The sticky-wage theory of the short-run aggregate supply curve says that when the price

level is lower than expected,

a. production is more profitable and employment rises.

b. production is more profitable and employment falls.

c. production is less profitable and employment rises.

d. production is less profitable and employment falls.

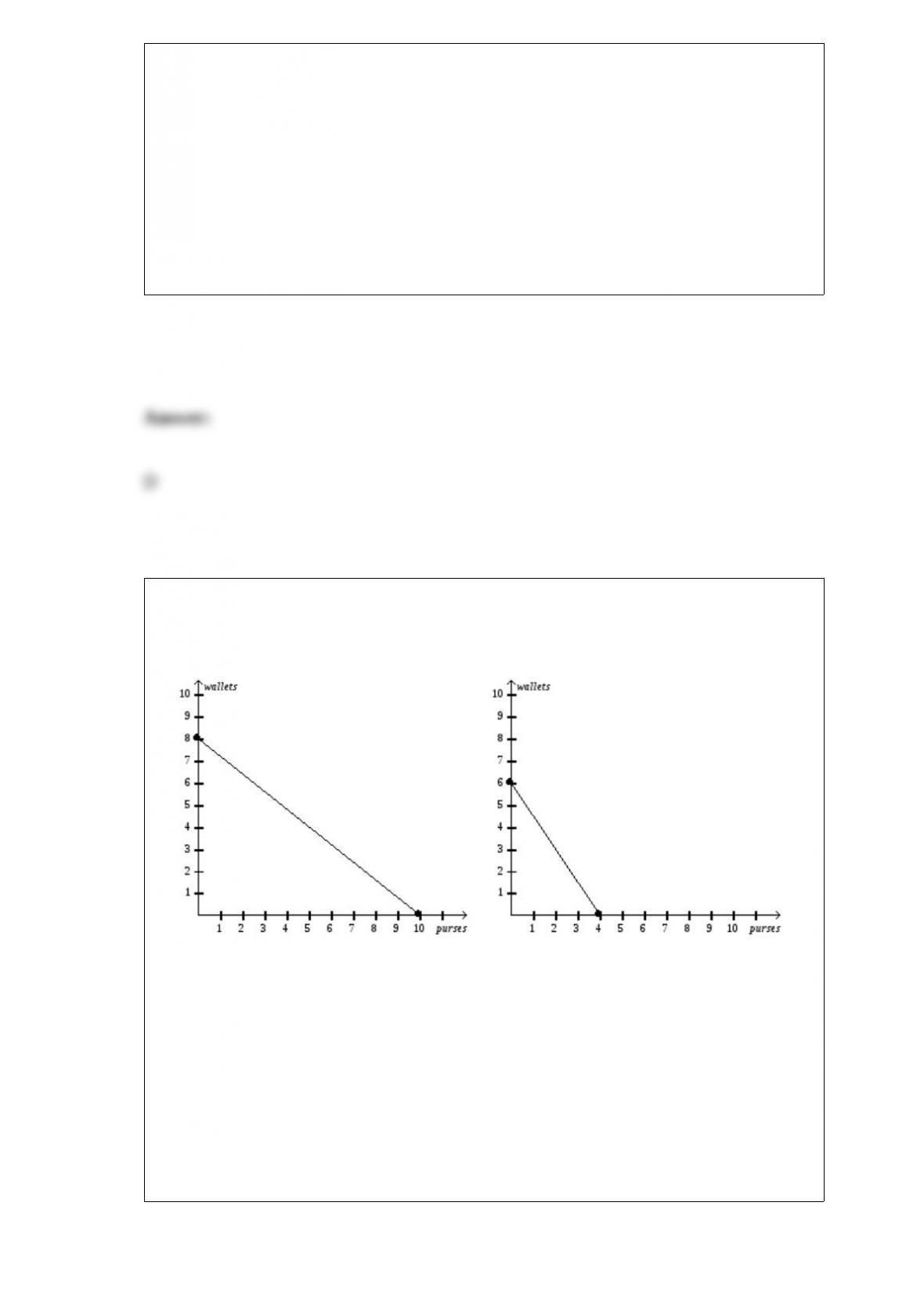

Figure 3-5

Hosne’s Production Possibilities Frontier Merve’s Production Possibilities Frontier

Refer to Figure 3-5. At which of the following prices would both Hosne and Merve

gain from trade with each other?

a. 5 wallets for 1.25 purses

b. 5 wallets for 2.5 purses

c. 5 wallets for 3.75 purses

d. Hosne and Merve could not both gain from trade with each other at any price.

If saving is greater than domestic investment, then

a. there is a trade deficit and Y > C + I + G.

b. there is a trade deficit and Y < C + I + G.

c. there is a trade surplus and Y > C + I + G.

d. there is a trade surplus and Y < C + I + G.

Which of the following is included in the investment component of GDP?

a. spending to build new houses

b. spending to build new factories

c. spending on business equipment such as welding equipment

d. All of the above are included in the investment component of GDP.

If the government passes a law requiring sellers of mopeds to send $200 to the

government for every moped they sell, then

a. the supply curve for mopeds shifts downward by $200.

b. sellers of mopeds receive $200 less per mopeds than they were receiving before the

tax.

c. buyers of mopeds are unaffected by the tax.

d. None of the above is correct.

For the following questions, use the diagram below:

Figure 21-7.

Refer to Figure 21-7. The aggregate-demand curve could shift from AD1 to AD2 as a

result of

a. an increase in government purchases.

b. a decrease in stock prices.

c. consumers and firms becoming more optimistic about the future.

d. an increase in the price level.

If a country’s budget deficit decreases, then the exchange rate

a. rises, which raises net exports.

b. rises, which reduces net exports.

c. falls, which raises net exports.

d. falls, which reduces net exports.

Figure 4-21

Refer to Figure 4-21. Which of the following movements would illustrate the effect in

the market for swimming lessons of an increase in the incomes of parents with

school-aged children?

a. Point A to Point B

b. Point C to Point B

c. Point C to Point D

d. Point A to Point D

The Patersons bought a home that was newly constructed in 2007 for $275,000. They

sold the home in 2009 for $205,000. Which of the following statements is correct

regarding the sale of the house?

a. The 2009 sale increased 2009 GDP by $205,000 and had no effect on 2007 GDP.

b. The 2009 sale reduced 2009 GDP by $70,000 and had no effect on 2007 GDP.

c. The 2009 sale increased 2009 GDP by $205,000; and caused 2007 GDP to be revised

downward by $70,000.

d. The 2009 sale affected neither 2007 GDP nor 2009 GDP.

Financial Crisis

Suppose that banks are less able to raise funds and so lend less. Consequently, because

people and households are less able to borrow, they spend less at any given price level

than they would otherwise. The crisis is persistent so lending should remain depressed

for some time.

Refer to Financial Crisis. If nominal wages are sticky, which of the following helps

explains the change in output?

