Private goods can have external benefits.

Labor skills are determined by innate ability, education and work experience.

A maximum price below the market equilibrium price will raise the total surplus of the

market.

The main purpose of advertising is to make a product appealing.

A bumper crop of wheat could be bad news to farmers if the price elasticity of demand

for wheat is greater than one.

What matters to people is the face value of money or income.

In essence, a pollution tax places a price on the right to pollute.

The cereal industry is an example of a oligopolistic industry.

To determine an appropriate congestion tax, an economist has to assume that people

respond to incentives.

The U.S. currently uses marketable permits to regulate automobile pollution.

Marginal revenue product equals marginal revenue times the price of output.

Using assumptions to make things simpler and focus attention on what really matters is

like using a road map to plan a trip.

The law of diminishing returns applies only in the long run when the fixed cost can be

flexible.

The government weighs the potential cost savings resulting from a merger against the

potential anticompetitive problems to determine whether or not to allow a merger to

take place.

In 1992, Hurricane Andrew caused the price of ice in Florida to increase in the long run.

Recent experiments by neuroscientists have shown that the more a person thinks about

the health consequences of an unhealthy food like a donut, the higher the perceived

benefit of the unhealthy food.

Automobiles create externalities when they create congestion and waste time of others.

A possible benefit of unions is lower turnover among workers, which in turn leads to

lower training costs.

Producer surplus increases as the price of a good decreases.

One result of adverse selection in the used car market is that few plums (high-quality)

are sold.

The opportunity cost of getting a master’s degree in engineering equals the tuition plus

the cost of books.

Among the problems associated with subsidizing an industry in the hope of establishing

a worldwide monopoly is that if two nations subsidize firms in the same industry, each

could lose money.

If peanut butter and jelly are complements, then an increase in the price of peanut butter

will reduce the demand for jelly.

Another source of inefficiency from a monopoly is the use of resources to acquire

monopoly power.

A price floor above the equilibrium price causes excess quantity demand.

All patent protected products would not have been developed without patent protection.

If marginal utility is negative consuming an additional unit of a product will cause total

utility to decline.

The principle of voluntary exchange is the concept that a voluntary exchange between

two people makes both people better off.

Negative relationships are also referred to as inverse relationships.

If a person has a comparative advantage in some activity, she must have an absolute

advantage in that activity as well.

There is a negative relationship between the price of labor and the quantity of labor

supplied, ceteris paribus.

The price elasticity of demand measures the responsiveness of changes in price to the

quantity demanded.

If incomes increase and hotdogs are inferior goods, then:

A) the demand for hotdogs increases.

B) the demand for hotdogs decreases.

C) the quantity demanded for hotdogs decreases.

D) the quantity demanded for hotdogs increases.

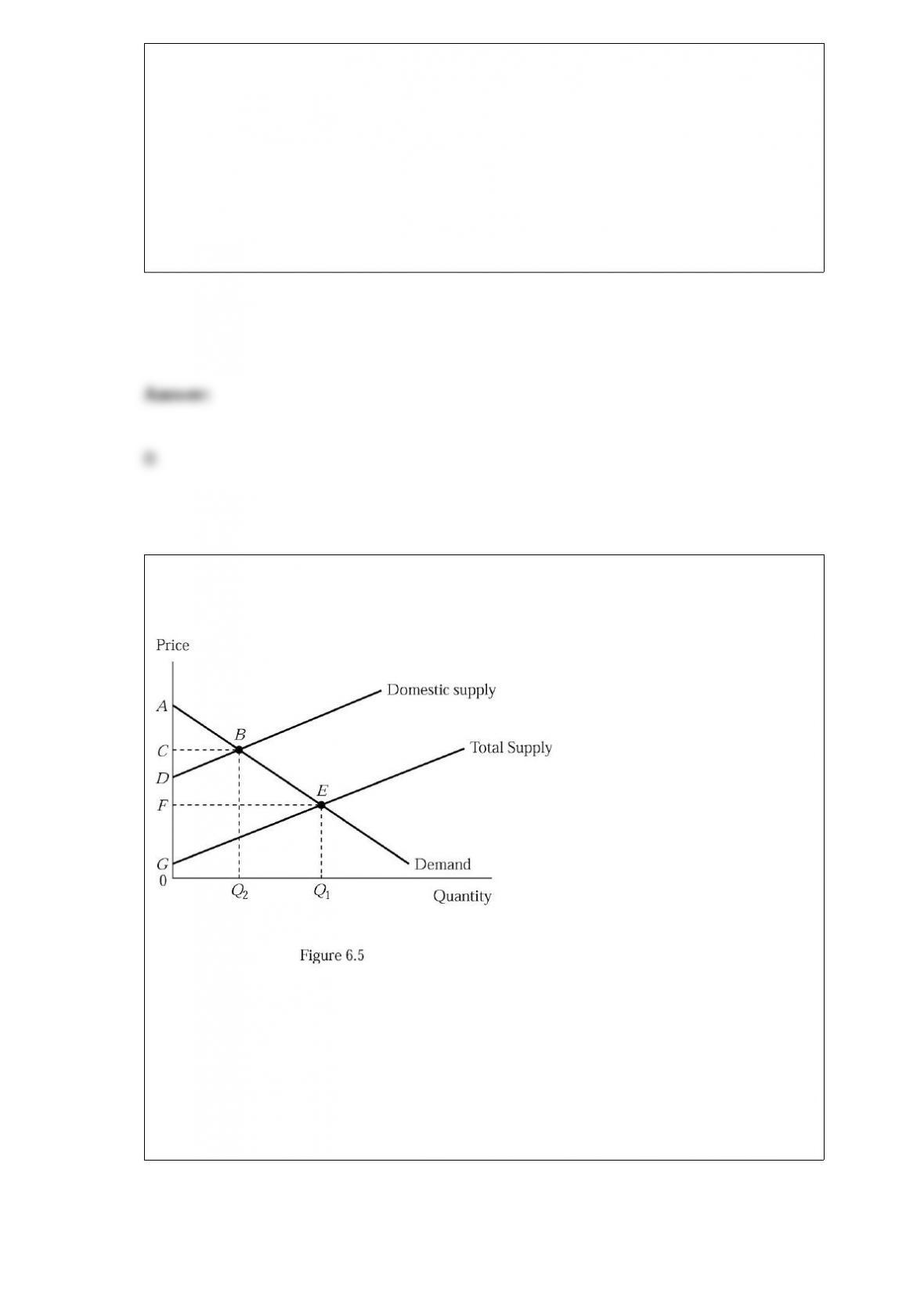

Figure 6.5 illustrates the market for sugar. With free trade, the price of sugar would be

at point:

A) C.

