The outside lags related to monetary policy tend to be quite long.

A decrease in the population of an economy is likely to lead to lower wages and a lower

quantity of labor used.

If the net international investment position of the U.S. equals $100 billion, this means

Americans hold $100 billion worth of foreign issued assets.

Technological progress means that we produce more output with the same amount of

inputs.

Disposable income is equal to total income minus net taxes.

Suppose the actual budget deficit remains unchanged when the economy falls into a

recession. This is an indication that

A) monetary policy was not used during the recession.

B) fiscal policy was not used during the recession.

C) monetary policy was used during the recession.

D) fiscal policy was used during the recession.

The presence of automatic stabilizers means that the federal budget deficit is ________

than it otherwise would be in a recession and ________ than it otherwise would be in

an expansion.

A) larger; smaller

B) smaller; larger

C) smaller; smaller

D) larger; larger

The speculative demand for money is:

A) positively related to income.

B) positively related to the interest rate.

C) negatively related to the interest rate.

D) negatively related to income.

The price of compact discs has fallen dramatically. Which of the following is likely to

happen?

A) The quantity supplied of compact discs will decrease.

B) The quantity supplied of compact discs will increase.

C) The supply of compact discs will decrease.

D) The supply of compact discs players will increase.

Recall Application 4, “Securitization: the Good, the Bad, and the Ugly,” to answer the

following questions:

According to the Application, ‘subprime” loans are loans that are:

A) offered to borrowers who would not qualify for loans using traditional criteria.

B) sold to the U.S. Treasury.

C) offered below prime interest rates.

D) low risk bonds sold to homeowners to finance their mortgages.

The production possibilities curve represents the set of all:

A) feasible combinations of goods given that a nation’s resources are fully employed.

B) factors of production that can be used to manufacture goods and services.

C) combinations of goods and services that can be used in the production of other goods

and services.

D) nonlinear forms of production in the economy.

The economy is in a recession and the housing market is in a slump. As a result of this,

a real estate firm lays off half of its real estate agents. This is an example of:

A) frictional unemployment.

B) structural unemployment.

C) cyclical unemployment.

D) natural unemployment.

