A consumer’s demand curve for pizza is identical to his total value curve for pizza.

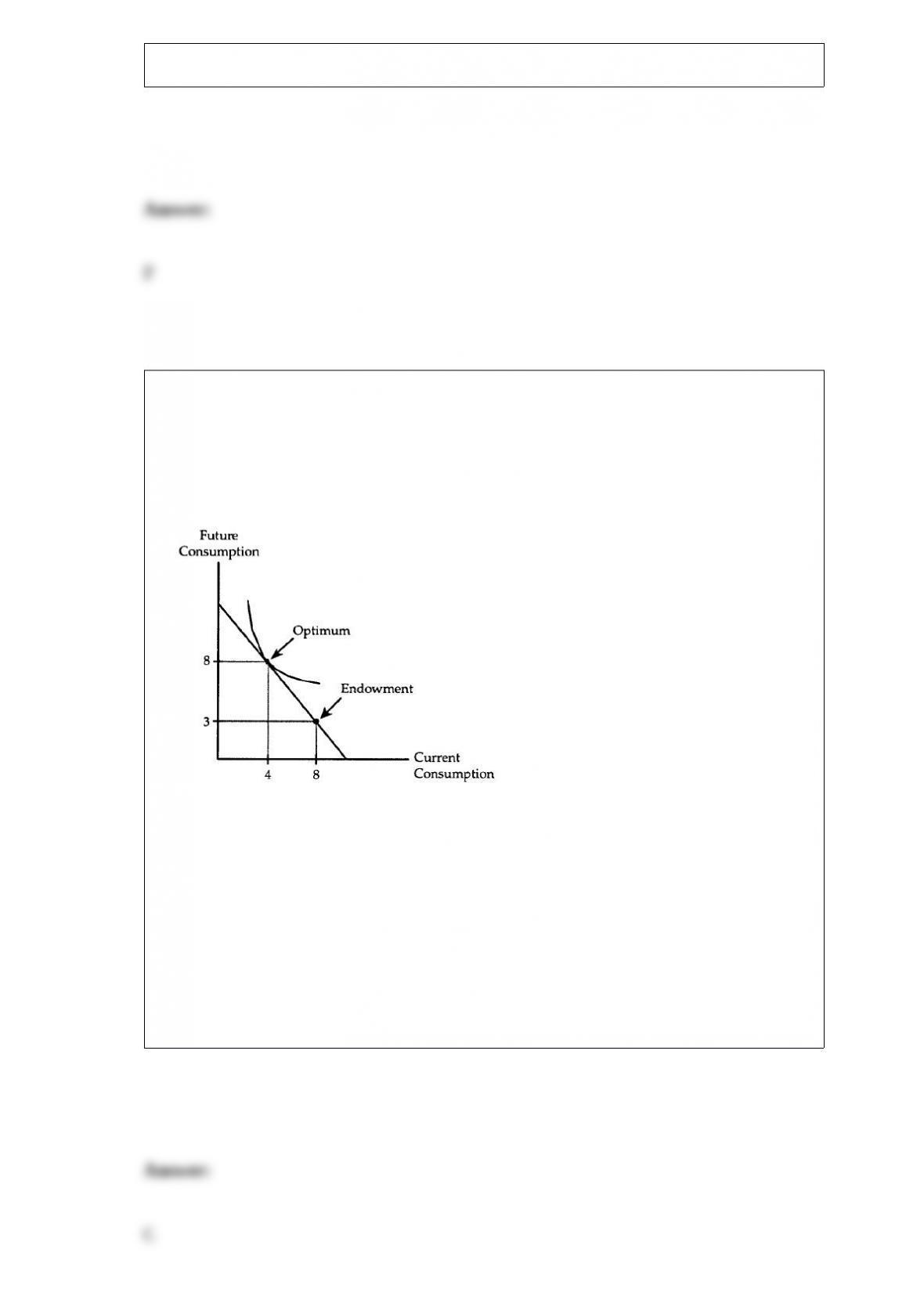

Current and Future Consumption

The following questions refer to the accompanying diagram, which shows a consumer’s

choice between current and future consumption.

The diagram shows the case of a

a. representative agent.

b. net borrower.

c. net lender.

d. disequilibrium situation.

The simultaneous imposition of a 3 cent sales tax and a 5 cent excise tax on the sale of a

cup of coffee would have the same effect on coffee sales as:

a. a 2 cent subsidy.

b. a 2 cent excise tax .

c. a 3 cent excise tax .

d. an 8 cent excise tax.

If a firm hires workers up to the point where the value of their marginal product equals