a. real wages fall, so firms choose to produce less

b. real wages fall, so firms choose to produce more

c. real wages rise, so firms choose to produce less

d. real wages rise, so firms choose to produce more

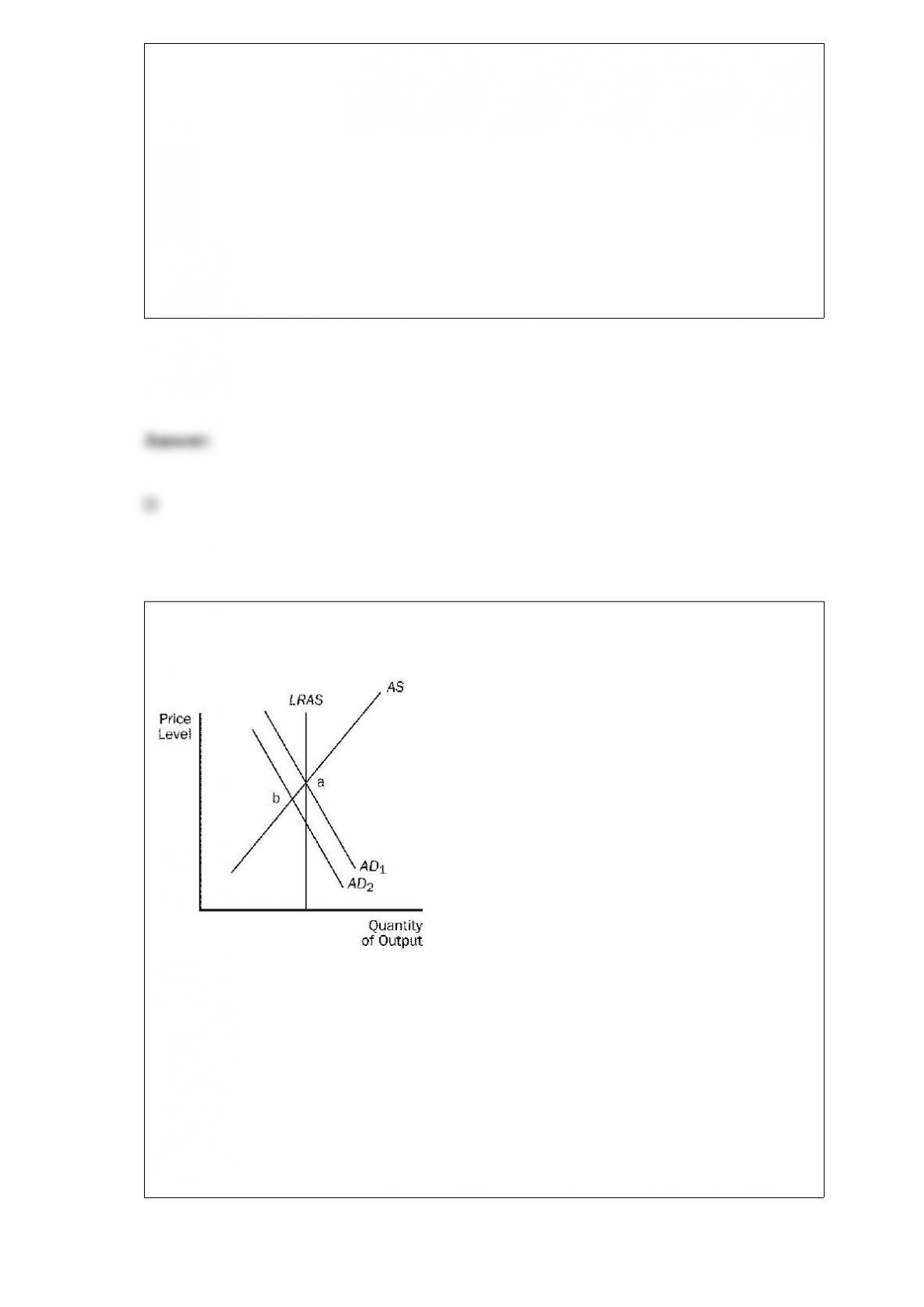

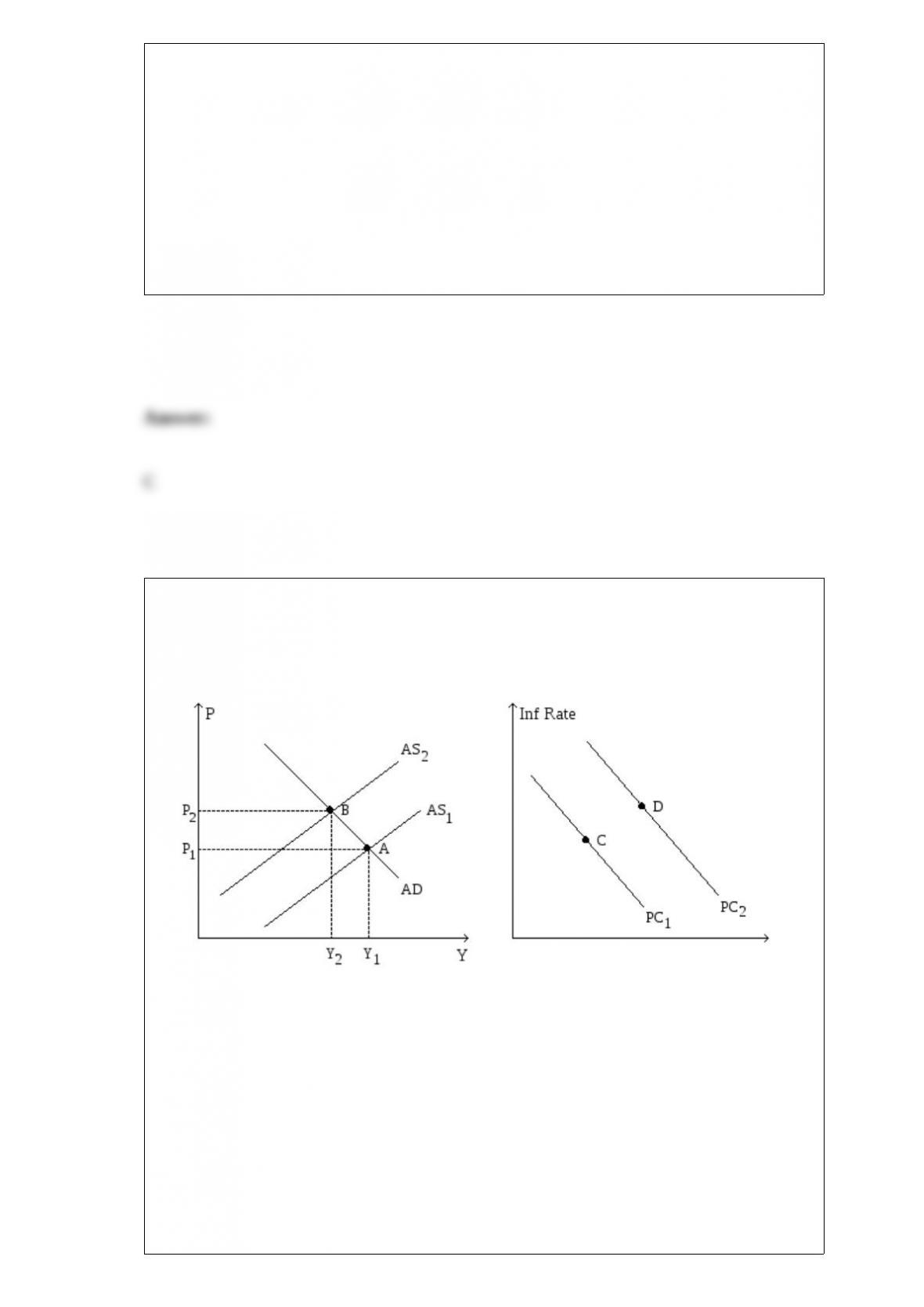

Figure 22-8. The left-hand graph shows a short-run aggregate-supply (SRAS) curve

and two aggregate-demand (AD) curves. On the right-hand diagram, “Inf Rate” means

“Inflation Rate.”

Refer to Figure 22-8. Faced with the shift of the Phillips curve from PC1 to PC2,

policymakers will

a. ask whether the shift is temporary or permanent.

b. be concerned with how people adjust their expectations of inflation as a result of the

shift.

c. face, as well, a decision as to whether to accommodate the shock.

d. All of the above are correct.

A tax placed on buyers of airline tickets shifts the

a. demand curve for airline tickets downward, decreasing the price received by sellers

of airline tickets and causing the quantity of airline tickets to increase.

b. demand curve for airline tickets downward, decreasing the price received by sellers

of airline tickets and causing the quantity of airline tickets to decrease.

c. supply curve for airline tickets upward, decreasing the effective price paid by buyers

of airline tickets and causing the quantity of airline tickets to increase.

d. supply curve for airline tickets upward, increasing the effective price paid by buyers

of airline tickets and causing the quantity of airline tickets to decrease.

