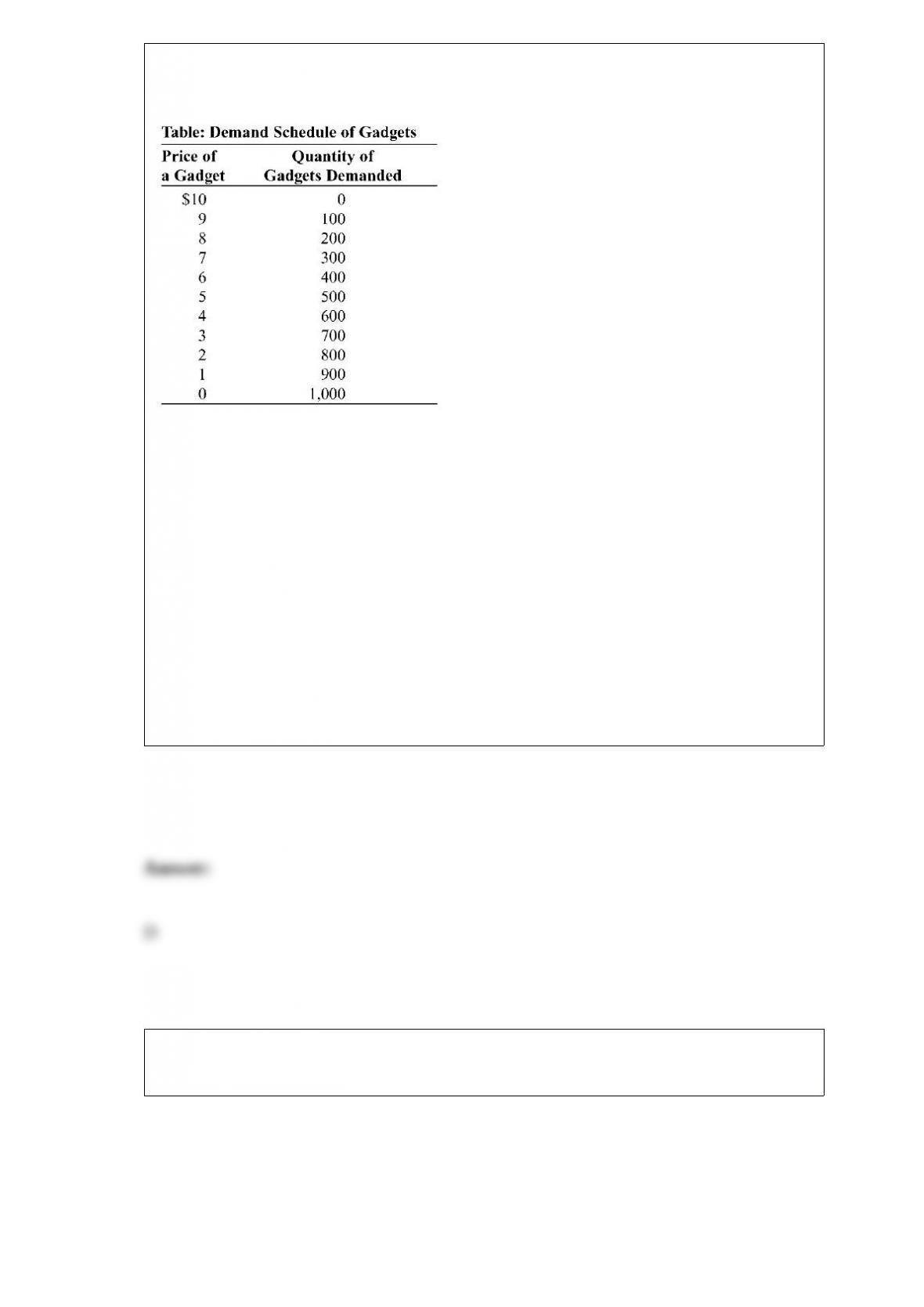

(Table: Demand Schedule for Gadgets) Look at the table Demand Schedule for

Gadgets. The market for gadgets consists of two producers, Margaret and Ray. Each

firm can produce gadgets with no marginal cost or fixed cost. If these two producers

formed a cartel and acted to maximize total industry profits, total industry output would

be _____ and the price would be _____.

A) 1,000; $10

B) 100; $9

C) 400; $6

D) 500; $5

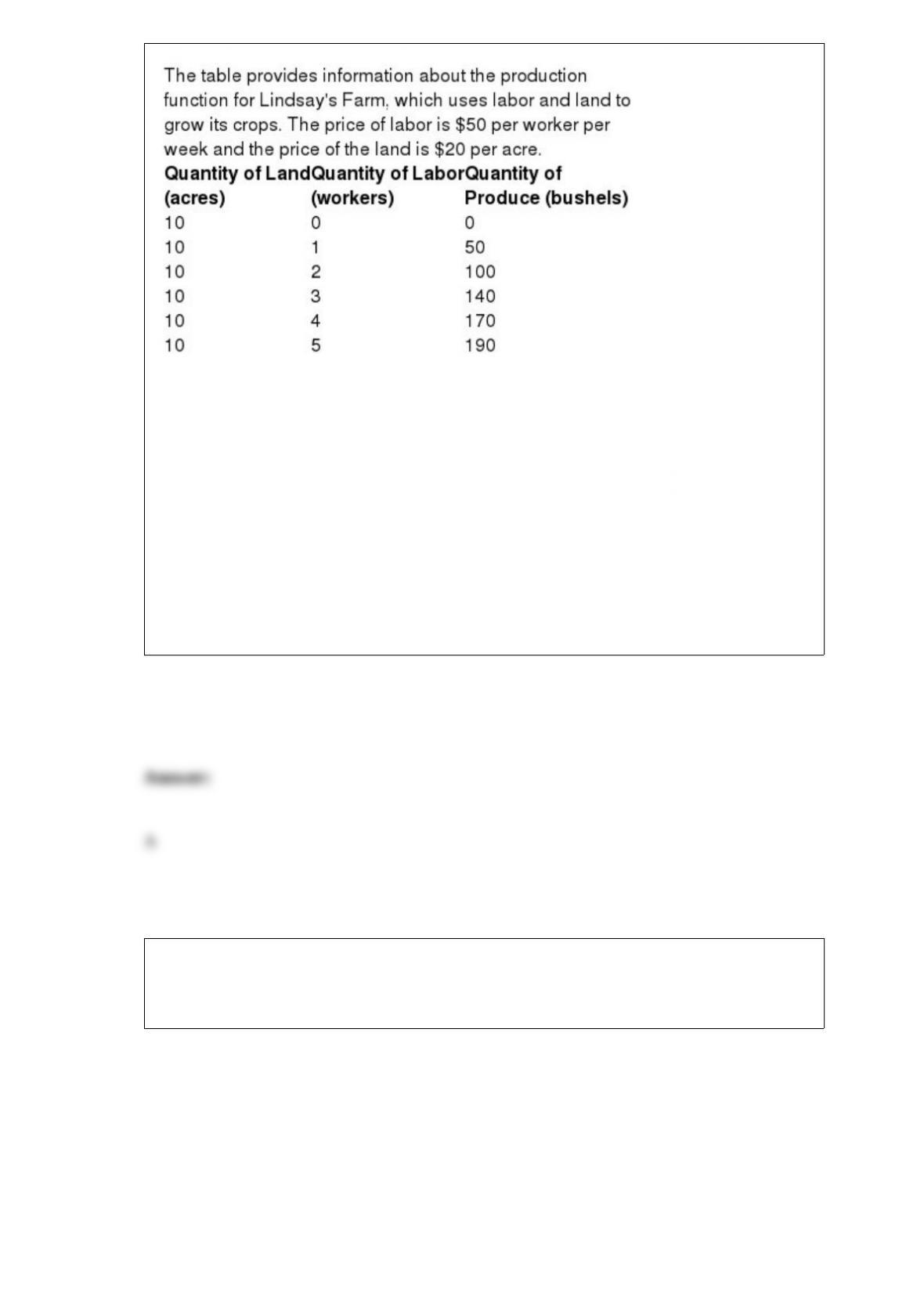

Table: Lindsay’s Farm

(Table: Bonnie’s Production Function for Good Z) Look at the table Bonnie’s

Production Function for Good Z. Suppose Bonnie spends $300 per month to rent the

building, $100 per month on insurance, and $100 per worker per month. Given this

information, Bonnie’s monthly fixed costs equal:

A) $400.