their wage, then the firm is

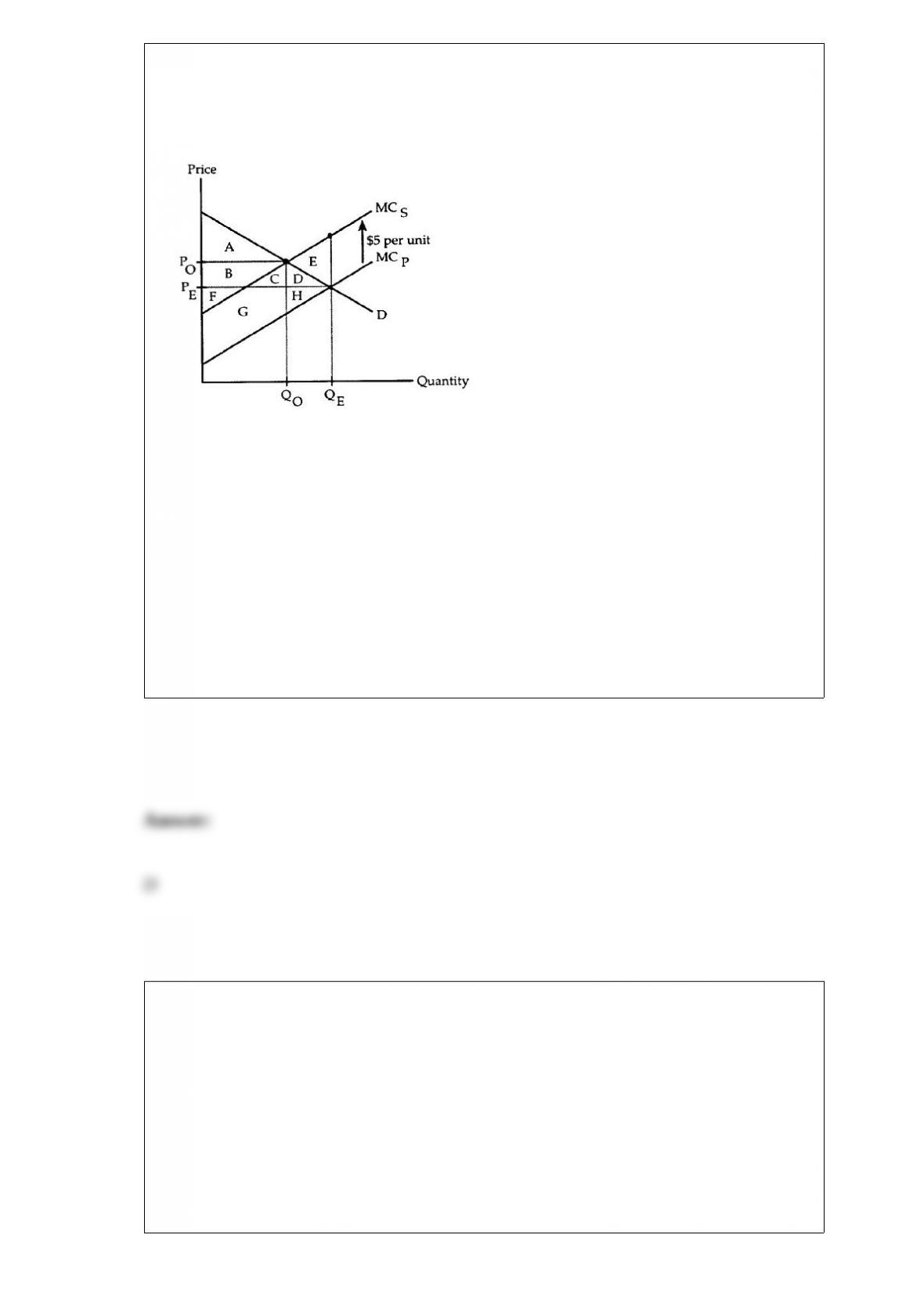

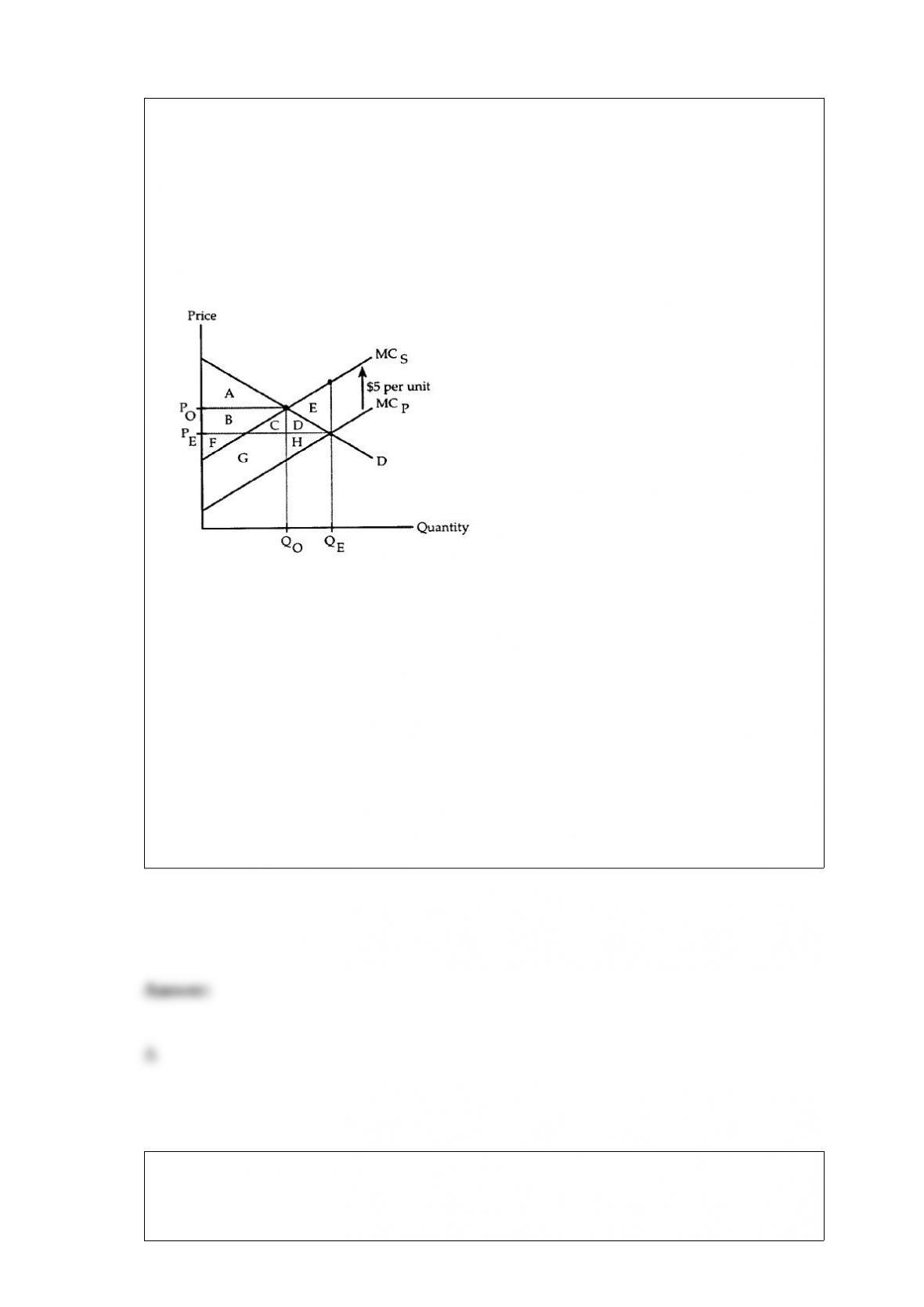

Negative Externality

The following questions refer to the accompanying diagram, which shows the effects of

