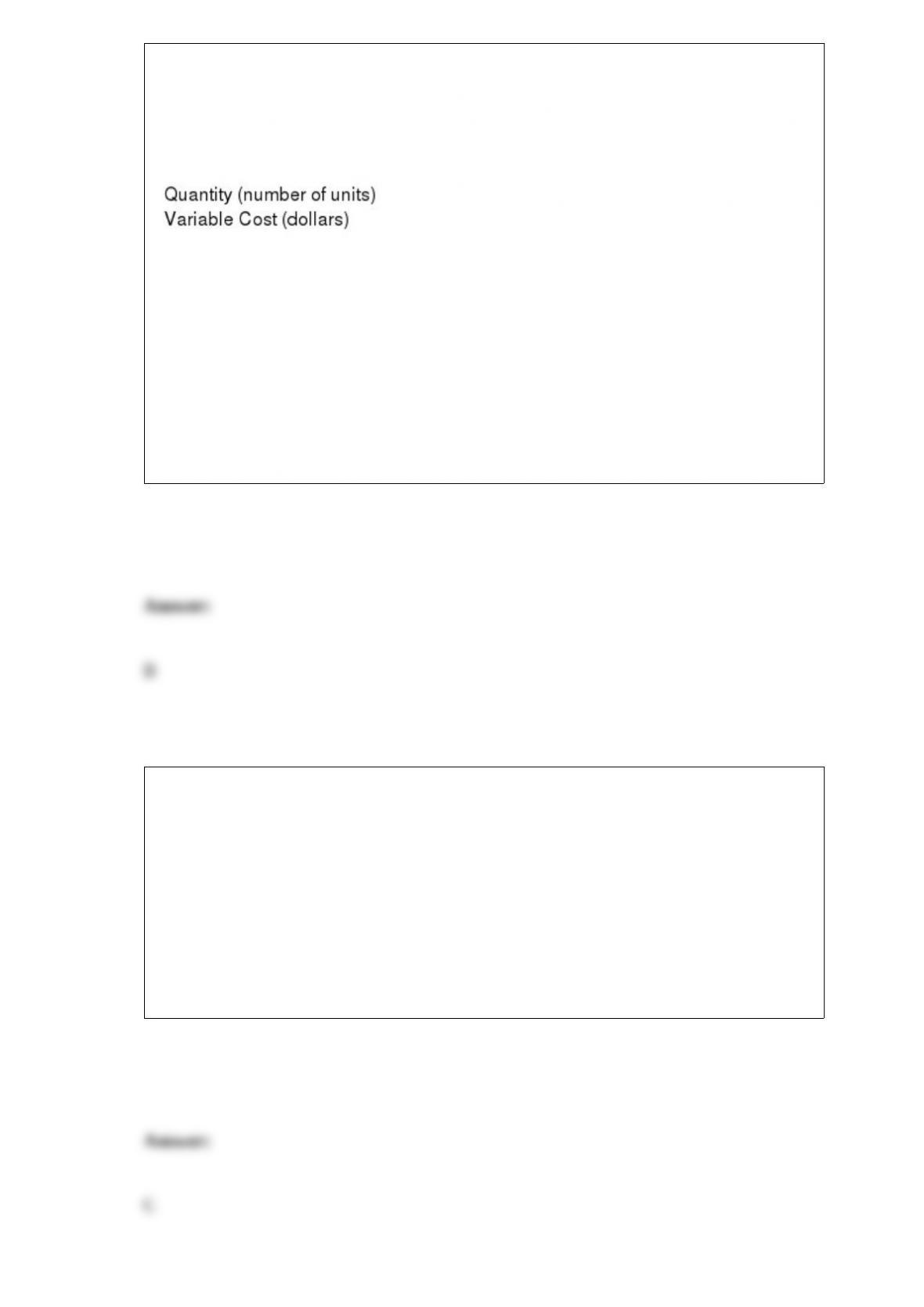

Variable Cost of Production

The following questions refer to the following table which shows a firm’s variable costs

of production.

If the firm instead has $15 in fixed costs, the average cost of the third unit of output is

a. $20 per unit.

b. $25 per unit.

c. $30 per unit.

d. $35 per unit.

When input prices are fixed, decreasing returns to scale implies that the long-run

average cost curve is

a. downward sloping.

b. horizontal.

c. upward sloping.

d. U-shaped.

