Finite distributed lag models are most useful for

a.) forecasting and economic policy analysis

b.) testing hypotheses and measuring economic dynamics

c.) measuring impacts and optimizing economic outcomes

d.) measuring autocorrelation and autoregressive dynamics

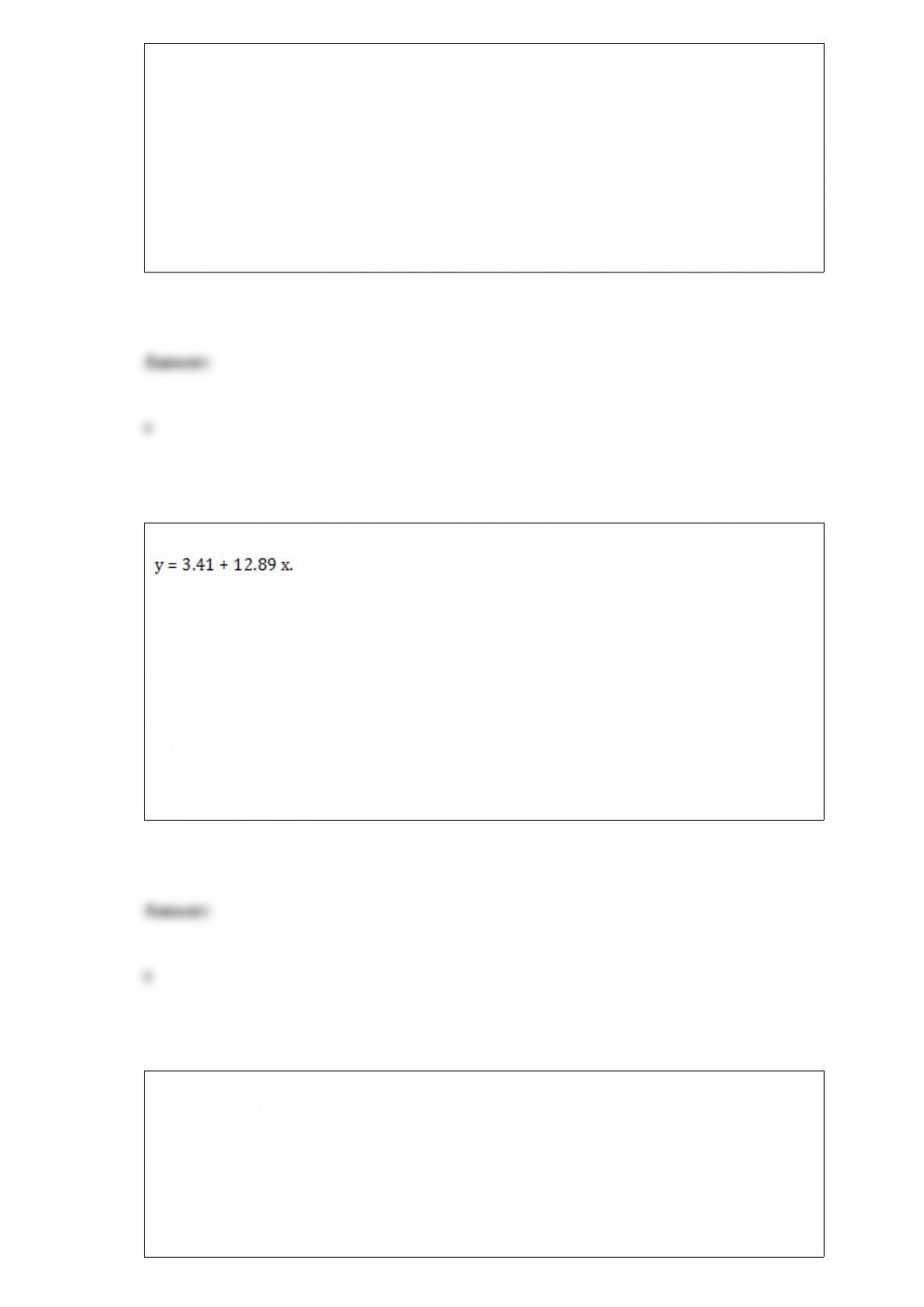

Applying the OLS model to our data give us the following regression equation:

What would the forecast value be when the independent variable is 15.0?

a.) 196.76

b.) 16.30

c.) 244.50

d.) 32.19

When are R2 and adjusted R2 equal?

a.) when the model is correctly specified

b.) when K = 1

c.) when the error terms are normally distributed

d.) when an unrestricted model is estimated

Using the notation ARDL(p,q) what does represent?

a.) the number of lagged dependent variables included as explanatory variables

b.) the number of lagged explanatory variables included

c.) the frequency of the time series

d.) the degree or integration in the error term

For which type of model does the researcher have to assume independence of irrelevant

alternatives?

a.) probit

b.) multinomial logit

c.) linear probability

d.) latent variable model

. A large company is accused of gender discrimination in wages. The following model

has been estimated from the company’s human resource information ln(WAGE) = 1.439

+ .0834 EDU + .0512 EXPER + .1932 MALE Where WAGE is hourly wage, EDU is

years of education, EXPER is years of relevant experience, and MALE indicates the

employee is male. What hypothesis would you test to determine if the discrimination

claim is valid?

a.) H0:MALE = 0 ; H1: MALE >= 0

b.) H0:MALE = EDU = EXPER = 0 ; H1: MALE ≠0 and EDU ≠0 and

EXPER ≠0

c.) H0:MALE = EDU = EXPER = 0 ; H1: MALE ≠0 or EDU ≠0 or EXPER

≠0

d.) H0:MALE =< EDU or MALE =< EXPER ; H1: MALE > EDU or MALE >

EXPER

Which of the following is NOT generally included in the study of econometrics?

a.) using economic data to estimate relationships

b.) testing economic hypotheses

c.) predicting economic outcomes

d.) developing new economic relationships.

Which type of model does not have a coefficient that varies with t or i ?

a.) a pooled model

b.) fixed effects

c.) random effects

d.) none of these

What does the T in T-ARCH stand for and when is it used?

a.) threshold, used to model asymmetric effects

b.) two stage, used to model indirect effects

c.) time, used to model time varying heteroskedasticity

d.) total, used to model total variance

Suppose there is a series, Yt, modeled by the following three equations:

yt = + et

etIt-1 ~ N(0, ht)

ht = 0+ 1e2

t-1, 0>0, 0=< 1<1

This model is classified as a(n)

a.) ARCH(1)

b.) ECM

c.) ARDL(1)

d.) VAR

What is the 4th moment of random variable x?

a.) E(x)4

b.) x / 4

c.) E(x4)

d.) (E(x4)-x4)/N

What is the null hypothesis of the Dickey-Fuller Test 2?

a.) the series is non-stationary over time

b.) the series is stationary

c.) the series is first order integrated

d.) the series are cointegrated

What is the difference between balanced and unbalanced panels?

a.) unbalanced panels have some observations missing, balanced do not

b.) balanced panels are demographically representative of the population being studied,

unbalanced are not

c.) balanced panels have an equal number of observations above and below the mean of

the dependent variable, unbalanced panels are skewed

d.) a balanced panel has T = N, an unbalanced panel has N>T or N<T

What is the difference between a VEC and a VAR?

a.) The VAR model is for only 2 series and VEC models accommodate 3 or more

variables.

b.) The VAR model is a special form of the VEC model and should be used for

nonstationary series.

c.) The VEC model is a special form of the VAR and should be used with cointegrated

series.

d.) The VAR model deals with stationary series while the VEC allows for dynamic

series.

What are the consequences of using least squares when heteroskedasticity is present?

a.) no consequences, coefficient estimates are still unbiased

b.) confidence intervals and hypothesis testing are inaccurate due to inflated standard

errors

c.) all coefficient estimates are biased for variables correlated with the error term

d.) it requires very large sample sizes to get efficient estimates

How are AR and exponential smoothing models similar?

a.) both use only previous observations of the same variable for forecasting future

values

b.) both incorporate past information in the form of moving averages of multiple

varaibles over time

c.) both incorporate information on current values of all relevant variables

d.) they generate forecasts with identically distributed expected values

If a scatter plot of the data reveals an inverted U shape, what data transformation would

allow it to be estimated with simple linear regression?