B) $300.

C) $500.

D) $100.

Figure: The Profit-Maximizing Output and Price

(Figure: The Profit-Maximizing Output and Price) Look at the figure The

Profit-Maximizing Output and Price. Assume that there are no fixed costs and AC =

MC = $200. At the profit-maximizing output and price for a perfectly competitive

industry, producer surplus is:

A) $0.

B) $200.

C) $1,600.

D) $3,200.

Table: The Cost and Benefit of Producing Gadgets Quantity of Gadgets Total Cost

Total Benefit 0 $100 $ 0 1 105 200 2 110 215 3 115 225 4 120 230 5 125 233

(Table: The Cost and Benefit of Producing Gadgets) Look at the table The Cost and

Benefit of Producing Gadgets. How many gadgets should you produce?

Quantity of Gadgets Total Cost Total Benefit

0 $100 $ 0

1 105 200

2 110 215

3 115 225

4 120 230

5 125 233

A) two

B) three

C) four

D) five

Overt collusion exists if:

A) firms agree openly on price and output and they jointly make other decisions aimed

at achieving monopoly profits.

B) smaller firms in an industry tacitly agree to charge the same price as the largest firm.

C) competition among a large number of small firms generates a stable market price.

D) competition among a large number of small firms generates similar but slightly

different prices.

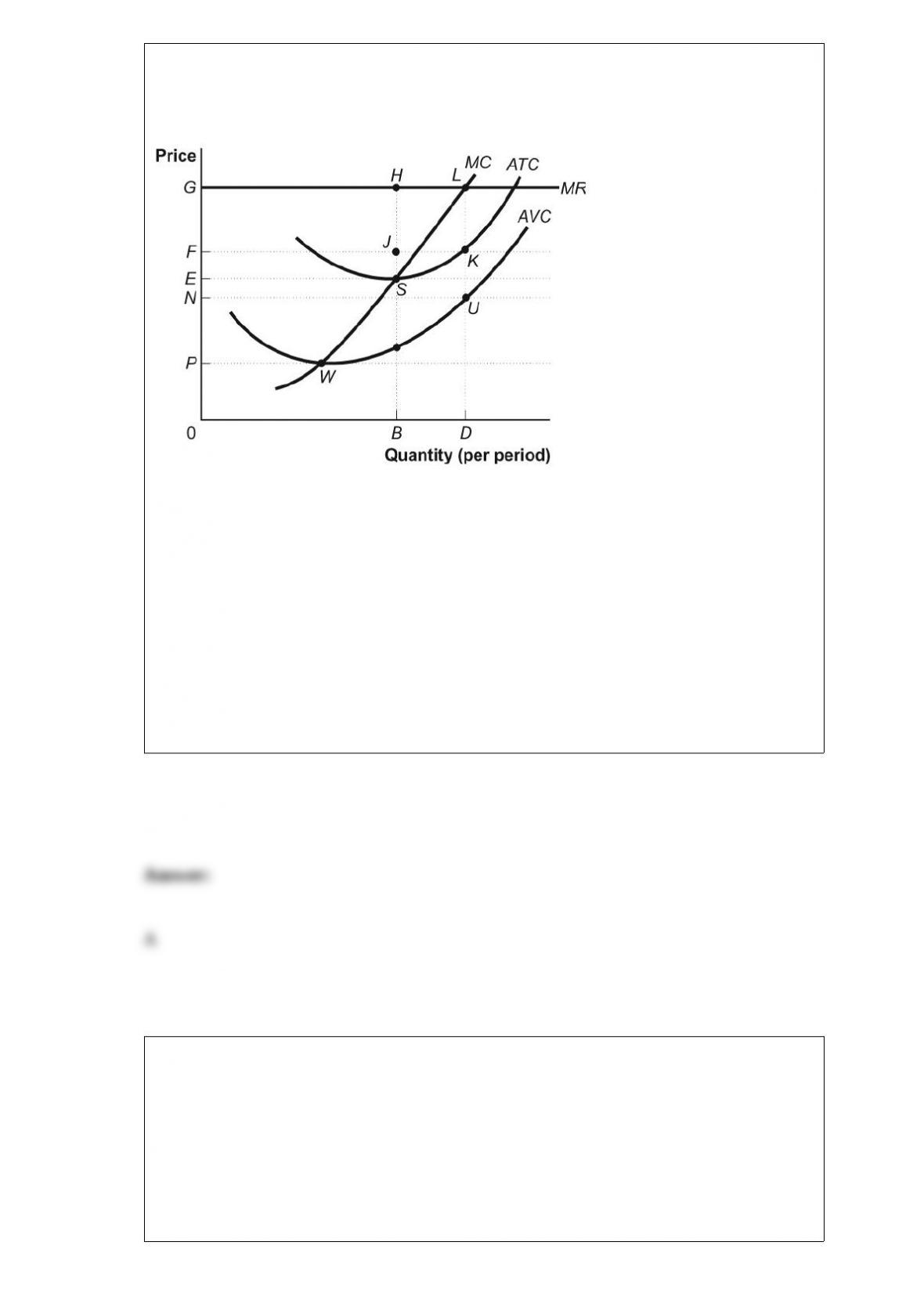

Figure: A Perfectly Competitive Firm in the Short Run

(Figure: A Perfectly Competitive Firm in the Short Run) Look at the figure A Perfectly

Competitive Firm in the Short Run. The firm’s total revenue from the sale of its most

profitable level of output is:

A) 0GLD.

B) 0GHB.

C) BH.

D) DL.

When perfect competition prevails, which of the following characteristics of firms are

we likely to observe?

A) None of them ever has diminishing marginal returns.

B) They all try to operate where price equals average variable cost.

C) They all try to operate where price equals total cost.

D) They are all price takers.

