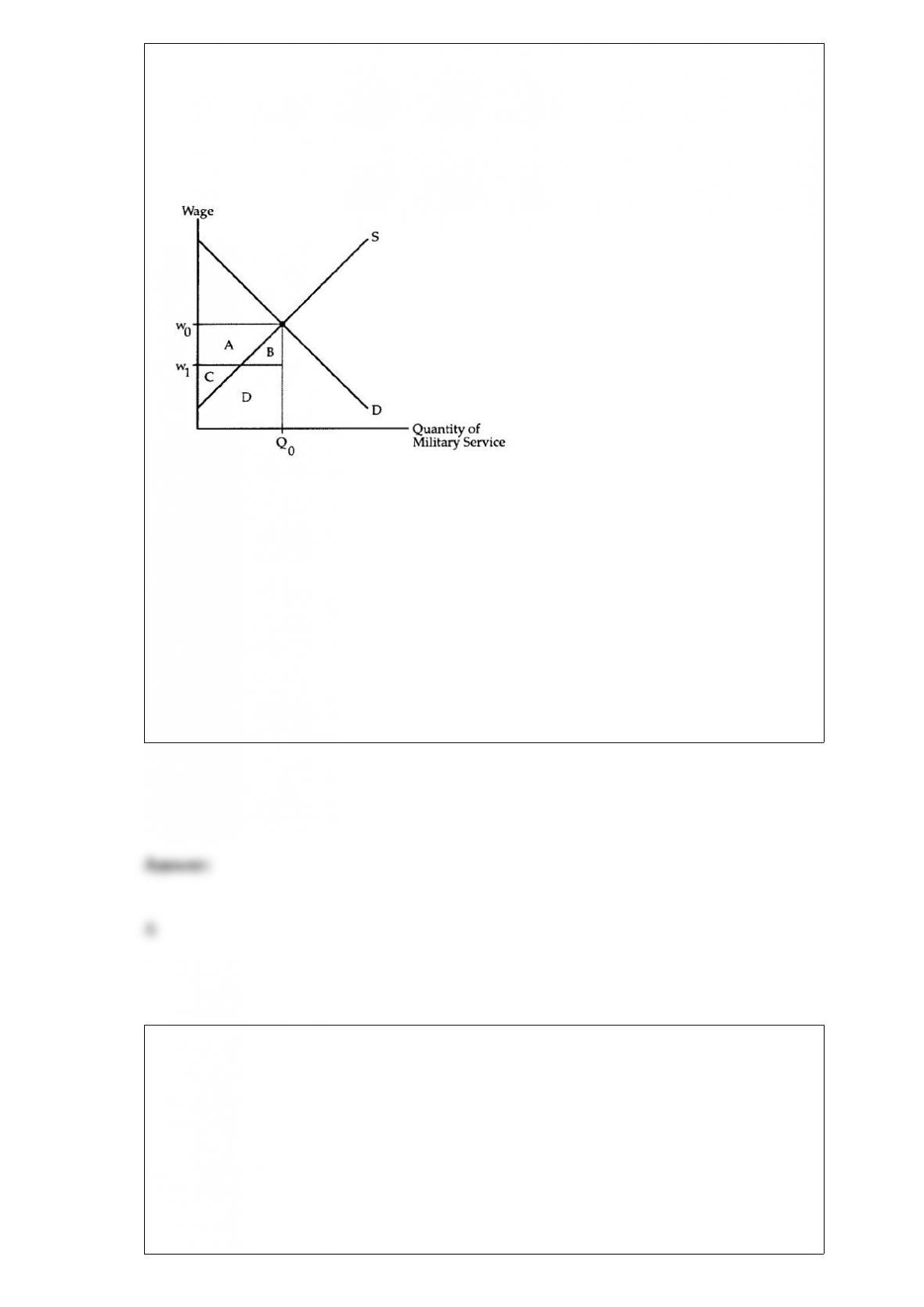

Supply and Demand

The following questions refer to the accompanying graph, which shows the supply and

demand for military service.

