A price ceiling will have NO effect if:

A) it is set above the equilibrium price.

B) the equilibrium price is above the price ceiling.

C) it is set below the equilibrium price.

D) it creates a shortage.

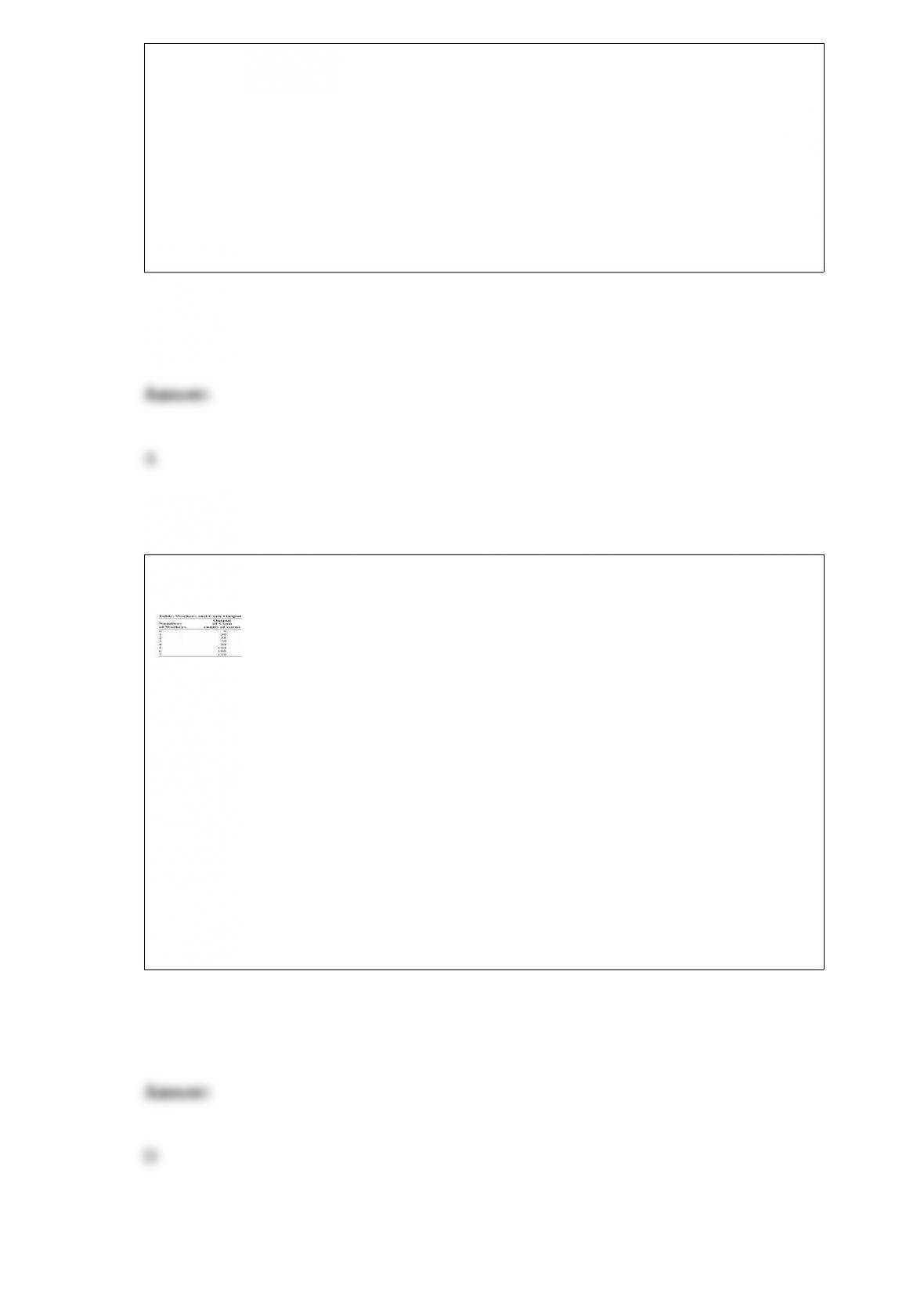

(Table: Workers and Corn Output) Look at the table Workers and Corn Output. Laura is

a price-taking farmer who produces corn. Assume the wage rate for workers is $130 and

the price per bushel of corn is $10. Suppose Laura is employing two workers. If she

adds the third worker, her profits will:

A) increase by $79.

B) decrease by $51.

C) decrease by $109.

D) increase by $80.

Figure: The Demand for Bricklayers

(Figure: The Demand for Bricklayers) Look at the figure The Demand for Bricklayers.

The equilibrium market wage for bricklayers is determined by:

A) the firm hiring the bricklayers.

B) demand and supply in the market for bricklayers.

C) the government.

D) where VMPLbricklayers = MPbricklayers × P of output.

