If the exchange rate between the United States and Portugal changes from $1 = 1 euro

to $1 = 2 euros, then holding everything else constant, the price of U.S. goods in

Portugal will decrease.

As firms hire additional units of labor, eventually the marginal revenue product will

always increase.

The airline industry is a good example of a monopolistically competitive industry.

When the price of a good decreases, the budget constraint does not change.

We call a market where there is only one producer of a good or service a monopoly.

Since 1975, income inequality in the United States has been declining.

When two people trade, one must lose.

Equity is the condition in which the economy is producing what people want at the least

possible cost.

Things that have already been produced that are in turn used to produce other goods and

services over time are called “capital.”

Horizontal equity hold that those with equal ability to pay should bear equal tax

burdens.

A government policy generates $250,000 of benefits to disaster victims at a cost of

$200,000 to taxpayers. The policy results in a Pareto improvement.

A government policy generates $10,000 of benefits to underprivileged youth at a cost of

$5,000 to taxpayers. The policy is Pareto efficient.

If an aid program is mandated at the federal level, all states must abide by federal law

and pay the same amount of benefits.

The income distribution has become more equal in the United States over the last 30

years.

A firm should invest as long as funds are available and the expected rate of return is

greater than the interest rate.

Positive economics questions “What ought to be?” Normative economics predicts the

consequences of alternative actions, answering the questions “What is?” or “What will

be?”

The impossibility theorem, demonstrated by Kenneth Arrow, shows that no system of

aggregating individual preferences into social decisions will always yield consistent,

nonarbitrary results.

Input and output markets are interdependent and thus should be analyzed together.

Marginal costs reflect changes in variable costs.

Schumpeter and Galbraith believed that concentrated industries had lower rates of

technological advances than less concentrated industries.

If someone is willing to pay $800 to go to the World Cup but can buy a ticket for $500,

they will get $300 in consumer surplus.

If income is equally distributed to the members of society, then there is an equitable

distribution.

Post hoc, ergo propter hoc literally translated means, “all else equal.”

Human capital is a type of intangible capital.

Quantity supplied is determined by how much producers are willing and able to

produce.

If the price of a normal good falls, the opportunity cost of that good falls and

households buy more of the good.

When marginal cost is between average variable cost and average total cost, marginal

cost is decreasing.

Despite its capital city (Mumbai) being one of the top ten centers of commerce in the

world, India is on the World Bank’s list of low-income countries.

The “economic problem” is that given scarce resources, how do large societies go about

answering the basic economic questions of what will be produced, how it will be

produced, and who will get it.

The more differentiated the products produced by oligopolists, the more their behavior

will resemble that of a perfectly competitive industry.

Comparative advantage refers to the ability to produce better quality goods than a

competitor.

A U.S. import fee on steel would increase the domestic quantity of steel demanded.

An efficient economy is one that produces what consumers demand and does so at the

least possible cost.

Consumer surplus is the difference between the most a person is willing to pay and

market price.

For a risk averse individual, marginal utility of income does not diminish.

Wealth is a stock measure.

Microfinance is aimed at encouraging entrepreneurs among the very poorest parts of the

developing world to relocate to high-income countries.

Firms engage in production to

A) develop a supply schedule.

B) participate in the circular flow.

C) acquire profits.

D) assume risk.

A “brain drain” is the tendency of talented people in developing countries to get

education in

A) developed countries and return home after graduation.

B) developed countries and stay there after graduation.

C) their own countries and leave after graduation.

D) their own countries and stay there after graduation.

The Social Security System includes three separate programs. They are ________.

A) Old Age and Survivors Insurance, Disability Insurance, and Health Insurance

B) Old Age and Survivors Insurance, Medicare, and Medicaid

C) Disability Insurance, Medicare, and Public Assistance (Welfare)

D) Old Age and Survivors Insurance, Medicare, and Unemployment Compensation

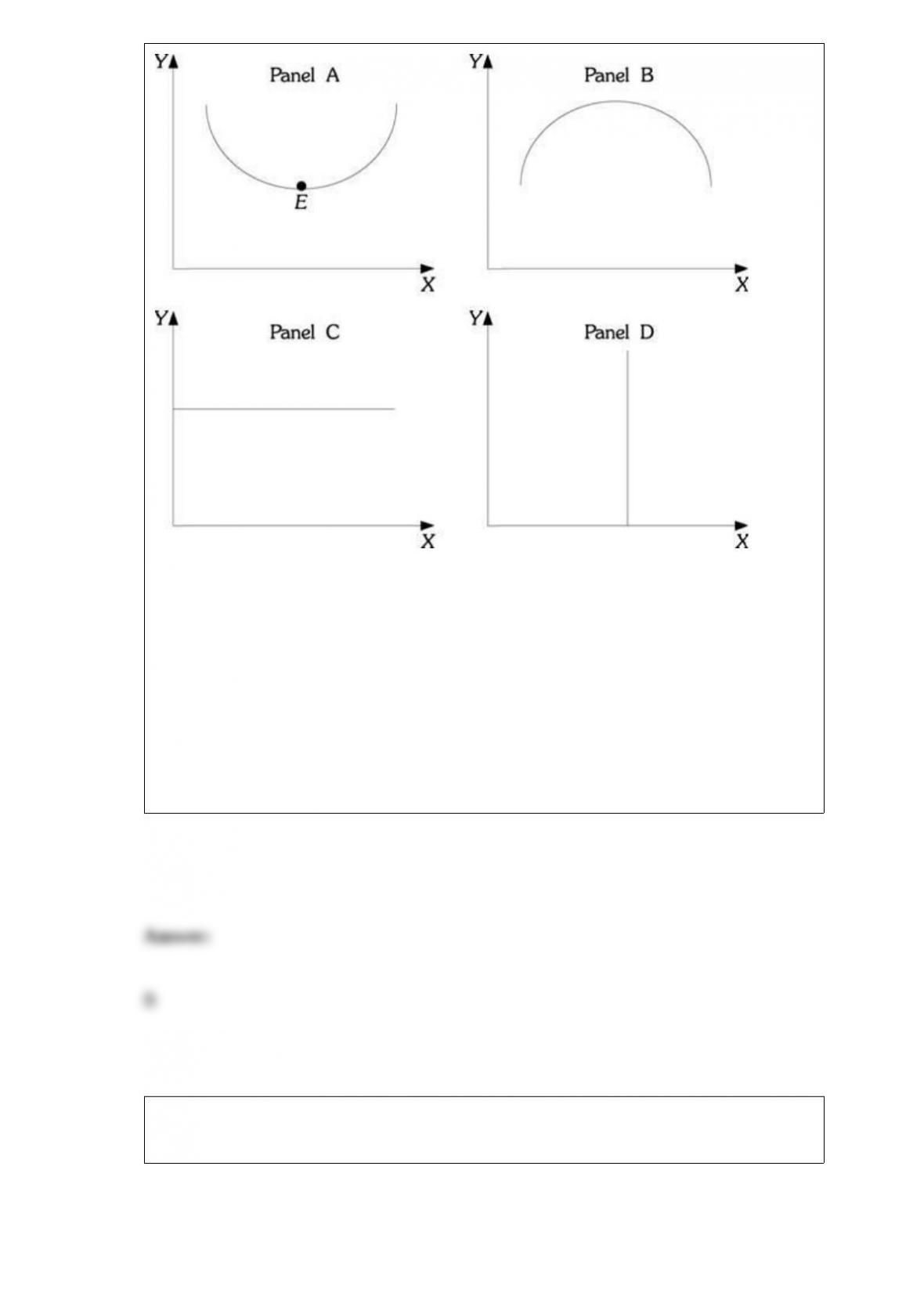

Figure 1.4

Refer to Figure 1.4. At Point E in panel A, the slope is

A) infinite.

B) zero.

C) negative.

D) indeterminate from this information.