A die is rolled. If it lands 1 or 2, the person receives $90. If it 3 or 4, the person receives

$30.00. If it lands 5 or 6, the person receives $60. If the person is willing to pay $60 to

take this gamble, they must be

a. risk-averse.

b. risk-neutral.

c. risk-preferring.

d. either risk-neutral or risk-preferring (not risk-averse).

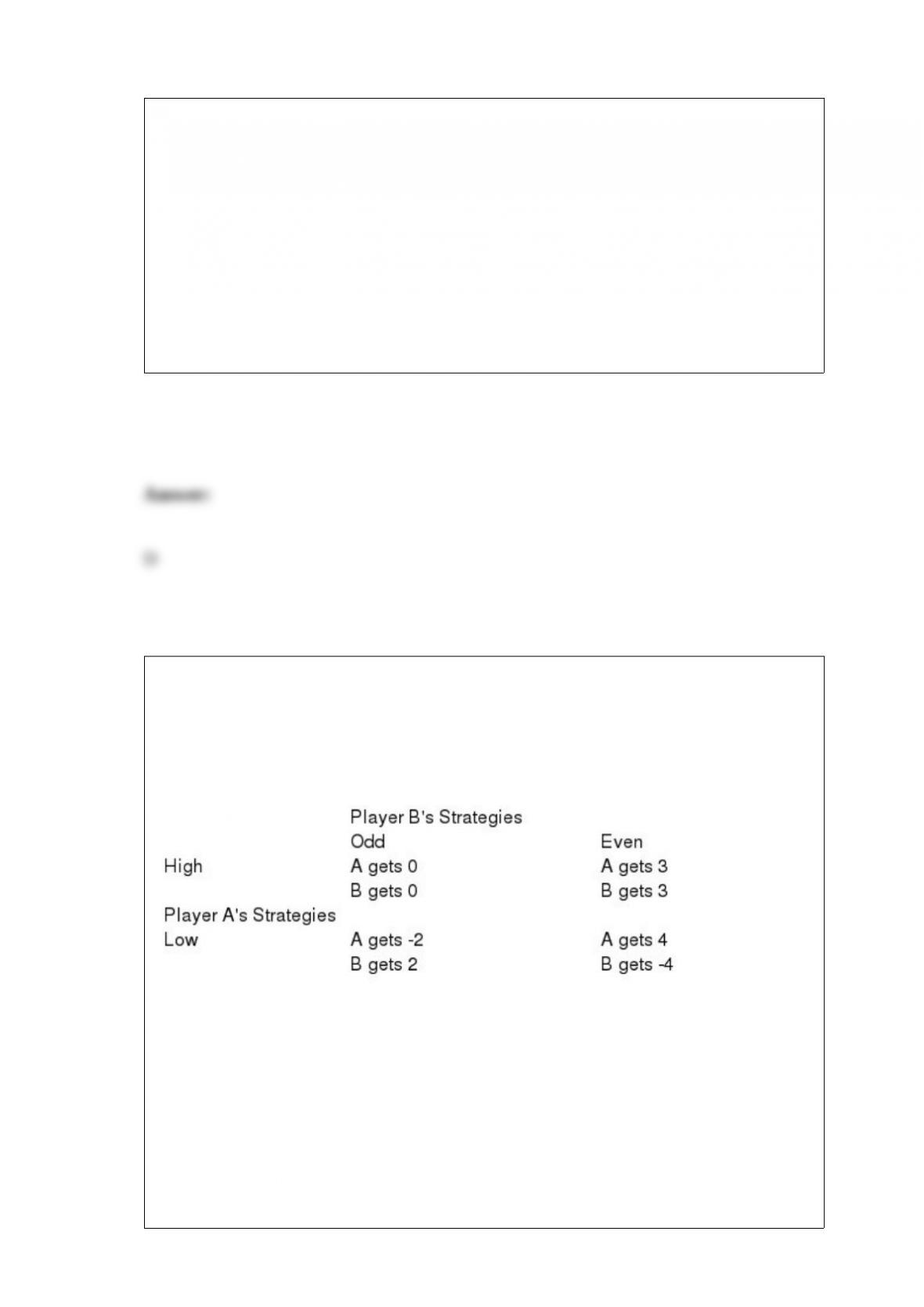

Game Matrix II

The following questions refer to the game matrix below. Player A can play the strategies

“High” and “Low,” and Player B can play the strategies “Odd” and “Even.”

