitive firm.

b.

is less than that of an otherwise similar perfectly competitive firm.

c.

occurs where average revenue equals marginal revenue.

d.

equals that of an otherwise similar perfectly competitive firm.

e.

is less than its profit-maximizing output in the short run.

94. Monopolistically competitive firms are unlikely to:

a.

operate where price equals marginal cost.

b.

charge a higher price than firms in perfect competition.

c.

produce a smaller quantity than firms in perfect competition.

d.

produce where price equals average total cost.

e.

exit the industry when demand falls below long-run average costs.

95. Which of the following is true of firms in monopolistic competition and perfect competition?

a.

Firms face a horizontal demand curve.

b.

Price exceeds marginal revenue.

c.

Firms can enter and leave the industry with relative ease.

d.

Price exceeds marginal cost.

e.

Products are differentiated.

96. One difference between perfect competition and monopolistic competition is that:

a.

firms in perfect competition cannot earn a long-run economic profit, whereas firms in monopolistic

competition can earn a long-run economic profit.

b.

firms in perfect competition take full advantage of economies of scale in long-run equilibrium, whereas firms

in monopolistic competition do not take advantage of economies of scale in long-run equilibrium.

c.

firms in perfect competition can easily exit the market, whereas firms in monopolistic competition find it

difficult to exit the market.

d.

firms in perfect competition face a downward-sloping demand curve, whereas firms in monopolistic

competition face a horizontal demand curve.

e.

there are many firms in a perfectly competitive market, whereas there are a few firms in a monopolistically

competitive market.

97. Which of the following characteristics do firms in perfect competition have in common with firms in monopolistic

competition?

a.

Firms in both markets are price takers.

b.

Firms in both markets produce homogeneous products.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

c.

Firms in both markets face competition from new entrants.

d.

Firms in both markets face a horizontal demand curve.

e.

Firms in both markets advertise their products.

98. Compared to a firm in perfect competition, a monopolistically competitive firm tends to:

a.

produce less and charge a higher price.

b.

produce less and charge a lower price.

c.

produce more and charge a lower price.

d.

produce more and charge a higher price.

e.

produce the same quantity.

99. Which of the following is a unique feature of perfect competition?

a.

The individual firm cannot earn economic profit in the long run.

b.

It is easy for new firms to enter the industry.

c.

The market demand curve slopes downward.

d.

The demand curve facing an individual firm is perfectly elastic.

e.

The firms in the industry produce a homogeneous product.

100. Firms in monopolistic competition and perfect competition typically:

a.

are price takers.

b.

produce identical products.

c.

earn zero economic profit in the long run.

d.

face a downward-sloping demand curve.

e.

face an upward-sloping total revenue curve at all rates of output.

101. Which of the following characteristics distinguishes oligopoly from other market structures?

a.

A horizontal demand curve

b.

A downward-sloping demand curve

c.

The production of homogeneous products

d.

The production of differentiated products

e.

Interdependence among firms in the industry

102. An oligopoly consists of:

a.

a few independent firms.

b.

a few interdependent firms.

c.

many interdependent firms.

d.

many independent firms.

e.

only one firm.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

103. The automobile, breakfast cereal, and tobacco industries are examples of:

a.

monopolistic competition.

b.

oligopolies.

c.

perfect competition.

d.

monopolies.

e.

monopsonies.

104. Oligopolists are more sensitive to the pricing and output policies of their rivals when:

a.

all firms produce identical products.

b.

their products are highly differentiated.

c.

there is freedom of entry and exit.

d.

there are barriers to entry.

e.

there are many firms in the industry.

a

105. It is harder to explain the behavior of firms in an oligopoly than in other market structures because:

a.

the firms act independently of each other in an oligopoly.

b.

firms base their decisions on what their rivals do.

c.

only differentiated products are produced by firms in an oligopoly.

d.

only homogeneous products are produced by firms in an oligopoly.

e.

the demand curve faced by a firm in an oligopoly can slope upward.

106. An oligopoly is characterized by:

a.

a few firms, which have control over market price.

b.

many firms and some barriers to entry.

c.

a large number of firms and no barriers to entry.

d.

a single firm and no barriers to entry.

e.

a single firm and significant barriers to entry.

a

107. If Ford raises the price of its automobiles, the demand curve for GM automobiles:

a.

shifts to the left.

b.

remains unaffected.

c.

becomes more elastic.

d.

shifts to the right.

e.

becomes vertical.