B) D.

C) F.

D) G.

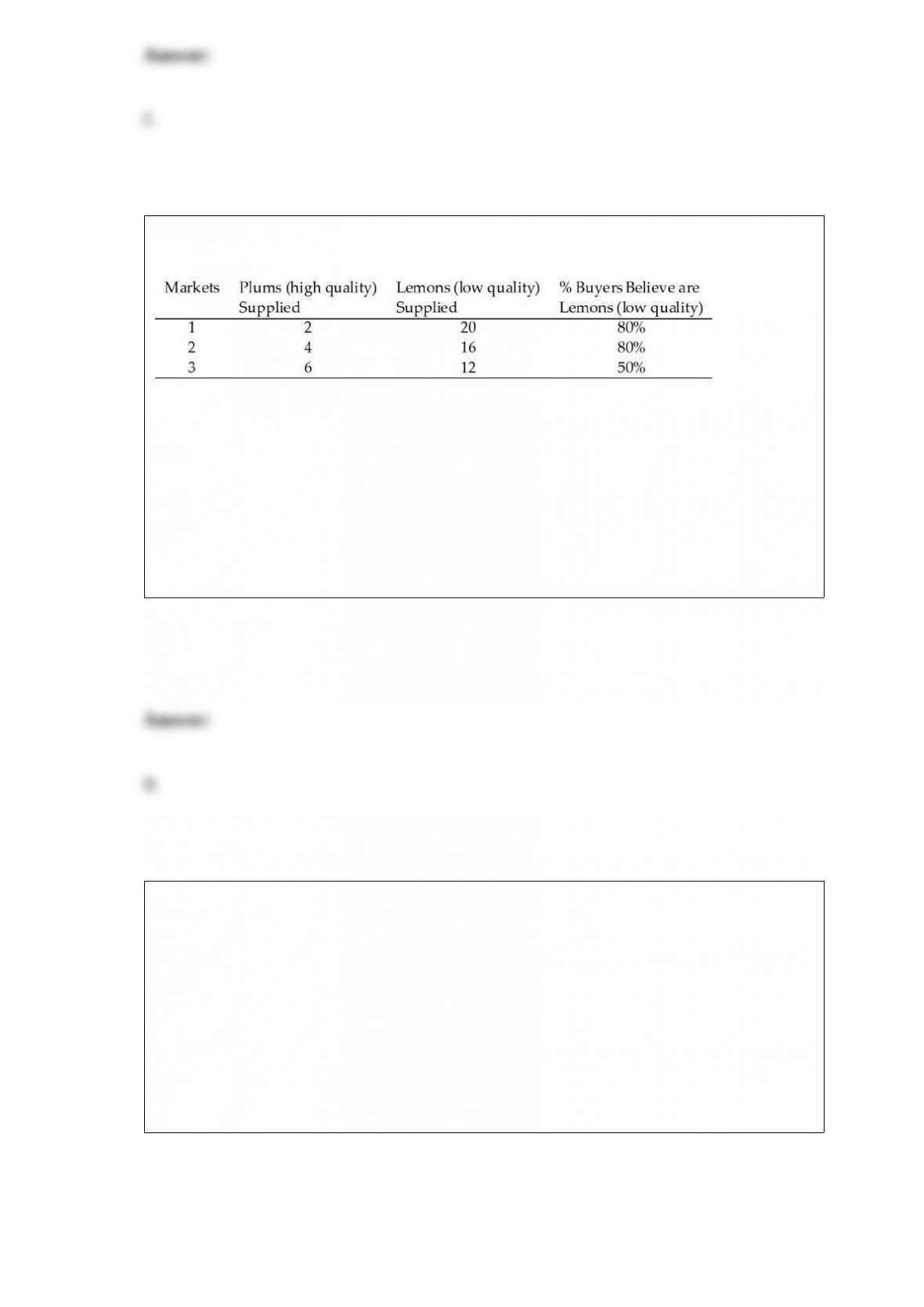

Refer to Table 14.4. In which market do buyers underestimate the chance of getting a

lemon?

Table 14.4

A) 1 and 2 only

B) 1 and 3 only

C) 2 and 3 only

D) none of the above

The value of money or income in terms of the quantity of goods the money can buy is

called its:

A) real value.

B) marginal value.

C) nominal value.

D) implicit value.

If your firm is producing a good at a level where marginal revenue equals marginal

cost, and price is less than average variable cost, then in the short run your firm should:

A) shut down and suffer a loss equal to your fixed costs.

B) continue to produce, but increase output.

C) continue to produce the same amount.

D) continue to produce, but decrease output.

The quantity supplied of bagels is 100 at the unit price $1. Suppose the price elasticity

of supply by the initial value method is 1.5, and you would like to induce sellers to

increase the quantity of bagels supplied to 130. Then the new price for bagels must be:

A) $11.

B) $10.20.

C) $1.20.

D) $1.10.

Recall the Application. During “happy hour,” many bars and restaurants face an

increase in demand for food and drink, and these establishments often cut prices during

these times of increased demand. When this demand increases, the bars and restaurants

face a ________ demand curve.

A) perfectly elastic

B) perfectly inelastic

C) more elastic

D) more inelastic

Which of the following characteristics are of a linear demand curve?

A) It has a constant slope.

B) It has a constant elasticity of demand.

C) The upper half of the liner demand curve is inelastic.

D) all of the above

The price of oranges has risen dramatically. Which of the following is likely to happen?

A) The quantity of oranges supplied will increase.

B) The quantity of oranges supplied will decrease.

C) The supply of oranges will decrease.

D) The supply of oranges will increase.

