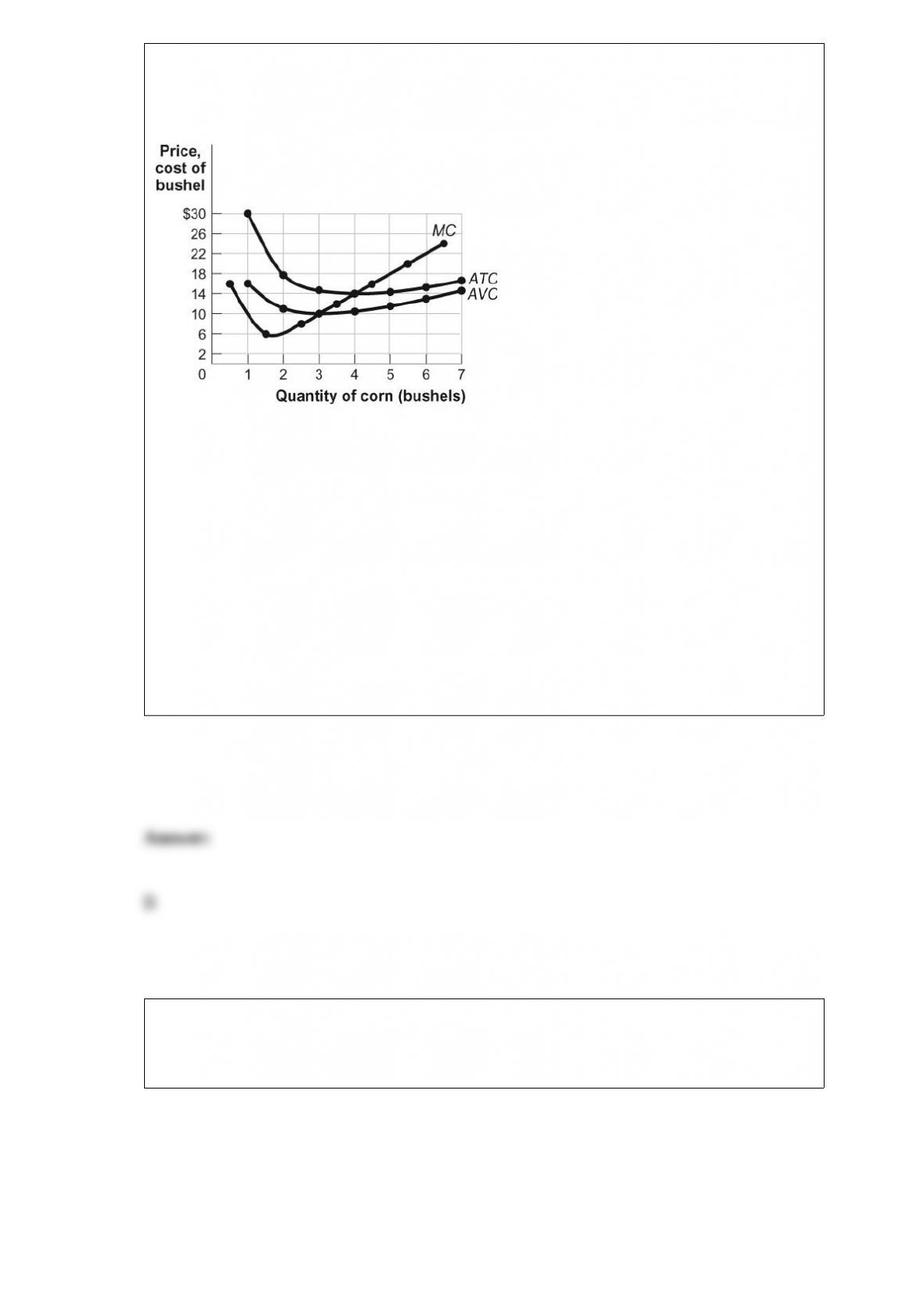

Figure: Cost Curves for Corn Producers

(Figure: Cost Curves for Corn Producers) Look at the figure Cost Curves for Corn

Producers. The market for corn is perfectly competitive. If the price of a bushel of corn

is $4, in the short run the farmer will produce _____ bushels of corn and earn an

economic _____ equal to _____.

A) 0; loss; average fixed costs

B) 0; loss; total fixed costs

C) 3; loss; $30 per bushel

D) 3; profit; $20 per bushel

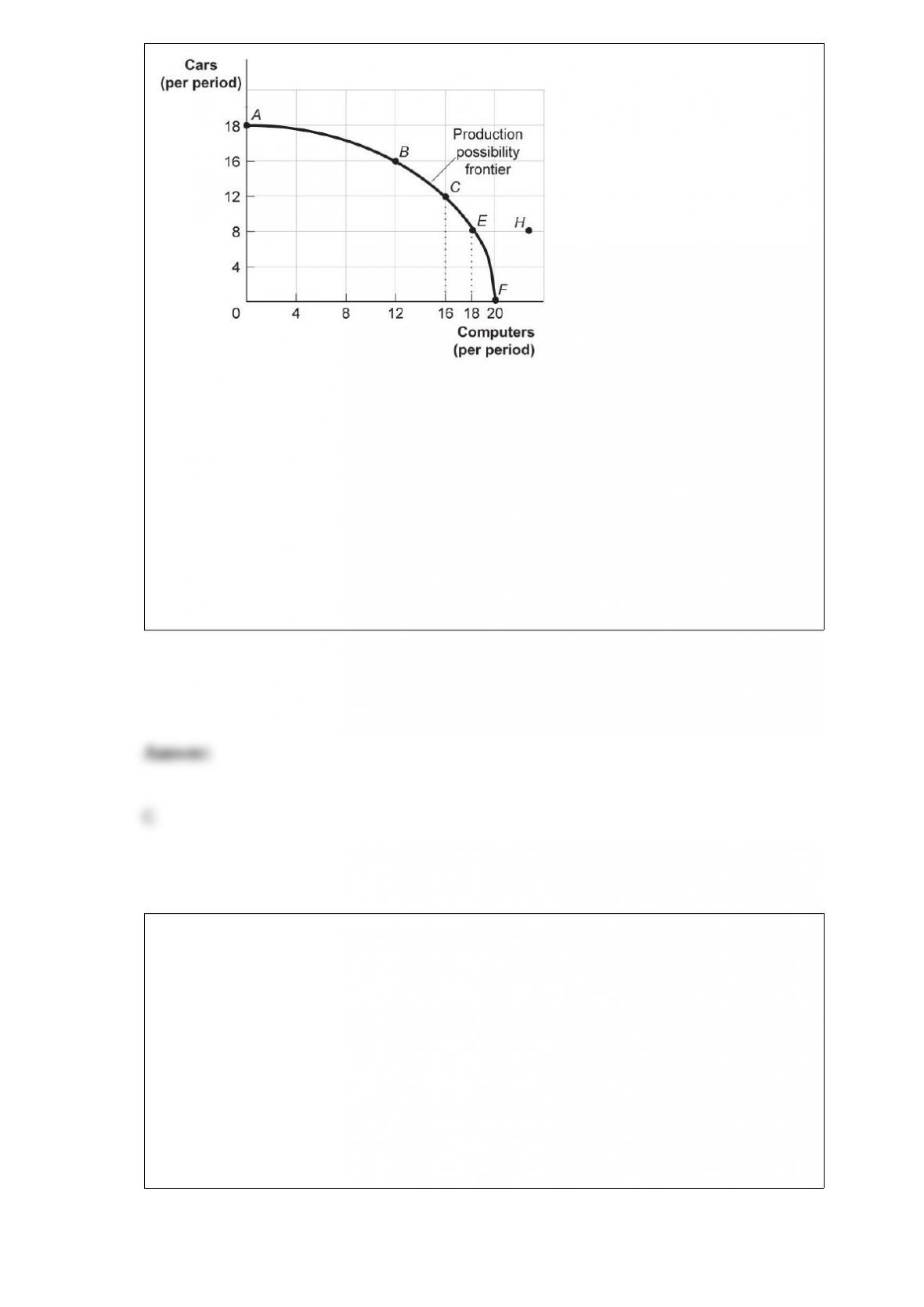

Figure: Production Possibility Frontier

(Figure: Production Possibility

Frontier) Look at the figure Production Possibilities Frontier. If the economy is

operating at point B, producing 16 cars and 12 computers per period, a decision to move

to point E and produce 18 computers:

A) indicates that you can have more computers and more cars simultaneously.

B) makes it clear that this economy has decreasing opportunity costs.