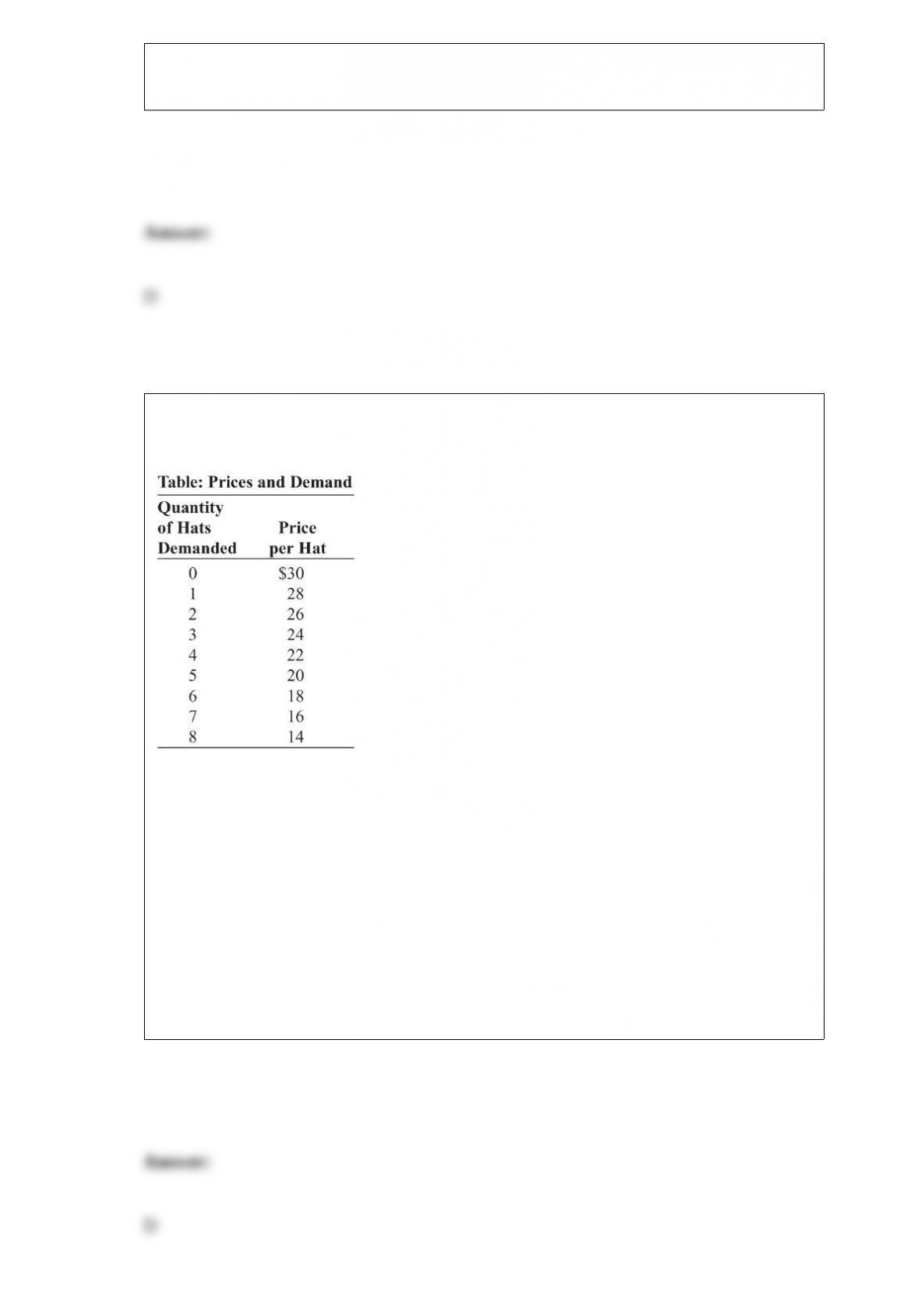

(Table: Prices and Demand) Look at the table Prices and Demand. The New Orleans

Saints have a monopoly on Saints logo hats. The marginal cost of producing a hat is

$18. How much is consumer surplus at the Saint’s profit-maximizing output?

A) $24

B) $18

C) $12

D) $9

If the combination of two goods occurs at a point of tangency between the budget line

and an indifference curve:

A) utility has been maximized.

B) some available income has not been spent.

C) utility can be decreased by consuming more of both goods.

D) utility can be increased by consuming more of one good and less of the other.

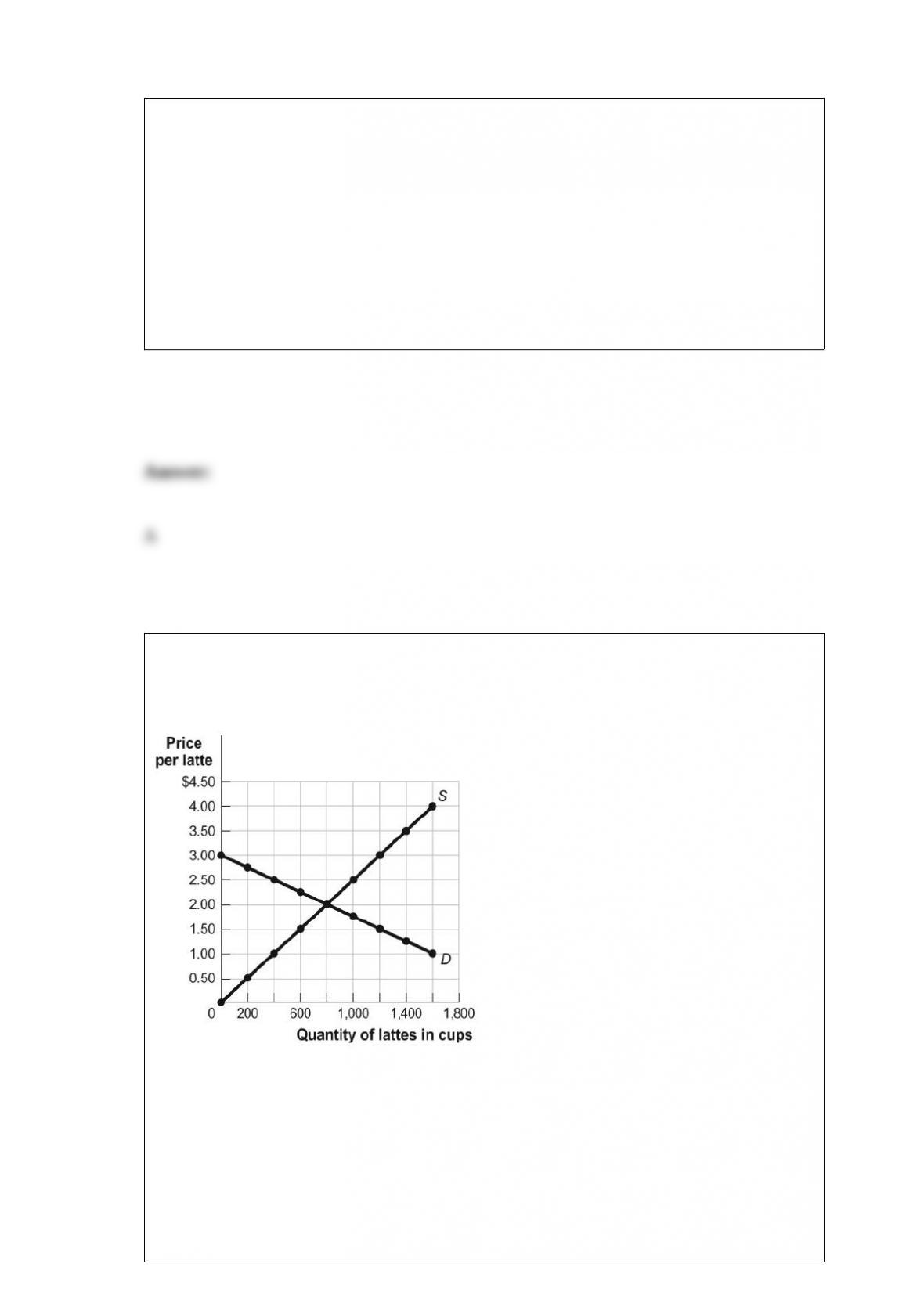

Figure: The Market for Lattes

(Figure: The Market for Lattes) Look at the figure The Market for Lattes. What is the

price elasticity of demand between $2 and $2.50 per cup, using the midpoint formula?