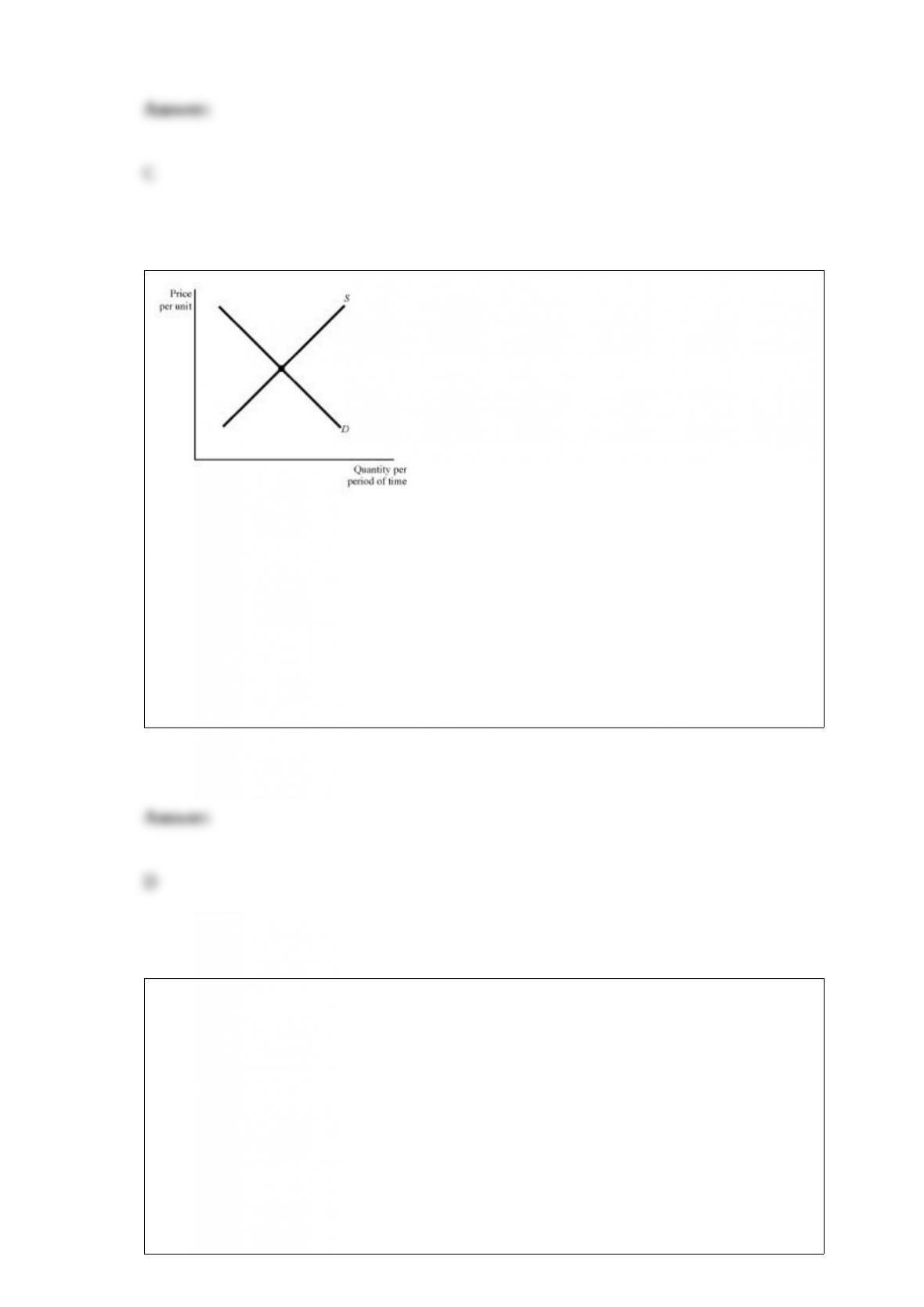

Figure 4.7 If demand falls in Figure 4.7, then the equilibrium:

A) price and quantity rise.

B) price rises and quantity falls.

C) price falls and quantity rises.

D) price and quantity fall.

Suppose that ramen noodles are an inferior good. When income increases, the

equilibrium quantity of ramen noodles will ________ and the equilibrium price of

ramen noodles will ________.

A) rise; rise

B) rise; fall

C) fall; rise

D) fall; fall

In the United States during the 1930s

A) government spending and taxes both increased, resulting in zero net fiscal

expansion.

B) government spending and taxes both decreased, resulting in a net fiscal contraction.

C) government spending increased and taxes decreased, resulting in a fiscal expansion.

D) government spending decreased and taxes increased, resulting in a fiscal contraction.

Since 1973, in the United States wages of skilled workers have:

A) risen more slowly than those of unskilled workers.

B) fallen due to foreign trade.

C) remained constant.

D) risen faster than those of unskilled workers.

Suppose George withdraws $60,000 from his bank. If the reserve ratio is 25 percent,

then this transaction will lead to a decrease of ________ in checking account balances.

A) $15,000

B) $45,000

C) $90,000

D) $180,000

Suppose the nation of Alphonia was charged with dumping electric lawnmowers in the

nation of Omegalon. The two reasons a nation like Alphonia would dump products in

another nation are

A) price discrimination and import licensing.

B) outsourcing and predatory pricing.

C) price discrimination and predatory pricing.

D) import licensing and outsourcing.

Additional Application INFLATION-INDEXED BONDS IN THE UNITED

STATES

Are there bonds that can protect your investments from inflation? In 1997, the U.S.

Department of the Treasury created a new financial instrument called the Treasury

Inflation-Protected Security, or TIPS. The key feature of TIPS is that the payments to

investors adjust automatically to compensate for the actual changes in the Consumer

Price Index. Therefore, TIPS provide protection to investors from inflation. Like other

government bonds, TIPS make interest payments every six months and a payment of

the original principal when the bond matures. However, unlike other Treasury bonds,

these payments are automatically adjusted for changes in inflation. Despite their

obvious attractions, the market for TIPS is still rather small. As of 2005, there were

about $200 billion in TIPS outstanding, compared to a total volume of about $4 trillion

($4,000 billion) total Treasury obligations. Because TIPS compensate for actual

inflation, the interest rate on these bonds differs from conventional bonds by the

expected inflation rate. By comparing the interest rates on TIPS to other government

bonds of similar maturity, economists can estimate the public’s expectations of inflation.

SOURCE: Simon Kwan, “Inflation Expectations: How the Market Speaks,” Federal

Reserve Bank of San Francisco Economic Letter, October 7, 2005. According to the

application, the difference between the interest rates on TIPS and the interest rates on

non-inflation indexed securities represents:

A) the public’s expectation of inflation in the future.

B) the public’s expectation of inflation in today.

C) the government’s expectation of inflation in the future.

D) the Fed’s expectation of inflation in the today.

A normal good is defined as a good for which demand decreases when:

A) the price increases.

B) income increases.

C) the price decreases.

D) income decreases.

Table 11.1

Refer to Table 11.1. If the marginal propensity to consume decreases to 0.05 (MPC =

0.05), what is the new equilibrium level of output?