C) entails a loss of 8 cars per period.

D) entails a loss of 4 cars per period.

If the price of chocolate-covered peanuts decreases from $1.15 to $0.90 and the

quantity demanded increases from 0 bags to 400 bags, then the price elasticity of

demand (by the midpoint method) is:

A) 0.5.

B) 1.

C) 2.

D) greater than 2.

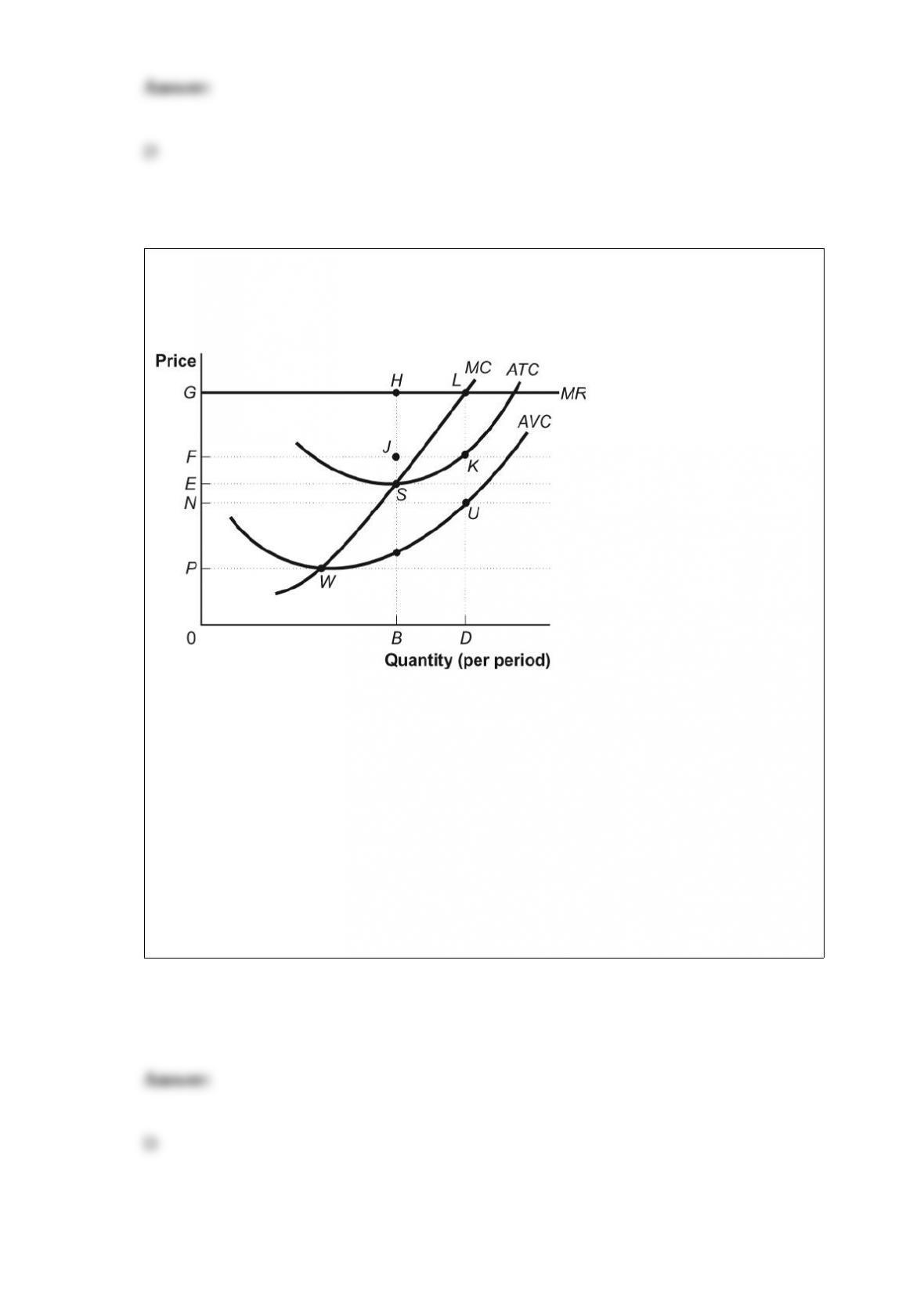

Figure: A Perfectly Competitive Firm in the Short Run

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm will produce in the short run if the price is

at least as high as point:

A) F.

B) E.

C) N.

D) P.

In a single year, Argentina can raise 100 tons of beef or produce 1,000 boxes of tulips.

In the same growing season, Venezuela can raise 50 tons of beef or produce 750 boxes

of tulips. When the two countries begin trading beef for tulips, we expect the consumer

surplus from beef consumption to:

A) fall in Argentina.

B) rise in Argentina.

C) stay the same in Argentina.

D) either rise or fall in Argentina.

The large barriers to entry are a reason a monopoly:

A) earns an economic profit in the long run.

B) produces at the minimum average total cost in the long run.

C) produces with no fixed costs in the long run.

D) maximizes its profits by producing where P = MC.

Market power in the United States was often gained in the latter part of the nineteenth

century by:

A) forming trusts.

B) the growth of competition.

C) international arrangements with Russian and Japanese firms.

D) opening up more industries to international trade.

Figure: The Demand for Bricklayers

(Figure: The Demand for Bricklayers) Look at the figure The Demand for Bricklayers.

If a shortage in the market for mortar lowers bricklayers’ productivity, then the value of

the marginal product of the eighth bricklayer will be:

A) less than $80.

B) greater than $100.

C) equal to $100.

D) greater than $80.

The U.S. production possibility frontier will _____ if there is a large influx of

working-age immigrants.

A) shift in

B) shift out

C) not change

D) The answer cannot be determined from the information provided.

A binding price ceiling is designed to:

A) keep prices below the equilibrium level.

B) increase the quality of the good.

C) prevent shortages.

D) increase efficiency.

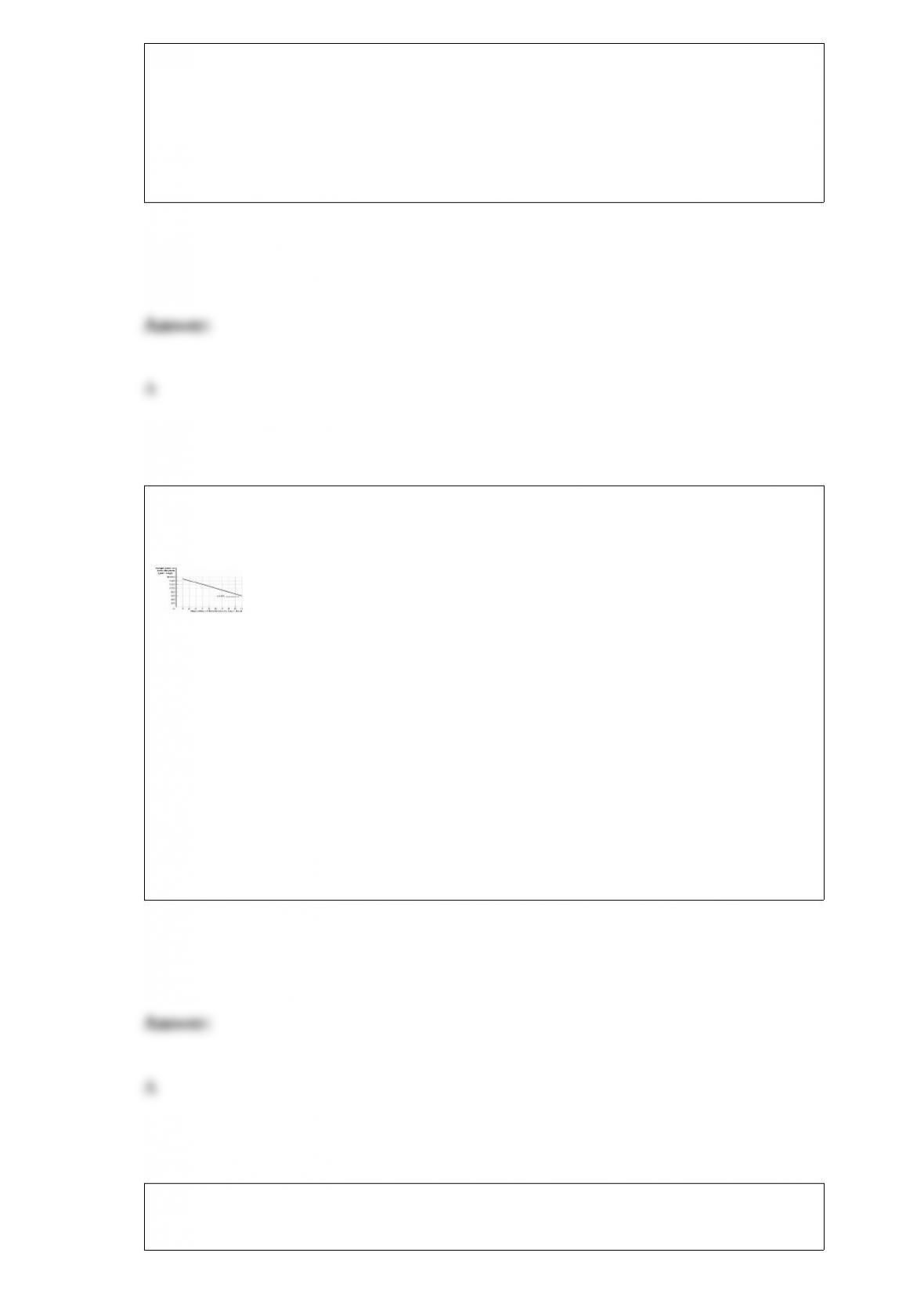

(Table: Income and Utility for Tyler) The table Income and Utility for Tyler shows the

utility Tyler receives at various income levels, but she does not know what her income

will be next year. There is a 40% chance her income will be $20,000, a 40% chance her

income will be $30,000, and a 20% chance her income will be $40,000. What is the

maximum amount of insurance Tyler would be willing to pay to guarantee an income of

$28,000?

A) $0

B) $1,484

C) $26,516

D) $126

A gas station operates in a monopolistically competitive market and is in short-run

equilibrium. Suppose that a fixed cost for this firm decreases. As a result, the firm’s

price will _____, the firm’s output will _____, and the firm’s economic profit will

_____.

A) increase; increase; increase

B) increase; increase; decrease

C) stay the same; stay the same; increase

D) decrease; stay the same; increase

Which of the following is an example of bounded rationality?

A) Ann proofreads her term paper six times.

B) Mary feels that she has studied enough to make an A+ on her economics exam but

studies another two hours just to be sure.

C) Tim studies only an hour on the morning of his economics exam because he is

satisfied just to make a passing grade.

D) Terry does his economics homework twice to be sure that he has a thorough

understanding of the topic.

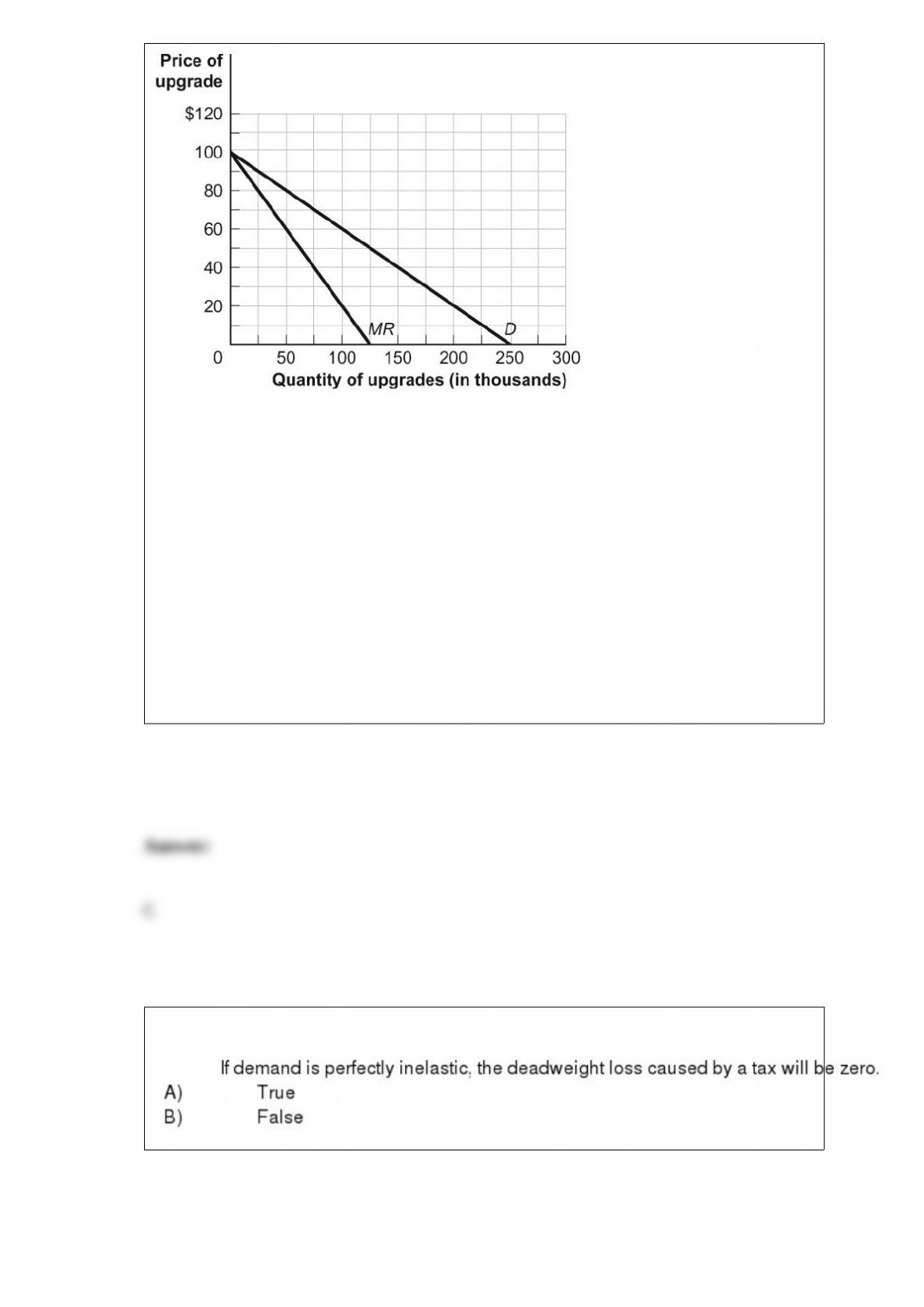

Figure: Demand and Marginal Revenue

(Figure: Demand and Marginal Revenue) The figure Demand and Marginal Revenue

refers to a software upgrade. The producer incurred fixed costs of $10 million to

produce the upgrade; the marginal cost of allowing consumers to download the upgrade

is zero. What is the deadweight loss associated with the profit-maximizing price and

quantity of the upgrade?

A) $0

B) $1.25 million

C) $3.125 million

D) $6.25 million

A monopolistically competitive industry is made up of:

A) a few firms, each producing a very differentiated good.

B) one firm that produces a standardized good.

C) market participants who are all price takers.

D) many firms producing a differentiated product.

Decreases in input costs and a longer time since a price change will tend to:

A) increase the price elasticity of supply.

B) decrease price elasticity of supply.

C) have no impact on the price elasticity of supply.

D) increase price elasticity of supply with decreases in input costs but decrease price

elasticity of supply with length of time.

Imposing a Pigouvian tax on a good, establishing a system of tradable licenses, and

assigning property rights are methods to alleviate the problems associated with:

A) private goods.

B) positive externalities.

C) public goods.

D) common resources.

