One important reason why the U.S. government is not likely to go bankrupt even with a

large public debt is that it has:

A. the ability to refinance debt as it comes due by selling new bonds.

B. s strong military to protect it from creditors.

C. the capacity to pay off its outstanding debt with gold.

D. the ability to decrease interest rates and increase investment spending.

In the United States, business cycles have occurred against a backdrop of a long-run

trend of:

A. declining unemployment.

B. stagnant productivity growth.

C. rising real GDP.

D. rising inflation.

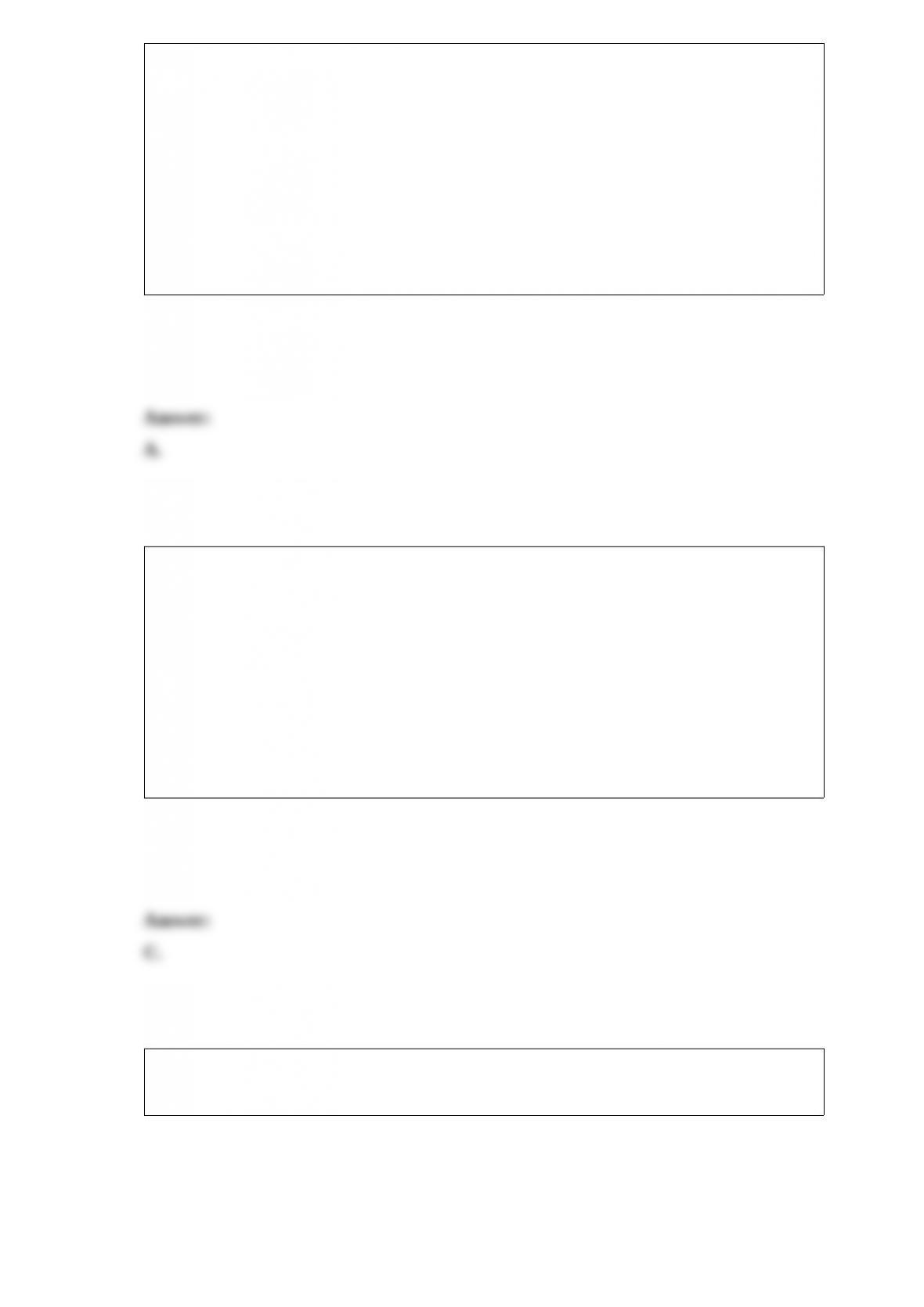

In the above graph, tax revenues vary:

A. directly with the level of GDP.

B. inversely with the level of GDP.

C. directly with the level of government spending.

D. inversely with the level of government spending.

What form of aid is used for Medicaid?