108. Which of the following is not considered a barrier to entry?

a.

Economies of scale

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

b.

Patents

c.

Control of a scarce resource

d.

Licensing

e.

Perfect price discrimination

e

109. In an oligopoly, the demand curve facing an individual firm depends upon the:

a.

behavior of competing firms.

b.

shape of the firm’s average total cost curve.

c.

shape of the firm’s marginal cost curve.

d.

firm’s supply curve.

e.

shape of the firm’s average variable cost curve.

a

110. Interdependent decision making on price, quality, or advertising is a characteristic of:

a.

perfect competition.

b.

monopolies.

c.

oligopolies.

d.

monopolistic competition.

e.

a monopsony market.

c

111. Which of the curves shown in Figure 10.6 represents the long-run average cost curve for an oligopolist?

Figure 10.6

a.

Curve a

b.

Curve b

c.

Curve c

d.

Curve d

e.

Curve e

112. A firm experiences economies of scale if:

a.

average cost declines as output increases.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

b.

marginal cost declines as output increases.

c.

total cost increases as output increases.

d.

average returns decline as output increases.

e.

marginal revenue increases as output increases.

113. The automobile industry is an example of a(n):

a.

monopolistically competitive market because firms in the automobile industry face an upward-sloping demand

curve.

b.

monopolistically competitive market because it experiences economies of scale.

c.

monopolistically competitive market for legal reasons.

d.

an oligopoly because each firm must produce a large amount of output before it can achieve low average costs.

e.

an oligopoly for legal reasons.

114. A firm _____is likely to be an oligopolist.

a.

that faces a horizontal demand curve

b.

that maximizes profit by producing a level of output at which marginal revenue exceeds marginal cost

c.

that produces a significant share of market output before low average costs can be achieved

d.

that acts as a price taker

e.

that earns zero economic profit in the long run

115. Which of the following is most likely to act as a barrier to entry in an oligopoly?

a.

The profit earned by existing firms in the short run

b.

Poorly defined property rights

c.

A well-established brand name

d.

A high price charged for the products

e.

A fall in the output produced by firms

116. Zara is the largest fashion retailer in Europe. Which of the following is not likely to be a barrier to entry into the

apparel industry that protects Zara’s market power?

a.

The development of a new item within two weeks, as opposed to an industry average of nine months

b.

The availability of 10,000 new designs a year

c.

A well-established brand name

d.

Low expenditure on advertising

e.

The distribution of new fashions more frequently compared to other firms in the industry

117. If a leading canned soup company introduces dozens of new flavors in order to dominate shelf space, the company is

most likely trying to create a barrier to entry by:

a.

increasing the total investment needed to reach the minimum efficient size.

b.

spending more on advertising than potential competitors can afford.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

c.

exploiting economies of scale.

d.

crowding out new entrants.

e.

establishing an undifferentiated oligopoly.

118. In which of the following ways do oligopolies compete with existing rivals and block new entries?

a.

By offering a variety of products

b.

By increasing the price of their products

c.

By reducing the quantity of output produced

d.

By increasing the wages paid to workers

e.

By producing homogeneous products

119. Suppose an established manufacturer in an oligopoly market introduces 10 new varieties of products in the same

year. Which of the following is a possible outcome of this action?

a.

It will lead to a fall in the profit earned by the firm.

b.

It will crowd out new entrants into the market.

c.

It will reduce the startup cost for a new entrant.

d.

It will help the manufacturer increase the price for its products.

e.

It will lead to a decrease in the demand for the products of the manufacturer.

120. If a firm in an industry achieves the minimum efficient scale at a low cost, then:

a.

competition in the industry is likely to decrease.

b.

competition in the industry is likely to increase.

c.

the price charged by the firm is likely to be high.

d.

the demand for the firm’s product is likely to be less.

e.

the profit earned by the firm is likely to be high.

121. A cartel’s marginal cost curve is the:

a.

highest of all the individual firms’ marginal cost curves.

b.

lowest of all the individual firms’ marginal cost curves.

c.

horizontal sum of all the individual firms’ marginal cost curves.

d.

same as the market supply curve.

e.

same as the marginal cost curve faced by all firms in the market.