A) 1.00

B) 1.29

C) 2.51

D) 3.00

Which of the following statements is TRUE?

A) The value of the marginal product of labor equals the marginal product of labor

times price.

B) The value of the marginal product of labor equals a one-unit change in a factor

divided by the change in total revenue.

C) Marginal cost equals change in total revenue divided by the one-unit change in a

factor.

D) The value of the marginal product of labor equals the change in the quantity of a

factor times the price of the factor.

Oscar’s Flower Shop maximizes profits by hiring four workers in a perfectly

competitive labor market. The workers and their value of the marginal product of labor

are Noe, $40; Barbara, $35; Calvin, $27; and Diana, $15. According to the marginal

productivity theory of income distribution, which of the following statements is TRUE?

A) In equilibrium, each worker is paid his or her value of the marginal product of labor.

B) Each worker is paid a wage equal to the highest value of the marginal product of

labor(i.e., $40).

C) Each worker is paid $15.

D) We need to know the product price before we can figure out the wage rate.

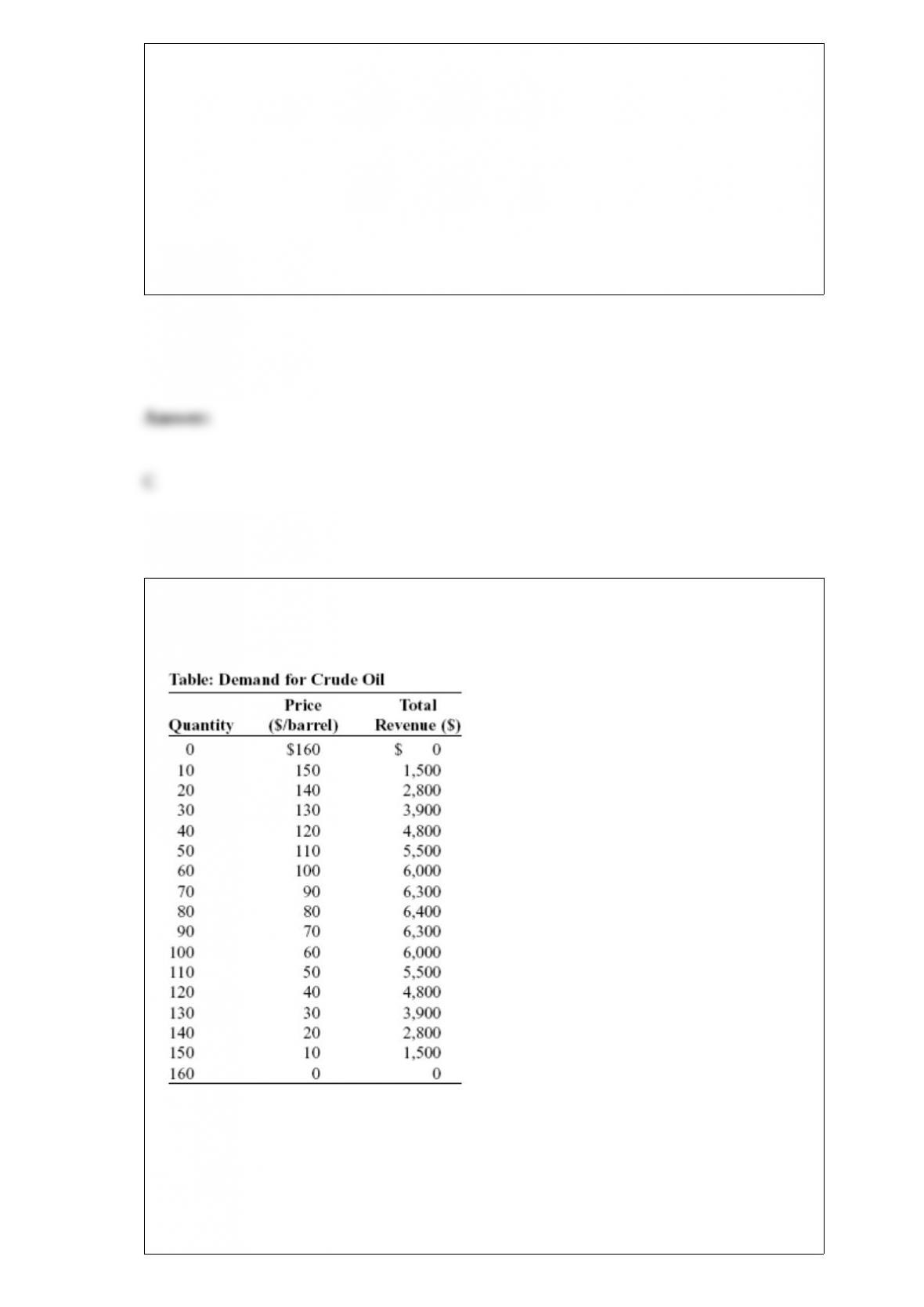

(Table: Demand for Crude Oil) Look at the table Demand for Crude Oil. Assume that

the crude oil industry is a duopoly and the marginal cost and fixed cost of producing

crude oil equal zero. Suppose that the two firms are maximizing industry profit and

splitting the profit evenly. If both firms decide to cheat and produce 10 more barrels

each, industry output will be _____ barrels.