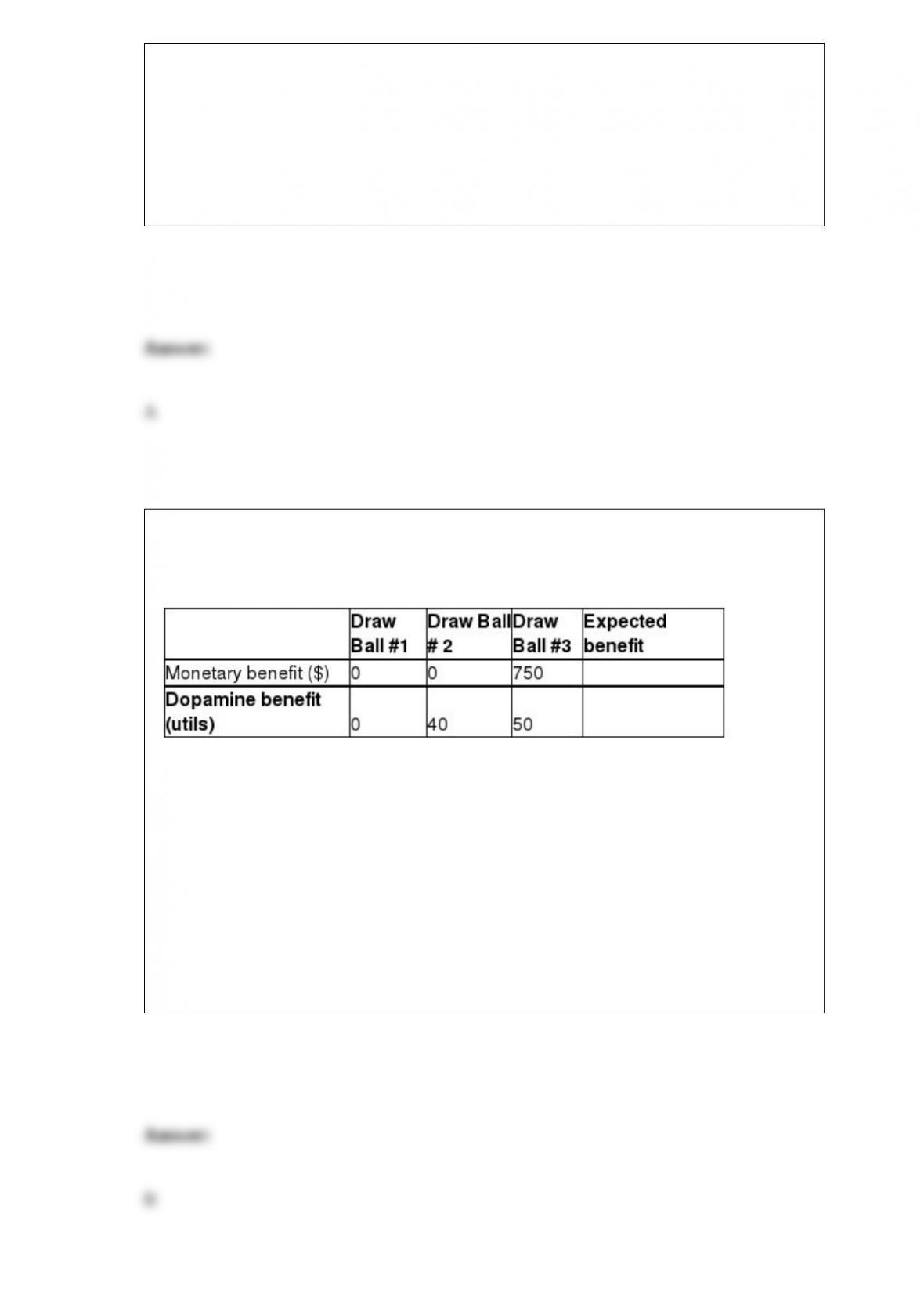

Refer to Table 7.1. For this game, the actual monetary benefit will exceed the expected

benefit:

Table 7.1

The Table represents the payoffs for a gambling game. The player blindly draws

one of three balls, marked 1, 2, and 3, from an urn. The cost to play the game is

$375 per draw.

A) if ball number 2 or number 3 are drawn.

B) only if ball number 3 is drawn.

C) if ball number 1 or number 2 are drawn.

D) The actual monetary benefit will never exceed the expected benefit.