Assume this game is played sequentially. When is the Stackelberg equilibrium of this

game also Pareto optimal?

a. Always.

b. When A is the first player.

c. When B is the first player.

d. Never.

If people have identical tastes, then the economic rent created by a common property is

a. zero.

b. as large as possible.

c. positive, but not as large as possible.

d. negative.

For a fixed resource like land to be allocated to its highest valued use

a. a good social plan is needed.

b. it should be allocated to those who will pay the most.

c. it should be taxed at 100 percent of its rental value.

d. it should be offered to those who promise to put it to its best use.

The difference between an absolute price and a relative price is that:

a. absolute prices are based on costs of production, relative prices are based on market

exchange.

b. absolute prices are in terms of currency, relative prices are in terms of another good.

c. absolute prices are in terms of another good, relative prices are in terms of currency.

d. absolute prices never change, relative prices change with inflation.

Which of the following is not necessarily true in the long for a competitive industry?

a. Firms earn zero profits.

b. Firms set MC = MR.

c. A firm will not produce if the market price is less than their break-even price.

d. The long-run supply curve is more elastic than the short-run supply curve.

The most basic concepts on which the social science of economics rests are

a. consumers and producers.

b. money, interest rates, and exchange rates.

c. supply and demand.

d. scarcity and choice.