A) 100

B) 120

C) 110

D) 160

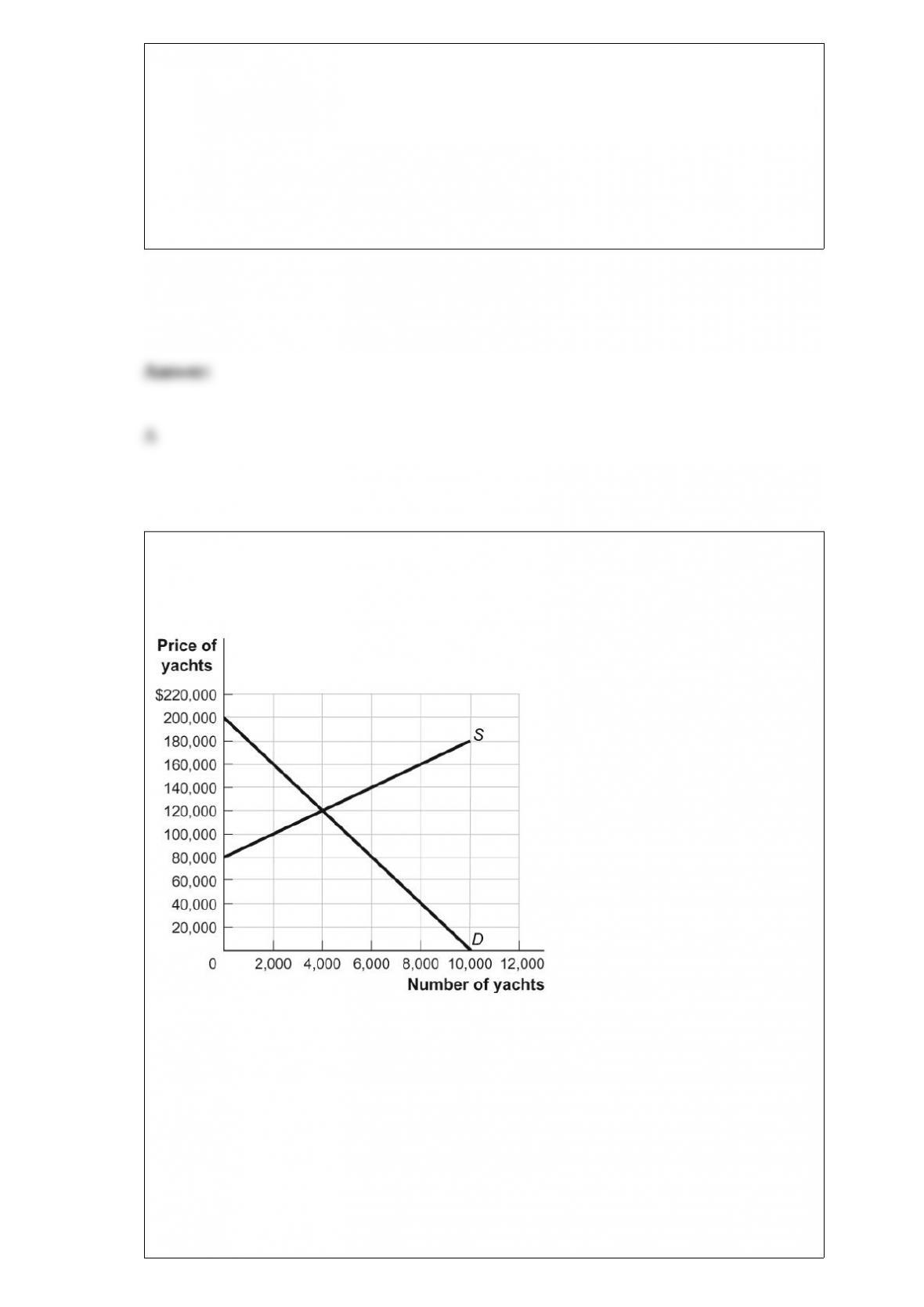

Figure: The Market for Yachts

(Figure: The Market for Yachts) Look at the figure The Market for Yachts. A quota of

_____ will bring about the same price and output in the market for yachts as would an

excise tax of $60,000.

A) 2,000

B) 3,000

C) 4,000

D) The answer is impossible to determine.

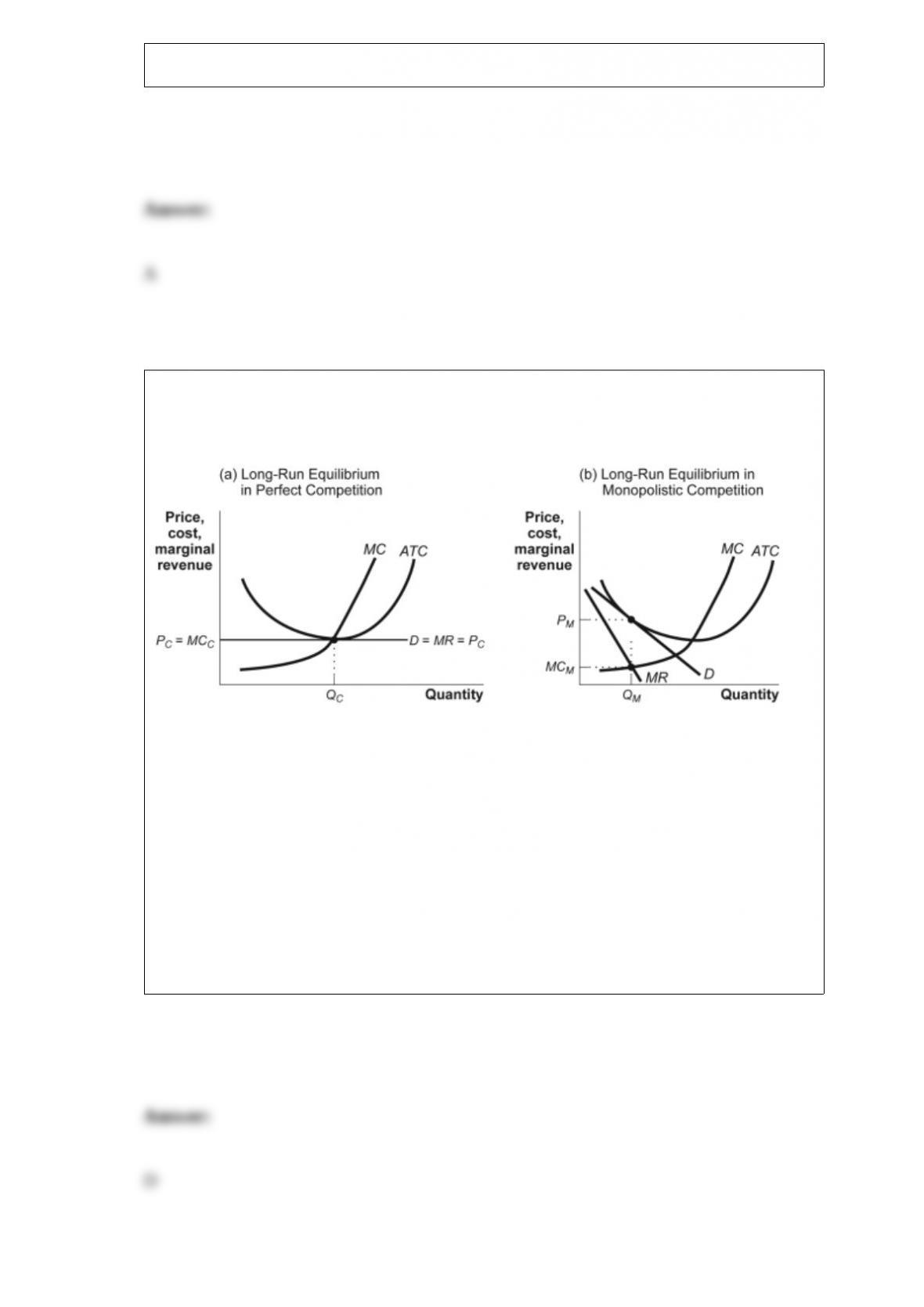

Figure: Comparing Long-Run Equilibriums

(Figure: Comparing Long-Run Equilibriums) In the figure Comparing Long-Run

Equilibriums, which of the following statements is TRUE?

A) Firms in the market structure shown in panel (a) cannot have excess profits in the

long run, but those in panel (b) can.

B) Both panels show markets that have few interdependent firms.

C) Both panels show markets that produce identical products.

D) Both panels show markets that have many firms.

An economy is said to have a comparative advantage in the production of a good if it

can produce that good:

A) with more resources than another economy.

B) with a higher opportunity cost than another economy.

C) outside its production possibilities curve.

D) at a lower opportunity cost than another economy.