A rationale for government involvement in a market economy is

a. markets sometimes fail to produce a fair distribution of economic well-being.

b. markets sometimes fail to produce an efficient allocation of resources.

c. property rights have to be enforced.

d. All of the above are correct.

National defense and knowledge are generally considered to be

a. private goods.

b. public goods.

c. proprietary goods.

d. societal goods.

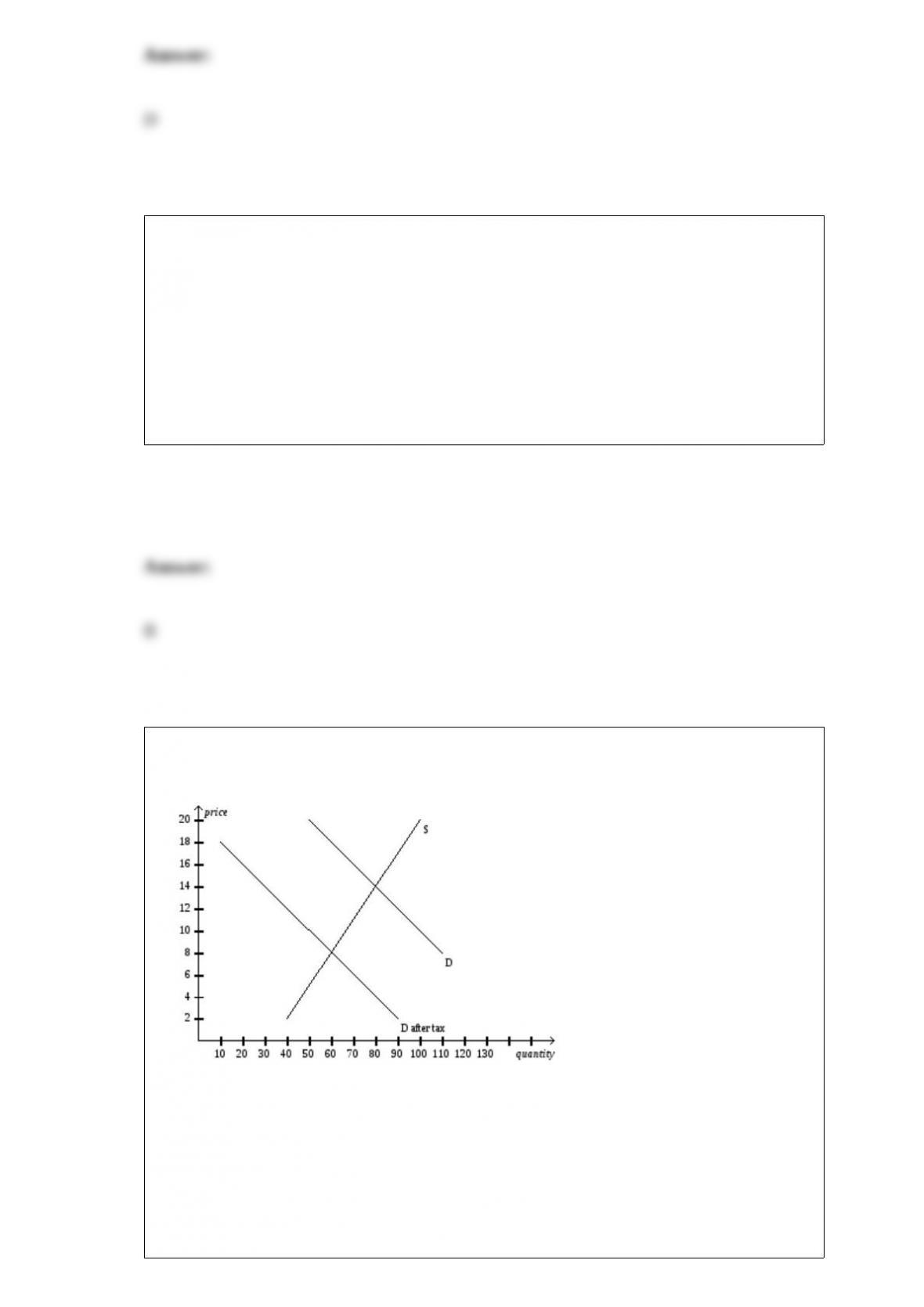

Figure 6-23

Refer to Figure 6-23. The per-unit burden of the tax is

a. $4 for buyers and $6 for sellers.

b. $5 for buyers and $5 for sellers.

c. $6 for buyers and $4 for sellers.

d. $10 for buyers and $0 for sellers.

To decrease the interest rate the Federal Reserve could

a. buy bonds. The fall in the interest rate would increase investment spending.

b. buy bonds. The fall in the interest rate would decrease investment spending.

c. sell bonds. The fall in the interest rate would increase investment spending

d. sell bonds. The fall in the interest rate would decrease investment spending.

