Assume there are two people in a society. Person A is willing to pay $70 to have one

unit of a public good produced and Person B is willing to pay $80 to have one unit of a

public good produced and $70 to have two units produced. As a result, for ________

unit(s) of this public good society would be willing to pay a price of ________.

A) 1; $150

B) 3; $100

C) 1; $100

D) 5; $80

For a monopolist, if total revenue increases as output increases, then marginal revenue

is

A) greater than the price.

B) zero.

C) positive.

D) negative.

ATC is

A) TC/q.

B) q/TC.

C) AFC – AVC.

D) ΔTC – Δq.

If the unemployment rate decreases from 9% to 6%, the economy will

A) move closer to a point on the ppf.

B) move away from the ppf toward the origin.

C) remain on the ppf.

D) remain on the origin.

During 2013, Yolanda’s assets equal $400,000 and her liabilities were $550,000.

Yolanda’s net worth is

A) -$150,000.

B) $150,000.

C) $475,000.

D) $950,000.

Firms will ________ a monopolistically competitive market until ________ are

eliminated.

A) exit; losses

B) enter; losses

C) exit; short-run profits

D) exit; long-run profits

If ________, a firm would operate in the short run and exit the industry in the long run.

A) TR > TVC and TR > TC

B) TR > TVC but TR < TC

C) TR < TC and TR < TVC

D) TR = TVC but TR > TC

In the short run a firm using variable labor and fixed capital inputs achieves the

efficient (lowest cost) level of output at the minimum point on its ________ cost curve.

A) average total

B) total variable

C) average fixed

D) marginal

The top 20% of families in the income distribution receive most of their income from

A) wages and salaries.

B) property income.

C) transfer income.

D) profit income.

Price will increase and output will decrease once government makes a firm

A) internalize a negative externality.

B) externalize a negative externality.

C) internalize a positive externality.

D) externalize a positive externality.

The whole class of goods that will be underproduced or not produced at all in a

completely unregulated market economy are referred to as

A) free goods.

B) Pareto goods.

C) private goods.

D) public goods.