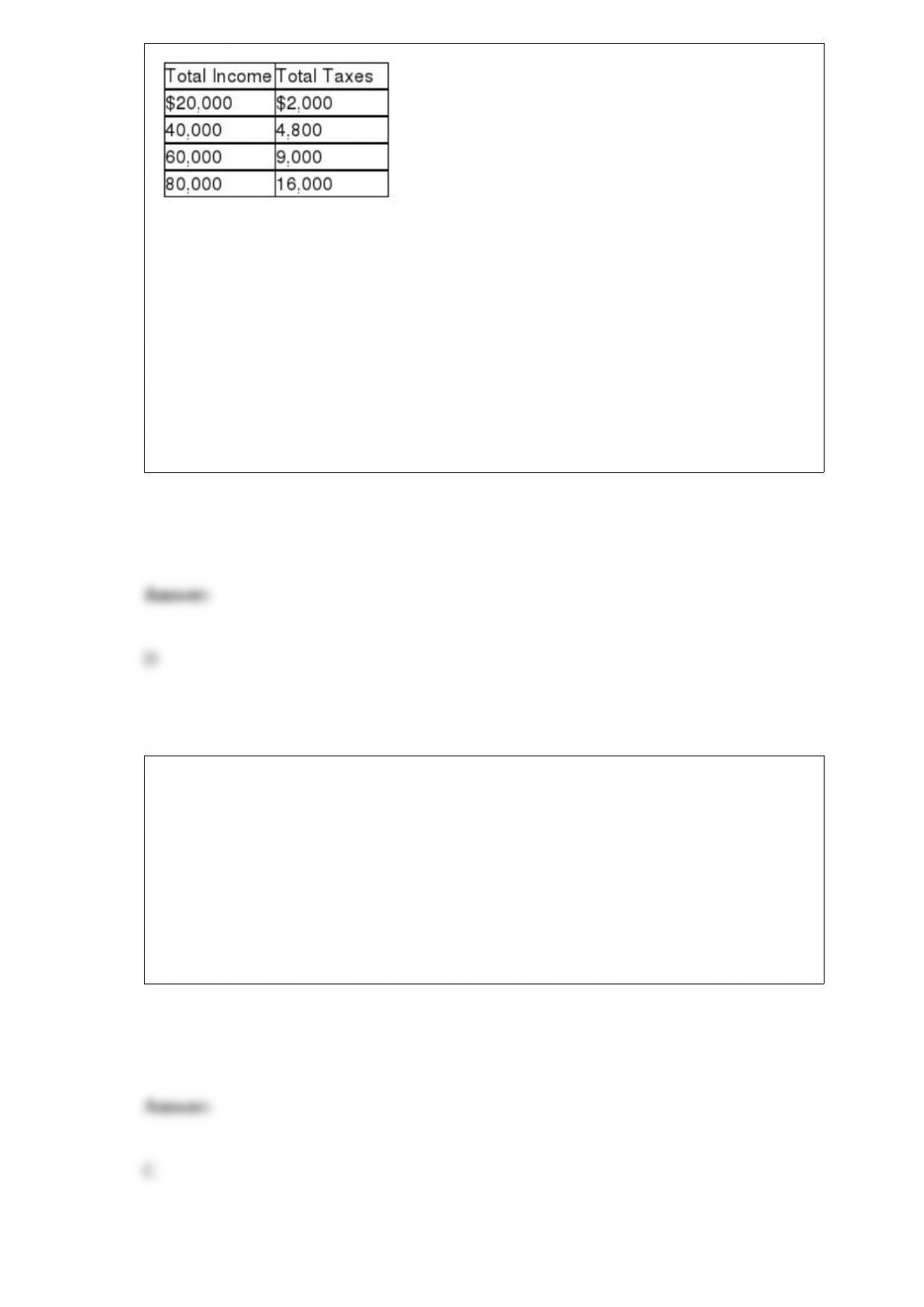

Table 19.1

Relating to the Economics in Practice on page 392: Refer to Table 19.1. At an income

level of $80,000, the average tax rate is

A) 2%.

B) 5%.

C) 15%.

D) 20%.

A government-imposed maximum price will have no economic impact if

A) it is below the equilibrium price.

B) it is at or below the equilibrium price.

C) it is above the equilibrium price.

D) there is a fixed supply of the good.

Governments often ________ activities that generate external ________.

A) tax; costs

B) subsidize; costs

C) tax; benefits

D) simultaneously tax and subsidize; costs

For inferior goods, an increase in income will cause the

A) quantity demanded to fall.

B) demand to increase.

C) demand to fall.

D) quantity demanded to increase.

All of the following are true about public goods EXCEPT:

A) bestow collective benefits on members of society.

B) are non-excludable since those who do not pay for them cannot be excluded from

enjoying them.

C) will be under supplied by the private sector.

D) are only produced by government agencies.

The table shows the relationship between income and utility for Celeste.

Table 17.1

Refer to Table 17.1. From the table, we can see that Celeste is

A) risk averse.

B) risk loving.

C) risk neutral.

D) We cannot determine Celeste’s attitude toward risk from the table.

Some economists advocate government intervention in a market economy when

resource costs for a private producer ________ to society.

A) are greater than the full cost

B) are equal to the full cost

C) do not reflect the full cost

D) have no relevant cost

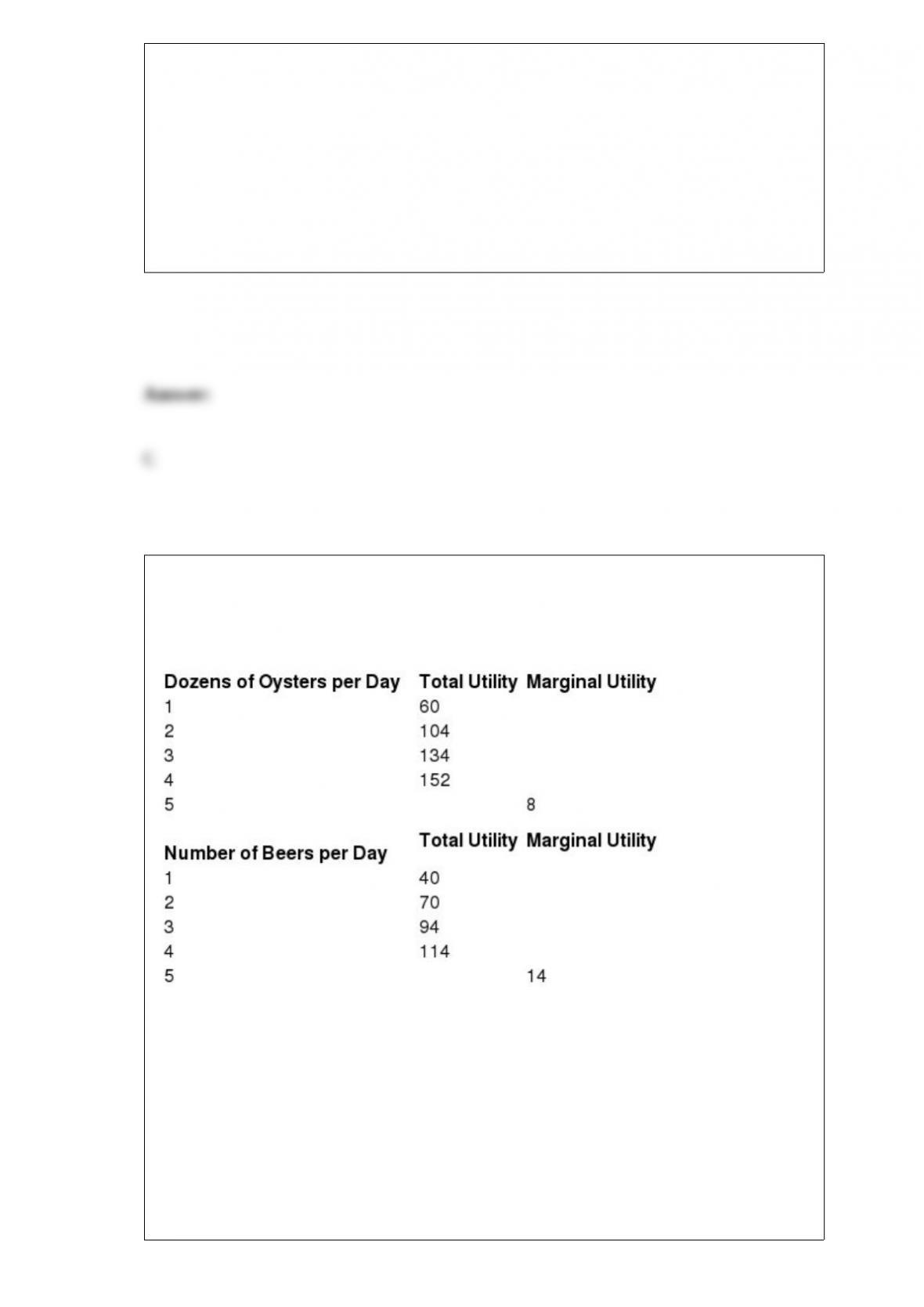

Table 6.1

Refer to Table 6.1. Assume that a store is giving oysters and beers away for free.

Consumers can have as many beers and oysters (by the dozen) as they want, but the

food has to be consumed one unit at a time. If Tyler has already had one beer and two

dozen oysters, then Tyler should

A) next consume a beer to maximize his utility.

B) next consume a dozen oysters to maximize his utility.

C) be indifferent between consuming the second beer or the third dozen oysters.

D) consume neither another beer nor another dozen oysters to maximize his utility.

In developing countries,

A) financial markets are well developed.

B) central banks are effective in controlling the macroeconomy.

C) labor productivity in agriculture is high.

D) infant mortality is high.