122. A cartel’s profit-maximizing quantity occurs where the cartel’s:

a.

marginal cost equals marginal revenue.

b.

marginal cost equals its average cost.

c.

price is highest.

d.

cost is lowest.

e.

demand curve has a kink.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a

123. A cartel is:

a.

a group of oligopolistic firms that engage in collusion.

b.

a group of monopolistically competitive firms that charge the same price.

c.

usually legal in the United States.

d.

an agreement among rival firms to set prices independently.

e.

illegal throughout the world.

a

124. Identify a statement that is true of a cartel.

a.

In a cartel, all firms produce the same amount of output and earn the same profit.

b.

In a cartel, all firms produce the same amount of output but earn different amounts of profit because their costs

differ.

c.

In a cartel, firms produce different amounts of output but earn the same profit.

d.

In a cartel, firms with higher average costs produce more so that all firms earn the same profit.

e.

In a cartel, firms with lower average costs often earn higher profits.

e

125. Which of the following helps make a cartel successful?

a.

Equal costs across firms

b.

Differentiated output

c.

Highly variable cost conditions across firms

d.

Highly variable demand conditions

e.

Rapidly changing technology

a

126. To maximize cartel profit, members must allocate output so that the marginal cost for the final unit produced by each

firm is:

a.

identical.

b.

unequal.

c.

negative.

d.

equal to the firm’s average total cost.

e.

maximized.

a

127. The chances of successful collusion are greatest when:

a.

firms are producing differentiated products.

b.

there are many firms in the industry.

c.

there are both small firms and large firms in the same industry.

d.

demand curves and cost curves are similar across firms in an industry.

e.

demand is falling.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

128. Collusion is easier to achieve and maintain when:

a.

there are many firms in the industry.

b.

the firms’ products are homogeneous.

c.

the firms’ cost structures are very different.

d.

there are very weak barriers to entry.

e.

the industry is located in the United States.

129. Tacit collusion occurs in industries that:

a.

are monopolistically competitive.

b.

have price leaders.

c.

experience rapid technological change.

d.

are regulated.

e.

produce public goods.

130. Which of the following hinders successful price leadership?

a.

Large economic profits earned by existing firms in a market

b.

Product differentiation among sellers

c.

The tendency of firms to follow the pricing decision of a rival

d.

The production of homogeneous goods by sellers

e.

Transparency in price coordination

131. Historically, the U.S. steel industry has been a good example of _____.

a.

monopolistic competition

b.

a cartel

c.

a pure monopoly

d.

an oligopoly with a kinked demand curve

e.

the price-leadership model of oligopoly

132. During certain periods in the past few decades, if one of the three major breakfast cereal producers in the United

States announced a price increase, the other two announced a similar price increase. This implies that the market for

breakfast cereals is a good example of _____.

a.

monopolistic competition

b.

a cartel

c.

a pure monopoly

d.

the kinked-demand-curve model of oligopoly

e.

the price-leadership model of oligopoly

133. The use of game theory in studying the behavior of firms in an oligopoly implies that firms:

a.

will be successful in colluding to raise prices.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

b.

follow suit when one firm raises its price.

c.

will match other firms’ price cuts but will not react to the other firm’s price increases.

d.

may attempt to avoid the worst outcome but may achieve a less-than-optimal outcome.

e.

are usually unable to avoid the worst outcome.

134. One common assumption when game theory is used to study firms in an oligopoly is that firms:

a.

try to avoid the worst outcome.

b.

try to achieve the best outcome.

c.

minimize losses.

d.

always cooperate.

e.

always compete.

135. Game theory focuses on:

a.

strategic behavior among interdependent firms.

b.

professional athletic events.

c.

competition between the players in board games.

d.

competition between those in the political arena and those in the market place.

e.

the interaction between firms in a competitive industry and those in a non-competitive industry.

136. The outcome of a game among oligopolists is dependent upon:

a.

the predicted response of competitors.

b.

the existence of a perfectly inelastic market demand curve.

c.

costs of production being constant.

d.

economies of scale in production.

e.

marginal revenue being equal to marginal cost.

137. The prisoner’s dilemma is a situation in which:

a.

players have difficulty in choosing a strategy based on trust.

b.

a firm’s competitors ignores its action while making their own decisions

c.

oligopolists behave irrationally.

d.

oligopolists attempt to maximize sales rather than profits.

e.

an oligopolist’s demand curve becomes perfectly inelastic.