Which of the following ideas is the most plausible?

a. Reducing a high tax rate is less likely to increase tax revenue than is reducing a low

tax rate.

b. Reducing a high tax rate is more likely to increase tax revenue than is reducing a low

tax rate.

c. Reducing a high tax rate will have the same effect on tax revenue as reducing a low

tax rate.

d. Reducing a tax rate can never increase tax revenue.

You have just been hired as a business consultant to determine what pricing policy

would be appropriate in order to increase the total revenue of a bakery. The first step

you would take would be to

a. increase the price of every loaf of bread in the store.

b. look for ways to cut costs and increase profit for the bakery.

c. determine the price elasticity of demand for the bakery’s products.

d. determine the price elasticity of supply for the bakery’s products.

Suppose the economy is in long-run equilibrium. If there is a sharp increase in the

minimum wage as well as an increase in pessimism about future business conditions,

then in the short run, real GDP will

a. rise and the price level might rise, fall, or stay the same. In the long run, the price

level might rise, fall, or stay the same but real GDP will be unaffected.

b. fall and the price level might rise, fall, or stay the same. In the long run, the price

level might rise, fall, or stay the same but real GDP will be unaffected.

c. rise and the price level might rise, fall, or stay the same. In the long run, the price

level might rise, fall, or stay the same but real GDP will be lower.

d. fall and the price level might rise, fall, or stay the same. In the long run, the price

level might rise, fall, or stay the same but real GDP will be lower.

As long as prices are rising over time, then

a. the nominal interest rate exceeds the real interest rate.

b. the real interest rate exceeds the nominal interest rate.

c. the real interest rate is positive.

d. the nominal interest rate is a better indicator than the real interest rate of how fast the

purchasing power of your bank account is changing over time.

In competitive markets,

a. firms produce identical products.

b. no individual buyer can influence the market price.

c. no individual seller can influence the market price.

d. All of the above are correct.

The long-run aggregate supply curve shifts right if

a. the price level rises.

b. the price level falls.

c. the capital stock increases.

d. the capital stock decreases.

The phenomenon of scarcity stems from the fact that

a. most economies’ production methods are not very good.

b. in most economies, wealthy people consume disproportionate quantities of goods and

services.

c. governments restrict production of too many goods and services.

d. resources are limited.

Which of the following is not correct?

a. A potential cost of deficits is that they reduce national saving, thereby reducing

growth of the capital stock and output growth.

b. Deficits give people the opportunity to consume at the expense of their children, but

they do not require them to do so.

c. The U.S. debt per-person is large compared with average lifetime income.

d. Current spending may benefit future generations.

Table 11-4

The table below pertains to Wrexington, an economy in which the typical consumer’s

basket consists of 20 pounds of meat and 10 toys.

Refer to Table 11-4. If the base year is 2004, then the CPI in 2005 was

a. 88.9.

b. 90.

c. 100.

d. 112.5.

Externalities are

a. side effects passed on to a party other than the buyers and sellers in the market.

b. side effects of government intervention in markets.

c. external forces that cause the price of a good to be higher than it otherwise would be.

d. external forces that help establish equilibrium price.

Which of the following is the correct expression for finding the present value of a

$1,000 payment one year from today if the interest rate is 6 percent?

a. $1,000 (1.06)

b. $1,000(1.06)

c. $1,000/(1.06)

d. None of the above is correct.

Which of the following is not possible?

a. Demand is elastic, and a decrease in price causes an increase in revenue.

b. Demand is unit elastic, and a decrease in price causes an increase in revenue.

c. Demand is inelastic, and an increase in price causes an increase in revenue.

d. Demand is perfectly inelastic, and an increase in price causes an increase in revenue.