a negative externality created by an industry’s production. The equilibrium quantity in

the absence of any attempt to internalize the externality is QE, and the optimal quantity

according to a Pigovian analysis is QO.

Suppose there is no attempt to internalize the externality. Pigovian analysis indicates

that the externality creates a deadweight loss equal to

a. area C + D + E + G + H.

b. area D + E + H.

c. area C + D + G + H.

d. area E.

The substitution effect shows that when the wage rate increases

a. an additional hour of labor is not worth pursuing.

b. an additional hour of leisure is now less costly in terms of foregone consumption.

c. an additional hour of leisure is now more expensive in terms of foregone

consumption.

d. there will be intertemporal substitution.

Insurance companies are not permitted to require AIDS tests as a precondition for

coverage, so they do not know whether or not the people they insure have already

contracted HIV (the virus that causes AIDS). This situation is an example of

a. signaling.

b. adverse selection.

c. the principal-agent problem.

d. moral hazard.

Relative to before the price ceiling, how much surplus do producers lose because of the

ceiling?

a. Area D+E+H

b. Area D+E

c. Area D+E+F

d. Area H.

Game Matrix I

The following questions refer to the game matrix below.

Player A can play the strategies and , and Player B can play the

strategies and .

The only outcome in this game that is not Pareto optimal is

a. the upper left-hand corner.

b. the upper right-hand corner.

c. the lower left-hand corner.

d. the lower right-hand corner.

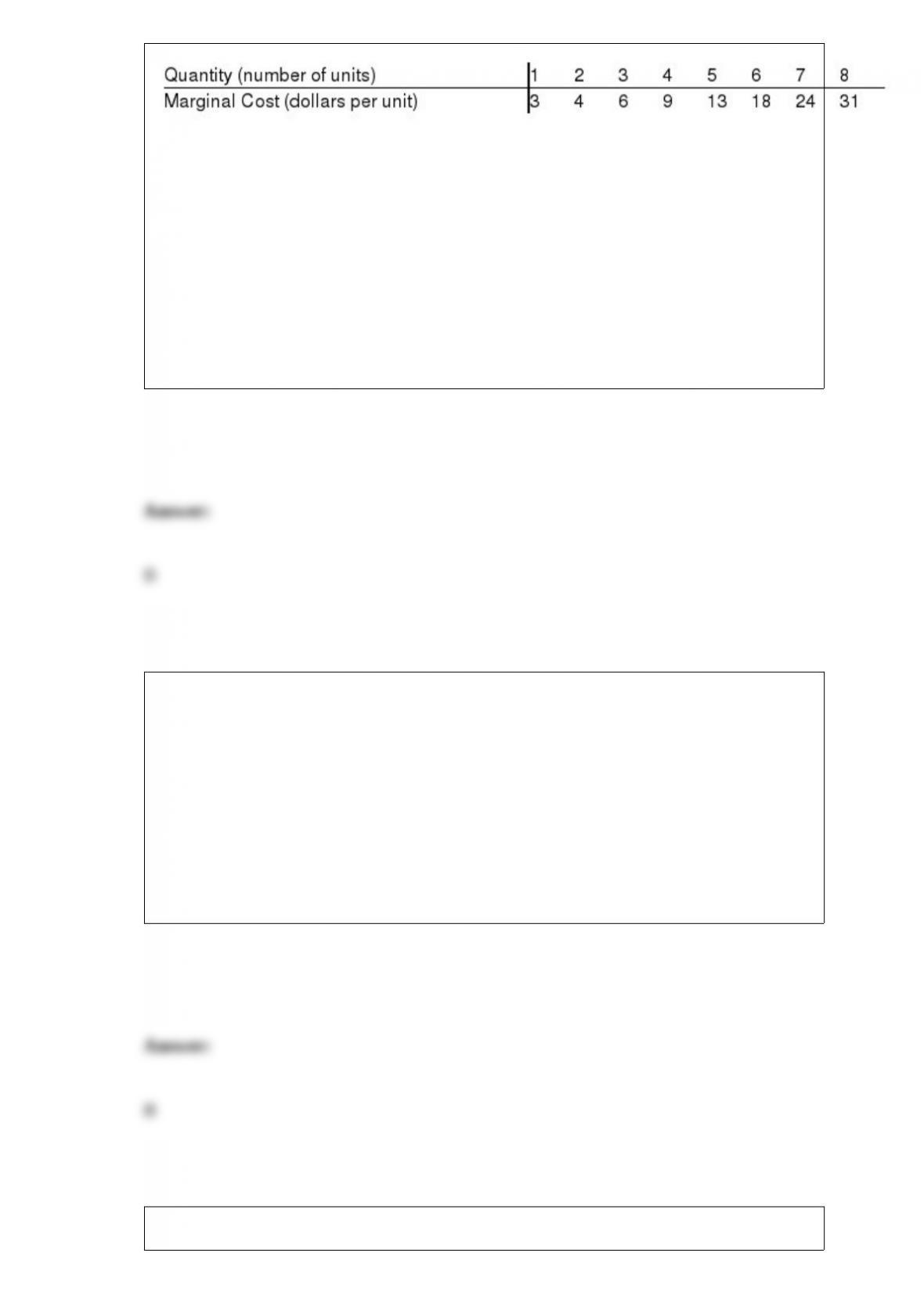

Marginal Cost of Production

The following questions refer to the following table which shows a firm’s marginal cost

of production.