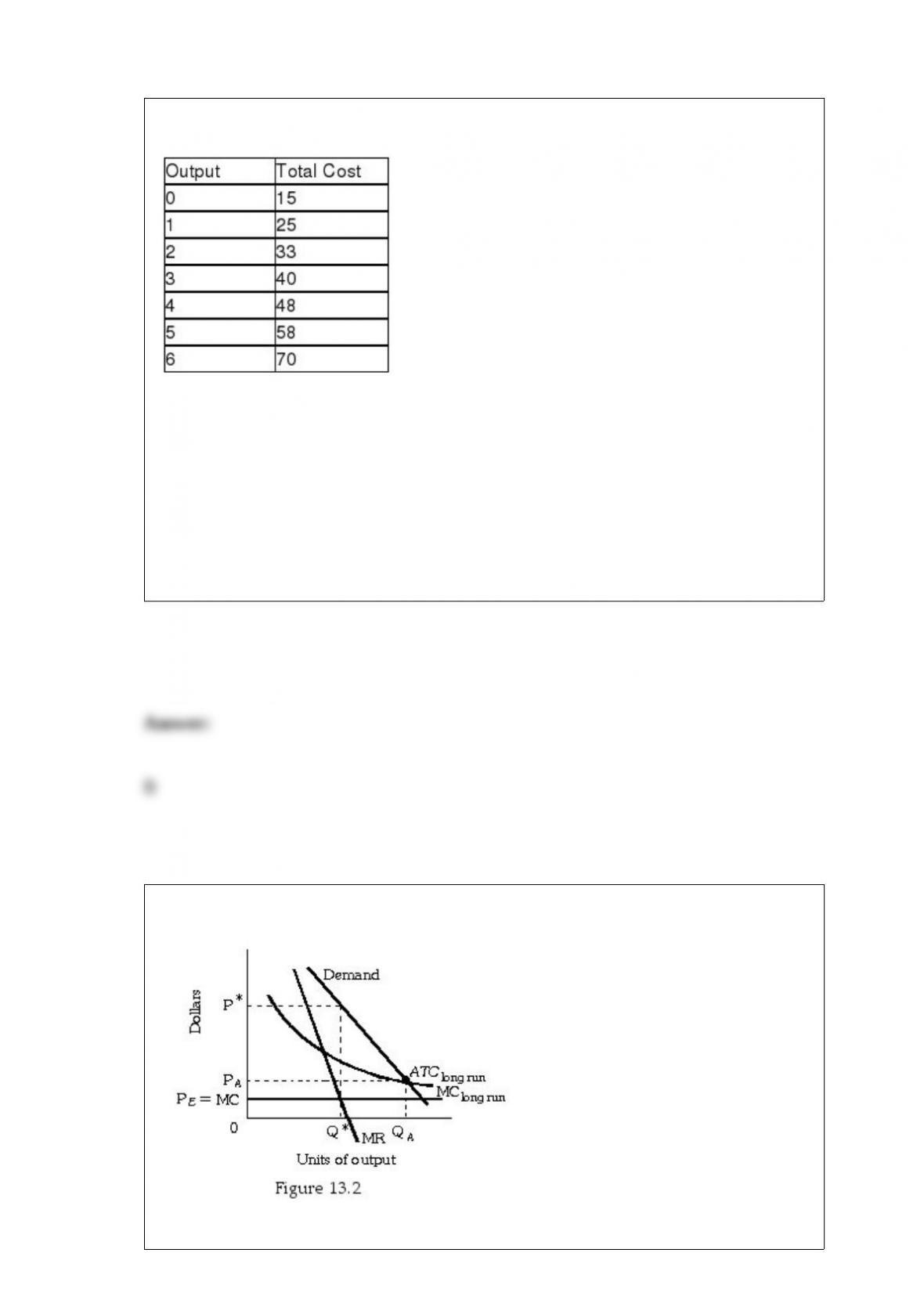

Refer to Table 8.5. The marginal cost of the third unit of output is:

Table 8.5

A) $0.

B) $7.

C) $8.

D) $40.

Refer to Figure 13.2. The profit-maximizing price for the unregulated firm would be:

A) .

B) .

C) .

D) cannot be determined from the information given

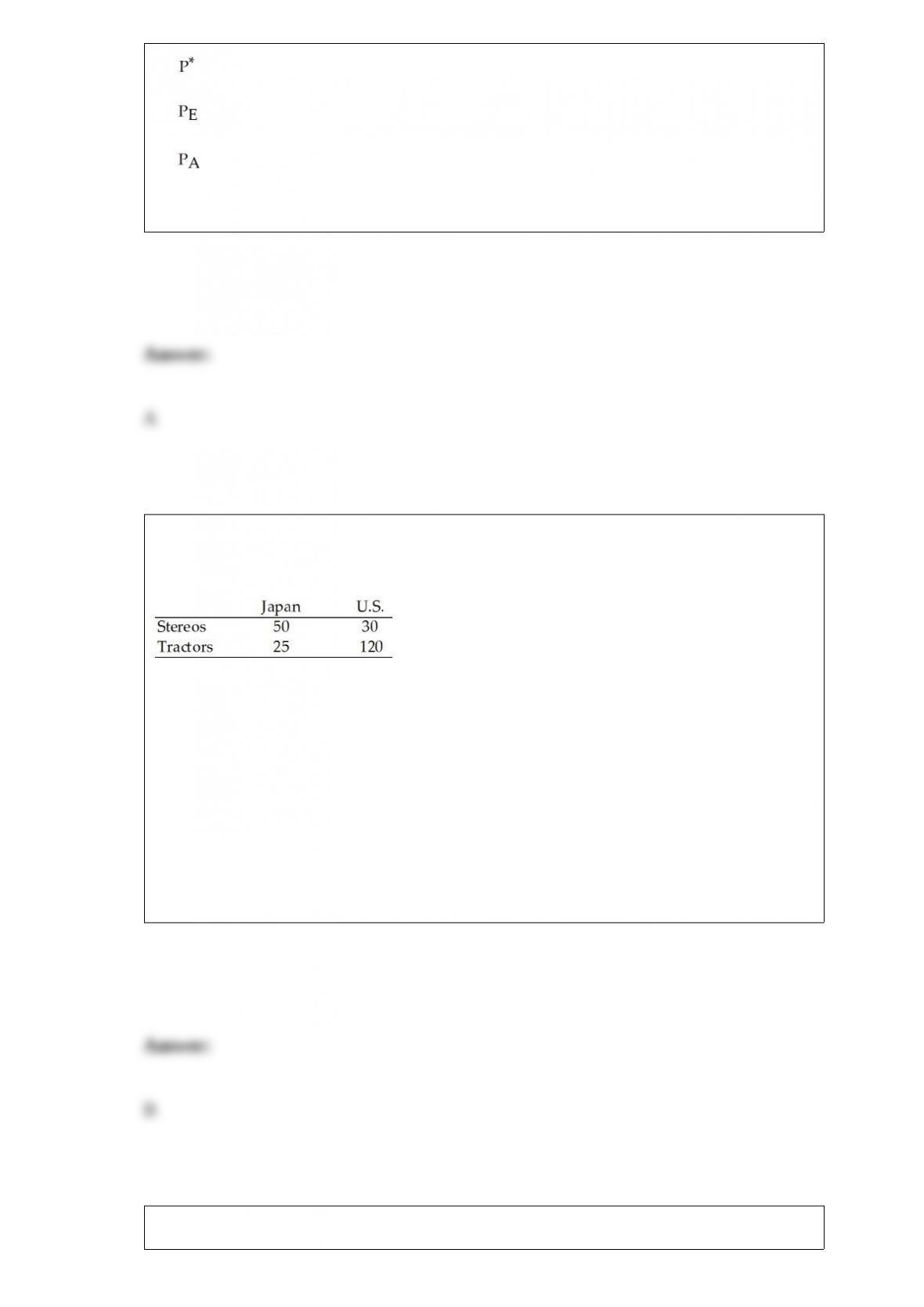

Daily Output of Japan and U.S.

Table 18.2

Refer to Table 18.2. The opportunity cost of tractors in the U.S. is:

A) 2 stereos.

B) 1/4 stereo.

C) 1/2 stereo.

D) 4 stereos.

If a product has only a few acceptable substitutes, demand for the product is most likely

to be:

A) very inelastic.

B) inelastic.

C) elastic.

D) very elastic.

Adverse selection describes the situation that occurs when:

A) people have perfect information.

B) high-quality products are driven from the market by low-quality products due to

imperfect information.

C) actions that were expected to happen do not occur.

D) low-quality products are driven from the market by high-quality products because of

imperfect information.

A minimum supply price is defined as:

A) the lowest price at which a product is made available for sale.

B) the lowest price at which a product is bought.

C) the lowest cost to produce a good.

D) the lowest price at which other sellers also want to sell the good.