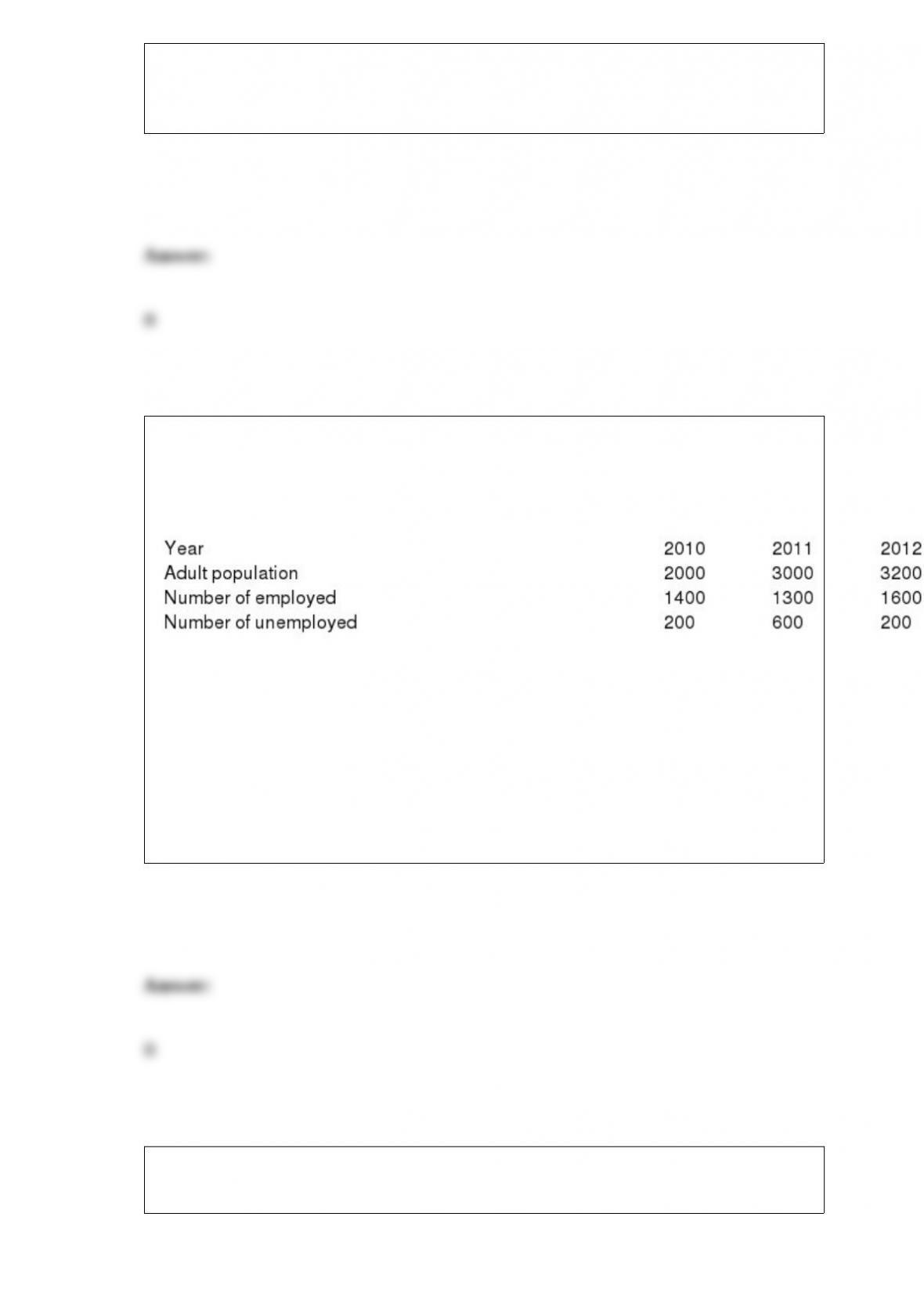

Table 15-1

Labor Data for Aridia

Refer to Table 15-1. The unemployment rate of Aridia in 2011 was

a. 20%.

b. 31.6%.

c. 46.2%.

d. 63.3%.

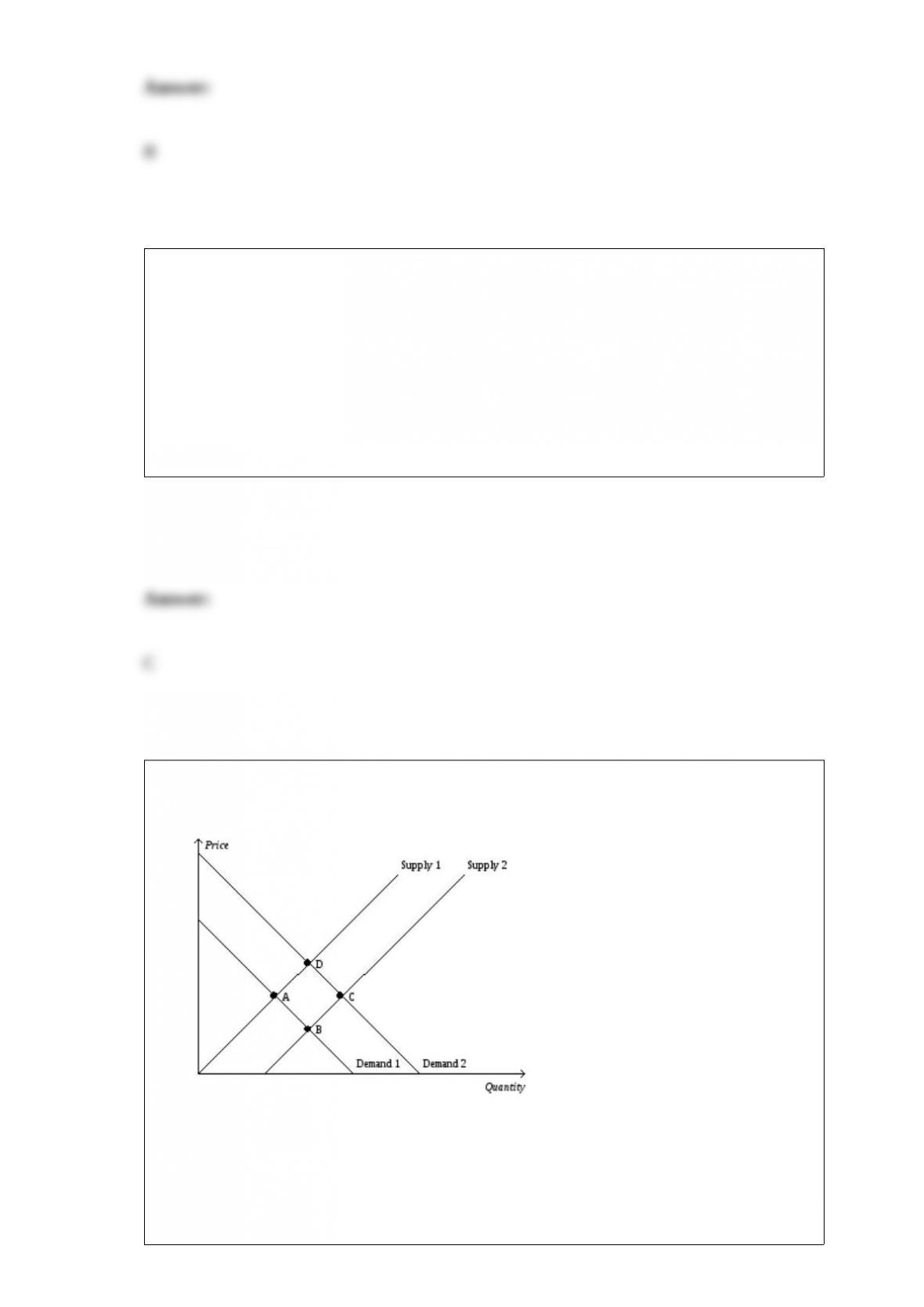

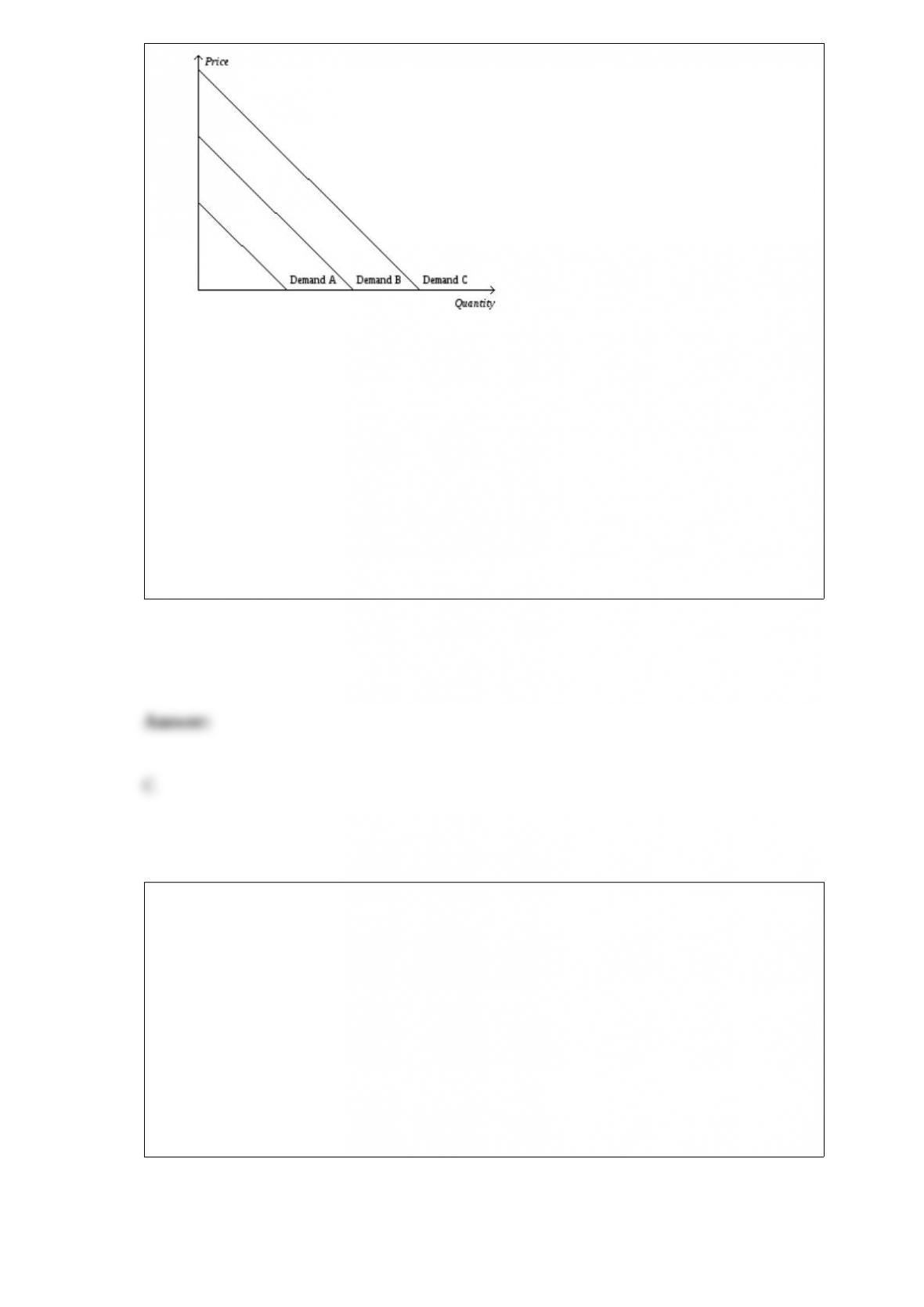

Figure 4-4

Refer to Figure 4-4. Which of the following would cause the demand curve to shift

from Demand C to Demand A in the market for DVDs?

a. an increase in the price of DVDs

b. a decrease in the price of DVD players

c. a change in consumer preferences toward watching movies in movie theaters rather

than at home

d. an expectation by buyers that their incomes will increase in the very near future

Suppose there is a decrease in aggregate demand. If the Fed wants to stabilize output it

could

a. buy bonds. These purchases also move the price level closer to its original level.

b. buy bonds. However these purchases move the price level farther from its original

level.

c. sell bonds. These sales also move the price level closer to its original level.

d. sell bonds. However these sales move the price level farther from its original level.