Suppose the firm has $20 in fixed costs, and demand for the firm’s product is horizontal

at a price of $18 per unit. What is the firm’s maximum profit?

a. $33.

b. $35.

c. $73.

d. $88.

The competitive firm’s long-run supply curve

a. is always perfectly horizontal.

b. includes only that part of the long-run marginal cost curve that lies above long-run

average cost.

c. includes only that part of the long-run marginal cost curve that is sloping upwards.

d. is identical to its long-run average cost curve.

When the supply of land is perfectly inelastic, the economic burden of an annual tax on

land

a. falls entirely on the people who owned land when the tax was imposed.

b. is passed on to future buyers of land in the form of higher prices.

c. is split between present and future landowners.

d. cannot be determined without information on the elasticity of the demand for land.

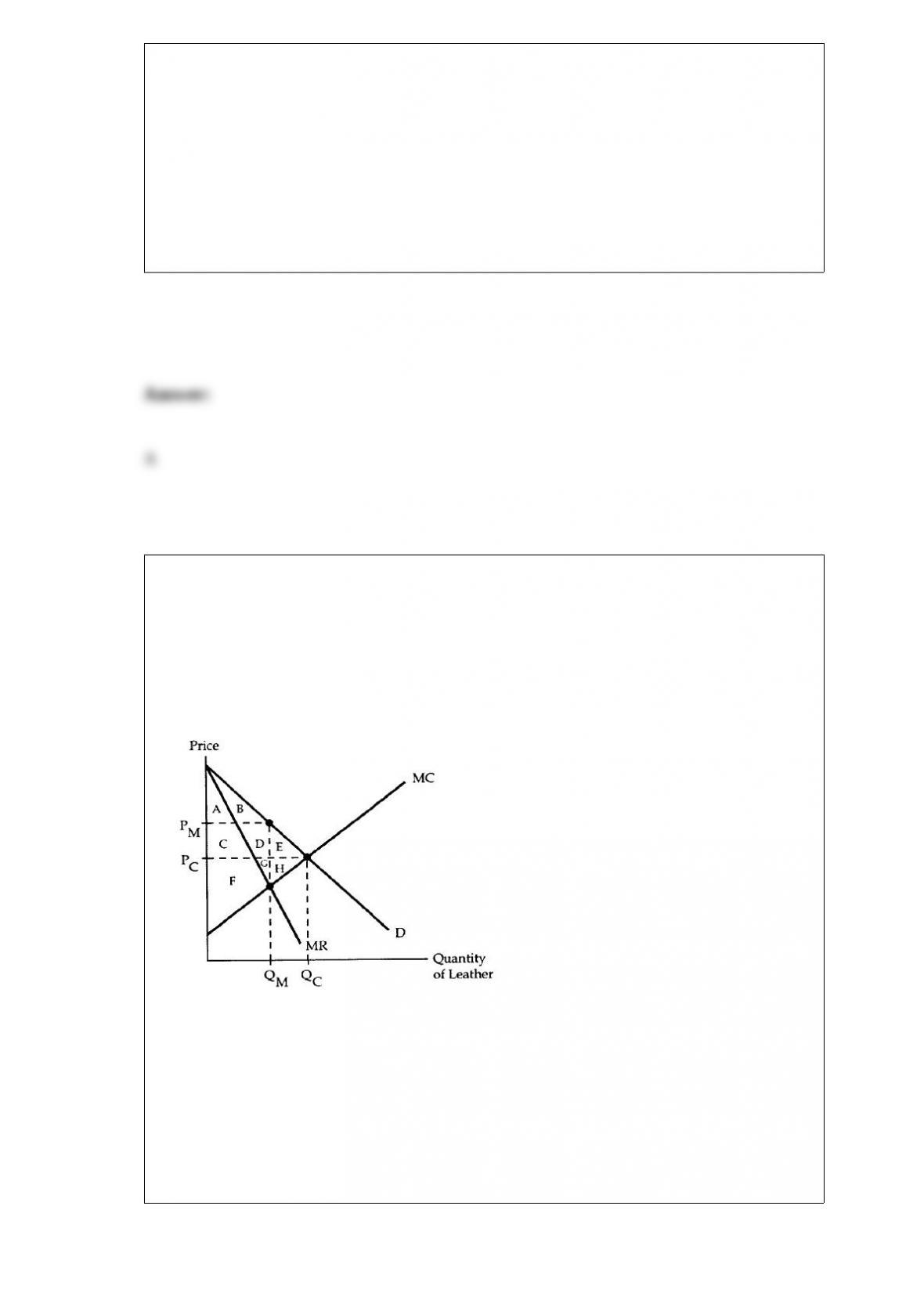

Refer to Monopoly Supplier and ManufacturerMonopoly Supplier and Manufacturer

The following questions refer to the accompanying diagram, which shows a monopoly

leather supplier selling leather to a monopoly shoe manufacturer. The leather supplier

initially produces QM and charges the shoe manufacturer PM. Then the leather supplier

acquires the shoe manufacturer in a vertical merger.

a. Area A + B.

b. Area A + B + C + D + E.

c. Area F + G + H.

d. Area A + B + C + D + E + F + G + H.

If increased capital usage reduces the firm’s short-run demand for labor, then

a. labor is a regressive factor.

b. labor and capital are complements in production.

c. labor and capital are substitutes in production.

d. labor is a Giffen factor.