Suppose the government drafts Q0 persons into the army and pays them the wage w1. In

this situation, the area B + D

a. underestimates the cost of the army to society.

b. equals the social gain created by the limited draft.

c. overestimates the amount of rent earned by draftees.

d. shows that this limited draft has the same cost as a volunteer army.

If the wage rate is $10 per hour and one worker can currently produce 2 units of output

per hour, then the marginal cost of production is

a. $5

b. $10

c. $20

d. the answer cannot be determined from the information given.

Which of the following would cause the firm’s short-run demand curve for labor to shift

to the right?

a. A decrease in the wage rate.

b. An increase in the price of the firm’s product.

c. An increase in the rental rate paid to capital.

d. A fall in the amount of complementary capital available.

New safety regulations increase manufacturers’ costs of producing insulation. What

happens in the market for insulation?

a. The demand falls as buyers refuse to bear the higher production costs.

b. The supply falls, resulting in a higher equilibrium price and lower equilibrium

quantity.

c. Both supply and demand fall, resulting in less insulation being bought and sold.

d. The supply rises as manufacturers attempt to use higher sales to offset their lower

profit margins.

Comparative statics involves

a. the application of principles of physics to economic analysis.

b. the process of studying how equilibria change in response to changes in exogenous

variables.

c. the process of studying how exogenous variables change.

d. comparing two uncertain states of the world.

Suppose coal is mined at a zero marginal cost and is priced competitively. If the price of

coal is growing faster than the interest rate, then coal miners

a. are making positive economic profits.

b. will increase the amount of coal left unmined.

c. should extract more coal now and less coal in the future.

d. will exit the industry in the long run.

A utility maximizing person gets marginal utility from consuming their last orange and

apple of 5 and 10 respectively. If apples cost 90 cents a piece, the oranges must cost

a. 45 cents a piece.

b. 90 cents a piece.

c. one dollar and eighty cents a piece.

d. two dollars and 70 cents a piece.

Consider the market for high-end wine. Statistics show that wealthier families spend a

greater proportion of their income on high-end wine than do poorer families. If

households’ incomes rise substantially during an economic recovery, then we can expect

a. an increased demand for high-end wine.

b. an increased supply of high-end wine.

c. a lower price for high-end wine.

d. the demand curve for high-end wine to shift to the left.

Consider a perfectly competitive firm with MC = 10 + q. If market demand is Q = 100 –

P and the current industry output is 80 units, then the firm will produce

a. zero units.

b. 10 units.

c. 20 units.

d. the answer cannot be determined without knowing what the supply curve is.

In the long run, a firm will exit an industry if the market price is less than its

a. break-even price.

b. shutdown price.

c. marginal cost.

d. fixed cost.

When you hire a company to paint your house, you cannot be sure of the quality of

paint that was used. This situation is an example of

a. moral hazard.

b. the adverse selection problem.

c. the market for lemons.

d. the principal-agent problem.

Cournot Problem. Consider Cournot Duopolists that produce homogeneous goods.

These firms each have constant marginal costs of $10. The market for these firms’

product has demand Q = 100 – P.

In the Nash Equilibrium, consumer surplus will be

a. $900

b. $1800

c. $2700

d. $3600

As increasing amounts of a good are produced, the marginal cost of production tends to

a. rise.

b. fall.

c. remain constant.

d. change unpredictably.