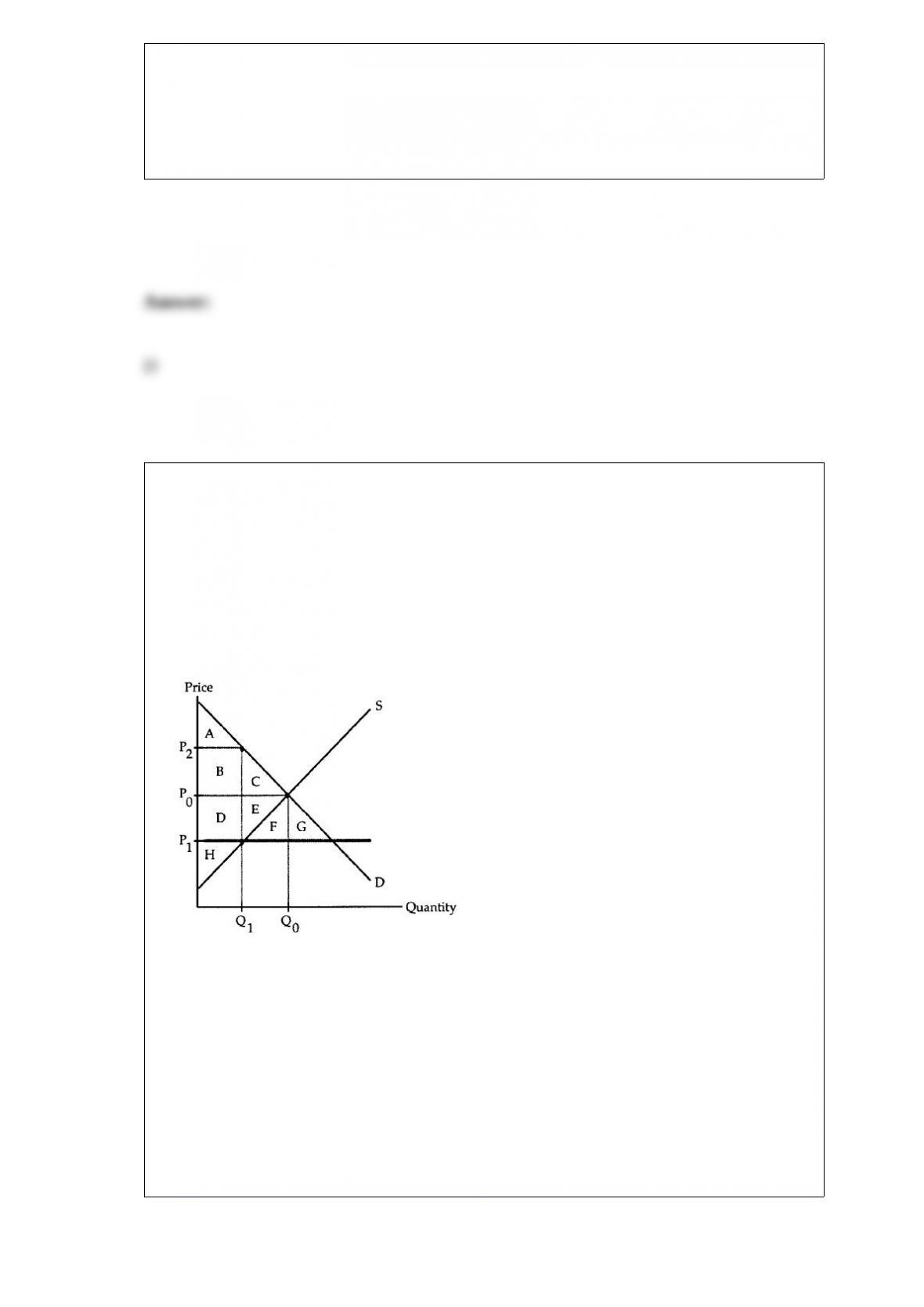

Price Ceiling

The following questions refer to the accompanying diagram which shows the effects of

a price ceiling. The initial price and quantity are P0 and Q0, respectively, and the price

ceiling is imposed at the price P1. Assume that none of the potential deadweight loss

can be avoided.

Area B + D represents

a. the deadweight loss due to the price ceiling.

b. the fall in consumers’ surplus caused by the imposition of the price ceiling.

c. the value of the time and resources spent by consumers to acquire the limited supply.

d. the post-ceiling profits earned by the producers of the good.

Which of the following would cause the demand curve for rice to shift to the left?

a. A rise in the price of rice.

b. A blight that destroyed 75% of the rice harvest.

c. A report claiming that the starch in rice causes heart disease.

d. A tariff that doubles the price of imported spaghetti.