If a firm’s marginal cost exceeds its marginal revenue, then

a. the firm’s profit is negative (i.e., the firm is suffering losses).

b. the firm should shut down its operations.

c. cutting back production will increase the firm’s profit.

d. the firm should reduce its per-unit cost by increasing its output.

Suppose there are only two goods: lettuce and grapes. In California, a head of lettuce

sells for 50¢ and a bunch of grapes sells for $1. In Nebraska, 25¢ must be added to

these absolute prices to cover transportation costs. How do these transportation costs

affect the relative prices of lettuce and grapes?

a. The transportation costs do not affect the relative prices of lettuce and grapes.

b. The relative prices of lettuce and grapes are both higher when transportation costs are

added.

c. The addition of transportation costs makes the relative price of grapes higher and the

relative price of lettuce lower.

d. The transportation costs raise the relative price of lettuce but lower the relative price

of grapes.

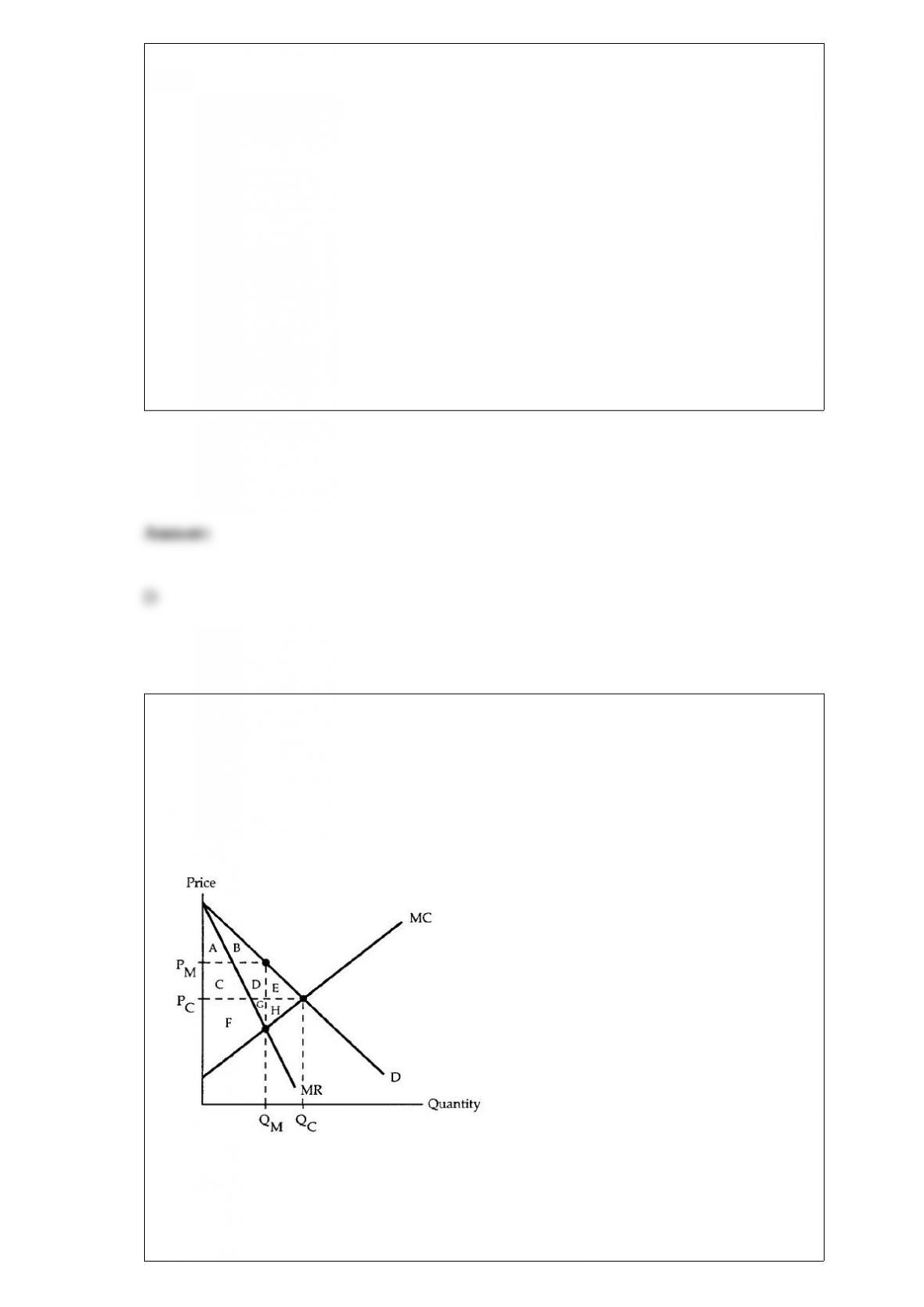

Market Diagram

The following questions refer to the accompanying market diagram. PC and QC are the

equilibrium price and quantity if the firm behaves competitively, and PM and QM are

the equilibrium price and quantity if the firm is a simple monopoly.

Of the surplus that the consumers lose because there is a monopoly (and not perfect

competition), how much has become deadweight loss?

a. Area E

b. Area H

c. Area E + H

d. Area C + D + H

When a simple monopolist chooses to sell an additional unit of a good or service

a. marginal revenue will be equal to the going market price.

b. marginal revenue will always be negative.

c. it will only have to lower its price on the additional unit.

d. it will have to lower its price on the additional unit and on all other units.

A solution concept for a game is

a. a measurement of the game’s complexity.

b. a way of determining whether the first or second player has an advantage.

c. a normative judgment of the desirability of the game’s outcome.

d. a rule for predicting the game’s outcome when it is actually played.

By and large, small countries tend to benefit the most from international trade because

a. their citizens tend to be the most different from the rest of the world.

b. they are unable to achieve self-sufficiency.

c. they can collect large amounts of tariff revenue from trading with larger countries.

d. their citizens are more likely to prefer the high-quality, capital-intensive goods

available only from larger countries.

If the price of marshmallow exceeds the marginal value that the consumer places on

marshmallows, then

a. the consumer is at the optimum.

b. the consumer’s level of satisfaction would increase if he buys more marshmallows

and less of other goods.

c. a surplus of marshmallows exists in the market.

d. the optimum contains fewer marshmallows than the consumer is currently buying.

When a policy creates the most social gain possible, it is considered “best” by the

a. efficiency criterion.

b. Pareto criterion.

c. Edgeworth criterion.

d. maximin criterion.

In order to practice any form of price discrimination, a monopoly must be able to

a. identify the maximum price that each customer is willing to pay.

b. separate its customers into distinct groups.

c. prevent resale of its product.

d. establish a legal barrier to entry.

Suppose that, in a sequential game, the first player chooses the strategy with the highest

payoff, taking into account an optimal response from the second player. The outcome

that results is

a. a Nash equilibrium.

b. Pareto optimal.

c. a Prisoners’ Dilemma.

d. a Stackelberg equilibrium.

An industry’s output is produced at the lowest possible cost when

a. firms’ marginal costs are equal.

b. firms minimize their average costs.

c. all firms earn the same profit.

d. output is evenly divided among the industry’s firms.

Which of the following could decrease the equilibrium price but increase the

equilibrium quantity of apples?

a. Higher wages are paid to the agricultural workers who harvest the apples.

b. A rise in the cost of treating pests destroying apples.

c. Many new apple orchards are planted.

d. An increase in the market supply of grapefruit.

When will a wage increase cause a firm to produce more output in the long run?

a. Always.

b. When labor and capital are complements in production.

c. When labor is a regressive factor.

d. Never.

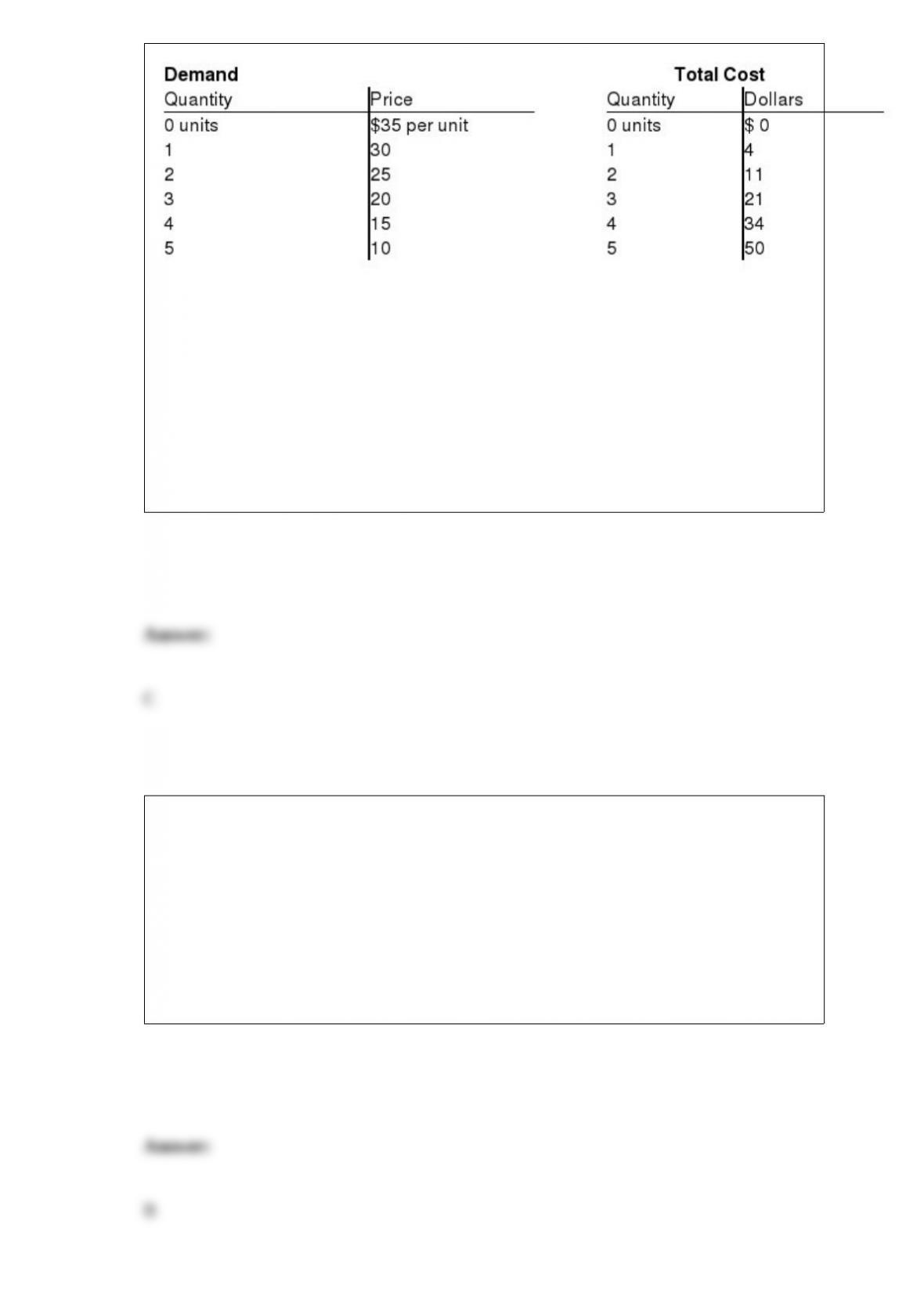

Demand and Total Cost of Production

The following questions refer to the following tables which show the demand for a

firm’s product and the firm’s total cost of production.

