Which of the following primarily takes futures positions that are outstanding for just

minutes?

a. Scalper

b. Local

c. Day trader

d. Position trader

e. Hedger

Answer:

A bank can establish a floor on interest rate costs by:

a. buying a call option on Eurodollar futures.

b. selling Eurodollar futures contracts.

c. selling a call option on Eurodollar futures.

d. a. and b.

e. b. and c.

Answer:

Non-interest income includes all of the following except:

a. checking account fees.

b. insufficient funds service charges.

c. trust income.

d. personnel expenses.

e. all of the above are considered non-interest income.

Answer:

In loan participations, the _____ makes the original loan and sells participations.

a. lead bank

b. interbank

c. loan production office

d. holding firm

e. originate bank

Answer:

A stripped security:

a. pays no interest.

b. has no par value.

c. is easier to value than a traditional bond.

d. should sell as a package of zero coupon bonds.

e. None of the above

Answer:

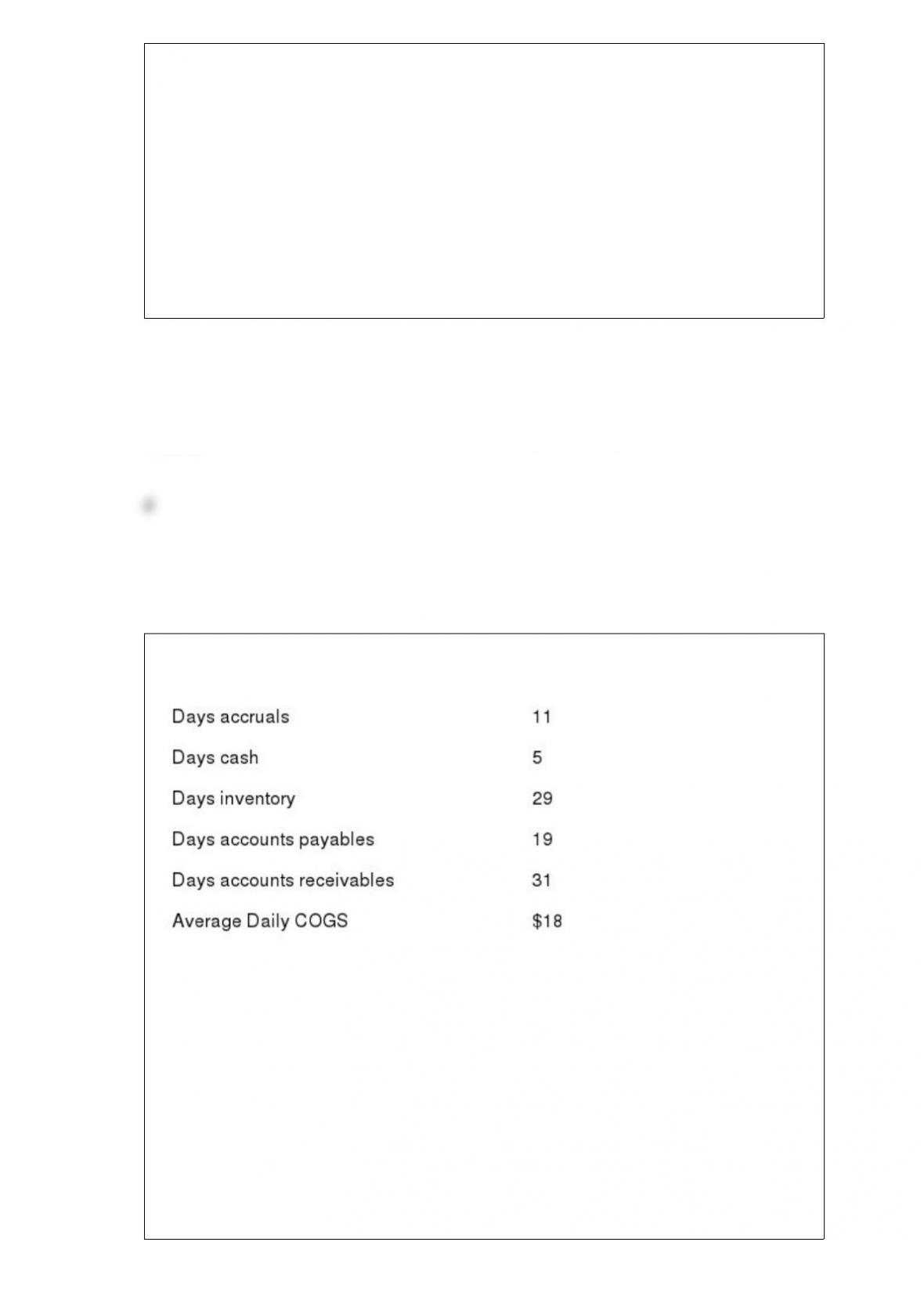

Use the following firm working capital cycle information.