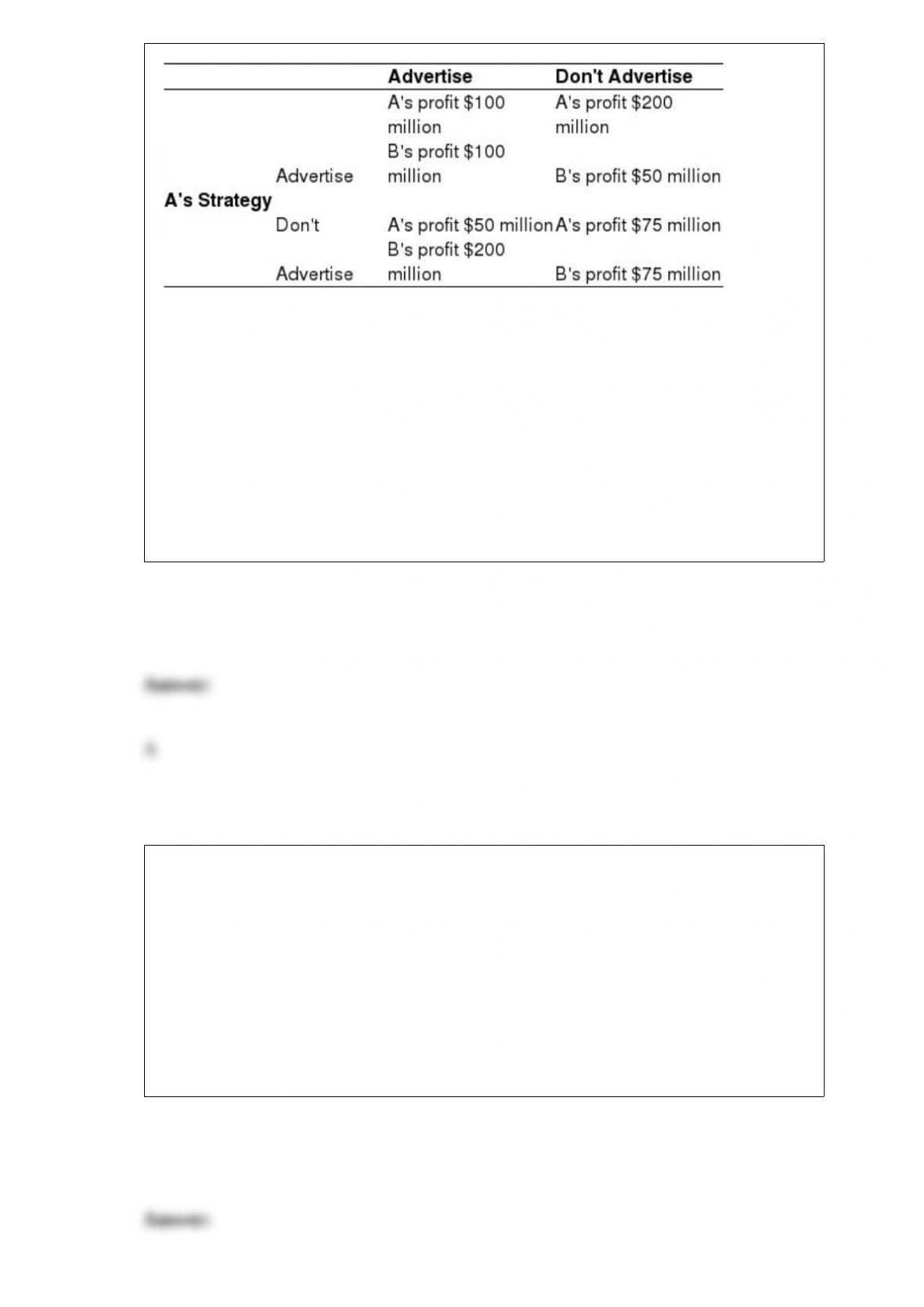

Table 2

B’s Strategy

Refer to Table 14.2. Firm A s dominant strategy isʹ

A) to advertise.

B) to not advertise.

C) dependent on what Firm B does.

D) indeterminate from this information, as no information is provided on Firm A s risk ʹ

preference.

In which system are decisions made by thousands of people who have information

about resources, production technology and consumer desires?

A) market system

B) centrally planned system

C) command system

D) socialist system

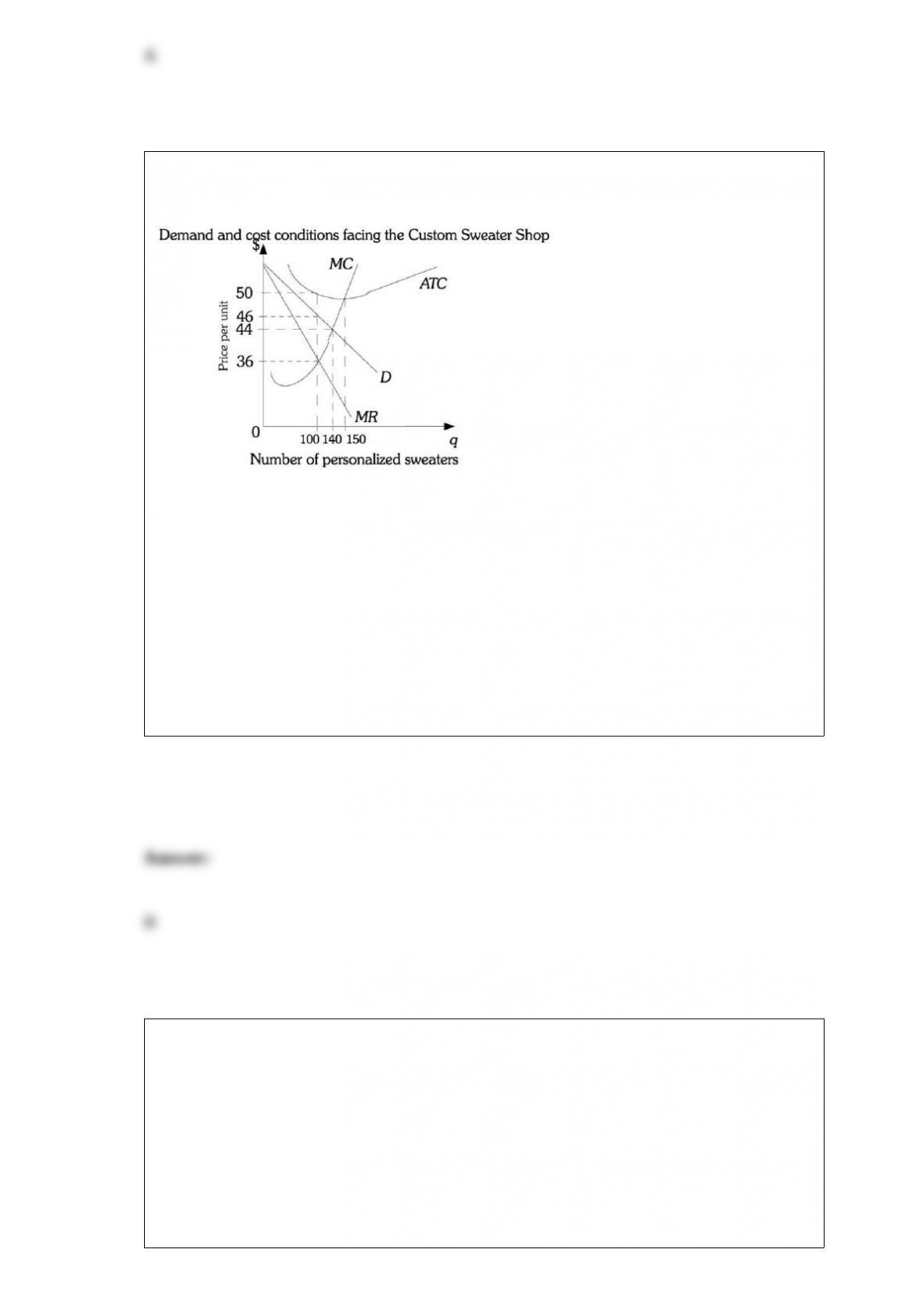

Figure 15.5

Refer to Figure 15.5. In the long run, in this monopolistically competitive industry,

A) firms will leave the industry until each firm earns an economic profit.

B) some firms will leave the industry until the remaining firms earn a normal profit.

C) firms will enter the industry, which will increase the demand for the product.

D) the government will subsidize the firms to eliminate any losses the firms incur.

You will still be able to get public broadcasting whether or not you contribute to their

fund-raising campaign, so you decide ________ contribute. This is an example of the

free-rider problem, and is intrinsic to ________ goods.

A) to; public

B) not to; public

C) to; private

D) not to; private

Table 9.1

Refer to Table 9.1. If the market price is $42, then in the long run the firm will

A) operate and expand.

B) operate but not expand.

C) shut down, but not go out of business.

D) go out of business.