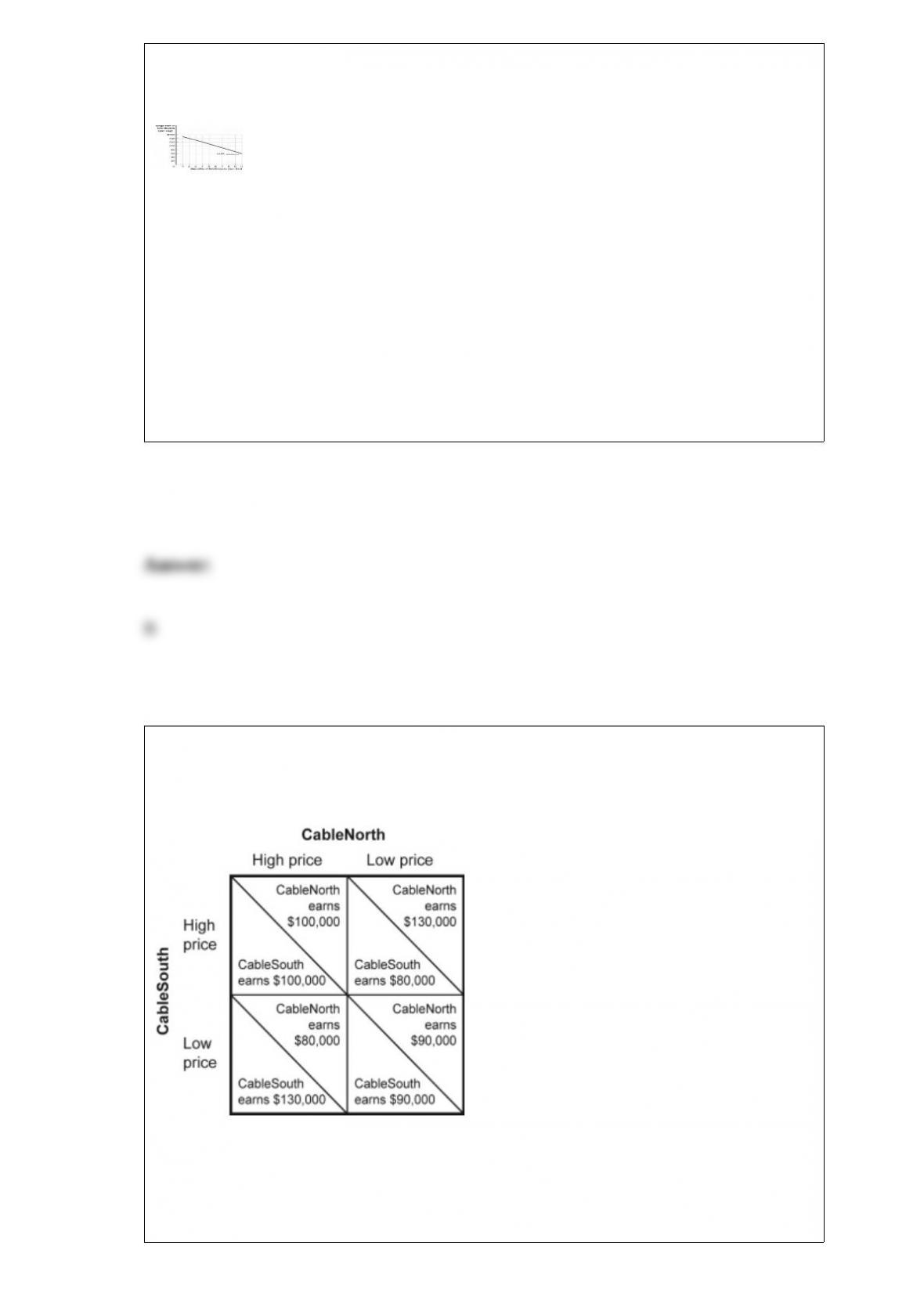

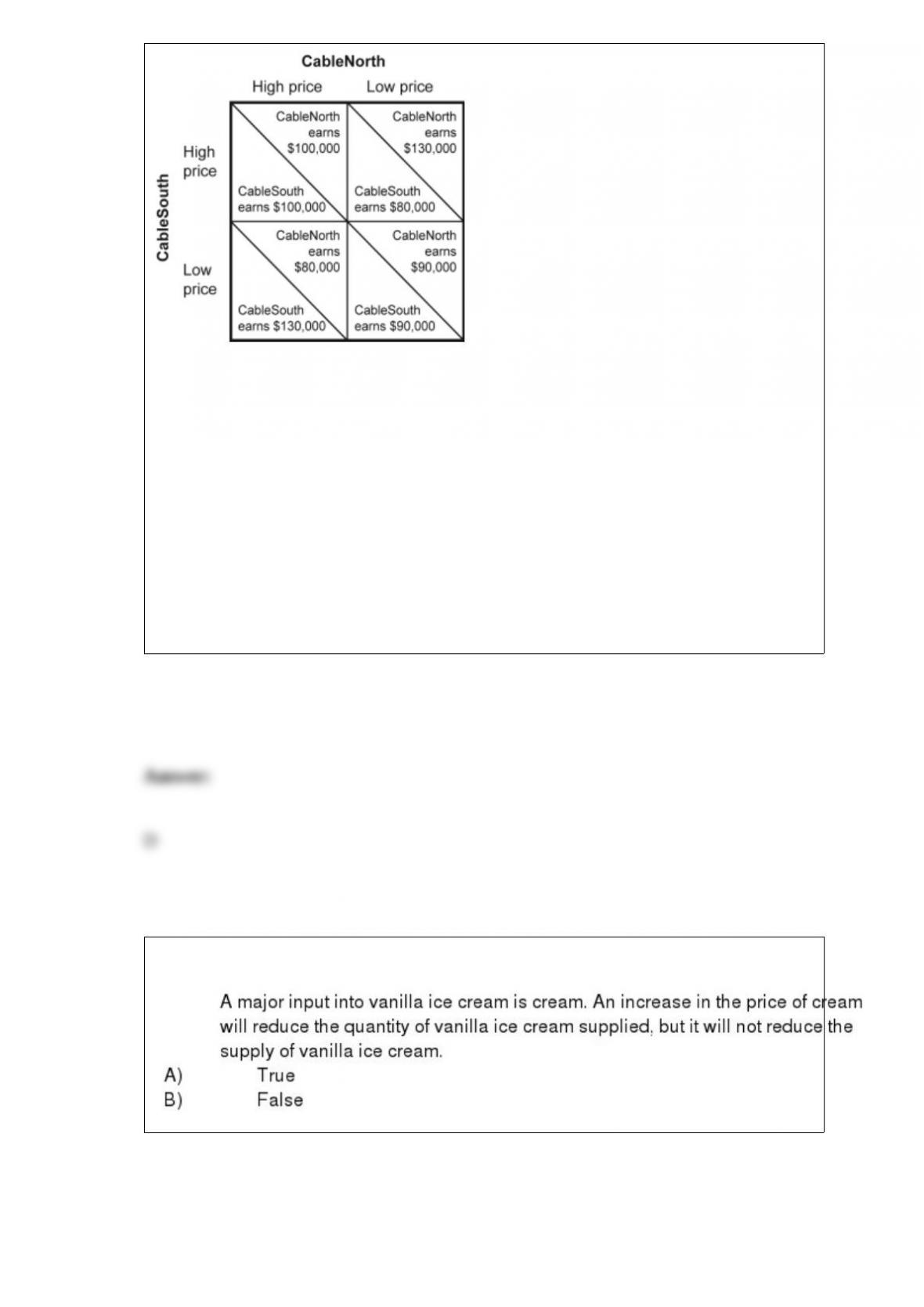

Figure: Pricing Strategy in Cable TV Market II

(Figure: Pricing Strategy in Cable TV Market II) Look at the figure Pricing Strategy in

Cable TV Market II. The Nash equilibrium in the cable TV market occurs when:

A) both firms set a low price and each earns $90,000 per month.

B) both firms set a high price and each earns $100,000 per month.

C) CableNorth sets a high price and earns $80,000 per month, and CableSouth sets a

low price and earns $130,000 per month.

D) CableNorth sets a low price and earns $130,000 per month, and CableSouth sets a

high price and earns $80,000 per month.

For Heidi, the marginal cost of producing one additional photograph equals the change

in _____ divided by the change in the _____ of photographs.

A) total cost; number

B) marginal cost; number

C) total cost; marginal product

D) average cost; number

In economics, the short run is:

A) less than 1 week.

B) less than 1 month.

C) enough time to vary output but not plant capacity.

D) enough time to change all inputs to production.

Bikul has just started a great job and plans to buy a fancy car worth $100,000. Bikul is

risk-averse in money matters, but he likes to drive fast, so the probability that he wrecks

the car (a total loss of $100,000) is 0.10. The probability that he has no accidents is

0.90. If an insurance company offers Bikul a fair insurance policy, the premium will be:

A) $10,000.

B) $90,000.

C) $80,000.

D) It is impossible to calculate a premium unless we know Bikul’s utility function.