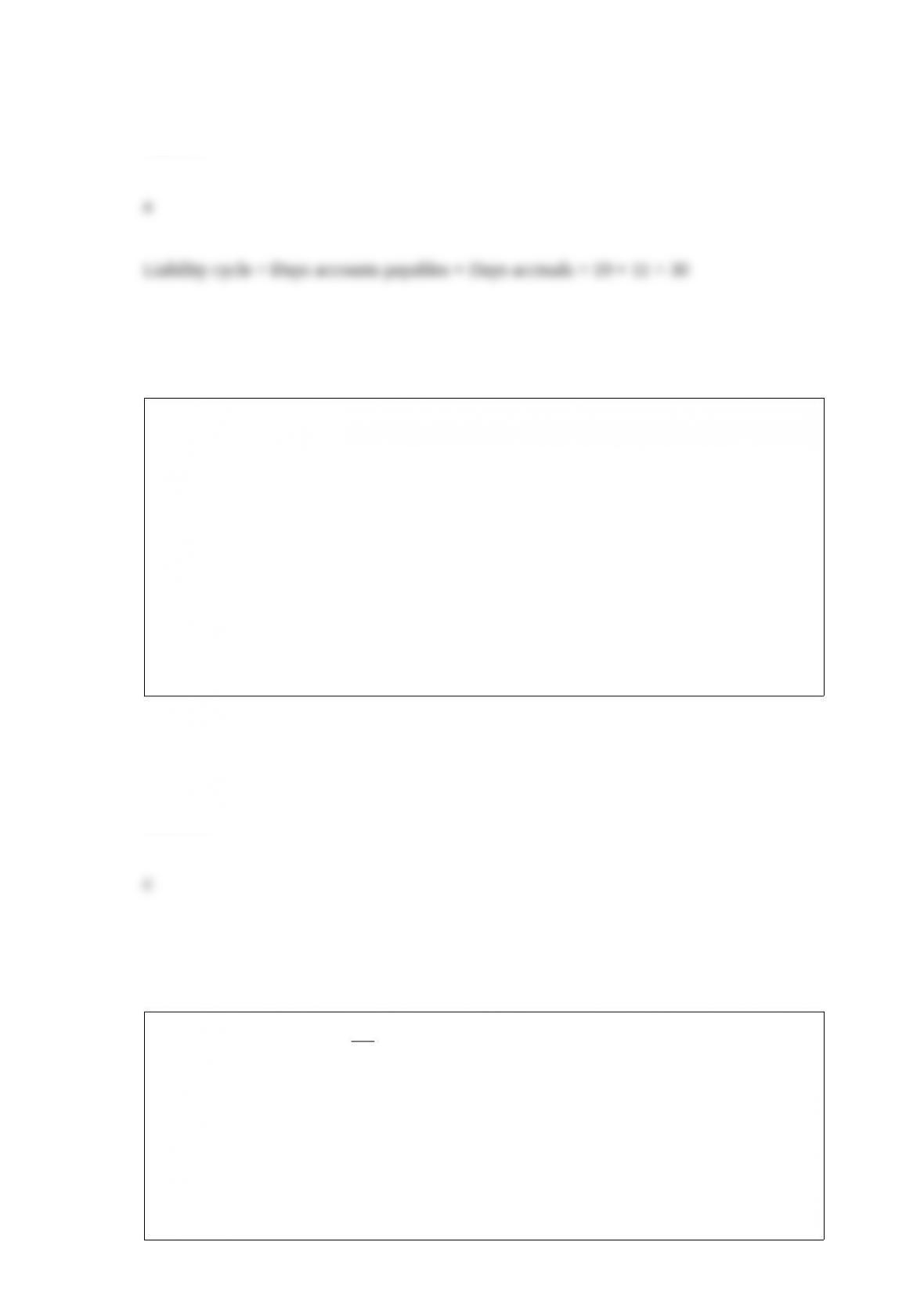

What is the firm’s liability cycle?

a. 30 days

b. 59 days

c. 65 days

d. 95 days

e. 113 days

Answer:

Controlling interest in a bank is defined as ownership or indirect control of ____ of the

voting shares in the bank.

a. 15%

b. 20%

c. 25%

d. 30%

e. 51%

Answer:

Which of the following is not a purpose of Check 21?

a. Prevent check truncation.

b. Foster innovation in the check collection system.

c. Improve overall efficiency of the payment system.

d. All of the above are purposes of Check

e. None of the above are purposes of Check 21.

Answer:

Deposits at credit unions are insured by the:

a. National Credit Union Association.

b. Federal Credit Union Administration.

c. Federal Reserve.

d. Federal Deposit Insurance Corporation.

e. Credit Union Insurance Corporation.

Answer:

A bank’s cumulative GAP:

a. is defined as the dollar amount of rate-sensitive assets divided by the dollar amount

of rate-sensitive liabilities.

b. is defined as the dollar amount of earning assets divided by the dollar amount of total

liabilities.

c. compares rate-sensitive assets with rate-sensitive liabilities across all time buckets.

d. compares rate-sensitive assets with rate-sensitive liabilities across a single time

bucket.

e. compares the dollar amount of earning assets times the average liability interest rate.

Answer:

In 2008, the U.S. Treasury financial supported financial institutions by:

a. purchasing troubled assets.

b. buying preferred stock in some financial institutions.

c. issuing guarantees on money market funds.

d. increasing the deposit insurance limit.