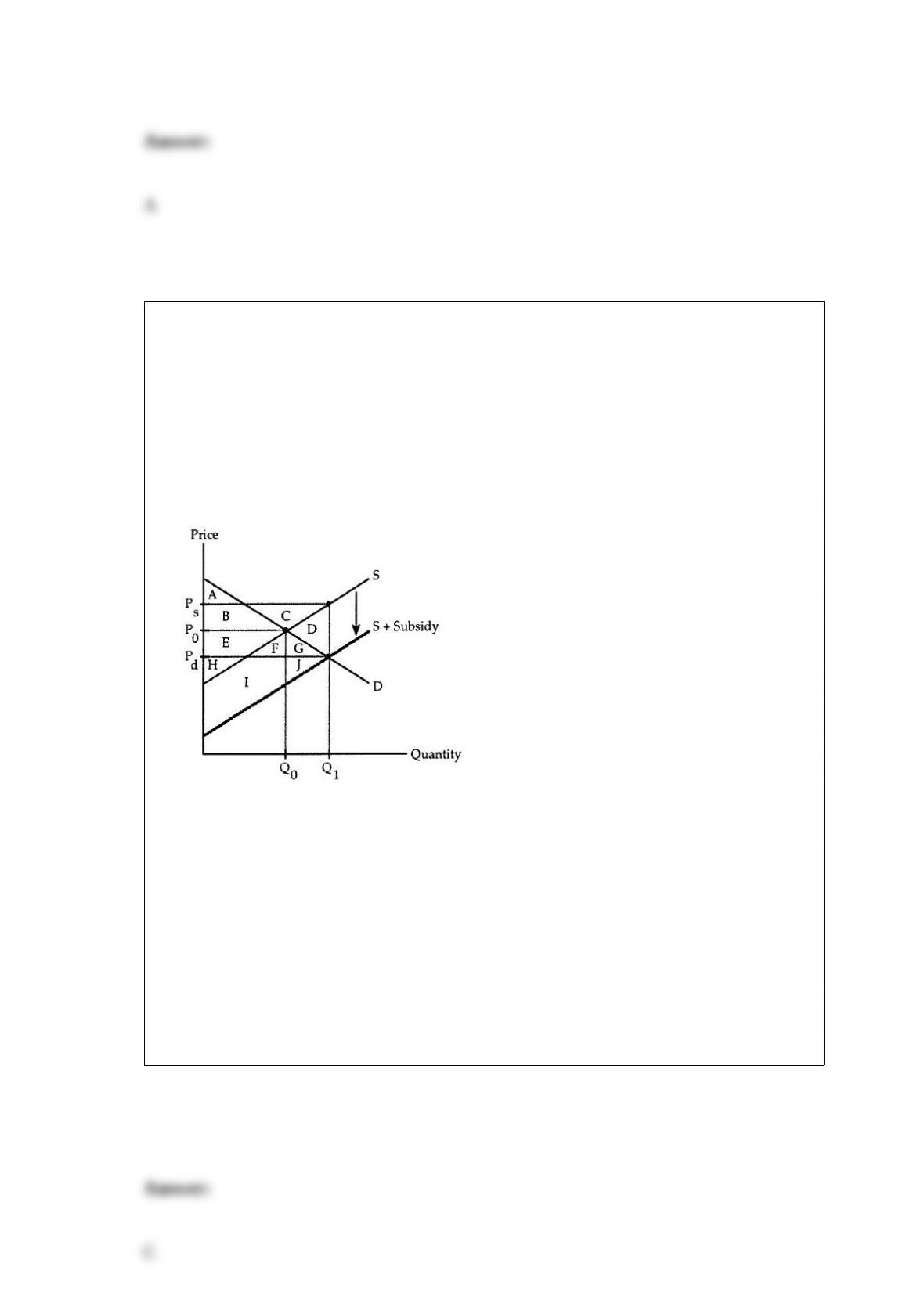

Excise Subsidy

The following questions refer to the accompanying diagram which shows the effects of

an excise subsidy given to firms. The initial price and quantity are P0 and Q0,

respectively. After the subsidy is granted, the equilibrium quantity is Q1, firms receive

the price Ps, and consumers pay the price Pd.

Which areas count as part of the measure for both consumer’s surplus and producer’s

surplus?

a. areas A, B, E and H.

b. areas B, E and F.

c. areas B and E.

d. no areas can count as part of the measure for both.