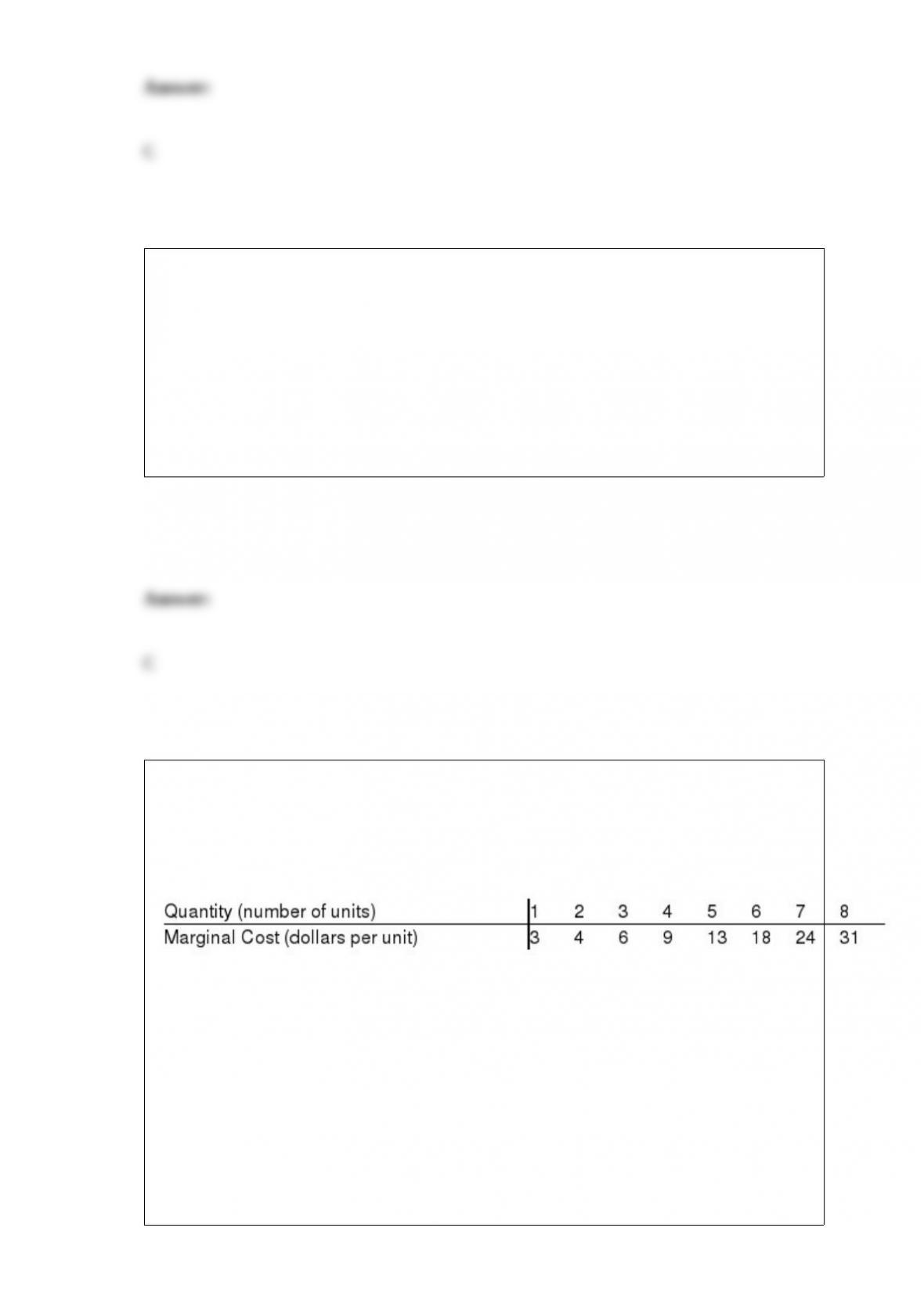

Marginal Cost of Production

The following questions refer to the following table which shows a firm’s marginal cost

of production.

Suppose the firm’s fixed costs increase to $60, and demand for the firm’s product

remains horizontal at a price of $18 per unit. What is the firm’s maximum profit?

a. $-7.

b. $-5.

c. $33.

d. $48.

All of the following statements about the free market equilibrium output are equivalent

except:

a. Total surplus is maximized.

b. There is zero dead-weight loss.

c. There are no allocations that a Pareto preferred.

d. There is positive dead-weight loss.

Who tends to receive the benefits from a public good that increases the desirability of

living in a certain area?

a. Government.

b. Residents.

c. Landlords.

d. No one.

When will an individual’s budget line coincide with an iso-expected value line?

a. Always.

b. Never.

c. When the individual is risk-neutral.

d. When the individual is offered fair odds.

Economists use the term normal good to refer to goods that

a. you consume on a daily basis.

b. you consume more of when your income falls.

c. you consume more of when your income rises.

d. consumers choose the same quantities of regardless of income.

An employee injured by a damaged machine that the employer knows is broken has

recourse under

a. the Good Samaritan Rule.

b. the standard of Strict Liability.

c. the legal principle of General Average.

d. the doctrine of Respondent Superior.