e. all of the above.

Answer:

Put the following steps in duration gap analysis in the proper order.

I. Estimate the economic value of assets, liabilities and equity.

II. Forecast the change in the economic value of equity for various interest rates.

III. Forecast future interest rates.

IV. Estimate the duration of assets and liabilities.

a. III, I, IV, II

b. I, II, III, IV

c. III, IV, I, II

d. IV, I, II, III

e. II, IV, I, III

Answer:

In determining reserves, the banks and the Federal Reserve currently use:

a. a leading reserve accounting system.

b. a contemporaneous reserve accounting system.

c. a lagged reserve accounting system.

d. an actual reserve accounting system.

e. a holding reserve accounting system.

Answer:

The Macaulay’s duration of a 10-year, 10% bond with a face value of $1,000 and a

market rate of 8%, compounded annually is:

a. 10 years

b. 11 years

c. 12 years

d. 13 years

e. None of the above

Answer:

Loans that finance the construction of roads and public utilities in new subdivisions are

labeled:

a. public work loans.

b. take-out loans.

c. domestic loans.

d. land development loans.

e. working capital loans.

Answer:

Which of the following is not a reason that banks hold cash assets?

a. To meet customer’s needs for currency.

b. To meet capital requirements.

c. To meet required reserves.

d. To compensate for correspondent bank services.

e. To assist in the check clearing process.

Answer:

Swap participants are subject to:

a. margin requirements.

b. fixed principal amounts.

c. exchange performance.

d. counterparty risk.

e. All of the above.