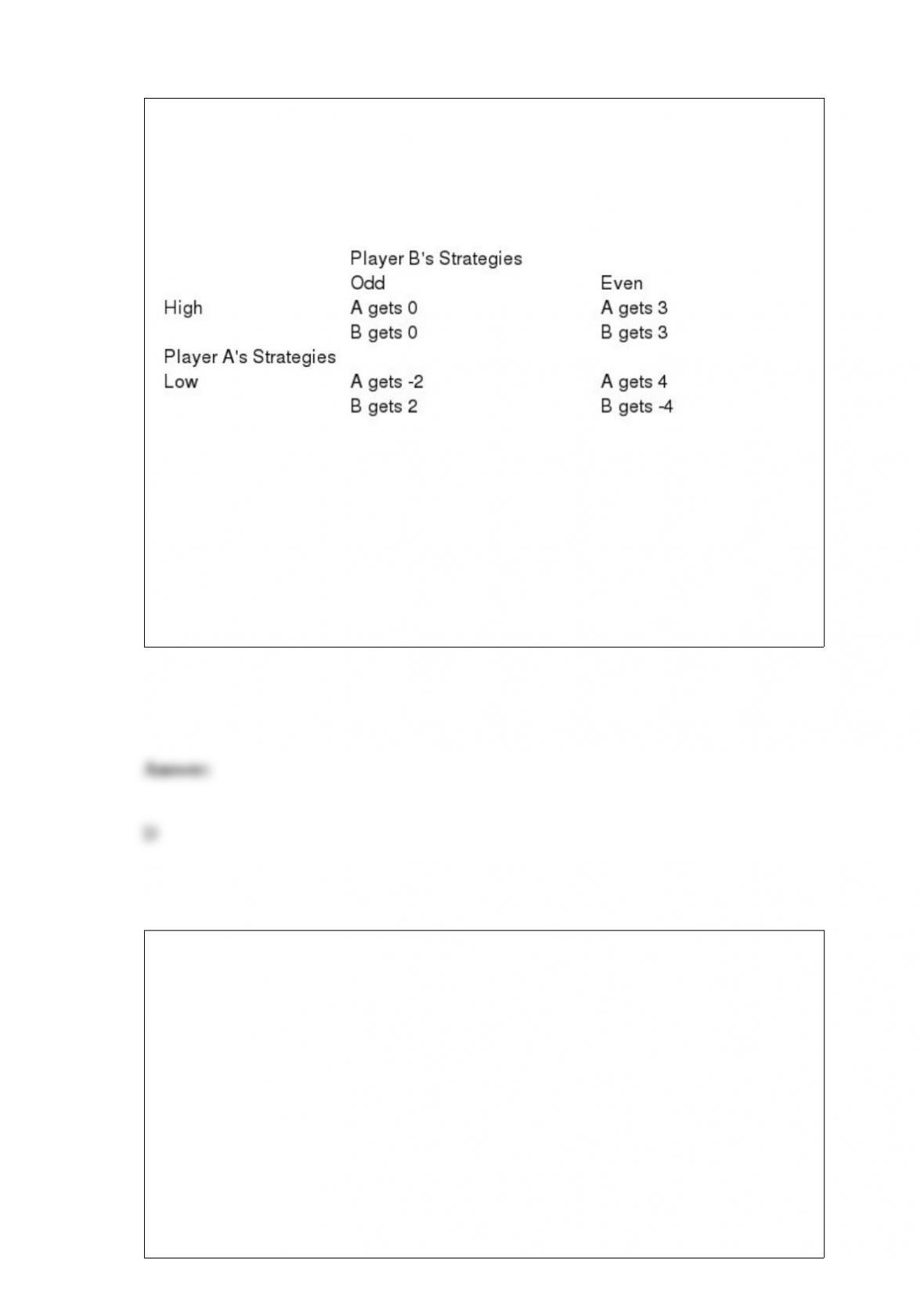

Game Matrix II

The following questions refer to the game matrix below. Player A can play the strategies

“High” and “Low,” and Player B can play the strategies “Odd” and “Even.”