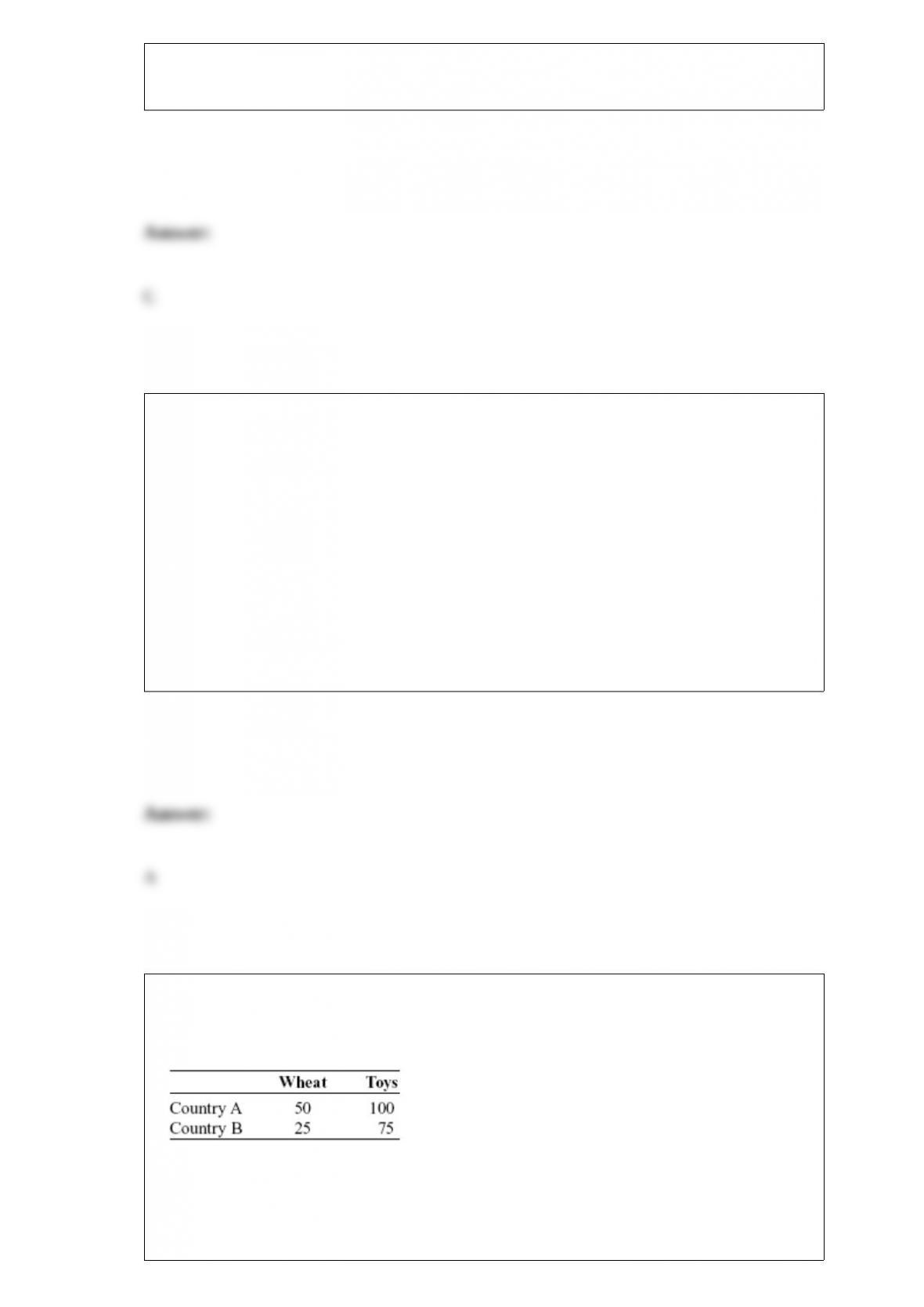

Scenario: The Production of Wheat and Toys

The table describes the production of two goods,

wheat and toys, in country A and country B. Each country has a linear production

possibility frontier with respect to its production of the two goods. The numbers in each

column represent the total number of units each country could produce if it used all of

its resources to produce the good.

(Scenario: The Production of Wheat and Toys) Look at the scenario Production of

Wheat and Toys. If each country specializes completely in the good for which it has the

comparative advantage, which combination represents a maximum possible amount of

total production of the two goods, given the specialization?

A) 50 wheat and 100 toys

B) 50 wheat and 75 toys

C) 25 wheat and 75 toys

D) 100 toys and 25 wheat

Programs associated with the welfare state are believed to cause deadweight loss, since

they:

A) affect the amount of disposable income that households below the poverty line have

to spend.

B) affect incentives to work and to save.

C) are supported by many political parties.

D) are based on the ability-to-pay principle.

A perfectly competitive firm will not produce any output in the short run and will shut

down if the price is:

A) greater than marginal cost.

B) less than marginal cost.

C) less than average variable cost.

D) greater than average variable cost and less than average total cost.

If a good has a marginal cost of production of zero and an inefficiently low level of

consumption, the good must be a(n):

A) private good.

B) public good.

C) common resource.

D) artificially scarce good.

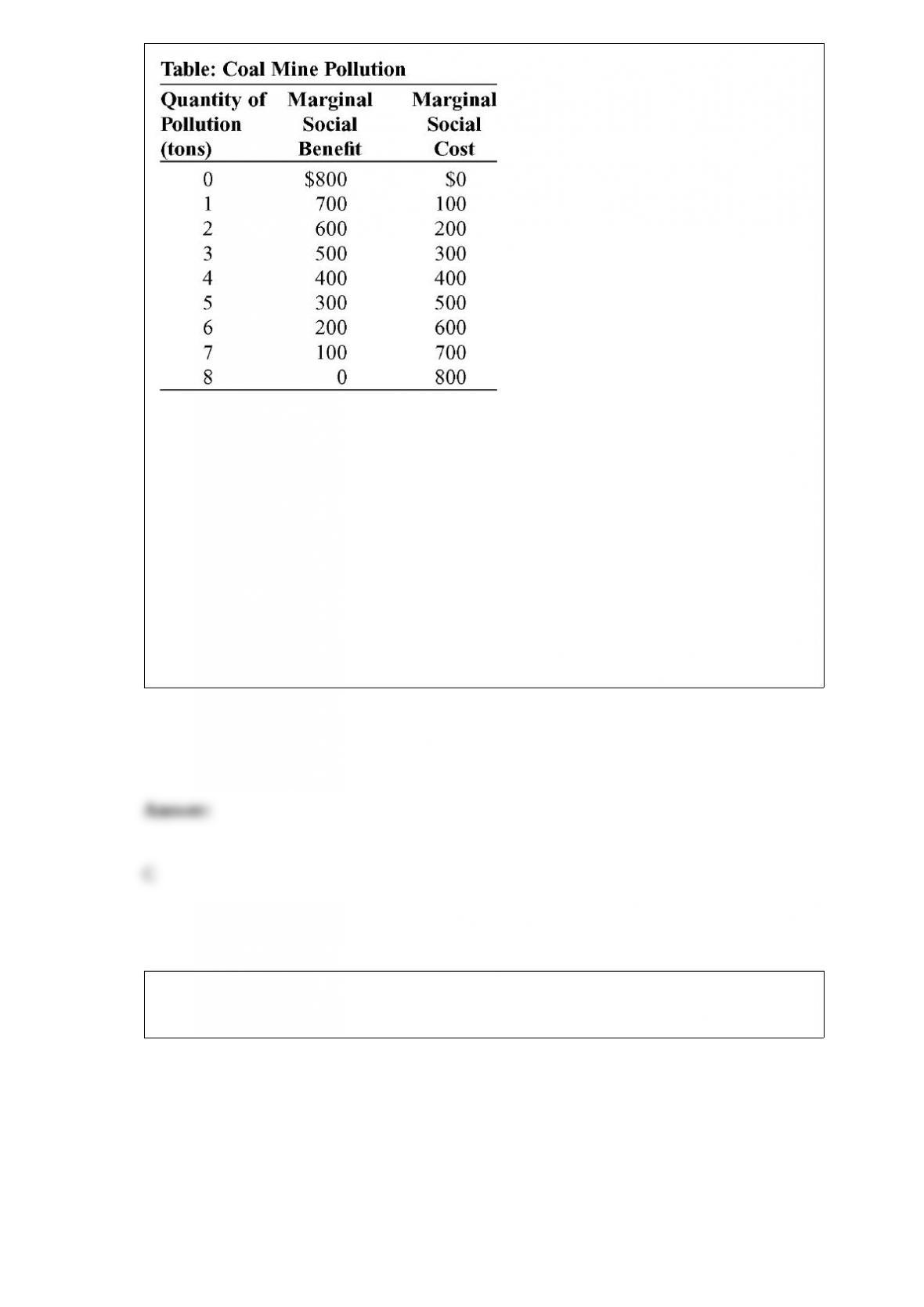

(Table: Coal Mine Pollution) The table Coal Mine Pollution shows the marginal social

benefit and cost of various amounts of pollution from a coal mine. Two tons of

pollution is:

A) too much.

