Which type of model has coefficients that vary with i, but are constant with t?

a.) pooled model

b.) fixed effects

c.) random effects

d.) none of these

Which of the following variables is most likely to be quantitative?

a.) gender

b.) education

c.) income

d.) employment

You have estimated a model of two variables related such that

ln(y) = 17.3 – .04 x

If x decreases by 2 units, what is the expected change in y?

a.) y decreases by .08 units.

b.) y increases by 8 percent.

c.) y increases by 4 units

d.) y decreases by 8 percent.

In which model are coefficient estimates determined by variation within individuals

rather than variation across individuals?

a.) pooled model

b.) fixed effects

c.) random effects

d.) none of these

When performing a LM test for serial correlation, how is the test statistic distributed

when the null hypothesis is true?

a.) 2

b.) tn-1

c.) F

d.) z

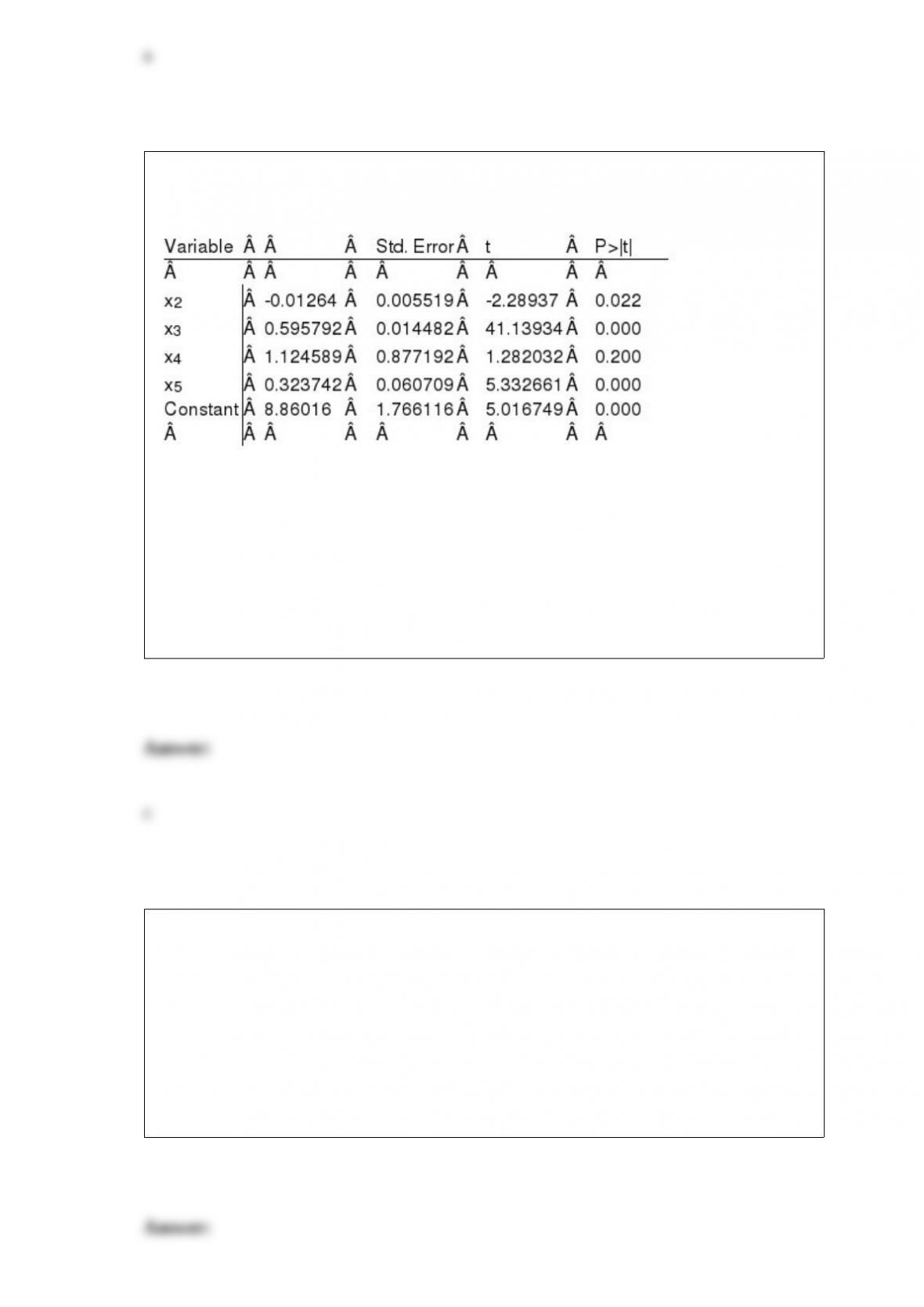

A model estimated using a dataset with 125 observations generates the following

results.

What are the endpoints for the 95% confidence interval for b3? a.)(-0.6842, 1.8758)

b.)(-1.3842, 2.5758)

c.)(.5672, 6245)

d.)(-40.5435 , 41.7251)

Impulse response funcitons can be difficult to identify as a result of

a.) interdependent dynamics and unobserved data

b.) violations of the ceteris paribus assumption

c.) unobserved data and violations of the ceteris paribus assumption

d.) interdependent dynamics and innovation

What is the primary advantage of a GARCH model rather than an ARCH model?

a.) fewer parameters to be estimated

b.) fewer assumptions required

c.) normally distributed estimators

d.) lower variance of estimates

If you model has heteroskedastic error terms, but you do not know the functional form

of the variance equation, what should be done?

a.) use White’s Robust Estimator

b.) use weighted least squares

c.) try different functional forms for the variance until the Lagrange Multiplier falls

10%

d.) add observations to the dataset and estimate again

Which model below has an autocorrelated error term?

a.) yt = f(xt, xt-1, xt-2‘¦’¦.)

b.) yt = f(yt-1, xt, xt-1, xt-2‘¦)

c.) yt = f(xt, x2

t, x3

t)

d.) yt = f(xt) + g(et-1)

When certain characteristics cause a person to choose to be in a treatment group,

selection bias can be overcome by using

a.) conditional randomization and fixed effects.

b.) difference in differences estimation.

c.) larger sample sizes.

d.) quasi-experiments.