In this game,

a. players A and B both have dominant strategies.

b. player A has a dominant strategy, but player B does not..

c. player B has a dominant strategy, but player A does not..

d. neither player has a dominant strategy..

Goods X and Y

For the following questions, assume that good X is on the horizontal axis and good Y is

on the vertical axis in the consumer-choice diagram. PX denotes the price of good X, PY

is the price of good Y, and I is the consumer’s income. Unless otherwise stated, the

consumer’s preferences are assumed to satisfy the standard assumptions.

If the indifference curves are downward sloping straight lines (rather than convex

curves), then we can conclude that

a. X does not affect the individual’s utility.

b. Y does not affect the individual’s utility.

c. both X and Y affect the individual’s utility.

d. neither good affects the individual’s utility.

The marginal revenue curve of a competitive firm is

a. U-shaped.

b. a ray from the origin.

c. a horizontal line at the market price.

d. downward sloping.

Technical analysts in the financial markets are those who

a. believe that markets always operate efficiently.

b. look for stocks to buy based on the degree to which the company is investing in

technology.

c. argue that a careful study of past prices of a given stock conveys useful information

about future prices.

d. base their analyses on the current state of the macroeconomy.

In a Walrasian equilibrium, which of the following constrains an individual when he

optimizes?

a. The market prices.

b. His tastes.

c. The actions of other individuals.

d. Nothing-the individual has no constraints in a Walrasian equilibrium.

Cournot Problem. Consider Cournot Duopolists that produce homogeneous goods.

These firms each have constant marginal costs of $10. The market for these firms’

product has demand Q = 100 – P.

In the Nash Equilibrium, the market price for this good will be

a. $10

b. $40

c. $55

d. $70

The price of a potato is $1.00 and the price of a tomato is 50 cents. It follows that the

slop of the budget line is

a. 1/2.

b. 1.

c. 2.

d. cannot be determined from the information given.

When some jobs are inherently more risky or unpleasant than other jobs, different

workers will be paid different wages because of

a. differences in human capital.

b. differing access to capital.

c. compensating differentials.

d. discrimination.

The second stage of economic analysis includes asking

a. if the process an individual uses to make decisions is rational or not.

b. what may cause preferences to change.

c. how the optimal solution would change if constraints change.

d. what other criteria might be used to evaluate an outcome.

If regulators require a monopoly to earn zero economic profit, the monopoly will

produce the quantity where

a. the marginal cost curve crosses the average cost curve.

b. the marginal cost curve crosses the demand curve.

c. the average cost curve crosses the demand curve.

d. the marginal cost curve crosses the marginal revenue curve.