Answer:

Which of the following is not a similarity among interest rate swaps, financial futures

and FRAs.

a. Each contract allows managers to alter a bank’s interest rate risk exposure.

b. None of the contracts require much of an initial cash commitment.

c. Each contract provides for cash receipts or payments depending on how interest rates

move.

d. Parties negotiate the notional principal amounts for each contract.

e. All of the above are similarities among interest rate swaps, financial futures and

FRAs.

Answer:

The efficiency ratio measures:

a. a bank’s ability to control interest expense.

b. a bank’s ability to control non-interest expense.

c. a bank’s spread.

d. a bank’s burden.

e. a bank’s operating leverage.

Answer:

The default risk associated with loans made to borrowers outside a bank’s home country

is called:

a. foreign exchange risk.

b. sovereign risk.

c. euro risk.

d. country risk.

e. LC risk.

Answer:

Which of the following are two of the “additional Cs” of consumer credit?

a. Customer relationships and Character

b. Competition and Continuous employment

c. Continuous employment and Character

d. Customer relationships and Competition

e. Competition and Character

Answer:

There is a short-run trade-off between a bank’s liquidity and _______.

a. asset quality

b. profitability

c. discount window borrowing

d. all of the above

e. a. & b. only

Answer:

Which of the following does not have an embedded option?

a. A callable Federal Home Loan Bank bond.

b. Demand deposit accounts.

c. A home mortgage loan.

d. An auto loan.

e. All of the above have embedded options.

Answer:

Non-interest expenses includes all of the following except:

a. occupancy expenses.

b. goodwill impairment.

c. insufficient funds service charges.

d. personnel expenses.

e. all of the above are considered non-interest expense.

Answer:

The _________ created the Office of Thrift Supervision.

a. Depository Institutions Act (Garn-St. Germain)

b. Competitive Equality Banking Act

c. Financial Institutions Reform, Recovery and Enforcement Act

d. Federal Deposit Insurance Corporation Improvement Act

e. Depository Institutions Deregulation and Monetary Control Act

Answer:

Liability management decisions determines all of the following except:

a. interest expense on borrowed funds.

b. check handling costs.

c. personnel costs.

d. fee income.

e. loan rates.

Answer:

Classified loans:

a. still accrue interest.

b. have not had a principle or interest payment made in 90 days.

c. exactly offset gross charge-offs.

d. are loans in which regulators have forced management to set aside reserves.

e. all of the above

Answer:

Federal funds are:

a. secured bank loans from the discount window.

b. unsecured short-term loans that are settled in immediately available funds.

c. secured inter-bank loans of reserves.

d. secured core deposits.

e. secured overnight loans.

Answer:

Which of the following is false?

a. As interest rates rise, bond prices rise, everything else the same.

b. Given an absolute change in interest rates, the percentage increase in a bond’s price

will be greater than the percentage decrease, everything else the same.

c. Long-term bonds change proportionately more in price than short-term bonds for a

given rate change, everything else the same.

d. A bond with a lower coupon will change more in price than a bond with a higher

coupon, everything else the same.

e. A bond’s duration is a measure of its price elasticity.

Answer:

Income statement GAP considers:

a. changes in interest rates.

b. changes in the volume of rate-sensitive assets due to a change in interest rates.

c. changes in the volume of fix-rate liabilities due to a change in interest rates.

d. mortgage prepayments.

e. Income statement GAP considers all of the above.

Answer:

Savings institutions must maintain what percent of their assets in housing-related assets

to be considered a “Qualified Thrift Lender”?

a. 100%

b. 15%

c. 70%

d. 85%

e. 65%

Answer:

Effective duration:

a. estimates when embedded options will be used.

b. directly indicates how much the price of a security will change given a change in

interest rates.

c. is always greater than maturity.

d. is a weighted average of the time until cash flows are received.

e. All of the above

Answer: