5. Some economists argue that a government-created monopoly in the medical field can be good for

the overall growth of an economy, even though it does create deadweight loss. Support this

argument.

6. Explain the price effect and the output effect as it pertains to the marginal revenue of a monopolist.

7. Julee has estimated the demand and marginal revenue for her product. They are P = 100 − 2Q

(quantity) and MR = 100 − 4Q, respectively. She also experiences constant marginal cost of $16.

a. Does Julee have any market power? How can you tell?

b. What is Julee’s profit-maximizing quantity?

c. What price should Julee charge at that profit-maximizing quantity?

8. Using a graph, show a situation in which a monopolist is incurring short-run losses. Explain how

this is possible.

9. Explain a situation in which, when holding costs constant, a monopolist that was earning economic

profits in the past can later incur an economic loss.

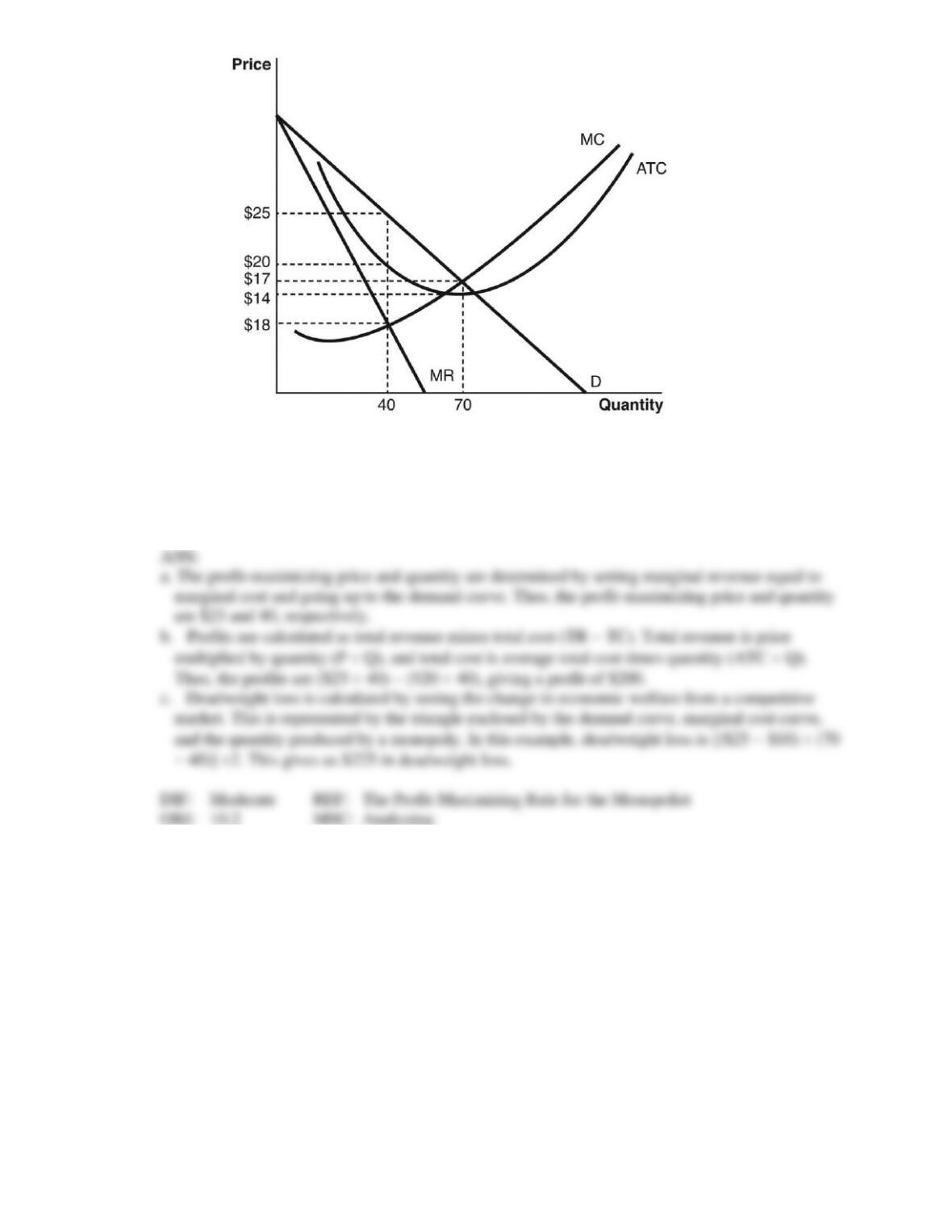

10. Answer the following questions based on the accompanying graph.

a. What is the profit-maximizing price and quantity?

b. At the profit-maximizing price and quantity, what are the total profits or losses made by this

firm?

c. At the profit-maximizing price and quantity, what is the approximate deadweight loss incurred

by society?