A. Cash

B. Charity

C. Vouchers

D. Subsidized services

A decrease in aggregate demand will decrease:

A. both real output and the price level.

B. the price level and increase the real domestic output.

C. the real domestic output and have no effect on the price level.

D. the price level and have no effect on real domestic output.

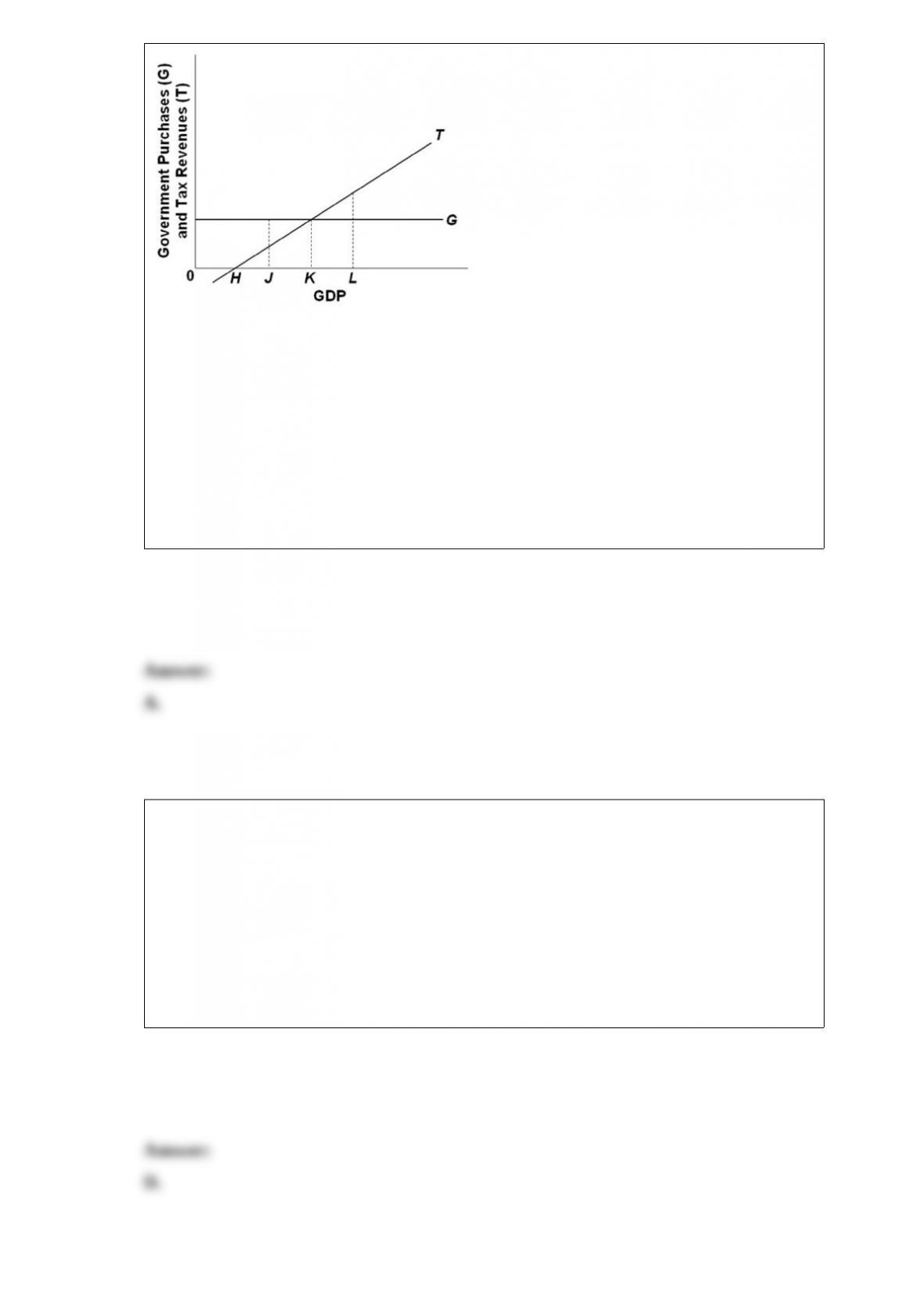

Refer to the above table. The rise in percentage of income received from before taxes

and transfers to after taxes and transfers is greatest for the:

A. lowest 20 percent of households.

B. third 20 percent of households.

C. fourth 20 percent of households.

D. highest 20 percent of households.

Greater income equality that is achieved through the redistribution of income is thought

to:

A. stimulate innovation and entrepreneurship.

B. promote economic efficiency in the economy.

C. increase incentives to work, save, and invest in the economy.

D. come at the opportunity cost of reduced production and income.

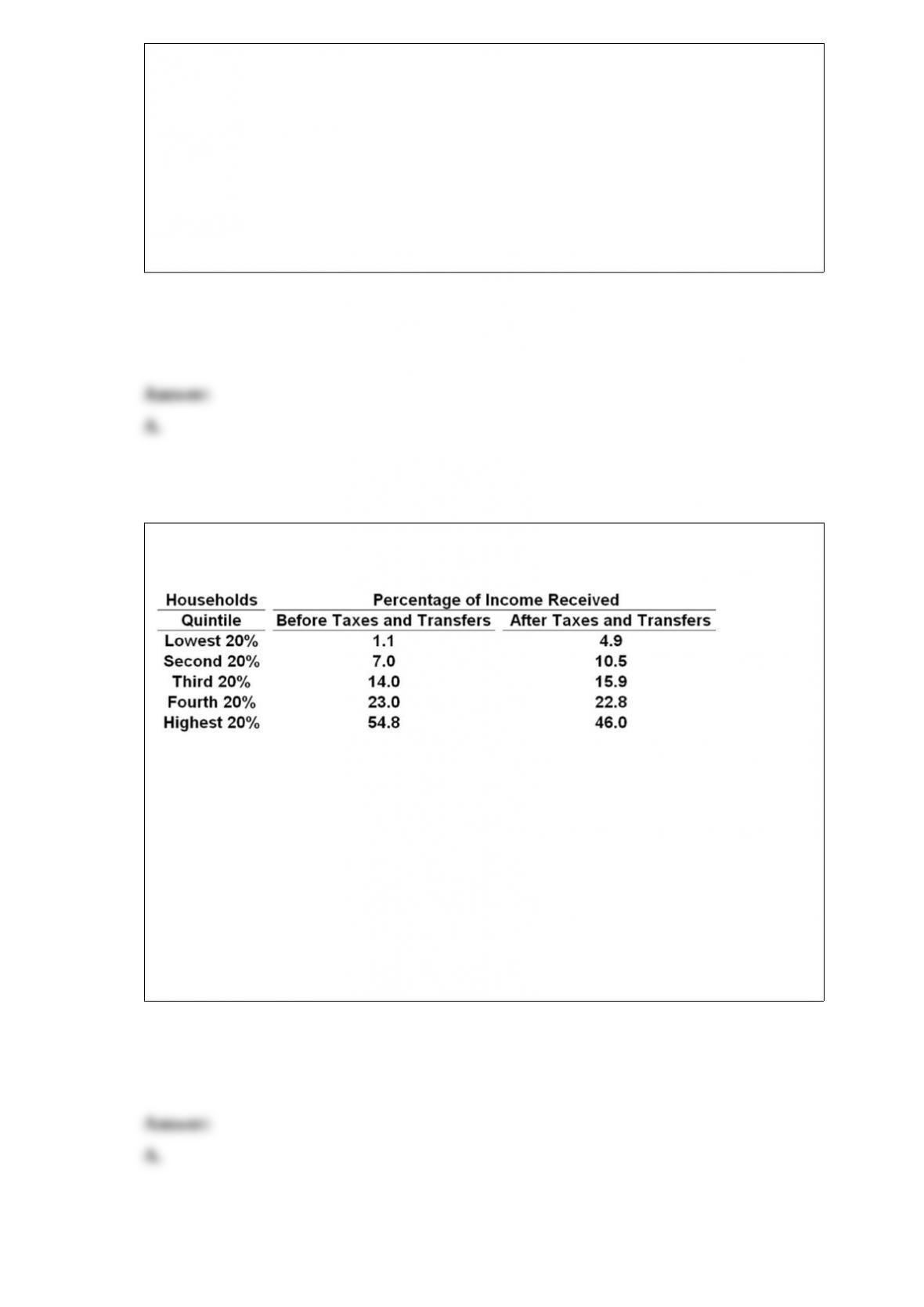

The following economy produces two products.

Refer to the above table. The opportunity cost of each additional tank in terms of autos:

A. remains constant.

B. falls as more tanks are produced.

C. increases as more tanks are produced.

In a free-market economy, a product that entails a spillover benefit will be:

A.overproduced.

B.underproduced.

C.produced at the optimal level.

D.associated only with goods and services provided by the government.

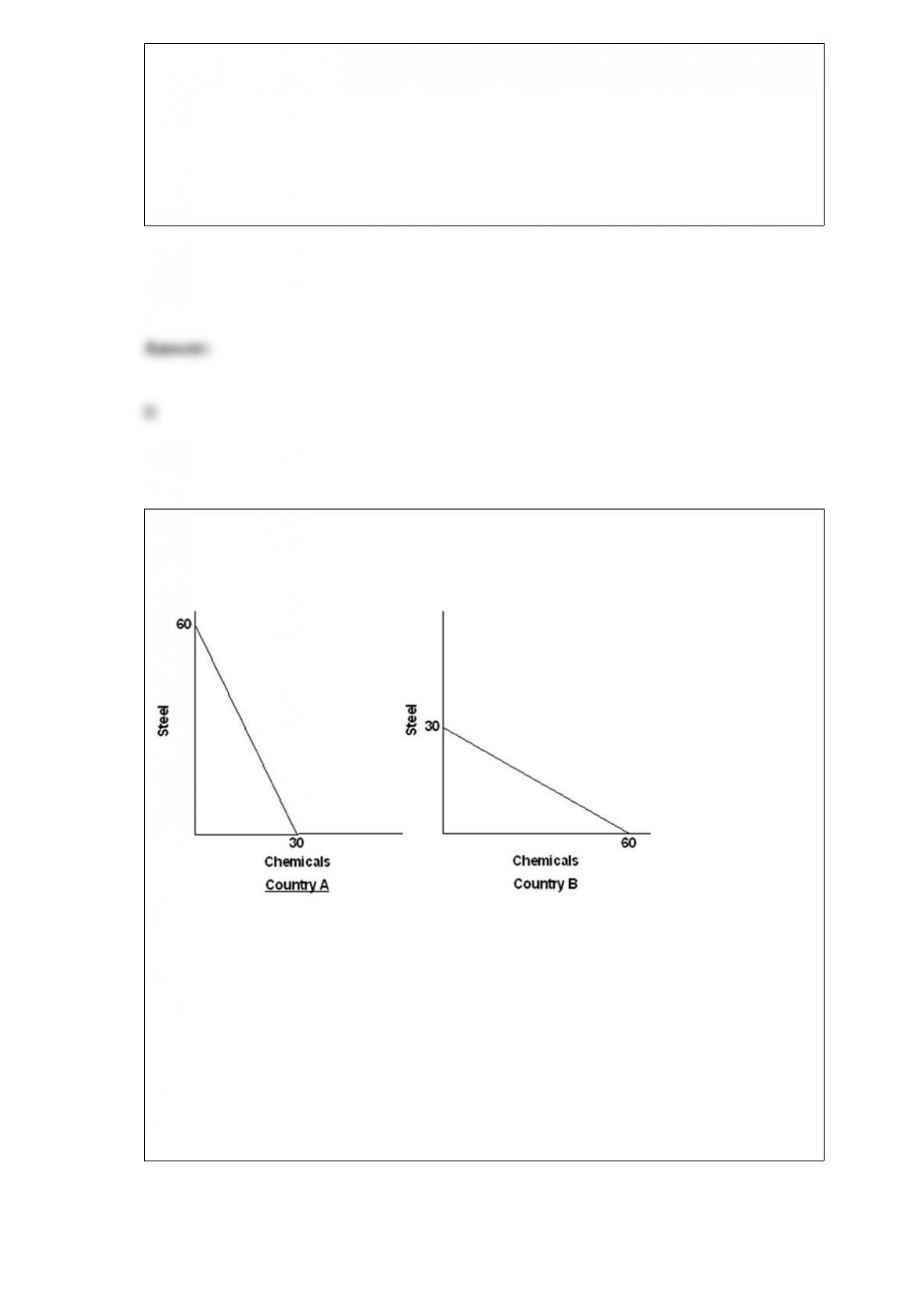

Suppose the world economy is composed of just two countries: A and B. Each can

produce steel or chemicals but at different levels of economic efficiency. The domestic

production possibilities curves are shown in the graphs below.

Refer to the above graphs and information. The assumption made about the domestic

opportunity costs in countries A and B is that they are:

A. constant.

B. variable.

C. increasing.

D. decreasing.

When an economist says that the demand for a product has increased, this means that:

A. consumers are now willing to purchase more of this product at each possible price.

B. the product has become particularly scarce for some reason.

C. product price has fallen and as a consequence consumers are buying a larger quantity

of the product.

D. the demand curve has shifted to the left.

To track the interest on the public debt over time and compare it to the productive

capacity of the economy, it is best:

A. measured relative to the GDP.

B. compared to consumer spending.

C. examined relative to budget deficits.

D. measured relative to the Consumer Price Index.

In the simple circular flow model:

A. households are sellers of resources and demanders of products.

B. households are sellers of products and demanders of resources.

C. businesses are sellers of resources and demanders of products.

D. businesses are sellers of both resources and products.

Which does not contribute to the production of the domestic output of an economy?

A. A police officer.

B. An insurance agent.

C. A full-time student.

D. A soldier.

In which two market models would advertising be used most often?

A. Pure competition and monopolistic competition

B. Pure competition and pure monopoly

C. Monopolistic competition and oligopoly

D. Pure monopoly and oligopoly

The crowding-out effect works through interest rates to:

A. increase the effectiveness of expansionary fiscal policy.

B. decrease the effectiveness of expansionary fiscal policy.

C. decrease the effectiveness of contractionary fiscal policy.

D. increase the effectiveness of contractionary fiscal policy.

If the interest rate increases, there will be a(n):