B) the efficient amount.

C) not enough.

D) the socially optimum amount.

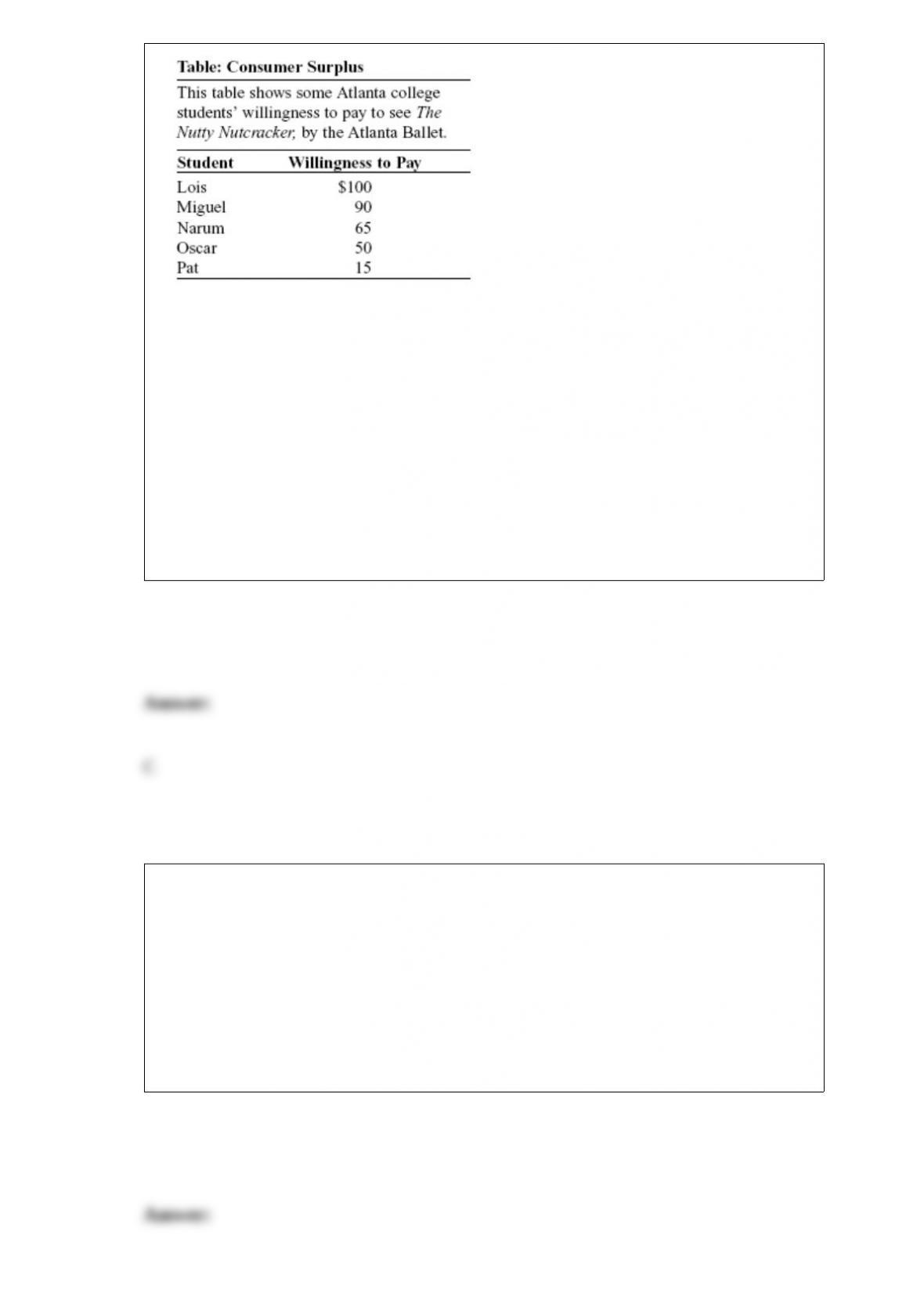

(Table: Consumer Surplus) Look at the table Consumer Surplus. Assume that each

student wants to buy one ticket. If the price of a ticket to see The Nutty Nutcracker is

$75, Miguel’s consumer surplus is:

A) $60.

B) $50.

C) $15.

D) $240.

Volunteer fire departments are good examples of the _____ provision of _____.

A) private; private goods

B) public; common resources

C) private; public goods

D) public; artificially scarce goods

The competitive model assumes all of the following EXCEPT:

A) a large number of buyers.

B) easy entry to and exit from the market.

C) standardized product.

D) patents and copyrights that serve as barriers to entry into the industry.

The ability-to-pay principle regarding taxes suggests that:

A) the efficiency of a tax is the key feature in designing it.

B) those who can afford it should bear the greater burden of the tax.

C) those who benefit most from the tax should bear the greater burden of the tax.

D) higher-income individuals should pay the same amount as lower-income individuals.

With one input fixed, a firm will find that as it attempts to produce more, the total

product curve increases at a decreasing rate and its marginal product curve is:

A) downward-sloping.

B) upward-sloping.

C) constant and horizontal at the marginal product axis.

D) constant and vertical at the quantity axis.

One framework used to analyze strategic choices is:

A) the tacit supply curve model.

B) game theory.

C) perfect competition.

D) risk assessment.