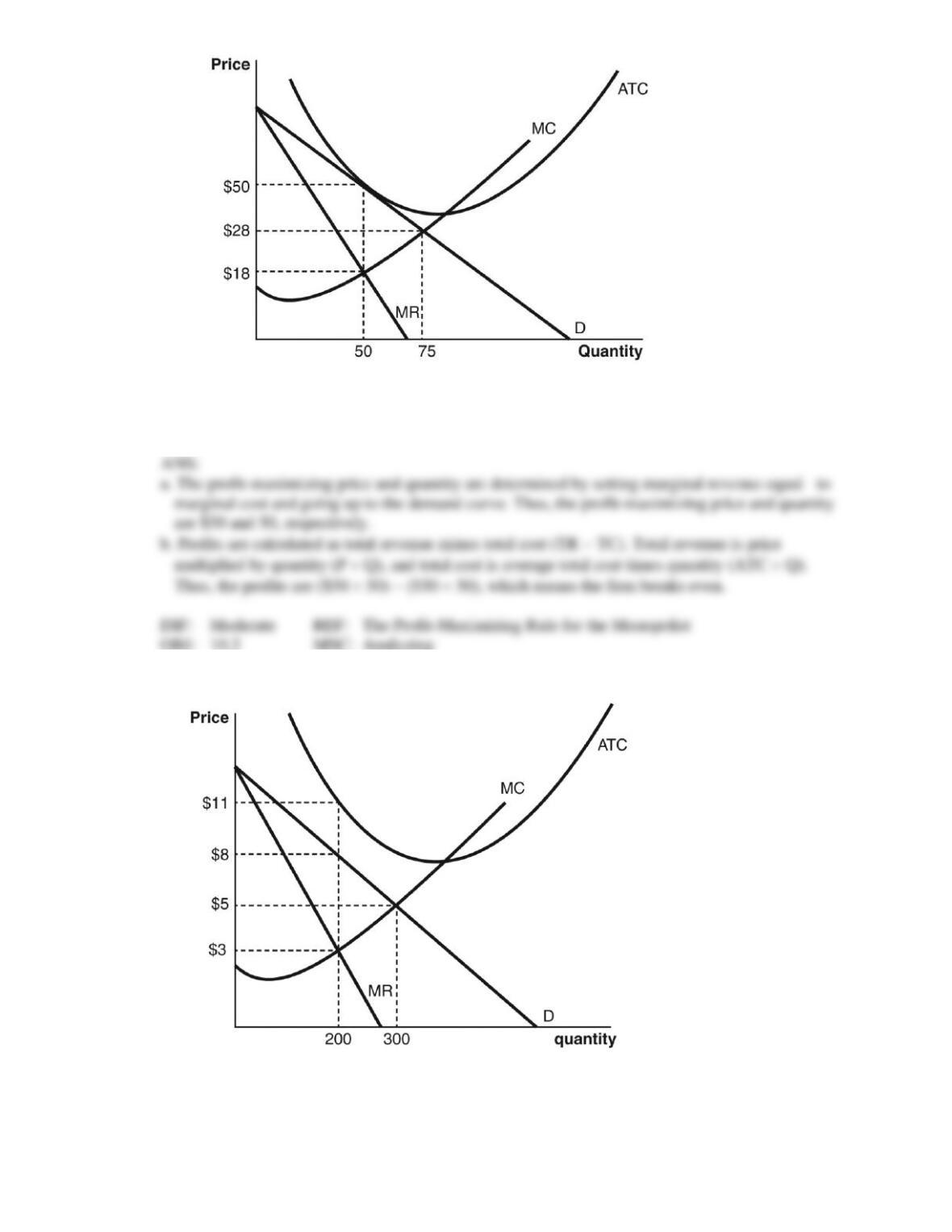

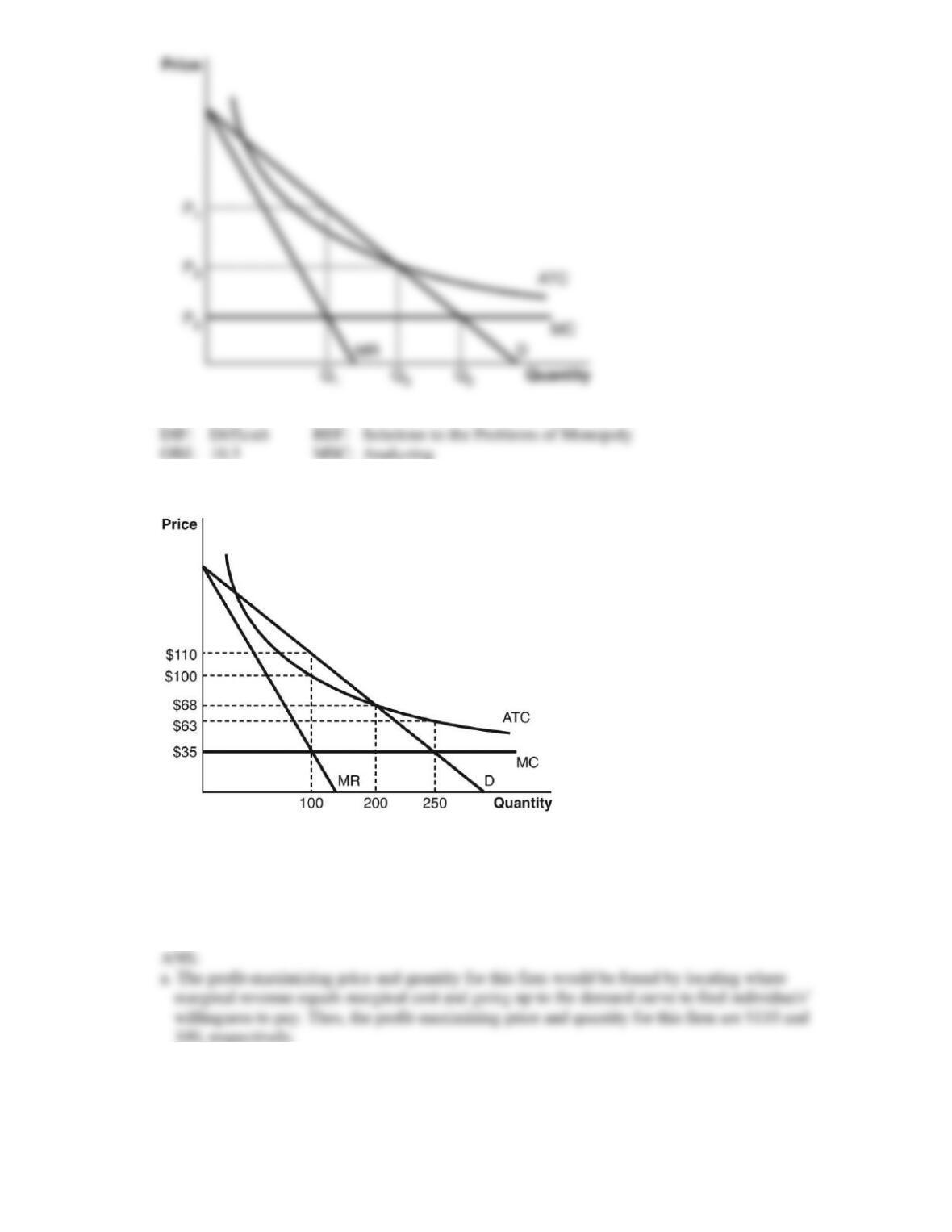

11. Answer the following questions based on the accompanying graph.

a. What are the profit-maximizing price and quantity?

b. At the profit-maximizing price and quantity, what are the total profits or losses made by this

firm?

12. Answer the following questions based on the accompanying graph.

a. What are the profit-maximizing price and quantity?

b. At the profit-maximizing price and quantity, what are the total profits or losses made by this

firm?