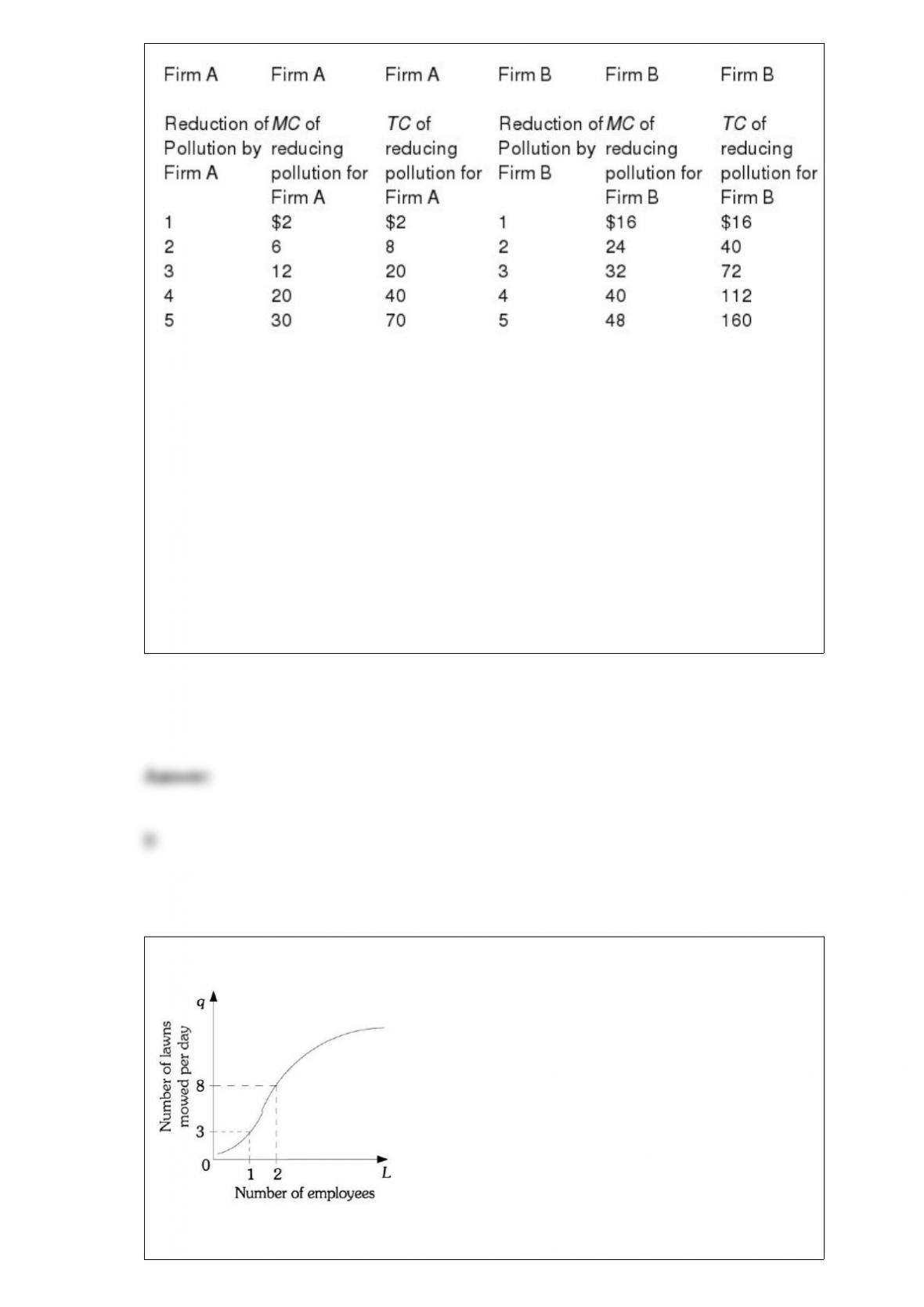

Table 16.4 shows the situation facing two firms, both of which are polluting. Assume

that each firm emits 5 units of pollution.

Table 16.4

Refer to Table 16.4. Suppose the government wants to reduce the total amount of

pollution from the current level of 10 to 4. To do this, the government caps each firm’s

emissions at 2 units and issues 2 permits to each firm. If firms are allowed to trade

permits, how many permits will be traded between the two firms?

A) A will buy two permits from B.

B) B will buy two permits from A.

C) A will buy one permit from B.

D) B will buy one permit from A.

Figure 7.2

Refer to Figure 7.2. The marginal product of the second worker is ________ lawns

mowed.

A) 3

B) 5

C) 8

D) 11

The tax ________ is the measure or value upon which a government levies a tax.

A) base

B) rate

C) structure

D) incidence

Upon graduating with an accounting degree, you open your own accounting firm of

which you are the sole employee. To start the firm you passed on a job offer with a

large accounting firm that offered you a salary of $60,000 annually. Last year you

earned a total revenue of $100,000. Rent and supplies last year were $50,000.

Your annual economic profit is

A) -$10,000.

B) $40,000.

C) $50,000.

D) $100,000.

If a firm’s demand curve is perfectly elastic, then at the profit maximizing level of

output

A) P = MR = MC.

B) P > MR > MC.

C) P < MR < MC.

D) P > 0 and MR = 0.

Which of the following will NOT cause a shift in the demand curve for DVDs?

A) a change in income

B) a change in wealth

C) a change in the price of Blu-ray discs

D) a change in the price of DVDs

The amount of exercise that one gets is an important factor in the determination of his

general state of health. This is best described as

A) a positive statement.

B) an example of the fallacy of composition.

C) a normative statement.

D) an example of marginalism.

Assume leisure is an inferior good instead of a normal good. The income effect of a

wage decrease will lead to a ________ demand for leisure and a ________ labor supply.

