Which statement best completes the following sentence; “The U.S. dollar is to the fifty

states as the euro is to”?

A. The European Central Bank

B. The states of the European Monetary Union

C. The National Central Banks

D. The European System of Central Banks

Answer:

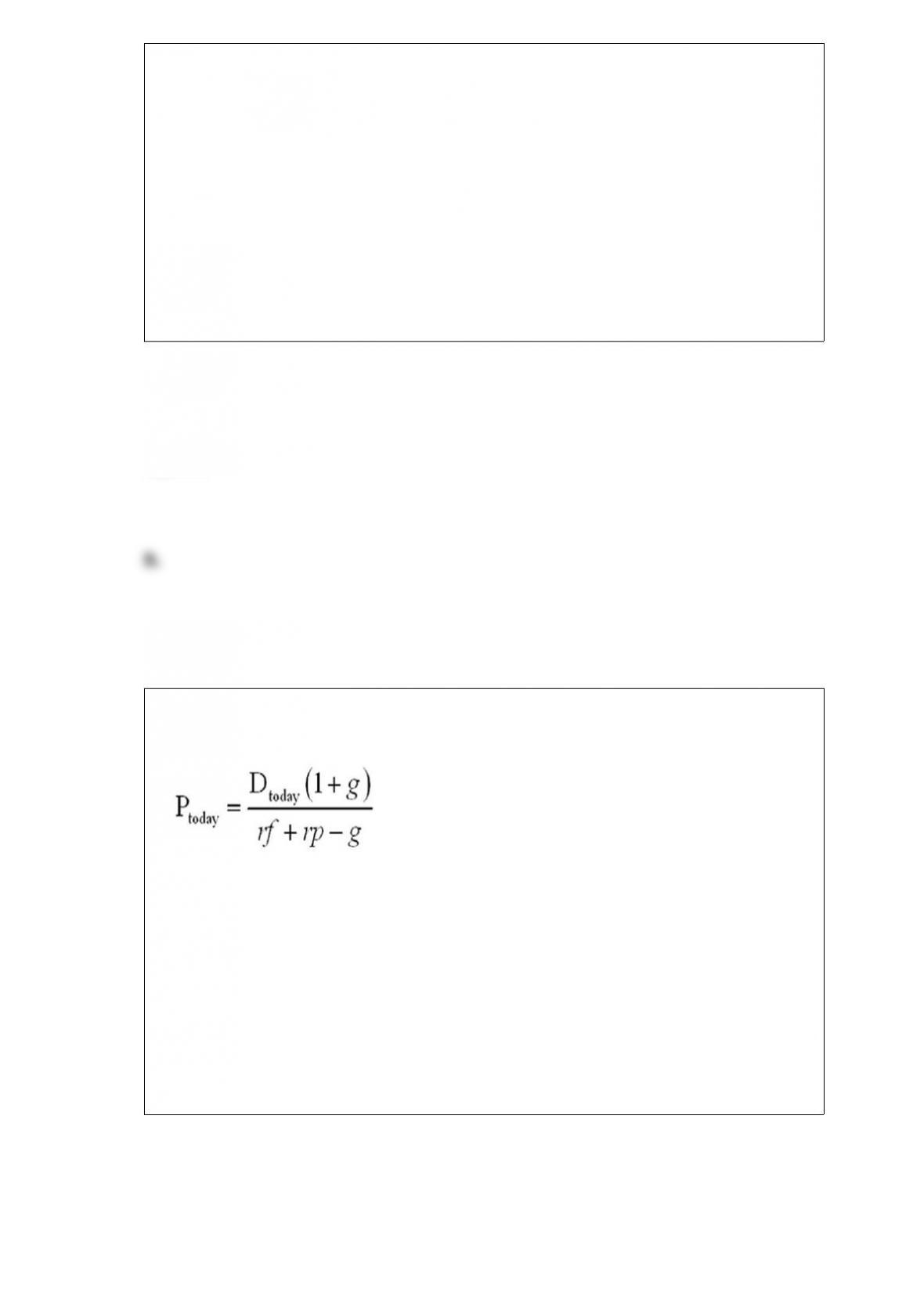

Which of the following will cause an increase in the current price of a stock?