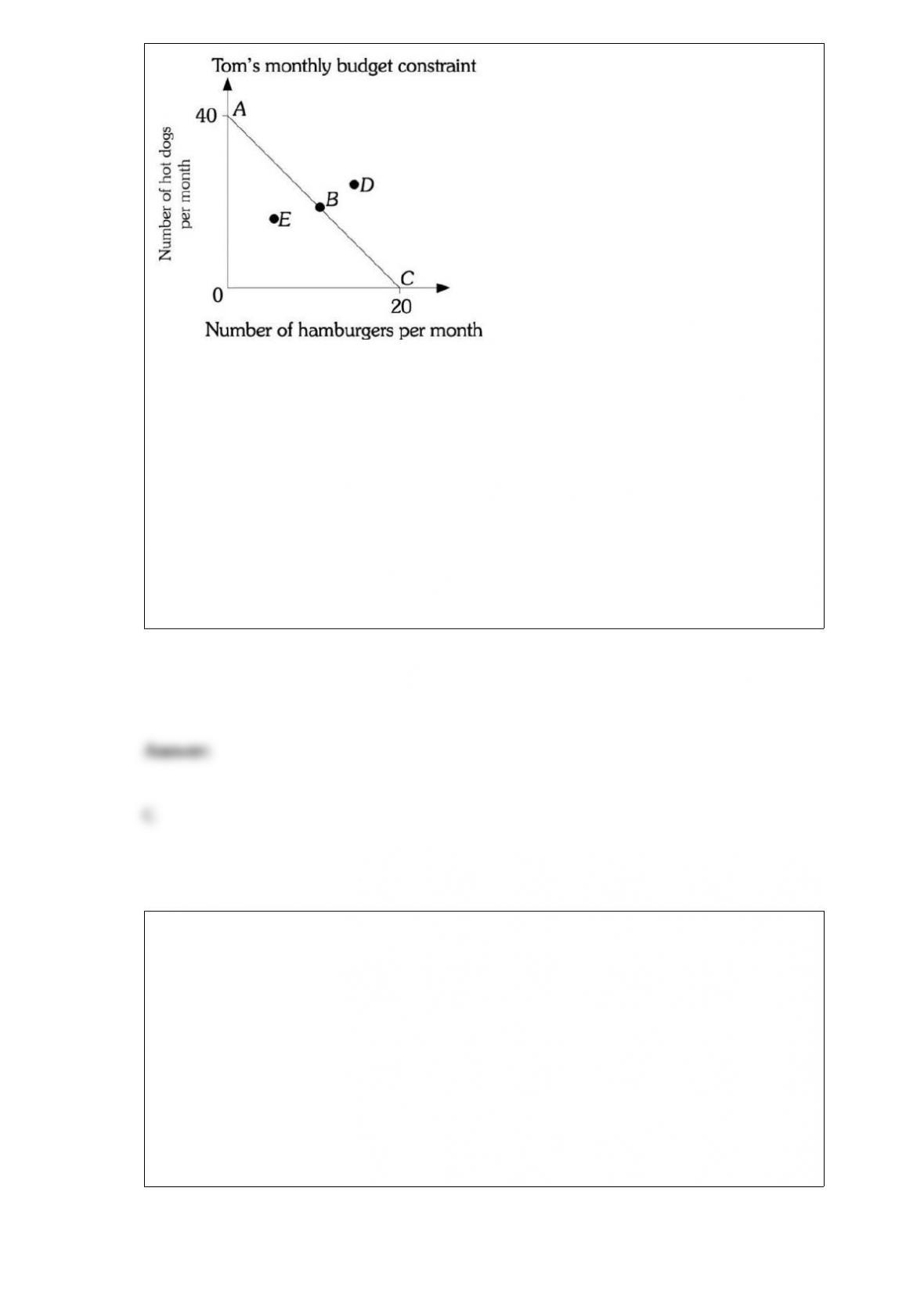

Figure 6.1

Refer to Figure 6.1. Assume Tom’s budget constraint is AC. He will have leftover

income if he purchases the bundle represented by point

A) A.

B) B.

C) E.

D) D.

Assuming there are no externalities, if a firm produces an output level where the

benefits to consumers ________ the cost to suppliers to produce it, then price is

________ marginal cost.

A) are less than; greater than

B) exceed; greater than

C) exceed; less than

D) equal; less than

Economics is best defined as the study of

A) financial decision making.

B) how consumers make purchasing decisions.

C) choices made by people faced with scarcity.

D) inflation, unemployment, and economic growth.

To the extent that oligopolies differentiate their products,

A) there is overproduction from society’s point of view.

B) they force themselves into deadlocks that waste resources.

C) there is the promise of new and exciting products.

D) they are also likely to price at marginal cost.

The labor theory of value states that

A) if all markets are competitive, then labor will be paid its marginal revenue product.

B) under capitalism all workers will be paid a subsistence wage.

C) the value of a commodity depends only on the amount of labor required to produce

it.

D) labor should be paid what is left over after all other factors of production have been

paid.

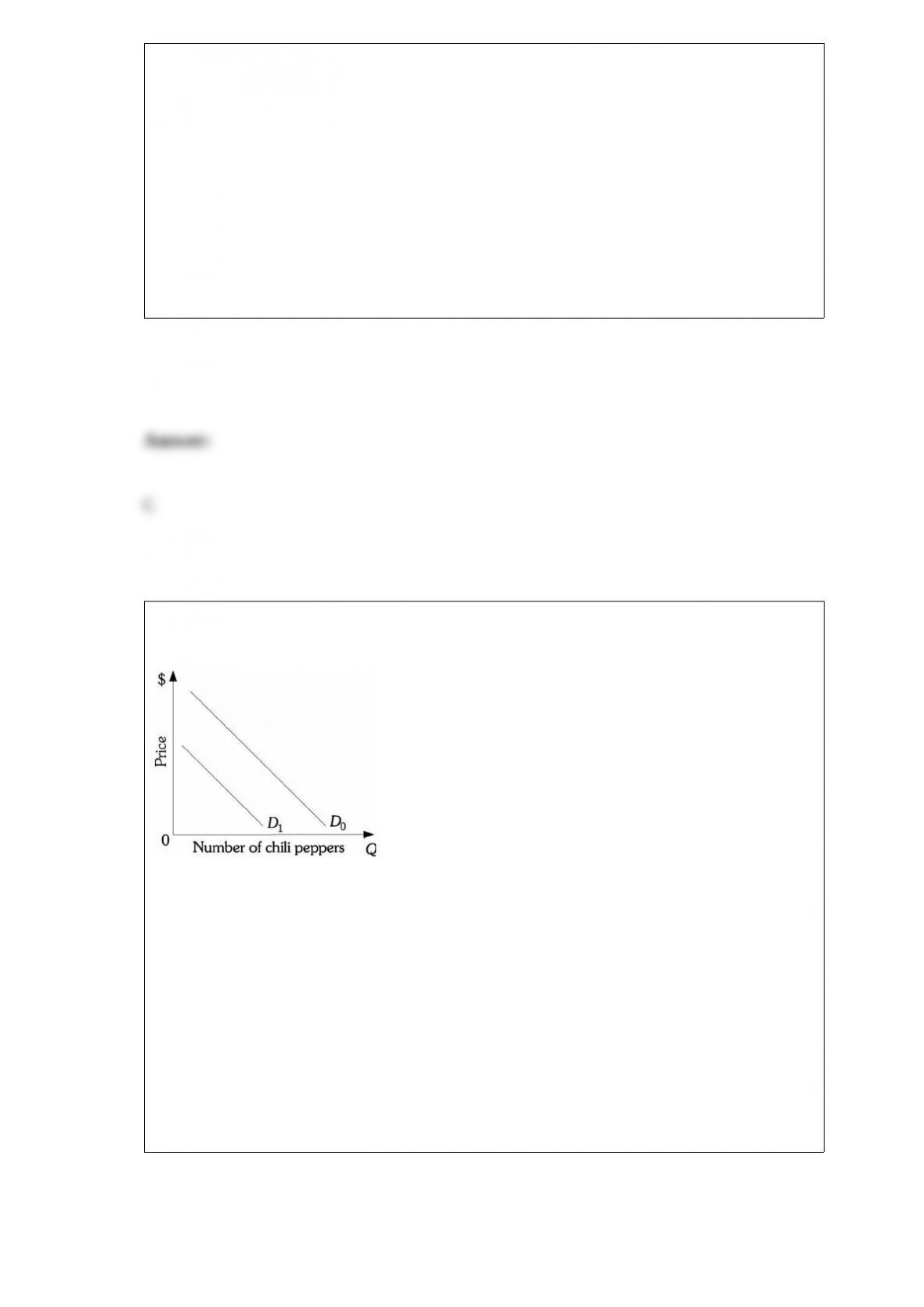

Figure 3.5

Refer to Figure 3.5. If consumer income increases, the demand for chili peppers shifts

from D0 to D1. This implies that chili peppers are a(n)

A) normal good.

B) inferior good.

C) substitute good.

D) complementary good.