A) 2,366.67

B) 3,166.67

C) 3,550.00

D) 4,750.00

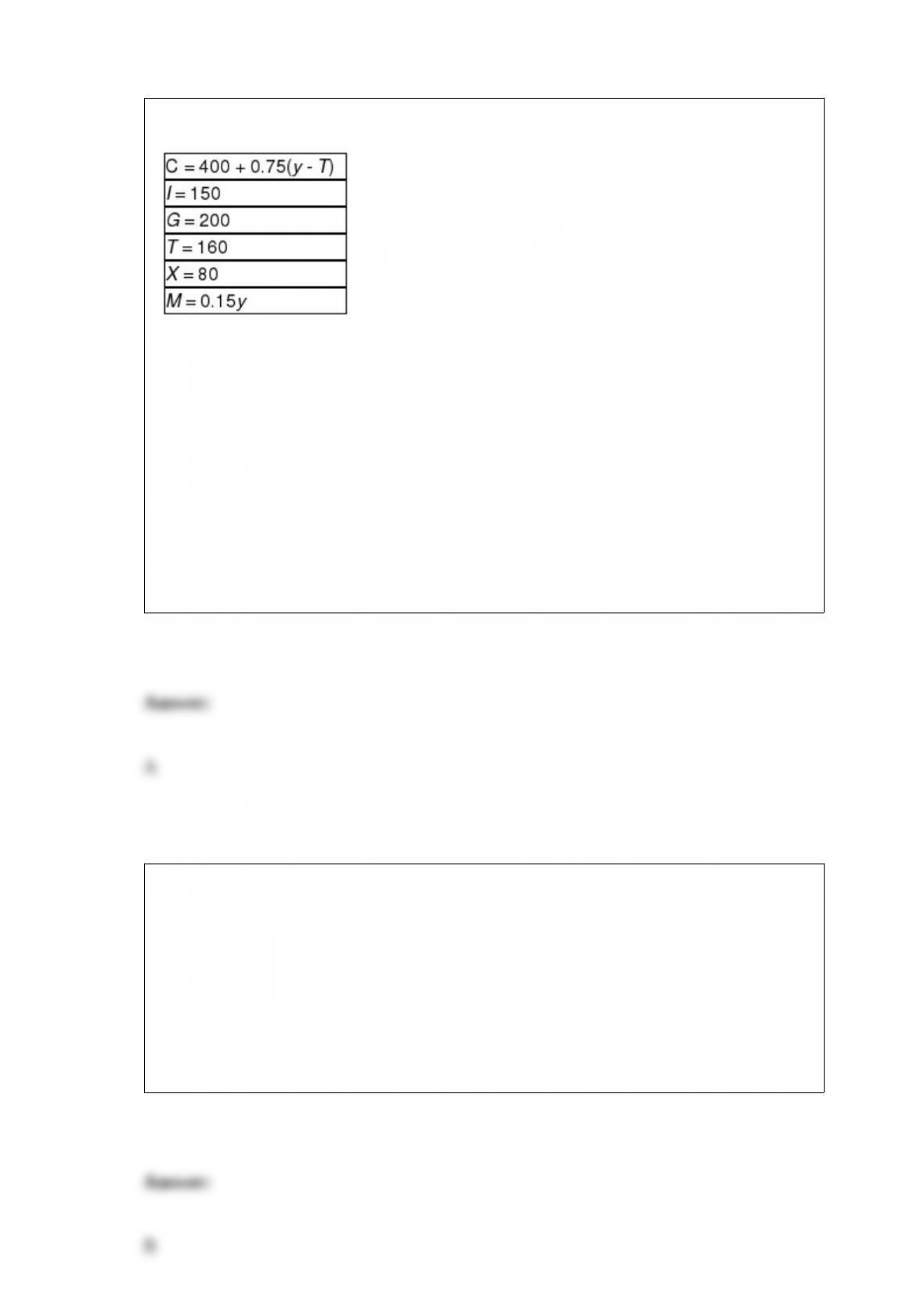

In the consumption function C = Ca + bY, the term represents:

A) the multiplier effect.

B) the marginal propensity to consume.

C) the autonomous consumption spending.

D) the marginal propensity to save.

What did Keynes mean by the phrase “animal spirits”? Why do these ‘spirits” make

investment a volatile component of GDP?

List two arguments against the passage of a balanced budget amendment.

Why are the heads of central banks typically very conservative and constantly warning

about the dangers of inflation?

Describe the adjustment process of returning an economy to full employment when

output is below full employment levels.

Use the supply and demand model to explain why it is difficult to find an on-campus

parking space during peak mid-day times, although it is much easier to find a parking

space during less popular evening hours.