Market equilibrium guarantees that all mutually beneficial transactions take place.

The conventional way to regulate a natural monopolist is to force it to charge a price

equal to marginal cost.

Economic cost differs from accounting cost because accountants do not consider

implicit costs.

Some monopolistically competitive firms differentiate their products simply by opening

a new store at a different location.

The prisoners’ dilemma naturally leads prisoners to the best possible outcome.

When Lonnie produces 1 pair of cowboy boots his costs total $300. When he produces

2 pairs of cowboy boots his total costs are $500. This means that Lonnie’s marginal cost

of producing the second pair of cowboy boots is $200.

As more satisfaction is expected from the purchase of a product, the flow of dopamine

in the brain increases.

There is asymmetric information in the auto insurance market because companies know

more about customers’ driving habits and can predict very well the chances of

customers getting into an accident than the customers.

If a 10% increase in price decreases the quantity demanded by 12%, the price elasticity

of demand is 1.2.

If the price level falls faster than the wage rate, then the real wage decreases.

Producers of close substitutes have little or no incentive to merge.

Department stores are monopolistically competitive because stores differ in the amount

of customer service they provide.

In a constant cost industry, inputs prices do not change with changes in output.

If a company’s total costs per day increase from $500 to $600 by adding another

worker, but its additional benefits are $150, it is sensible to add that additional worker.

Since all costs positive, then economic profits would always be smaller than accounting

profits.

Firms gain control over price in monopolistic competition by differentiating their

products.

When two parties engage in voluntary exchange, one must be made worse off.

A perfectly competitive firm maximizes profit where marginal revenue or pice equals

marginal cost.

A payoff matrix shows each possible outcome of a game and the consequences for each

player.

To be an example of a public good a good must be both rival in consumption and

nonexcludable.

An increase in wages will shift the supply curve up and to the left.

Suppose that income increases and the quantity demanded of guitars stays the same.

This means that the income elasticity of guitars is unitary.

Water pollution is not an example of an external cost.

A consumption possibilities curve shows the combinations of two goods that can be

consumed when a nation specializes in producing a particular good and trades with

another nation.

The difference between the short run and long run is a firm’s flexibility in choosing

inputs.

A power plant is emitting nitrogen oxides, a contributing factor in acid rain and in urban

smog. If the power plant is taxed on the emission of nitrogen oxides then we can expect

the amount of energy produced by the power plant to decrease.

The dominant strategy of the in the advertising dilemma is to advertise even if it

reduces industry profits.

Ceteris paribus is the same as rise / run.

Monopolies are characterized by a firm demand curve that is more elastic than the

market demand curve.

The median voter rule says that the government will make choices that reflect the

preferences of the voters whose preferences are held by at least 51% of the voters.

The dominant strategy in the advertising dilemma is to not advertise no matter what the

other firm does.

Firms participating in implicit price leadership openly discuss their pricing strategies

with one another.

Command-and-control policies are desirable because their tough pollution reduction

targets force firms to develop new technologies to survive.

According to the textbook, a famous study of the eyeglass market found that advertising

promoted price competition.

From the perspective of consumers, a quota is preferred to a tariff.

In order for a monopoly to maximize its profit, the monopoly will produce the quantity

at which marginal revenue is less than marginal cost.

When buyers assume that there is a 70% chance of getting a lemon, and seven lemons

(low quality) and three plums (high quality) are supplied, there is an equilibrium.

Even though in oligopoly the actions of one firm has a perceptible effect on the other

firms, oligopoly firms act independently.

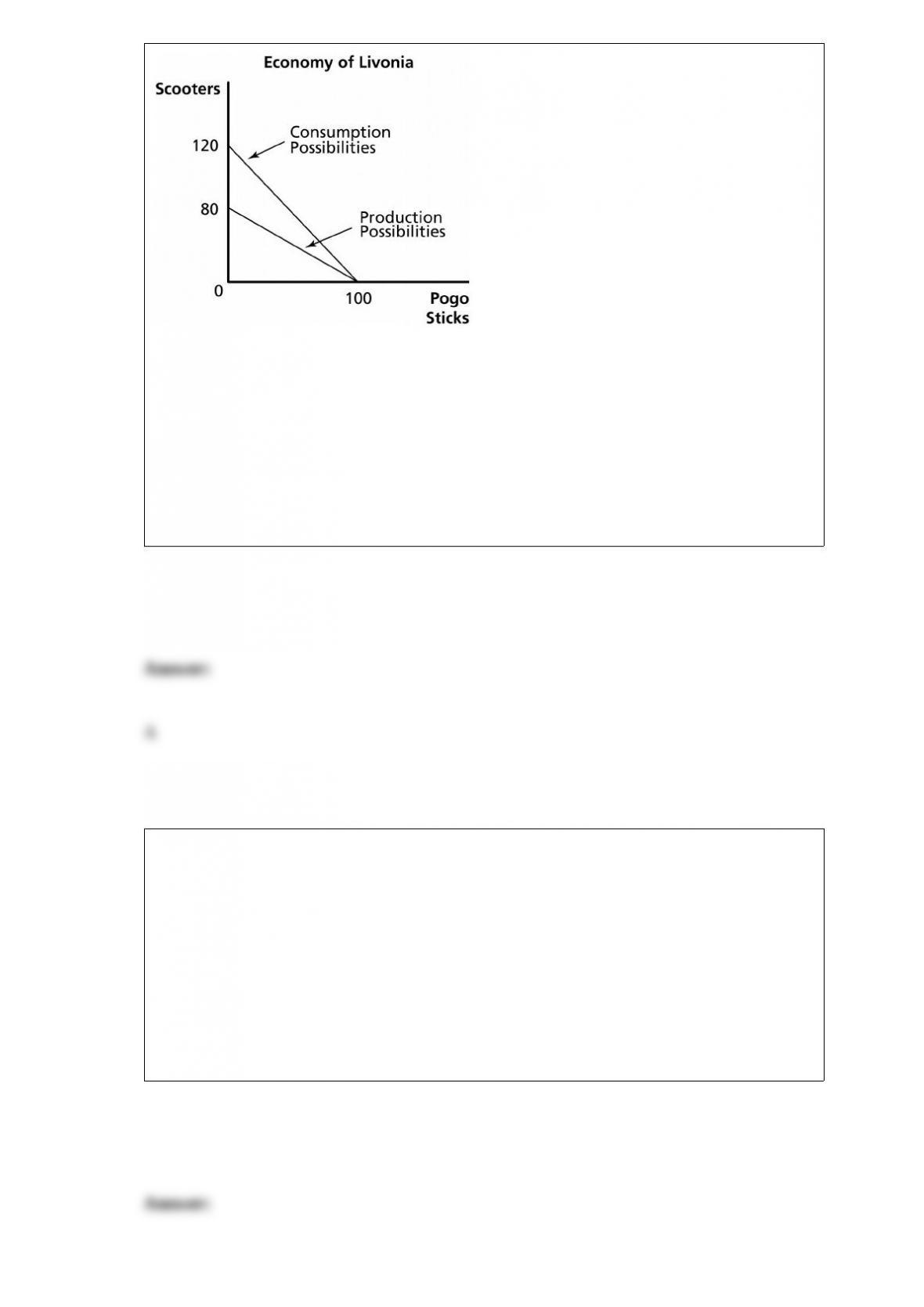

Refer to Figure 18.3. After trade and specialization begin, the maximum amount of

scooters that Livonia can consume is:

Figure 18.3

A) 120.