A. A decrease in the risk-free return

B. A decrease in the current dividend

C. A decrease in the dividend growth rate

D. Both an increase in the risk-free return or an increase in the current dividend

Answer:

Which of the following individuals is least likely to use value at risk as an important

factor in his/her investment decision?

A. An individual considering a mortgage to buy his first home.

B. A family considering purchasing health insurance.

C. A policy maker considering regulation of depository institutions.

D. A mutual fund manager choosing the allocation of investments in the fund’s

portfolio.

Answer:

The additional capital requirements put in place following the banking crisis of the

1980s led to a:

A. quick rebound in the willingness and ability of banks to make loans.

B. further slowdown in bank lending.

C. period of rapid economic growth in the early 1990s.

D. prolonged economic slowdown lasting much of the 1990s.

Answer:

Which of the following statements best describes financial markets?

A. Financial markets lower the cost and increase the speed of buying and selling

financial instruments.

B. Financial markets increase the speed of buying and selling, but they also increase

the cost since people are earning fees for these transactions.

C. Financial markets are a good example of unregulated markets.

D. Financial markets today offer fewer instruments than they did in the past.

Answer:

An easing of monetary policy should:

A. increase spending by households and businesses and increase net exports.

B. raise net exports but lower spending by households and businesses.

C. decrease spending by households and businesses as well as net exports.

D. increase investment and household spending but lower net exports.

Answer:

Index funds are often preferred to other mutual funds because:

A. they offer greater diversification.

B. they are managed better.

C. they have greater liquidity.

D. on average they have lower management fees.

Answer:

The U.S. Treasury issues bonds where the return is indexed to the consumer price

index. We should expect that these bonds, relative to other U.S. Treasury bonds, will

have:

A. lower price and lower return due to the decreased risk.

B. lower price and a lower fixed return since the demand for them should be higher.

C. higher price and higher fixed return since we always seem to have some inflation.

D. higher price and lower return due to the decreased risk from inflation in holding

these bonds.

Answer:

Each of the Reserve Banks has a president who is:

A. appointed by the bank’s board of directors but approved by the board of governors.

B. appointed by the board of governors but approved by the bank’s board of directors.

C. elected by the commercial banks in their district.

D. selected from the Board of Directors.

Answer:

A proposed increase in the federal income tax rate should:

A. have no impact on the slope of the yield curve since the tax laws impact all

maturities the same.

B. cause the slope of the yield curve to become negative.

C. increase the slope of the yield curve since it increases the risk premium of longer

maturities.

D. flatten the yield curve.

Answer:

Which of the following regulates commercial banks as well as savings banks and

savings and loans?

A. The Federal Reserve System

B. Securities and Exchange Commission

C. The Office of the Comptroller of the Currency

D. The Internal Revenue Service

Answer:

Which of the following statements is most correct?

A. High real interest rates cause recessions.

B. Central bankers raise real interest rates to cause recessions.

C. There is no evidence that high real interest rates are followed by lower levels of

growth.

D. There is evidence that high real interest rates are followed by lower levels of

growth.

Answer:

Which of the following statements is most correct?

A. the higher the deposit insurance limit the lower the risk of moral hazard.

B. the higher the deposit insurance limit the greater the risk of moral hazard.

C. deposit insurance limits do not impact moral hazard, they impact adverse selection.

D. increasing the deposit insurance limits above $100,000 would increase coverage for

over 50 percent of all depositors.

Answer:

The importance of the bank lending transmission mechanism of monetary policy:

A. has increased over the past twenty years.

B. has decreased over the past twenty years.

C. should continue to grow in importance.

D. has always been the weakest of all of the mechanisms.

Answer:

If your stockbroker gives you bad advice and you lose your investment:

A. the government will reimburse you similar to reimbursing depositors if a bank fails.

B. the government will not reimburse you for the loss; you are not protected from bad

advice by your stockbroker.