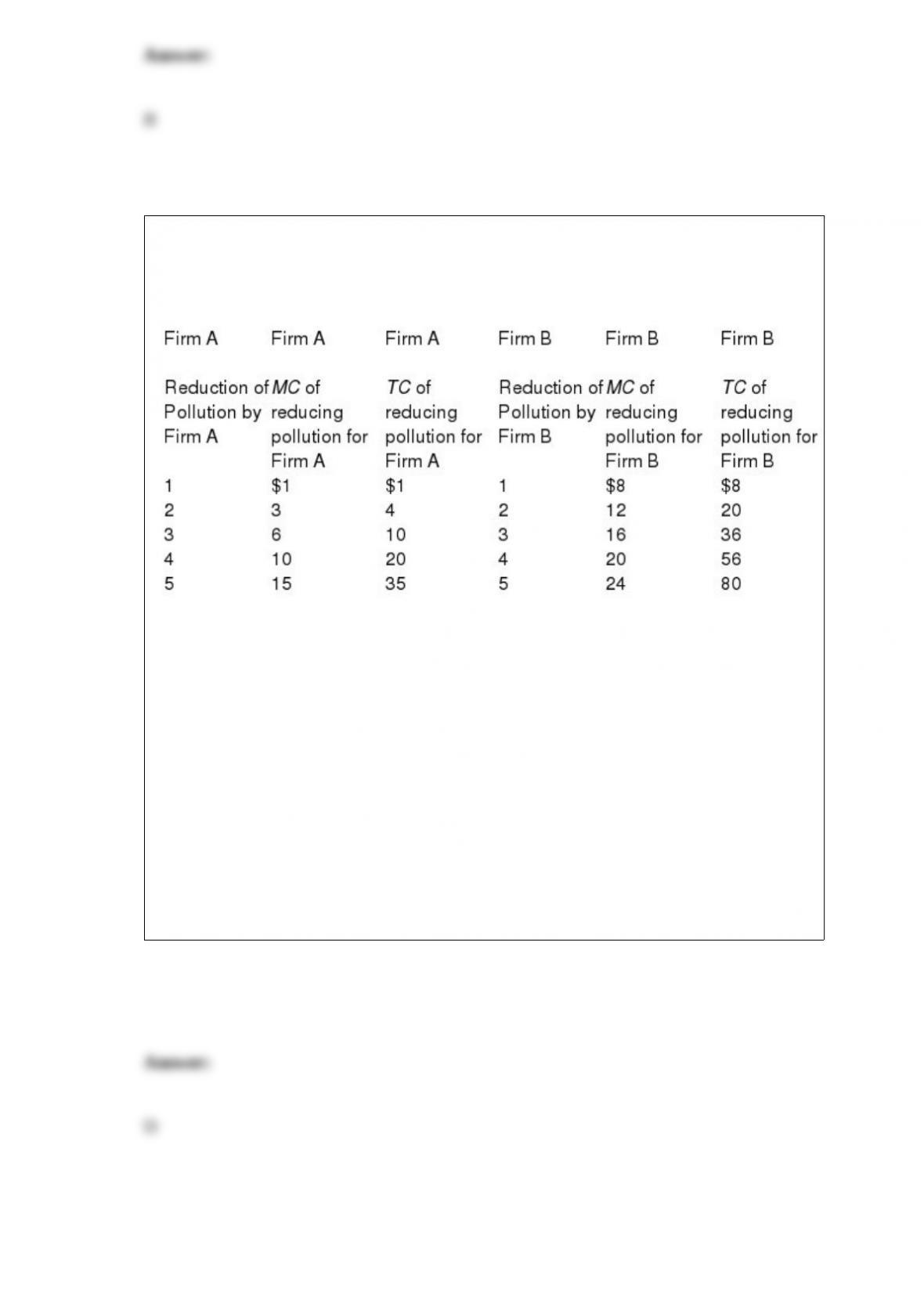

Table 16.4 shows the situation facing two firms, both of which are polluting. Assume

that each firm emits 5 units of pollution.

Table 16.4

Refer to Table 16.4. Suppose the government wants to reduce the total amount of

pollution from the current level of 10 to 4. To do this, the government caps each firm’s

emissions at 2 units and issues 2 permits to each firm. If firms are allowed to trade

permits and all possible trades are made, Firm A will reduce its pollution by a total of

________ units.

A) 2

B) 3

C) 4

D) 5

An economy in which a central authority draws up a plan that establishes what will be

produced and when, sets production goals, and makes rules for distribution is a

A) free market economy.

B) laissez-faire economy.

C) public goods economy.

D) command economy.

Education is a ________ good that creates a ________ externality.

A) public; positive

B) private; positive

C) public; negative

D) private; negative

Suppose that a normal rate of return in the economy is 14% and the rate of return that

firms earn in a competitive industry equals exactly 14%. Which of the following is a

CORRECT prediction based on this information?

A) New firms will want to enter this industry, as the existing firms are earning an

economic profit.

B) Firms already in the industry will want to expand to try to increase their rate of

return.

C) Firms in the industry will not undertake any investment projects other than to

replace depreciating capital stock.

D) The industry size will contract.

Figure 2.4

According to Figure 2.4, a decrease in unemployment may be represented by the

movement from

A) B to A.

B) B to D.

C) C to D.

D) A to C.

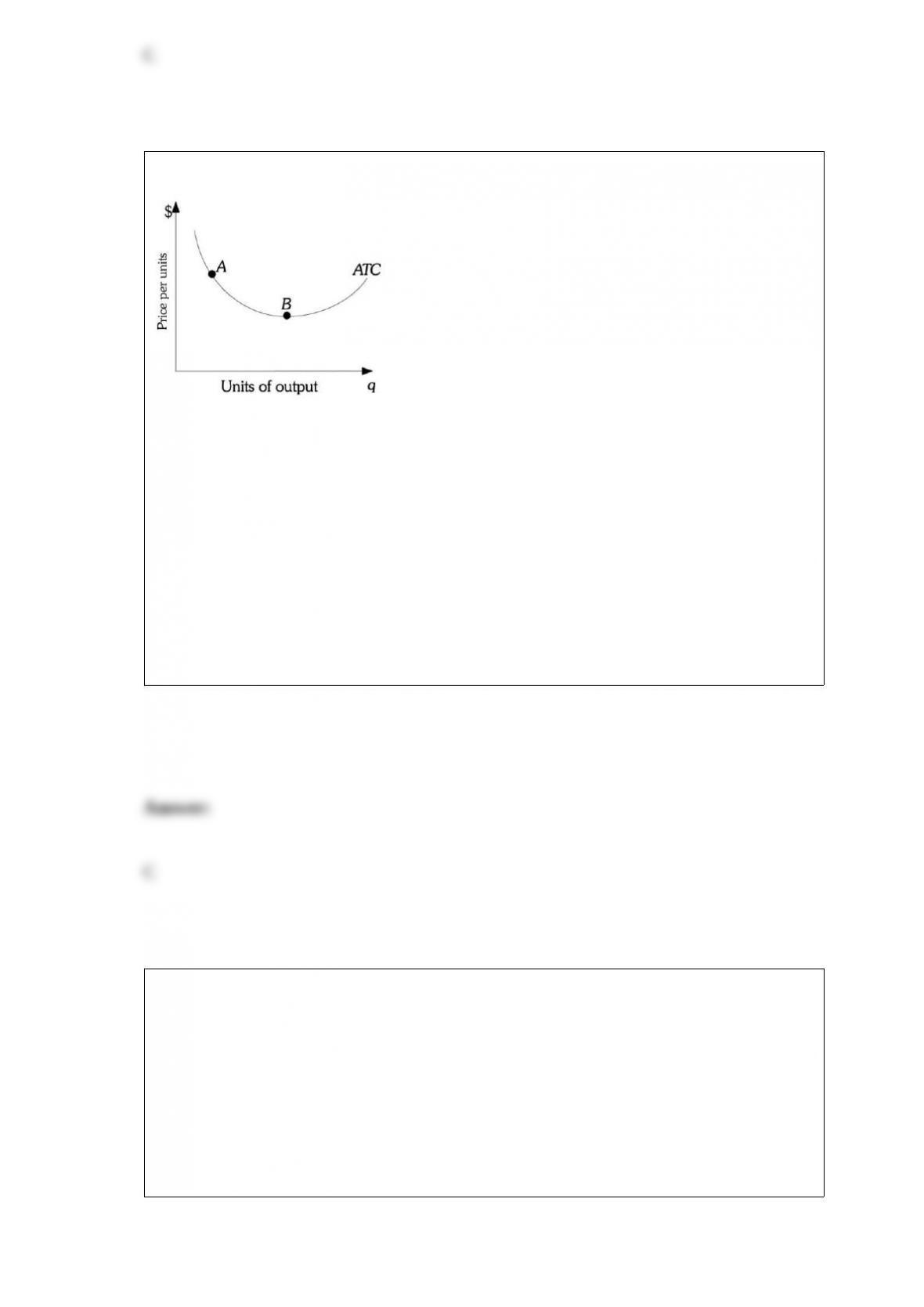

Figure 12.1

Refer to Figure 12.1. This firm is currently at Point A on the ATC curve. If this firm

moves toward Point B, this will make the

A) distribution of outcome more equitable.

