You estimate a simple linear regression model using a sample of 25 observations and

obtain the following results (estimated standard errors in parentheses below coefficient

estimates):

y = 97.25 + 19.74 *x

(3.86) (3.42)

You want to test the following hypothesis: H0: = 1, H1: >12. If you choose to

reject the null hypothesis based on these results, what is the probability you have

committed a Type I error?

a.)between .01 and .02

b.)between .02 and .05

c.)less than .005

d.) It is impossible to determine without knowing the true value of b2

) You estimate a model with 5 explanatory variables and an intercept from a data set

with 247 observations. To test hypotheses on this model you should use a t distribution

with how many degrees of freedom?

a.) 242

b.) 120

c.) ∞

d.) 241

Final grades in Professor Pickle’s course are calculated as a weighted average of the

midterm and final exam. The midterm is weighted at 0.4 and the final is weighted as

0.6. This semester grades on the midterm exam were normally distributed with = 63

and = 14. Grades on the final exam were also normally distributed with = 75 and

= 20.

a.) Calculate the average final grade in Professor Pickle’s course?

b.) What do you expect the variance of the distribution of final grades to be? Why?

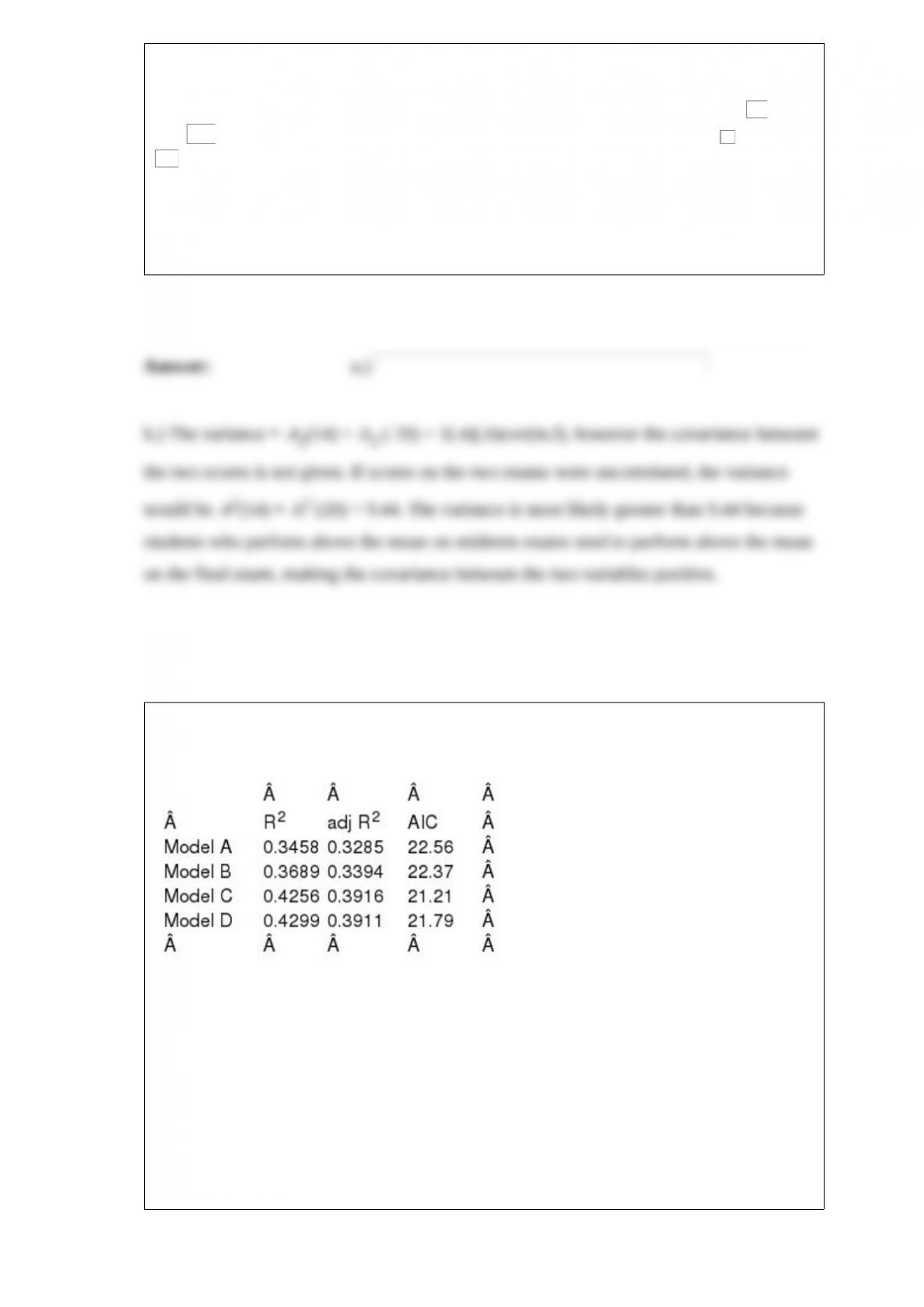

You estimate 4 different specifications of an econometric model by adding a variable

each time and get the following results

Which model appears to be correctly specified?

a.)A

b.)B

c.)C

d.)D

When a decision maker has to choose between two mutually exclusive outcomes an

econometrician may choose to use a(n)

a.) binary choice model

b.) ECM

c.) random effects model

d.) fixed effects model

What is second order sample autocorrelation?

a.) correlation between a mean and the second moment of the sample distribution

b.) a test statistic distributed N(0, )

c.) correlation between observations that are two time periods apart

d.) correlation between the dependent variable and a squared explanatory variable

What type of model tells you whether two series are significantly related to each other?

a.) a VAR model

b.) an impulse response function

c.) variance decomposition

d.) an ARDL model

When should a researcher consider transforming the explanatory variable in a simple

linear regression model?

a.) when a data plot suggests there is a non-linear functional form

b.) to get a coefficient estimate with the sign predicted by economic theory

c.) to reduce the variation in the explanatory variable

d.) to maximize SSR

Which of the following is NOT a reason nonlinear least squares is used to estimate an

AR(1) model?

a.) linear least squares is not possible since the transformation that allows the new error

term to be uncorrelated is no longer linear in parameters

b.) using OLS to estimate the untransformed model provides incorrect standard errors

c.) the algorithmic nonlinear optimization is less complicated to compute when error

terms are correlated

d.) minimizing the sum of squares of uncorrelated error terms produces an estimator

that is unbiased and consistent

If you use a times series data set with 100 years worth of data to estimate a distributed

lag model of order 5, how many observations will you have for estimation?

a.) 100

b.) 5

c.) 95

d.) 105

You estimate a simple linear regression model using a sample of 25 observations and

obtain the following results (estimated standard errors in parentheses below coefficient

estimates):

y = 97.25 + 19.74* x

(3.86) (3.42)

What are the endpoints of the interval estimator for with a 98% interval estimate?

a.) (-5.77, 25.51)

b.) ( 16.32 , 23.16)

c.) (11.19, 28.29)

d.) (12.90, 26.58)

What is accomplished by using a Tobit model rather than the least squares estimator?

a.) it generate unbiased and consistent estimates on censored data

b.) it corrects sample selection bias

c.) it allows for choice models to be estimated using GLS

d.) it generates the same unbiased coefficient estimates, but with smaller variances

Which of the following is a common way to convert a nonstationary series to a

stationary series?

a.) detrending

b.) autoregression

c.) estimating distributed lags

d.) cointegrating