The marginal cost of producing the third unit is

a. $21 per unit.

b. $20 per unit.

c. $10 per unit.

d. $7 per unit.

According to Coase’s analysis, when are private costs and social costs the same?

a. Always.

b. When there are no transactions costs.

c. When property rights are clearly defined.

d. Never.

Negative Externality

The following questions refer to the accompanying diagram, which shows the effects of

a negative externality created by an industry’s production. The equilibrium quantity in

the absence of any attempt to internalize the externality is QE, and the optimal quantity

according to a Pigovian analysis is QO.

Suppose there are no transactions costs. Also suppose the externality is internalized

when the damaged parties offer producers a bribe of $5 per unit to reduce their

production. Coasian analysis indicates that social gain in this situation will equal

a. area A + B + F.

b. area A + B + F – E.

c. area A + B + C + D + F + G + H.

d. area A + B + C + F + G.

You are deciding whether or not to take your car on a 1,500 mile highway trip. Which

of the following is the least likely to affect your decision?

a. The price of gasoline.

b. The cost of oil changes.

c. Your annual insurance payment.

d. Highway tolls.

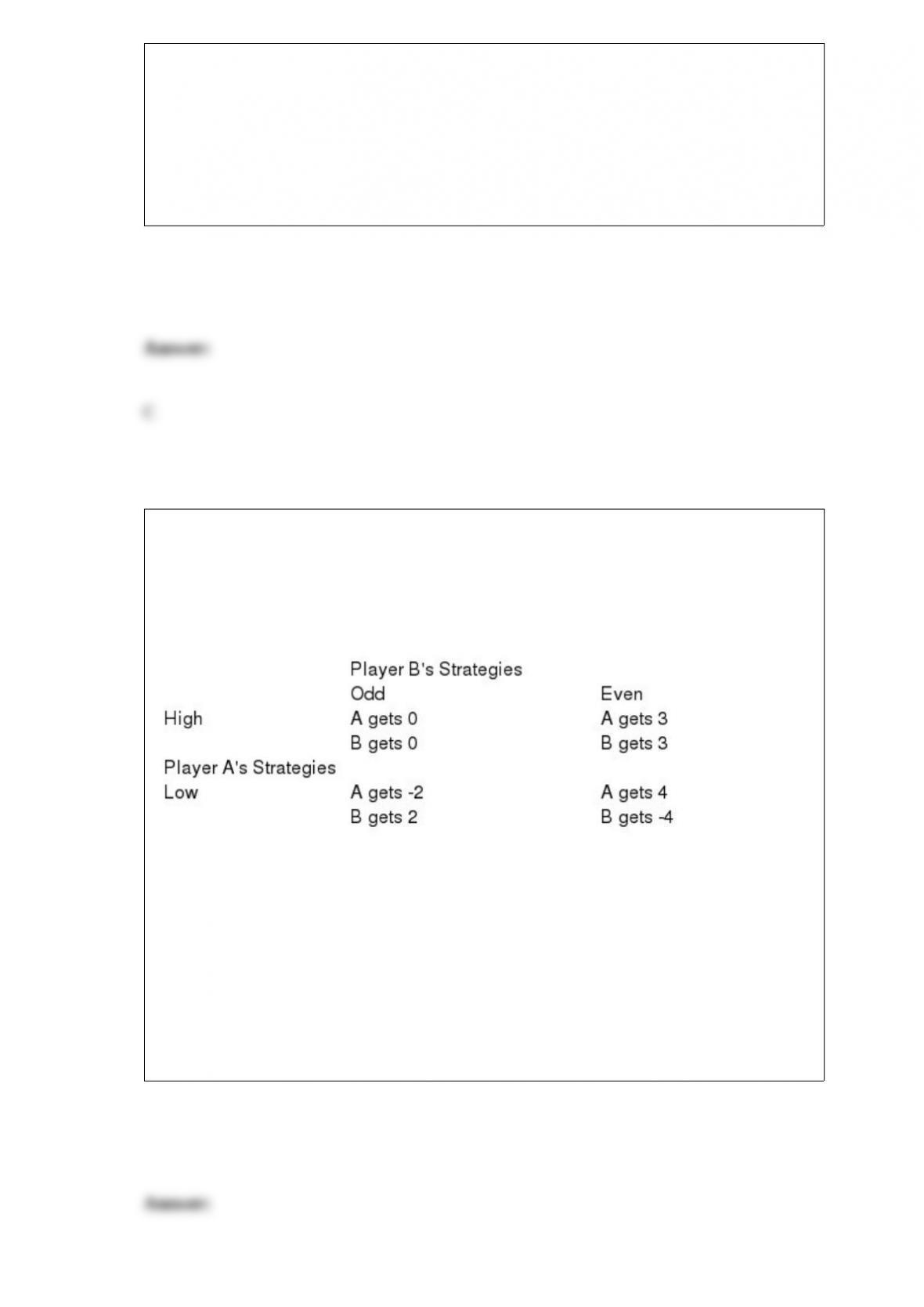

Game Matrix II

The following questions refer to the game matrix below. Player A can play the strategies

“High” and “Low,” and Player B can play the strategies “Odd” and “Even.”

Which outcomes in this game are Nash equilibria?

a. The upper right-hand corner only.

b. The upper left-hand corner only.

c. Both the upper right-hand and lower left-hand corners.

d. This game has no Nash equilibria.

When the Pareto criterion is used to choose between different policies, any

recommendation requires unanimous agreement.

Moving down and to the right on an isoquant tells us how much quantity increases as

inputs increase.

Inputs owned by the firm are excluded when calculating its costs.

A change in the price of bonds causes a change in interest rates.