A. decrease in the amount of money held as assets.

B. decrease in the transactions demand for money.

C. increase in the transactions demand for money.

D. increase in the amount of money held as assets.

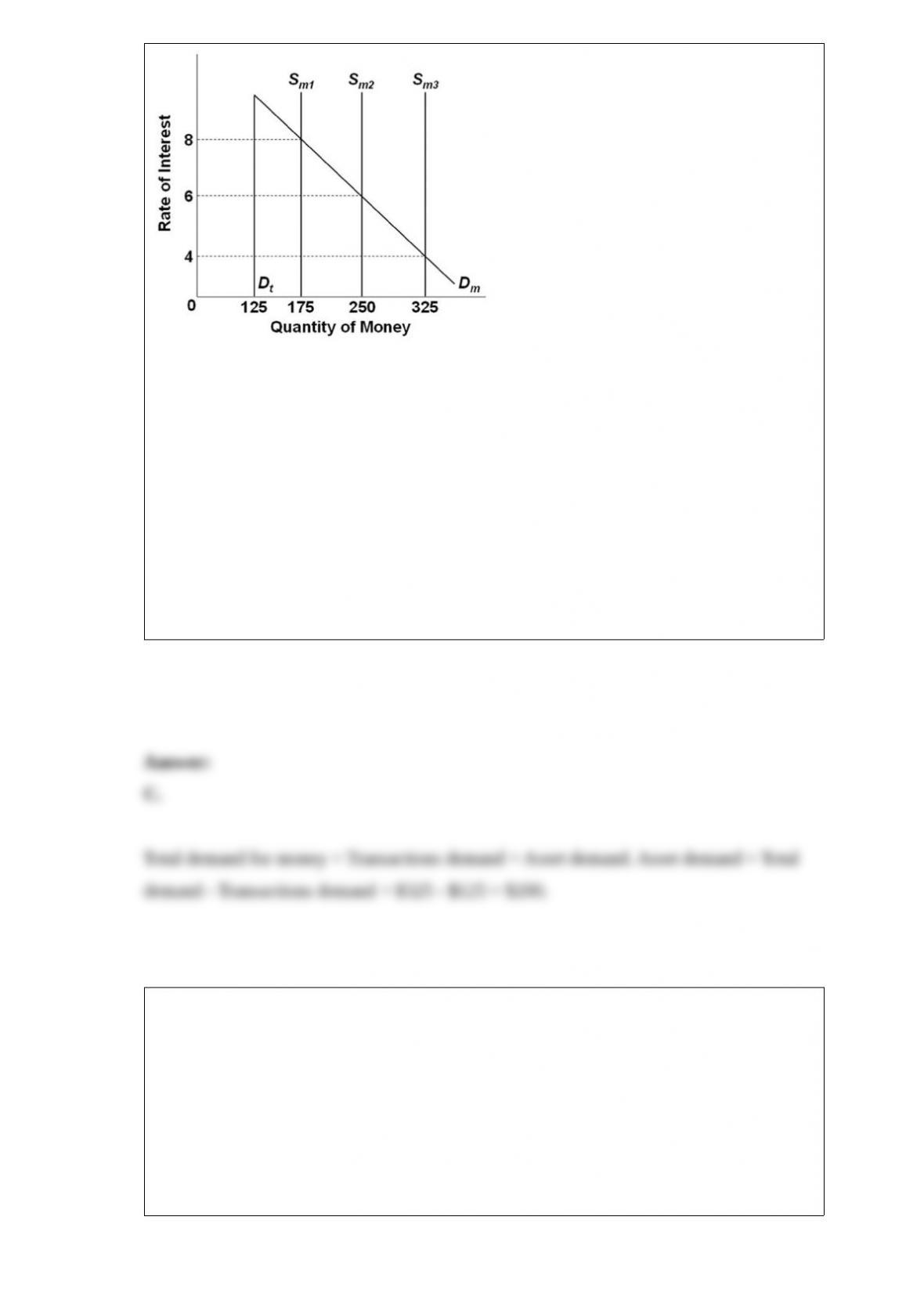

Refer to the above graph, in which Dt is the transactions demand for money, Dm is the

total demand for money, and Sm is the supply of money. If the interest rate was 4

percent, the asset demand for money would be:

A. $125.

B. $175.

C. $200.

D. $225.

One principal advantage of the corporations is that owners:

A. are not taxed for income received.

B. always control the company.

C. are sole proprietors.

D. have limited liability.

A fixed cost is:

A. associated with any productive resource whose price is fixed.

B. any cost that increases proportionately with output.

C. any cost that a firm would incur even if output was zero.

D. associated with all inputs whose short-run supply is perfectly inelastic.

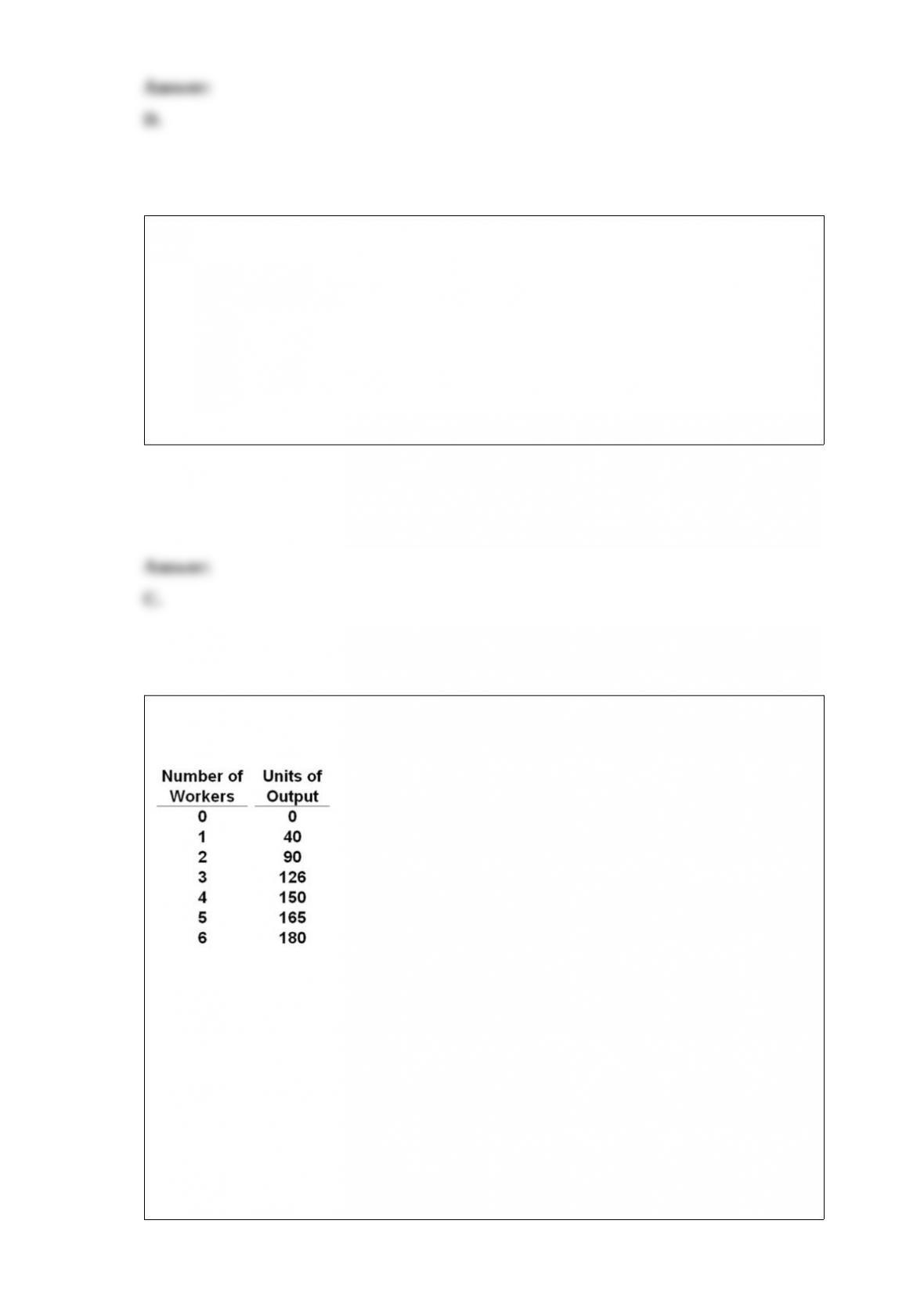

Refer to the above data. Diminishing marginal returns become evident with the addition

of the:

A. sixth worker.

B. fourth worker.

C. third worker.

D. second worker.

Which of the following is correct as it relates to cost curves?

A. Average variable cost intersects marginal cost at the latter’s minimum point.

B. Marginal cost intersects average total cost at the latter’s minimum point.

C. Average fixed cost intersects marginal cost at the latter’s minimum point.

D. Marginal cost intersects average fixed cost at the latter’s minimum point.

Entry fees at national parks and monuments are an example of:

A. the ability-to-pay principle of taxation.

B. the benefits-received principle of taxation.

C. government bureaucracy and inefficiency.

D. the principle of limited and bundled choice.

In long-run equilibrium under conditions of pure competition and productive efficiency,

all firms produce at minimum:

A. average total cost.

B. marginal cost.

C. total cost.

D. average variable cost.

All of the following accurately describe a market economy except:

A. government establishes maximum and minimum prices for most goods and services.

B. prices serve as a signaling mechanism to buyers and sellers.

C. the allocation of resources is determined by their prices.

D. the actions of buyers and sellers establish a product’s price.

After graduating from high school, Ron Willis plans to go to college. The college

tuition is $15,000 a year. But, instead of going to college, Ron could take a full-time job

paying $20,000. If Ron decides to go to college, what is his opportunity cost for

attending for one year?