B) economy more stable.

C) economy more efficient.

D) economy less stable.

Price and total revenue move in inverse directions when demand is

A) price elastic.

B) price inelastic.

C) unit price elastic.

D) perfectly price inelastic.

A(n) ________ industry has a single, unique product and blocked entry.

A) perfectly competitive

B) monopolistically competitive

C) monopolistic

D) oligopolistic

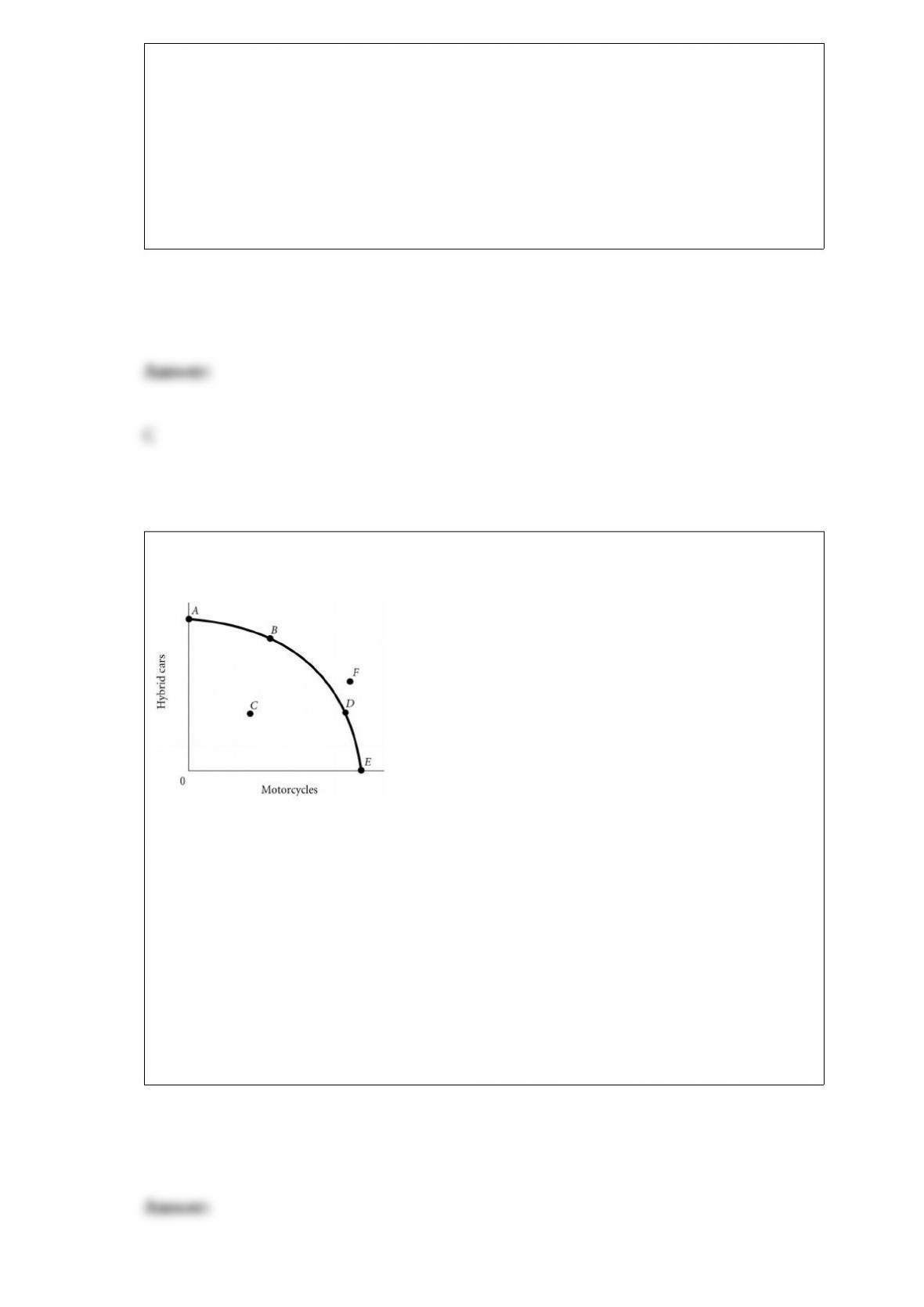

Specialization and trade allow a country to produce ________ its production possibility

frontier and consume ________ it.

A) outside; outside

B) outside; inside

C) outside; on

D) on; outside

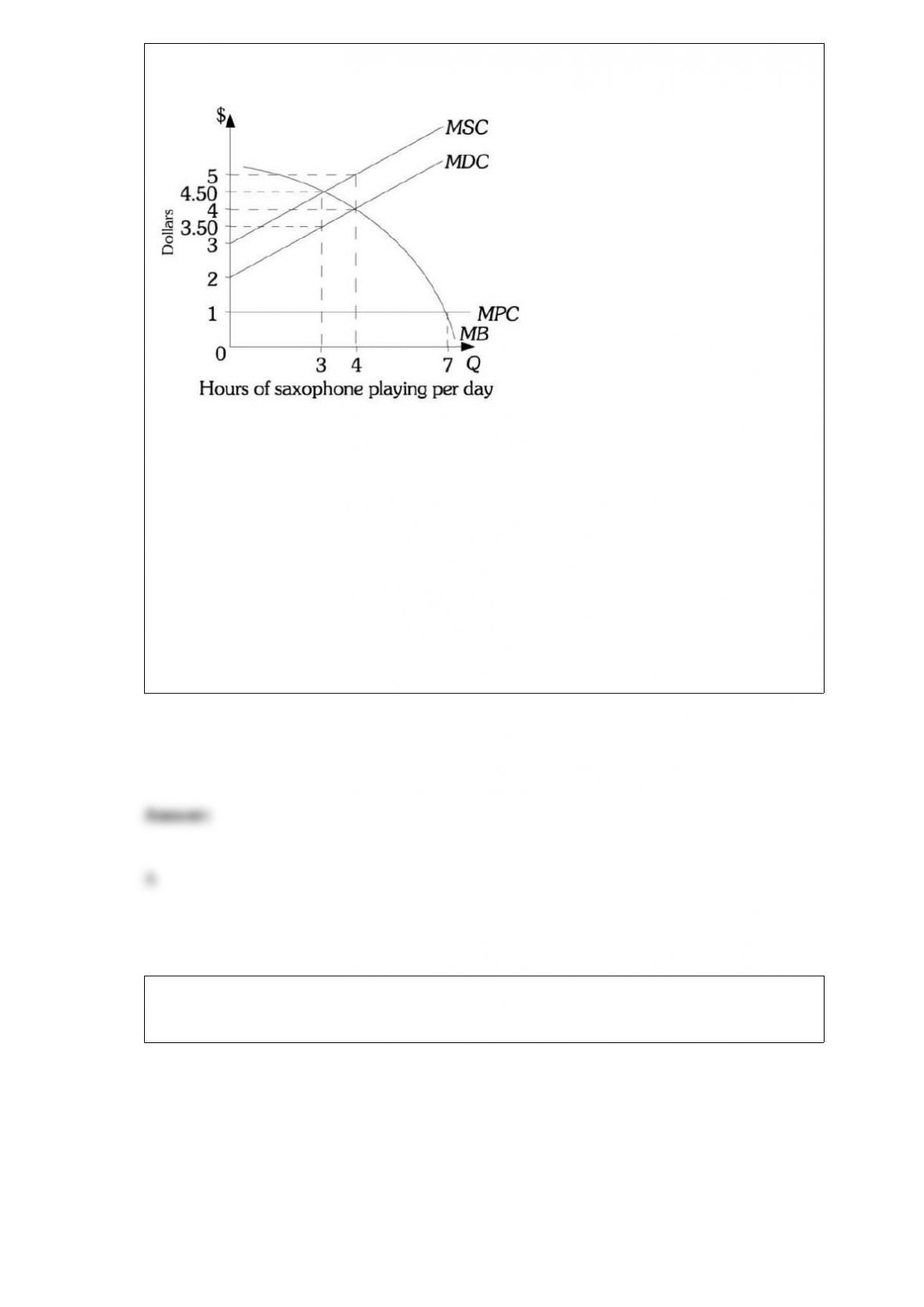

Figure 16.3

Refer to Figure 16.3. When Bill plays his saxophone, he imposes costs on his wife.

________, he will play his saxophone for seven hours per day.

A) If Bill does not take these costs into consideration

B) If Bill takes these costs into consideration

C) Whether or not Bill takes these costs into consideration

D) Bill will never play his saxophone for seven hours per day.

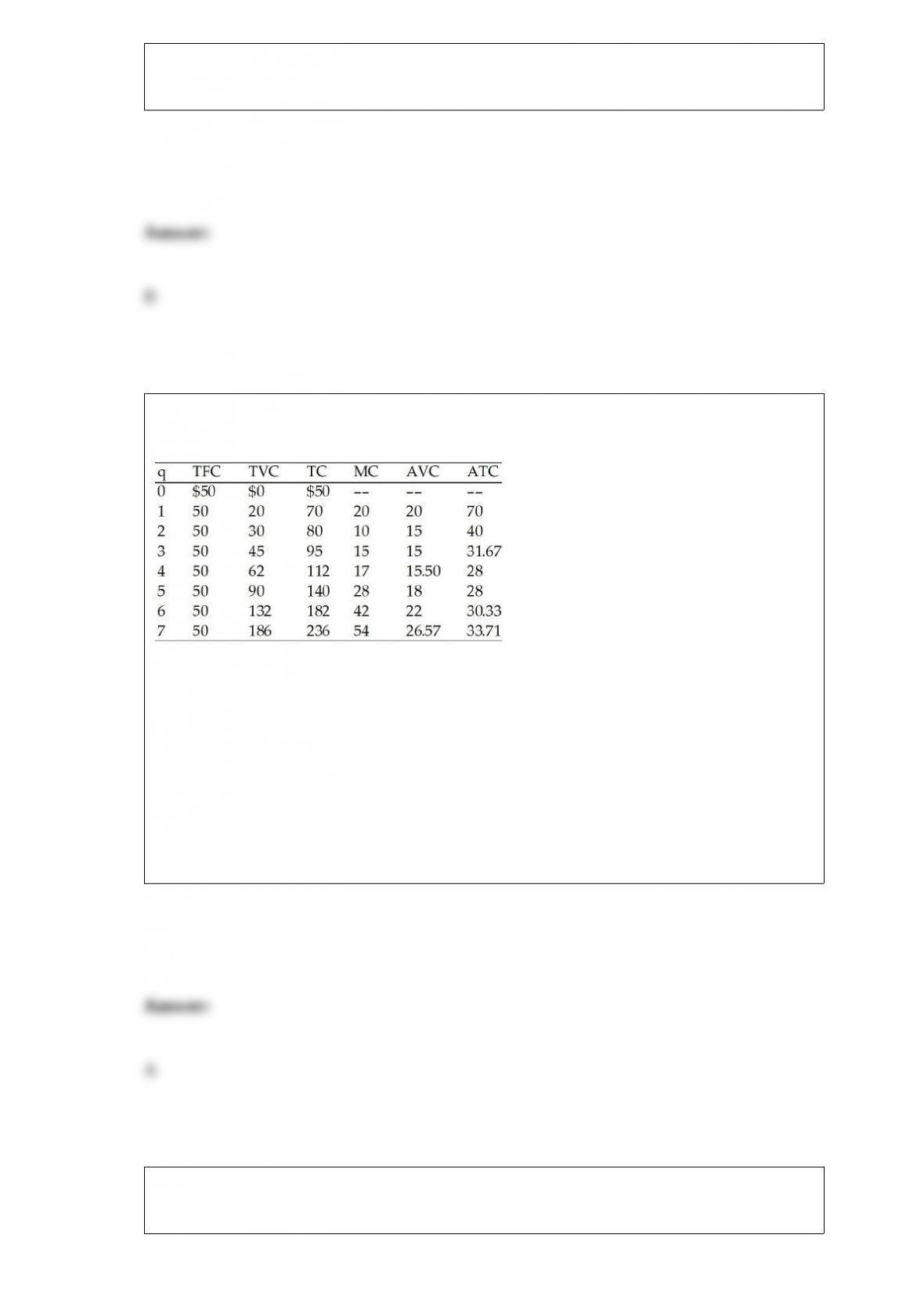

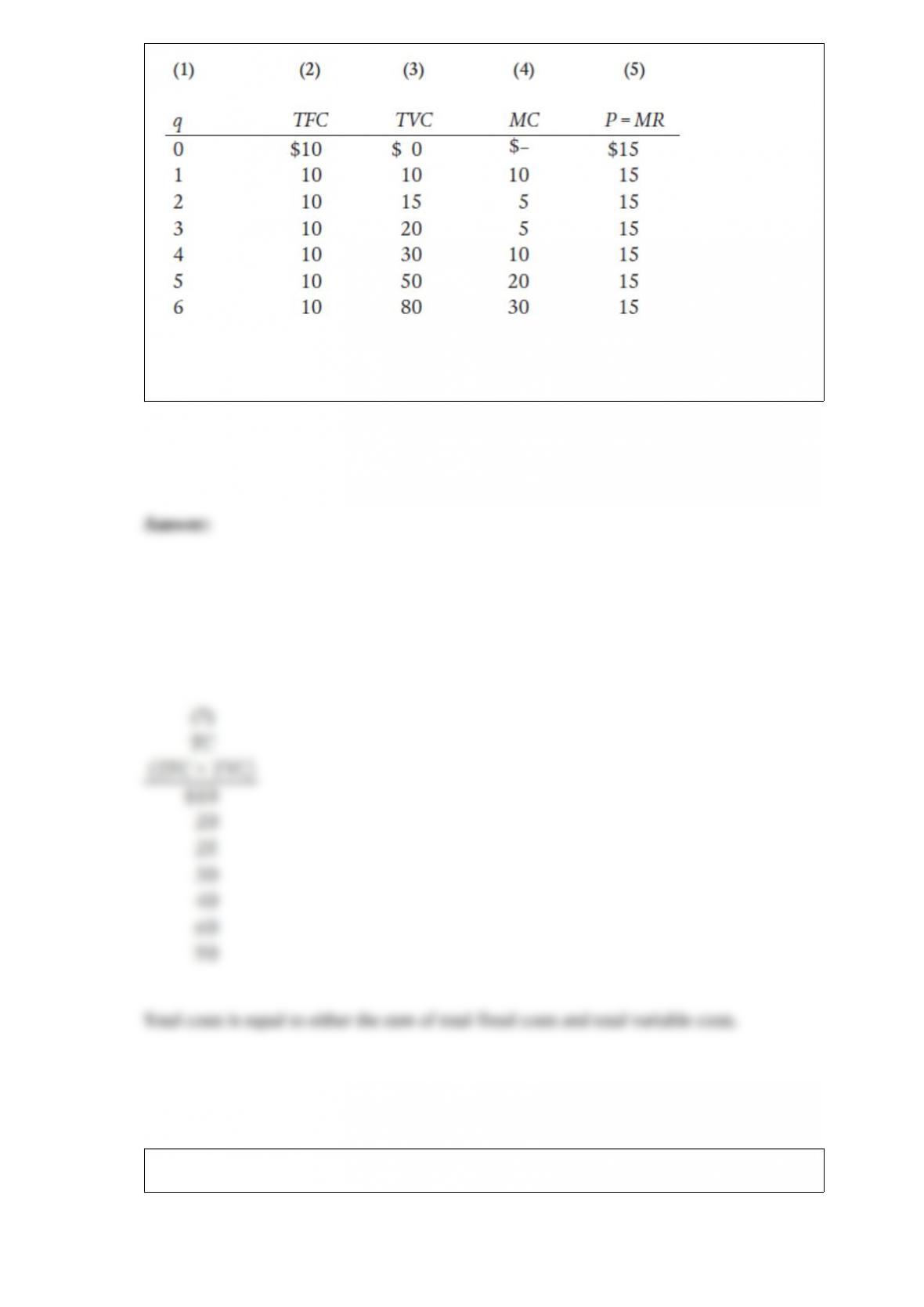

Table 8.5

Referring to Table 8.5 create a seventh column for total cost and explain how you

calculated it.

What is the opportunity cost of attending class today?

Compare and contrast the tax base with the tax rate structure.

In economics, what differentiates the short run from the long run?

