As the rate of interest on borrowed funds increases, the quantity of investment funds

demanded diminishes.

a. True

b. False

If the United States imposed a 25 percent tariff on imports of minivans, the effect would

be to

a. raise the price and reduce the quantity of imports.

b. raise the price and the quantity of imports.

c. lower the price and the quantity of imports.

d. raise the quantity and reduce the price of imports.

The term “random walk” means that stock prices are fairly predictable.

a. True

b. False

Explain briefly the following concepts:

(a) Increasing returns to scale.

(b) Decreasing returns to scale.

(c) Constant returns to scale.

The quantity demanded in a market depends on many things, but the concept of

elasticity focuses on the effect of changes in the price of the good.

a. True

b. False

Suppose that in a free market 2,000 patients purchase an operation to receive an

artificial heart at a price of $500,000 per operation. Without the heart, each patient will

die. The government decides this price is too high and imposes a maximum price of

$200,000. Everything else equal,

a. more patients will now die.

b. fewer patients will now die.

c. more patients will now die only if the demand curve is vertical.

d. more patients will now die only if the demand curve is horizontal.

In the fifteenth and sixteenth centuries, most towns prohibited individuals from

accumulating stocks of grain. Since such individuals sold the grain and profited greatly

during food shortages, they were considered to be exploiting people in need. The result

of this prohibition was

a. wilder fluctuation in the price of grain.

b. more grain shortages.

c. losses to farmers in a good crop year.

d. All of the above are correct.

The apparent stickiness of the price of goods sold by oligopolists can be explained by

the

a. contestable markets model.

b. sales maximization model.

c. kinked demand curve model.

d. entry deterrence model.

A supply curve slopes upward because quantity supplied is higher when price is higher.

a. True

b. False

Which of the following is not a symptom associated with a price floor?

a. Excess of quantity demanded over quantity supplied.

b. Sellers offering discounts in disguised forms.

c. Problem of disposal created by excess supply.

d. Survival of inefficient businesses.

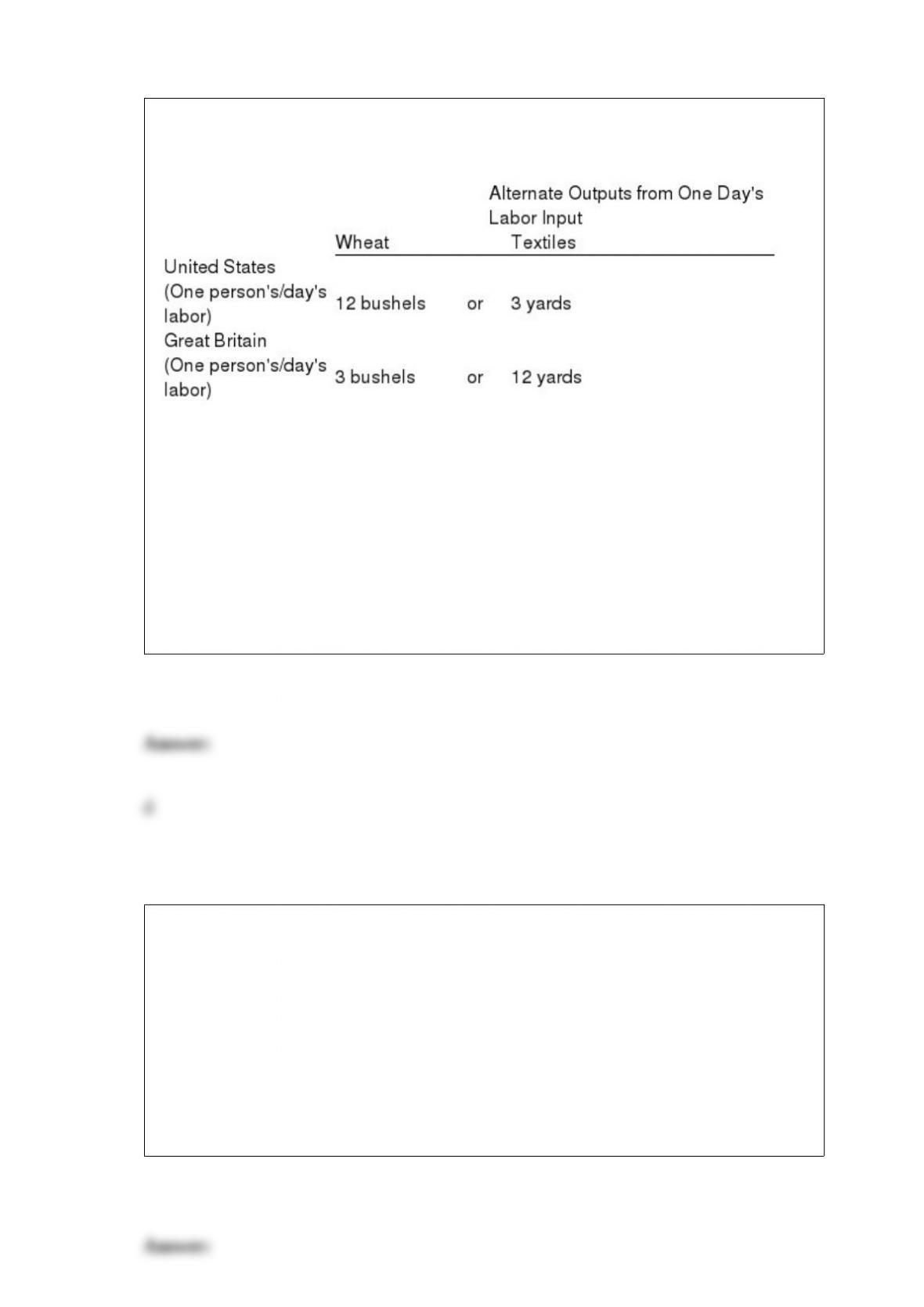

Table 22-1

From Table 22-1, the opportunity cost of one bushel of wheat in Great Britain is

a. 1/4 yard of textiles.

b. 3 yards of textiles.

c. 12 yards of textiles.

d. 4 yards of textiles.

For which of the following workers would the substitution effect be more likely to

outweigh the income effect of an increase in wage?

a. air traffic controller

b. marketing manager

c. waitress

d. dentist

The United States has been willing to trade off greater efficiency for greater wage

equality.

a. True

b. False

A firm operating at MC = MR must be making a profit.

a. True

b. False

The necessity for choice, in economics, arises from

a. high incomes and many goods.

b. scarcity of economic means for satisfying economic wants.

c. scarcity of time and knowledge, and numerous similar goods.

d. All of the above are correct.

Which of the following is a source of inequality in incomes?

a. luck

b. willingness to take risks

c. differences in investment in human capital

d. All of the above are correct.

To maximize sales revenue, an oligopolist will expand output until the elasticity of

demand becomes

a. negative.

b. zero.

c. one.

d. infinite.

The 1994 book by Murray and Herrnstein, The Bell Curve, was about

a. government debt.

b. the intelligence factor.

c. capital growth.

d. military readiness.

Subsidizing firms that pollute will reduce pollution in the long run.

a. True

b. False

Which of the following is a series of rules that stops trading on an exchange for a

relatively short period of time?

a. program trading

b. market limits

c. stop orders

d. circuit breakers

At the equilibrium point in a perfectly competitive industry, the total surplus (the sum

of the consumer surplus and producer surplus) will be at its maximum.

a. True

b. False

The proliferation of new products that we are used to today has been occurring since the

advent of the Industrial Revolution.

a. True

b. False