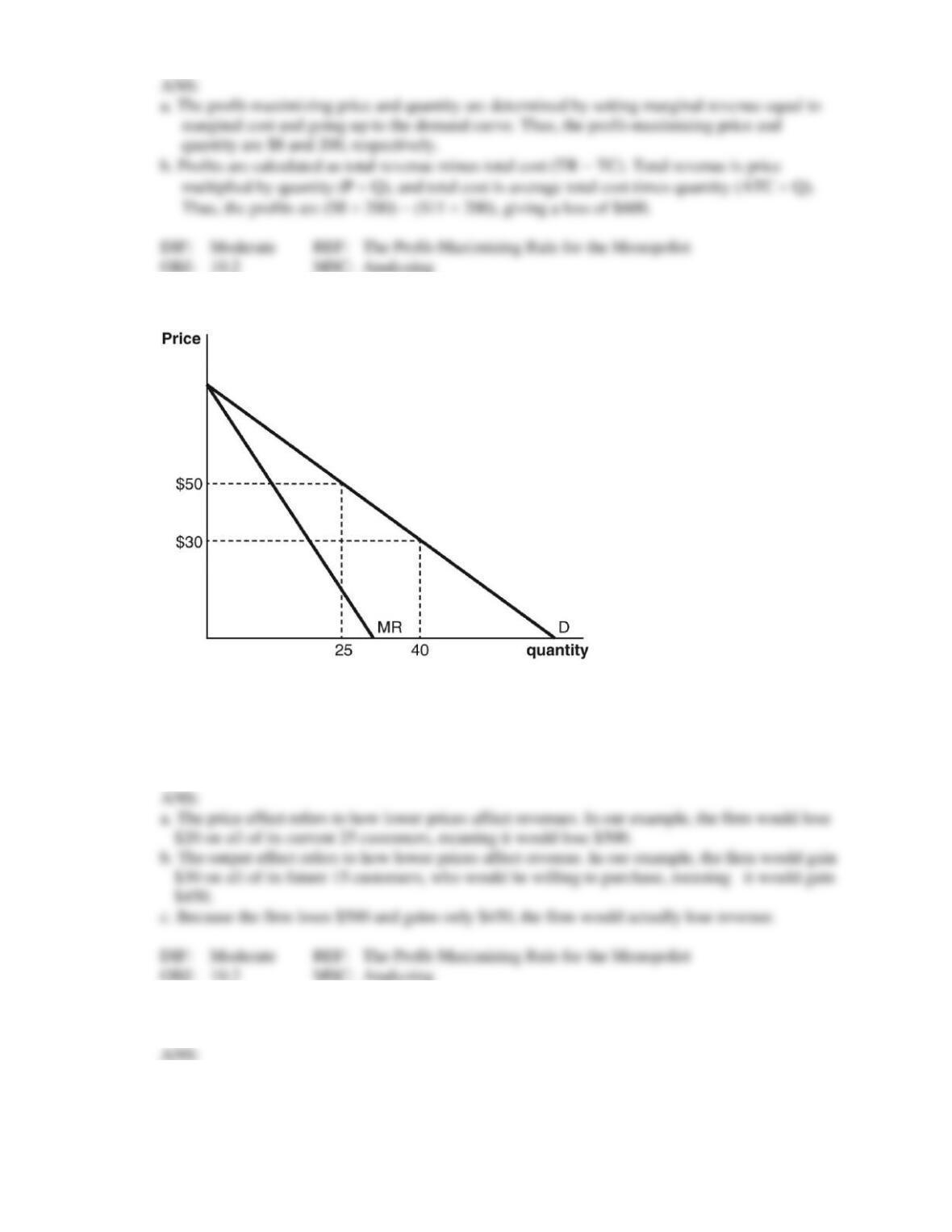

13. Answer the following questions based on the accompanying graph.

a. What is the change in revenues associated with the price effect for this firm when the price

decreases from $50 to $30?

b. What is the change in revenues associated with the output effect for this firm when the price

decreases from $50 to $30?

c. Would the firm gain revenue if it lowered the price from $50 to $30? Explain.

14. Using a graph, explain the concepts of the price effect and output effect.

15. Make the case for government regulation of high-speed Internet service, using the concept of

elasticity of demand.

16. Joseph owns the only ice cream shop in a small town outside Mobile, Alabama. According to the

accompanying table, which shows production and costs for Joseph’s ice cream shop, answer the

following questions.

Price Quantity Fixed Cost Variable Cost

$8 0 $3 $0

$7 1 $3 $2

$6 2 $3 $4

$5 3 $3 $7

$4 4 $3 $12

$3 5 $3 $20

a. By using the profit-maximizing rule, what is the quantity Joseph should produce to maximize his

profits?

b. By using the profit-maximizing rule, what is the price Joseph should set to maximize his profits?

c. At the price and quantity you found, what is the profit Joseph makes?

17. Draw a figure to illustrate how the emergence of a monopoly leads to deadweight loss for society

as a whole, and explain the circumstances that fix the amount of that deadweight.