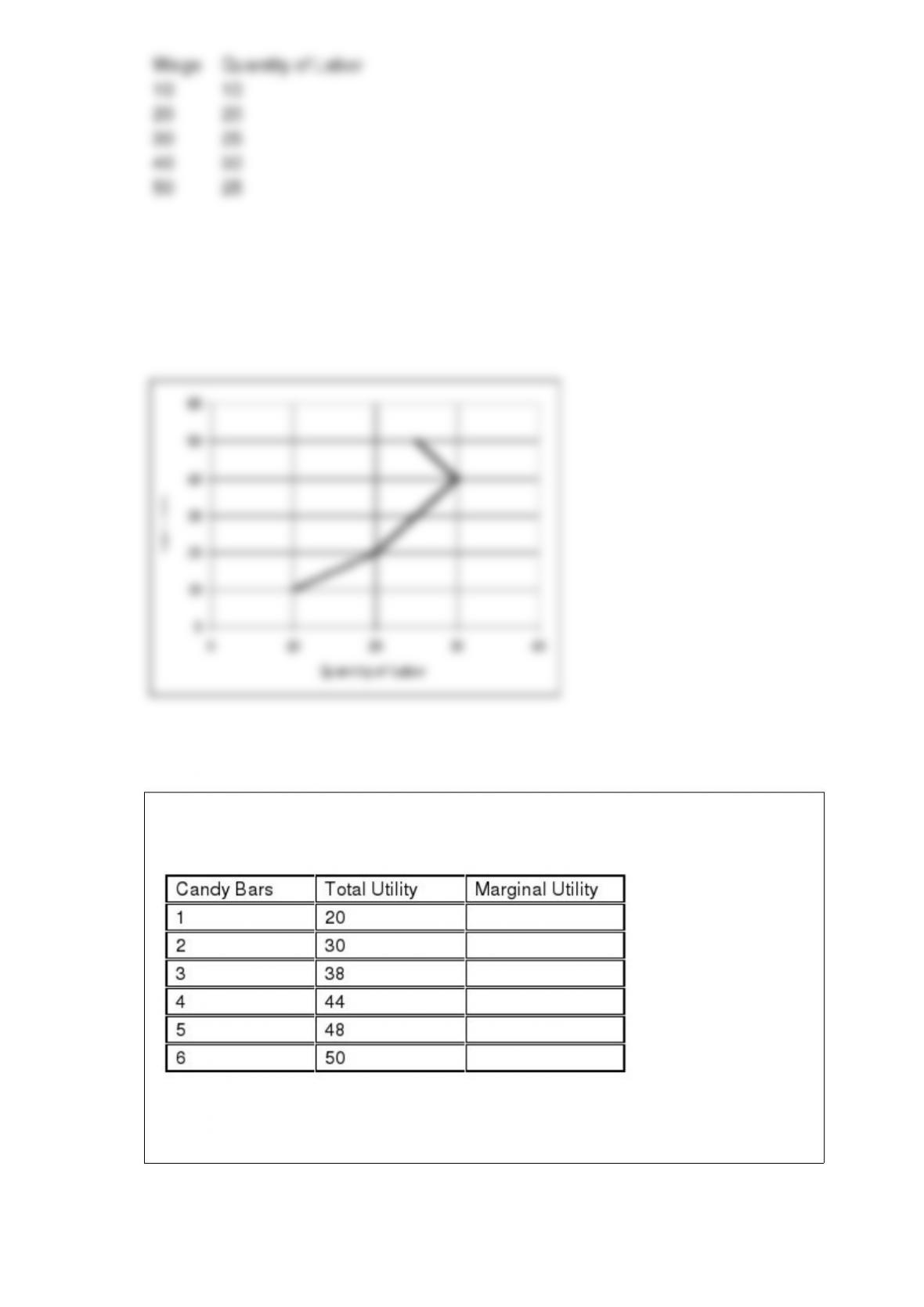

Suppose that as wages increase the quantity of labor supplied increases as well.

However, assume that at some point as indicated in the table below increases in wages

actually lead to a reduction in the quantity of labor supplied. Graph this relationship

with the quantity of labor on the horizontal axis and the wage rate on the vertical axis.

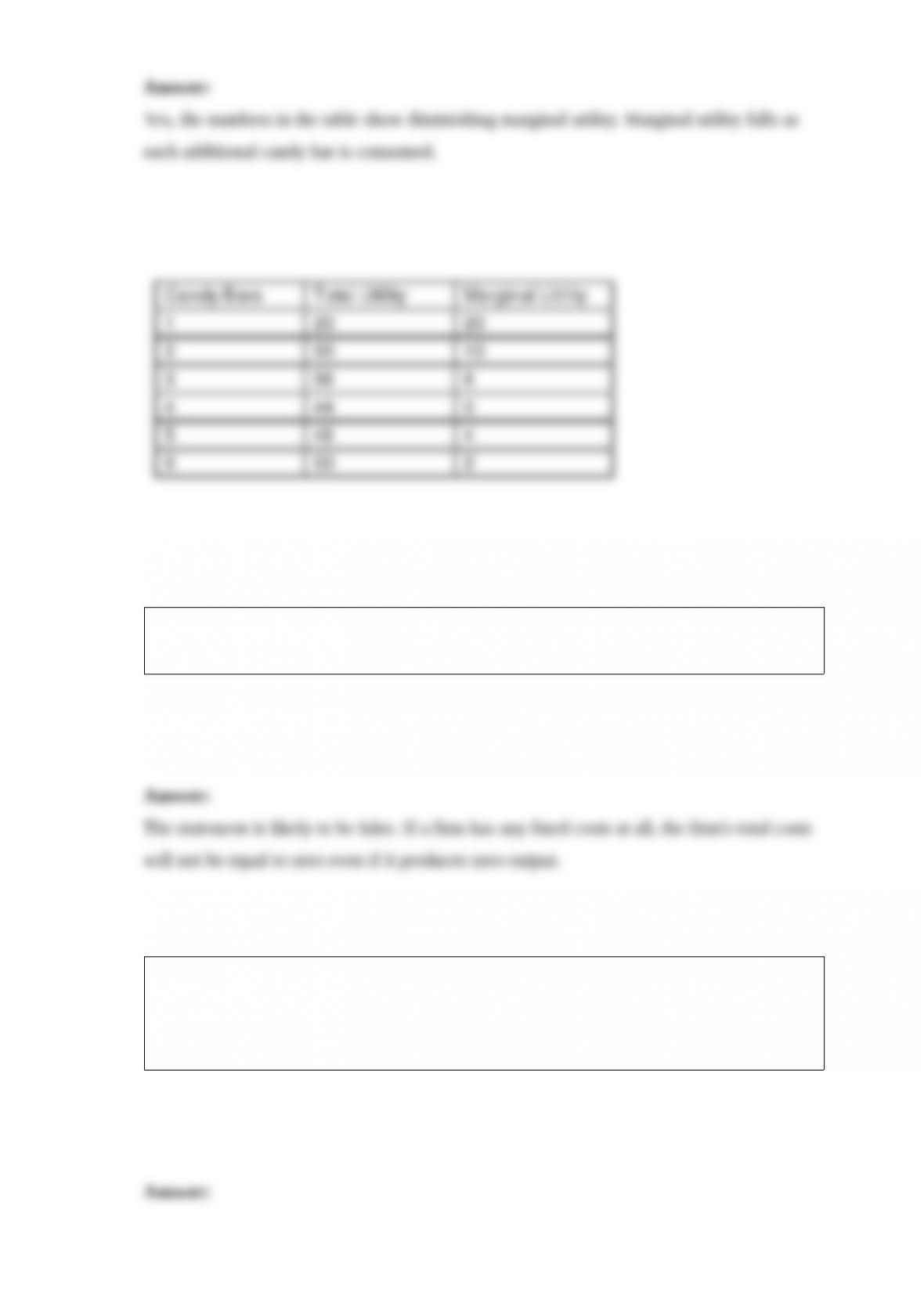

The table below shows how the total utility that Zach derives from eating candy bars

changes as he consumes more and more candy bars each day:

Fill in the table above. Do the numbers in the table support the law of diminishing

marginal utility? Explain.

Comment on the following statement: “In the short run, a firm’s total costs will be zero

if the firm chooses to produce nothing.”

A manager of a small company makes the following statement ” “We need to keep

hiring additional workers up to the point where the marginal productivity of the last

worker we hire is at its maximum. This way we can maximize the total productivity of

the firm.” Critically evaluate this statement.

Assume that you are a plaintiff and have won a structured settlement from a lawsuit that

entitles you to $1 million each year over the next ten years. An attorney from the

defense team approaches you afterward and offers you $6 million in exchange for your

settlement. How would you go about evaluating whether this is a good deal for you or

not?

What is the likely price elasticity of demand for crabs? Why?

A decrease in the demand for eggs results in a surplus of eggs at the original

equilibrium price. Explain how market forces will act to eliminate the surplus.

What does the assumption of perfect knowledge include?

Tony spends $36 per month on cookies. For him, chocolate chip cookies and peanut

butter cookies are perfect substitutes. Chocolate chip cookies are $4 per dozen and

peanut butter cookies are $3 per dozen. How many dozen of each type of cookie will

Tony buy in a given month if he wants to maximize his utility?

How would an economist go about examining the net costs of immigration? What have

recent studies suggested?

What conclusion did the 1962 University of Chicago study on the burden of the

corporate tax rate make?

What is the Earned Income Tax Credit?

In the face of gasoline prices approaching $4.00 automobile dealerships are heavily

marketing their compact cars and hybrid vehicles. However, an interesting development

is that many of these dealerships are offering their economy cars at MSRP

(manufacturers suggested retail price) without offering discounts. What do you suppose

these dealerships believe about the price elasticity of demand for these economy cars?