A. $5,000

B. $15,000

C. $20,000

D. $35,000

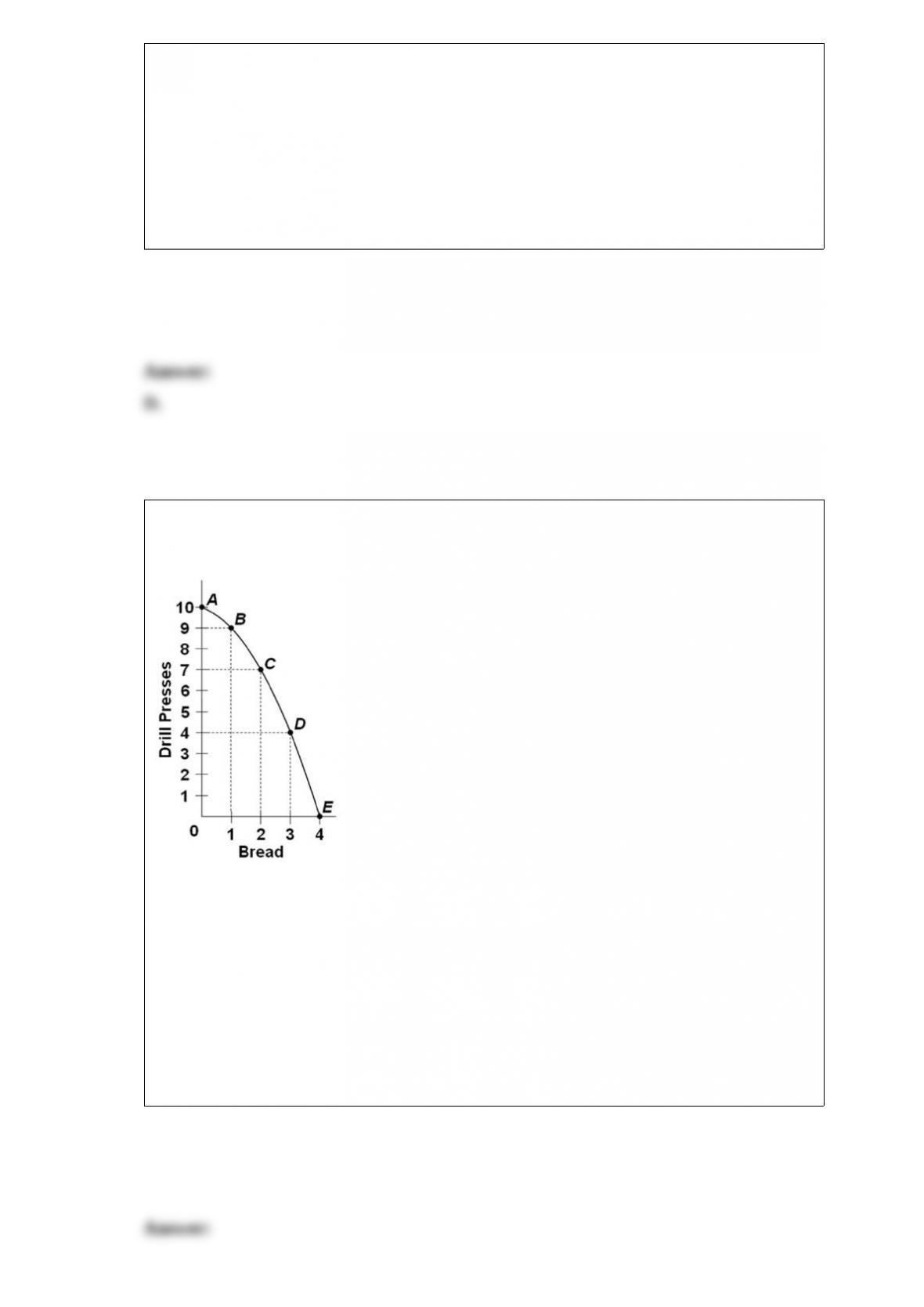

Refer to the above graph. The marginal opportunity cost of the fourth unit of bread is:

A. 1 unit of drill presses.

B. 2 units of drill presses.

C. 3 units of drill presses.

D. 4 units of drill presses.

When the federal government takes action to change taxes and spending to stimulate the

economy, such policy is:

A. passive.

B. automatic.

C. discretionary.

D. nondiscretionary.

An antigrowth view states that there may be a significant trade-off between productivity

and:

A. education.

B. employment.

C. economies of scale.

D. the quality of life.

Which is the main problem with the barter system of exchange? Barter:

A. encourages self-interest and selfishness.

B. fosters specialization and division of labor.

C. requires a coincidence of wants.

D. undermines the right to leave property to one’s heirs.

Which increases the excess reserves of commercial banks?

A. The central banks sell bonds to the public.

B. The central banks sell bonds to commercial banks.

C. The central banks buy bonds from commercial banks.

D. The Board of Governors increases the discount rate.

Ticket scalping implies that:

A. event sponsors have set ticket prices at above-equilibrium levels.

B. an event is not likely to be sold out.

C. event sponsors have set ticket prices at below-equilibrium levels.

D. the demand for tickets has fallen between the time tickets were originally sold and

the event takes place.