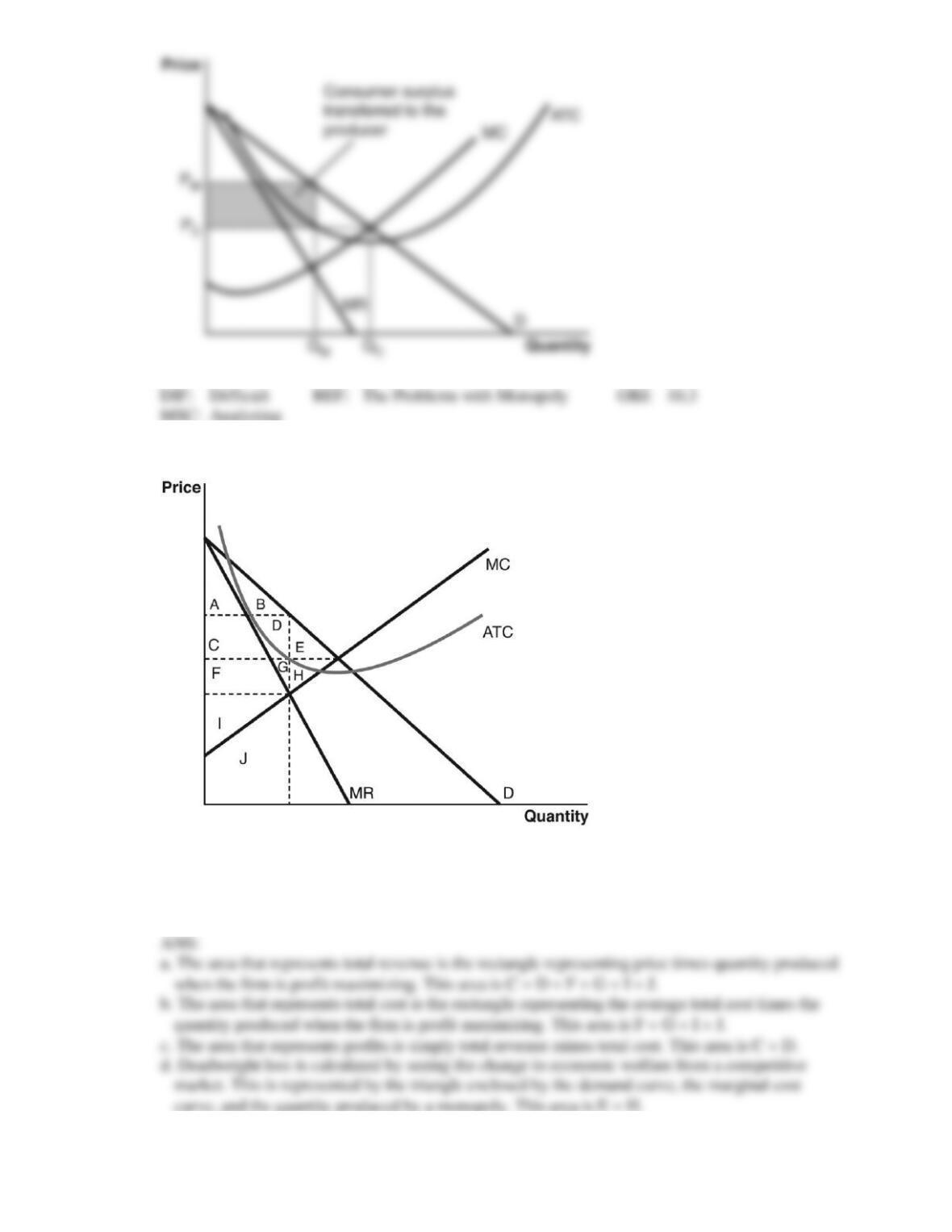

18. When a competitive market is controlled by a monopolist, part of consumer surplus gets

transferred to producer surplus. Show this area on a graph.

19. Answer the following questions based on the accompanying graph.

a. What area(s) of the graph represent(s) total revenue for this firm if it was profit maximizing?

b. What area(s) of the graph represent(s) total cost for this firm if it was profit maximizing?

c. What area(s) of the graph represent(s) profits for this firm if it was profit maximizing?

d. What area(s) of the graph represent(s) deadweight loss if the firm was profit maximizing?

20. In the year 2576, intergalactic travel is possible. A firm on Earth, Plantorium, produces 95 percent

of Earth’s jetpacks. A planet with easy access to Earth, Xerckyia, is coming out with new

technology that will allow it to produce jetpacks at a lower cost. Describe a scenario in which

Plantorium will engage in rent seeking.

21. How did AT&T’s position in the market for telephone service evolve from 1980 to the present?

22. Explain why it is unrealistic to regulate a natural monopoly for a price and quantity that maximizes

total economic surplus in society.

23. Draw graphs of a normal monopoly and a natural monopoly and discuss their differences.

24. Draw a graph of a typical natural monopoly. Label the profit-maximizing price and quantity P1 and

Q1, respectively. Also label the price and quantity that will maximize total economic welfare P2

and Q2, respectively. Label the price and quantity that cause the firm to break even P3 and Q3,

respectively.

25. Answer the following questions based on the accompanying graph.

a. What is the profit-maximizing price and quantity for this firm?

b. What is the price and quantity combination that creates the greatest economic welfare for

society? At this price and quantity, is the firm making a profit or a loss?

c. What will the firm do if it is incurring a loss? What is the lowest price the government could

force the firm to charge?