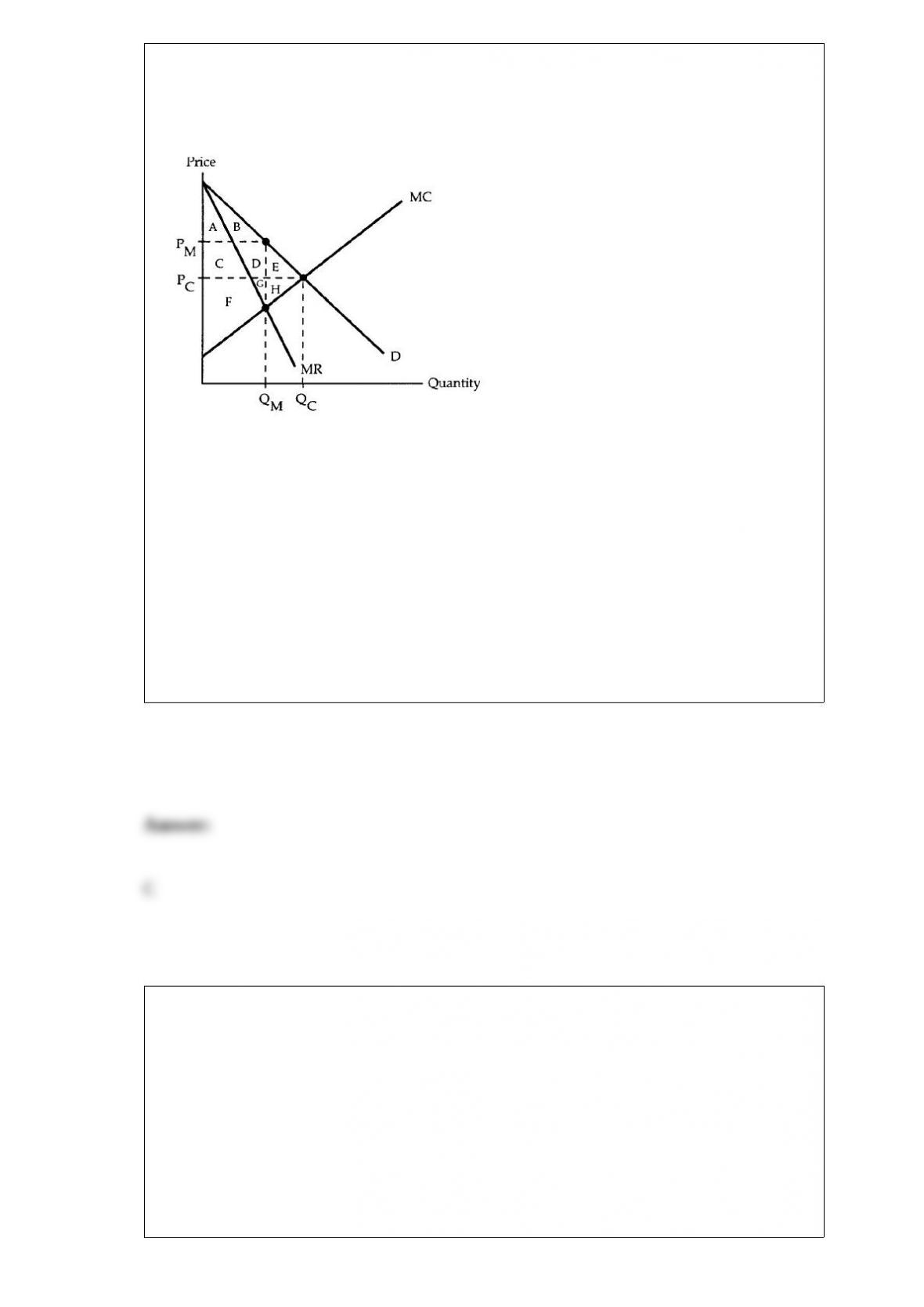

Market Diagram

The following questions refer to the accompanying market diagram. PC and QC are the

equilibrium price and quantity if the firm behaves competitively, and PM and QM are

the equilibrium price and quantity if the firm is a simple monopoly.

Relative to the surplus achieved under perfect competition, how much surplus is lost

(deadweight loss) when there is a monopoly?

a. E

b. H

c. E + H

d. D + G + E + H

If the substitution and income effects are in opposite directions, the law of demand will

hold

a. always.

b. as long as the substitution effect outweighs the income effect.

c. as long as the income effect is the larger of the two effects.

d. only if the good is normal.

In the market for insurance, the adverse selection problem arises because

a. fair odds are different for different people, and the insurance company cannot tell

who is who.

b. people tend to behave more recklessly when they are insured.

c. some events simultaneously affect a large number of people.

d. insurance companies must tilt the odds in their favor to cover their basic operating

costs.

The prices typically studied in microeconomics are

a. relative prices.

b. absolute prices.

c. money prices.

d. retail prices.

Legal restrictions on entry into an industry

a. are strongly opposed by those already in an industry.

b. are promoted through lobbying efforts by those already in the industry, thereby

further increasing the social costs of monopoly.

c. are promoted by those who wish to enter the industry, thereby potentially increasing

the social welfare generated by the industry.

d. are always instituted to protect the public’s health and welfare.