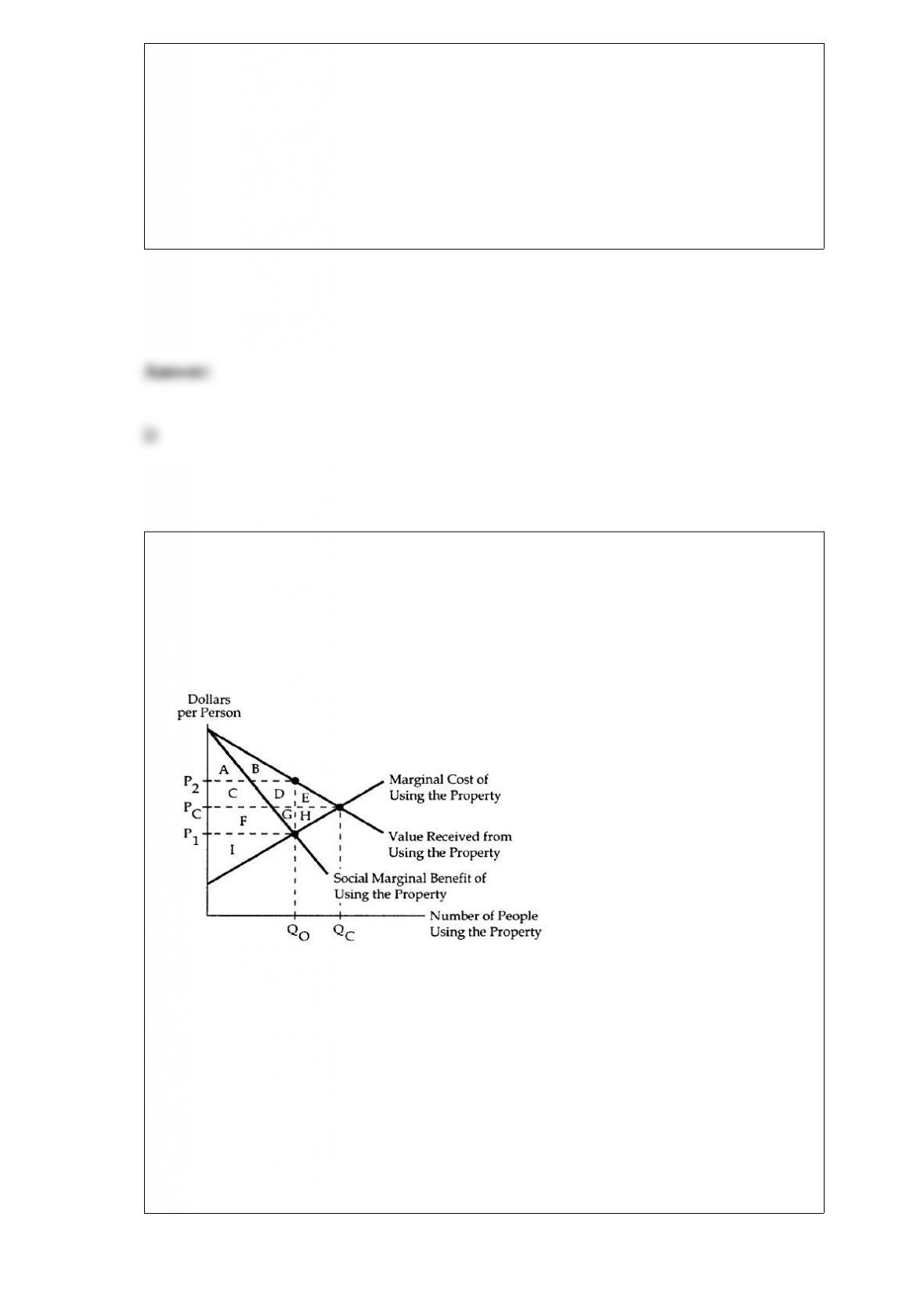

Common Property II

The following questions refer to the accompanying diagram, which shows the benefits

and costs associated with the use of a common property.

If the common property is privately owned, the amount of the good supplied equals

a. QO

b. QC

c. zero.

d. none of the above.

Why might an equation that has always predicted accurately in the past prove to be

wrong following a policy change?

a. Because the policy may change people’s behavior and invalidate the equation.

b. Because people’s expectations may cease to be rational.

c. Because uncertainty means that every equation contains some degree of error.

d. Because the policy change may affect economic variables not contained in the

equation.

When do new firms tend to enter a competitive industry?

a. When the large firms in the industry are earning zero profit.

b. When the smaller firms are leaving the industry.

c. When the new entrants can earn positive profits.

d. When there is an absence of fixed costs in the long run.

Third-degree price discrimination occurs when a monopoly

a. separates its customers into distinct markets, charging a different price to each group.

b. charges different prices for the same good sold to the same customer.

c. requires the consumer to pay a separate fee simply for the right to purchase the good.

d. charges each customer the maximum that he is willing to pay for each item

purchased.

When should a firm increase its production?

a. When it is earning a positive profit.

b. When its revenues are too low to cover the firm’s fixed costs.

c. When there is a fall in the price of its product.

d. When its marginal revenue exceeds its marginal cost.

Tax Problem. Consider a perfectly competitive market were demand is Q = 100 – P and

Supply isQ = P – 10.

If the government imposes a $10 per unit consumption tax, then the market will

produce

a. 20 units

b. 40 units

c. 45 units

d. 90 units

Goods X and Y

For the following questions, assume that good X is on the horizontal axis and good Y is

on the vertical axis in the consumer-choice diagram. PX denotes the price of good X, PY

is the price of good Y, and I is the consumer’s income. Unless otherwise stated, the

consumer’s preferences are assumed to satisfy the standard assumptions.

If the indifference curves are horizontal, then we can conclude that

a. X does not affect the individual’s utility.

b. Y does not affect the individual’s utility.

c. both X and Y affect the individual’s utility.

d. neither good affects the individual’s utility.

Montana cattle ranchers are complaining about mountain state sheep ranchers whose

animals they contend are eating too much grass on the open range. The sheep ranchers

claim that the cattle are eating too much of the grass. This is an example of

a. an external benefit.

b. the reciprocal nature of externalities.

c. the principal agent problem.

d. a situation in which strict liability would be the more efficient solution.