B) 100.

C) 80.

D) 40.

Suppose you know that at the current level of production average total cost equals

marginal cost, then you know that it is also true that:

A) fixed costs are zero.

B) average fixed costs are increasing.

C) average total cost will decrease if production is increased.

D) average total cost is minimized at the current level of output.

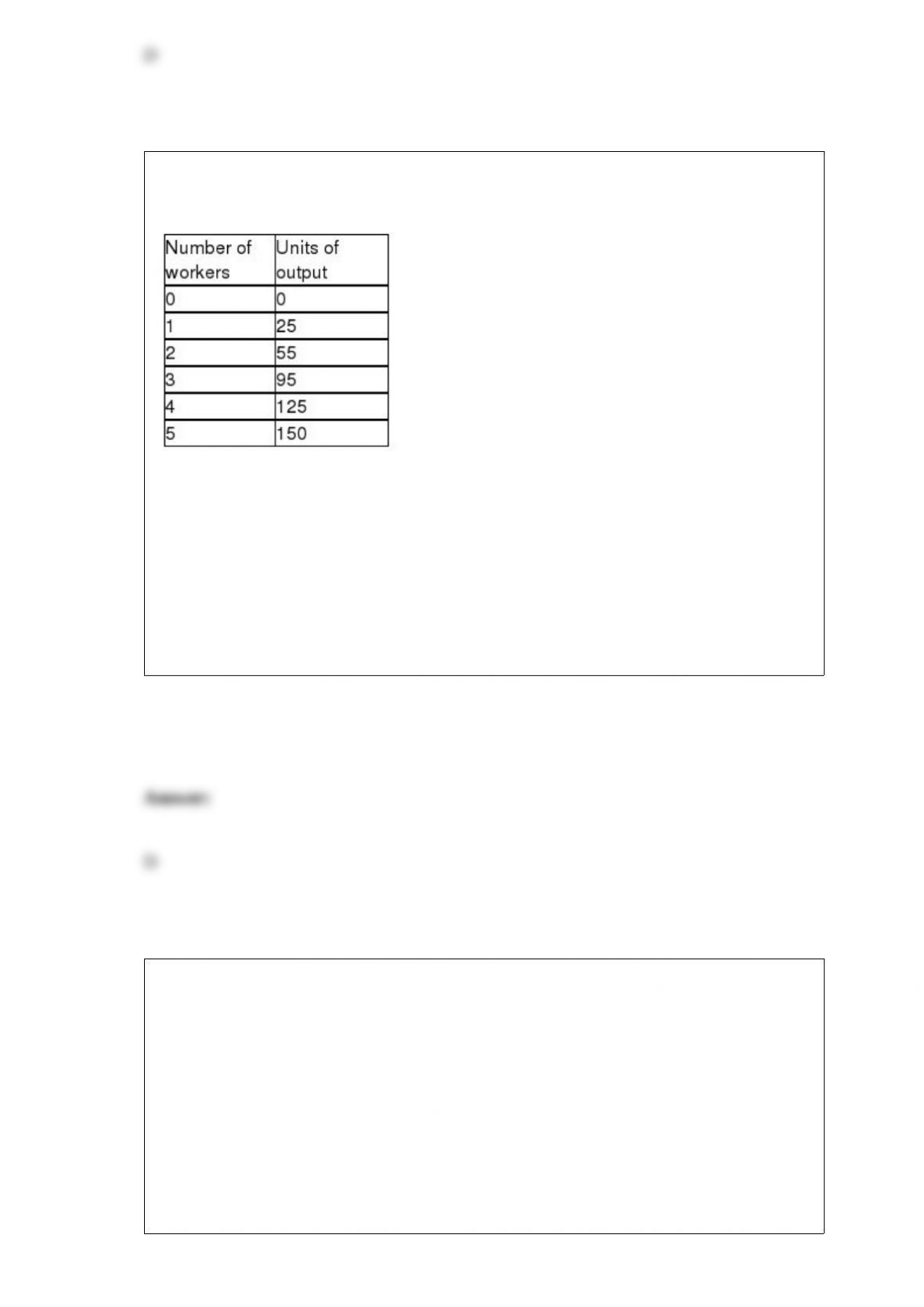

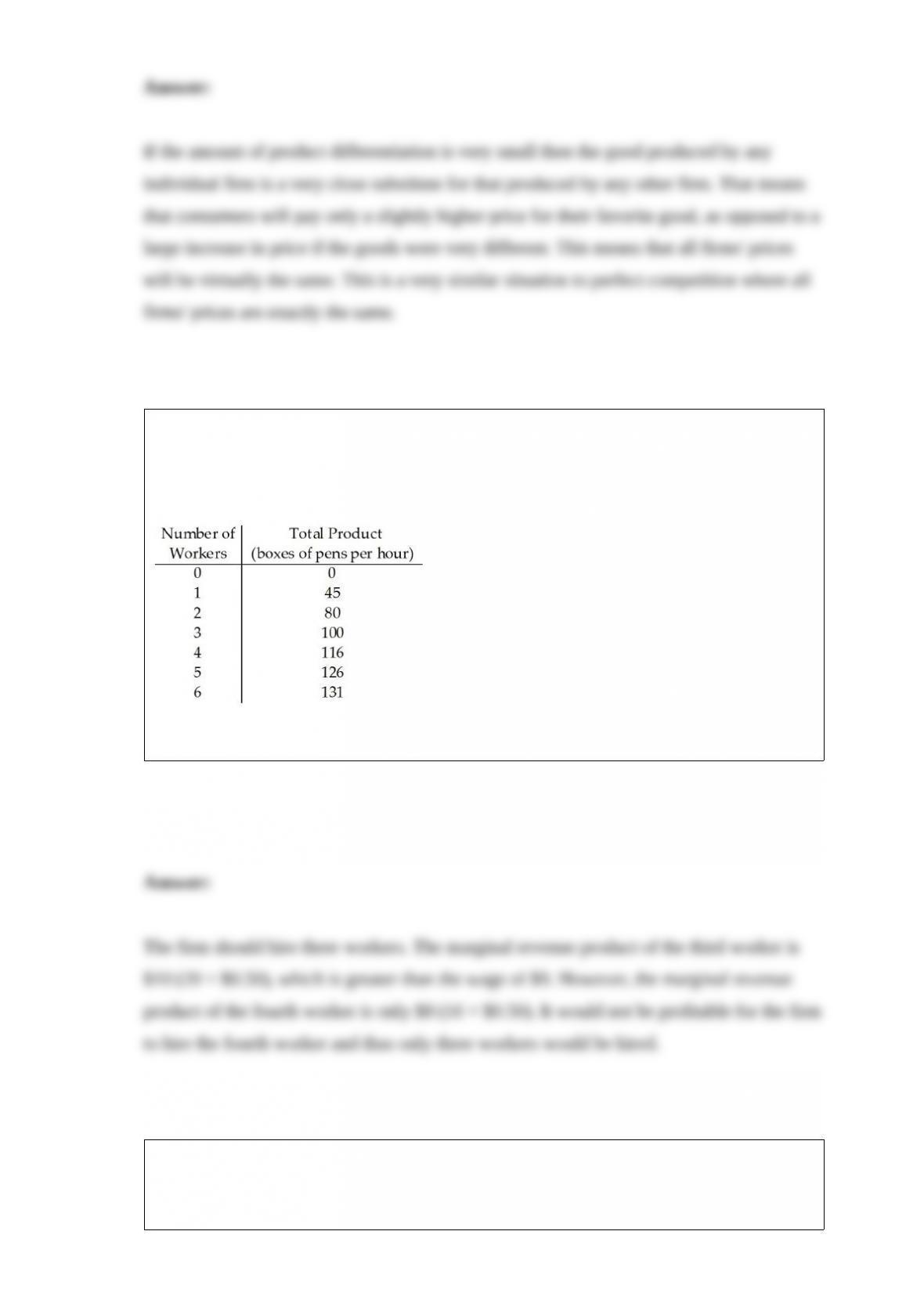

Refer to Table 8.2, which gives a firm’s production function. Assume that all non-labor

inputs are fixed. The marginal product of the fourth worker is:

Table 8.2

A) 0 units.

B) 10 units.

C) 25 units.

D) 30 units.

Government taxes and transfers:

A) increase the wealth of the poorest Americans and reduce the wealth of the richest

Americans.

B) reduce the wealth of all Americans.

C) increase the wealth of all Americans.

D) reduce the wealth of the poorest Americans and increase the wealth of the richest

Americans.

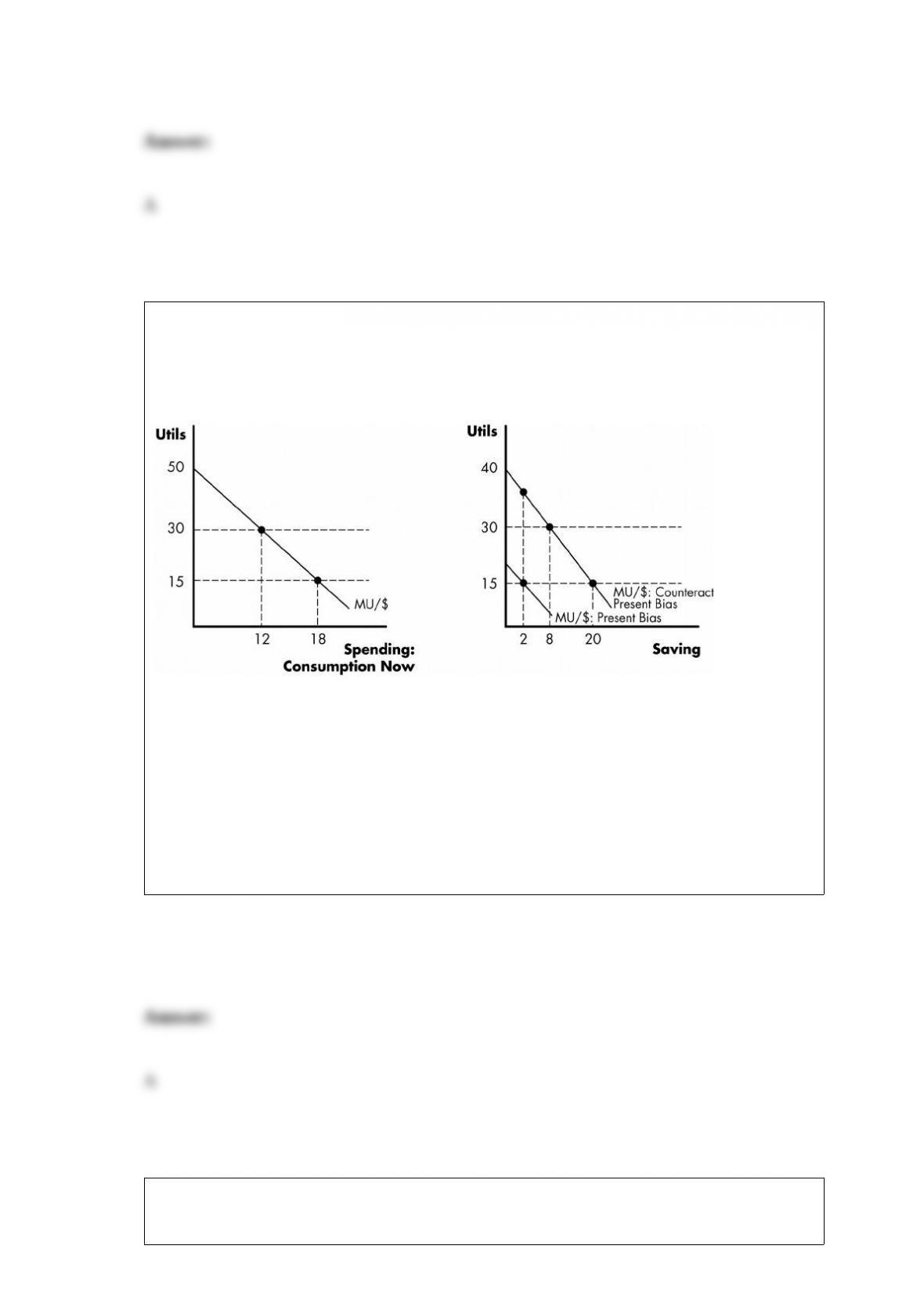

Refer to Figure 7.5. If the consumer is subject to present bias, he will maximize utility

at a marginal utility per dollar of ________ utils for consumption and ________ utils

for saving.

Figure 7.5

The consumer must decide how to split $20 between spending and saving.

A) 15: 15

B) 15: 30

C) 30: 15

D) 30: 30

The opportunity cost of something is:

A) the cost of the labor used to produce it.

B) what you sacrifice to get it.

C) the price charged for it.

D) the search cost required to find it.

Experience ratings provide firms with an incentive to:

A) hire older workers.

B) invest in health and safety programs.

C) hire disabled workers.

D) none of the above

Which of the following organizations has over 149 member nations and oversees the

General Agreement on Trade and Tariffs?

A) North American Free Trade Agreement

B) World Trade Organization

C) European Union

D) Asian Pacific Economic Cooperation

Relative to a perfectly competitive market, a monopoly produces:

A) more output, charges higher prices, and earns economic profits.

B) more output, charges higher prices, and earns economic losses.

C) less output, charges higher prices, and earns only a normal profit.

D) less output, charges higher prices, and earns economic profits.

A pollution tax will:

A) always be paid entirely by producers.

B) not change the price buyers pay for a good.

C) be shared between buyers and sellers.

D) always be paid entirely by buyers in the form of a price increase equal to the amount

of the tax.

Figure 1A.2

The slope of the curve:

A) is negative.

B) is positive.

C) is zero.

D) changes along the curve.

Additional Application

Late in the day on August 7, 2006 numerous U.S. airlines cut their fares on leisure

travelers. These included American Airlines, Delta, Continental, and Southwest. This

fare cut, which was approximately 4 to 8 percent, occurred during a period of rising fuel

costs and a record number of seats being filled. If costs are up and demand is strong,

why did these airlines reduce their prices on this class of passengers? The explanation is

that they were following the lead of United. United Airlines is the implicit price leader

in this industry and many other carriers watch closely what the leader does and base

their decisions on the leader’s actions. Such behavior is not uncommon in an industry

dominated by a few large firms.

“United Airlines sparks fare war,” August 9, 2006, retrieved November 3, 2006 from

http://money.cnn.com/2006/08/09/news/companies/airfares/index.htm.

In this article on airlines, when the firms experienced an increase in cost of production,

their price ________.

A) increased

B) decreased

C) did not change

D) change was ambiguous

What is the largest category in federal government spending?

A) Social Security

B) national defense

C) income security

D) health

In short-run equilibrium for a competitive firm:

A) price will not equal marginal revenue.

B) marginal revenue will be greater than marginal cost.

C) price will equal marginal cost.

D) price will be greater than marginal cost.

Which of the following is NOT likely to be an example of a product with an inelastic

demand?

A) water

B) cars

C) cigarettes

D) eggs

Based on what you learned from the application, how will the “constructed value”

method used by the Department of Commerce affect the number of cases that it will

deem as dumping?

A) The Department of Commerce will identify fewer cases of dumping into the U.S.

B) The Department of Commerce will identify all cases brought in front of them as “not

dumping.”

C) The Department of Commerce will identify more cases of dumping into the U.S.

D) The Department of Commerce will correctly identify all cases as “dumping.”

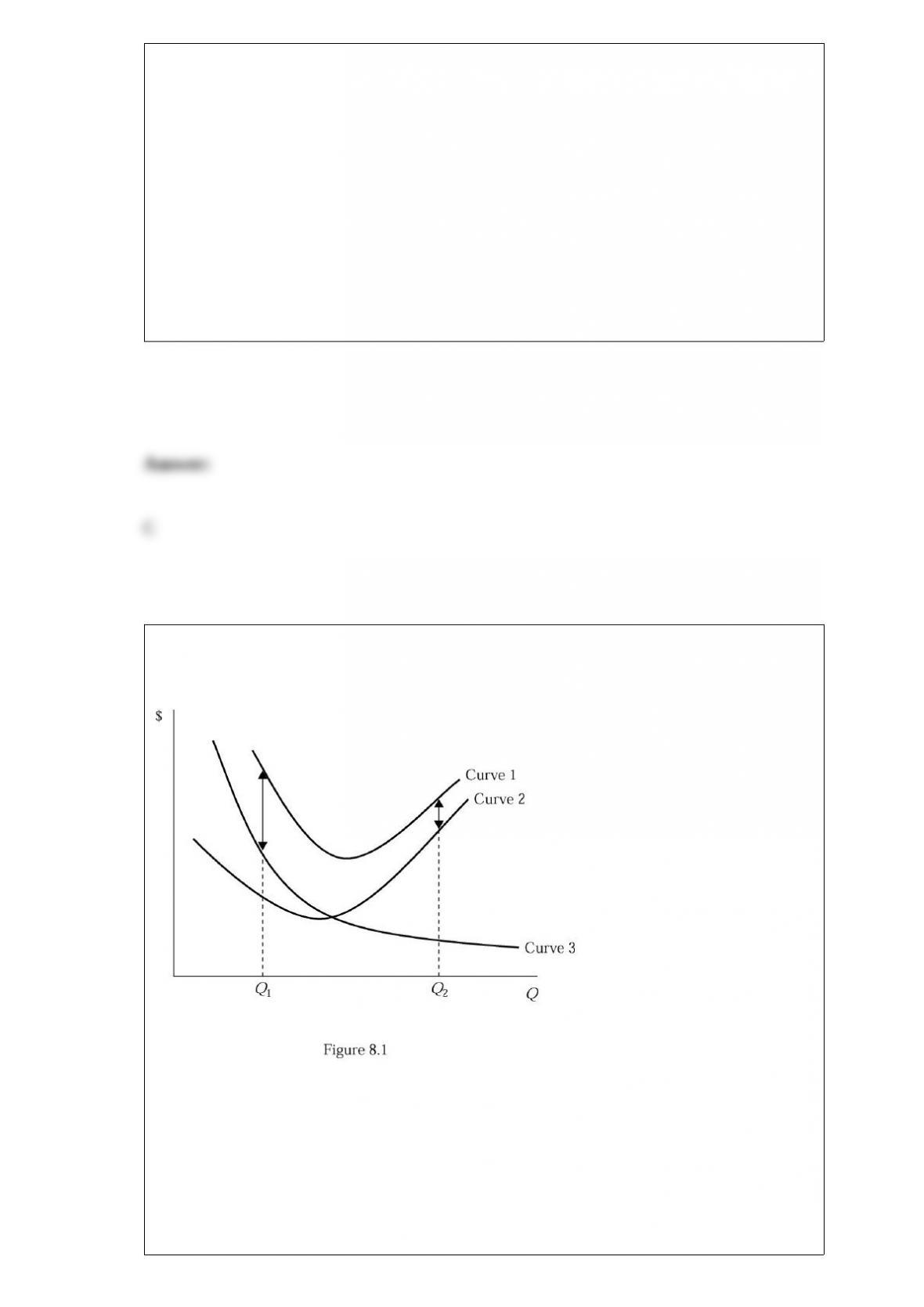

Refer to Figure 8.1, which shows a family of average cost curves. The average fixed

cost curve is represented by:

A) Curve 1.

B) Curve 2.

C) Curve 3.

D) the vertical sum of curve 1 and curve 2.