A) higher; higher

B) higher; lower

C) lower; higher

D) lower; lower

In the long run, a firm

A) can shut down, but it cannot exit the industry.

B) has no fixed factors of production.

C) can vary all inputs, but it cannot change the mix of inputs it uses.

D) must make positive economic profits.

Which of the following is false?

A) An import quota does not generate government revenue.

B) Tariffs on imports generate government revenue as long as the domestic price is

larger than the world price plus the tariff.

C) Tariffs on imports do not generate government revenue if the domestic price is larger

than the world price plus the tariff.

D) all of the above

If labor is a variable input in production, the law of diminishing marginal returns

implies that in the short run

A) labor’s marginal product is constant.

B) labor’s marginal product decreases after a certain point.

C) total product is negative.

D) total product is negative after a certain point has been reached.

If we know average total cost and the amount of output, then we can always calculate

total cost by

A) adding average total cost and the amount of output.

B) subtracting the amount of output from average total cost.

C) multiplying average total cost by the amount of output.

D) dividing average total cost by the amount of output.

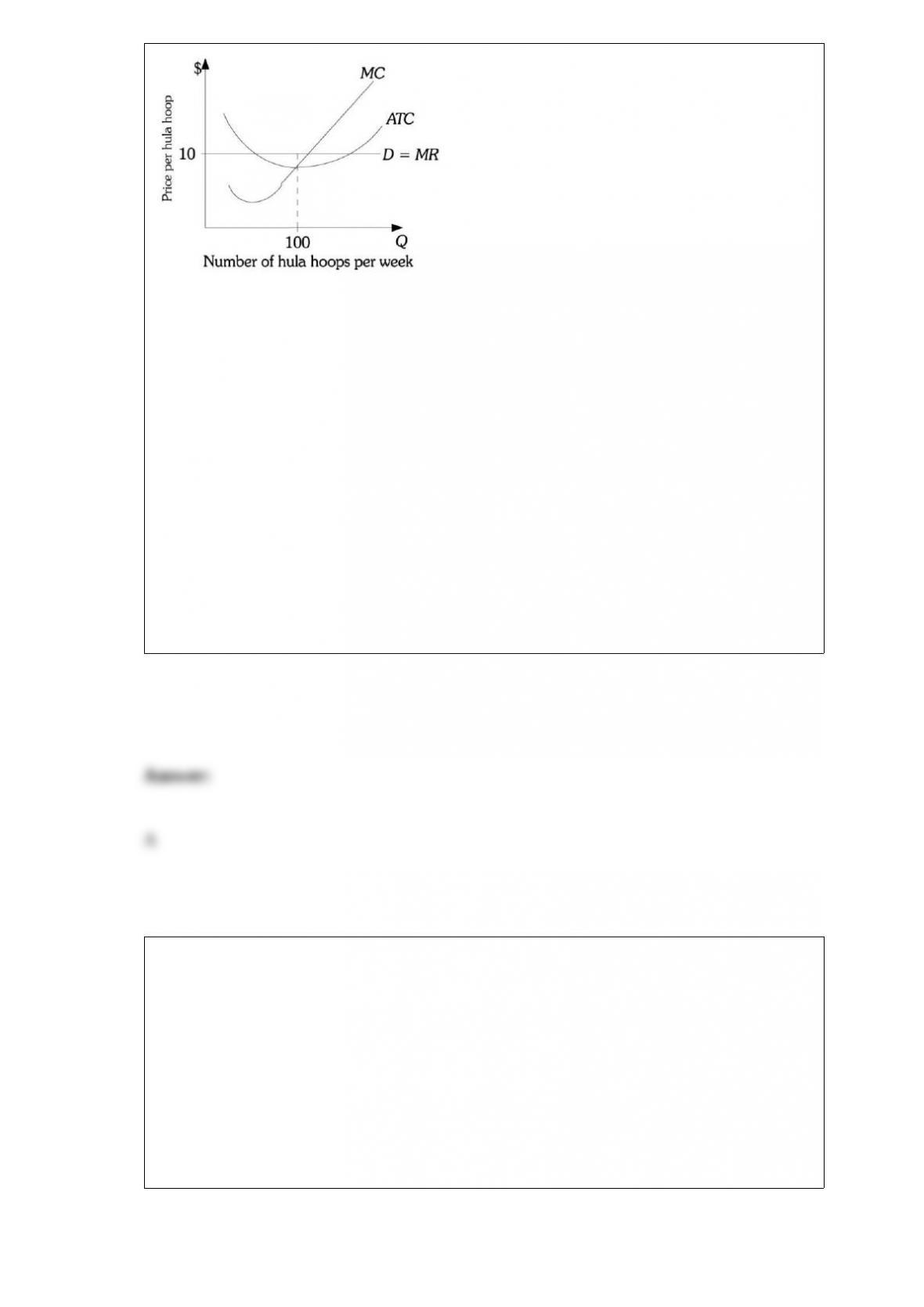

Figure 4

Refer to Figure 12.4. Hula hoops are produced in a perfectly competitive market. This

hula hoop firm is currently producing and selling 100 hula hoops per week. Which of

the following is true?

A) Society would be better off if more hula hoops were produced because at the current

level of production price is greater than marginal cost.

B) Society would be better off if fewer hula hoops were produced because if this firm

reduced its production, its profits would increase.

C) Hula hoop production is at the efficient level because ATC is minimized.

D) Fewer resources should be devoted to hula hoop production because ATC is less than

price.

You agree to lend a friend $15,000 for a year at an annual interest rate of 20%. At the

end of the year your friend must pay you ________ in interest.

A) $133

B) $750

C) $1,500

D) $3,000

Assume you earn $75,000 a year and your favorite entertainment magazine costs you

$25 a year. Your demand for the entertainment magazine is likely to be

A) elastic.

B) inelastic.

C) perfectly elastic.

D) perfectly inelastic.

In the United States most people’s wealth comes from

A) inheritance.

B) transfer payments.

C) saving.

D) profits.

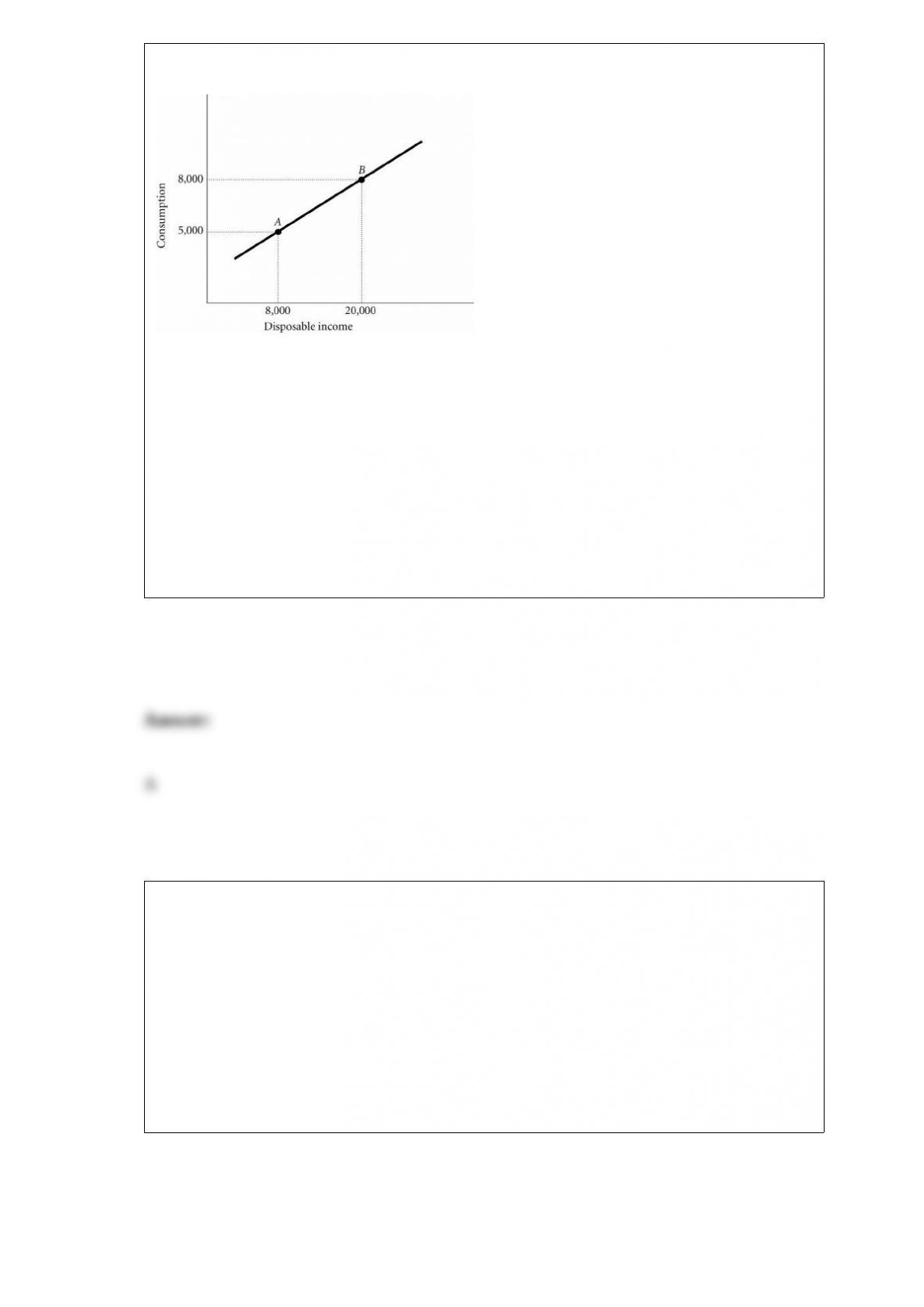

Figure 1.2

Refer to Figure 1.2. The slope of the line between Points A and B is

A) 25.

B)4

C) -0.25.

D) -4.

The oligopolistic model in which firms produce exactly the same results as would exist

if a monopolist controlled the entire industry is called the ________ model.

A) Cournot

B) price leadership

C) maximin strategy

D) collusion

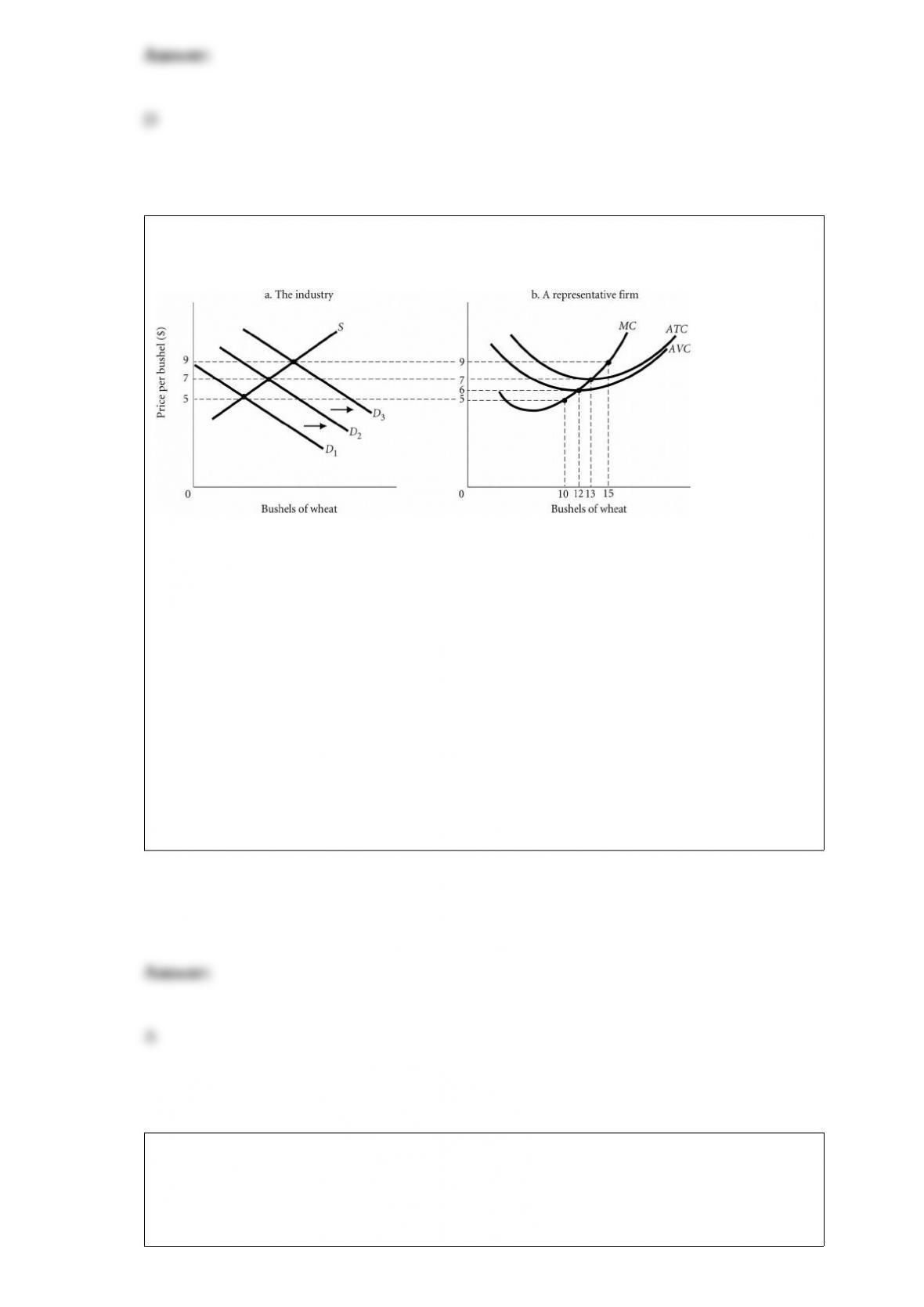

Figure 9.7

Refer to Figure 9.7. Suppose demand for wheat is initially D2. If the price of rice (a

substitute for wheat) rises, then demand for wheat will shift to ________. This will

________ the equilibrium price of wheat, and individual profit maximizing firms will

produce ________ bushels of wheat.

A) D3; increase; 15

B) D1; increase; 13

C) D3; decrease; 10

D) D1; decrease; 0

You lend a friend $20,000 for a year at an annual interest rate of 5%. At the end of the

year your friend must pay you ________ in interest.

A) $133

B) $750

C) $1,000

D) $1,900

Toby tells you that he prefers hamburgers to hot dogs, hot dogs to tacos, and tacos to

hamburgers. This violates what assumption made when analyzing consumer

preferences?

A) that more is better

B) that there is a diminishing marginal rate of substitution

C) that consumers are rational

D) that consumers are able to choose among all the combinations of goods and services

available

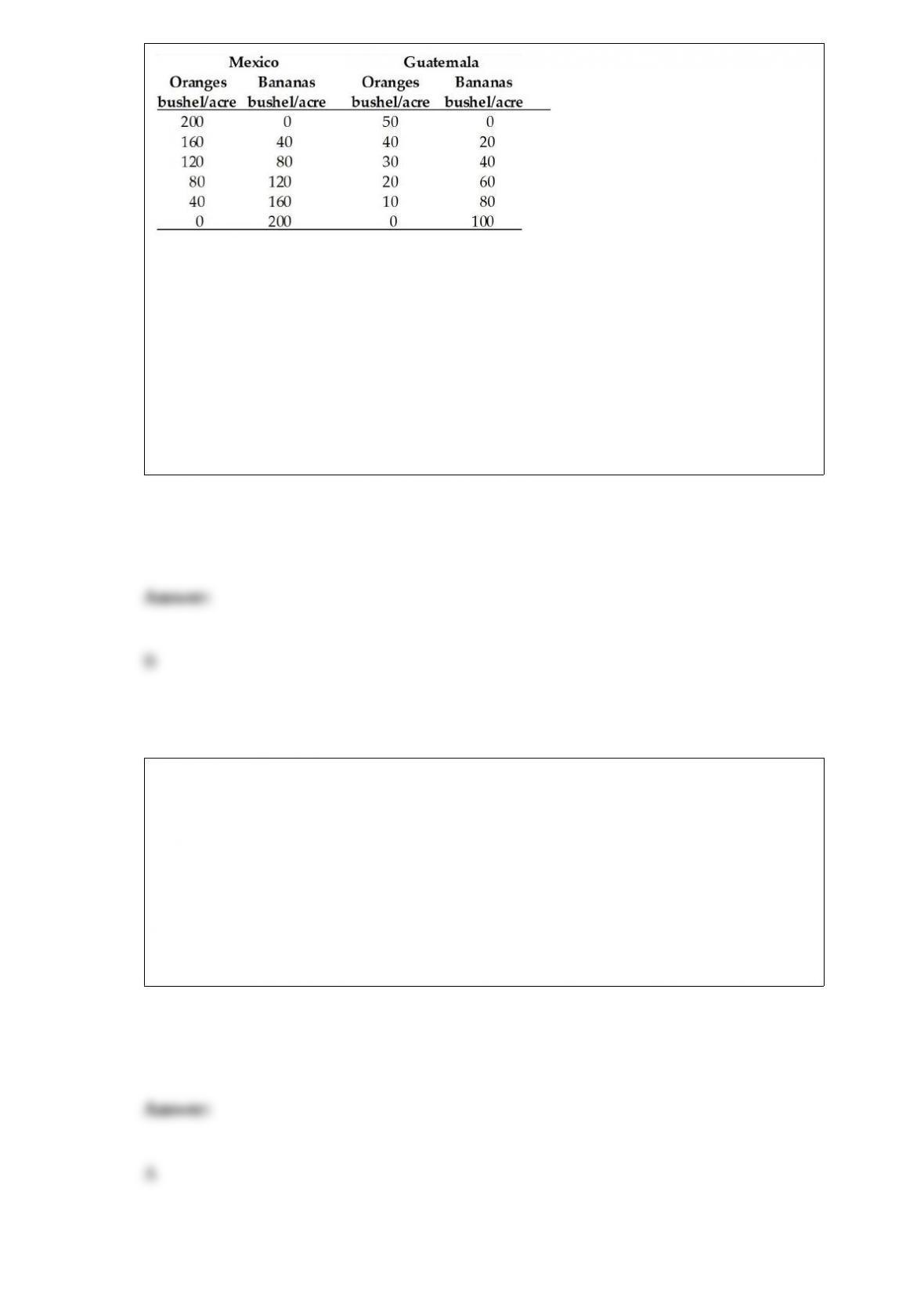

Table 20.1

Refer to Table 20.1. Guatemala has

A) a comparative advantage but not an absolute advantage in orange production.

B) a comparative advantage but not an absolute advantage in banana production.

C) an absolute advantage and a comparative advantage in banana production.

D) an absolute advantage and a comparative advantage in orange production.

If the marginal cost curve is above the average variable cost curve, then

A) average variable cost is increasing.

B) average variable cost is decreasing.

C) average variable cost is constant.

D) marginal cost is decreasing.

Hector has $1,000 a month to spend on clothing and food. The price of clothing is $50

and the price of food is $20. Hector spends his entire income when he purchases

________ units of clothing and ________ units of food.

A) 10; 10

B) 25; 5

C) 12; 20

D) 16; 8