Dino spends his income on two goods, cigars and peppermints. He considers both

goods to be normal goods. If Dino’s income remains constant and the relative price of

cigars decreases, he will purchase:

A) more cigars and fewer peppermints.

B) more cigars and more peppermints.

C) fewer cigars and more peppermints.

D) fewer cigars and fewer peppermints.

Which of the following is a topic under microeconomics?

A) money supply

B) exchange rates

C) why the price of gold is rising

D) All of the above are topics in microeconomics

A tie-in sale occurs when:

A) it encourages the enforcement of cooperative agreements.

B) a business sells a few products that work well when used together.

C) a business forces the buyer of one product to purchase another product.

D) a business sells a product at a price below its production cost.

Which of the following is an example of how a business owner uses macroeconomics to

make informed business decisions?

A) A business owner can use macroeconomics to determine whether college graduates

are better employees than non-college graduates.

B) A business owner can use macroeconomics to predict whether the Fed will increase

or decrease the interest rates in the future in order to determine whether to borrow

money now or later.

C) A business owner can use macroeconomics to predict whether television prices will

be higher today or in the future.

D) A business owner can use macroeconomics to predict it should sell more red t-shirts

as opposed to white t-shirts.

A carbon tax placed on coal would:

A) raise the costs of goods produced using coal, raising their price, and thus decreasing

the quantity demanded of these goods.

B) not affect emissions of greenhouse gases.

C) shift the demand curve for coal to the right.

D) make coal a more attractive form of energy.

Total revenue will decrease if price:

A) increases and demand is inelastic.

B) increases and demand is elastic.

C) decreases and demand is elastic.

D) decreases and demand is unitarily elastic.

If a seller of a high-quality good cannot prove the quality of that good:

A) buyers will not be willing to pay the amount for which they value a high-quality

good.

B) buyers will only be willing to pay the amount for which they value a low-quality

good.

C) the good will never be offered for sale.

D) the good will trade at its equilibrium price.

Which of the following is a result of the monopolization of a perfectly competitive

industry, ceteris paribus?