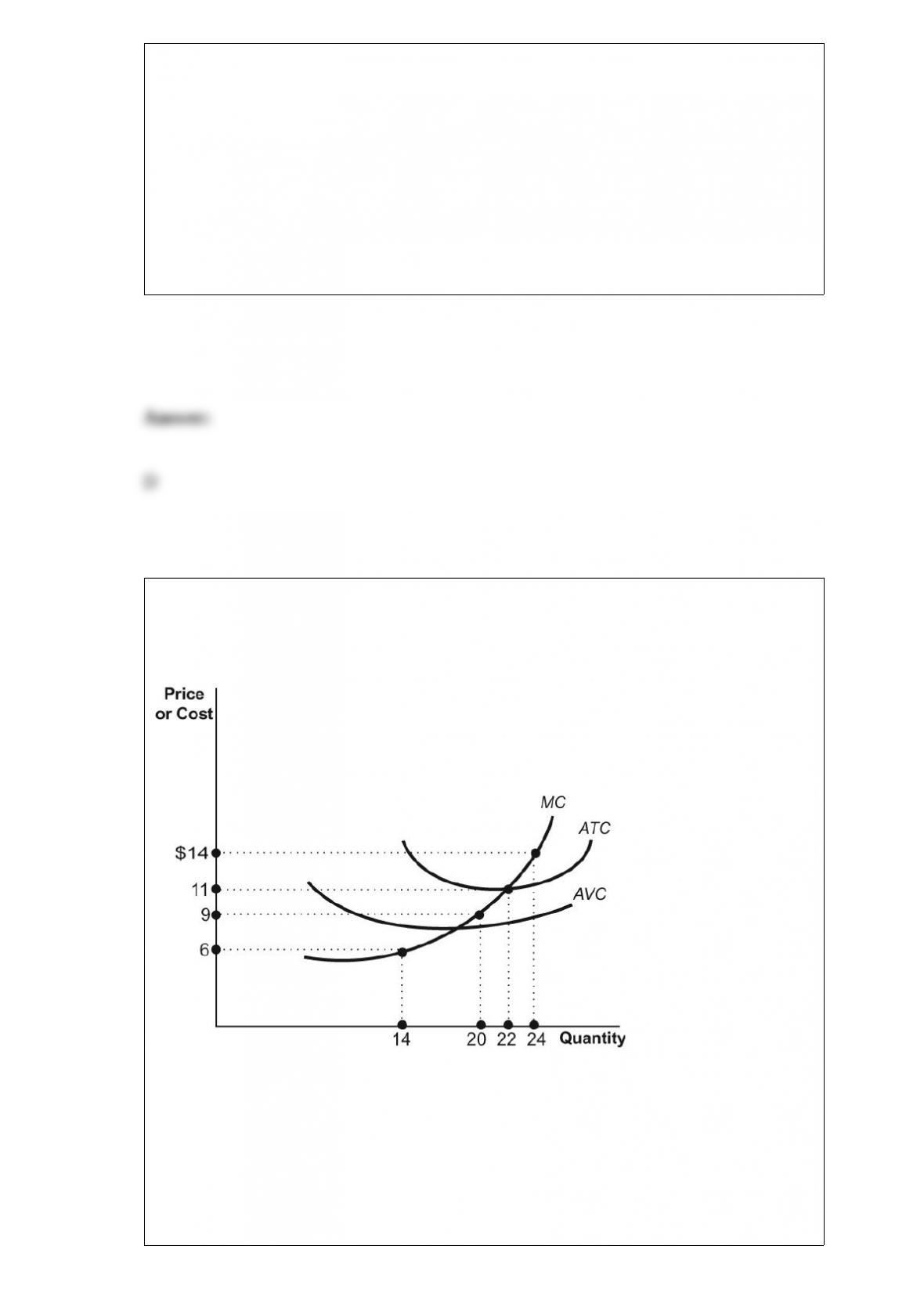

Figure: Game-Day Shirts

(Figure: Game-Day Shirts) Rick is one of 10 vendors who sell game-day T-shirts at

football games in a perfectly competitive market. His costs are identical to the costs of

the other 9 vendors. If the industry is in long-run equilibrium, the price of each shirt

will be:

A) $6.

B) $9.

C) $11.

D) $14.

Increases in resources or improvements in technology will tend to cause a society’s

production possibility frontier to:

A) shift inward.

B) shift outward.

C) remain unchanged.

D) become vertical.

A tax of $10 on an income of $100, $25 on an income of $200, and $60 on an income

of $300 is:

A) progressive.

B) proportional.

C) regressive.

D) flat.

For a firm producing at any level of output LOWER THAN the most profitable one, an

increase in output adds:

A) more to total cost than to total revenue.

B) more to total revenue than to total cost.

C) the same amount to total revenue as to total cost.

D) to total revenue but not to total cost.

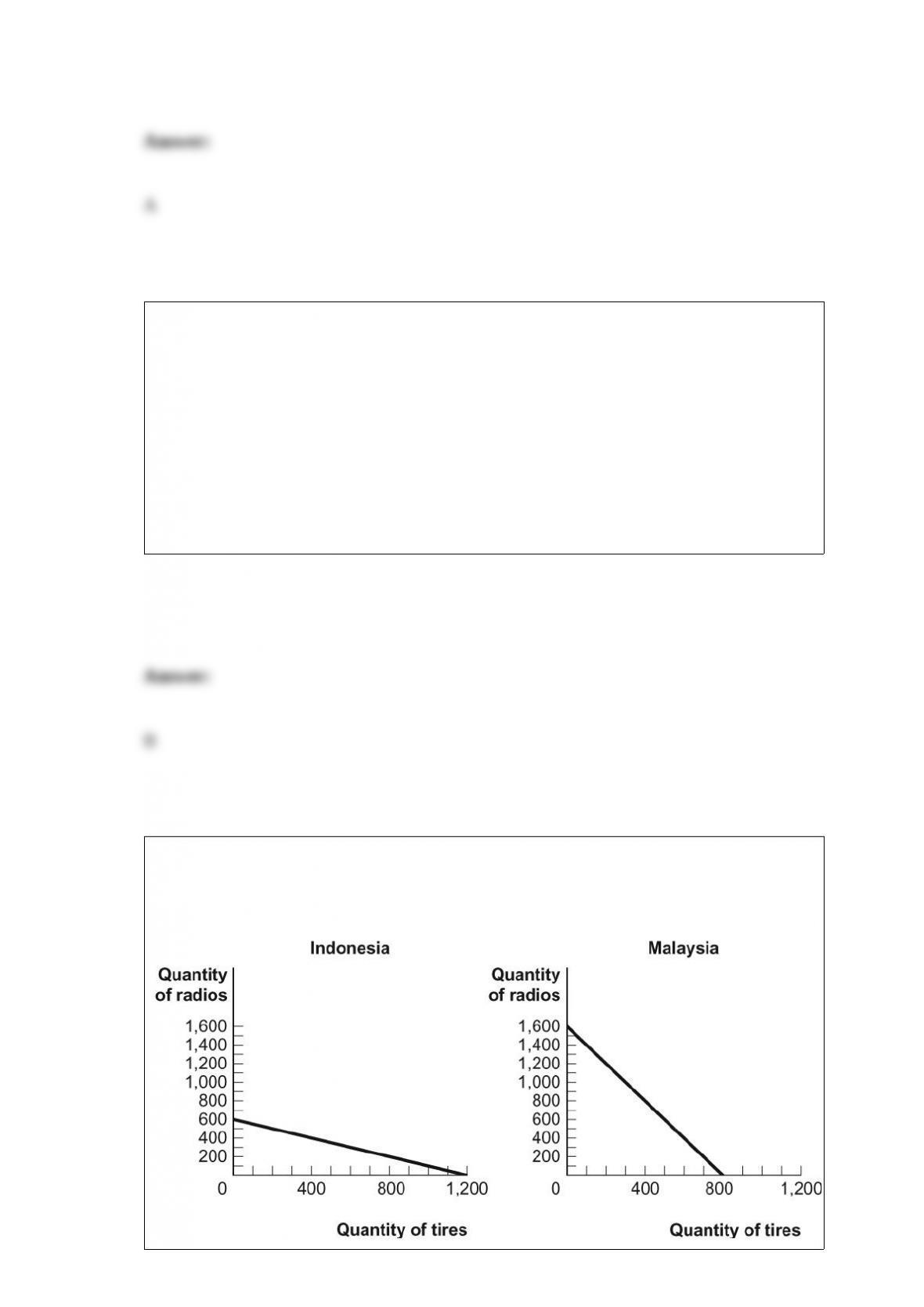

Figure: The Production Possibilities for Two Countries

(Figure: The Production Possibilities for Two Countries) Look at the figure The

Production Possibilities for Two Countries. Trade will NOT take place if 1 radio trades

for:

A) 0.25 tire.

B) 1 tire.

C) 1.5 tires.

D) 1.75 tires.

Along the upward-sloping supply curve for brownies, a decrease in the price of

brownies will:

A) increase producer surplus.

B) decrease producer surplus.

C) increase consumer surplus.

D) increase producer surplus and consumer surplus.

Zoe’s Bakery determines that P < ATC and P > AVC. In the short run, Zoe should:

A) continue to operate even though she is taking an economic loss.

B) continue to operate, as she is making an economic profit.

C) shut down immediately, as she is taking an economic loss.

D) raise the price until she has maximized her profits.