138. The principal advantage of the game theory approach is that it allows to:

a.

take all possible information into consideration before developing a theory.

b.

better understand why firms in a competitive industry avoid games.

c.

better understand how the government should regulate a natural monopoly.

d.

better understand decision making when one person’s choices affect another person’s choices.

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

e.

understand the relationship between the demand curves faced by a firm and the industry as a whole.

139. The term “strategy” in terms of game theory refers to:

a.

the tendency of firms to earn zero economic profit in the long run.

b.

the tendency of firms in an oligopoly to exit the market in the long run.

c.

each firm’s game plan for making decisions.

d.

each firm’s decision to charge a higher price than the price charged by the rival firm in an industry.

e.

the tendency for collusive firms to generate normal profits.

140. Game theory is most useful in understanding the decision-making behavior of firms in _____.

a.

perfect competition

b.

a command economy

c.

monopolistic competition

d.

a closed economy

e.

an oligopoly

141. The advantage of game theory is that it allows us to focus on:

a.

each firm’s incentives to cooperate or not to cooperate.

b.

the relationship between business and ethics in a market

c.

the costs and benefits of government regulation in a market.

d.

the market share of each firm in a market.

e.

each firm’s incentive to charge a higher price for its product.

142. A payoff matrix is a list that shows:

a.

the price of each good a firm sells.

b.

the rewards and penalties associated with pursuing various strategies.

c.

the cost of production incurred by each firm in an industry.

d.

the quantity of resources owned by each firm in an industry.

e.

the revenue earned by each firm in an industry.

143. The dominant-strategy equilibrium in a game implies that each firm:

a.

ignores the reactions of competitors.

b.

colludes with competitors to maximize industry profits.

c.

ignores the decisions of the other firms.

d.

takes all potential bits of information into consideration before making a decision.

e.

selects the optimal solution to a game.

144. The tit-for-tat strategy implies that firms:

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

will ignore the strategy of the dominant firm if it involves decreases in prices.

b.

will follow the lead of the dominant firm in making pricing decisions.

c.

will change the price of their products whenever fixed cost changes.

d.

cooperate on the first round and then follow the competitor’s reactions in the second round.

e.

will change the price of their products only if demand changes.

145. In a coordination game, a Nash equilibrium occurs when:

a.

each player ignores the strategy of the other player.

b.

each player chooses no strategy, but maintains the status quo.

c.

each player chooses the same strategy.

d.

one player can improve the outcome by changing his strategy.

e.

each player chooses different strategies.

146. If oligopolists engaged in some sort of collusion, industry output would be _____ and the price would be _____ than

under perfect competition.

a.

smaller; lower

b.

smaller; higher

c.

smaller; no different

d.

greater; lower

e.

greater; higher

147. Firms with market power offer differentiated products in order to:

a.

lower costs of production.

b.

increase profits.

c.

support their contractors in low-wage countries.

d.

fill up costly warehouses.

e.

increase social welfare.

148. Differentiate between perfect competition and an oligopoly?

a.

Firms in an oligopoly earn economic profit in the long run, whereas firms in perfectly competitive market earn

zero economic profit in the long run.

b.

Firms in an oligopoly charge a lower price than firms in a perfectly competitive market.

c.

Firms in an oligopoly face horizontal demand curves, whereas firms in a perfectly competitive market face

downward-sloping demand curves.

d.

An oligopoly is characterized with low barriers to entry, whereas a perfectly competitive market is

characterized with high barriers to entry.

e.

There are many firms in an oligopoly, whereas there are only a few firms in a perfectly competitive market.

149. Which of the following is true of oligopolists?

Name:

Class:

Date:

Chapter 10: Monopolistic Competition and Oligopoly

a.

Oligopolists earn comparatively higher profits than perfectly competitive firms due to economies of scale.

b.

Oligopolists earn comparatively lower profits than perfectly competitive firms due to economies of scale.

c.

Oligopolists produce homogeneous products.

d.

Oligopolists face horizontal demand curves.

e.

Oligopolists charge comparatively lower prices for their products than firms in a perfectly competitive market.

150. An oligopoly firm that _____ will earn long-run economic profit.

a.

enjoys huge brand loyalty

b.

spends less on advertisement

c.

charges a higher price for its product

d.

incurs high cost to achieve the minimum efficient scale

e.

charges a low price for its product