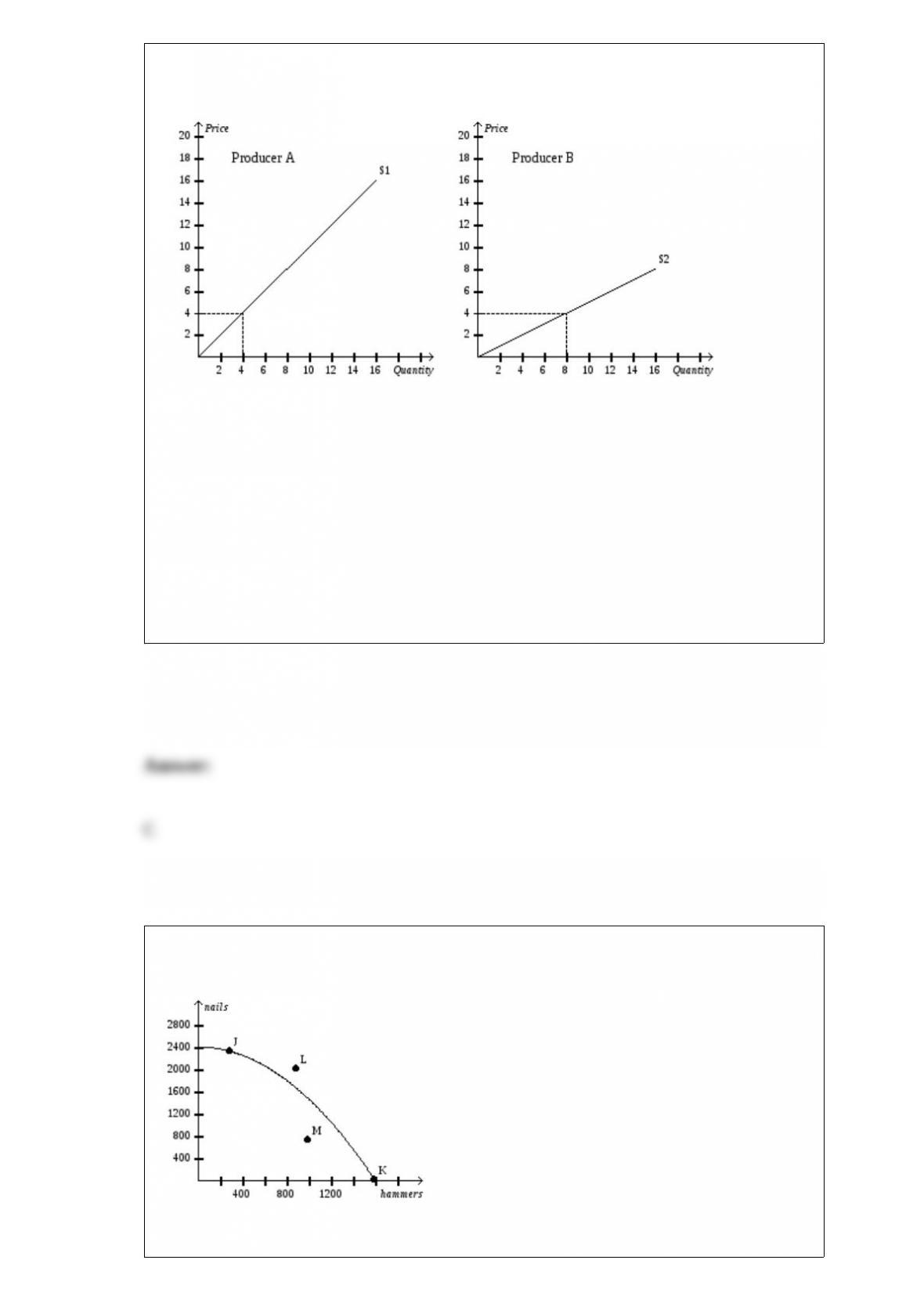

Figure 4-12

Refer to Figure 4-12. If Producer A and Producer B are the only producers in the

market, then the market quantity supplied when the price is $4 is

a. 4 units.

b. 8 units.

c. 12 units.

d. 16 units.

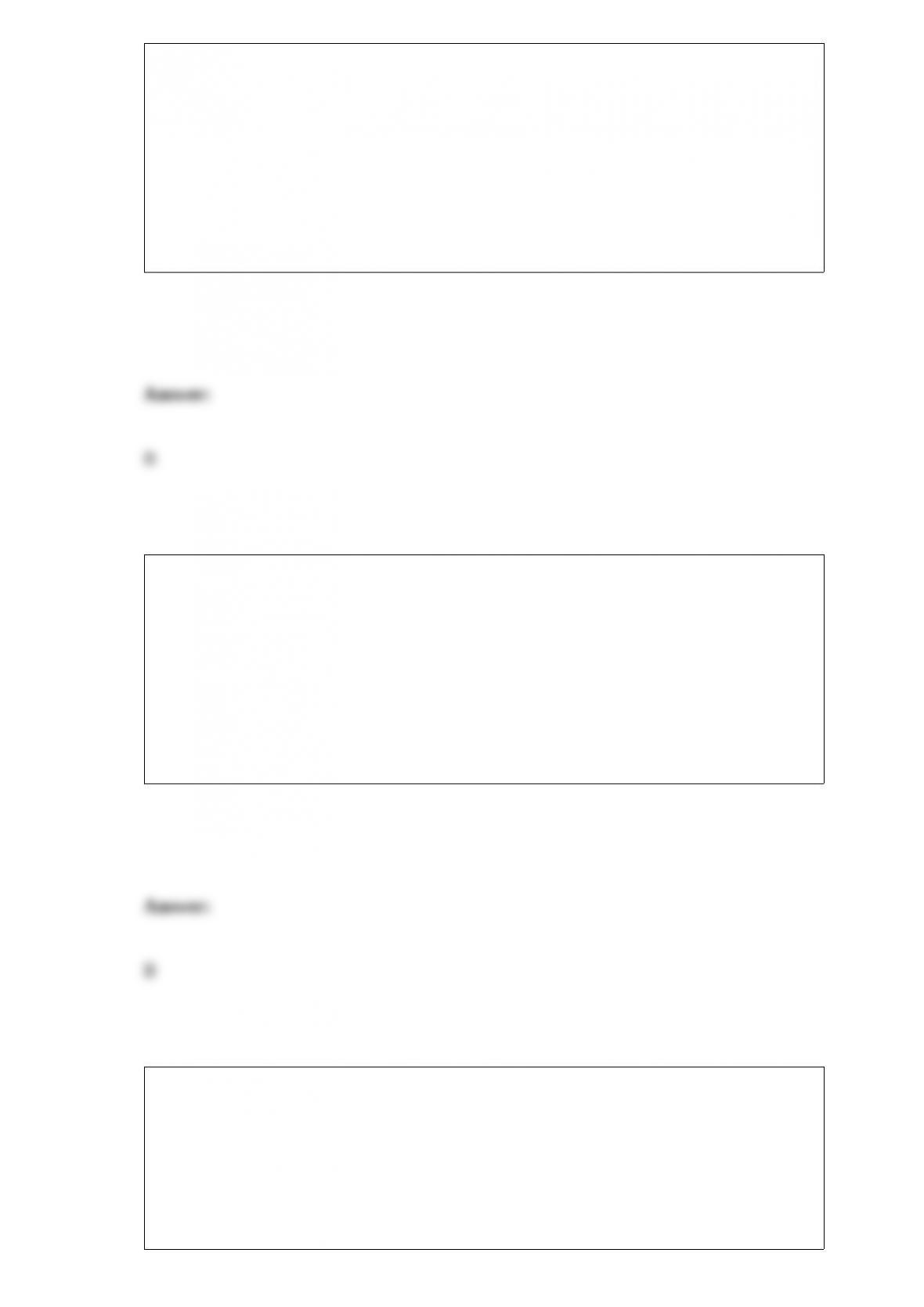

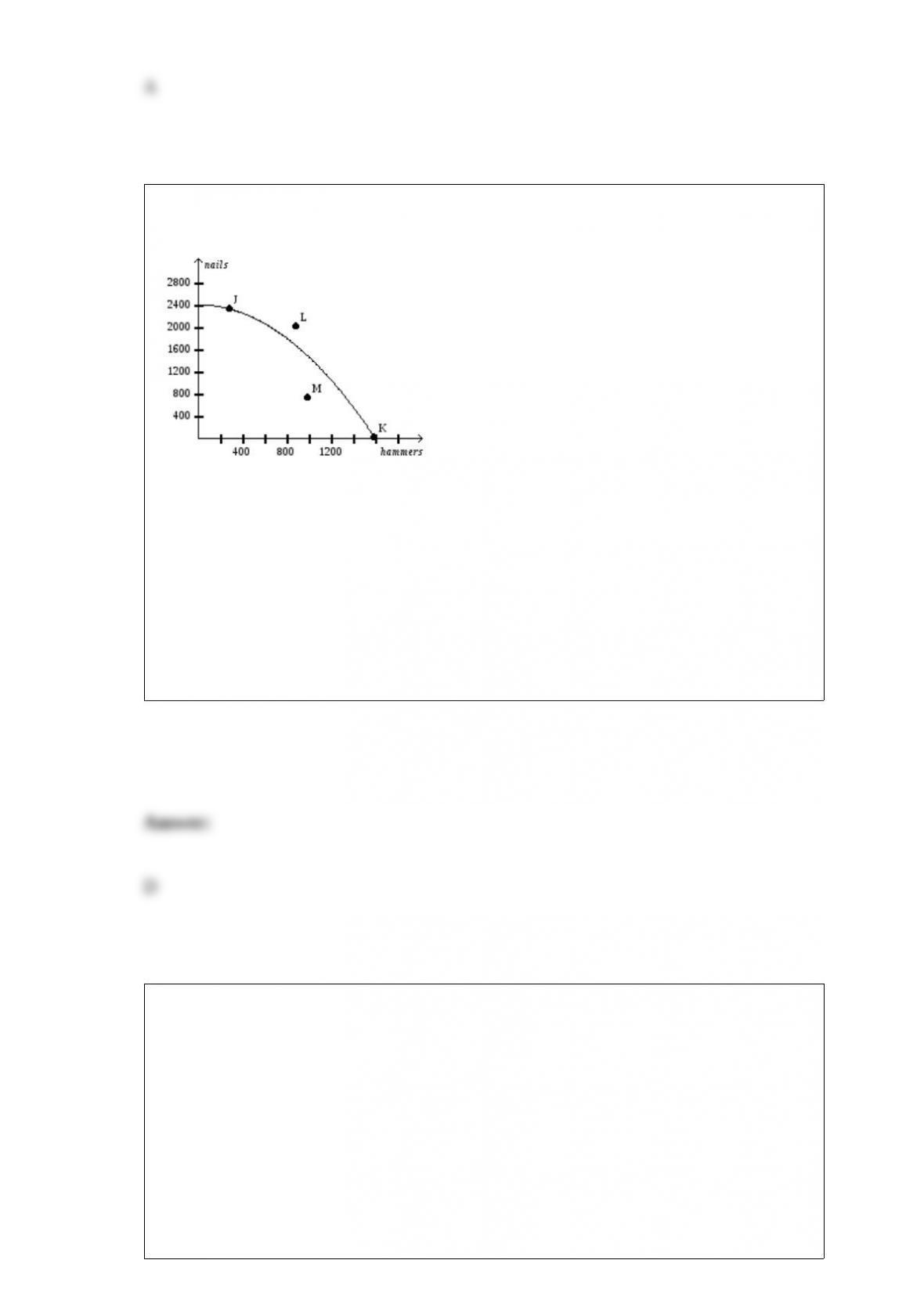

Figure 2-7

Refer to Figure 2-7. For this economy, as more and more hammers are produced, the

opportunity cost of an additional hammers produced, in terms of nails,

a. remains constant.

b. increases.

c. decreases.

d. This cannot be determined from the graph.

The consumer price index is used to

a. convert nominal GDP into real GDP.

b. turn dollar figures into meaningful measures of purchasing power.

c. characterize the types of goods and services that consumers purchase.

d. measure the quantity of goods and services that the economy produces.

Which U.S. president, when asked why he had proposed a tax cut, responded by saying

“To stimulate the economy. Don”t you remember your Economics 101?”

a. Dwight D. Eisenhower

b. John F. Kennedy

c. Ronald Reagan

d. Bill Clinton

The misperceptions theory of the short-run aggregate supply curve says that if the price

level is higher than people expected, then some firms believe that the relative price of

what they produce has

a. decreased, so they increase production.

b. decreased, so they decrease production.

c. increased, so they increase production.

d. increased, so they decrease production.

Suppose the economy is in long-run equilibrium. In a short span of time, there is a

sharp increase in the minimum wage, a major new discovery of oil, a large influx of

immigrants, and new environmental regulations that raise the cost of electricity

production. In the short run

a. the price level will rise and real GDP will fall.

b. the price level will fall and real GDP will rise.

c. the price level and real GDP will both stay the same.

d. All of the above are possible.

Scenario 11-3

Sue Holloway was an accountant in 1944 and earned $12,000 that year. Her son, Josh

Holloway, is an accountant today and he earned $210,000 in 2008. The price index was

17.6 in 1944 and 184 in 2008.

Refer to Scenario 11-3. Josh Holloway’s 2008 income in 1944 dollars is

a. $11,931.82.

b. $20,086.96.

c. $1,985,454.55.

d. $2,195,454.55.

The Eye of Horus incense company has $10 million in cash which it has accumulated

from retained earnings. It was planning to use the money to build a new factory.