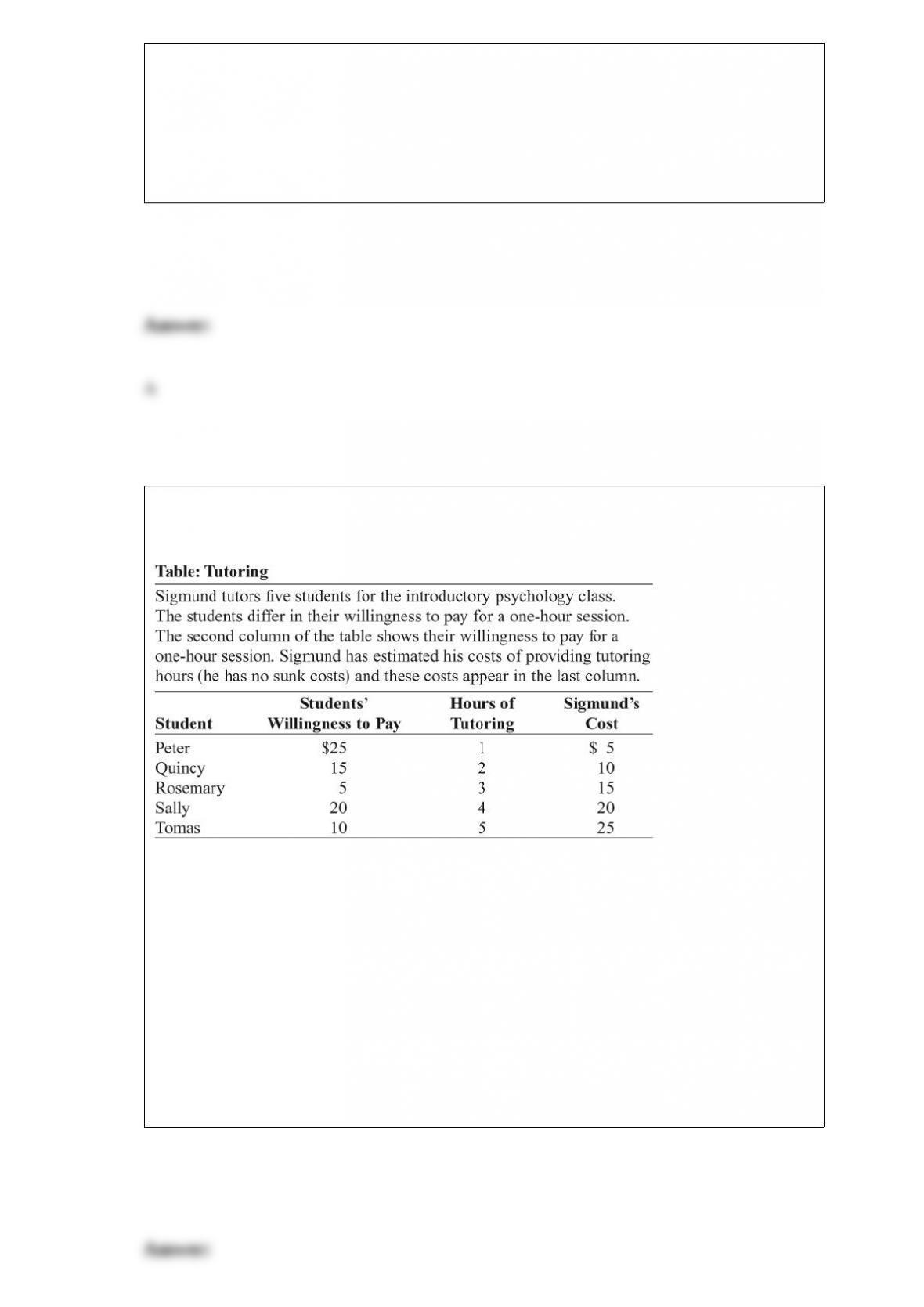

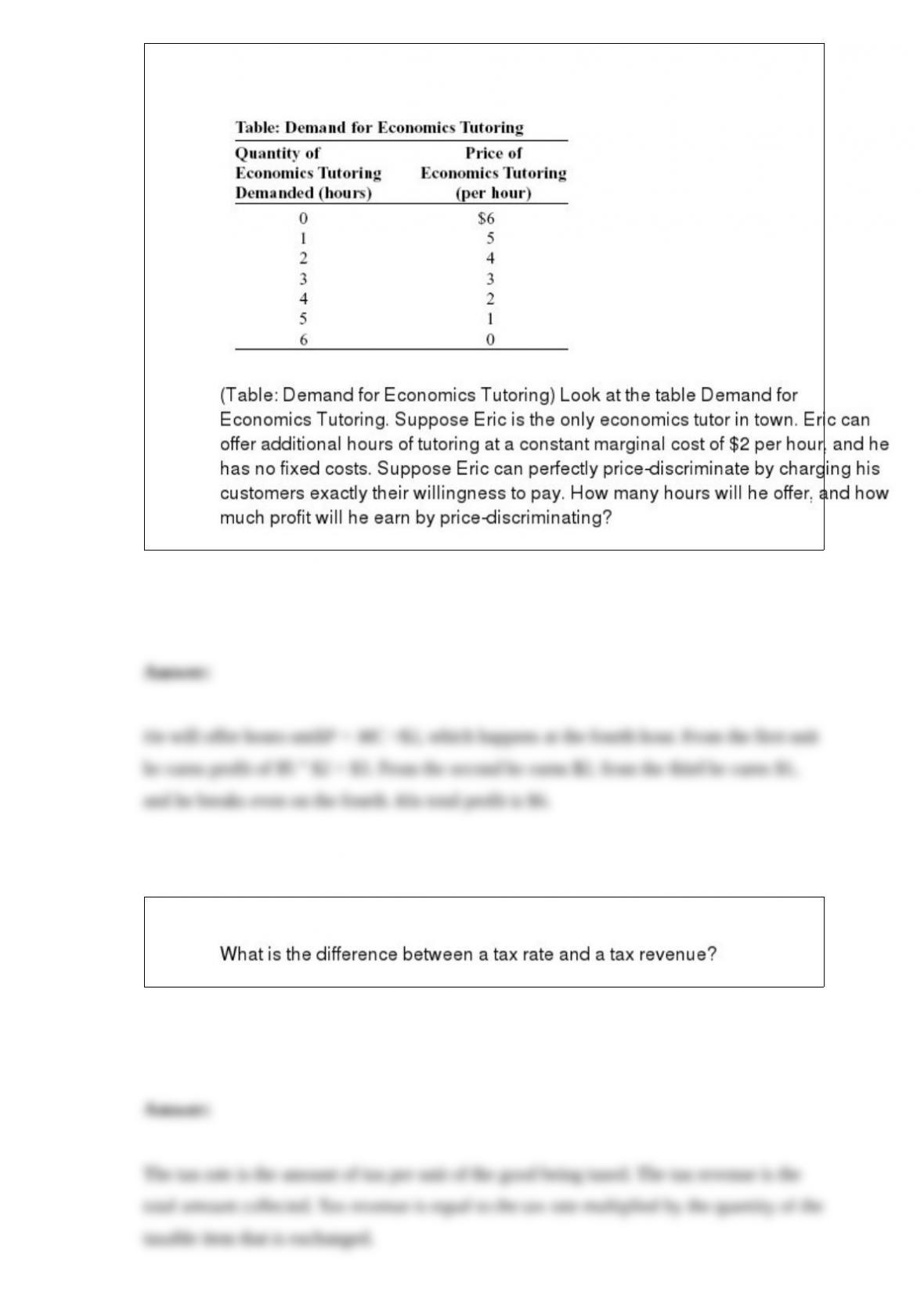

(Table: Tutoring) Look at the table Tutoring. If the college requires all tutors to register

with the dean and charges each tutor $10 to register, Sigmund’s optimal number of

tutoring hours will be:

A) five.

B) four.

C) three.

D) two.

Macroeconomics deals with:

A) bits and pieces of the economy.

B) how a business unit should operate profitably.

C) the working of the entire economy or large sectors of it.

D) how individuals make decisions.

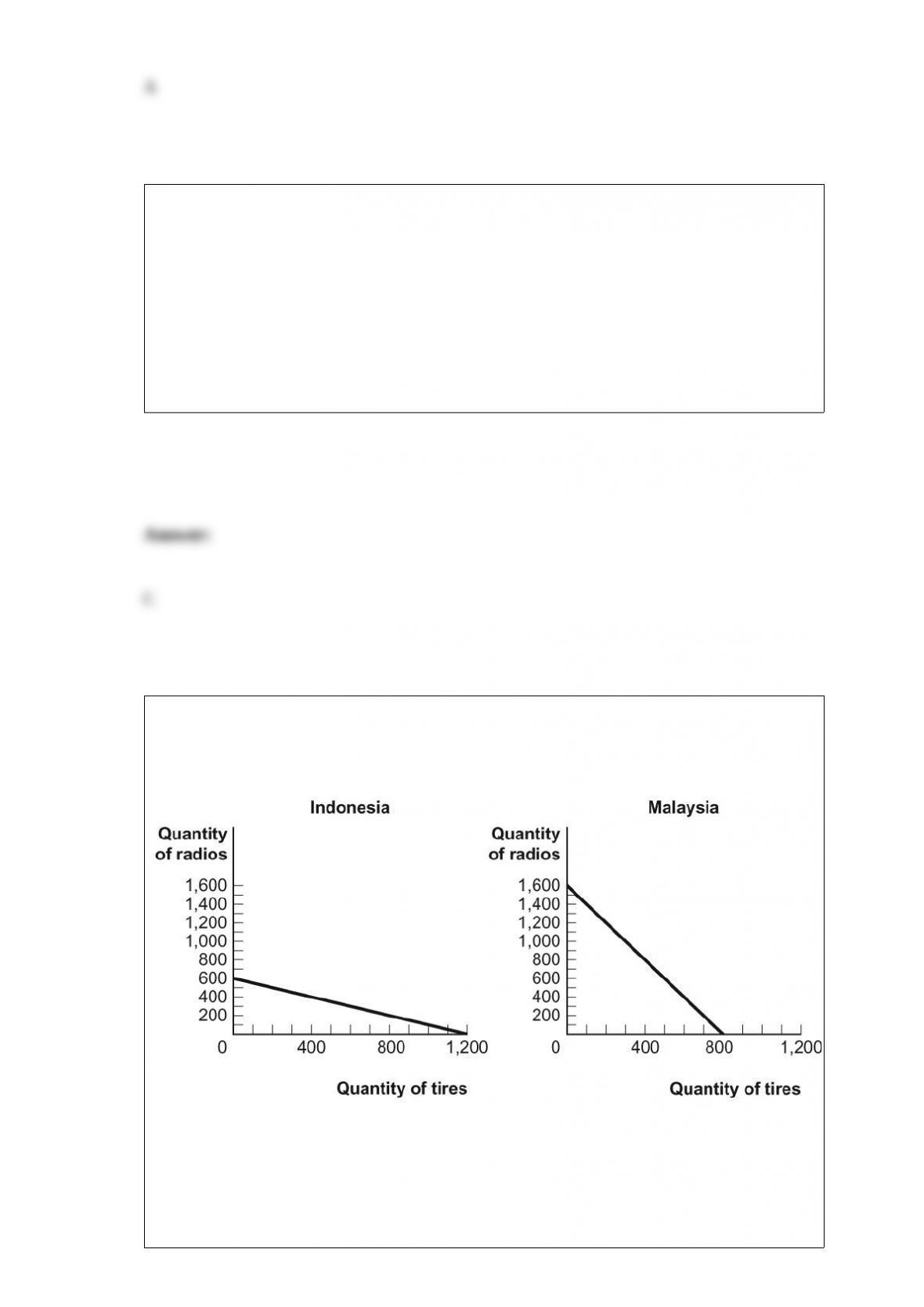

Figure: The Production Possibilities for Two Countries

(Figure: The Production Possibilities for Two Countries) Look at the figure The

Production Possibilities for Two Countries. If Indonesia and Malaysia specialize

completely in the production of the good of their comparative advantage, the two

nations together will produce _____ tires and _____ radios.

A) 600; 800

B) 800; 1,200

C) 1,200; 1,600

D) 800; 600

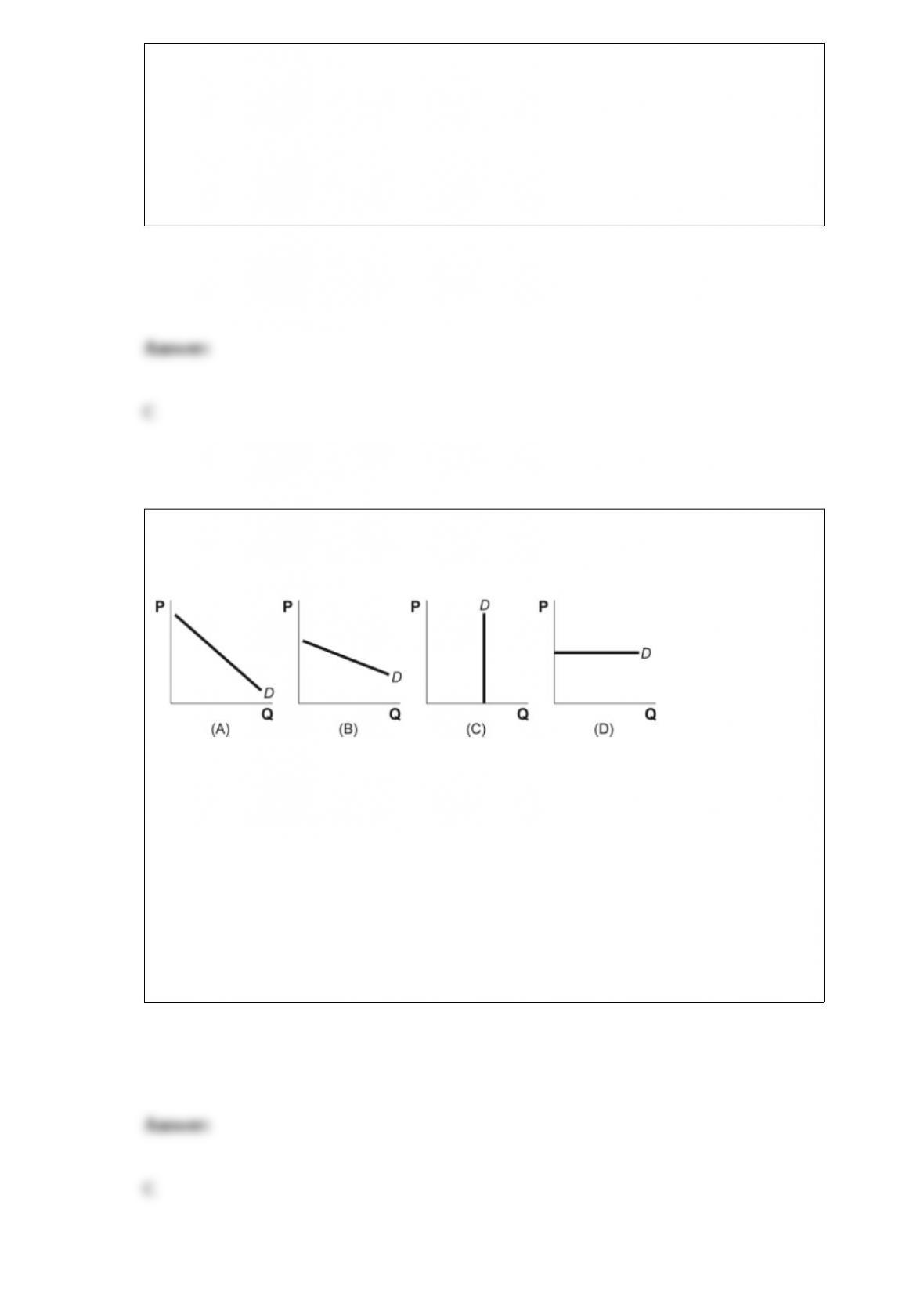

Figure: Demand Curves

(Figure: Demand Curves) Look at the figure Demand Curves. Which graph shows a

perfectly inelastic demand curve?

A) A

B) B

C) C

D) D

Scenario: Flood Area

Suppose you own a home that is estimated to be worth $250,000. You live in a flood

plain; as a result, the probability that you will lose your home to a flood is 30%.

(Scenario: Flood Area) Look at the scenario Flood Area. Suppose an insurance

company offers you flood insurance. Most likely this insurance would require a

premium payment:

A) greater than $250,000.

B) greater than $75,000.

C) less than $15,000.

D) equal to $100,000.