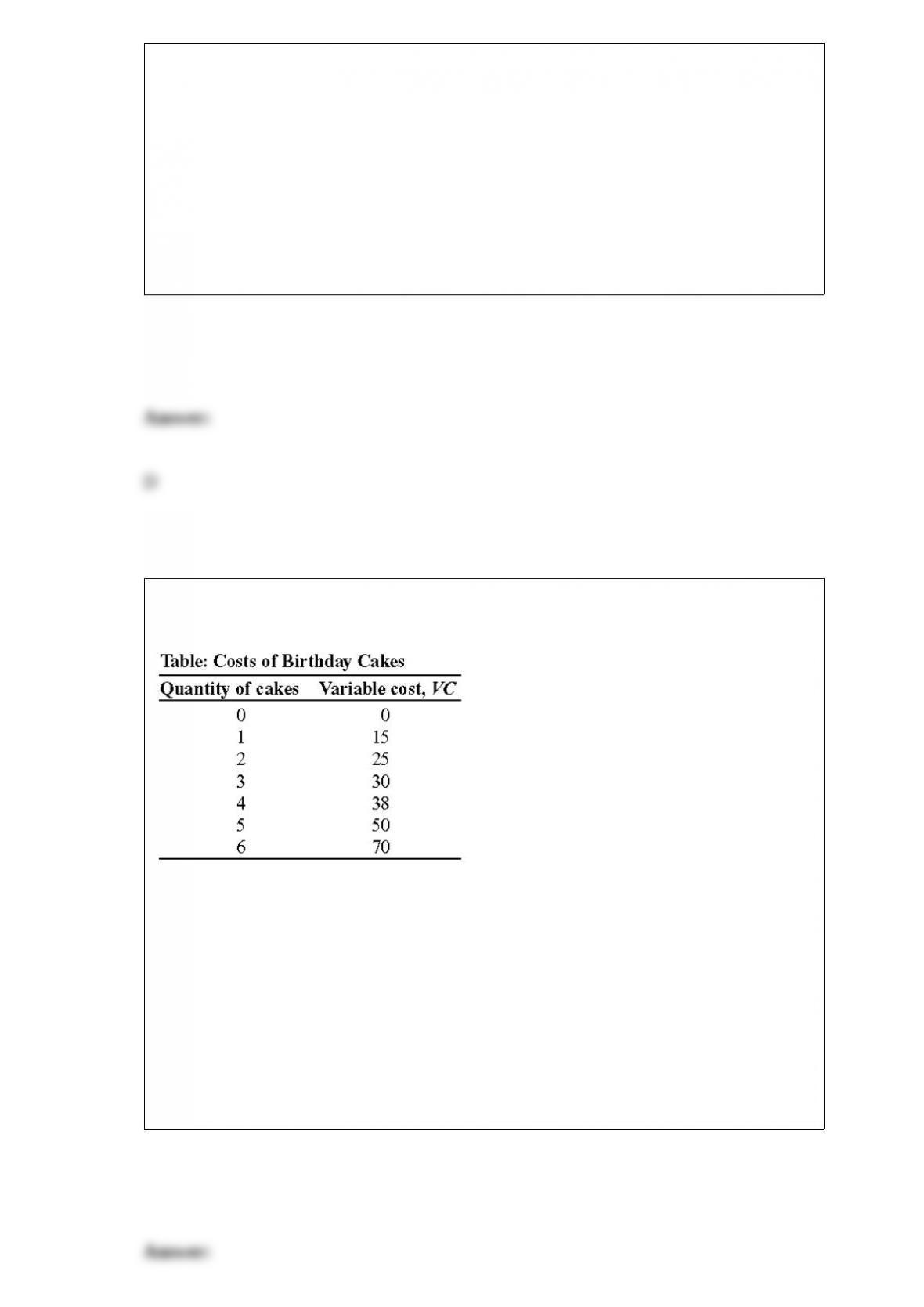

(Table: Costs of Birthday Cakes) Look at the table Costs of Birthday Cakes. Assume

that fixed costs are $10. The minimum average total cost occurs at output of:

A) 6.

B) 5.

C) 3.

D) 2.

Figure: Equilibrium in the Labor Market

(Figure: Equilibrium in the Labor Market) In the figure Equilibrium in the Labor

Market, a decrease in the price of the good produced, when everything else stays the

same, will lead to a(n) _____ in the equilibrium quantity of labor and a(n) _____ in the

equilibrium price of labor.

A) increase; increase

B) decrease; increase

C) increase; decrease

D) decrease; decrease

Quantity controls set below the equilibrium quantity cause all of the following

EXCEPT:

A) incentives for illegal activities.

B) missed opportunities in the form of mutually beneficial transactions that don’t occur.

C) the supply price of the quantity transacted exceeding the demand price of the

quantity transacted.

D) quota rents.

Assume the price of a tradable emissions permit for a ton of sulfur dioxide is $150.

Which of the following is INCORRECT?

A) A firm that buys permits has an incentive to limit pollution to the point at which the

marginal benefit of emissions is equal to $150.

B) A firm that has more permits than it plans to use has an incentive to limit pollution to

the point at which the marginal benefit of emissions is equal to $150.

C) The opportunity cost of emitting a ton of sulfur dioxide is $75 for all firms.

D) The opportunity cost of emitting a ton of sulfur dioxide is $150 for all firms.

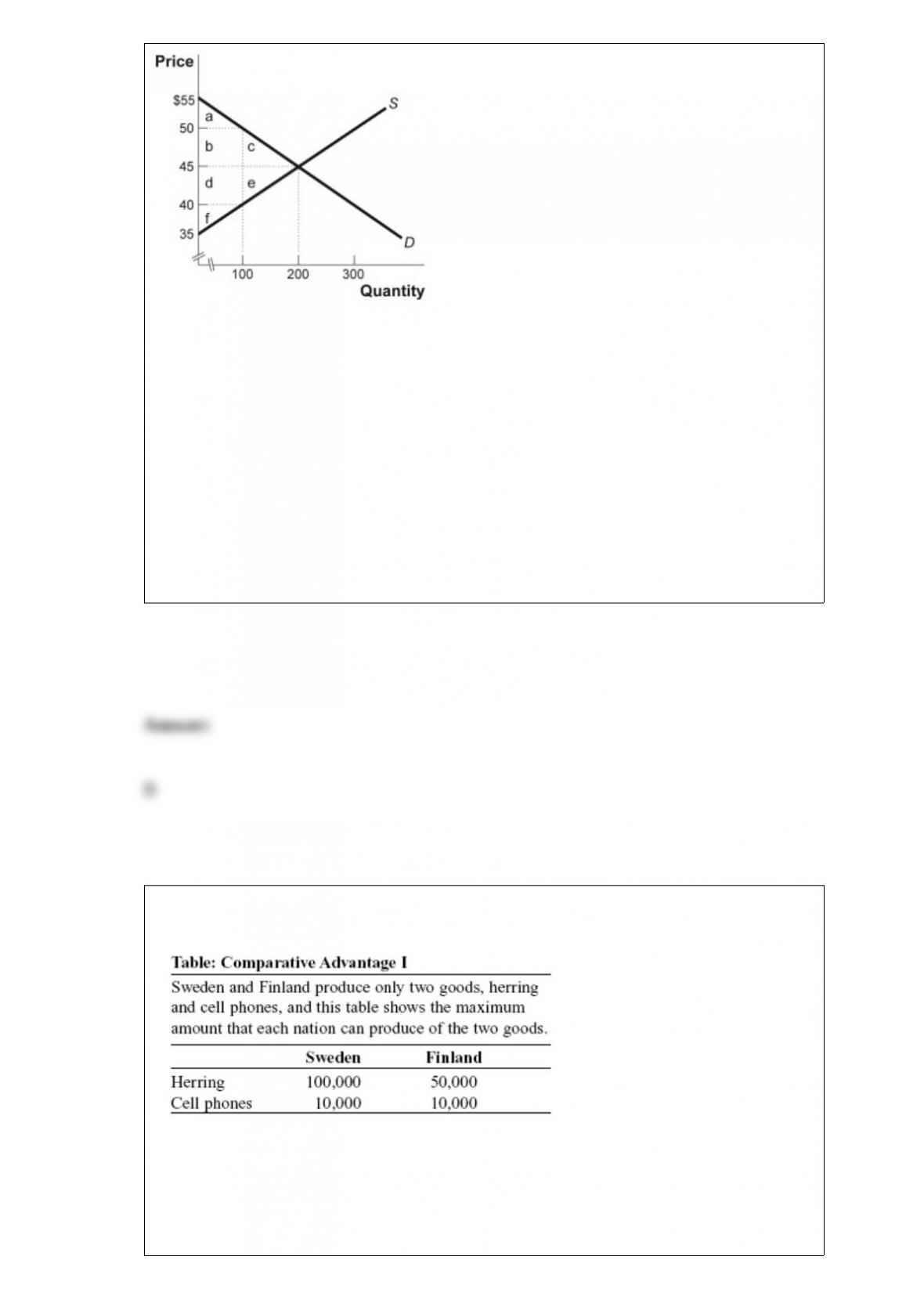

Figure: Consumer and Producer Surplus

(Figure: Consumer and Producer Surplus) Look at the figure Consumer and Producer

Surplus. If the price is held above equilibrium, consumer surplus _____ and total

surplus _____.

A) increases; decreases

B) decreases; stays the same

C) increases; stays the same

D) decreases; decreases

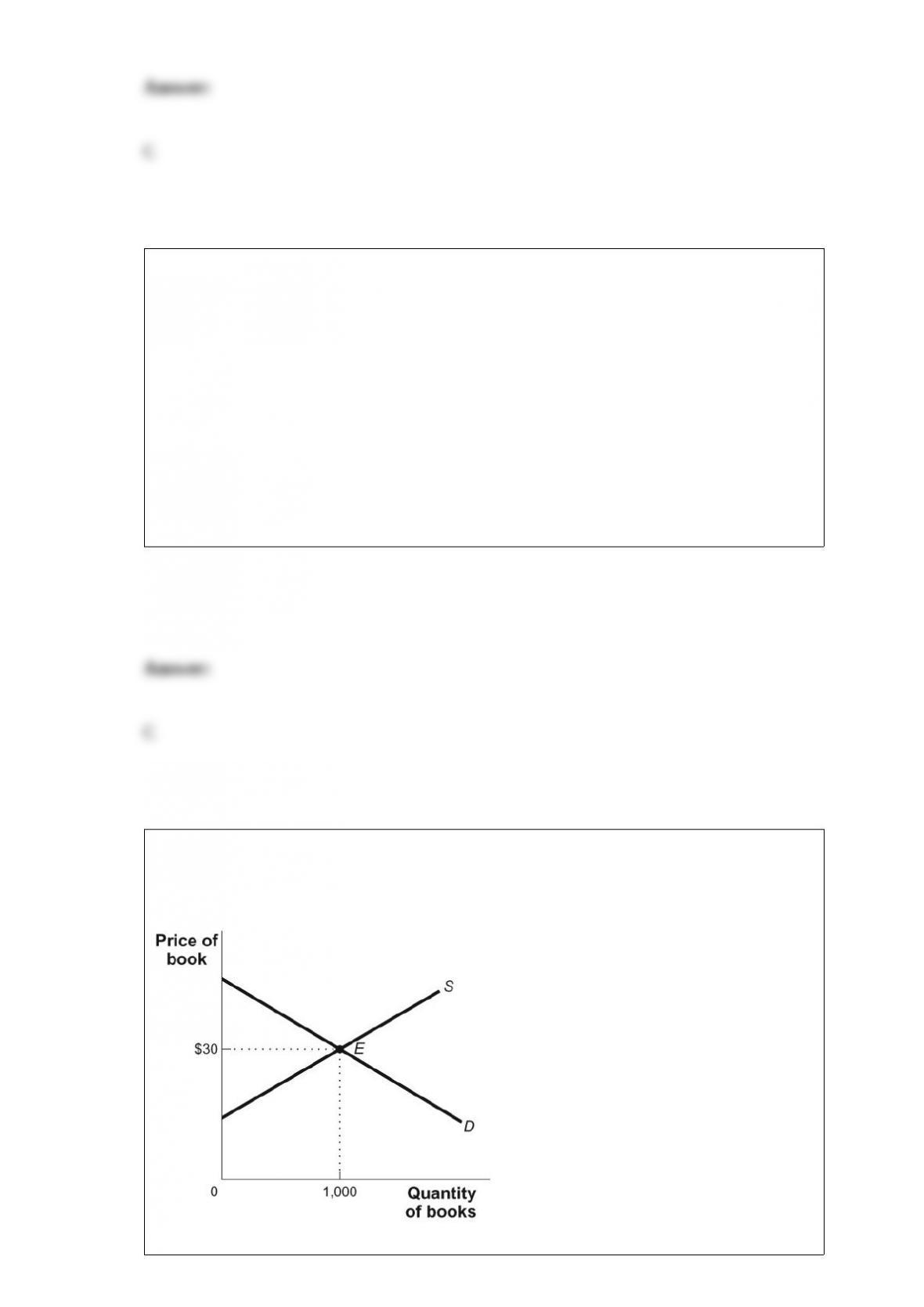

Figure: The Market for Blue Jeans

(Figure: The Market for Blue Jeans) Look at the figure The Market for Blue Jeans. The

government recently levied a $10 tax on the producers of blue jeans. What is the

deadweight loss?

A) $1,000

B) $500

C) $250

D) $1,250

(Table: Comparative Advantage I) Look at the table Comparative Advantage I. The

opportunity cost of producing 1 box of cell phones for Finland is _____ box(es) of

herring.

A) 10

B) 0.5

C) 5

D) 0.1

Scenario: Health Costs

Alan is hoping for a healthy year, meaning that he would have zero health costs. Given

his habits, there is a 40% chance that Alan will develop a health issue resulting in

$50,000 in health costs. Assume these are the only two conditions that could exist for

Alan in the coming year.

(Scenario: Health Costs) Look at the scenario Health Costs. When Alan’s probability of

developing a health problem decreases, holding everything else constant, Alan’s

expected value of health care costs:

A) increases.

B) decreases.

C) stays constant.

D) increases, decreases, or stays constant.

The amount by which an additional unit of a good or service changes a consumer’s total

satisfaction, all other things unchanged, is _____ utility.

A) marginal

B) maximum

C) average

D) required

The ratio of the percentage change in quantity demanded to the percentage change in

price is the _____ elasticity of demand.

A) price

B) quantity

C) income

D) cross-price

Two individuals make up the auto insurance market. Bonnie drives well, and the

probability of her having an accident is 10% this year. Lisa also drives carefully, and

her probability of having an accident is 5%. What is the probability that Bonnie and

Lisa will both have accidents this year?