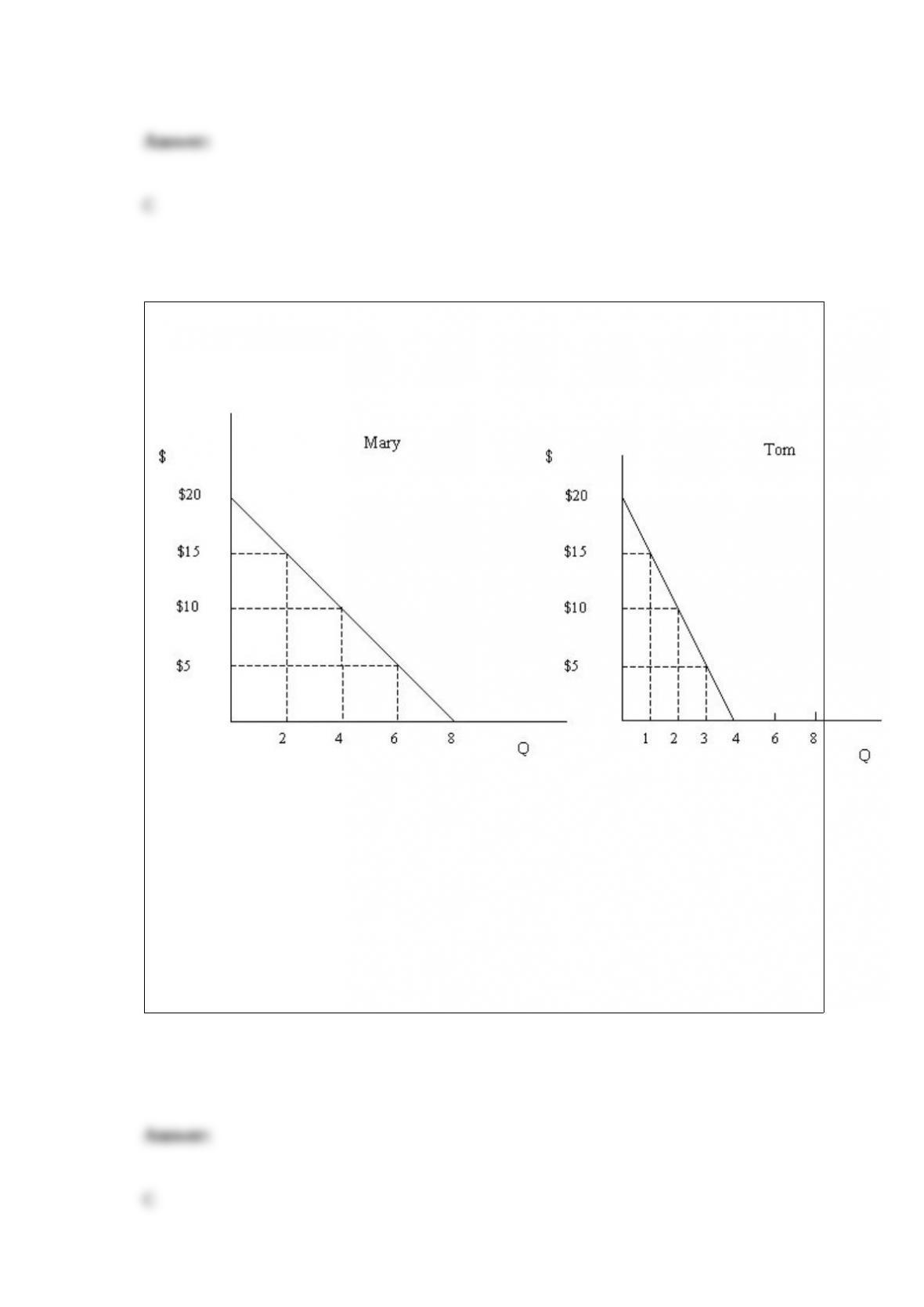

Refer to Figure 4.1 that shows Mary and Tom’s individual demand curves for meals per

week at Fratelli’s Italian Restaurant. Assuming Mary and Tom are the only consumers in

the market, if the market quantity demanded is 3 the price must be:

Figure 4.1

A) $5.

B) $10.

C) $15.

D) $20.

Compared to the short run, the elasticity of demand in the long run is likely to:

A) decrease.

B) remain unitary elastic.

C) increase.

D) remain unchanged.

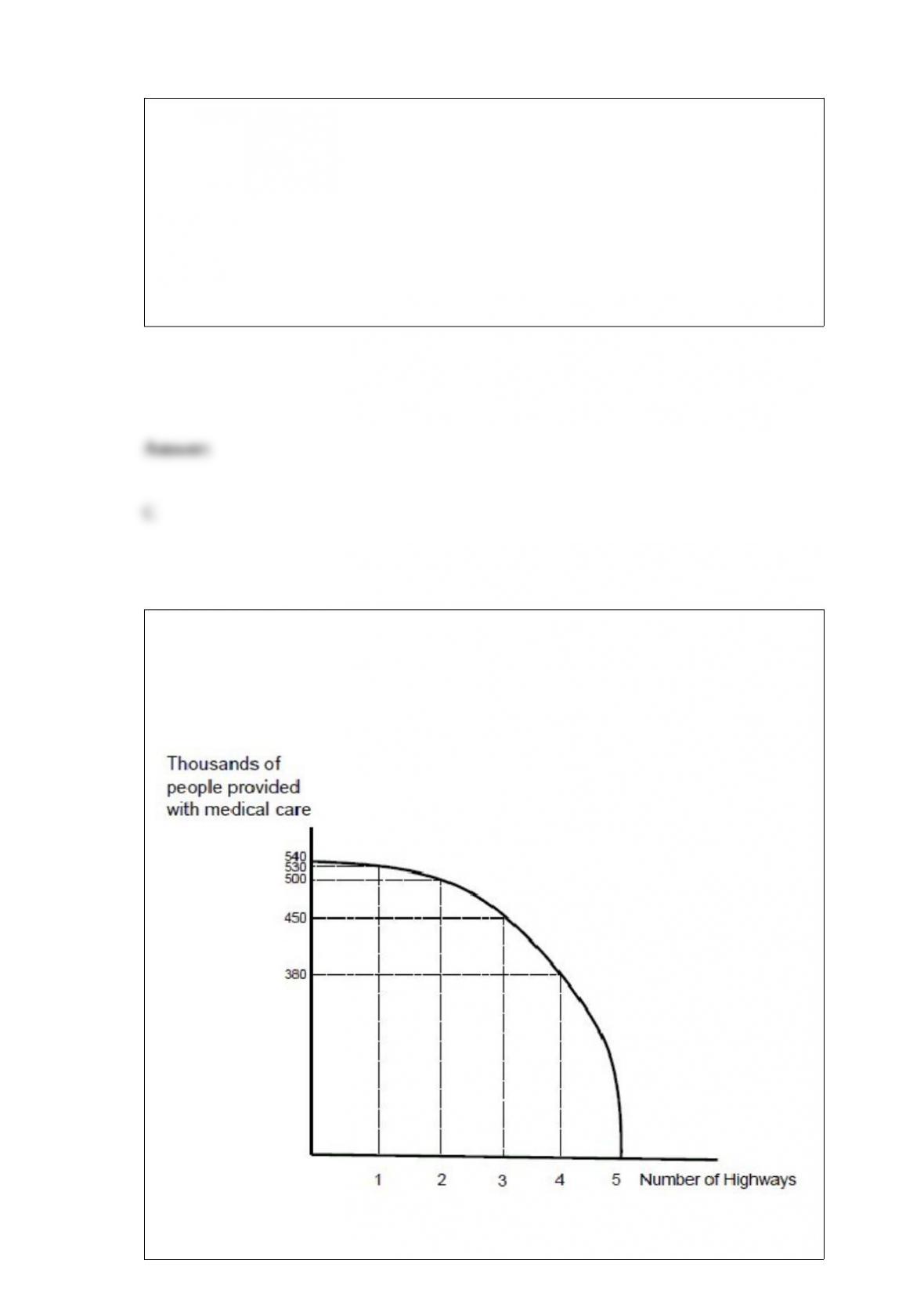

Figure 2.2 presents a production possibilities curve for a country that can either produce

highways or provide people with medical care in a given year. The reason why the

production possibilities curve is shaped as it is (bowed outward) is because inputs for

healthcare and highways are:

Figure 2.2

A) used in precisely the same ratios.

B) substitutable, but not perfectly substitutable.

C) not substitutable at all.

D) perfectly substitutable.

Suppose your bank pays you 5% interest per year on your savings account while prices

increase by 3% per year over that time. Approximately how much nominal value do you

gain by keeping $100 in the bank for a year?

A) $5

B) $2.50

C) $0

D) $2.00

If a firm is operating in a monopolistically competitive market, then in the long run:

A) the firm will earn a zero economic profit.

B) the firm will maximize its profit by producing the output level at which the average

cost is minimized.

C) the firm will maximize its profit by producing the output level at which the marginal

revenue is minimized.

D) all of the above

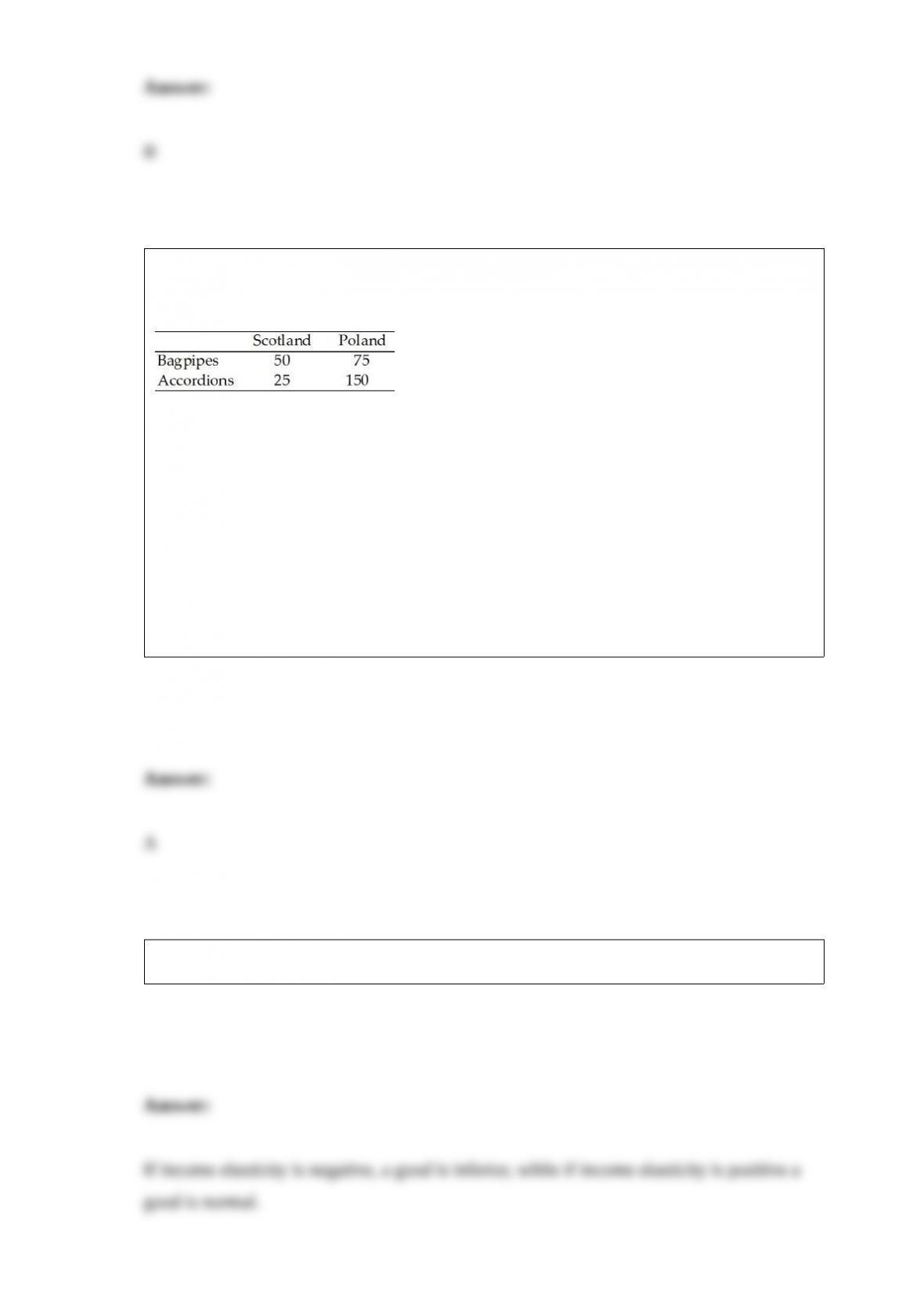

Daily Output of Scotland and Poland

Table 18.1

Refer to Table 18.1. If Scotland produces 50 bagpipes, how many accordions can they

produce for the rest of the day?

A) zero

B) 25

C) 50

D) 1/2

Reductions in pollution from a specific starting level of existing pollution is called:

A) abatement.

B) the EPA.

C) command and control.

D) usage tax.

The cost savings from outsourcing often lead to ________ for consumers and ________

for the outsourcing company.

A) lower prices; less output

B) lower prices; more output

C) higher prices; less output

D) higher prices; more output

The Environmental Protection Agency requires that automakers install equipment in

vehicles that lowers emissions. In most cases a more efficient way of lowering the

pollution generated by cars is to:

A) ban the use of vehicles during daylight hours.

B) create an annual pollution tax on each car.

C) require automakers to develop a car that produces no emissions.

D) None of the abovethis regulation is the most efficient way to reduce automobile

emissions.

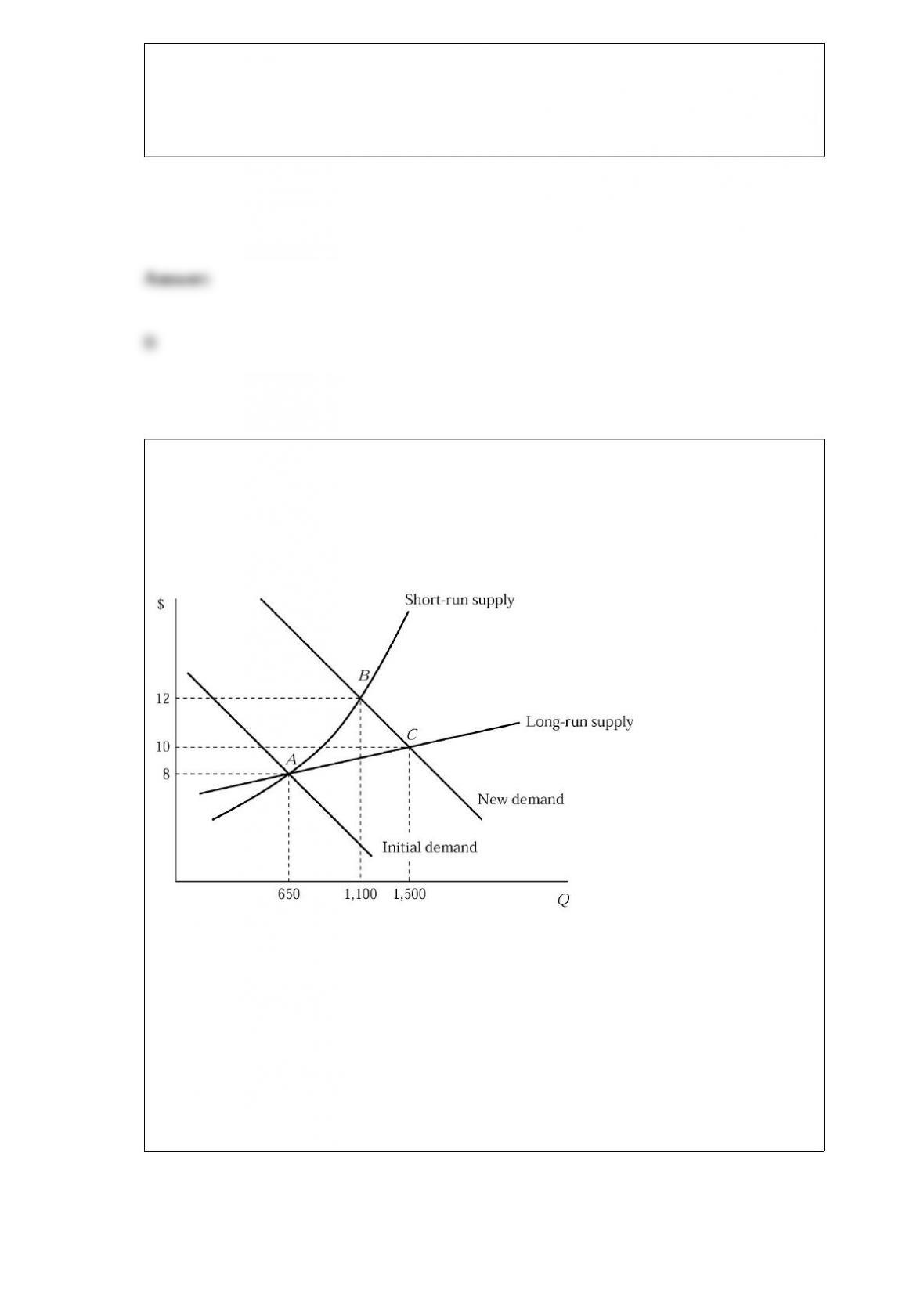

Figure 9.5 shows the short-run and long-run effects of an increase in demand of an

industry. The market is in equilibrium at point A, where 100 identical firms produce 6

units of a product per hour. If the market demand curve shifts to the right, what will

happen to the number of firms in the industry as the industry moves from point A to

point B?

Figure 9.5

A) It increases.

B) It decreases.

C) It remains the same.

D) either A or B or C

The problems of thin markets can be addressed by:

A) guaranteed price matching.

B) increasing the number of sellers in the market.

C) imposing price ceilings.

D) warranties and repair guarantees.

If there is the legitimate threat of entry into a market, then the market is said to be:

A) perfectly competitive.

B) contestable.

C) secure.

D) reactive.

Recall the Application about how lottery contributions are distributed among

income groups to answer the following question(s).

Recall the Application. As a percentage of household income, the amount spent on

lotteries by households of varying income levels is:

A) progressive.

B) regressive.

C) proportional.

D) exponential.

Suppose Robin’s Clock Works produces in a perfectly competitive market. Suppose the

average total cost of clocks is $95, the average variable cost of clocks is $90, and the

price of clocks is $85. If the firm is producing the level of output where marginal cost

equals price, then in the short run the firm:

A) should shut down.

B) should continue to produce since total revenue exceeds total variable cost.

C) is earning a positive economic profit.

D) can increase profit by increasing output.

The owner of Instant Printing, a firm that prints business cards, tells you that as a result

of an increase in the wage rate of printer operators he has reduced the amount of output

he produces and the amount of capital he uses. How would you respond to this?

A) You should tell him that this doesn’t make any economic sense because according to

the input-substitution effect he should have substituted toward capital and away from

labor.

B) This seems logical, because the output effect of an input price increase would cause

a firm to demand less of all inputs, not just the input whose price increased.

C) You should tell him that instead of reducing output and the demand for all inputs, he

should increase output and the demand for inputs so that he can meet the higher labor

costs by generating more revenue.

D) You tell him that the input-substitution effect and the scale effect both suggest that

he decrease the amount of capital he uses when his workers’ wage rate increases.