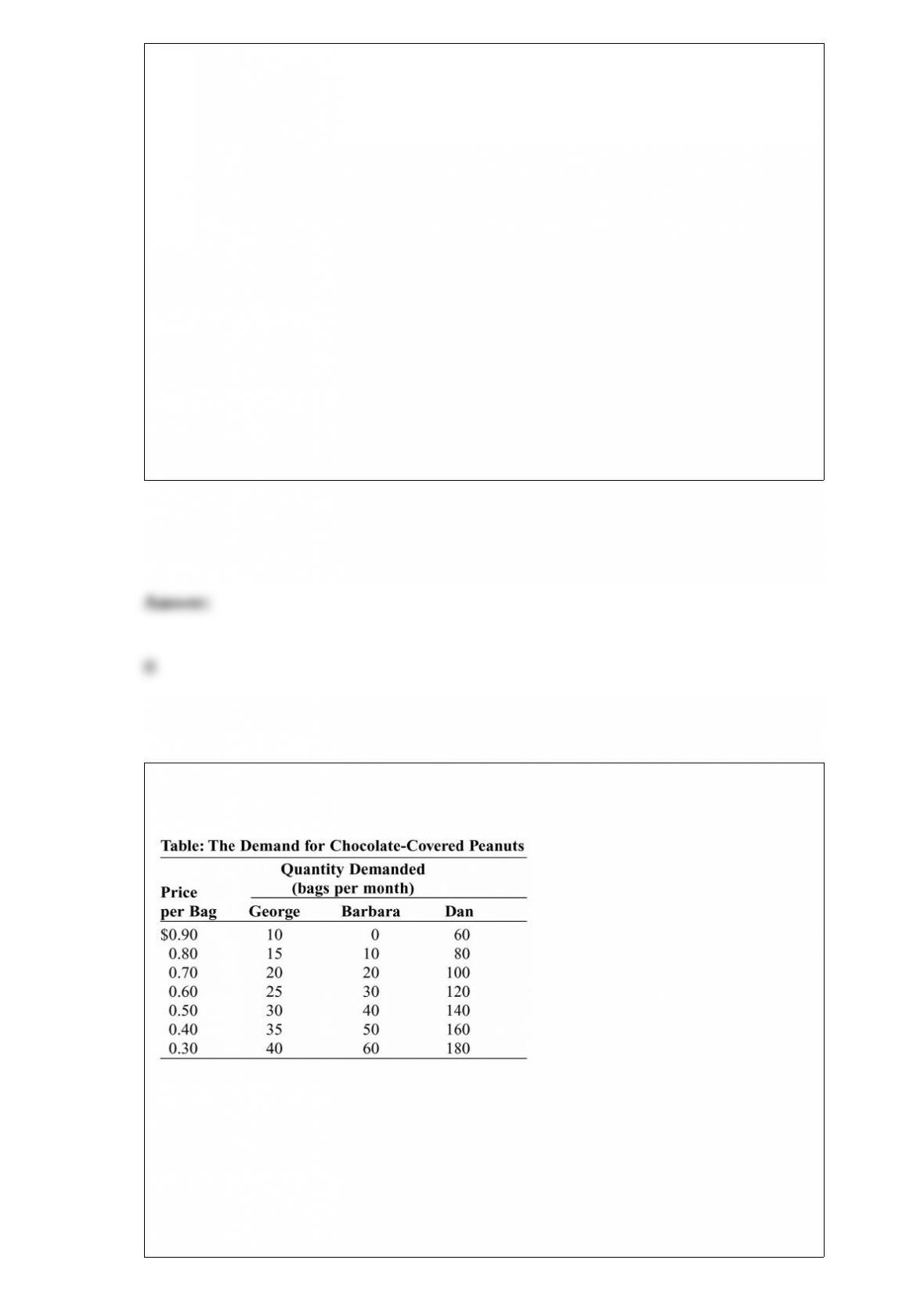

(Table: The Demand for Chocolate-Covered Peanuts) Look at the table The Demand for

Chocolate-Covered Peanuts. If the price of chocolate-covered peanuts is $0.60, the

quantity demanded by George is _____ bags per month.