If the consumer chooses not to purchase potatoes, then the marginal value of potatoes

must be less than or equal to the relative price of potatoes.

Only variable costs are relevant to a firm’s decision to shut down.

Private markets tend to undersupply nonrivalrous goods because of free riding.

If all inputs are variable in the long run, then there cannot be decreasing returns to

scale. But if some inputs remain fixed in the long run, then decreasing returns to scale

can occur.

Marginal value equals relative price at the consumer’s optimum, even if the optimum is

a corner solution.

If the price of a non-Giffen good falls, then the income effect causes a rise in the

quantity demanded.

A stock that is guaranteed to increase in value is risk-free.

Economists attempt to understand firm behavior by making the generalization that firms

act to maximize growth.

Demand in a perfectly competitive market is Q = 100 – P. Supply in that market is Q = P

– 10. What is the market equilibrium price and quantity? Given that price and quantity,

how much consumer surplus, producer surplus, and deadweight loss is there? If the

government imposes a $40 price ceiling, what quantity will be produced and sold?

Assuming that those who value the good the most actually get after the ceiling is

imposed, how much consumer surplus, producer surplus, and dead-weight loss is there?

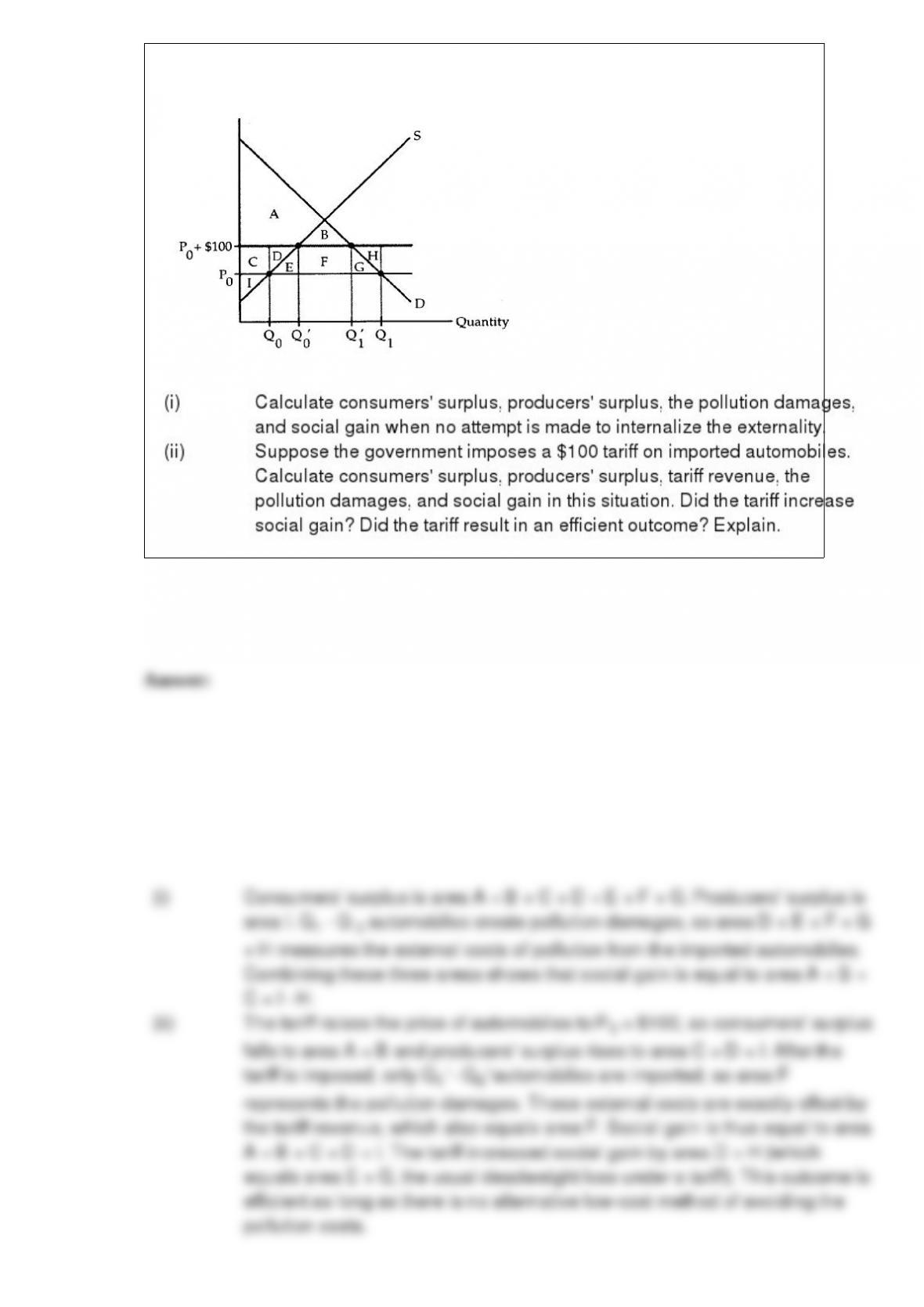

The accompanying diagram shows the U.S. market for automobiles. P0 is the world

price of automobiles, Q0 is the quantity of American automobiles produced, and Q1 –

Q0 is the quantity of automobiles imported. Consumers are indifferent between

American and imported automobiles, but each imported automobile creates $100 of

pollution costs.

How is a compensated demand curve different from an ordinary demand curve? Why

must the law of demand always hold for one while it may be violated for the other?

Firms’ total output is higher in the Cournot oligopoly model than in the Bertrand

oligopoly model.

The fact that grocery stores and convenience stores sell physically identical products for

different prices is a violation of the “law of one price.”

When a consumer spends all of the income, it must be true that they are consuming a

basket of goods on their budget line.

The producer of a public good creates a positive externality, so that such goods tend to

be overproduced.