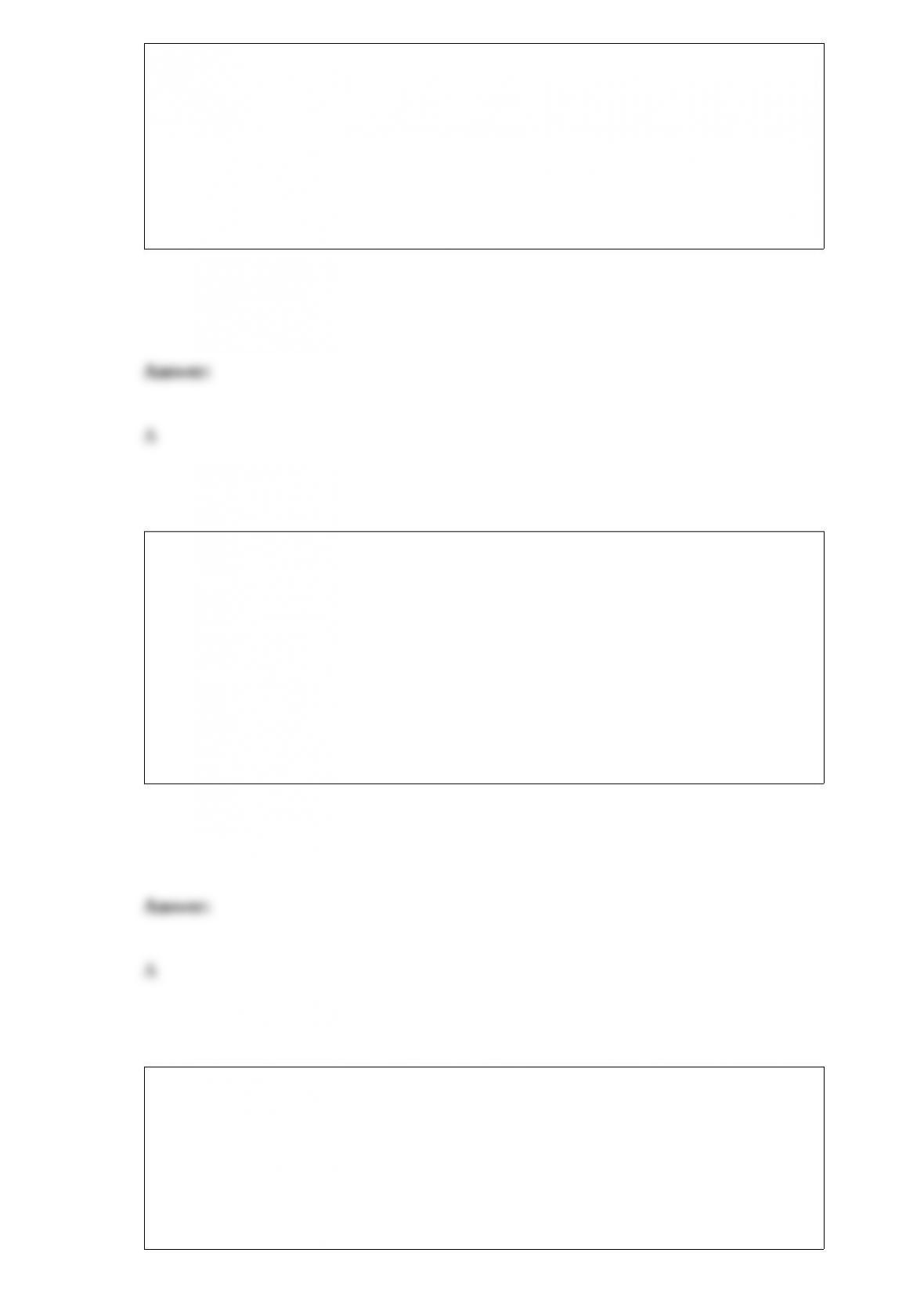

Figure: Pricing Strategy in Cable TV Market II

(Figure: Pricing Strategy in Cable TV Market II) Look at the figure Pricing Strategy in

Cable TV Market II. If the two firms in the cable TV market collude:

A) CableNorth will set a high price and earn $80,000 per month, and CableSouth will

set a low price and earn $130,000 per month.

B) CableNorth will set a low price and earn $130,000 per month, and CableSouth will

set a high price and earn $80,000 per month.

C) both firms will set a low price and each will earn $90,000 per month.

D) both firms will set a high price and each will earn $100,000 per month.

A quota is:

A) a lower limit on quantity.

B) an upper limit on quantity.

C) a maximum price.

D) a minimum price.

Which of the following is TRUE of firms in both perfect competition and monopolistic

competition?

A) The long-run price is equal to marginal revenue, marginal cost, and average total

cost.

B) Long-run economic profits are equal to zero.

C) The long-run level of output is at the point where average total cost is minimized.

D) Price is equal to marginal cost, ensuring that the efficient level of output is produced.

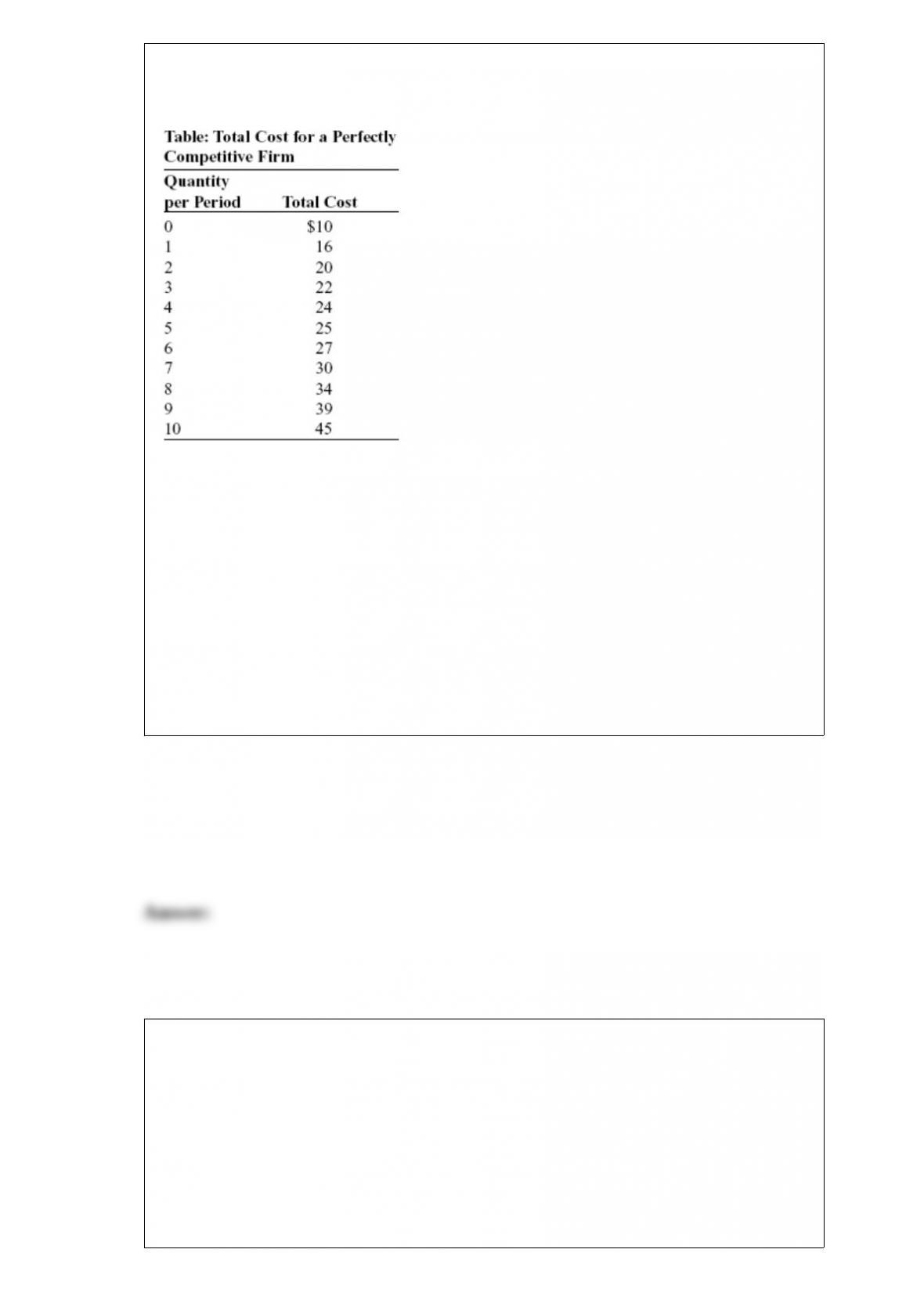

(Table: Total Cost for a Perfectly Competitive Firm) Look at the table Total Cost for a

Perfectly Competitive Firm. If the market price is $4.50, profit at the profit-maximizing

quantity of output is:

A) $2.00.

B) $4.50.

C) $5.00.

D) $34.00.

_____ occurs when the only two firms in an industry agree to fix the price at a given

level.