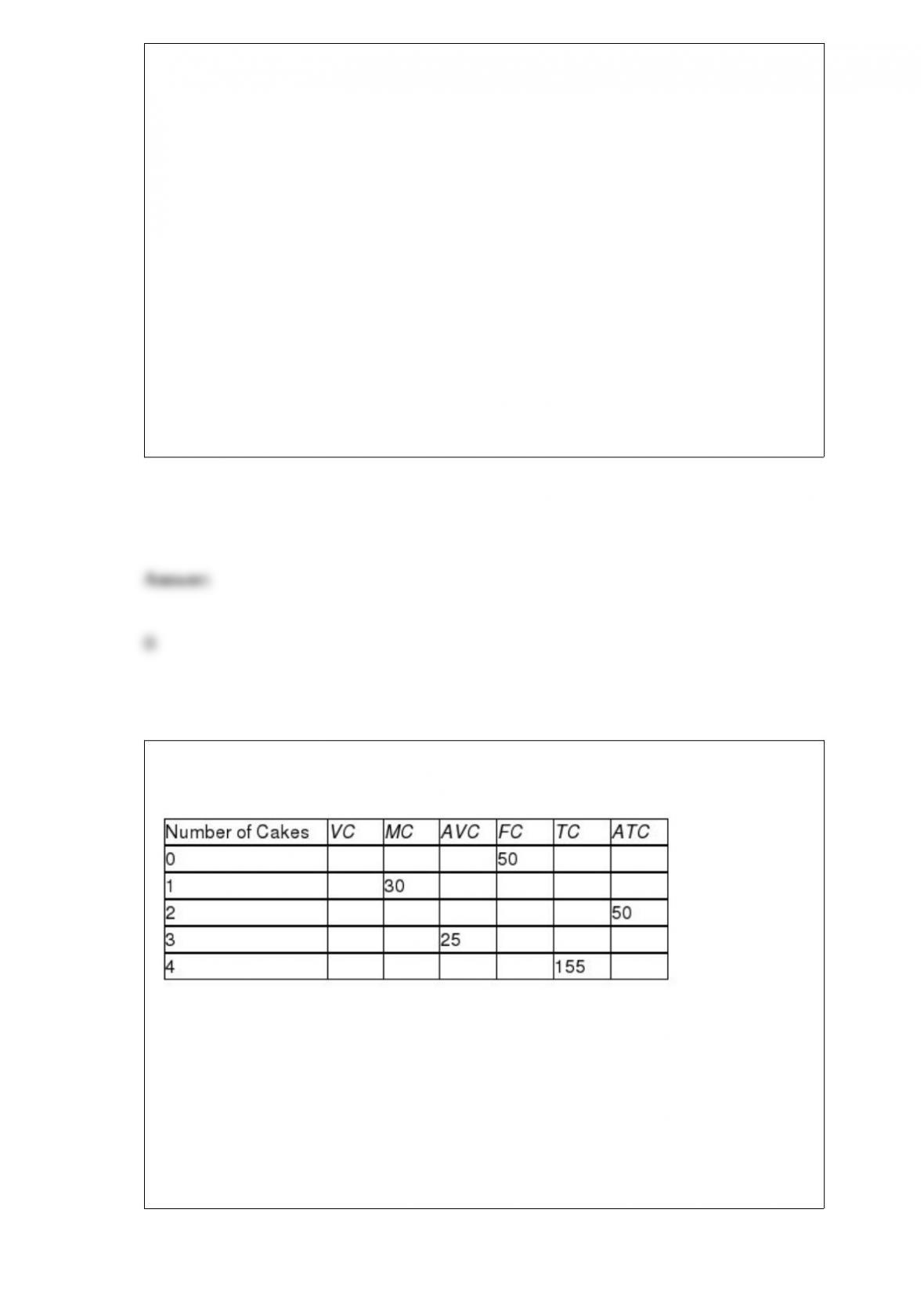

Table 8.3 presents the cost schedule for Candy’s Cakes. If Candy produces three cakes,

Candy’s marginal costs are:

Table 8.3

A) $0.

B) $25.

C) $41.67.

D) $75.

Daily Output of Scotland and Poland

Table 18.1

Refer to Table 18.1. The opportunity cost of an accordion in Scotland is:

A) 2 bagpipes.

B) 1/2 bagpipe.

C) 6 bagpipes.

D) 1/3 bagpipe.

How do you interpret the value of income elasticity?

Global warming has become a major international environmental issue. Using the

concept of externality, explain why countries around the world seldom reach an

agreement to reduce the use of fossil fuels.

Explain the real-nominal principle.

What is a tariff?

Tyler’s wage rises and he chooses to increase the number of hours he supplies to the

labor market. What does this imply about the relative sizes of the substitution effect and

the income effect? Explain.

Some states have laws that require that used car dealers give buyers a 30-day period

during which they can return cars that are discovered to be lemons (low-quality). Whom

do laws like this help? Whom do they hurt?

“If the amount of product differentiation in a monopolistically competitive industry is

very small, the outcome in that market will not be very different than if it were a

perfectly competitive industry.” Explain.

A firm producing ink pens reports the production information in Table 17.5. The pens

sell in a competitive market at a price of $0.50 each. The firm hires workers in a

competitive labor market at a wage of $9 per hour. How many workers should the firm

hire? Explain your answer.

Table 17.5

A decrease in the cost of labor or some other input will make the production of a

product less costly and more profitable at a given price, so producers will supply more

of it. This is an example of ________.

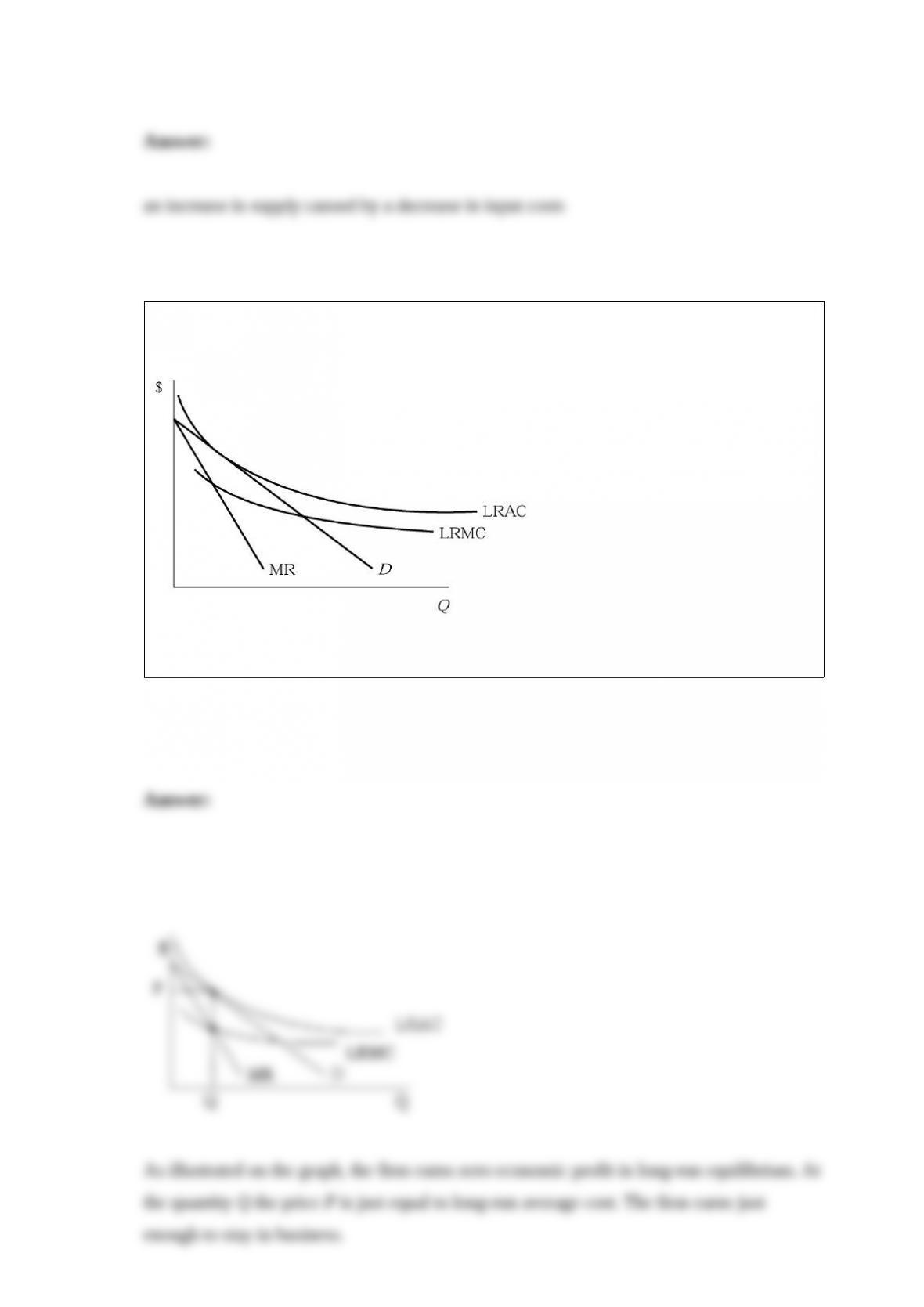

Referring to Figure 11.6, how much economic profit does the monopolistically

competitive firm earn in long-run equilibrium?

Figure 11.6

Explain the conditions that must be satisfied for a monopolistically competitive industry

to be in long-run equilibrium.

What is rent seeking?

Suppose that a paper producer is dumping waste into a nearby river. The government

imposes a tax to correct for this external cost. What will be the effects of this pollution

tax on the market for paper in a competitive market?

How does a tax credit for hybrid vehicles reduce the externalities associated with

automobiles?

What is a marginal cost?