If U.S. consumers increase their demand for apples from New Zealand, then other

things the same New Zealand’s

a. imports and net exports rise.

b. imports rise and net exports fall.

c. exports and net exports rise.

d. exports rise and net exports fall.

A 10 percent increase in gasoline prices reduces gasoline consumption by about

a. 6 percent after one year and 5 percent after five years.

b. 2.5 percent after one year and 6 percent after five years.

c. 10 percent after one year and 20 percent after five years.

d. 0 percent after one year and 1 percent after five years.

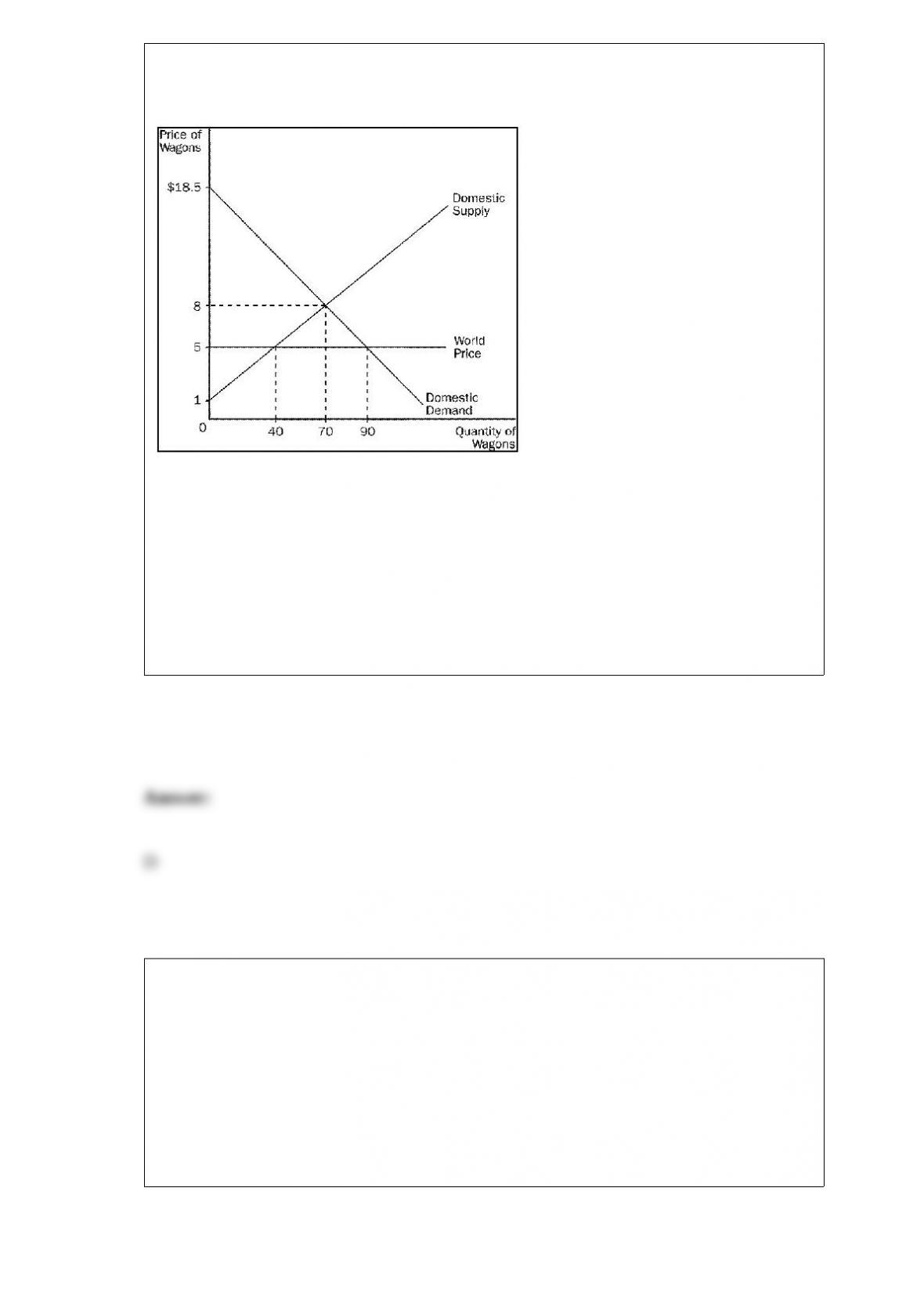

Figure 9-5

Refer to Figure 9-5. Without trade, total surplus amounts to

a. $122.50.

b. $245.

c. $367.50.

d. $612.50.

A tax imposed on the buyers of a good will lower the

a. price paid by buyers and lower the equilibrium quantity.

b. price paid by buyers and raise the equilibrium quantity.

c. effective price received by sellers and lower the equilibrium quantity.

d. effective price received by sellers and raise the equilibrium quantity.