A) lower prices

B) greater efficiency

C) reduced profits

D) deadweight loss

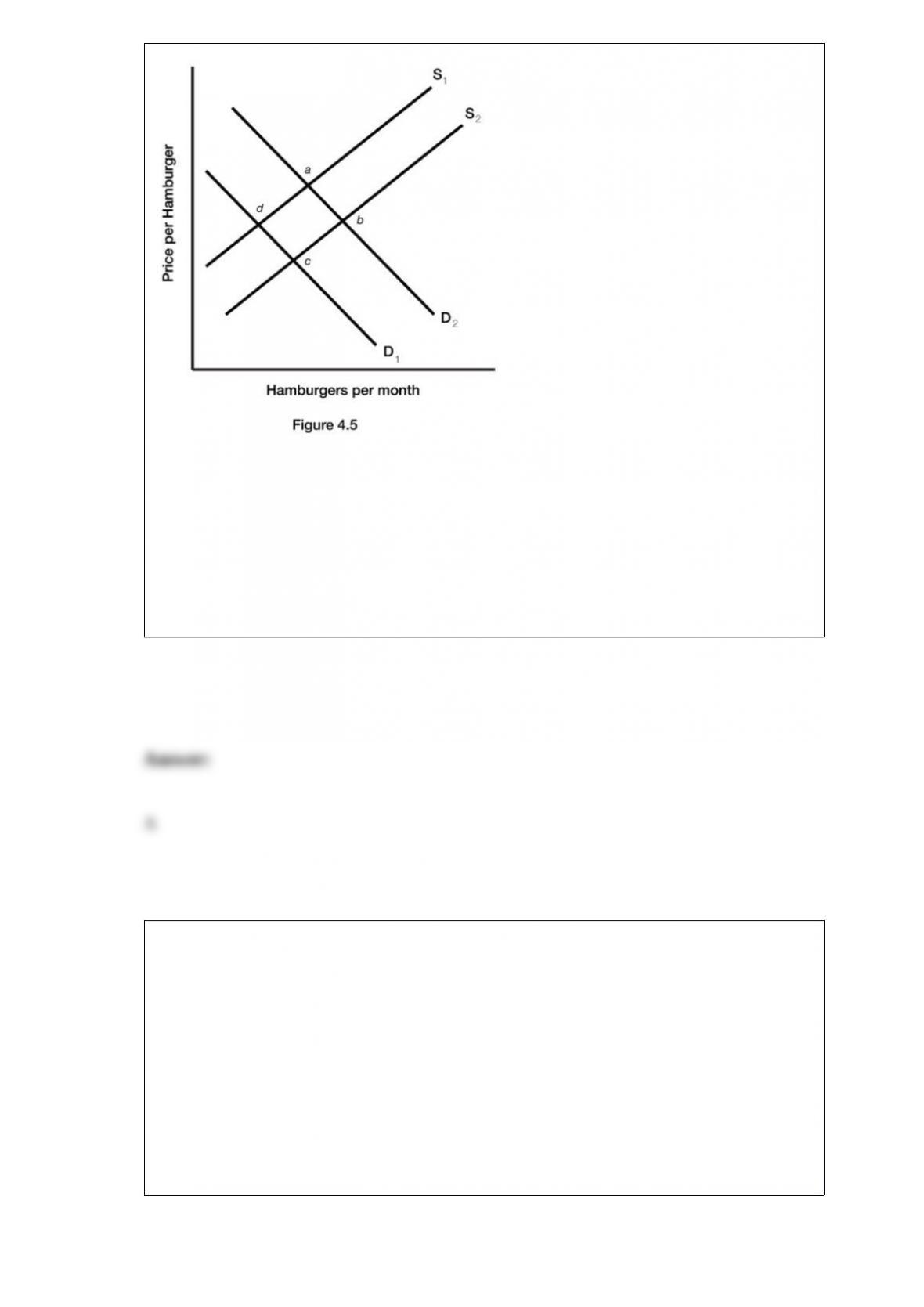

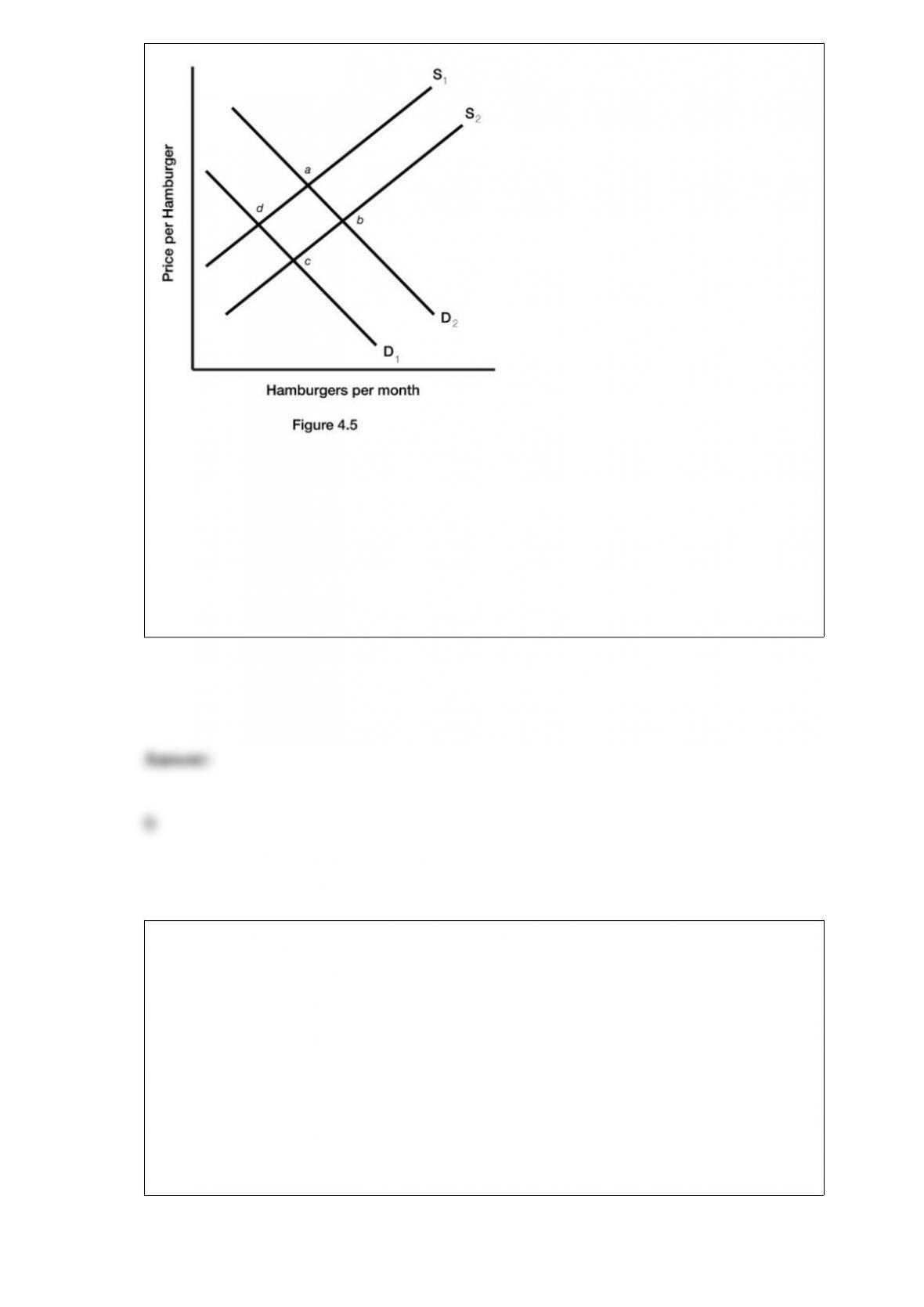

Figure 4.5 illustrates a set of supply and demand curves for hamburgers. An increase in

supply and an increase in demand are represented by a movement from:

A) point d to point b.

B) point d to point a.

C) point c to point a.

D) point b to point c.

In a market economy, what is the role of the government with regards to public goods?

A) The government has to facilitate the collective decision making in the production of

public goods.

B) The government must force the firms to produce all the public goods.

C) The government must take over the production of all goods in the market, public or

private.

D) The government must hold a referendum before any public good is produced.