A) 10

B) 15

C) 25

D) 30

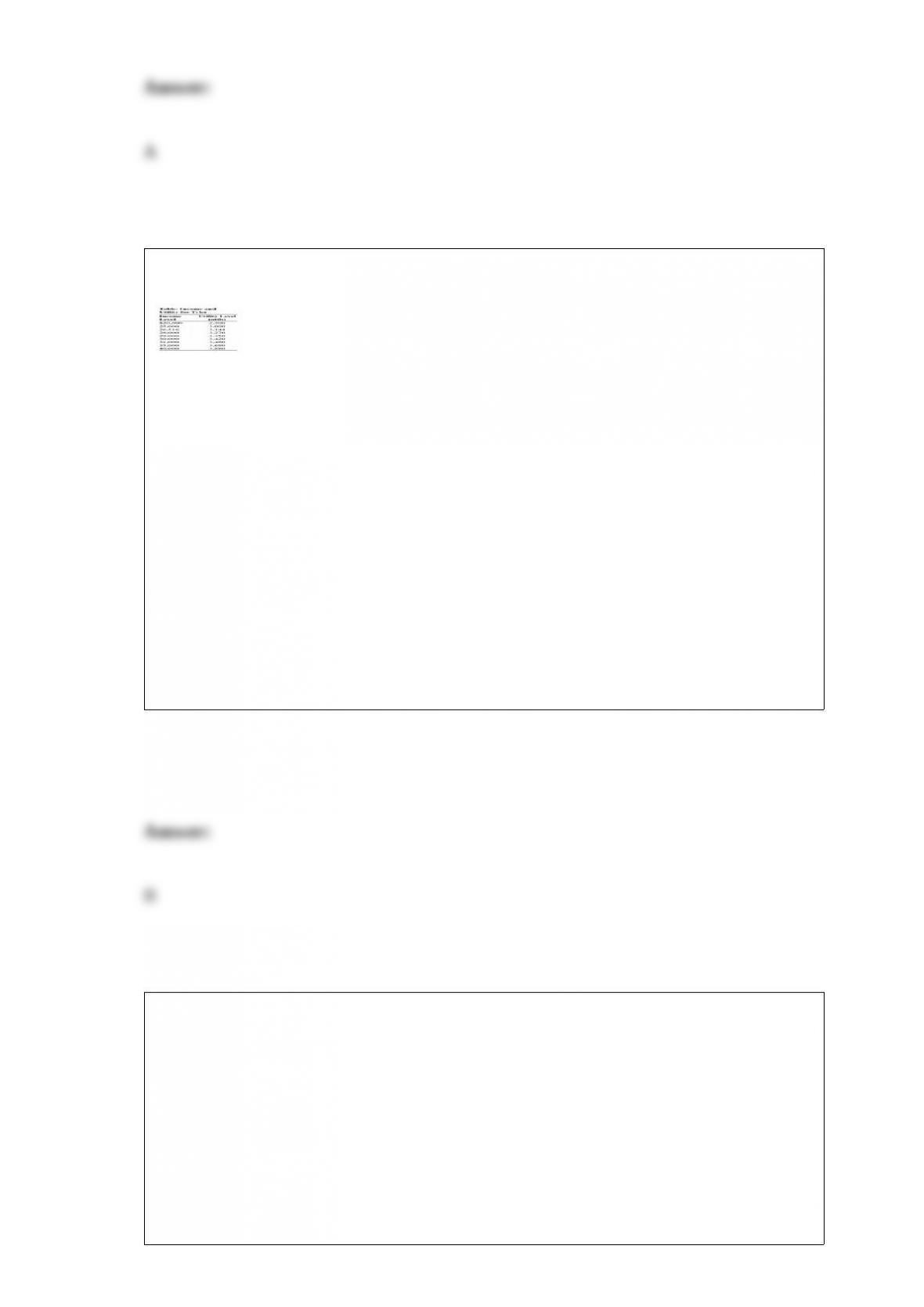

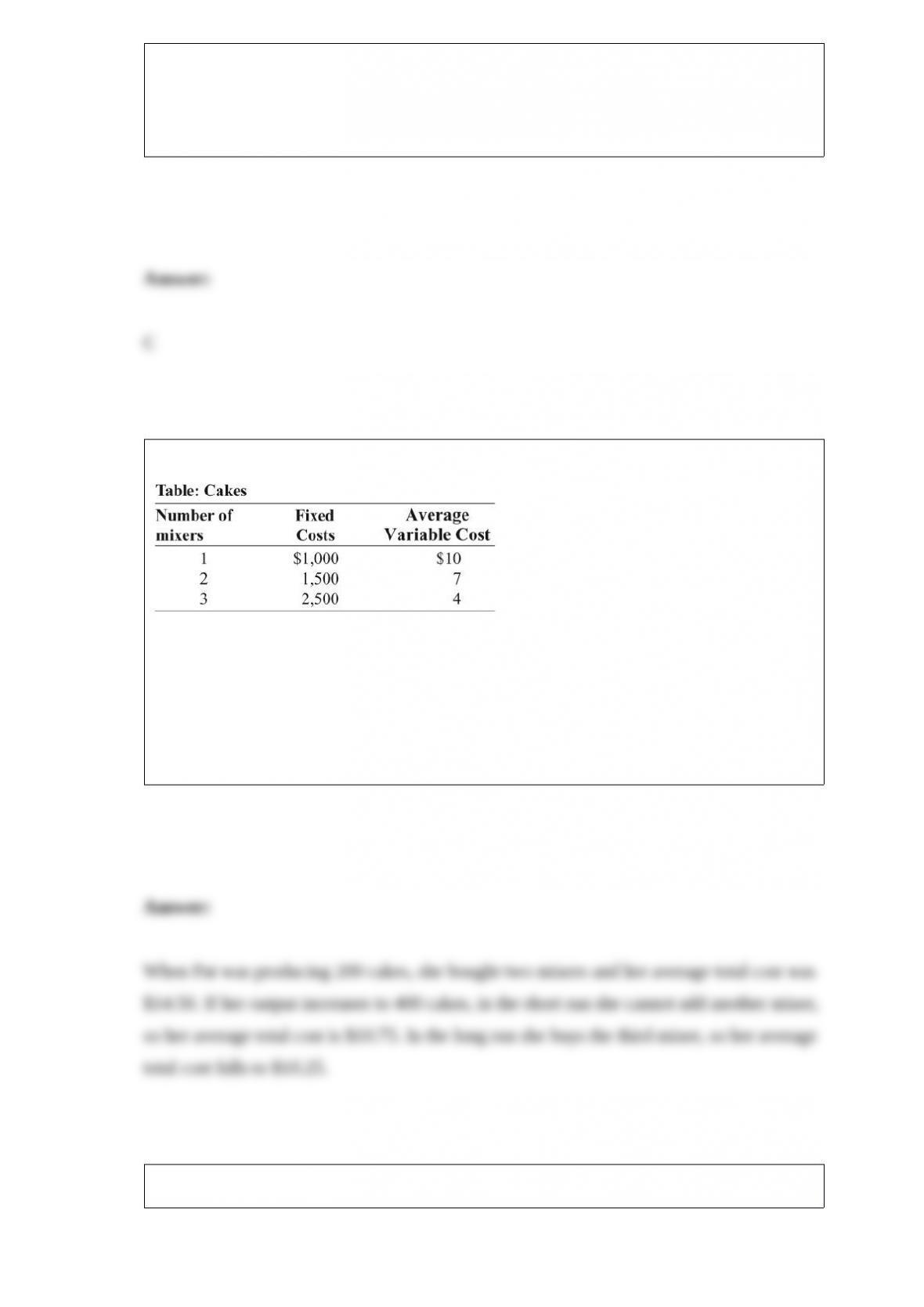

(Table: Cakes) Look at the table Cakes. Pat is opening a bakery to make and sell special

birthday cakes. Her estimated fixed and average variable costs if she purchases one,

two, or three mixers are shown in the table. Assume that average variable costs do not

vary with the quantity of output. Suppose that Pat used to produce 200 cakes, but she

has a sudden increase in demand, so that she begins to produce 400 cakes. Explain how

her average total cost will change in the short run and in the long run.

In the short run, why is it believed that the total product curve increases at a decreasing

rate when more labor is added to the production function?

Why are economists so particular about the difference between an increase in quantity

demanded and an increase in demand? Aren’t they the same thing?

Two consumers go to the insurance company to purchase life insurance. James is a

smoker and a police officer who races motorcycles in his spare time. Kathy is a

nonsmoker and a librarian who likes to make quilts in her spare time. The insurance

company knows that both consumers are 40 years old, but the company has no

information about occupations or hobbies. How does the private information in this

situation set up an adverse-selection problem? How could the insurance company lessen

this problem?

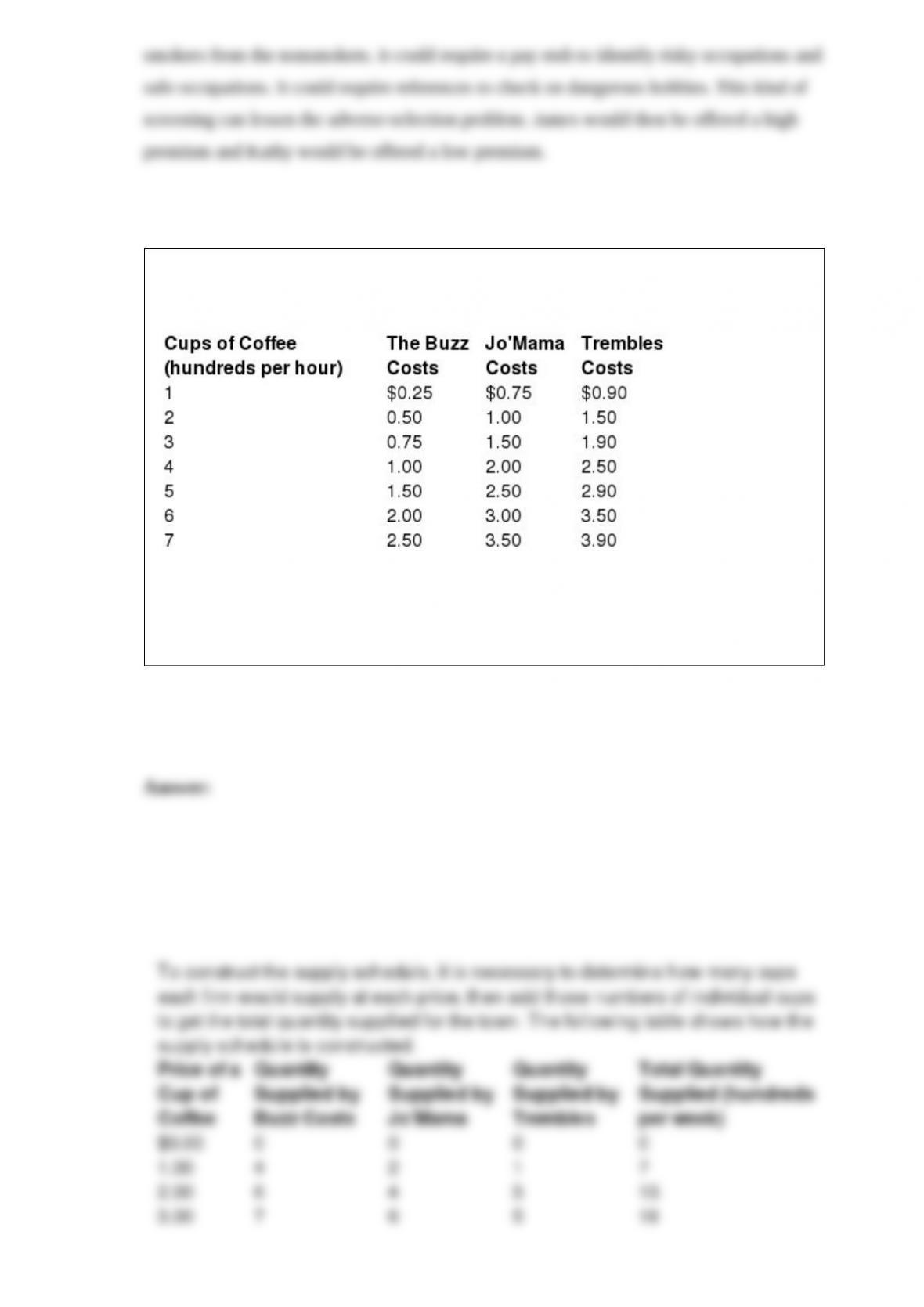

Table: Coffee Shops

(Table: Coffee Shops) Look at the table Coffee Shops. The three coffee shops in a small

town supply cups of coffee at slightly different costs. Use the table to construct the

supply schedule for coffee at prices of $0, $1, $2, and $3.

The city government is losing millions of dollars on its buses and subways. The

government proposes to increase the fare by 20% to raise revenue and has asked your

advice. You know that the price elasticity of demand for mass transit in the city is

approximately equal to 0.75. What do you think of the proposal to increase the fare to

raise revenue for the city? Be as specific as possible.

Suppose that two police officers are identical in every way. One officer is employed in

Chicago, a metropolis of 5 million people, and the other officer is employed in

Madison, Indiana, a town of 25,000 people. Which officer is likely to receive the higher

wage? What is a likely source of this wage difference?