A) Collusion

B) The ability to satisfy demand

C) Price extortion

D) Price leadership

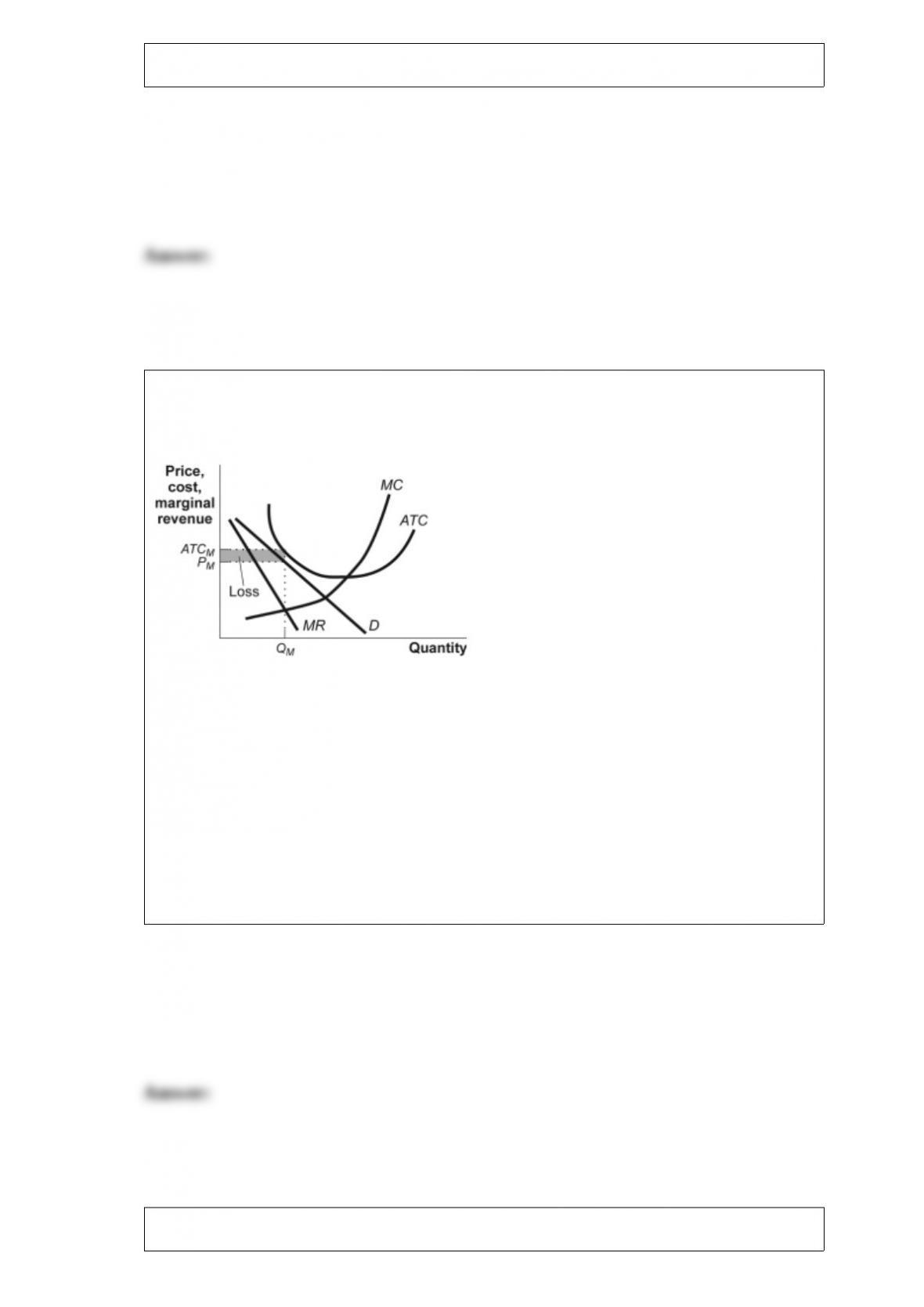

Figure: Monopolistic Competition VI

(Figure: Monopolistic Competition VI) In the figure Monopolistic Competition VI, in

the long run firms will:

A) enter this market until all firms earn a zero economic profit.

B) exit this market until all remaining firms earn a zero economic profit.

C) enter this market, leading to excess profit for all of the firms.

D) exit this market, leading to excess profit for all of the remaining firms.

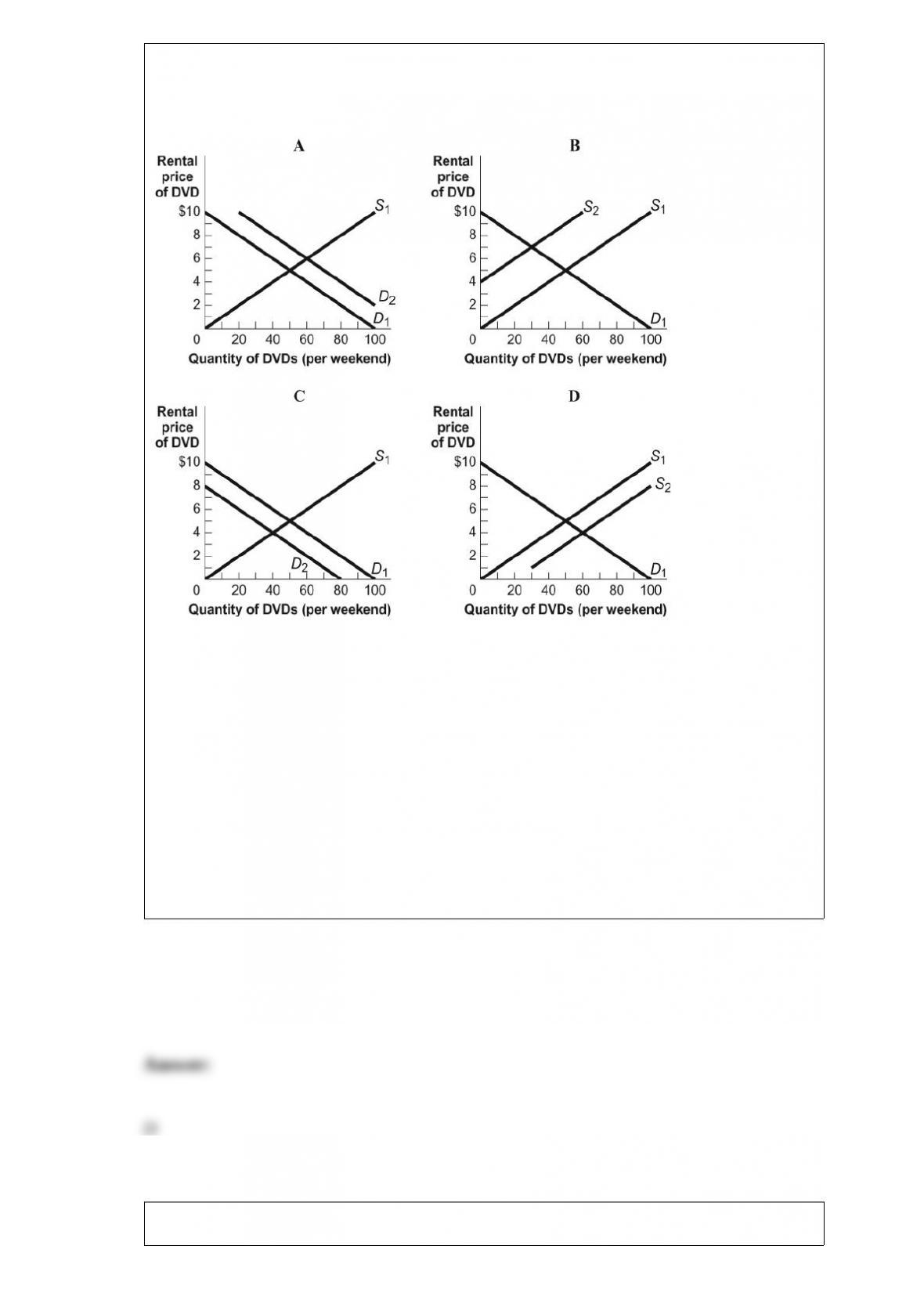

Figure: Four Markets for DVDs

(Figure: Four Markets for DVDs) Look at the figure Four Markets for DVDs. Which of

the graphs illustrates what may happen in the market for DVDs if D1 or S1 is the

original curve and D2 or S2 is the new curve and if the cost of producing DVDs falls?