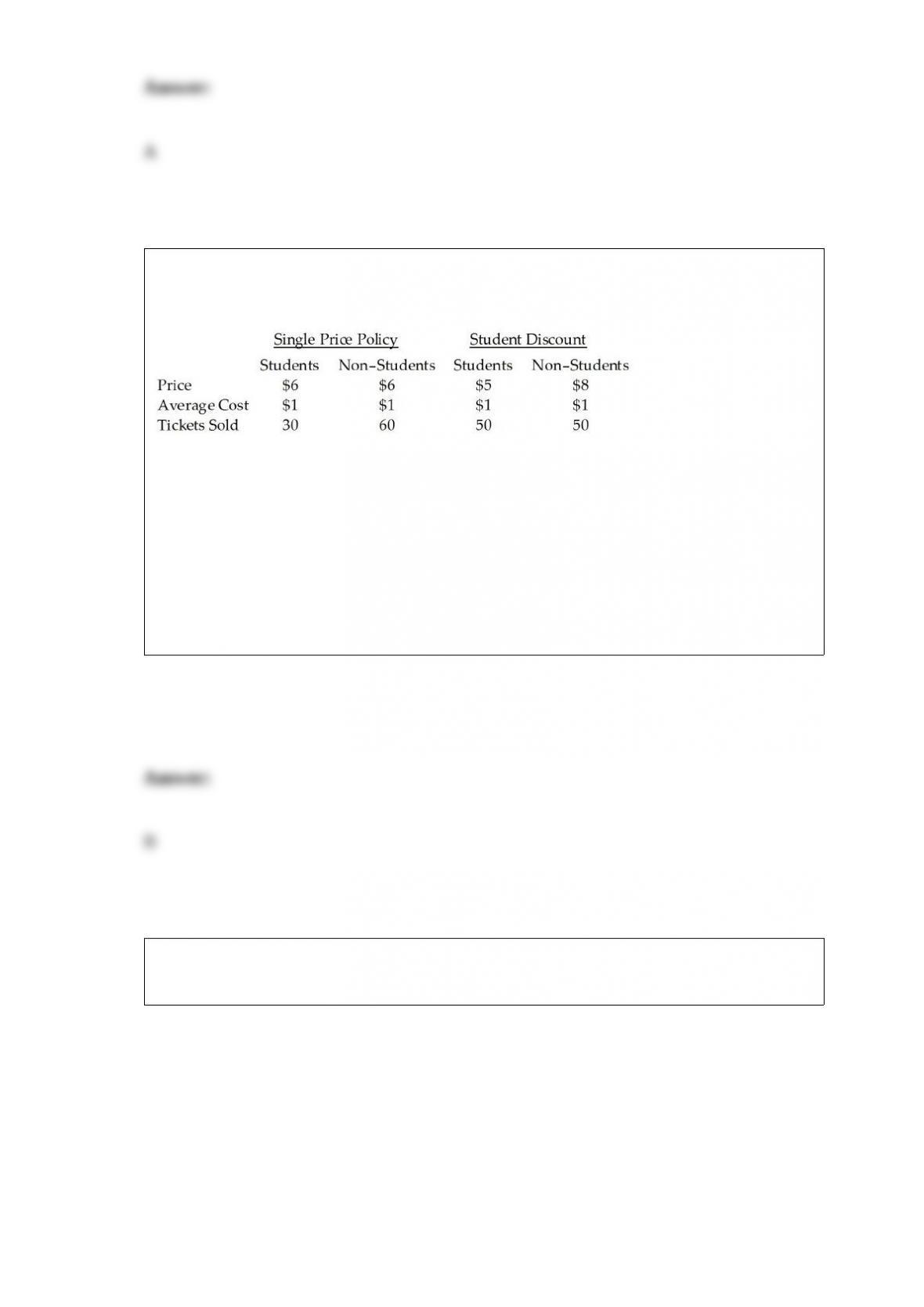

Table 10.2 contains price, demand, and cost data for the Capri Theater, the only first-run

movie theater in a small town. What is its revenue from students under the single price

policy?

Table 10.2

A) $150

B) $180

C) $450

D) $540

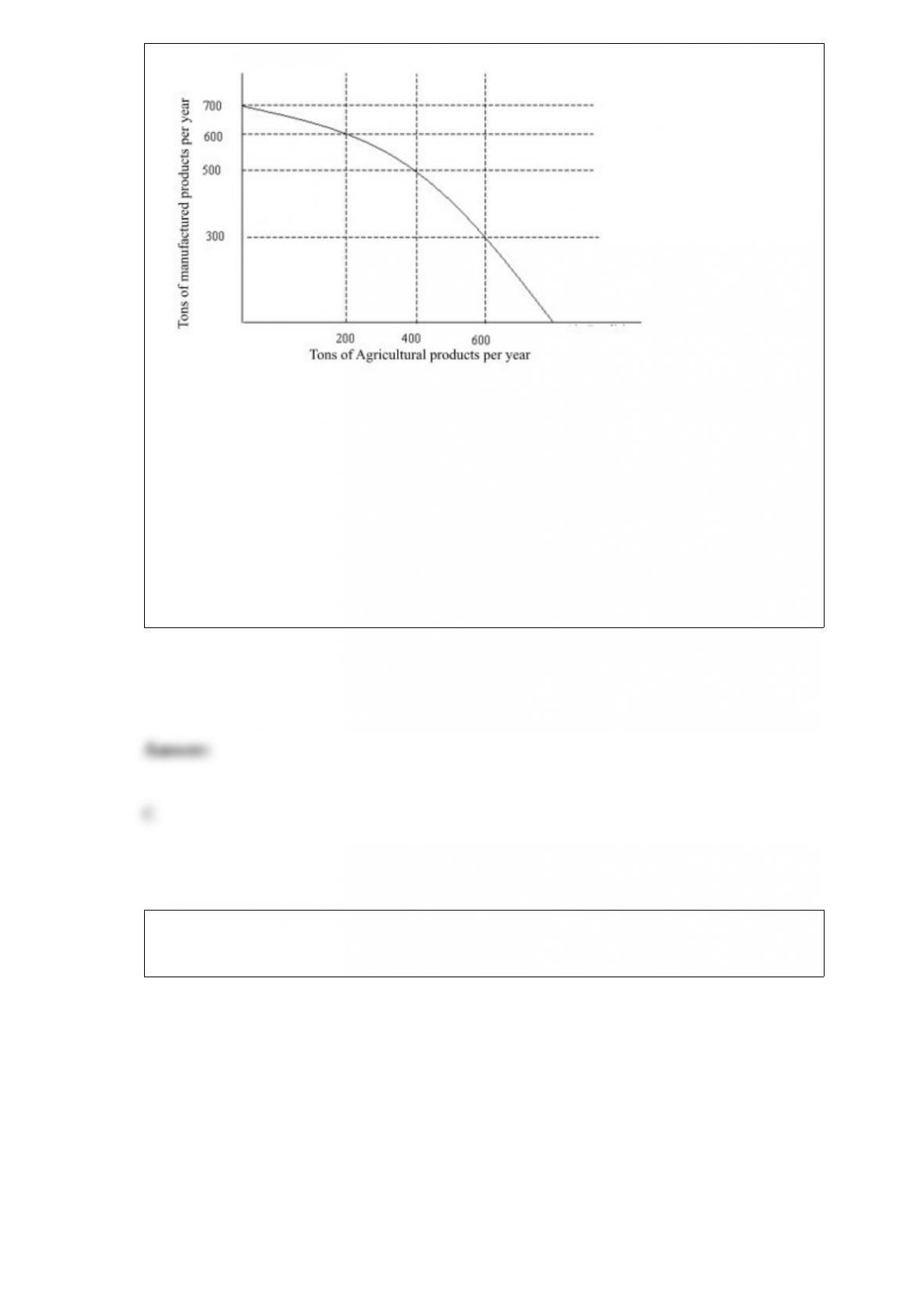

On the production possibilities curve in Figure 2.1 the opportunity costs of increasing

agricultural production from 400 tons to 600 tons is:

Figure 2.1

A) 600 tons of manufacturing.

B) 500 tons of manufacturing.

C) 200 tons of manufacturing.

D) 100 tons of manufacturing.

Figure 4.5 illustrates a set of supply and demand curves for hamburgers. A decrease in

supply and a decrease in quantity demanded are represented by a movement from:

A) point a to point d.

B) point c to point d.

C) point c to point a.

D) point b to point c.

If the consumer gets 40 utils from consuming four CDs, 45 utils from consuming five

CDs and 48 utils from consuming six CDs, then the consumer’s marginal utility from

the fifth CD is:

A) 5 utils.

B) 10 utils.

C) 42.5 utils.

D) 45 utils.

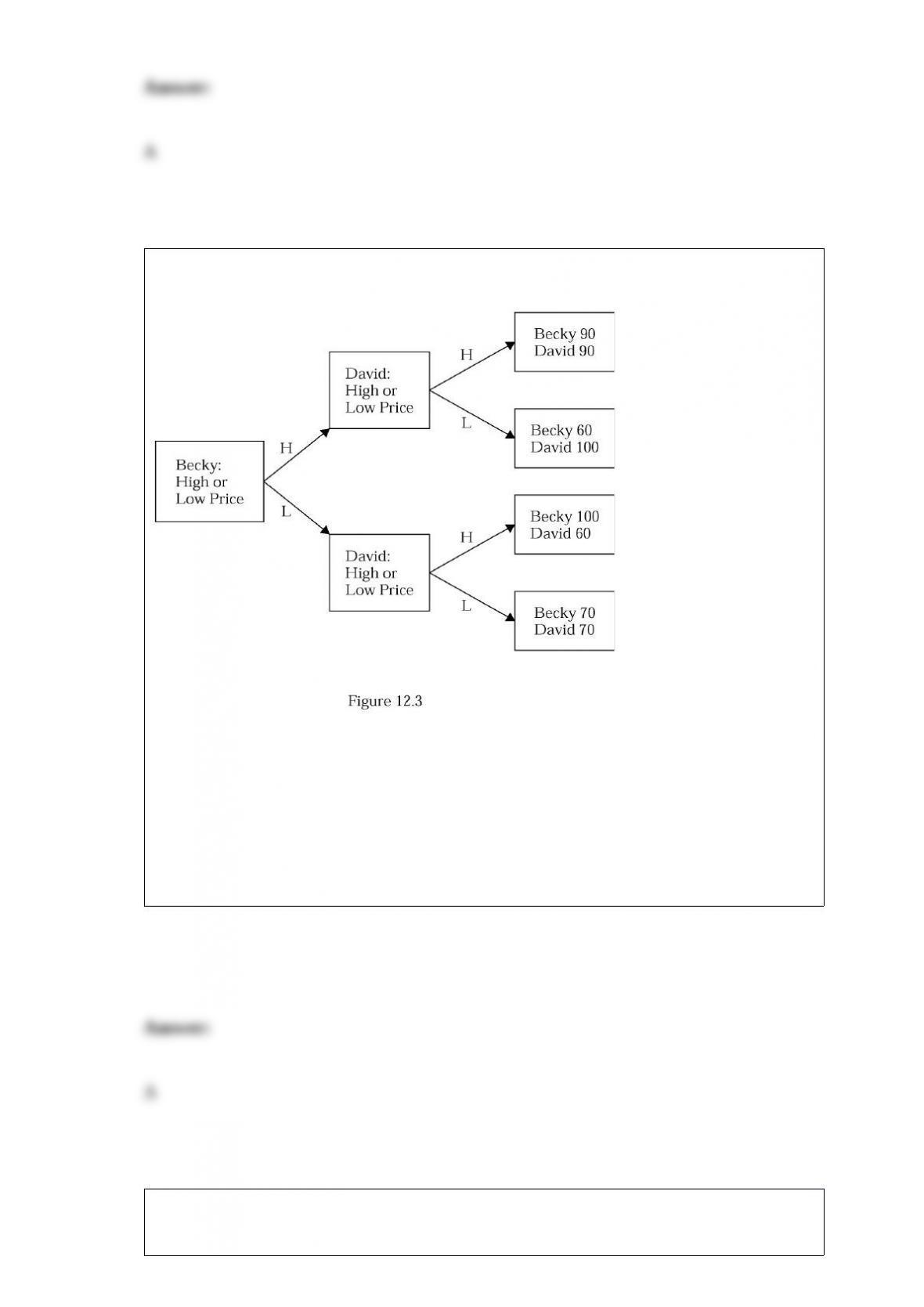

Consider Figure 12.3. Which of the following statements is true?

A) Both David and Becky have a dominant strategy.

B) Neither David nor Becky has a dominant strategy.

C) David has a dominant strategy but Becky does not.

D) Becky has a dominant strategy but David does not.

In a duopoly, one firm’s low-price guarantee:

A) eliminates the other firm’s incentive to undercut the first firm’s price.

B) encourages the other firm to cut its prices.

C) guarantees that consumers will pay the lowest price possible.

D) is ineffective because firms always have an incentive to break their agreements.

The self-interest theory of government was suggested by:

A) James Buchanan.

B) Charles M. Tiebout.

C) bureaucrats.

D) the European Union.

Suppose that a technological advancement substantially reduces the cost of laser eye

surgery. This would cause the equilibrium:

A) price of technology to increase.

B) quantity of technology to decrease.

C) quantity of laser eye surgery to increase.

D) quantity of laser eye surgery to decrease.

What are the main features of the Sherman Act?

Why does it make sense for unprofitable firms to stay in business?

Define the term “import.”

Given percentage change in supply and the price elasticity of supply, explain how

percentage change in equilibrium price varies as the price elasticity of demand changes

from 0 to infinity.

What characterizes a constant cost industry and what causes it to be a constant cost

industry?

Describe the changes in the variables that will cause supply for a product to increase,

shifting the supply curve down and to the right.

Define an “inferior good” as it relates to markets.

Recall the Application about the merger of Sirius Satellite Radio and XM Satellite

Radio to answer the following question(s).

Recall the Application. What were the tradeoffs that government regulators had to

consider in determining whether to allow the Sirius and XM to merge?

Use a diagram of a competitive labor market and a representative firm to explain how

much labor a profit-maximizing firm will hire.

List the three conditions that must be met when a perfectly competitive industry is in

long-run equilibrium.

Explain the equimarginal rule.

Suppose that buyers are willing to pay $1000 for a plum used computer and $300 for a

lemon. If buyers expect 40% of the used computers to be plums, what is the maximum

amount that buyers will be willing to pay for a used computer?

Why would a firm continue to pollute even when it is fined (taxed) for doing so?

Which is likely to be more elastic: the demand for orange juice or the demand for a

particular brand of orange juice? Explain.

Between an “individual demand curve” and a “market demand curve,” which one has a

steeper slope?

What is the learning effect of a college education?

Describe the changes in the variables that will cause demand for a product to decrease,

shifting the demand curve to the left.

Different people eat different amounts of food when they go to buffet restaurants, even

though they all pay the same price. Explain how this relates to the marginal principle.