A fair coin is flipped. If it lands heads the person receives $1.00. If it lands tails, the

person receives $11.00. If the person is not willing to pay $6.00 to take this gamble,

they must be

a. risk-neutral.

b. risk-averse.

c. risk-preferring.

d. either risk-neutral or risk-preferring (i.e. not risk averse)

Market basket B is to the northwest of basket A but lies on the same indifference curve

for a consumer. Market basket C also lies to the northwest of A but is above the

indifference curve. This consumer

a. prefers C to A.

b. is also indifferent between A and C.

c. prefers B to A.

d. prefers C to B.

Suppose the market rate of interest is 8%. The local government imposes a tax of $40

per acre on all land located within city limits. The year after the tax is imposed, Val sells

an acre of land on which she had planned to build a house. How much was Val’s share

of the economic burden of the tax?

a. Zero.

b. $40.

c. $320.

d. $500.

Suppose there are only two goods: bread and wine. In Mexico, the absolute price of

wine is 30 pesos per bottle. If the relative price of wine in terms of bread is 5 loaves per

bottle, then the absolute price of bread is

a. 5 pesos per loaf.

b. 6 pesos per loaf.

c. 25 pesos per loaf.

d. 150 pesos per loaf.

When investment is possible, why is the supply of current consumption upward

sloping?

a. Because capital will be more productive in the future than in the present.

b. Because people prefer to have goods today over goods tomorrow.

c. Because of diminishing marginal returns to capital.

d. Because higher interest rates lead to increased investment.

If either player is receiving his maximum payoff, then that outcome is Pareto optimal.

A technological improvement that is permanent is more likely to raise employment than

one that

is temporary.

In a long-run competitive equilibrium, both more efficient and less efficient firms earn

zero economic profit.

In terms of the marginal product of labor, how much labor is needed to produce one

more unit of output? If the cost of that labor is w, then how much does one more unit of

output cost to produce? If a firm is a perfectly competitive profit maximizer, show why

they produce where w equals the marginal revenue product of labor.

It is possible for a firm engaging in predatory pricing to make a profit on the good even

thought the price is set artificially low.

A monopsonist’s short-run demand curve for labor coincides with its marginal revenue

product of labor curve.

Define the term adverse selection. Why is an insurance company unable to offer fair

odds when it faces an adverse selection problem? How might the insurance company

deal with an adverse selection problem?

Social costs are equal to the costs imposed on others.

Laura can type a manuscript in two hours and her opportunity cost of one hour is $20.

Spencer can type the same manuscript in one hour and his opportunity cost of one hour

is $30. If Laura is charged with typing the manuscript, can both be made better off if

Laura pays Spencer to type the manuscript instead? Explain.

An unexpected increase in inflation, by diluting the informational content of prices, will

lead to an increase in unemployment.

The Stigler and Friedland study shows that regulation always has significant effects on

price, although those effects may be positive or negative.

Explain why crossing indifference curves would lead to a logical inconsistency.

Suppose the price of cheese has recently risen from $4 to $6 per pound, while the price

of fruit has fallen from $8 to $6 per pound. During this time, Miguel’s income has

stayed fixed at $48 per week. Before the price changes, Miguel had been buying 4

pounds of cheese and 4 pounds of fruit per week. Since the price changes, he has been

buying 2 pounds of cheese and 6 pounds of fruit weekly. Assuming Miguel’s

preferences have not changed, is it possible to say whether the price changes have made

Miguel better off or worse off? Explain.

Demand in a perfectly competitive market is Q = 100 – P. Supply in that market is Q = P

– 10. What is the market equilibrium price and quantity? Given that price and quantity,

how much consumer surplus, producer surplus, and deadweight loss is there? If the

government imposes a $10 per unit sales tax, what is the new equilibrium price and

quantity? Once the government imposes the tax, how consumer surplus, producer

surplus, and dead-weight loss is there?

A factor’s rent tends to rise from the short run to the long run.

Short-run and long-run average cost curves are both U-shaped because the firm must

eventually encounter diminishing marginal returns to labor.