A) A

B) B

C) C

D) D

A firm that has lower costs per unit as it increases production in the long run has:

A) increasing returns to scale.

B) decreasing returns to scale.

C) increasing opportunity costs.

D) scale reduction.

While eating pizza, you discover that the marginal benefit of eating one more slice is

greater than the marginal cost of that slice. You conclude that:

A) you will be better off if you eat one more slice.

B) you will be no better off and no worse off if you eat one more slice.

C) you will be worse off if you eat one more slice.

D) the total cost of eating the pizza will be more than the total benefit of eating the

pizza.

The opportunity cost of production:

A) is the price of a good.

B) is what you give up to produce the good.

C) decreases as production increases.

D) is what you gain by producing the good.

A formal agreement to limit production and raise prices leads to:

A) a cartel.

B) perfect competition.

C) monopolistic competition.

D) oligopoly.

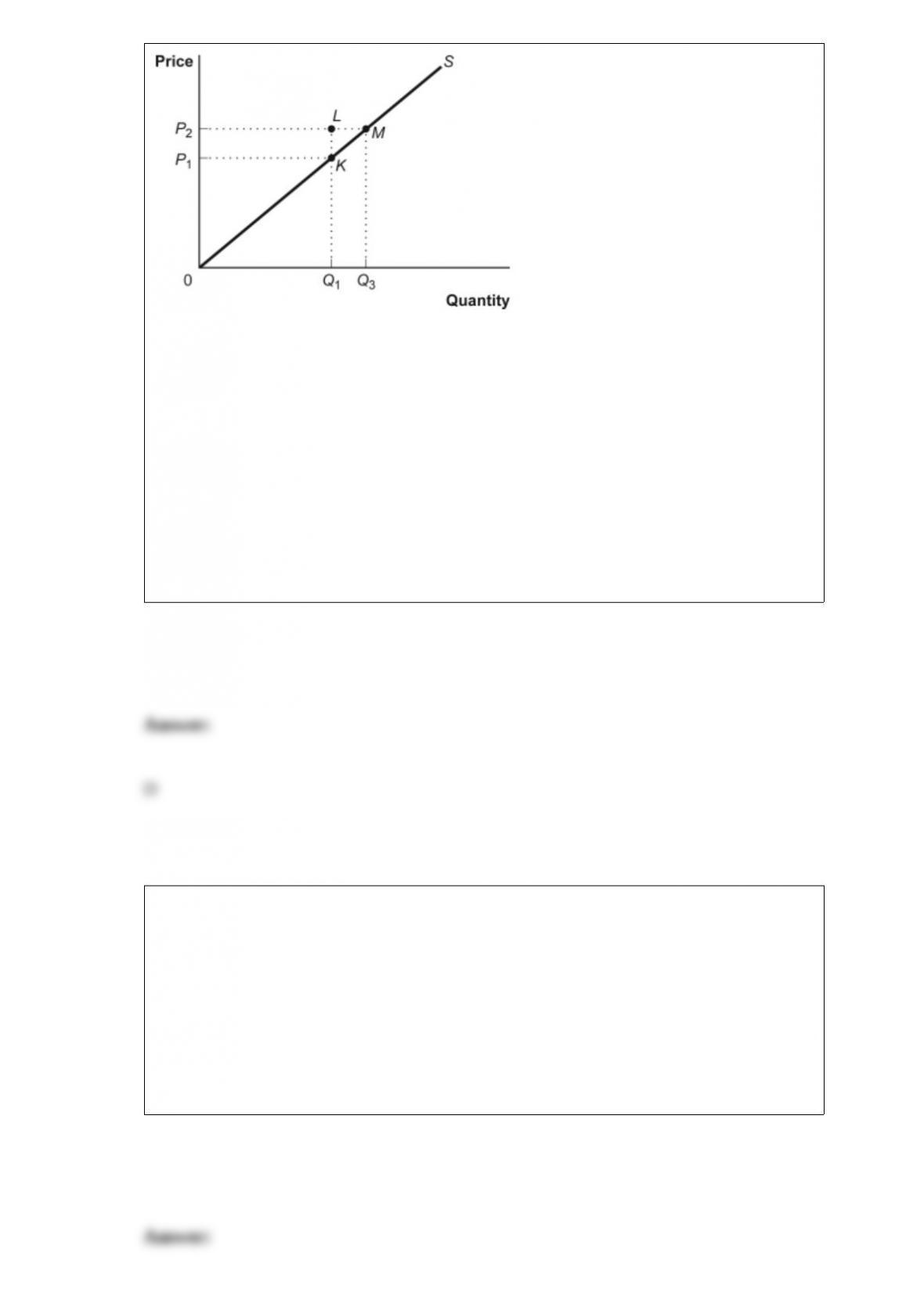

Figure: Producer Surplus II

(Figure: Producer Surplus II) Look at the figure Producer Surplus II. If the price falls

from P2 to P1, producer surplus decreases by the area:

A) LMK.

B) P1K0.

C) P2M0.

D) P2P1KM.

Which of the following would result in a movement along the demand curve?

A) a change in preferences

B) an increase in the number of buyers

C) an increase in the number of suppliers

D) a decrease in income

Some products, like tobacco, are taxed. Why would the government interfere in a

market that if left untaxed would probably move to equilibrium on its own?

Suppose two gas stations operate at the same busy intersection. You notice that the

posted prices are almost always the same. Assuming that these firms are engaged in

tacit price collusion, can we automatically conclude that there is no competition for

customers between the two stations?

Most college-bound high school seniors apply for admission to several colleges of

varying reputations and admission standards. Explain how this behavior is similar to

diversification of assets discussed in the chapter.

