1) When the market price is below the equilibrium price, suppliers are unable to sell all

they want to sell.

a.True

b.False

2) Patent protection is one way to deal with technology spillovers.

a.True

b.False

3) A firm that is a natural monopoly

a.is not likely to be concerned about new entrants eroding its monopoly power.

b.is taking advantage of diseconomies of scale.

c.would experience a lower average total cost if more firms entered the market.

d.All of the above are correct.

4) Vertical equity in taxation refers to the idea that people

a.in unequal conditions should be treated differently.

b.in equal conditions should pay equal taxes.

c.should pay taxes based on the benefits they receive from the government.

d.should pay a proportional tax rather than a progressive tax.

5) Suppose that a university charges students a $100 “tax” to register for business

classes. The next year the university raises the “tax” to $150. The deadweight loss from

the “tax” triples.

a.True

b.False

6) Adam Smith asserted that a person should never attempt to make at home

a.what it will cost him more to make than to buy.

b.any good in which that person does not have an absolute advantage.

c.any luxury good.

d.any necessity.

7) In the short run, which of the following rates of growth in the money supply is likely

to lead to the highest level of unemployment in the economy?

a.1 percent per year

b.2 percent per year

c.3 percent per year

d.4 percent per year

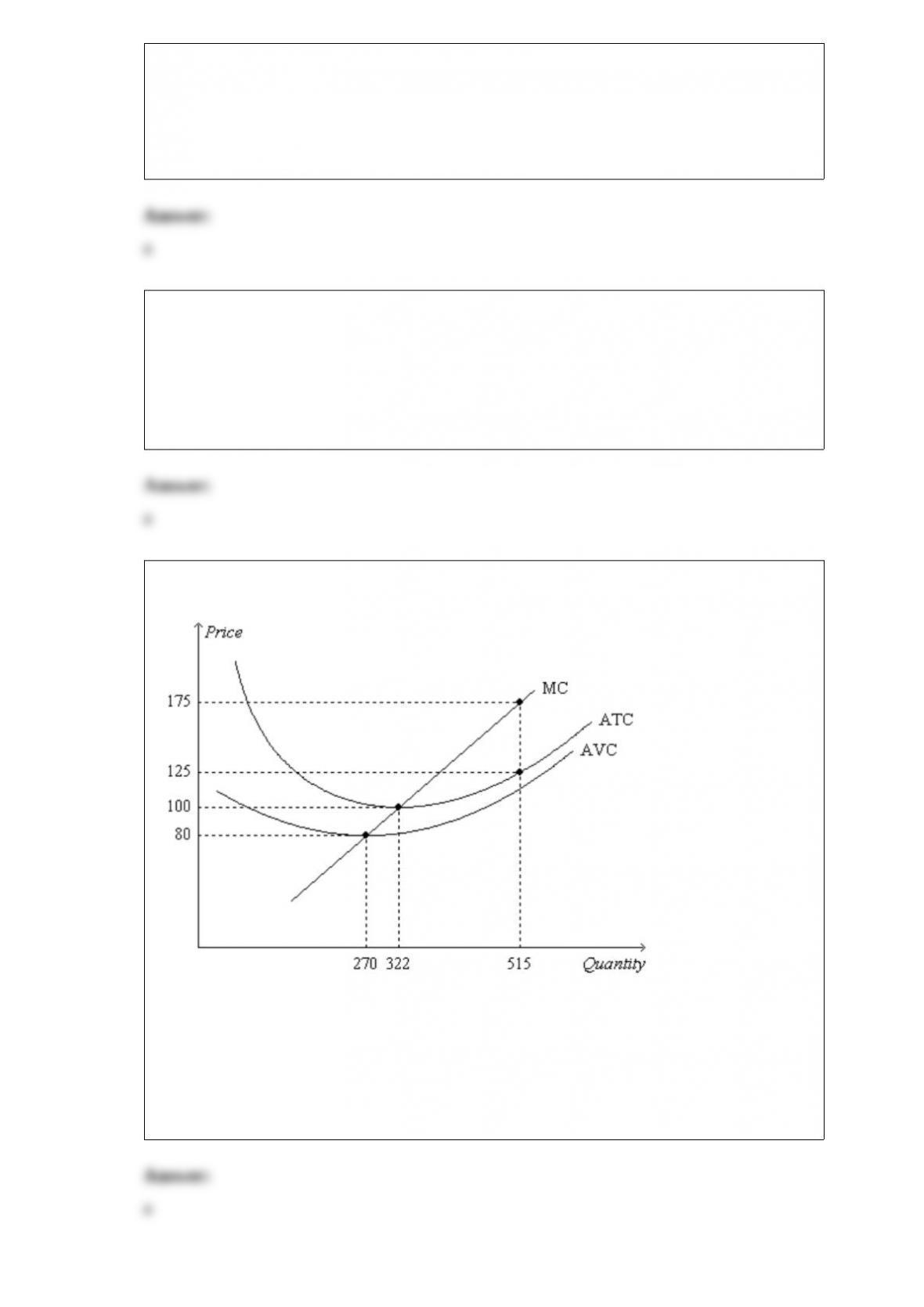

8) Figure 14-7

In the short run, the firm‘s maximum profit (or minimum loss) is the same at which of

the following pairs of prices?