C. these losses would be covered under FDIC insurance.

D. your investment would only be covered if the stockbroker was employed by a bank.

Answer:

Policymakers could neutralize all of the following except:

A. an increase in federal government spending on defense.

B. an increase in the price of oil.

C. a trade deficit.

D. a decrease in business confidence.

Answer:

The yield on a tax-exempt bond:

A. equals the taxable bond yield times one minus the tax rate.

B. is equal to the yield on a U.S. 30-year bond.

C. is called the risk-free yield.

D. only applies to foreign bonds because they are exempt from U.S. income taxes.

Answer:

The International Monetary Fund’s primary role under the Bretton Woods System was

to be:

A. the issuer of gold.

B. the clearinghouse for international transactions.

C. a short-term lender for countries with an excess of imports over exports.

D. the arbiter of trade disputes.

Answer:

Which of the following is an example that can help explain increased profits for large

financial holding companies?

A. Financial holding companies offer a wide array of services under many brand

names.

B. Financial holding companies need only one CEO, one Board of Directors, and one

computer system regardless of size.

C. Financial holding companies are not well diversified and receive a higher return for

the higher risk.

D. Financial holding companies are exempt from having to pay for FDIC insurance.

Answer:

Today, reserve requirements are:

A. set in a way that makes reserve demand highly unpredictable.

B. changed whenever the target federal funds rate is changed.

C. changed instead of making changes in the discount rate.

D. really not a direct tool of monetary policy.

Answer:

The seller of a put option is transferring the risk:

A. of a price decrease of the stock to the buyer of the option.

B. of a price increase of the stock to the buyer of the option.

C. this statement is incorrect since options do not transfer risk.

D. this statement is incorrect since only sellers of call options are transferring risk.

Answer:

Many health insurers require a deductible where the policyholder pays the first part of

any loss. The use of a deductible most directly treats the problem of:

A. free riding.

B. adverse selection.

C. people going uninsured.

D. moral hazard.

Answer:

The only solution available to a country experiencing extremely high rates of inflation

is to:

A. raise interest rates.

B. peg your currency to another country’s currency.

C. reduce money growth.

D. revert to a gold standard.

Answer:

A country that has a capital account surplus:

A. is a net seller of assets.

B. has a current account surplus.

C. is a net buyer of assets.

D. will see its currency remain steady.

Answer:

The purpose of derivatives is to:

A. increase the risk so the return is larger.

B. eliminate risk for both parties in the transaction.

C. postpone the risk for both parties in the transaction.

D. transfer the risk from one person to another.

Answer:

An increase in the price of oil should cause the short-run aggregate supply curve to:

A. shift to the right.

B. become vertical.

C. become horizontal.

D. shift to the left.

Answer:

If the annual interest rate is 5%(.05), the price of a six-month Treasury bill would be:

A. $97.50

B. $97.59

C. $95.25

D. $95.00

Answer:

The collapse of the Thai currency, the baht, was partially due to:

A. inaction by the Federal Reserve.

B. the European Central Bank.

C. information provided by the central bank of Thailand.

D. information not provided by the central bank of Thailand.

Answer:

A bagel cost $1 in New York and 0.5 euros in Paris. If the real exchange rate is one-half

of a New York bagel for a Parisian bagel, how many euros should you receive in

exchange for one dollar?

A. 0.1

B. 2

C. 0.25

D. 1.5

Answer:

The fact that, for most of its history, the Fed was reluctant to make discount loans

actually:

A. at times was a destabilizing force for financial markets.

B. proved to be a very stabilizing force for financial markets.

C. pushed the discount rate above the target federal funds rate.

D. resulted in banks in very strong financial shape as being the only ones borrowing

from the Fed.

Answer:

For every $100 in assets, a bank has $30 in interest-rate sensitive assets, and the other

$70 in non-interest-rate sensitive assets. The same bank has $60 for every $100 in

liabilities in interest-rate sensitive liabilities, the other $40 are in liabilities that are not

interest-rate sensitive. If the interest rate on assets decreases from 6 to 5 percent, and

the interest rate on liabilities decreases from 4 to 3 percent, the impact on the bank’s

profits per $100 of assets will be:

A. a reduction of $0.30.

B. an increase of $0.30.

C. a reduction of $3.00.

D. zero since the interest rates on assets and liabilities fell by the same amount.

Answer:

Bond prices and yields:

A. move together in the same direction.

B. do not change if the coupon is fixed.

C. move together inversely.

D. are independent of each other.

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer:

Answer: