Continue to suppose as in the previous question that the utility function for each of the

firm’s 5 workers is

where l is hours worked and w is the wage. Suppose now that the firm can only monitor

the total hours worked by the group and pay each worker an equal share of the wage

times the total number of hours. How many hours will each worker choose to

work?

a. 2 hours.

b. 4 hours.

c. 8 hours.

d. 10 hours.

The output effect of a change in the wage rate on a firm’s demand for labor input will be

greater

a. the larger the share of labor costs in total costs and the greater the price elasticity of

demand for output.

b. the larger the share of labor costs in total costs and the smaller the price elasticity of

demand for output.

c. the larger the share of labor costs in total costs and the higher the quantity demanded.

d. the smaller the possibilities of substituting capital for labor.

A firm’s marginal revenue is defined as

a. the ratio of total revenue to total quantity produced.

b. the additional output produced by lowering price.

c. the additional revenue received due to technical innovation.

d. the additional revenue received when selling one more unit of output.

As long as marginal cost is below average cost, average cost will be

a. falling.

b. rising.

c. constant.

d. changing in a direction that cannot be determined without more information.

The condition for optimal portfolio choice can be represented by:

a. .

b. .

c. .

d. .

Which of the following illustrates adverse selection?

a. Individuals sometimes mistakenly buy defective cameras.

b. Individuals will not search for bargains for low cost items.

c. Individuals know a lot about their family health history when they buy insurance.

d. Individuals can choose whether to drive safely or not.

A firm’s demand for labor is known as a “derived demand” because

a. the firm gains utility from hiring more labor.

b. the amount of labor hired depends upon how much output the firm can sell.

c. the wage rate paid to workers is derived from the market for labor.

d. it is derived from the demand for capital.

The rate of product transformation (RPT) measures the ability of

a. a consumer to trade one good for another while still maximizing his or her utility.

b. a firm to substitute one input for another and still maintain the same production level.

c. society to substitute the production of one good for another while still using a fixed

supply of inputs efficiently.

d. a firm to produce a final good while starting with only natural resources.

The subgame-perfect equilibrium of a two-stage game in which firms first choose

capacities and then engage in a Bertrand price setting game resembles the equilibrium

in

a. the competitive model.

b. the Cournot model.

c. the cartel model.

d. the price leadership model.

Consider a twogood production economy in which both goods are produced with fixed

proportions production functions. Then, some efficient allocations will exhibit

unemployment of some factor providing

a. the firms use the inputs in different proportions.

b. the firms exhibit diminishing returns to scale.

c. the firms exhibit increasing returns to scale.

d. production can never be efficient if there are unemployed inputs.

The marginal rate of technical substitution (RTS) of labor for capital measures

a. the amount by which capital input can be reduced while holding quantity produced

constant when one more unit of labor is used.

b. the amount by which labor input can be reduced while holding quantity produced

constant when one more unit of capital is used.

c. the ratio of total labor to total capital.

d. the ratio of total capital to total labor.

The supply curve for a monopoly is given by

a. the firm’s marginal cost curve above the average variable cost curve.

b. the one point on the demand curve that corresponds to the quantity for which price is

equal to MC.

c. the one point on the demand curve that corresponds to the quantity for which MR

equals MC.

d. the entire demand curve above the point where price is equal to average cost.

Which statement is true if the monopolist can observe the consumer’s type in the

nonlinear-pricing application?

a. The monopolist supplies the consumer with as much of the good as if it

were competitively priced.

b. The monopolist’s profit approaches the upper bound from the simple linear

pricing problem.

c. The monopolist extracts all of the surplus from the low type but not the high type.

d. The monopolist extracts all of the surplus from the high type but not the low type.

A firm’s isoquant shows

a. the amount of labor needed to produce a given level of output with capital held

constant.

b. the amount of capital needed to produce a given level of output with labor held

constant.

c. the various combinations of capital and labor that will produce a given amount of

output.

d. none of these answers is correct.

The market demand curve for any good is

a. independent of individuals’ demand curves for the good.

b. the vertical summation of individuals’ demand curves.

c. the horizontal summation of individuals’ demand curves.

d. derived from the firm’s marginal cost of production.

An efficient allocation of productive inputs requires that

a. each output has the same rate of technical substitution among inputs used.

b. each output has the same marginal rate of substitution for consumers.

c. each pair of outputs has the same rate of product transformation.

d. each individual has the same marginal rate of substitution between outputs.

If an individual’s indifference curve map does not obey the assumption of a diminishing

MRS, then

a. the individual will not maximize utility.

b. the individual will buy none of good X.

c. tangencies of indifference curves to the budget constraint may not be points of utility

maximization.

d. the budget constraint cannot be tangent to an appropriate indifference curve.

Perfectly competitive markets will tend to underallocate resources to nonexclusive

public goods because

a. these goods are produced under conditions of increasing returns to scale.

b. no single individual can appropriate the total benefits provided by the purchase of

such goods.

c. these goods are best produced under conditions of monopoly.

d. no private producer can provide the capital necessary to produce such goods.

Suppose a person’s utility of wealth is given by and his or her initial

wealth is 10,000. What is the maximum amount he or she would pay for insurance

against a 50 percent chance of losing 3,600?

a. 1,800.

b. 1,900.

c. 2,000.

d. 2,100.

An increase in the corporate profits tax will most likely lead to

a. a decrease in the rental rate of capital in the corporate sector.

b. no change in the rental rate of capital in the corporate sector.

c. no change in the rental rate of capital in the noncorporate sector.

d. an increase in the rental rate of capital in the corporate sector.

What tradeoffs are present in the moral-hazard-in-insurance problem?

a. Full insurance benefits the risk-averse customer but gives him excessive

incentives to take care to avoid harm.

b. Full insurance benefits the risk-averse customer but provides him with no

incentive to take care to avoid harm.

c.Full insurance benefits the risk-averse consumers but does not allow the

insurer to extract as much surplus from all types.

d. Full insurance is beneficial for all consumers, but if sold at an actuarially fair price

for the population will draw only the riskiest types.

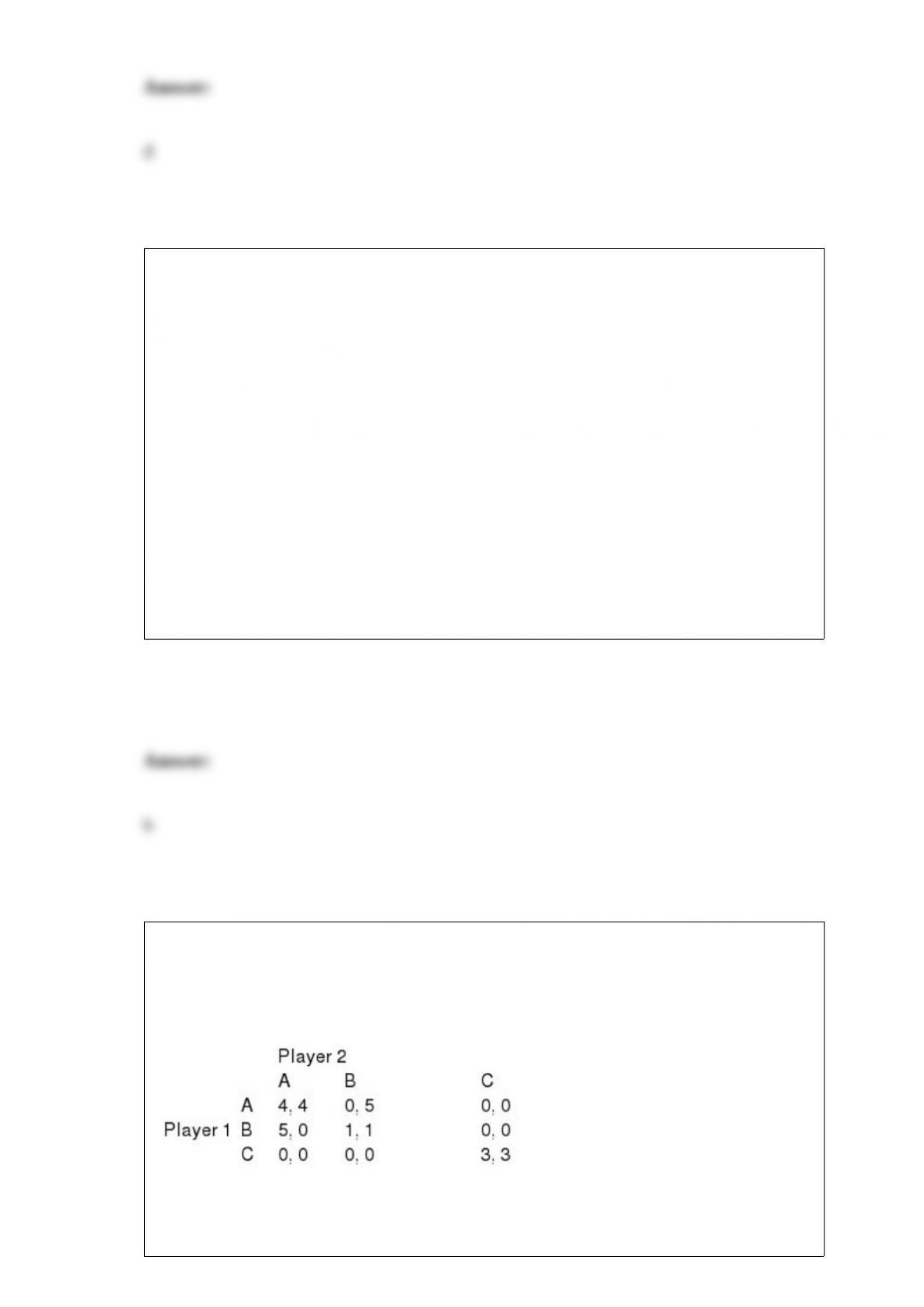

In the mixed-strategy Nash equilibrium of the following game in which players

randomize between B and C and do not play A at all, what is the probability that each

plays B?

a. 3/4.

b. 1/2.

c. 1/4.

d. 1/3.

Each of the following provides incentives to reduce a negative externality except

a. merger with affected firms.

b. subsidizing consumption of the good being produced.

c. bargaining among firms.

d. taxation of the externality.

If a firm is a price taker, its marginal revenue is

a. equal to market price.

b. less than market price.

c. greater than market price.

d. a multiple of market price that may be either greater than or less than one.

In order to maximize profits, a firm should produce at the output level for which

a. average cost is minimized.

b. marginal revenue equals marginal cost.

c. marginal cost is minimized.

d. price minus average cost is as large as possible.

Quasi-concavity of utility functions insures that with only two goods, these goods must

be

a. gross substitutes.

b. gross complements.

c. net substitutes.

d. net complements.

If the compensated and Marshallian demand curves for a good intersect, at that point

the Marshallian curve will be

a. flatter if this is a normal good.

b. steeper if this is a normal good.

c. flatter if this is an inferior good.

d. horizontal.

An individual will never buy complete insurance if

a. he or she is risk averse.

b. insurance premiums are unfair.

c. he or she is a risk taker.

d. insurance premiums are fair.

Under perfect competition, if an industry is characterized by positive economic profits

in the short run

a. firms will leave the market in the long run and the short-run supply curve will shift

outward.

b. firms will enter the market in the long run and the short-run supply curve will shift

outward.

c. firms will enter the market in the long run and the short-run supply curve will shift

inward.

d. firms will leave the market in the long run and the short-run supply curve will shift

inward.

An inner tube company which is maximizing its own profits will keep renting machines

up to the point where

a. the marginal productivity of a capital is maximized.

b. the marginal value product of machines is maximized.

c. the marginal value product of machines is equal to the market rental rate for

machines.

d. the machine’s market rental rate is minimized.

If the demand faced by a firm is elastic, selling one less unit of output will

a. increase revenue.

b. decrease revenue.

c. keep revenues constant.

d. decrease price.

Society’s demand curve for a public good

a. is given by the horizontal summation of individual demand curves.

b. is given by the vertical summation of individual demand curves.

c. cannot be derived from individual demand curves due to the nature of a public good.

d. is given by the average citizen’s individual demand curve.