a. $65 and $75

b. $75 and $85

c. $80 and $100

d. $125 and $175

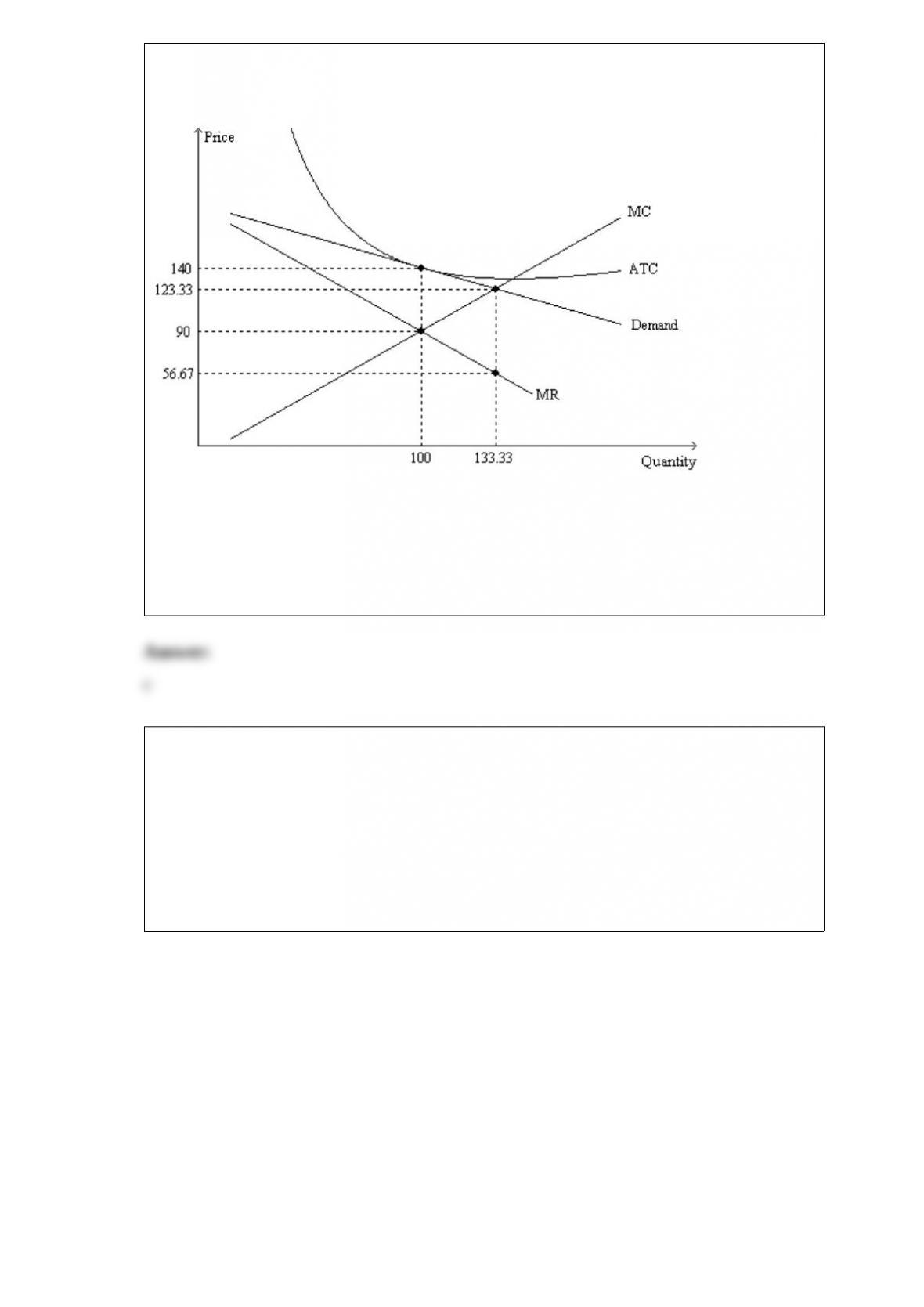

9) Figure 16-9

The figure is drawn for a monopolistically-competitive firm.

When the firm is maximizing its profit, the markup over marginal cost amounts to

a. $16.67.

b. $33.33.

c. $50.00.

d. $66.66.

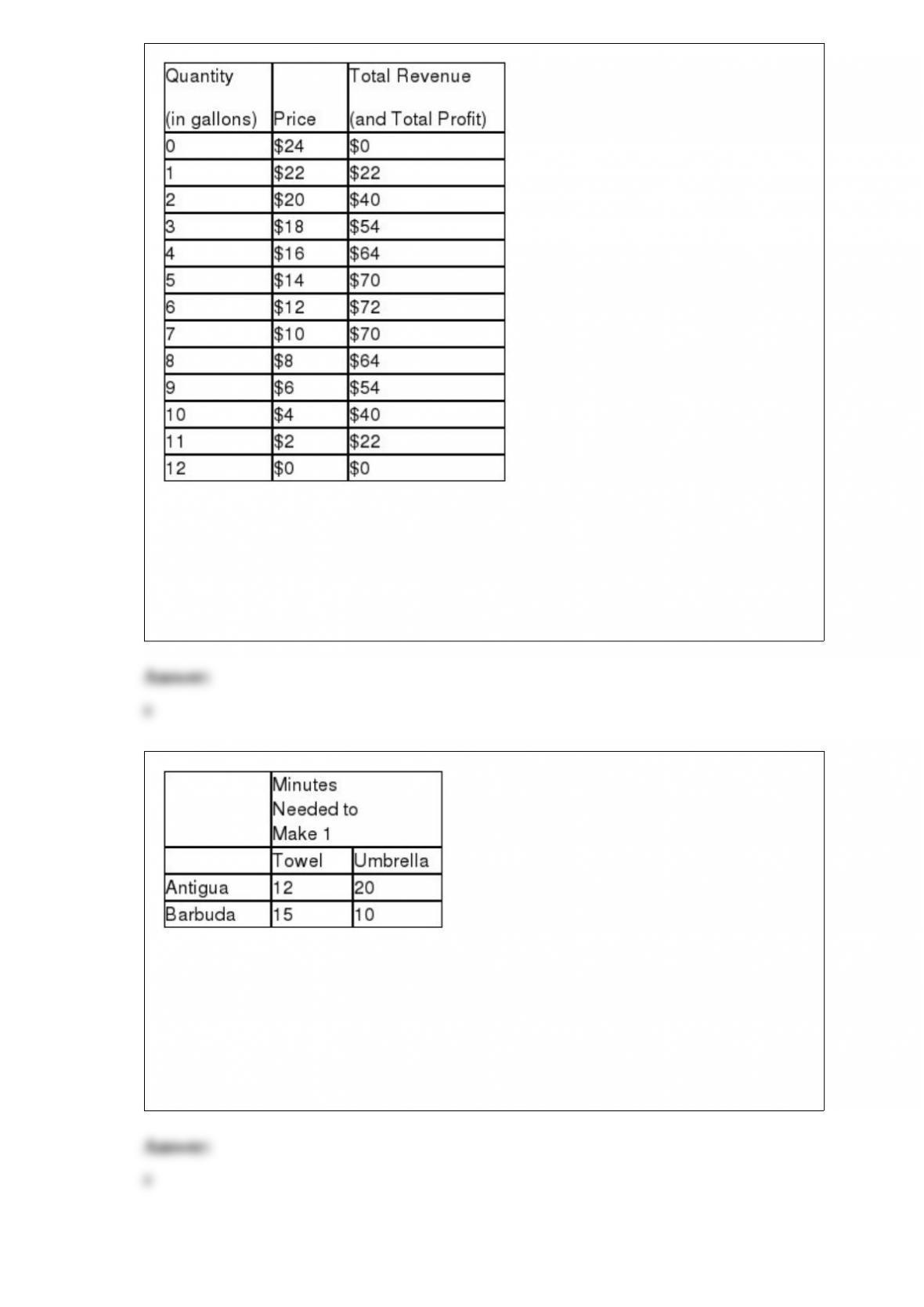

10) Table 17-3

Imagine a small town in a remote area where only two residents, Maria and Miguel,

own dairies that produce milk that is safe to drink. Each week Maria and Miguel work

together to decide how many gallons of milk to produce. They bring milk to town and

sell it at whatever price the market will bear. To keep things simple, suppose that Maria

and Miguel can produce as much milk as they want without cost so that the marginal

cost is zero. The weekly town demand schedule and total revenue schedule for milk is

shown in the table below:

Refer to Table 17-3. If this market for milk were perfectly competitive instead of

monopolistic, how many gallons of milk would be produced and sold?

a.12 gallons

b.8 gallons

c.6 gallons

d.0 gallons

11) Antigua has a comparative advantage in the production of

a.towels and Barbuda has a comparative advantage in the production of umbrellas.

b.umbrellas and Barbuda has a comparative advantage in the production of towels.

c.both goods and Barbuda has a comparative advantage in the production of neither

good.

d.neither good and Barbuda has a comparative advantage in the production of both

goods.

12) The difference between social cost and private cost is a measure of the

a.loss in profit to the seller as the result of a negative externality.

b.cost of an externality.

c.cost reduction when the negative externality is eliminated.

d.cost incurred by the government when it intervenes in the market.

13) Refer to Figure 9-23. Consumer surplus with free trade is

a. $75.

b. $150.

c. $200.

d. $300.

14) A compensation scheme that pays salespeople a percentage of the sales they make is

attempting to reward

a.work effort.

b.loyalty to the firm.

c.years of schooling.

d.years of experience.

15) When a country that imported a particular good abandons a free-trade policy and

adopts a no-trade policy,

a.producer surplus increases and total surplus increases in the market for that good.

b.producer surplus increases and total surplus decreases in the market for that good.

c.producer surplus decreases and total surplus increases in the market for that good.

d.producer surplus decreases and total surplus decreases in the market for that good.

16) Scenario 18-8

Suppose the following events occur in the market for university economics professors.

Event 1: A recession in the U.S. economy lowers the opportunity cost of going to

graduate school in economics to become a university economics professor.

Event 2: A decreasing number of students in U.S. primary and secondary schools

decreases the number of students entering college, decreasing the output price of

university economics professors’ services.

Refer to Scenario 18-8. As a result of these two events, holding all else constant, the

equilibrium wages of university economics professors will

a.increase.

b.decrease.

c.not change.

d.It is not possible to determine what will happen to the equilibrium wage.