The Federal Reserve would be encouraged to buy government bonds in the open market

to maintain current interest rates when:

A. the demand for money decreases.

B. the demand for money increases.

C. investment demand decreases.

D. the discount rate increases.

A graph of the long-run aggregate supply curve is:

A. horizontal, and a graph of the short-run aggregate supply is upsloping.

B. upsloping, and a graph of the short-run aggregate supply is vertical.

C. upsloping, and a graph of the short-run aggregate supply is horizontal.

D. vertical, and a graph of the short-run aggregate supply is upsloping.

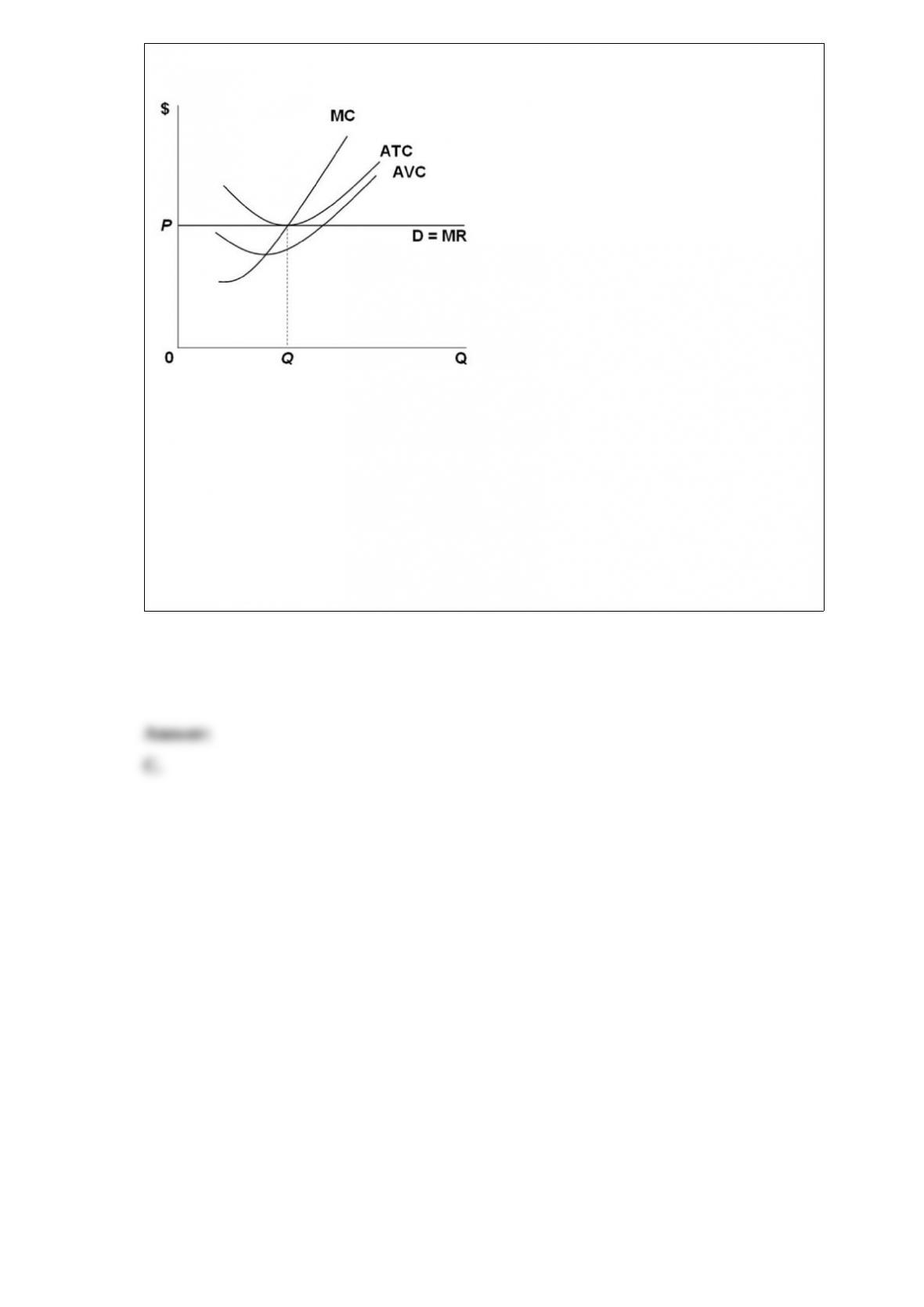

Consider the purely competitive firm pictured above. The firm is earning:

A. normal profits since its price is above AVC.

B. economic profits since its price is above AVC.

C. normal profits since its price just covers ATC.

D. losses since it is operating at the shutdown point.