A) 0.15%

B) 0.75%

C) 0.005%

D) 0.5%

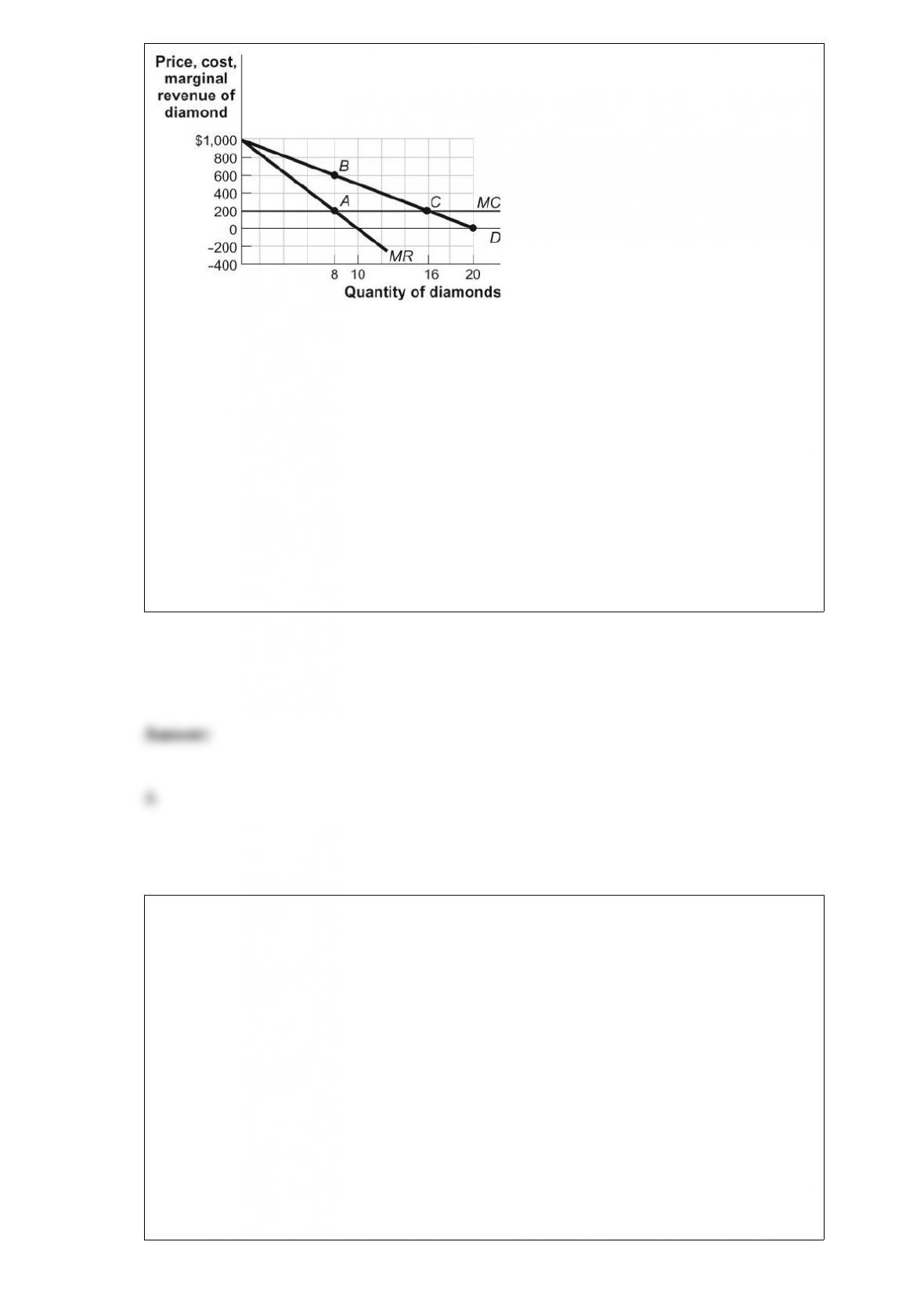

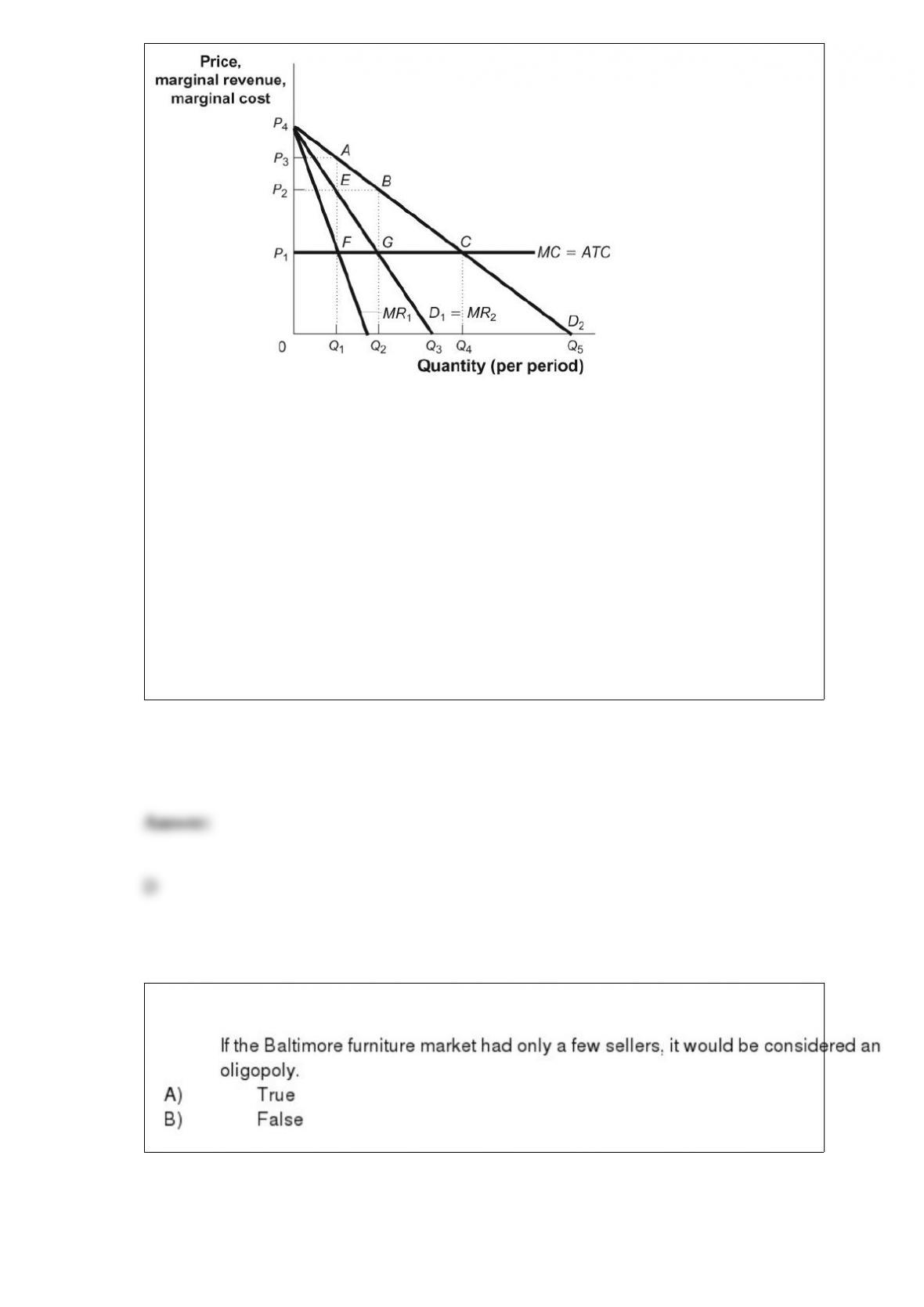

Figure: Monopoly Profits in Duopoly

(Figure: Monopoly Profits in Duopoly) The figure Monopoly Profits in Duopoly shows

how an industry consisting of two firms that face identical demand curves (D1) can

collude to increase profits. The market demand curve is D2. Which of the following

assumptions is part of the analysis illustrated by the model?

A) The two firms have identical marginal cost but different average total cost.

B) The two firms sell differentiated products.

C) The MR curve is not relevant to either firm’s choices.

D) The firms can act as a cartel and maximize their combined economic profit.

The price of popcorn is $0.50 per box and the price of peanuts is $0.25 per bag. You

have $10 to spend on both goods. The maximum number of bags of peanuts that you

can purchase is:

A) 5.

B) 10.

C) 20.

D) 40.