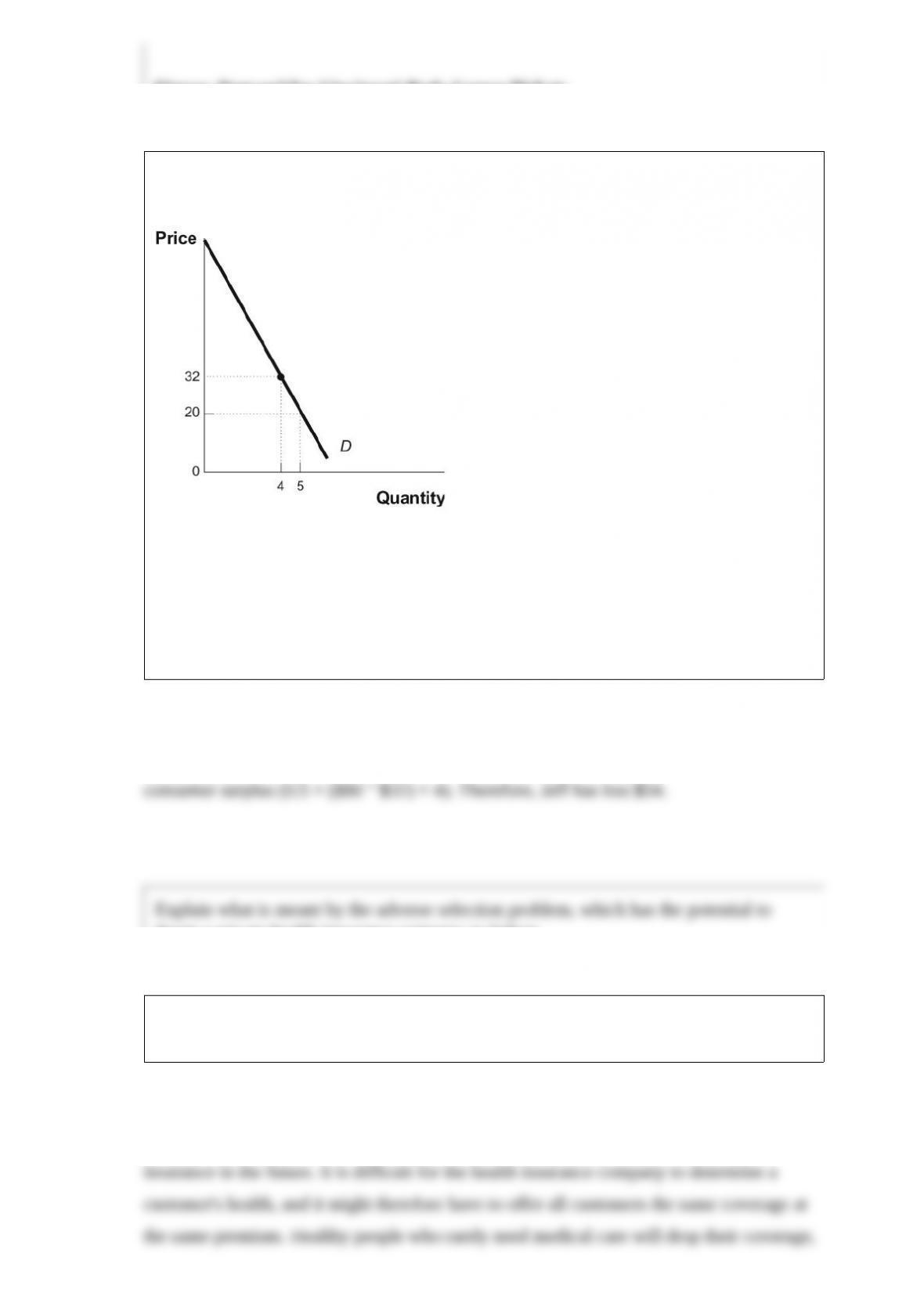

Figure: Demand for Cincinnati Reds Games Tickets

(Figure: Demand for Cincinnati Reds Games Tickets) The figure Demand for

Cincinnati Red Games Tickets represents Jeff’s annual demand for tickets to Cincinnati

Reds baseball games. Suppose the Reds required all fans to purchase a $12 parking pass

for each game. This effectively raises the price of a ticket to $32, and Jeff will decrease

his quantity demanded for Reds baseball by one ticket this year. How much consumer

surplus has Jeff lost?

Explain what is meant by the adverse selection problem, which has the potential to

doom a private health insurance company to failure.

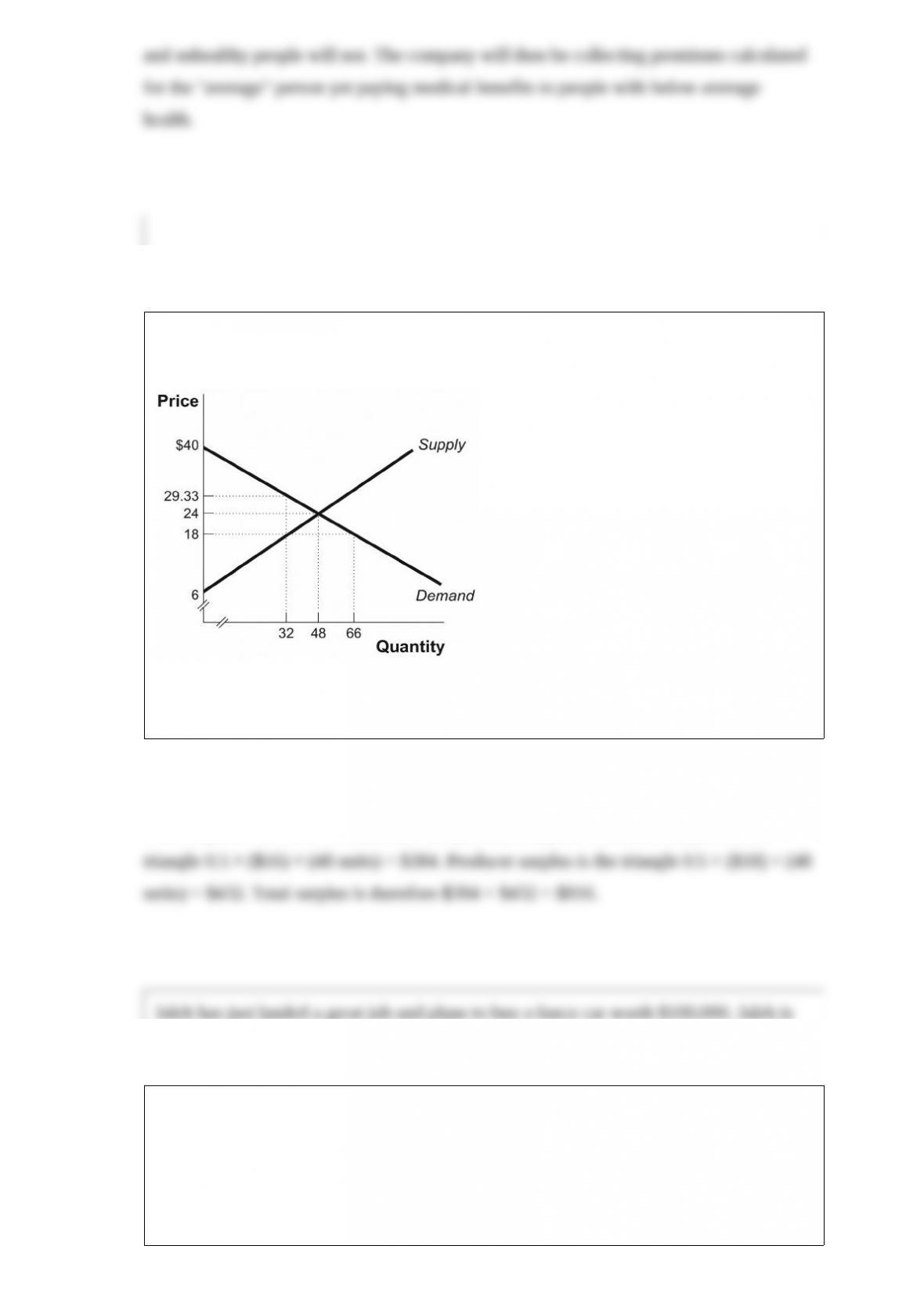

Figure: The Market for Books

(Figure: The Market for Books) Look at the figure The Market for Books. At the

equilibrium price of $24, find the total surplus in the market for books.

Jaleh has just landed a great job and plans to buy a fancy car worth $100,000. Jaleh is

otherwise risk-averse, but she likes to drive fast, so the probability that she wrecks the

car (a total loss of $100,000) is 0.1. The probability that she has no accidents is 0.9. If

an insurance company were to offer Jaleh a fair insurance policy that completely

replaced her car, how much would she pay? What is the most she would pay for an

insurance policy that would completely replace her car if she totaled it?