Recently, the rate of interest has increased. The increase in the rate of interest should

a. not influence the decision to build the factory because The Eye of Horus doesn’t have

to borrow any money.

b. not influence the decision to build the factory because its stockholders are expecting

a new factory.

c. make it more likely that The Eye of Horus will build the factory because a higher

interest rate will make the factory more valuable.

d. make it less likely that The Eye of Horus will build the factory because the

opportunity cost of the $10 million is now higher.

In the long run, a decrease in the money supply growth rate

a. shifts both the long-run and the short-run Phillips curves right.

b. shifts the long-run Phillips curve left and the short-run Phillips curve right.

c. shifts the long-run Phillips curve right and the short-run Phillips curve left.

d. None of the above is correct.

Tax cuts shift aggregate demand

a. right as do increases in government spending.

b. right while increases in government spending shift aggregate demand left.

c. left as do increases in government spending.

d. left while increases in government spending shift aggregate demand right.

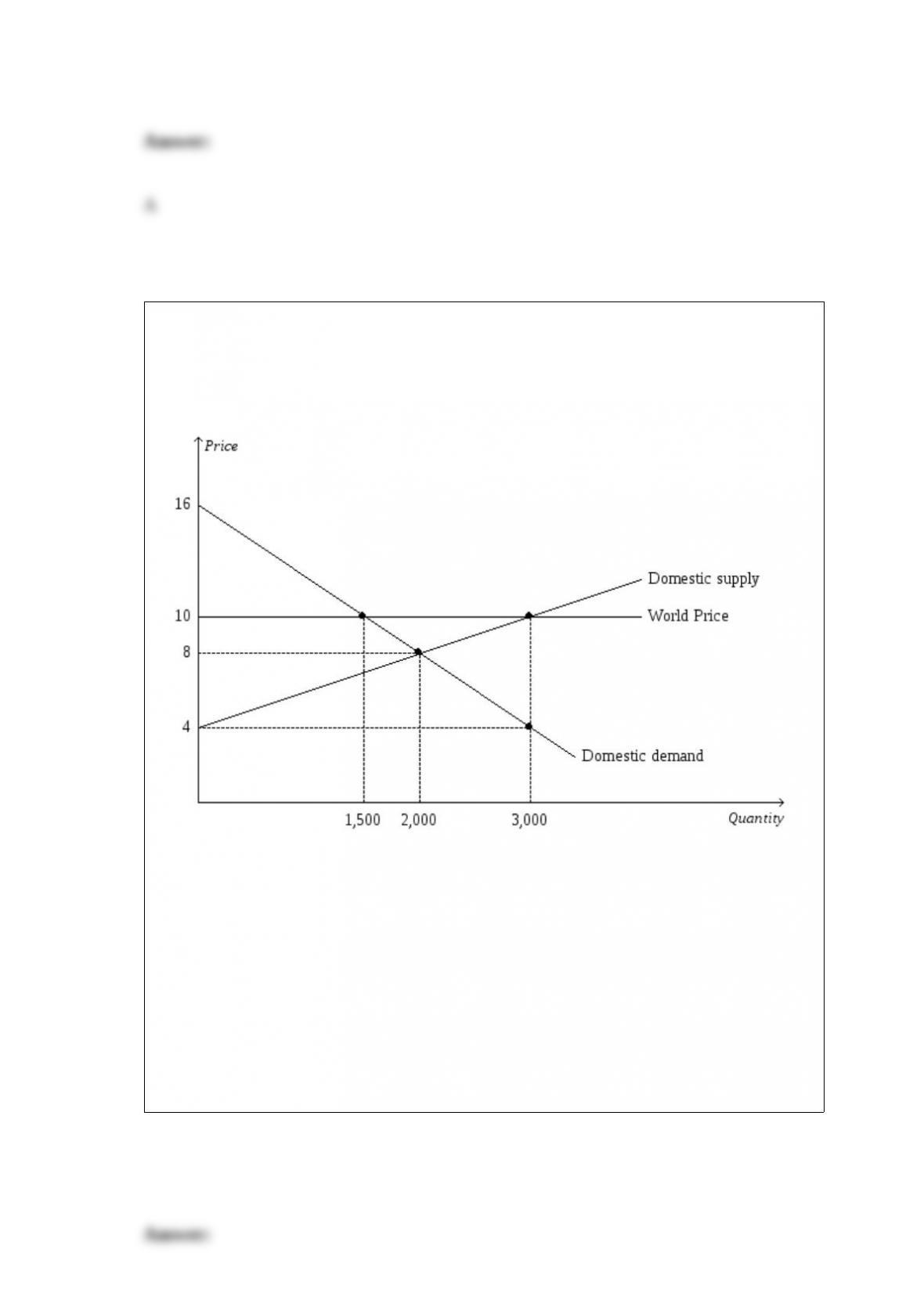

Figure 9-20

The figure illustrates the market for rice in Vietnam.

Refer to Figure 9-20. Given that Vietnam is a small country, it is apparent from the

figure that

a. Vietnam will export rice if trade is allowed.

b. Vietnam will import rice if trade is allowed.

c. Vietnam has nothing to gain either by importing or exporting rice.

d. the world price will fall if Vietnam begins to allow its citizens to trade with other

countries.

Figure 2-7

Refer to Figure 2-7. Inefficient production is represented by which point(s)?

a. K, M

b. L

c. L, M

d. M

Susan switches from going to Speedy Lube for an oil change to changing the oil in her

car herself. Which of the following is correct? The value of changing the oil is

a. included in GDP whether Susan pays Speedy Lube to change it or changes it herself.

b. included in GDP if Susan pays Speedy Lube to change it but not if she changes it

herself.

c. included in GDP if Susan changes it herself, but not if she pays Speedy Lube to

change it.

d. not included in GDP whether Susan pays Speedy lube to change it or she changes it

herself.

Which of the following items is the one type of household expenditure that is

categorized as investment rather than consumption?

a. spending on education

b. the purchase of stocks and bonds

c. the purchase of a new house

d. the purchase of durable goods such as stoves and washing machines

An increase in the U.S. government budget deficit shifts the

a. demand for loanable funds right and decreases investment spending.

b. supply of loanable funds right and increases investment spending.

c. supply of loanable funds left and decreases investment spending.

d. None of the above is correct.

The nominal interest rate is 6 percent and the real interest rate is 2 percent. What is the

inflation rate?

a. 3 percent.

b. 4 percent.

c. 8 percent.

d. 12 percent.

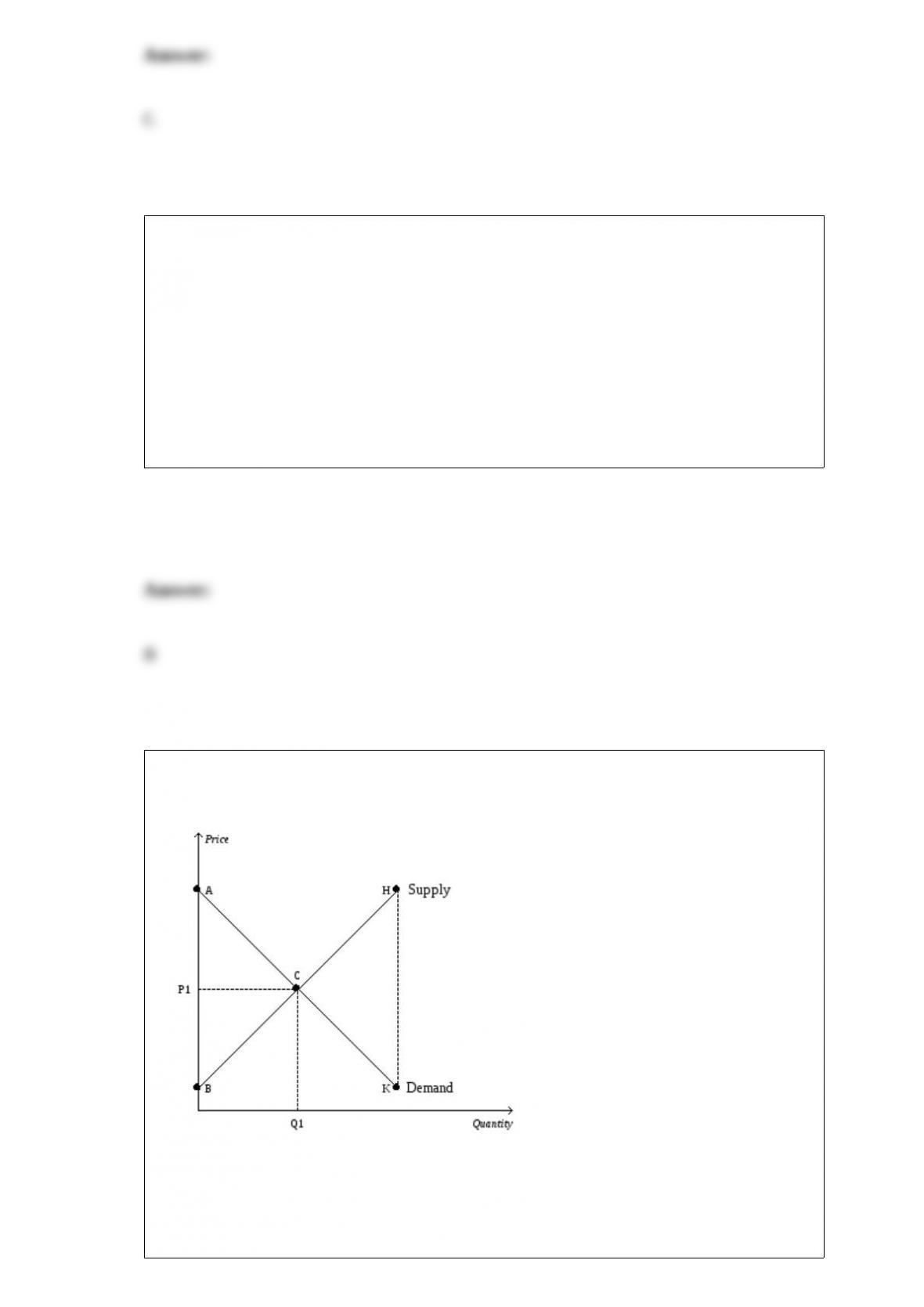

Figure 7-21

Refer to Figure 7-21. Buyers who value this good less than the equilibrium price are

represented by which line segment?

a. AC.

b. CK.

c. BC.

d. CH.

The Fed sets the interest that borrowers pay on loans from

a. the discount window and the term auction facility

b. the discount window but not the term auction facility

c. the term auction facility but not the discount window

d. neither the discount window nor the term auction facility

James offers you $1,000 today or $X in 7 years. If the interest rate is 4.5 percent, then

you would prefer to take the $1,000 today if and only if

a. X < 1,045.00.

b. X < 1,188.89.

c. X < 1,266.67.

d. X < 1,360.86.

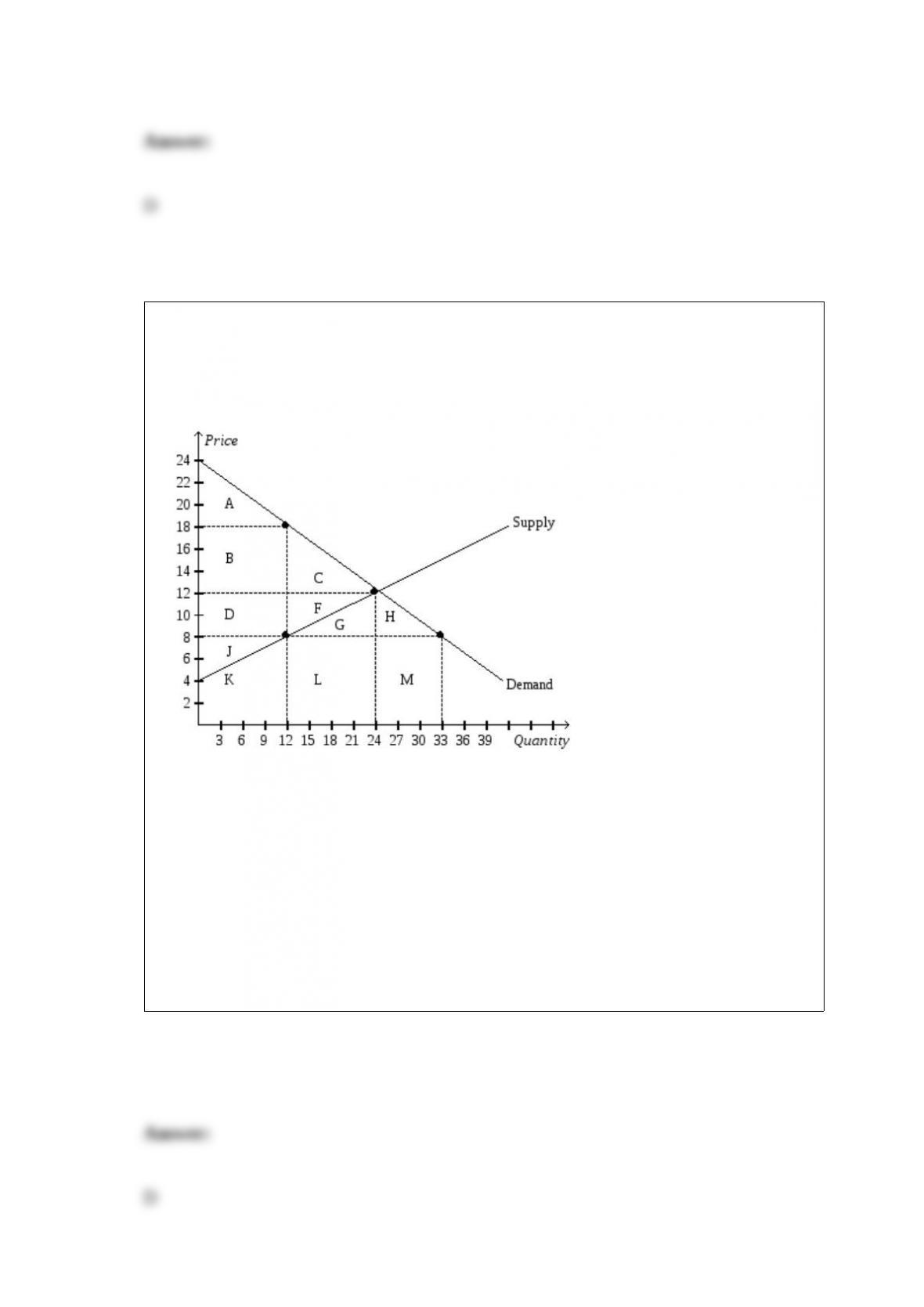

Figure 8-8

Suppose the government imposes a $10 per unit tax on a good.

Refer to Figure 8-8. The decrease in consumer and producer surpluses that is not offset

by tax revenue is the area

a. C.

b. F.

c. G.

d. C+F.

Changes in the interest rate help explain

a. only the slope of, not shifts of aggregate demand.

b. only shifts of, not the slope of aggregate demand.

c. both the slope of and shifts of aggregate demand.

d. neither the slope nor shifts of aggregate demand.

Bolivia had a smaller budget deficit in 2003 than in 2002. Other things the same, we

would expect this reduction in the budget deficit to have

a. increased both interest rates and investment.

b. increased interest rates and decreased investment.

c. decreased interest rates and increased investment.

d. decreased both interest rates and investment.

Unemployment that results because the number of jobs available in some labor markets

may be insufficient to give a job to everyone who wants one is called

a. the natural rate of unemployment.

b. cyclical unemployment.

c. structural unemployment.

d. frictional unemployment.

For economists, substitutes for laboratory experiments often come in the form of

a. natural experiments offered by history.

b. untested theories.

c. “rules of thumb” and other such conveniences.

d. reliance upon the wisdom of elders in the economics profession.

Which of the following is always measured in prices from a base-year?

a. both nominal and real GDP

b. nominal but not real GDP

c. real but not nominal GDP

d. neither nominal nor real GDP

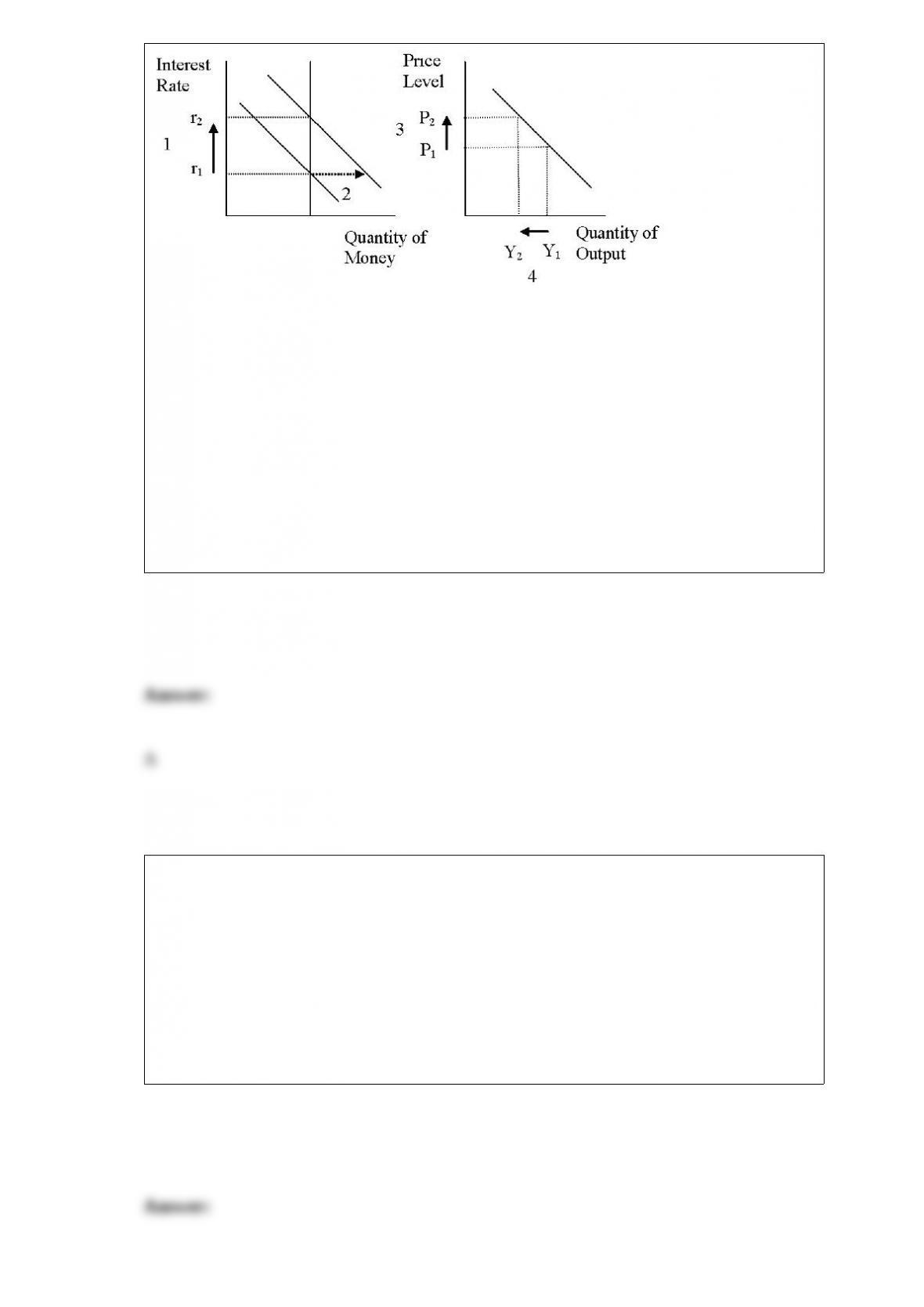

Which of the following sequences best explains the negative slope of the

aggregate-demand curve?

a. price level demand for money equilibrium interest rate

quantity of goods and services demanded

b. price level demand for money equilibrium interest rate

quantity of goods and services demanded

c. price level demand for money equilibrium interest rate

quantity of goods and services demanded

d. price level equilibrium interest rate demand for money

quantity of goods and services demanded

Figure 21-3.

Refer to Figure 21-3. What quantity is represented by the vertical line on the left-hand

graph?

a. the supply of money

b. the demand for money

c. the rate of inflation

d. the quantity of bonds that was most recently sold or purchased by the Federal

Reserve

If the reserve ratio is 4 percent, then $81,250 of new money can be generated by

a. $325 of new reserves.

b. $3,250 of new reserves.

c. $20,312.50 of new reserves.

d. $2,031,250 of new reserves.

The government buys new weapons systems. The manufacturers of weapons pay their

employees. The employees spend this money on goods and services. The firms from

which the employees buy the goods and services pay their employees. This sequence of

events illustrates

a. the accelerator effect.

b. the multiplier effect.

c. the chain effect.

d. the bandwagon effect.

If the government removes a binding price floor from a market, then the price received

by sellers will

a. decrease, and the quantity sold in the market will decrease.

b. decrease, and the quantity sold in the market will increase.

c. increase, and the quantity sold in the market will decrease.

d. increase, and the quantity sold in the market will increase.

A tax places a wedge between the price buyers pay and the price sellers receive.

Consumer surplus can be measured as the area between the demand curve and the

equilibrium price.

If a country has a higher level of productivity than another, then it also has a higher

level of real GDP.

Suppose Ecuador imposes a tariff on imported bananas. If the increase in producer

surplus is $50 million, the reduction in consumer surplus is $150 million, and the

deadweight loss of the tariff is $30 million, then the tariff generates $130 million in

revenue for the government.

Microeconomics and macroeconomics are closely intertwined.

Why do many economists advocate a consumption tax rather than an income tax?

A price floor set above the equilibrium price is binding.

Macroeconomic statistics include GDP, the inflation rate, the unemployment rate, retail

sales, and the trade deficit.

The financial system coordinates investment and saving, which are important

determinants of long-run real GDP.

Economists study how people make decisions.

The results of a 2008 Los Angeles Times poll suggest that a significant majority of

Americans believe that free international trade helps the American economy.

The goal of President Obama’s stimulus package and increased government spending

following the deep economic downturn in 2008 and 2009 was to reduce inflation.

Net capital outflow represents the quantity of dollars supplied in the foreign-currency

exchange market.

Since economists cannot use natural experiments offered by history, they must use

carefully constructed laboratory experiments instead.

A change in the money supply changes only nominal variables in the long run.

Today, unions play a larger role in Europe than they do in the U.S.

When demand is relatively elastic, the deadweight loss of a tax is larger than when

demand is relatively inelastic.

When the Soviet Union began breaking up in the late 1980s, cigarettes began replacing

the ruble as the medium of exchange even though the ruble was legal tender. The

cigarettes provide an example of commodity money.