Employers may choose to pay efficiency wages that are higher than the equilibrium

wage because

a. workers will be more willing to accept monitoring by their employers.

b. the threat of unemployment will help prevent workers from shirking.

c. the higher compensation will encourage workers to take more risks.

d. higher wages will attract only the most qualified workers and thus help solve the

employer’s adverse selection problem 2.

At a corner solution, which of the following is know to be true?

a. The slope of the indifference curve equals the slope of the budget line.

b. The slope of the indifference curve is greater than the slope of the budget line.

c. The slope of the indifference curve is less than the slope of the budget line.

d. The slope of the indifference curve does not equal the slope of the budget line.

A state lottery commission offers a new millionaire game – a one in a million chance to

win one million dollars. If the price of a lottery ticket is $1.50, who would buy any?

a. Only risk-neutral individuals.

b. Only risk-preferring individuals.

c. Both risk-neutral and risk-preferring individuals.

d. Anyone, risk preferences would not matter.

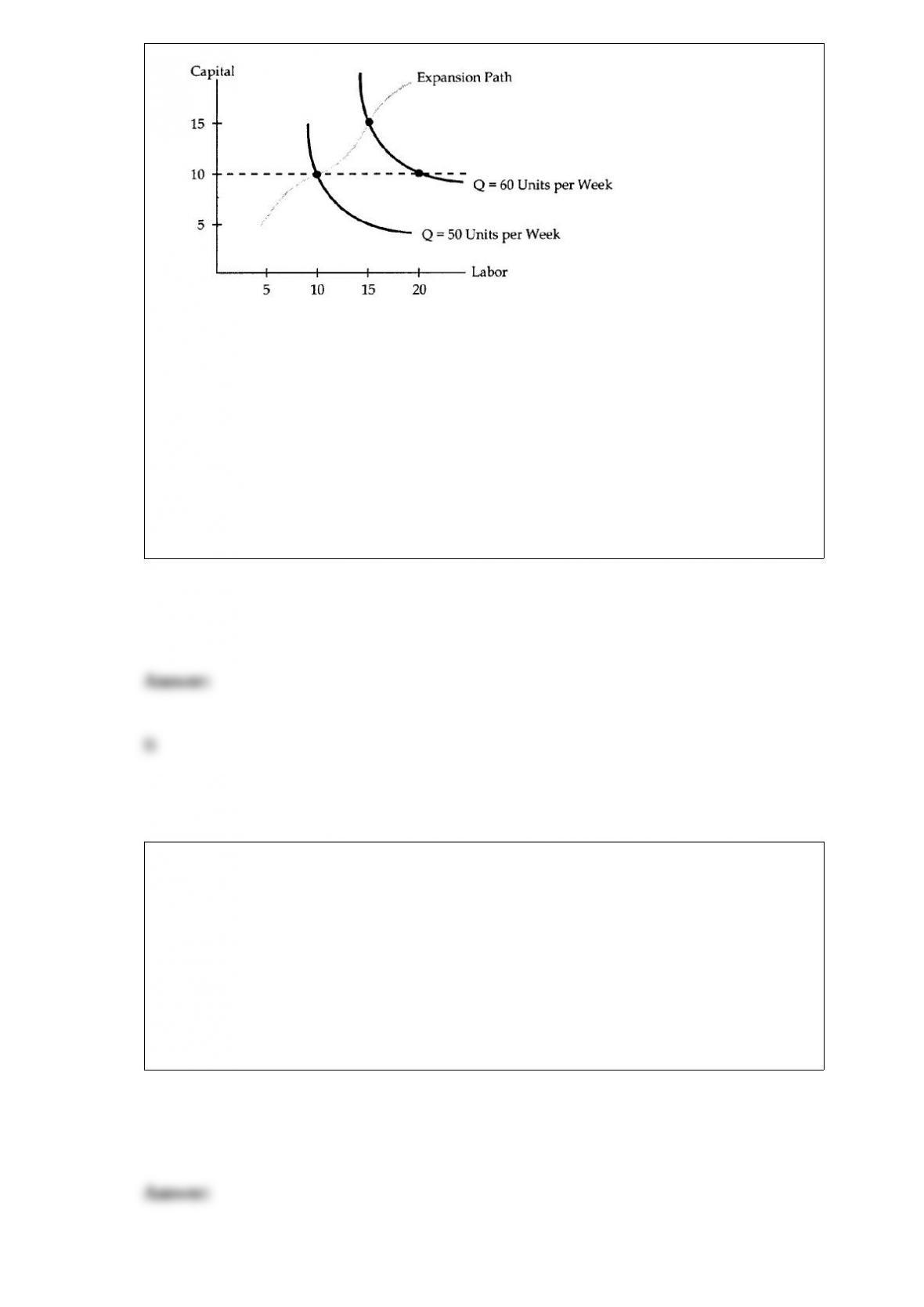

Cost of Production

The following questions refer to the diagram below. The wage rate is assumed to be $12

per hour, the rental rate is assumed to be $6 per hour, and capital is assumed to be fixed

in the short run at 10 hours.

. The short-run average cost of producing 50 units of output per week is

a. $3 per unit.

b. $3.60 per unit.

c. $5 per unit.

d. $2.77 per unit.

A promise to pay at some time in the future

a. indicates the present value of a future payment.

b. is a bond.

c. is the interest rate on debt.

d. is a dividend.

A neighbor slips on an icy sidewalk in front of your house, resulting in $500 of medical

bills. The court rules that the accident had a 20% chance of occurring. Under a

negligence standard, you will be held liable for damages if removing the ice from the

sidewalk would have cost you less than

a. $20.

b. $100.

c. $500.

d. $1,000.

Which of the following best describes the substitution effect caused by a price increase?

a. A change in consumption due to the fact that you will not buy goods whose marginal

value is below the new price.

b. A change in consumption due to the fact that you cannot afford your original market

basket.

c. A smaller percentage change in quantity than in price.

d. A larger percentage change in quantity than in price.

As more of an activity is undertaken, it is reasonable to assume that

a. the total benefits will decline.

b. the marginal benefits will decline.

c. the fixed costs will decline.

d. the marginal benefits will increase.

How are a firm’s short-run and long-run average cost curves related?

a. SRAC is greater than LRAC, which forces the LRAC curve to be upward sloping.

b. SRAC and LRAC slope up or down together, but SRAC is always the steeper of the

two curves.

c. The SRAC curve is tangent to and lies above the LRAC curve.

d. The LRAC curve just touches the SRAC curve at its minimum point.

Suppose favorable weather conditions temporarily raise the marginal productivity of

existing capital. Weather conditions are expected to return to normal next year, so there

is no change in the expected marginal productivity of future capital. In this situation, the

interest rate will

a. rise.

b. fall.

c. remain unchanged.

d. react unpredictably.

Suppose a sales tax of $1 is imposed on DVDs. Suppose the tax causes the price

received by suppliers of the DVDs to fall by 60 cents. In this situation, the economic

incidence of the sales tax

a. falls more heavily on the demanders of DVDs.

b. falls more heavily on the suppliers of DVDs.

c. is evenly split between the demanders and suppliers of the DVDs.

d. is the same as the legal incidence of the tax.

Total cost and marginal cost can both be plotted on the same graph since both include a

measure of quantity.

A risk neutral individual has indifference curves that are identical to the iso-expected

lines of a fair gamble.

What is a principal-agent problem and why does it create inefficiency? What are

efficiency wages and how can they help correct principal-agent problems?

Explain why many models of discrimination result in the prediction of segregated

workforces.

The Cournot oligopoly model is based on the assumption that firms treat their rivals’

output as fixed and given.

In order to profit maximize, the price of a firm’s output should be equated to the ration

of the price of its labor to the marginal product of its labor.

In the absence of transactions costs, changes in property rights have no effect on the

distribution of income.

Higher wages always cause a worker to increase the quantity of labor supplied.

Unlike regular indifference curve analysis, that involving the labor consumption

trade-off only includes income effects (not substitution effects) because labor only

generates income.

Describe how a speculator can improve social welfare when he correctly anticipates

that future demand will be higher than suppliers expect.

The amount of output produced by doupolists in a Cournot setting is greater than that

produced by a monopoly, but smaller than that which would be produced if the market

were perfectly competitive.

Pigovian analysis of externalities is wrong when transactions costs are zero, but it

remains valid when transactions costs prevent bargaining.

Odds are said to be fair if they reflect the true probabilities of the various states of the

world.

Whether or not people have identical tastes, free entry to a common property leads to a

suboptimal outcome.

How does the adverse selection problem faced by insurance companies differ from the

moral hazard problem they face? How might an insurance company deal with each

problem?

The slope of the budget line depends on the wage rate and the amount of human capital

the worker has accumulated.

By definition, someone who has an absolute advantage must also have a comparative

advantage.