What type of model provides information about sources of volatility?

a.) a VAR model

b.) an impulse response function

c.) variance decomposition

d.) an ARDL model

Unobservable variables that enter into decisions are called

a.) latent variables

b.) endogenous variables

c.) heterogeneity

d.) count data

Which test is commonly performed to check for the presence of ARCH effects?

a.) Chow test

b.) Wald test

c.) LM

d.) F-test

When should a researcher consider transforming the explanatory variable in the simple

linear regression model?

a.) to estimate a coefficient on the dependent variable that matches economic theory

b.) to allow non-constant marginal effects

c.) to reduce variance in the dependent variable

d.) to reduce (Note: the “hat” should be over the whole expression, but I

can’t accomplish that in my software right now)

If we use as an estimator of it is _______________, but it can be corrected by

_______________.

a.) biased, changing the numerator to

b.) non-linear, changing the denominator to N – 2

c.) biased, changing the denominator to N-2

d.) non-linear, taking the log of each term.

A measure of the daily change in the closing value of the DJIA is a ____________

variable and a variable indicating whether it moved up or down is a ______________

variable.

a.) continuous, discrete

b.) flow, stock

c.) random, determined

d.) discrete, continuous

The minimum number of times a series must be differenced to generate a stationary

series is the

a.) unit root

b.) order of integration

c.) trend coefficient

d.) spurious regression degree

If a structural model has M simultaneous equations, what is the necessary condition for

a unique parameter value to be consistently estimated for each variable in the equation?

a.) The number of endogenous variables excluded from the equation must be at least as

large as M-1

b.) the number of endogenous variables excluded must be at least M/2

c.) the number of exogenous variables in the equation must be greater than the number

of endogenous variables in the equation

d.) the sample size must be large enough to allow M * (M-1) degrees of freedom

If 1 is an estimator for such that E(1) = , then it must be the case that

a.) 1 is an efficient estimator

b.) 1 is an unbiased estimator

c.) 1 is a linear estimator

d.) 1 is a preferred estimator

If you have the following economic model

y = b1 + b2x – b3x2

What is dy/dx?

a.) b2

b.) b3+b2

c.) b2 ‘“ 2b3x

d.) b1 + 2b2

An ARDL model with nonstationary variables is a(n)

a.) error correction model

b.) VEC

c.) VAR

d.) variance decomposition

The OLS estimators for and are formulas derived by minimizing _____________.

a.) the sum of the error terms or residuals

b.) the sum of the squared residuals

c.) the slope of the regression line

d.) the fit of the regression line to the observed data.

You have estimated a regression model and your printout includes the following

information

xy= 3614.00

x= 12.72

y= 394.61

SST = 758912.00.

What is R2 for this regression model?

a.) .72

b.) .11

c.) .03

d.) .53

A large company is accused of gender discrimination in wages. The following model

has been estimated from the company’s human resource information ln(WAGE) = 1.439

+ .0834 EDU + .0512 EXPER + .1932 MALE Where WAGE is hourly wage, EDU is

years of education, EXPER is years of relevant experience, and MALE indicates the

employee is male. How much more do men at the firm earn, on average?

a.) $1.21 per hour more than females

b.) 19.32% more than females

c.) $19.32 per hour

d.) $19,320 more per year than females

If you perform a Hausman test on a random effects model and have a test statistic that

exceeds your critical value, which of the following is not correct?

a.) at least one of the regressors in the RE model is endogenous

b.) none of the common coefficient estimates in the RE model will be significantly

different in the FE model

c.) FE may be the preferred estimation technique

d.) this model may be better estimated using the Hausman-Taylor estimator

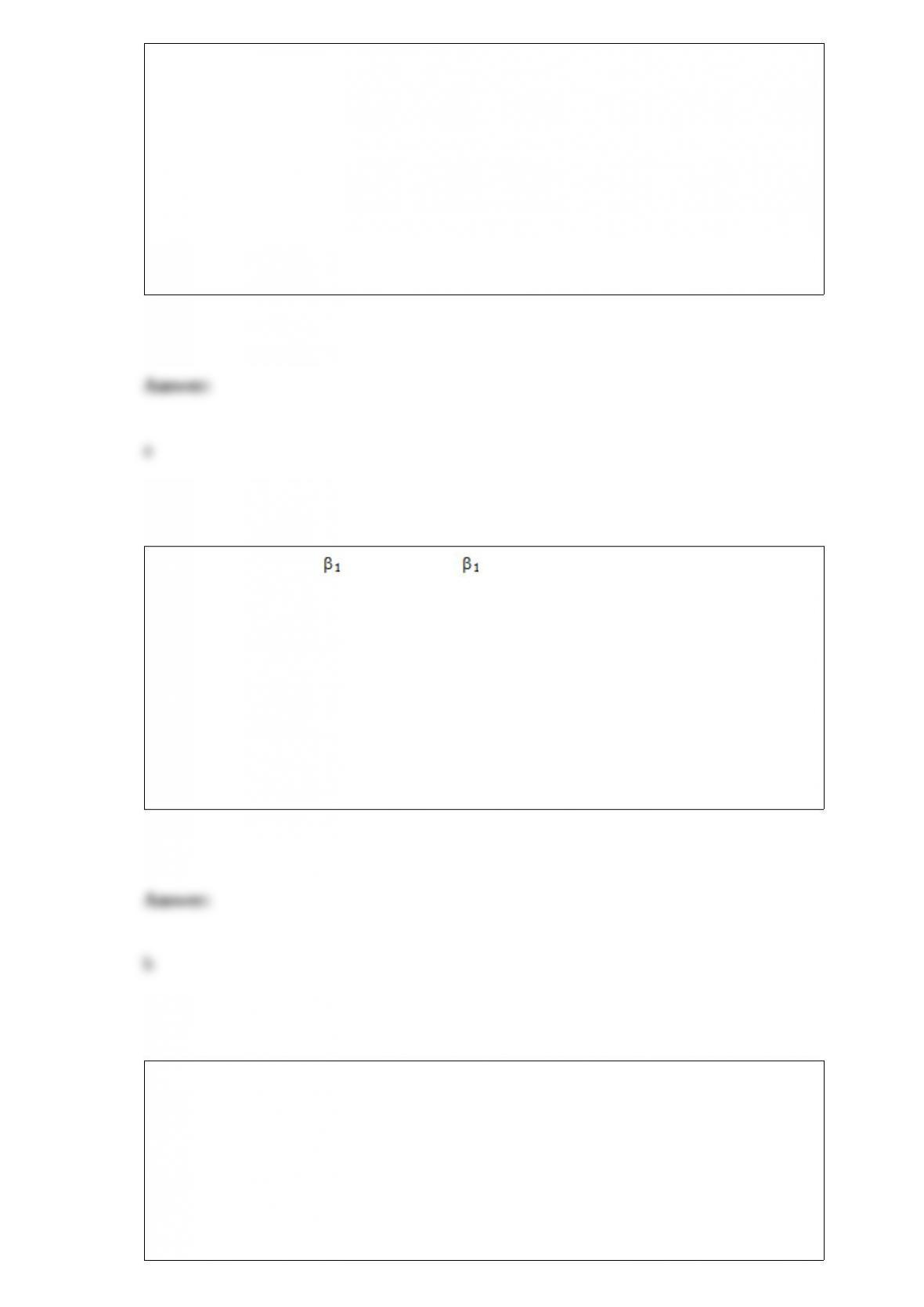

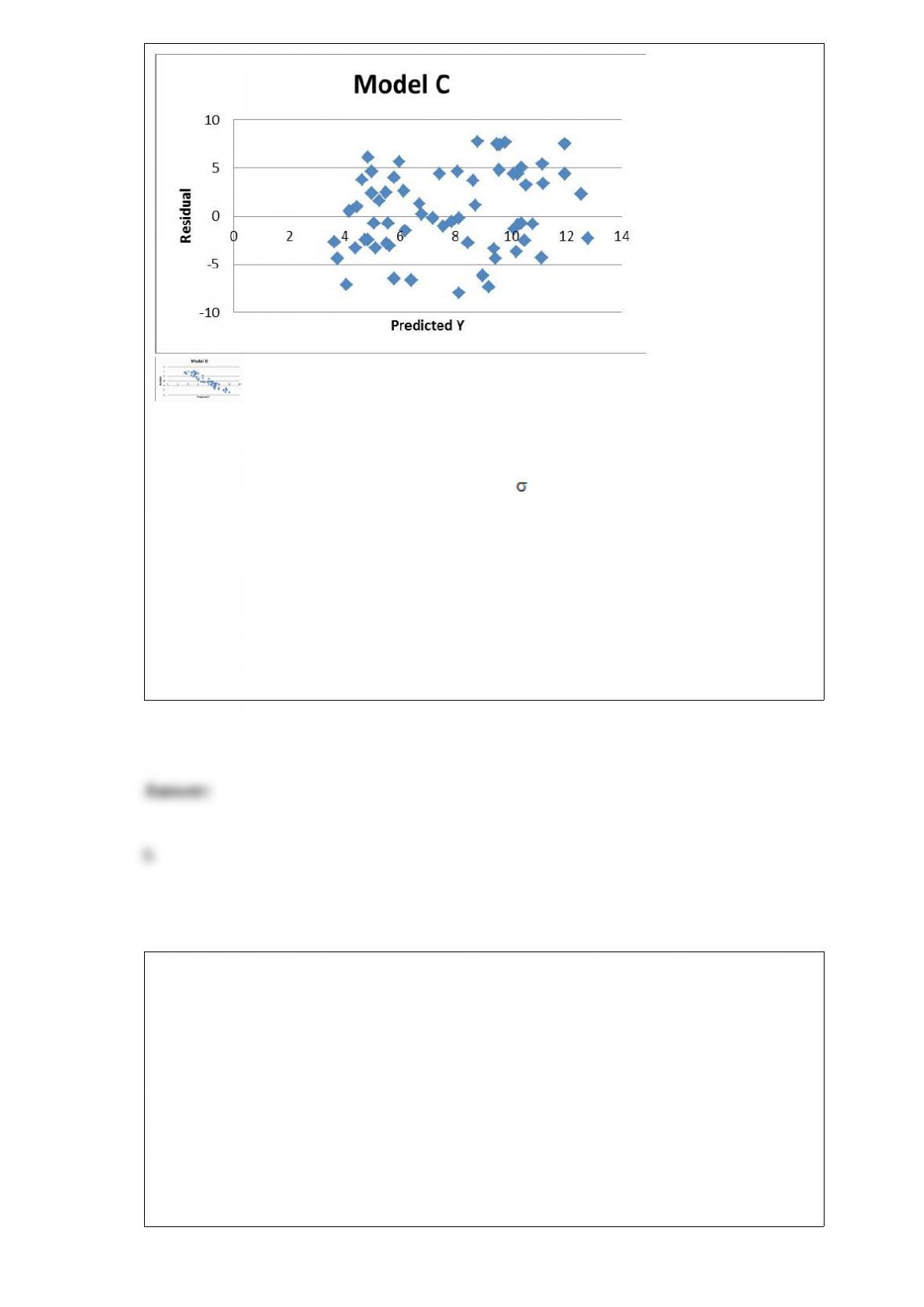

(See graphs of Model A – D) The scatterplots show the estimated residuals plotted

against predicted values of the dependent variable. Which model is MOST likely to

have violated the assumption var(yi) = var(ei) = 2?

a.) Model A

b.) Model B

c.) Model C

d.) Model D

Suppose you stand outside a store and randomly give some shoppers coupons as they

enter while other shoppers receive none. You then record how much each shopper

spends in the store. The data you collect are

a.) survey data

b.) random data

c.) experimental data

d.) selective data